Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

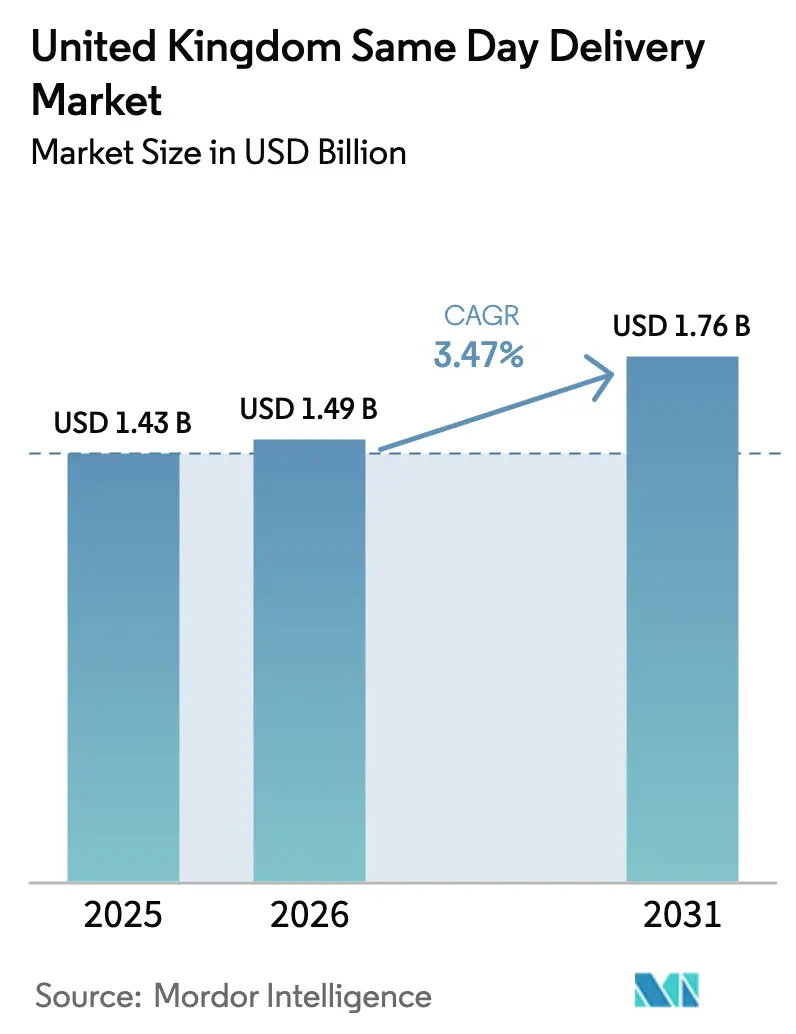

| Base Year Market Size (2025) | USD 1.43 Billion |

| Market Size (2026) | USD 1.49 Billion |

| Market Size (2031) | USD 1.76 Billion |

| Growth Rate (2026 - 2031) | 3.47% CAGR |

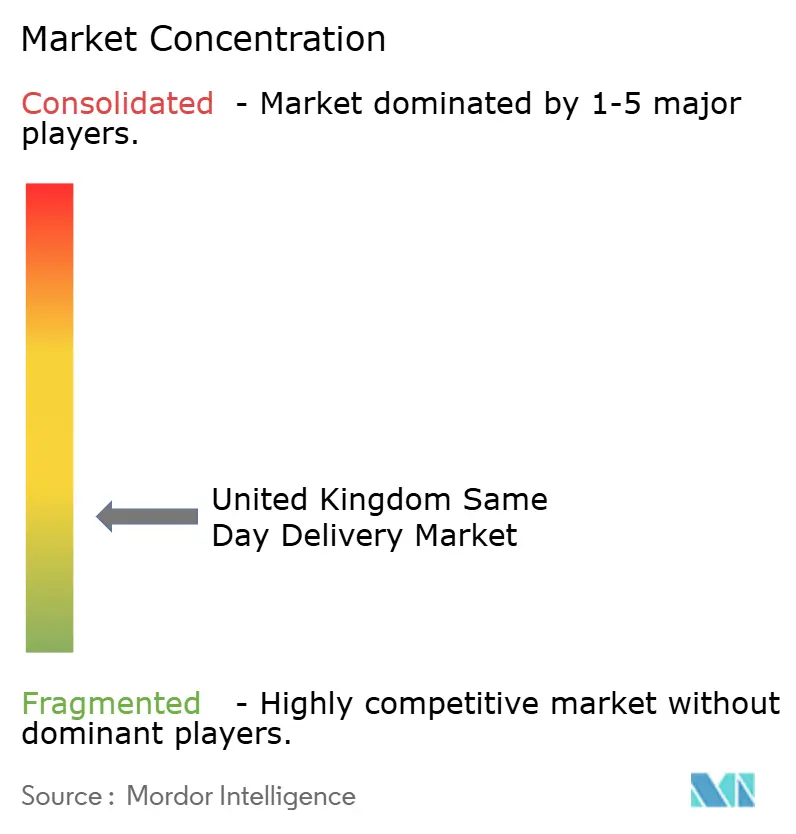

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Same Day Delivery Market Analysis by Mordor Intelligence

The United Kingdom Same Day Delivery Market size is estimated at USD 1.49 billion in 2026, and is expected to reach USD 1.76 billion by 2031, at a CAGR of 3.47% during the forecast period (2026-2031).

Demand is coalescing around hyper-local fulfillment nodes that cut transit legs, while congestion penalties inside low-emission zones accelerate fleet electrification and cargo-bike adoption. E-commerce parcel density still underpins route economics, yet premium B2B lanes in healthcare, aerospace, and financial services now contribute a disproportionate share of operating profit. Consolidation is reshaping service breadth: DPD UK’s purchase of CitySprint brings 88% national coverage within 60 minutes, whereas InPost’s acquisition of Yodel marries doorstep delivery with 14,000 locker locations for hybrid fulfillment. Technology investment has become table stakes as carriers deploy dynamic dispatch software that trims route distance by 25% and lifts on-time-in-full scores by 15%.

Key Report Takeaways

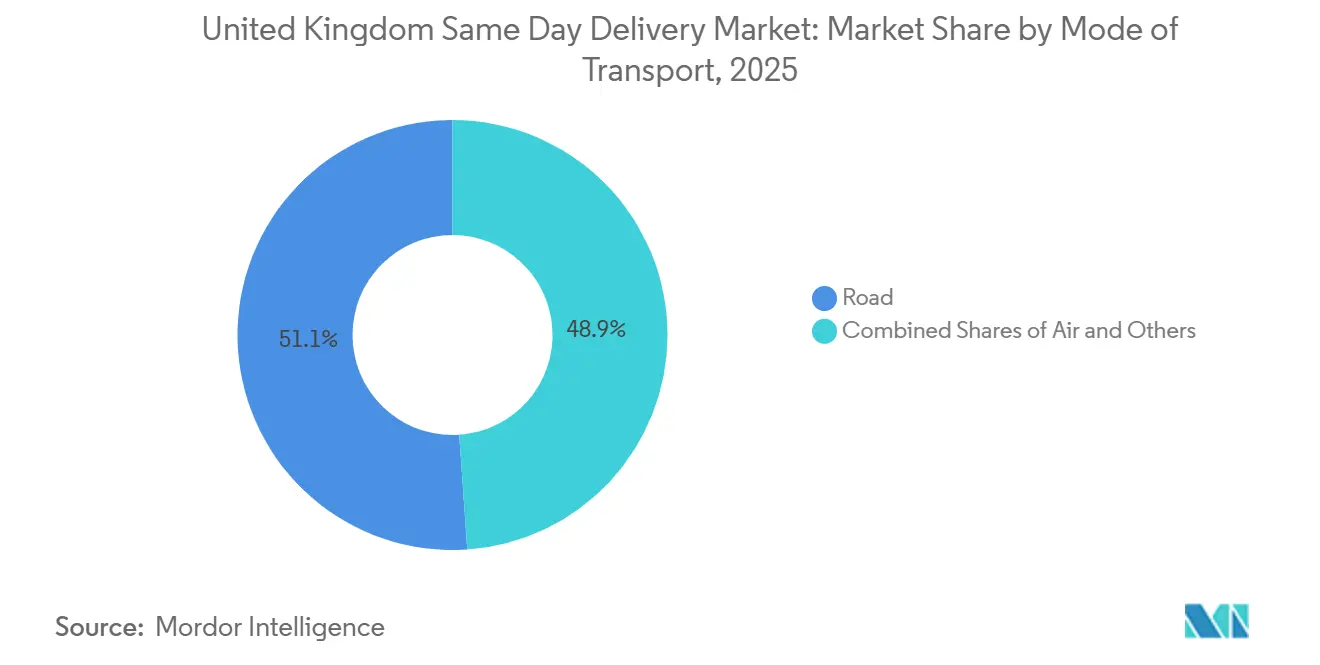

- By mode of transport, road captured 51.09% of the United Kingdom same day delivery market share in 2025, while air freight is set to advance at a 3.92% CAGR through 2031.

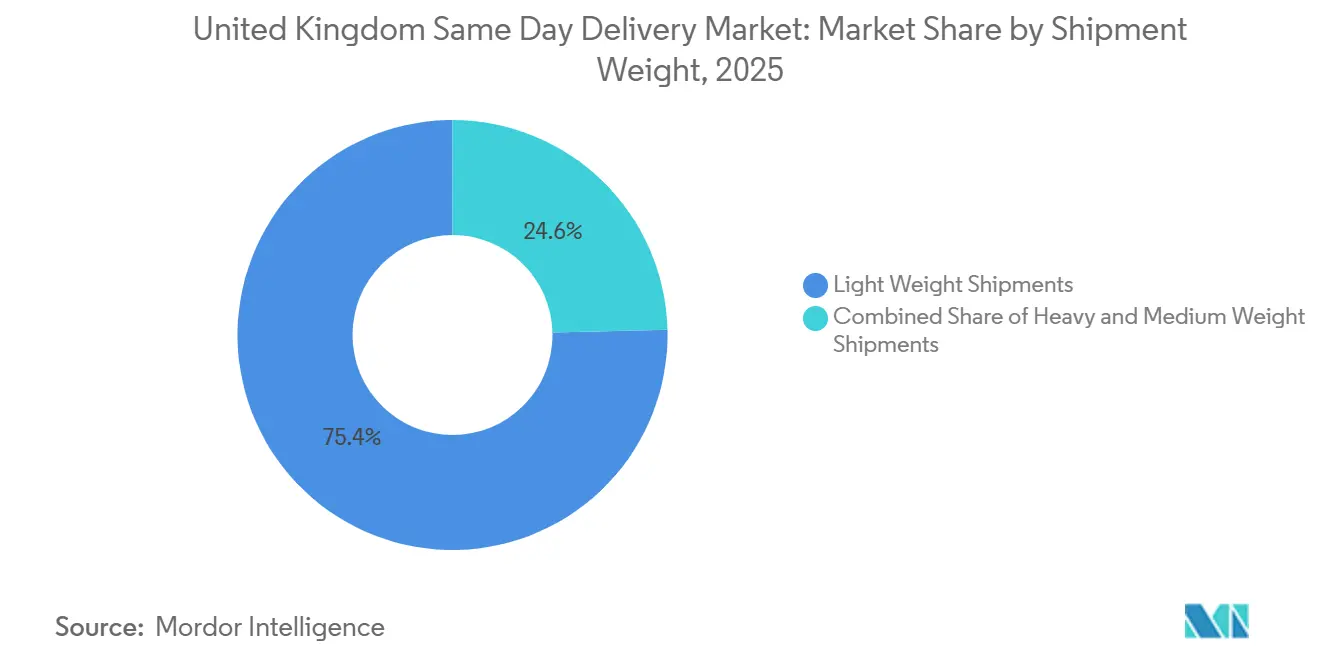

- By shipment weight, light-weight parcels accounted for 75.38% of the United Kingdom same day delivery market size in 2025 and are forecast to expand at a 4.21% CAGR to 2031.

- By customer type, B2C deliveries held 69.71% of volume in 2025, whereas wholesale and retail trade offline is growing fastest at a 3.99% CAGR.

- By end-user industry, e-commerce commanded 53.23% share in 2025, but offline retailers’ click-and-collect programs are the quickest-rising use case at 3.99% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Kingdom Same Day Delivery Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging hyper-local e-grocery demand post-pandemic | +0.8% | London, Manchester, Birmingham metros | Medium term (2-4 years) |

| Retailer investment in urban micro-fulfillment centres | +0.7% | Major conurbations nationwide | Long term (≥ 4 years) |

| Rapid shift to 100%-tracked deliveries by major carriers | +0.5% | National | Short term (≤ 2 years) |

| ULEZ-linked incentives for zero-emission cargo-bike fleets | +0.6% | London, Bristol, Manchester, Birmingham | Medium term (2-4 years) |

| Retail delivery-pass/subscription models boosting repeat orders | +0.7% | Urban postcodes nationwide | Short term (≤ 2 years) |

| Public sustainability policy driving urban micro-hubs | +0.5% | London, Manchester, Birmingham, Edinburgh, Glasgow | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging Hyper-local E-grocery Demand Post-pandemic

On-demand grocery platforms processed close to 100 million UK orders worth about USD 4.06 billion in 2025, yet Deliveroo’s withdrawal from dark stores exposed fragile unit economics, pushing capacity back into supermarket estates. Waitrose’s GBP 85 (USD 114) annual Delivery Pass underwrote same-day slots from 200-plus stores, illustrating how subscriptions anchor repeat demand[1]Corporate Communications, “Delivery Pass Information,” Waitrose, waitrose.com. Ocado’s micro-fulfillment sites now exceed 300 picks per hour, enabling two-hour windows that manual warehouses cannot match. With average delivery radii shrinking under five kilometers, cargo-bike fleets gain a cost advantage inside low-emission zones. As a result, the United Kingdom's same-day delivery market is pivoting from long-haul trunking toward dense urban spokes that reward micro-hubs and zero-emission assets.

Retailer Investment in Urban Micro-fulfillment Centers

Marks & Spencer committed USD 460 million to an automated DC in 2025, targeting 300 picks per hour to support 500 stores’ click-and-collect promises. British Land is converting vacant high-street units into logistics nodes, as rents per square meter for parcel throughput now exceed those for apparel tenants. Argos already fulfills Fast Track orders from 300 outlets, demonstrating parity with pure-play e-commerce on speed while lowering return rates through in-person inspection. These moves cement brick-and-mortar stores as last-mile inventory buffers, sustaining the United Kingdom's same-day delivery market shift toward store-as-warehouse configurations in traffic-restricted cores.

Rapid Shift to 100%-tracked Deliveries by Major Carriers

Descartes routing tools cut van mileage by 25% and improve punctuality by 15%, while insurers grant 10% premium discounts for fleets with telematics-verified proof of delivery. Mapbox’s AI clustering reduces stop distances by 23%, which manual planning cannot replicate. Amazon has begun Prime Air drone drops in Darlington to guarantee sub-60-minute service where van density is low. In consequence, real-time visibility has become baseline rather than value-added, and laggards risk churn as customers migrate to carriers offering live ETAs.

ULEZ-linked Incentives for Zero-emission Cargo-bike Fleets

Transport for London offers up to USD 12,860 toward electric van replacements and USD 2,031 for cargo bikes, estimating that bikes could displace up to 17% of van kilometers by 2030. Amazon has already executed 150 million zero-emission UK deliveries since 2022, validating cargo bikes within a three-kilometer radius. Large-scale carriers now split fleets: cargo bikes in inner ULEZ districts, electric vans in outer boroughs, and diesel only for depot trunking. This bifurcation favors operators with the capital depth to manage multiple asset classes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic courier labor shortages & rising wage floors | -0.6% | Nationwide, acute in London and South East | Short term (≤ 2 years) |

| Van-mile congestion penalties in major UK cities | -0.4% | London, Birmingham, Manchester, Bristol | Medium term (2-4 years) |

| Tight working-time reforms for gig riders from 2027 | -0.5% | National | Medium term (2-4 years) |

| Retailer push-back on premium-speed fees | -0.3% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Chronic Courier Labor Shortages & Rising Wage Floors

The Road Haulage Association calculates a 60,000-driver annual recruitment need from 2025 onward, while the National Living Wage climbed to USD 16.54 per hour in April 2025, squeezing operators reliant on gig labor. Automation helps only at the margin: Prime Air drones remove some van routes, but payload limits confine them to sub-2-kilogram parcels. Carriers without the scale to spread higher wages over dense routes risk ceding share to integrators able to fund electric fleets and robotics.

Van-mile Congestion Penalties in Major UK Cities

A non-compliant van running 250 days a year incurs up to USD 6,094 in fees in London and Birmingham, plus 10%-15% higher insurance premiums and lower resale value[2]Insight Paper, “Clean Air Zone Birmingham,” Birmingham City Council, birmingham.gov.uk . Some carriers respond by renting micro-hubs inside ULEZ perimeters, yet British Land reports these spaces lease at 20%-30% above traditional warehouses. Smaller firms therefore face a capital hurdle that accelerates consolidation in the United Kingdom same-day delivery market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Transport: Air Freight Captures High-Value Lanes

The United Kingdom same-day delivery market size for air freight is expanding at a 3.92% CAGR, outpacing all other modes, even though road still owns 51.09% share in 2025. High-value consignments such as temperature-controlled pharmaceuticals and mission-critical aerospace parts justify per-kilogram rates exceeding USD 67.69, explaining IAG Cargo’s “Critical” service gains. Virgin Atlantic’s Courier product and DHL’s Air Priority bridge standard next-day and bespoke charter pricing, giving shippers a mid-tier option.

Road networks remain indispensable for e-commerce volume, yet zero-emission vans and cargo bikes increasingly handle inner-city drops, while rail lanes pre-position goods overnight to cut peak-hour van mileage. This multimodal mix demonstrates how the United Kingdom's same-day delivery market is diverging: air competes on reliability, road on cost per drop, and bikes on regulatory compliance.

By Customer Type: B2C Volume, B2B Margin

B2C retained 69.71% of the United Kingdom's same-day delivery market share in 2025 and will continue growing at a 3.58% CAGR, buoyed by Amazon’s 80-city footprint. Nonetheless, willingness to pay seldom exceeds USD 13.54, forcing carriers toward automation to achieve a sub-USD 4.06 cost per drop. In contrast, B2B and B2G clients pay USD 27.07-USD 67.69 for mission-critical shipments, safeguarding margins against consumer belt-tightening.

Healthcare, aerospace, and finance depend on guaranteed delivery windows backed by chain-of-custody documentation, and UPS Healthcare’s cold-chain launch exemplifies this specialization[3]Service Overview, “UPS Healthcare Cold-Chain,” UPS Healthcare, ups.com . Carriers that balance high-volume B2C with high-margin B2B therefore enjoy a more resilient revenue mix across economic cycles.

By Shipment Weight: Light-weight Parcels Fuel Micromobility

Light-weight parcels under 2 kg accounted for 75.38% of the United Kingdom same-day delivery market size in 2025 and will rise at a 4.21% CAGR. These items align with the 100 kg payload ceiling of modern cargo bikes, allowing 20-30 stops per run in dense boroughs. Medium-weight parcels remain the province of electric vans, while heavy loads above 20 kg require larger vehicles whose ULEZ surcharges erode profitability.

DPD’s CitySprint absorption brought 3,500 multi-size vehicles under one network, illustrating the scale needed to balance different weight classes. Going forward, carriers that optimize fleet mix to weight distribution will gain cost leadership, further segmenting competition within the United Kingdom same-day delivery market.

By End-user Industry: Offline Retail’s Click-and-collect Resurgence

E-commerce produced 53.23% of demand in 2025, yet brick-and-mortar chains are the fastest-growing end-users at 3.99% CAGR as they deploy same-day click-and-collect to lure footfall. John Lewis launched a two-hour collection from select stores, leveraging existing inventory rather than dark stores. Marks & Spencer’s automated DC underpins a 500-store network that meets parity with Amazon on speed while retaining in-store upsell opportunities.

Healthcare continues to command premium prices, proven by NHS Blood and Transplant’s organ courier lanes exceeding USD 676.98 per trip. Manufacturing just-in-time replenishment and financial services document transfer round out high-margin verticals, giving carriers diversification beyond cyclical retail volumes.

Geography Analysis

Greater London delivered the largest slice of the United Kingdom's same-day delivery market in 2025, aided by population density above 5,700/km² and TfL incentives that cover up to USD 12,860 per electric van. Cargo bikes have already completed 150 million zero-emission drops city-wide, and TfL forecasts 1%-17% van-kilometer displacement by 2030.

Second-tier metros Manchester, Birmingham, and Edinburgh are witnessing rapid micro-fulfillment roll-outs as retailers seek two-hour windows without dark-store capital outlays. InPost’s enlarged 14,000-locker network offers suburban consumers lower-cost same-day alternatives where doorstep density is weak. Wales and Northern Ireland remain smaller contributors; nonetheless, Amazon’s rail partnership on the West Coast Main Line shows how overnight intermodal legs can extend same-day reach without adding daytime van mileage[4]Press Release, “West Coast Main Line Rail Deliveries,” Amazon UK, aboutamazon.co.uk .

The Competition and Markets Authority’s approval of the Evri/DHL merger, which provided that no single segment exceeds a 40% share, suggests regulators will support consolidation that funds emission-compliant fleets. Local specialists Gophr, eCourier retain niche advantages but face higher per-unit costs in ULEZ districts. Consequently, profitability across the United Kingdom same-day delivery market will diverge by locale: London favors micromobility, while regional towns rely on electrified vans and hybrid locker networks.

Competitive Landscape

No operator controls more than 15% of the United Kingdom's same-day delivery market, giving the sector a low concentration profile. DPD UK’s acquisition of CitySprint and InPost’s purchase of Yodel both show that parcel companies are buying rivals so they can handle more parcels and grow in scale. This larger volume makes it easier for them to afford electric delivery vehicles and smarter route-planning technology, which are expensive but important for efficiency and sustainability. Amazon’s vertically integrated network covers 80 cities with same-day service and now layers Prime Air drones onto rural fringes, compelling rivals to match sub-60-minute promises or pivot toward specialist B2B niches.

Technology is the principal battleground. Descartes and Mapbox algorithms cut route miles and fuel, while full-stack telematics shave insurers’ risk premia. Smaller couriers that delay tech adoption instead tout local knowledge, yet the Employment Rights Bill 2024 will raise their labor cost floor by 2027, eroding this advantage.

Hybrid fulfillment is emerging as a white-space play. InPost processes 115 million locker parcels annually and projects 300 million post-Yodel, enabling carriers to blend doorstep and locker networks for cost-tiered offerings. Zedify’s cargo-bike franchising model further fragments last-mile choices, proving that capital-light, zero-emission formats can steal share where vans face congestion fees and parking limits. The competitive outlook therefore favors operators that achieve national density, field multi-modal fleets, and sustain software investment.

United Kingdom Same Day Delivery Industry Leaders

Royal Mail

DPD UK

CitySprint

Amazon Logistics

Deliveroo Hop

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Amazon confirmed new same-day fulfillment centers in Hull (2,000 jobs) and Northampton (opening 2026, another 2,000 jobs) to widen AI-defined “fast-delivery areas.

- Sep 2025: The Competition and Markets Authority cleared the Evri/DHL merger, creating a parcel giant while capping next-day pricing.

- April 2025: InPost bought Yodel for GBP 106 million (USD 143.5 million ), combining 8% market share with 300 million parcels a year.

- January 2025: Royal Mail started a same-day pilot with Amazon in three London boroughs to test service-level parity.

United Kingdom Same Day Delivery Market Report Scope

By Mode of Transport

| Air |

| Road |

| Others |

By Customer Type/Buyer

| B2C (Consumer Deliveries) |

| B2B (Incl. B2G) |

By Shipment Weight

| Heavy Weight Shipments |

| Light Weight Shipments |

| Medium Weight Shipments |

By End User Industry

| E-Commerce |

| Financial Services (BFSI) |

| Healthcare |

| Manufacturing |

| Primary Industry |

| Wholesale & Retail Trade (Offline) |

| Others |

| By Mode of Transport | Air |

| Road | |

| Others | |

| By Customer Type/Buyer | B2C (Consumer Deliveries) |

| B2B (Incl. B2G) | |

| By Shipment Weight | Heavy Weight Shipments |

| Light Weight Shipments | |

| Medium Weight Shipments | |

| By End User Industry | E-Commerce |

| Financial Services (BFSI) | |

| Healthcare | |

| Manufacturing | |

| Primary Industry | |

| Wholesale & Retail Trade (Offline) | |

| Others |

Key Questions Answered in the Report

How large will the United Kingdom same-day delivery market be by 2031?

It is forecast to reach USD 1.76 billion, expanding at a 3.47% CAGR from 2026 to 2031.

Which segment contributes the most revenue today?

Road transport remains dominant, holding 51.09% of 2025 revenue.

Why are cargo bikes gaining traction?

Low-emission-zone fees and grants of up to GBP 1,500 per bike make micro-mobility cheaper than vans for inner-city routes.

What drives premium pricing in B2B lanes?

Time-critical shipments in healthcare, aerospace, and financial services command GBP 20-GBP 50 per parcel due to strict delivery windows.

How is technology reshaping last-mile operations?

Dynamic dispatch software cuts route distance 25% and, along with telematics, earns insurers’ premium discounts of 10%-15%.

Page last updated on: