Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

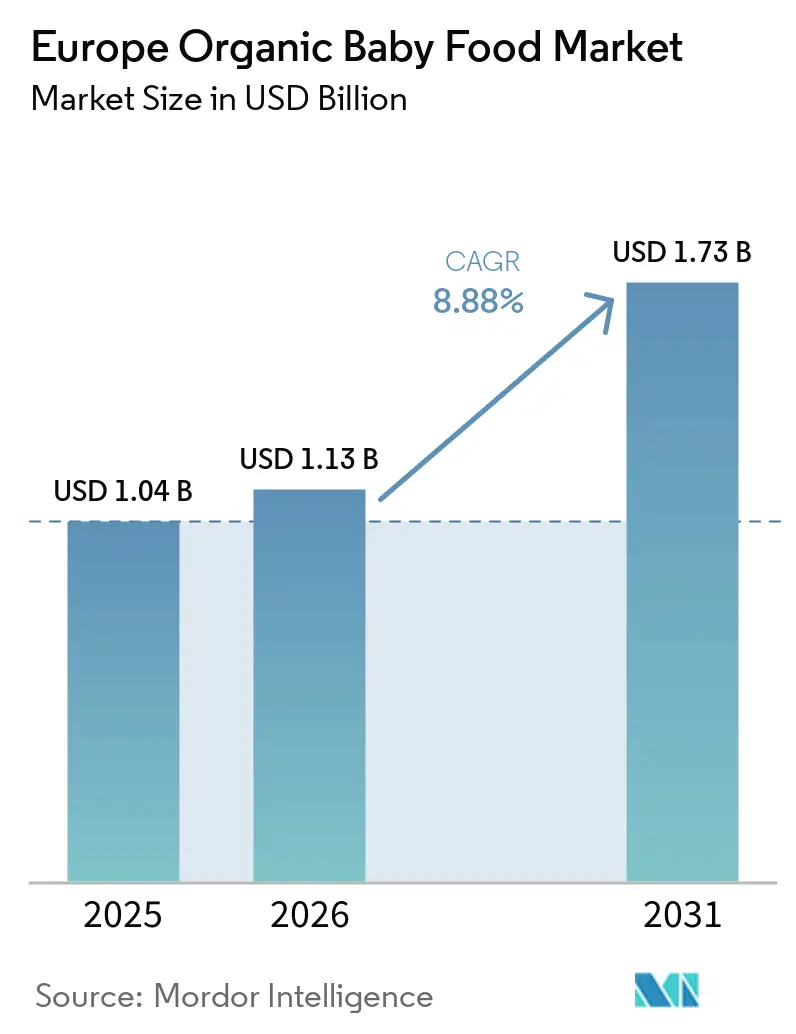

| Base Year Market Size (2025) | USD 1.04 Billion |

| Market Size (2026) | USD 1.13 Billion |

| Market Size (2031) | USD 1.73 Billion |

| Growth Rate (2026 - 2031) | 8.88% CAGR |

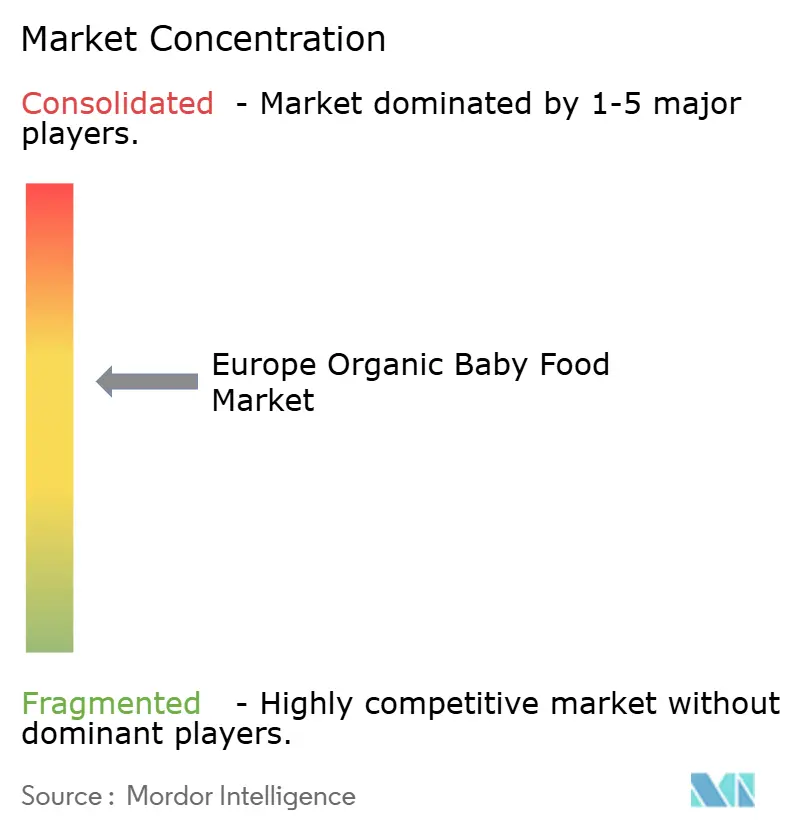

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Organic Baby Food Market Analysis by Mordor Intelligence

The Europe Organic Baby Food Market size was valued at USD 1.04 billion in 2025 and estimated to grow from USD 1.13 billion in 2026 to reach USD 1.73 billion by 2031, at a CAGR of 8.88% during the forecast period (2026-2031). Parents' increasing preference for clean-label and pesticide-free nutrition options, along with growing awareness of early nutrition's impact on long-term health, drives this growth. The rise in working mothers and busy family schedules has increased demand for convenient, ready-to-eat organic baby food options, particularly given the region's low exclusive breastfeeding rates. Companies such as HiPP, Holle, and Kendamil are developing organic infant formulas that replicate breast milk composition through functional ingredients. The market shows expansion in specialized formulas, including goat milk-based options and those enhanced with probiotics and prebiotics, addressing specific dietary requirements. The European Union's stringent organic certification standards support market growth while creating substantial barriers to entry for new market participants.

Key Report Takeaways

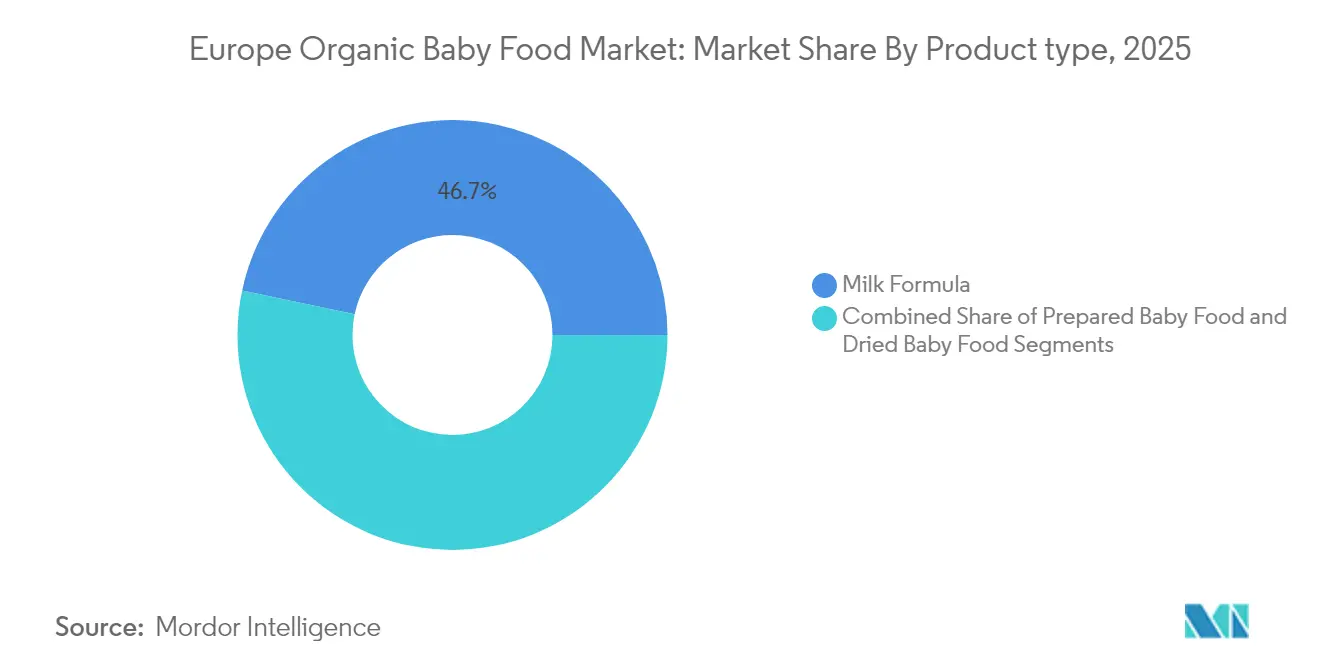

- By product type, milk formula led with 46.68% of the Europe organic baby food market share in 2025; dried baby food is projected to expand at an 11.45% CAGR to 2031.

- By age group, the 6–12 months segment accounted for 38.08% share of the European organic baby food market size in 2025, while the 18–24 months segment posts the highest projected CAGR at 10.18% through 2031.

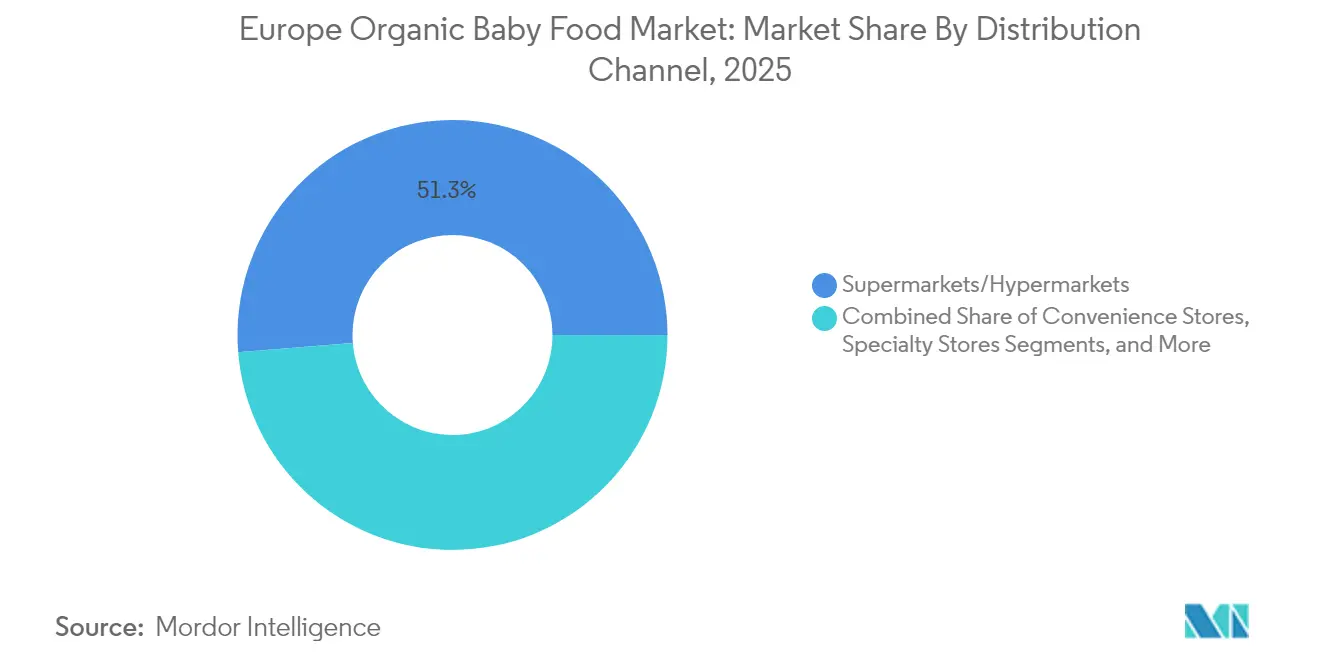

- By distribution channel, supermarkets/hypermarkets held 51.27% of the Europe organic baby food market share in 2025; online retail is forecast to grow at an 8.21% CAGR between 2026-2031.

- By geography, Germany captured 21.92% of the European organic baby food market share in 2025; the Netherlands is set to advance at a 13.52% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Organic Baby Food Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in Parent Awareness for Infant Nutrition | +2.30% | Pan-European, with higher impact in Northern and Western Europe | Medium term (2-4 years) |

| EU Organic Certification Stringency Elevates Consumer Trust & Demand | +1.80% | EU member states, with spillover effects to UK and Switzerland | Long term (≥ 4 years) |

| Growing Demand for Goat Milk-based Organic Formula | +1.40% | Western Europe, particularly France, Germany, and Netherlands | Short term (≤ 2 years) |

| Strategic Investment by Players | +1.20% | Pan-European, concentrated in manufacturing hubs in Germany, France, and Netherlands | Medium term (2-4 years) |

| Enhanced Retail Distribution Networks for Organic Baby Food | +1.10% | Pan-European, with higher penetration in urban centers | Medium term (2-4 years) |

| Growing Demand for Sustainable and Eco-friendly Food Options | +0.90% | Northern and Western Europe, particularly Scandinavia and Germany | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rise in Parent Awareness for Infant Nutrition

The Europe organic baby food market is experiencing growth driven by increased parental awareness of infant nutrition. European parents are seeking organic, nutrient-rich, and allergen-free baby food options due to concerns about the health impacts of processed foods, artificial additives, and chemical residues. This has led to a preference for organic baby foods with clear labeling that demonstrate safety and quality standards. The market has evolved to meet these consumer needs by developing products enhanced with functional ingredients like probiotics, prebiotics, DHA, ARA, and human milk oligosaccharides (HMOs), which support immune function, cognitive development, and digestive health. In October 2023, Little Freddie introduced a new line of dairy-free yogurt alternatives in the baby food category, featuring two organic yogurt-style pouches in Banana & Raspberry and Strawberry flavors.

EU Organic Certification Stringency Elevates Consumer Trust & Demand

The European Union's organic certification framework, established through Regulation (EU) 2018/848, sets comprehensive standards that enhance consumer trust in organic baby food products [1]European Commission, "EU organic certification according to Reg. (EU) 2018/848", https://european-union.europa.eu/. The regulation specifies strict requirements for organic production and labeling, including the prohibition of hydroponic crop production and the requirement for organic livestock feed, ensuring ingredient quality in baby food. This regulatory framework influences parents' purchasing decisions, as they prioritize product safety and reliable certification. The European Union standards, being more stringent than those in other regions, provide European producers with market advantages and attract consumers seeking high-quality products worldwide. The certification process includes strict pesticide residue limits for infant and young children's food, with a general maximum residue level (MRL) of 0.01 mg/kg (European Food Safety Authority, 2024).

Growing Demand for Goat Milk-based Organic Formula

The demand for goat milk-based organic formula continues to grow due to its digestibility and nutritional benefits compared to conventional cow's milk formulas. Goat milk contains smaller protein molecules that enable easier digestion in infants, while its natural prebiotics enhance digestive health. These characteristics appeal to parents seeking alternatives for infants with digestive sensitivities. The European Food Safety Authority (EFSA) has validated goat milk protein as a suitable protein source for infant formula, providing regulatory validation for this market segment. The goat milk-based organic formula market demonstrates significant growth in Western Europe, particularly in France, Germany, and the Netherlands. Consumers in these markets show readiness to pay premium prices for improved digestive benefits. This market evolution creates opportunities for specialized manufacturers to establish themselves alongside traditional cow's milk formula producers, indicating a shift in the European organic baby food market.

Strategic Investment by Players

Major companies in the Europe organic baby food market are making strategic investments to expand product lines, drive innovation, and improve distribution capabilities. Companies like Nestlé, Danone, HiPP, Holle, Hero Group, and Abbott Laboratories are investing in research and development to develop organic baby food products that meet consumer demand for clean-label, allergen-free, and nutritionally enhanced options. These investments support the development of formulas with ingredients that better match breast milk's nutritional composition, addressing parents' focus on infant health and development. Danone is implementing its "Renew Danone" strategic plan, which emphasizes portfolio optimization and growth in segments including organic baby food. Companies are also investing in sustainable packaging initiatives, with Arla Foods moving toward 100% recyclable materials and HiPP working to reduce plastic usage. These environmental commitments align with both regulations and consumer preferences, helping companies maintain market position and customer loyalty.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatility in Organic Raw Material Prices after Ukraine Conflict | -1.50% | Pan-European, with higher impact in Eastern Europe | Medium term (2-4 years) |

| Limited Shelf-life Challenges for Fresh/Frozen Organic Baby Food Logistics | -1.10% | Northern and Eastern European markets with less developed cold chain infrastructure | Short term (≤ 2 years) |

| Regulatory Cap on Sugar Content Restricting Formulation Flexibility | -0.80% | EU member states, particularly impacting products for 12+ months age segments | Medium term (2-4 years) |

| Premium Pricing Limiting Mass Market Penetration | -0.70% | Pan-European, with higher impact in Southern and Eastern European markets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatility in Organic Raw Material Prices after Ukraine Conflict

The Europe organic baby food market faces significant constraints due to volatile organic raw material prices, intensified by the Ukraine conflict. Ukraine, a major exporter of agricultural commodities like grains and sunflower oil, plays a crucial role in supplying essential ingredients for organic baby food production. The disruption in Ukraine's agricultural operations, distribution networks, and trade routes has created persistent supply chain bottlenecks and shortages across Europe. The termination of the Black Sea Grain Initiative in July 2023 amplified these challenges, as alternative trade routes increased shipping and warehousing costs, which manufacturers transferred to consumers [2]World Economic Forum, "What does the future of food security look like after the collapse of the Black Sea grain deal?", www.weforum.org. The combination of supply instability, rising input costs, and inflation has reduced profit margins for organic baby food producers, affecting their ability to maintain stable pricing and consistent supply.

Regulatory Cap on Sugar Content Restricting Formulation Flexibility

The European Union's regulatory limits on sugar content in infant and follow-on formula have emerged as a significant constraint in the organic baby food market. EU regulations, specifically Regulation (EU) No 609/2013 and its supplementing acts, establish strict compositional requirements for infant nutrition products, including specific restrictions on carbohydrate and sugar content. While these regulations aim to protect infant health by reducing early sugar exposure and its associated risks of obesity and metabolic disorders, they restrict manufacturers' options in using natural sweeteners and fruit-based ingredients that could enhance product taste and nutritional value. The implementation of the Codex Alimentarius standard for follow-up formula and young children's products, with its more stringent sugar content criteria, is likely to further constrain product development, resulting in more standardized offerings across the market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Milk Formula Dominates Despite Diversification

Milk formula holds a dominant 46.68% share in for 2025 in Europe organic baby food market, serving as the primary alternative to breastfeeding. This position is strengthened by continuous innovation in organic formulations and strict EU regulations, specifically Delegated Regulation (EU) 2016/127, which enforces high safety and nutritional standards. European organic milk formulas adhere to stringent guidelines on sugar content, with regulations mandating lactose as the main carbohydrate source and restricting certain sugars common in non-European formulas.

Dried baby food is expected to grow at a CAGR of 11.45% from 2026-2031. This growth is attributed to its convenience, long shelf life, and ability to maintain nutritional value without artificial preservatives. The segment benefits from improved freeze-drying and air-drying technologies that preserve nutrients more effectively than traditional heat processing. While prepared baby food maintains a substantial market presence, it faces challenges in shelf-life and cold chain requirements, particularly for organic products. However, high-pressure processing (HPP) technology is helping overcome these limitations by extending product life while maintaining nutritional and sensory qualities.

By Age Group: Weaning Period Drives Market Dynamics

The 6-12 months age segment holds 38.08% of the Europe organic baby food market share in 2025, as this period marks the essential transition from exclusive milk feeding to solid foods. During this complementary feeding phase, parents prioritize nutritional quality and variety, creating opportunities for organic baby food products.

The 18-24 month segment is expected to grow at a CAGR of 10.18% from 2026 to 2031, making it the fastest-growing category. This growth stems from parents' increased awareness of how this period influences children's long-term eating habits and nutritional development. Manufacturers are developing products with diverse flavors and textures while maintaining organic standards.

The 0-6 months segment primarily consists of organic milk formula. The 12-18 months and over 24 months segments offer a wider range of products, including finger foods and toddler meals. Manufacturers face the challenge of meeting age-specific nutritional requirements across all segments, particularly following the European Parliament's restriction on early-age labeling for baby foods. This regulation requires careful product positioning within developmental stages.

By Distribution Channel: Online Retail Disrupts Traditional Dominance

Supermarkets/hypermarkets hold 51.27% market share in 2025 as the main distribution channel, benefiting from their wide physical presence and convenience for parents seeking one-stop shopping. The prominence of traditional supermarkets in organic sales aligns with broader European patterns. According to IFOAM Organics Europe, the organic retail market grew by 3% in 2023 compared to 2022, reaching EUR 46.5 billion. These retailers are increasing their organic baby food sections and introducing premium private label products to meet the rising demand for cost-effective organic options. Specialty stores, including organic and baby boutiques, remain important market players by providing selected products and individualized customer service, particularly for first-time parents seeking advice on organic feeding choices.

Online retail channels show significant expansion with an expected CAGR of 8.21% from 2026-2031, changing traditional distribution through improved convenience, broader product range, and direct consumer interaction. E-commerce platforms allow smaller organic brands to reach consumers without competing for physical retail space, improving market access and product development speed. Pharmacies and drugstores maintain their importance, especially for specialized organic formulas, while convenience stores provide select organic baby food options. The distribution landscape now features overlapping channels and integrated retail strategies, as companies work to deliver consistent shopping experiences across physical and digital platforms.

Geography Analysis

Germany holds 21.92% market share in 2025, supported by its established organic food ecosystem and retail infrastructure. The market volume of organic food in 2023 amounts to EUR 16.08 billion and includes sales in food retail, natural food retail, and other shopping outlets, which include drugstores, health food shops, etc . German parents show strong concerns about conventional infant food nutrition, preferring organic products with clear sourcing and processing information. The market offers organic baby food through multiple retail channels, from discount supermarkets to specialized organic stores, making Germany the region's largest and most developed market.

The Netherlands demonstrates the highest growth potential with a projected CAGR of 13.52% from 2026 to 2031. This growth stems from urbanization, higher disposable incomes, and government support for organic agriculture. The USDA Foreign Agricultural Service reports that the Dutch government has set a target to expand organic farmland to 15% by 2030, supporting organic baby food production.

Eastern European markets, including Poland and Russia, show growth potential as organic awareness increases and retail infrastructure improves. Nordic countries, particularly Sweden and Denmark, demonstrate high organic product adoption due to environmental awareness, with Danish consumers maintaining organic preferences despite inflation. According to the Research Institute of Organic Agriculture (FiBL), Europe maintained 19.5 million hectares of organic agricultural land in 2023 . Southern European markets display varied adoption rates, with Italy showing a stronger organic market presence. The European market exhibits distinct variations in organic market development, regulatory compliance, and consumer preferences, requiring manufacturers to develop region-specific approaches while complying with European Union regulations.

Competitive Landscape

The European Organic Baby Food Market shows moderate concentration, with multinational companies holding significant market share through their extensive distribution networks and brand equity. Key players, including Danone S.A., Nestlé S.A., HiPP GmbH & Co. Vertrieb KG, Holle baby food AG, and Hero Group, maintain their market positions through global scale and specialized nutrition expertise.

Companies are increasing investments in supply chain transparency and ingredient traceability as competitive advantages. They implement strict testing protocols for contaminants to address parental safety concerns. Market opportunities exist in developing organic products for specific dietary requirements, including allergen-free formulations and functional ingredients. For instance, in October 2023, Little Freddie, an organic baby food brand, unveiled two dairy-free yoghurt-style pouches: Banana & Raspberry and Strawberry. Packaged in recyclable pouches, Little Freddie asserts these products cater to parents with children allergic to cow's milk protein and those opting for plant-based weaning.

New competitors include direct-to-consumer brands using e-commerce platforms and companies implementing high-pressure processing (HPP) technology to enhance product shelf life while maintaining nutritional value. The European Union's Regulation 2018/848 on organic production and labeling creates substantial compliance requirements, benefiting established companies with regulatory expertise while creating entry barriers for new market participants.

Europe Organic Baby Food Industry Leaders

-

Danone S.A.

-

Nestlé S.A.

-

HiPP GmbH & Co. Vertrieb KG

-

Hero Group

-

Abbott Laboratories

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: "OH BABY," a new infant formula brand, launched in major supermarkets across the United Kingdom. The brand targets parents seeking affordable, high-quality infant formula products.

- September 2024: Happy Family Organics launched its Happy Baby Infant Formula line, which features USDA and EU organic certifications. The formula, manufactured in Europe, incorporates a patented blend of probiotics and prebiotics.

- August 2024: Abbott Laboratories expanded its Pure Bliss by Similac product line, offering organic and European-made infant formulas to meet diverse consumer preferences.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study treats the Europe organic baby food market as all commercially packaged foods and milk formulas whose every ingredient meets EU-certified organic standards and is intended for infants and toddlers up to 24 months. Value is tracked in USD at manufacturer selling price before retail margins.

Scope exclusion: Products marketed for children above two years, specialty dietary supplements, and any conventional or partially organic baby foods are left out.

Segmentation Overview

-

By Product Type

- Milk Formula

- Prepared Baby Food

- Dried Baby Food

-

By Age Group

- 0-6 Months

- 6-12 Months

- 12-18 Months

- 18-24 Months

- More than 24 months

-

By Distribution Channel

- Supermarkets /Hypermarkets

- Convenience Stores

- Specialty Stores

- Pharmacies & Drugstores

- Online Retail Channels

- Other Distribution Channels

-

By Country

- United Kingdom

- Germany

- France

- Spain

- Italy

- Netherlands

- Sweden

- Denmark

- Poland

- Rest of Europe

Detailed Research Methodology and Data Validation

Primary Research

Interviews with pediatricians, organic farmers' cooperatives, dairy processors, and e-commerce buyers across Germany, France, Spain, the U.K., and Poland supplied real-world conversion ratios, average shelf-life losses, and likely channel mix shifts that desk sources could not quantify fully.

Desk Research

Mordor analysts began with public-domain datasets from Eurostat live birth files, FAO organic farmland statistics, national food safety agencies, and trade flows recorded by COMEXT. Industry insights came from bodies such as IFOAM-EU and retailers' scanner disclosures, supported by company 10-Ks and recent prospectuses. Paid intelligence from D&B Hoovers and Dow Jones Factiva helped size leading vendors and spot price swings in organic dairy inputs. Numerous additional secondary references were consulted; the list above is illustrative, not exhaustive.

Market-Sizing & Forecasting

A top-down reconstruction starts with live births and average daily calorie need, then applies organic adoption rates, wastage factors, and average selling prices to reach 2024 demand. Select bottom-up checks, supplier revenue roll-ups and sampled SKU price × volume pulls, calibrate totals. Key variables shaping the model include organic share of total baby food shelf space, per-capita spend on organic foods, goat-milk formula penetration, inflation in organic raw milk prices, e-commerce share of baby food sales, and EU farmland conversion targets. Five-year forecasts rely on multivariate regression blended with scenario analysis, and trend coefficients are cross-verified with our primary panel before lock-in. Gaps in granular country data are bridged using Nearby-Country analogs adjusted for income and fertility differences.

Data Validation & Update Cycle

Outputs pass variance checks against independent retail audit snapshots, and anomalies trigger a second analyst review. The model refreshes annually, with interim tweaks when policy or commodity shocks materially move any core driver.

Why Mordor's Europe Organic Baby Food Baseline Commands Reliability

Published estimates often differ because firms stretch or shrink product scope, assume varying price ladders, or refresh at different cadences.

Key gap drivers here include: some studies merge conventional and organic lines, others price at consumer checkout rather than ex-factory, and a few project on fertility scenarios frozen before recent inflation. Mordor's disciplined scope, dual-path model, and yearly update avoid those pitfalls.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.04 B (2025) | Mordor Intelligence | - |

| USD 1.15 B (2024) | Regional Consultancy A | uses broader age band to 36 months and partial retail pricing |

| USD 18.77 B (2025) | Global Consultancy B | covers all baby food, mixes organic and conventional, top-line only |

| USD 9.75 B (2023) | Industry Association C | combines infant formula with baby meals and applies three-year-old exchange rates |

In sum, buyers gain a transparent, replicable baseline from Mordor Intelligence that ties every dollar to clear variables and can be rerun as soon as fresh data emerges.

Key Questions Answered in the Report

What is the current value of the European organic baby food market?

The market is valued at USD 1.13 billion in 2026 and is on track to reach USD 1.73 billion by 2031.

Which segment dominates within the European organic baby food market?

Milk formula holds the lead, accounting for 46.68% of revenue in 2025, owing to its pivotal role during the 0–6 months feeding stage.

Why is goat-milk formula gaining share?

Goat milk’s smaller proteins improve digestibility, and EFSA has validated its suitability for infant nutrition, prompting Western European parents to pay premiums for the alternative.

How important is e-commerce to future growth?

Online retail is projected to expand at a 8.21% CAGR, giving small brands direct consumer access and enabling established players to offer subscription services.

Page last updated on: