Europe Out Of Home (OOH) Delivery Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

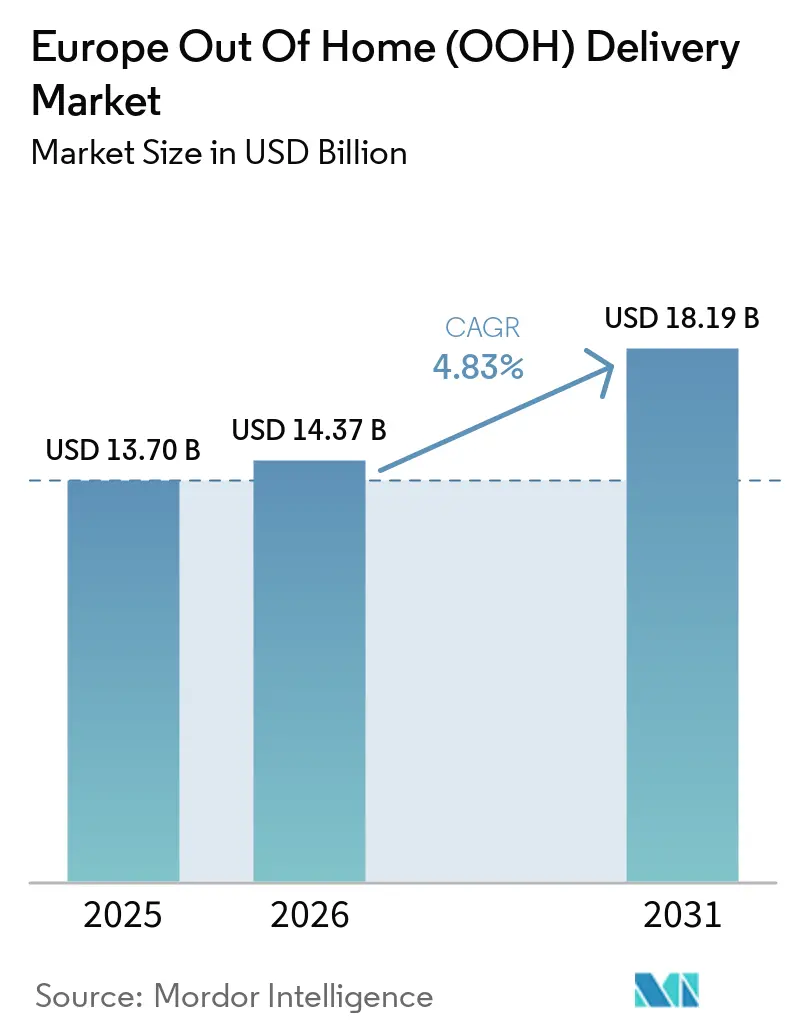

| Base Year Market Size (2025) | USD 13.70 Billion |

| Market Size (2026) | USD 14.37 Billion |

| Market Size (2031) | USD 18.19 Billion |

| Growth Rate (2026 - 2031) | 4.83% CAGR |

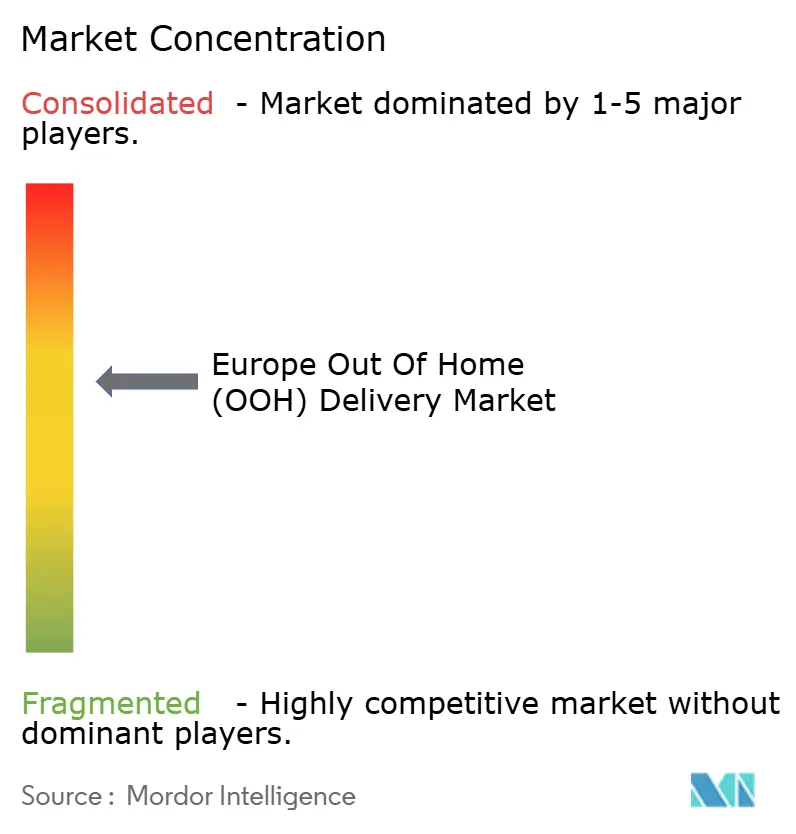

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Out Of Home (OOH) Delivery Market Analysis by Mordor Intelligence

The Europe out-of-home (OOH) delivery market size was valued at USD 13.7 billion in 2025 and is estimated to grow from USD 14.37 billion in 2026 to reach USD 18.19 billion by 2031, growing at a CAGR of 4.83% from 2026 to 2031.

The expansion reflects a clear shift in last-mile design, because automated parcel machines are scaling faster than traditional pick-up and drop-off points and are narrowing the infrastructure gap across Western, Southern, and Central Europe. Consumer use has also moved beyond occasional convenience: 35% of Europeans already direct deliveries to an out-of-home location, and 79% use a parcel locker or parcel shop for returns, indicating that the network now supports both delivery and reverse logistics within the same shopping journey[1]DHL eCommerce, “2025 Out-of-Home Delivery & Returns Trends,” DHL eCommerce Global Insights, dhl.com. That pattern gives retailers and carriers a stronger reason to treat access-point coverage as a service requirement rather than a premium add-on, especially as checkout choice increasingly influences conversion and retention. The Europe out-of-home (OOH) delivery market is also becoming more commercially disciplined, with operators favoring open-access formats, retail-linked installations, and shared locker models that raise utilization and defend returns volume. This leaves the strongest opportunities in dense commuter corridors, cross-border parcel flows, and reverse logistics programs that depend on predictable, always-available collection and drop-off points.

Key Report Takeaways

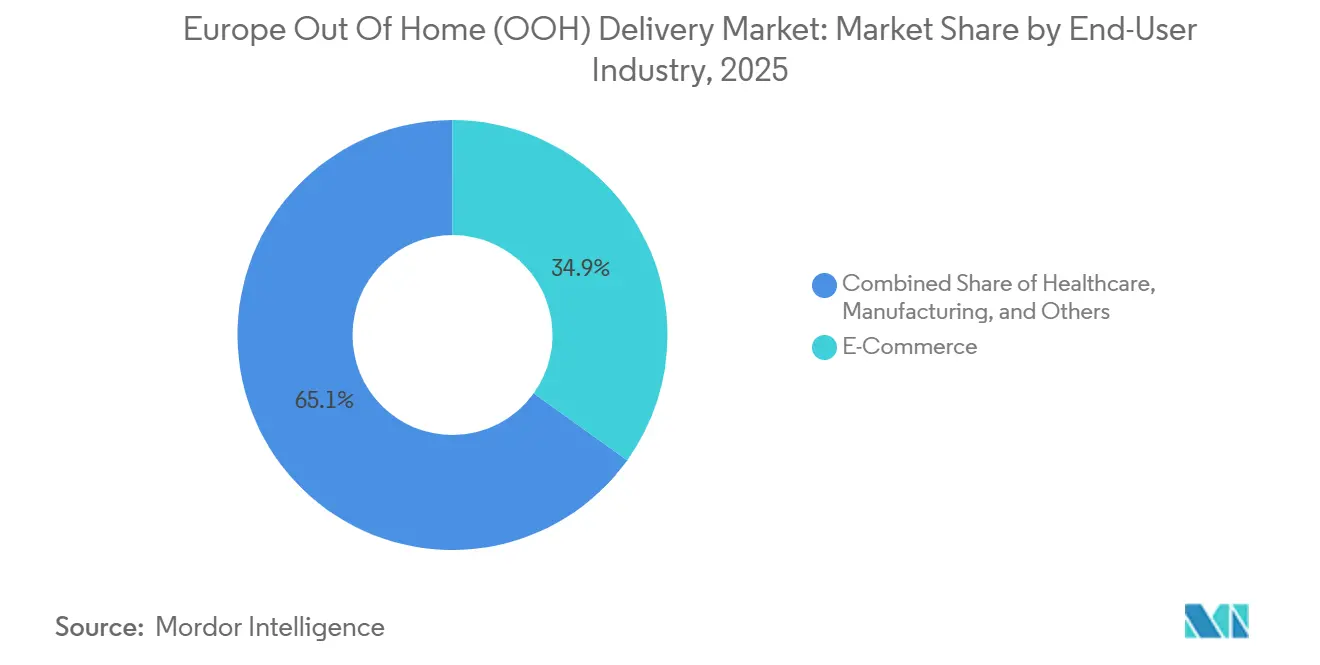

- By end-user industry, e-commerce held 34.91% of the Europe out-of-home (OOH) delivery market share in 2025 and is projected to expand at a 5.14% CAGR through 2031.

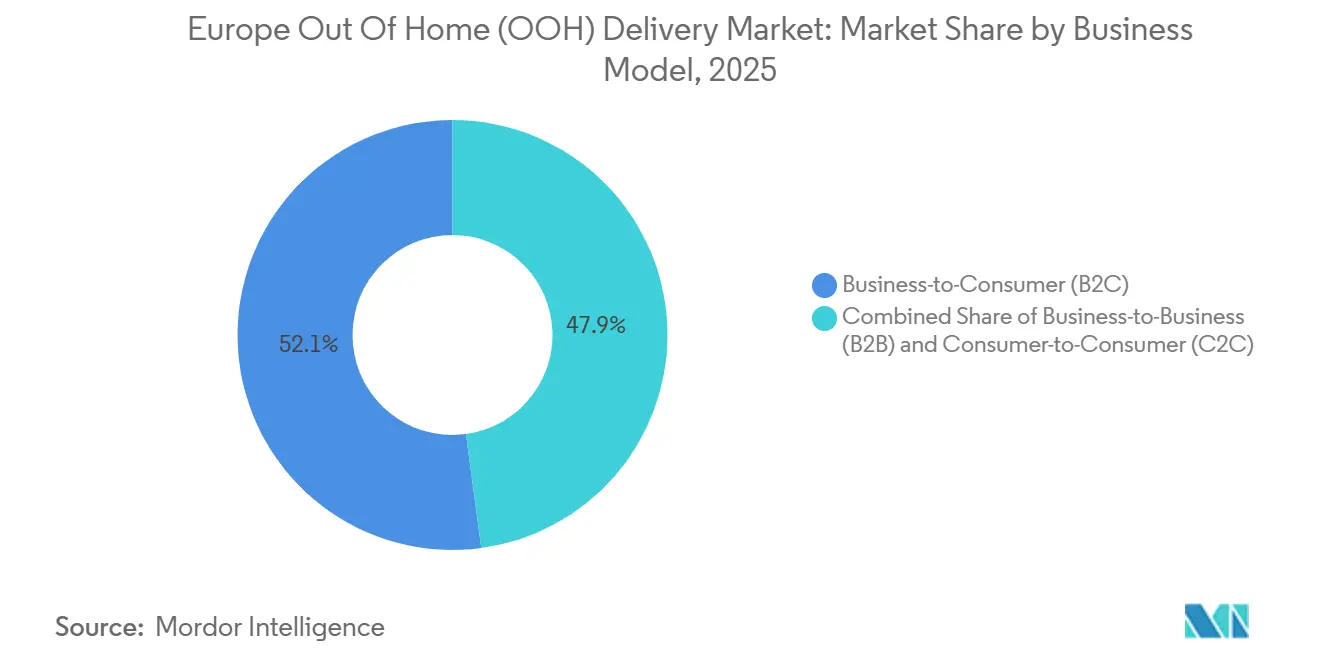

- By business model, B2C accounted for 52.14% share of the Europe out-of-home (OOH) delivery market size in 2025 and is forecast to grow at a 5.67% CAGR through 2031.

- By Country, Germany captured 18.34% share in 2025, while the Czech Republic is expected to record the highest CAGR of 6.03% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Worldwide, activity is shaped by contributions from multiple regions, with Europe representing one of the more structurally developed among them. The global report on out of home (ooh) delivery market by Mordor Intelligence reflects how these regional layers combine into a single system.

Europe Out Of Home (OOH) Delivery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-Commerce Checkout Shift to Flexible Delivery | +1.5% | Global, with highest impact in the UK, Germany, France, and Nordic markets | Short term (≤ 2 years) |

| Carrier Cost Pressure From Failed Home Delivery | +0.9% | Western Europe, with spillover into Central Europe | Short term (≤ 2 years) |

| Cross-Border Parcel Growth Raising OOH Use Cases | +0.8% | Pan-European, concentrated in Poland, France, Germany, and Spain | Medium term (2-4 years) |

| Locker and PUDO Densification in Urban Transit Hubs | +0.7% | Eastern Europe and rapidly expanding into Western Europe | Medium term (2-4 years) |

| Carrier-Neutral Software Improving Network Utilization | +0.5% | Strongest early adoption in Germany, the Netherlands, and Belgium | Long term (≥ 4 years) |

| Return-Heavy Shopping Behavior Favoring OOH Drop-Off | +0.6% | Highest volume impact in the UK, Germany, France, and Italy | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

E-Commerce Checkout Preference Shift Toward Flexible Delivery

The Europe out-of-home (OOH) delivery market is gaining support from a checkout environment where shoppers now expect to choose how and where a parcel will be delivered. DHL reported in 2025 that 81% of global shoppers abandon a basket if their preferred delivery option is unavailable, and 79% abandon if their preferred returns method is unavailable, tying conversion directly to delivery choice. Geopost stated in its 2025 E-Shopper Barometer that 46% of European regular online shoppers preferred out-of-home options, up 15 percentage points from 2019, and that parcel lockers had become the second-most-preferred delivery option in Europe[2]Geopost, “Geopost Releases Its E-Shopper Barometer 2025 Highlighting Important Changes in Online Shopping Behaviours,” La Poste Groupe, lapostegroupe.com. DHL also showed that younger users are more comfortable with locker-based returns, with Gen Z choosing parcel lockers for returns more often than Baby Boomers, which keeps the medium-term demand trend tilted upward as shopping cohorts change. As a result, access-point coverage is moving into retailer service agreements, because limited network reach now risks both checkout loss and lower returns convenience. This is why the European out-of-home (OOH) delivery market is increasingly defined by reach, visibility at checkout, and the ability to present a reliable non-home option before a parcel is even dispatched.

Carrier Cost Pressure From Failed Home Delivery Attempts

The Europe out-of-home (OOH) delivery market is also advancing because home delivery still carries avoidable reattempts, customer service work, and low stop density in congested routes. When carriers move more parcels into lockers or staffed collection points, one vehicle stop can serve many recipients, improving route productivity in a way doorstep delivery often cannot during peak periods. This is one reason large operators are building shared and open-access formats rather than relying solely on proprietary residential delivery models. DHL has already signaled that public access and scale matter to future rollout economics through its open-access and expanded Packstation approach in Germany, while DPD and GLS are jointly building the inboxx network to spread volume across shared infrastructure. The commercial logic is straightforward because every parcel redirected away from an uncertain home handoff improves stop efficiency and reduces the need for repeated attempts in dense cities. That operating pressure keeps pushing the Europe out-of-home (OOH) delivery market toward pricing models and service designs that make non-home delivery more attractive to both carriers and end users.

Cross-Border Parcel Growth Increasing OOH Use Cases

The Europe out-of-home (OOH) delivery market is benefiting from cross-border e-commerce, because sellers and marketplaces need delivery options that remain reliable across different address systems, languages, and customer expectations. Cross-Border Commerce Europe reported that the European cross-border e-commerce market reached EUR 358.7 billion (USD 421.94 billion) in 2024/2025, with online marketplaces accounting for 70% of that volume[3]Cross-Border Commerce Europe, “Sixth Edition of the Top 100 Cross-Border Marketplaces Europe Report,” Cross-Border Commerce Europe, cbcommerce.eu. La Poste Groupe stated that Geopost’s 2025 results underscored the importance of cross-border volumes and a broad European out-of-home footprint, indicating that access-point density now influences parcel-network selection for marketplace sellers. These flows align well with lockers and PUDO points, because recipients buying from foreign merchants are often more price-sensitive and more willing to accept a collection point in exchange for lower friction and fewer failed deliveries. Packeta’s 2025 volume growth, supported by integrations with platforms such as Vinted and Aukro, also shows that regional operators can take meaningful cross-border share when they combine marketplace links with established OOH access. This gives the Europe out-of-home (OOH) delivery market a broader role than domestic convenience, because it is becoming part of how cross-border parcel risk and cost are managed at scale.

Locker and PUDO Network Densification In Urban Transit Hubs

The Europe out-of-home (OOH) delivery market continues to strengthen, with operators installing lockers and collection points along daily commuter routes rather than at isolated destinations. Leaders in Logistics reported that bpost saw adoption rise from 18% to 33% after it tripled locker capacity, reinforcing the value of close proximity to where people already travel for work, shopping, and transit[4]Leaders in Logistics, "Out-of-Home Networks", leaders-in-logistics.com. DPD and GLS are following the same logic in Germany through the shared inboxx network at ECE shopping center car parks, which connects parcel access to existing retail traffic and limits the need for dedicated collection trips. Operators are also expanding the usable site pool with solar-powered, battery-autonomous lockers, reducing dependence on fixed electrical connections and making petrol stations, forecourts, and other high-footfall sites easier to activate. That matters because footfall and convenience now influence throughput as much as hardware count. The Europe out-of-home (OOH) delivery market, therefore, gains not only from more locations but also from better location economics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Uneven Locker Footprint in Rural and Low-Density Areas | -0.3% | Rural Germany, Eastern European periphery, and Southern and Iberian interiors | Long term (≥ 4 years) |

| Municipal Permitting and Street-Furniture Constraints | -0.2% | Western European cities and expanding into Central and Eastern European capitals | Medium term (2-4 years) |

| Asset Theft, Vandalism, and Maintenance Downtime | -0.1% | UK and Western European urban cores | Short term (≤ 2 years) |

| Interoperability Gaps Across Carrier Networks and Systems | -0.2% | Pan-European, most visible in Central and Eastern Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Uneven Locker Footprint In Rural and Low-Density Areas

The Europe out-of-home (OOH) delivery market still faces a practical coverage gap outside urban and suburban corridors, where lower parcel density weakens the economics of new access-point rollout. In rural districts, carriers often continue to prioritize home delivery even when those routes are more expensive, because the locker network is not yet deep enough to change behavior at scale. This creates a circular problem: thin coverage limits usage, and low usage slows future investment. Evidence from comparative deployment discussions in Europe shows that per-capita locker access remains much stronger in the most mature OOH territories than in large rural areas that still depend on traditional delivery patterns. Solar and battery-based hardware helps with site feasibility, but it does not fully solve the volume challenge in remote areas where each stop serves fewer users. Unless shared infrastructure, public facilitation, or broader carrier collaboration improves rural economics, the Europe out-of-home (OOH) delivery market will keep expanding unevenly across the region.

Municipal Permitting And Street-Furniture Constraints

The Europe out-of-home (OOH) delivery market is also constrained by local approval processes, because public-space rules often move more slowly than operator expansion plans. City-level permitting can vary by district, design standards, and siting conditions, lengthening deployment cycles and raising the cost of densification in high-demand urban zones. Prague adopted clearer criteria for parcel locker installations on municipal land in June 2025, which improved transparency but also showed how cities are increasingly formalizing design and technical rules for operators. Germany presents a similar issue, where DHL’s long-term Packstation rollout is tied not only to demand but also to the pace of municipal approvals for suitable sites. That mismatch matters because dense public placement is a major driver of consumer adoption, yet the best locations are usually the most regulated. The Europe out-of-home (OOH) delivery market, therefore, remains exposed to a medium-term bottleneck that is administrative as much as commercial.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-User Industry: E-Commerce Drives Both Scale and Velocity

E-commerce accounted for 34.91% share of the Europe out-of-home (OOH) delivery market size in 2025, and it is expected to post the fastest disclosed end-user CAGR at 5.14% through 2031. That lead comes from a direct fit between online order behavior and the core strengths of OOH delivery, namely flexible pickup timing, easier returns, and lower last-mile consolidation costs. Geopost’s 2025 shopper research showed that 46% of European regular online shoppers preferred out-of-home options, which supports the strong positioning of e-commerce within the Europe out-of-home (OOH) delivery industry. Categories such as fast fashion, beauty, and consumer electronics are especially relevant because they tend to combine high order frequency with high return intensity. That increases throughput per transaction, since a single order can generate both a delivery event and a return event over the same network.

The same structure makes e-commerce the segment with the clearest incentive to push access-point visibility earlier in the purchase path. Retailers gain from fewer missed handoffs and more predictable reverse logistics, while carriers gain from route consolidation and higher stop productivity. This mutually reinforcing logic is why the Europe out-of-home (OOH) delivery market keeps seeing OOH access treated as part of the online shopping proposition rather than only as a logistics backend feature. Financial services, healthcare, and manufacturing remain meaningful secondary users where secure document exchange, sample movement, and small-parts distribution benefit from controlled access. Primary industry, offline wholesale and retail trade, and other institutional categories still contribute smaller shares, but they widen the base of addressable demand by using the network for scheduled, secure, and non-urgent parcel movement.

By Business Model: B2C Leads, C2C Outpaces Expectations

B2C represented 52.14% of the Europe out-of-home (OOH) delivery market share in 2025 and is projected to grow at a 5.67% CAGR through 2031, making it the largest and fastest quantified business model segment in the current dataset. Its lead is rooted in parcel density, because consumer deliveries generate the highest volume of small shipments that benefit from flexible collection rather than a timed doorstep handoff. DHL reported that home delivery remained the preferred option for 54% of European consumers in 2025, yet the steady rise of parcel lockers and parcel shops suggests the default is shifting toward a mixed delivery pattern rather than a home-only model. That trend supports the Europe out-of-home (OOH) delivery market by pulling mainstream consumer traffic into lockers and staffed collection points without requiring a complete abandonment of home delivery. It also helps carriers shape demand with price and convenience levers at checkout.

B2B remains a solid supporting layer, especially in city centers, where office access limitations, delivery windows, and building controls make direct courier handoffs less efficient. C2C has also become more relevant as resale platforms push more peer-to-peer parcel volume into structured drop-off networks. Packeta’s partnership expansion with Vinted across Central and Eastern Europe showed how platform integrations can direct re-commerce parcels into lockers at scale. Geopost also noted that consumers now use an average of 2.6 different delivery options, which suggests that B2C and C2C users are becoming more comfortable switching between home and OOH channels depending on the item, urgency, and return probability. This behavioral flexibility gives the Europe out-of-home (OOH) delivery market room to grow across multiple use cases even when headline parcel demand changes by channel.

Geography Analysis

Germany accounted for 18.34% of the Europe out-of-home (OOH) market in 2025, making it the largest national market in the region. The country’s lead rests on a mature Packstation base, a large parcel economy, and a growing shift toward shared infrastructure rather than single-carrier buildout alone. DHL has stated that it plans to expand its Packstation network from around 15,500 units to 30,000 by 2030, which shows that Germany still has room for additional density despite its mature starting point. The DPD and GLS inboxx program adds another layer to that expansion path by targeting 20,000 shared OOH points, including up to 6,000 lockers, by 2027 under a common brand. Furthermore, the Czech Republic is expected to record the fastest CAGR at 6.03% through 2031.

The United Kingdom, France, and Italy form the next major cluster of opportunity in the Europe out-of-home (OOH) delivery market, but each follows a different infrastructure path. The United Kingdom is accelerating from a lower historical base, with stronger retailer and forecourt partnerships helping locker usage become more visible in everyday locations. France benefits from Geopost’s broad access-point estate and a shopper base that already uses OOH options frequently for both delivery and returns. Italy remains important because return-heavy retail categories and urban density suit staffed pickup and locker-based delivery, even if network depth is less mature than in Germany or Poland.

Spain and the rest of Europe provide a wider expansion field for the Europe out-of-home (OOH) delivery market as operators extend partnerships into retail, fuel, and transit environments. Cross-border marketplace activity is especially relevant here, because a broader regional network allows sellers to serve multiple countries with a more consistent delivery proposition. The strongest geographic pattern is no longer just national scale, but the ability to connect dense domestic networks into interoperable regional systems. Markets with mature locker habits tend to support faster returns adoption, while less mature markets often begin with convenience-led pickup use cases before returns follow. This makes geography in the Europe out-of-home (OOH) delivery market a story of both current density and future network compatibility.

Mordor Intelligence provides coverage of the out of home (ooh) delivery market across other key regional markets. Detailed country-level analysis extends to Saudi Arabia incorporating local coverage and market participation, as required.

Competitive Landscape

The Europe out-of-home (OOH) delivery market shows moderate concentration within individual countries, but the competitive field becomes much more fragmented at the pan-European level. National leaders still hold strong positions in their home territories, yet no single operator has built a continent-wide position that fully mirrors the dominance seen in some other logistics segments. The clearest strategic signal came in February 2026, when FedEx and Advent agreed to acquire InPost at a total valuation of EUR 7.8 billion (USD 9.2 billion), confirming that large OOH networks are now treated as strategic infrastructure assets rather than secondary parcel accessories. That move also showed that ownership of dense locker infrastructure can strengthen cross-border reach, regain control, and influence checkout simultaneously. The Europe out-of-home (OOH) delivery market is therefore competing on density, interoperability, and the ability to turn access points into a commercial moat.

A second strategic path is visible in shared and carrier-neutral expansion. DPD and GLS created the inboxx brand in Germany to combine delivery volumes and scale shared access points under a single network identity, reducing the burden of building separate, proprietary estates. Myflexbox offers another version of this model by providing carrier-neutral lockers that different logistics partners can use, as shown by its 2026 cooperation with Nova Post in Austria. These models matter because utilization often determines site economics more than pure hardware ownership. They also lower the barrier for newer parcel operators that want OOH presence without a full hardware rollout.

Competition is also broadening into hardware design, power flexibility, and software coordination across networks. Battery-based and solar-based lockers allow operators to pursue sites that were previously too difficult or too slow to connect, which changes the economics of rollout in forecourts, parking areas, and temporary high-footfall locations. SwipBox’s ownership transition in early 2026 underlined the value investors still place on scalable, carrier-agnostic locker platforms with room for faster rollout. The main white spaces remain rural and peri-urban coverage, returns-focused network design, and orchestration software that can present multiple OOH options inside a single checkout flow. That keeps the Europe out-of-home (OOH) delivery market open to consolidation, but it also leaves meaningful room for specialized operators that solve utilization and interoperability better than larger incumbents.

Europe Out Of Home (OOH) Delivery Industry Leaders

-

DHL Group

-

DSV A/S

-

La Poste (including Geopost)

-

InPost (including Mondial Relay)

-

GLS Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Austrian Post expanded its partnership with Amazon, providing access to over 1,600 post stations across Austria. Customers can now select these stations at checkout. The company also plans to add 150 more stations by the end of 2026, further growing the OOH addressable market in Central Europe.

- May 2026: Nova Post announced the expansion of its courier services to five regions in the Czech Republic and its partnership with myflexbox for parcel lockers in Austria and the Netherlands.

- April 2026: myflexbox and Nova Post launched a parcel delivery partnership in Austria, with Nova Post using its own vehicle fleet to deliver into myflexbox's carrier-neutral locker network in Vienna, with a rollout to over 550 partner locker locations planned nationwide by end-2026.

- February 2026: A consortium led by FedEx and Advent International reached a conditional agreement to acquire InPost, giving FedEx access to InPost's 61,000+ European APM network.

Europe Out Of Home (OOH) Delivery Market Report Scope

The Europe out-of-home delivery market refers to logistics services that enable the delivery of goods to locations outside of traditional home addresses, such as parcel lockers, collection points, and pick-up/drop-off locations. This market supports e-commerce, retail, food, and grocery deliveries, offering flexible and efficient alternatives to doorstep deliveries.

The report provides a comprehensive background analysis of the europe out-of-home delivery market, covering the current market trends, restraints, technological updates, and detailed information on various segments and the industry's competitive landscape. Additionally, the impact of geopolitics and the pandemic has been incorporated and considered during the study. The europe out-of-home delivery market is Segmented By End-User Industry (E-commerce & Retail, Food & Grocery Delivery, Healthcare & Pharmaceutical, Logistics & Transportation, Consumer Electronics and Other End-User Industries), By Customer Type (Business-to-Business (B2B), Business-to-Consumer (B2C) and Consumer-to-Consumer (C2C)) and By Country (United Kingdom, Germany, France, Poland, Italy and Other Countries). The report offers the europe out-of-home delivery market size and forecasts in values (USD) for all the above segments.

| E-Commerce |

| Financial Services (BFSI) |

| Healthcare |

| Manufacturing |

| Primary Industry |

| Wholesale and Retail Trade (Offline) |

| Others |

| Business-to-Business (B2B) |

| Business-to-Consumer (B2C) |

| Consumer-to-Consumer (C2C) |

| Germany |

| France |

| Poland |

| Italy |

| Spain |

| United Kingdom |

| Rest of Europe |

| By End-User Industry | E-Commerce |

| Financial Services (BFSI) | |

| Healthcare | |

| Manufacturing | |

| Primary Industry | |

| Wholesale and Retail Trade (Offline) | |

| Others | |

| By Business Model | Business-to-Business (B2B) |

| Business-to-Consumer (B2C) | |

| Consumer-to-Consumer (C2C) | |

| By Country | Germany |

| France | |

| Poland | |

| Italy | |

| Spain | |

| United Kingdom | |

| Rest of Europe |

Key Questions Answered in the Report

What is the 2026 value of Europe out-of-home delivery?

The Europe out-of-home (OOH) delivery market is valued at USD 14.37 billion in 2026 and is forecast to reach USD 18.19 billion by 2031 at a 4.83% CAGR.

Which end-user segment contributes the most demand?

E-commerce leads with 34.91% share in 2025 and also posts the fastest disclosed end-user growth at 5.14% through 2031.

Why are parcel lockers gaining faster traction than traditional pickup points?

Locker growth is supported by checkout flexibility, easier returns, and stronger route efficiency for carriers. It also improves convenience because users can collect parcels on their own schedule.

Which business model is the largest in this space?

B2C is the largest model with 52.14% share in 2025, and it is also the fastest quantified segment with a 5.67% CAGR through 2031.

Which countries are shaping regional growth the most?

Germany is the largest country market with 18.34% share in 2025, while the Czech Republic is forecast to expand the fastest at 6.03% CAGR through 2031.

What is the main constraint on wider OOH adoption in Europe?

The biggest limits are uneven rural coverage and slow municipal permitting in urban areas, both of which delay network densification where convenience matters most.

Page last updated on: