Europe Power Transistor Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

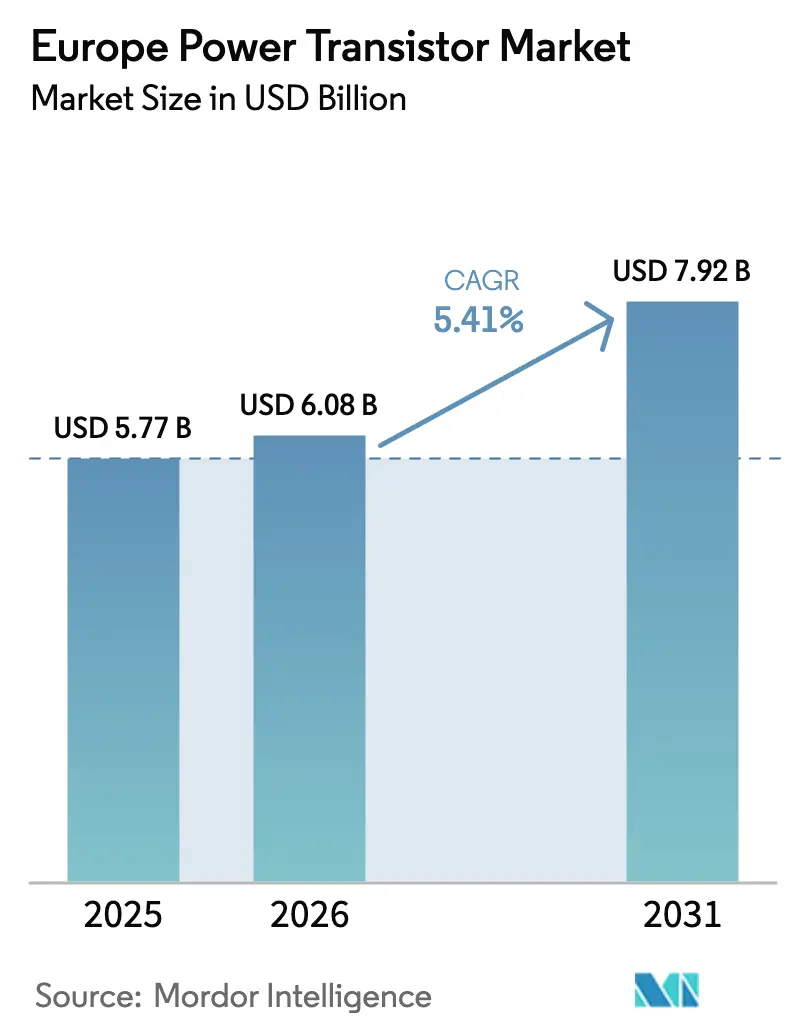

| Base Year Market Size (2025) | USD 5.77 Billion |

| Market Size (2026) | USD 6.08 Billion |

| Market Size (2031) | USD 7.92 Billion |

| Growth Rate (2026 - 2031) | 5.41% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Power Transistor Market Analysis by Mordor Intelligence

The Europe power transistor market size was valued at USD 5.77 billion in 2025 and estimated to grow from USD 6.08 billion in 2026 to reach USD 7.92 billion by 2031, at a CAGR of 5.41% during the forecast period (2026-2031). Momentum stems from accelerating electrification in mobility, renewable generation, and digital infrastructure. Automakers are shifting to silicon-carbide-based traction inverters that extend driving range and cut charging times, while utilities expand high-voltage direct-current links that demand robust high-efficiency switches. Wide-bandgap devices benefit from the European Union’s Green Taxonomy, which funnels low-cost capital to projects with verifiable efficiency gains. Meanwhile, data-center operators face strict power-usage-effectiveness rules that favor gallium-nitride converters delivering 98% efficiencies. Finally, the continent’s push for semiconductor sovereignty is spurring local production of SiC substrates and GaN epitaxy, tempering supply-chain risk and supporting long-term growth.

Key Report Takeaways

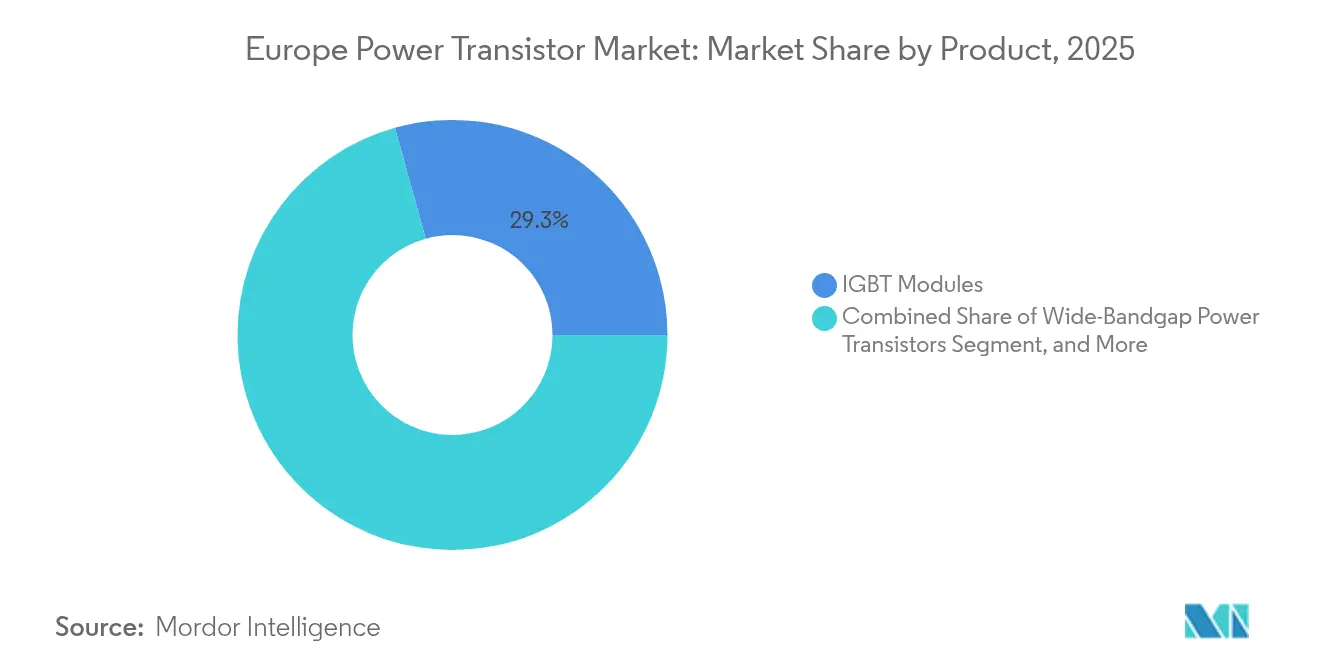

- By product, IGBT modules led with 29.31% revenue share in 2025; wide-bandgap transistors are projected to expand at a 7.38% CAGR to 2031.

- By material, silicon accounted for 56.78% of the Europe power transistor market share in 2025, while gallium nitride is set to grow at 6.26% CAGR through 2031.

- By type, MOSFETs captured 49.35% share of the Europe power transistor market size in 2025 and heterojunction bipolar transistors are advancing at a 5.75% CAGR through 2031.

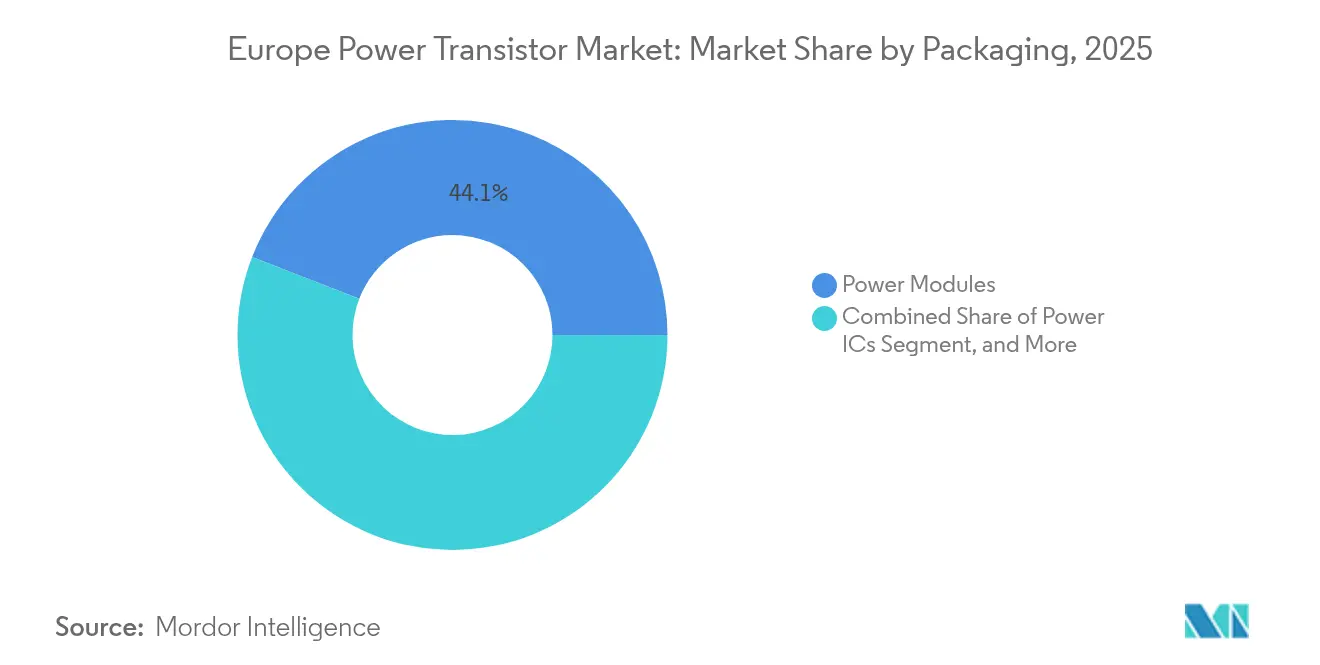

- By packaging, power modules held 44.10% share in 2025; power ICs register the fastest-growth outlook at 6.03% CAGR through 2031.

- By power rating, medium-power devices commanded 45.32% share in 2025, whereas high-power devices above 600 V post a 5.31% CAGR through 2031.

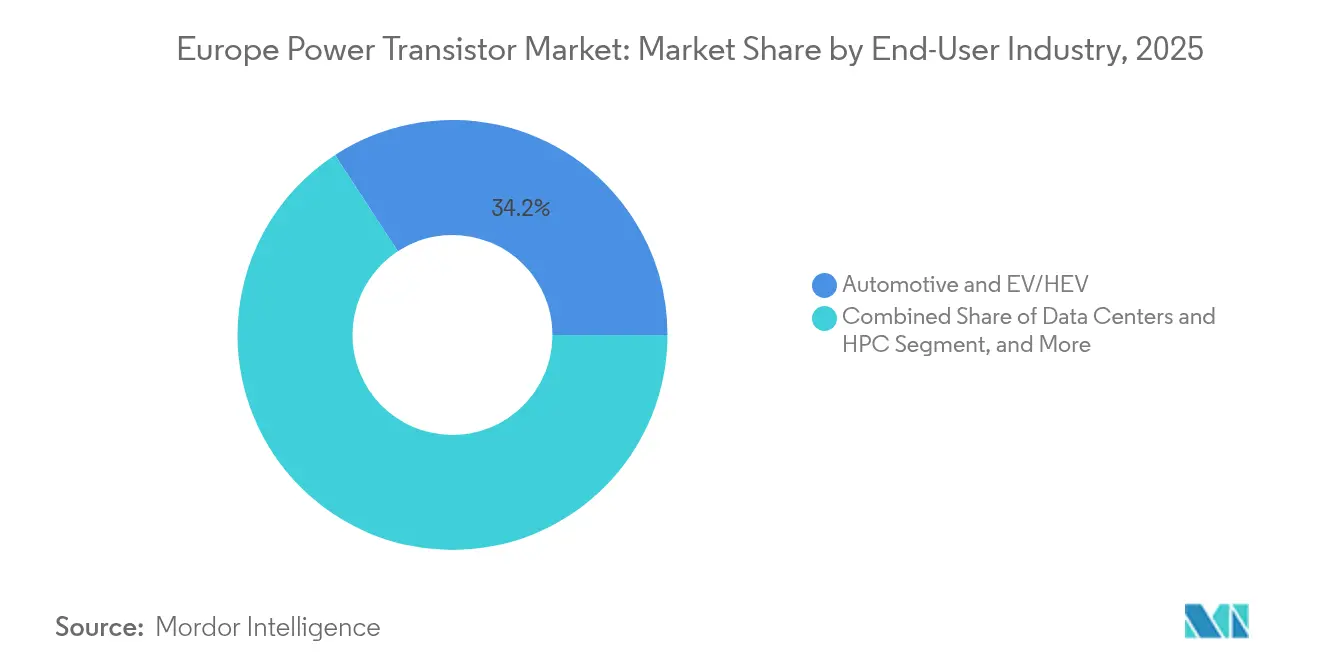

- By end-user, automotive and EV/HEV applications led with 34.20% share in 2025; data centers and HPC are rising at a 6.43% CAGR through 2031.

- By application, inverters and converters took 30.74% of the Europe power transistor market size in 2025, while RF power amplifiers chart a 5.92% CAGR through 2031.

- By country, Germany contributed 34.05% of 2025 revenue and Spain exhibits the fastest 7.64% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Worldwide, activity is shaped by contributions from multiple regions, with Europe representing one of the more structurally developed among them. The global report on power transistor market by Mordor Intelligence reflects how these regional layers combine into a single system.

Market Trends and Insights

Drivers Impact Analysis of Europe Power Transistor Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EV-related demand surge for SiC MOSFETs | +1.2% | Germany, France, Nordic nations | Medium term (2-4 years) |

| Renewable energy and smart-grid build-out | +1.0% | Pan-European, led by Germany and Spain | Long term (≥4 years) |

| 5G infrastructure roll-outs across Europe | +0.8% | United Kingdom, Germany, France, Italy | Short term (≤2 years) |

| EU Green-Taxonomy financing levers WBG uptake | +0.7% | EU-27, notably Germany and Netherlands | Medium term (2-4 years) |

| ISO 26262 functional-safety push to higher-voltage designs | +0.5% | Germany, France, Italy | Medium term (2-4 years) |

| Data-center PUE mandates favor high-efficiency transistors | +0.6% | Ireland, Netherlands, Germany, France | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

EV-Related Demand Surge for SiC MOSFETs

European automakers increasingly specify silicon-carbide MOSFET traction inverters because these devices raise drivetrain efficiency and add 5-8% driving range compared with silicon IGBTs.[1]STMicroelectronics, “STMicroelectronics Reports 2024 Third Quarter Financial Results,” St.com Euro 7 emissions rules accelerate the switch as manufacturers pursue every kilowatt-hour saved. Infineon has expanded SiC capacity in Austria and Italy, signaling clear confidence that the Europe power transistor market will keep absorbing higher volumes through 2030. As charging infrastructure migrates toward 800 V architectures, demand for 1 200 V SiC devices should intensify, locking in medium-term growth.

Renewable Energy and Smart-Grid Build-Out

The REPowerEU plan targets 1,236 GW of renewables by 2030, requiring roughly EUR 300 billion (USD 330 billion) in grid upgrades that rely on efficient high-voltage switching.[2]European Commission, “REPowerEU: Affordable, Secure and Sustainable Energy for Europe,” Europa.eu High-power IGBT and SiC modules enable multi-gigawatt HVDC links such as Statnett’s interconnectors, which reinforce cross-border power flow and stabilize variable generation. Grid codes rewarding lower switching losses push utilities toward wide-bandgap devices, cementing long-term demand in the European power transistor market.

5G Infrastructure Roll-Outs Across Europe

Telecom operators invested USD 60.97 billion in 2024 to deploy 5G, with power electronics accounting for about 15% of radio hardware cost. Gallium-nitride transistors deliver superior power density at C-band, enabling smaller base-stations that meet energy-efficiency mandates. Ericsson’s supply agreements with European GaN foundries illustrate the synergy between regional chip production goals and telecom modernization, generating near-term lift for the Europe power transistor market.

Data-Center PUE Mandates Favor High-Efficiency Transistors

The Energy Efficiency Directive requires European data centers to hit PUE below 1.4 by 2030, prompting hyperscalers to overhaul power supplies with GaN or SiC devices that reach 98% efficiency. CSA Catapult estimates compound semiconductors could slash facility energy use by 20%, amplifying procurement of high-efficiency switche.

Restraints Impact Analysis of Europe Power Transistor Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| SiC substrate supply bottlenecks | -0.9% | Europe-wide | Medium term (2-4 years) |

| Premium pricing of wide-band-gap devices | -0.7% | Southern and Eastern Europe | Short term (≤2 years) |

| EU eco-design labels elongate replacement cycles | -0.4% | EU-27 consumer markets | Long term (≥4 years) |

| Gallium export-control volatility in EU-China trade | -0.5% | Germany, France, Italy | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

SiC Substrate Supply Bottlenecks

Lead times for 150 mm SiC wafers stretch to 52 weeks, constraining device output and dampening near-term revenue. Chinese vendors control 35% of global substrate capacity, leaving European fabs exposed to trade policy shocks. Infineon and STMicroelectronics signed multi-year take-or-pay deals and are co-investing in local boule growth, yet meaningful volumes will not arrive before 2027, keeping a lid on the Europe power transistor market’s upside.

Premium Pricing of Wide-Band-Gap Devices

SiC MOSFETs cost roughly three to five times more than silicon counterparts, while GaN devices price at two to three times, limiting penetration in cost-sensitive appliances and entry-level EVs. Although total-cost-of-ownership models favor wide-bandgap technology through smaller magnetics and cooling, upfront sticker shock slows adoption in Southern and Eastern Europe where purchasing power is lower. EIB financing schemes aim to bridge that gap, but price erosion remains pivotal to broadening the Europe power transistor market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Europe Power Transistor Market Segment Analysis

By Product:

IGBT Modules Lead Industrial TransitionIGBT modules generated the largest slice of the Europe power transistor market size with 29.31% revenue in 2025. Their dominance stems from entrenched use in variable-speed drives, solar inverters, and rail traction systems that value rugged high-voltage performance. The modules pair multiple dies with optimised thermal paths, squeezing more power per cubic centimeter and fulfilling EU energy-efficiency rules. Discrete IGBTs still sell into retrofit drives, but OEMs increasingly migrate toward integrated modules that simplify assembly and improve reliability.

Wide-bandgap transistors record the quickest 7.38% CAGR and will chip away at incumbent modules, especially where every percentage-point loss impacts system economics, such as EV fast chargers. The hybrid landscape encourages vendors to co-package SiC MOSFETs with driver ICs, pushing integration advantages further. As module makers adopt direct-bonded-copper substrates and sintered silver die-attach, thermal cycles improve, extending lifetime metrics demanded by automotive traction warranties.

By Material:

Silicon Dominance Challenged by Wide-Bandgap InnovationSilicon retained 56.78% of 2025 revenue owing to its mature 200 mm fabs and cost leadership, but its share will steadily erode as designers chase higher temperature and frequency operation. Gallium nitride, growing at 6.26% CAGR, is the preferred choice for high-frequency power supplies and 5G radios where its 600 V devices outperform silicon super-junction MOSFETs. The Europe power transistor market share of SiC is also advancing as 1 200 V MOSFETs unlock EV platforms targeting 800 V battery stacks.

Strategic-autonomy policy has funneled PERTE Chip funds into Spanish and French pilot lines for GaN epitaxy, while Germany backs SiC boule growth to ease import reliance. These programs aim to shorten learning curves, drive wafer-cost parity with silicon, and reinforce local supply. Gallium arsenide and emerging oxides will remain niche, serving defense phased-array and niche scientific instrumentation.

By Type:

MOSFETs Capitalize on Switching Efficiency DemandsMOSFETs commanded 49.35% revenue in 2025. Their gate-charge efficiency and linear voltage scaling suit everything from smartphone PMICs to 350 kW traction inverters, safeguarding a broad install base. The Europe power transistor market continues to lean on MOSFET innovation, notably trench structures that cut RDS(on) below 3 mΩ.

Heterojunction bipolar transistors, advancing at 5.75% CAGR, ride the 5G tailwind where GaN HBTs deliver high gain at C-band. Bipolar junction transistors retain footholds in harsh linear regulators and welding inverters. As ISO 26262 tightens diagnostic demands, FET architectures with predictable failure modes, like normally-off SiC JFETs, pique automotive interest.

By Packaging:

Power Modules Enable System IntegrationPower modules owned 44.10% of 2025 sales, mirroring the European shift to compact drivetrain inverters and grid-scale string inverters. Integration slashes loop inductance, boosting switching speed and cutting electromagnetic interference crucial for EV traction. The Europe power transistor market sees module vendors adding embedded current sensing to support functional safety.

Power ICs are set for a brisk 6.03% CAGR as data-center PSUs consolidate control and power stages into multi-chip modules. GaN devices favor chip-scale packaging with bottom-side cooling, while SiC half-bridge modules increasingly use silver sinter to hit 200 °C junction ratings. Discrete TO-247 devices persist in retrofit industrial drives where design flexibility and price rank higher than volumetric power density.

By Power Rating:

Medium Power Dominates Industrial ApplicationsDevices rated 40-600 V captured 45.32% of the Europe power transistor market size in 2025. This bracket aligns with 400 V AC mains, industrial DC buses, and 48 V mild-hybrid architectures, blending manageable conduction losses with affordable package options. Vendors ship super-junction MOSFETs and GaN e-mode FETs into server power supplies, slicing switching loss at hundreds of kilohertz.

High-power devices above 600 V show the fastest 5.31% CAGR. Grid operators specify 3.3-kV SiC MOSFETs for solid-state transformers that handle multi-megawatt loads without oil cooling, while 1.7-kV IGBTs dominate wind turbine converters. Low-voltage parts below 40 V stay relevant in wearables and USB-PD chargers, but volume growth hinges on handset design cycles set mostly outside Europe.

By End-User Industry:

Automotive Electrification Drives GrowthAutomotive and EV/HEV captured 34.20% of the Europe power transistor market share in 2025. Volkswagen’s USD 208.97 billion electrification roadmap secures long-term pull for 750 V SiC power modules. Tier-one suppliers bundle traction inverters, DC-DC converters, and on-board chargers, inflating per-vehicle semiconductor billings.

Data centers and HPC top growth tables at 6.43% CAGR. Hyperscalers in Ireland and the Netherlands integrate GaN FET multiphase VRMs that meet stringent PUE targets. Industrial automation holds steady as plant retrofits introduce variable-speed drives. Aerospace and defense remain niche but strategic, emphasizing radiation-hard devices and sovereign sourcing.

By Application:

Inverters and Converters Lead Power ConversionInverters and converters represented 30.74% of 2025 revenue and remain the backbone of the Europe power transistor market. Solar farms, motor drives, and EV powertrains all depend on bidirectional, high-efficiency conversion. Multi-level topologies employing fast SiC switches unlock 99% efficiency in 1 MW string inverters, cutting LCOE for renewables.

RF power amplifiers, at 5.92% CAGR, rise on massive-MIMO roll-outs. GaN HEMTs push 65% drain efficiency at 3.5 GHz, slashing base-station electricity bills. Motor control continues steady expansion as EU Eco-design rules make variable-speed drives mandatory for pumps and HVAC. Battery charging tallies growth via public 350 kW stations across Trans-European Transport corridors.

Geography Analysis

Germany Power Transistor Market

Germany dominated the Europe power transistor market with 34.05% revenue in 2025. Its Energiewende-driven renewable build-out and automotive power-train shift underpin high local demand. Berlin earmarked USD 3.48 billion for semiconductor R&D through 2027, ensuring ongoing fab modernization.

Broader European Markets

France leverages STMicroelectronics’ cluster in Grenoble and Tours and dedicates USD 6.97 billion under France 2030 to power devices, elevating domestic output. The United Kingdom pursues resilience via its USD 19.28 million power-electronics grant scheme, emphasizing automotive SiC substrate onshoring. Italy benefits from Catania’s 200 mm SiC line while championing renewable installations to decarbonize heavy industry. Spain posts the swiftest 7.64% CAGR, buoyed by the USD 14.23 billion PERTE Chip program that lures IMEC’s first non-Belgian site to Málaga. The Nordic region’s hydropower surplus translates into aggressive HVDC projects that consume high-voltage modules. Eastern European states modernize grids and attract automotive tier-ones, yet weaker purchasing power tempers short-term volume.

Mordor Intelligence provides coverage of the power transistor market across other key regional markets, including Asia, each with their regulatory frameworks and demand patterns. Detailed country-level analysis extends to China and Japan incorporating local coverage and market participation, as required.

Competitive Landscape

The Europe power transistor market shows moderate concentration. Infineon, STMicroelectronics, and Nexperia anchor integrated device manufacturing, collectively supplying over half the continent’s Si and SiC output. U.S. multinationals Texas Instruments and onsemi maintain European design centers, expanding wide-bandgap portfolios through acquisitions such as onsemi’s purchase of Qorvo’s SiC JFET assets in 2024.[4]onsemi, “onsemi to Acquire Silicon Carbide JFET Technology,” Onsemi.com

Strategic thrusts revolve around vertical integration of substrates and advanced packaging. Wolfspeed’s planned Saarland SiC fab and Infineon’s Villach expansion signal race-to-capacity. Module suppliers differentiate via embedded digital current sensors and prognostic health monitoring aligned with ISO 26262. Start-ups focus on GaN-on-Si e-mode FETs and integrated gate drivers that shave PCB area for notebook chargers. Supply-chain risk triggers cooperative EU-funded pilot lines, nudging the market toward regional self-sufficiency.

Europe Power Transistor Industry Leaders

Infineon Technologies AG

Renesas Electronics Corporation

Texas Instruments Incorporated

ON Semiconductor Corporation

Mitsubishi Electric Corporation

- *Disclaimer: Major Players sorted in no particular order

Europe Power Transistor Market Companies Covered in this Report

- Infineon Technologies AG

- STMicroelectronics N.V.

- ON Semiconductor Corporation

- Nexperia B.V.

- ROHM Co., Ltd.

- Toshiba Electronic Devices and Storage Corporation

- Mitsubishi Electric Corporation

- Vishay Intertechnology, Inc.

- Renesas Electronics Corporation

- Texas Instruments Incorporated

- Analog Devices, Inc.

- IXYS LLC

- Littelfuse, Inc.

- Microchip Technology Inc.

- Wolfspeed, Inc.

- GeneSiC Semiconductor LLC

- UnitedSiC LLC

- Semikron Danfoss GmbH and Co. KG

- Dialog Semiconductor Limited

- Alpha and Omega Semiconductor Limited

Recent Industry Developments in Europe Power Transistor Market

- March 2025: CSA Catapult study projected compound semiconductors could cut European data-center energy use by 20%.

- January 2025: European Commission formally launched Spain’s PERTE Chip initiative to scale microelectronics R&D and manufacturing.

- December 2024: onsemi agreed to acquire Qorvo’s SiC JFET business for USD 115 million, broadening high-voltage portfolio for AI servers.

- October 2024: QPT Ltd won UK Advanced Propulsion Centre grant to build a 400 V/60 kW GaN inverter demonstrator switching at 1 MHz.

Europe Power Transistor Market Report Scope

The power transistors are used to amplify and regulate signals. They are made from high-performance semiconductor materials like germanium and silicon. These transistors can amplify and regulate a certain voltage level and handle specific ranges of high-level and low-level voltage ratings.

The Europe power transistor market is segmented by product (low-voltage FETs, IGBT modules, RF and microwave transistors, high voltage FETs, and IGBT transistors), by type (bipolar junction transistor, field effect transistor, heterojunction bipolar transistor, and other types), by end-user (consumer electronics, communication and technology, automotive, manufacturing, energy and power, and other end-users), and by geography (United Kingdom, Germany, France, Italy, Rest of Europe). The report offers market forecasts and size in value (USD) for all the above segments.

Segmentation Overview

| Low-Voltage FETs |

| High-Voltage FETs |

| Discrete IGBT |

| IGBT Modules |

| Super-Junction MOSFETs |

| RF and Microwave Transistors |

| Wide-Bandgap Power Transistors (SiC, GaN) |

| Silicon |

| Silicon Carbide (SiC) |

| Gallium Nitride (GaN) |

| Gallium Arsenide (GaAs) |

| Other Materials |

| Bipolar Junction Transistor (BJT) |

| Field-Effect Transistor (MOSFET, JFET) |

| Heterojunction Bipolar Transistor (HBT) |

| Discrete Devices |

| Power Modules |

| Power ICs / Integrated Power Stages |

| Low Power (< 40 V) |

| Medium Power (40–600 V) |

| High Power (> 600 V) |

| Automotive and EV/HEV |

| Consumer Electronics and Mobile |

| Industrial Automation and Motor Drives |

| Energy and Power (Renewables, Smart Grid) |

| Data Centers and HPC |

| Telecom and 5G Infrastructure |

| Aerospace and Defense |

| Inverters and Converters |

| Motor Control and Drives |

| Power Supplies and Adapters |

| Battery Charging and BMS |

| RF Power Amplifiers |

| Lighting and Display Drivers |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Nordics (Denmark, Sweden, Norway, Finland) |

| Rest of Europe |

| By Product | Low-Voltage FETs |

| High-Voltage FETs | |

| Discrete IGBT | |

| IGBT Modules | |

| Super-Junction MOSFETs | |

| RF and Microwave Transistors | |

| Wide-Bandgap Power Transistors (SiC, GaN) | |

| By Material | Silicon |

| Silicon Carbide (SiC) | |

| Gallium Nitride (GaN) | |

| Gallium Arsenide (GaAs) | |

| Other Materials | |

| By Type | Bipolar Junction Transistor (BJT) |

| Field-Effect Transistor (MOSFET, JFET) | |

| Heterojunction Bipolar Transistor (HBT) | |

| By Packaging | Discrete Devices |

| Power Modules | |

| Power ICs / Integrated Power Stages | |

| By Power Rating | Low Power (< 40 V) |

| Medium Power (40–600 V) | |

| High Power (> 600 V) | |

| By End-User Industry | Automotive and EV/HEV |

| Consumer Electronics and Mobile | |

| Industrial Automation and Motor Drives | |

| Energy and Power (Renewables, Smart Grid) | |

| Data Centers and HPC | |

| Telecom and 5G Infrastructure | |

| Aerospace and Defense | |

| By Application | Inverters and Converters |

| Motor Control and Drives | |

| Power Supplies and Adapters | |

| Battery Charging and BMS | |

| RF Power Amplifiers | |

| Lighting and Display Drivers | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Nordics (Denmark, Sweden, Norway, Finland) | |

| Rest of Europe |

Key Questions Answered in the Report

What is the projected revenue for Europe’s power transistor space by 2031?

The Europe power transistor market size is forecast to reach USD 7.92 billion by 2031.

Which device category currently dominates shipments in Europe?

IGBT modules hold the largest share at 29.31% thanks to widespread use in industrial drives and renewable inverters.

How fast are gallium-nitride devices growing across the region?

GaN transistors are projected to rise at a 6.26% CAGR between 2026 and 2031 as data-center and 5G applications scale.

Why is Spain considered a key growth hotspot?

Spain’s PERTE Chip program funnels USD 14.23 billion into domestic semiconductor capacity, pushing a 7.64% CAGR through 2031.

What supply risks could moderate market expansion?

Limited SiC substrate availability and possible gallium export controls remain the most significant headwinds for European producers.

Page last updated on: