Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 47.21 Billion |

| Market Size (2026) | USD 50.19 Billion |

| Market Size (2031) | USD 68.19 Billion |

| Growth Rate (2026 - 2031) | 6.32% CAGR |

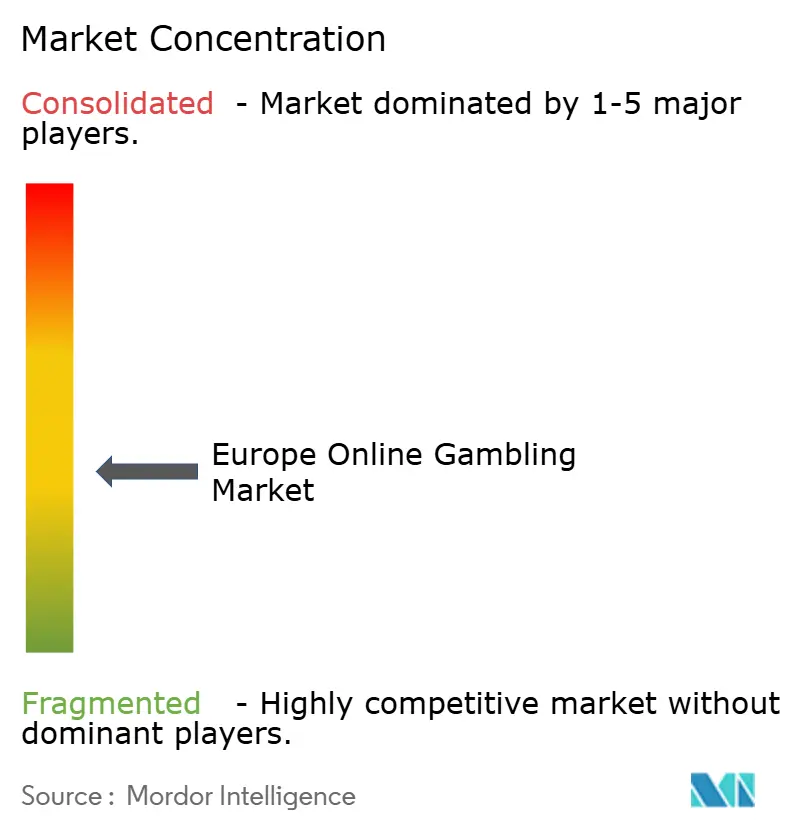

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Online Gambling Market Analysis by Mordor Intelligence

The Europe online gambling market size is expected to grow from USD 47.21 billion in 2025 to USD 50.19 billion in 2026 and is forecast to reach USD 68.19 billion by 2031 at 6.32% CAGR over 2026-2031. Smartphones dominate the market due to their convenience and widespread use. Casino game innovations are closing the gap with other popular categories. Younger, tech-savvy individuals are driving market demand through their preference for digital platforms. Artificial intelligence enhances user experiences with personalized recommendations and improved responsible gambling measures. Sports betting remains the most popular segment, supported by major tournaments and in-play wagering. Regulatory changes, such as Italy's reforms and anticipated gambling law liberalization in France, create opportunities for operators adapting to diverse compliance needs. The European online gambling market is moderately competitive, with the top ten operators accounting for less than half of the total revenue, leaving room for smaller players to grow.

Key Report Takeaways

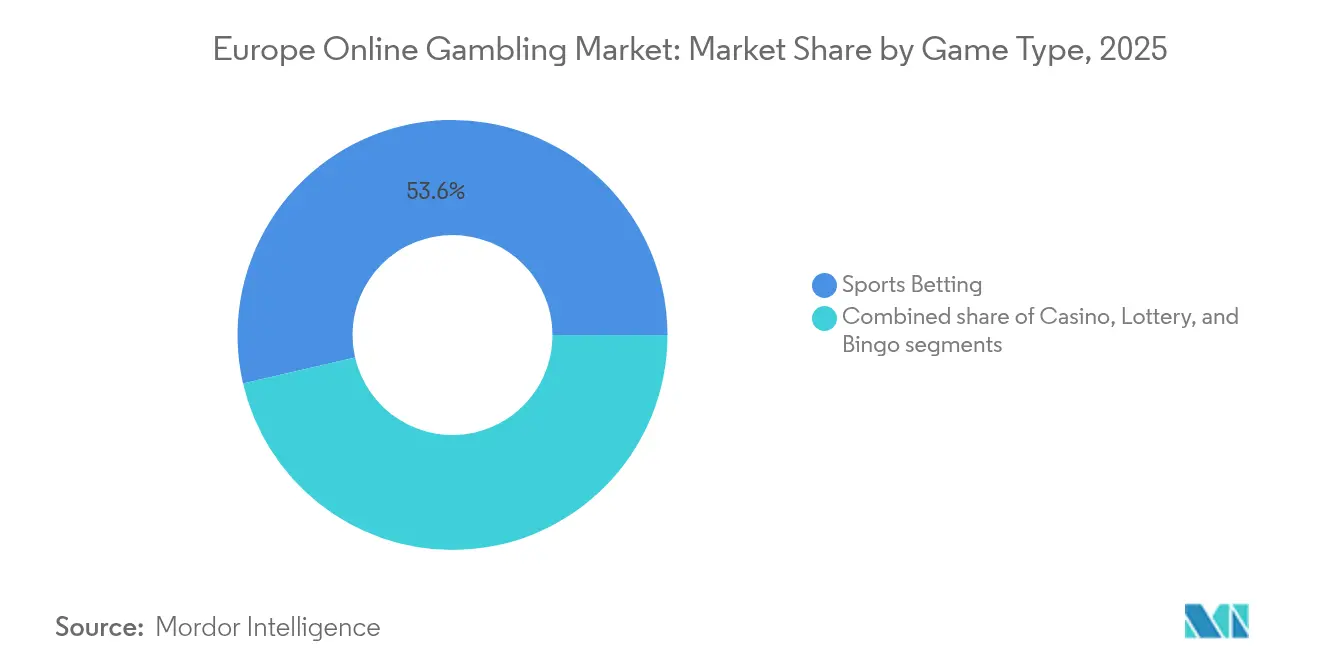

- By game type, sports betting led with 53.62% revenue share in 2025, while casino games are forecast to expand at an 7.78% CAGR to 2031.

- By device, mobile accounted for 58.74% of the Europe online gambling market share in 2025 and is growing at a CAGR of 8.18%,

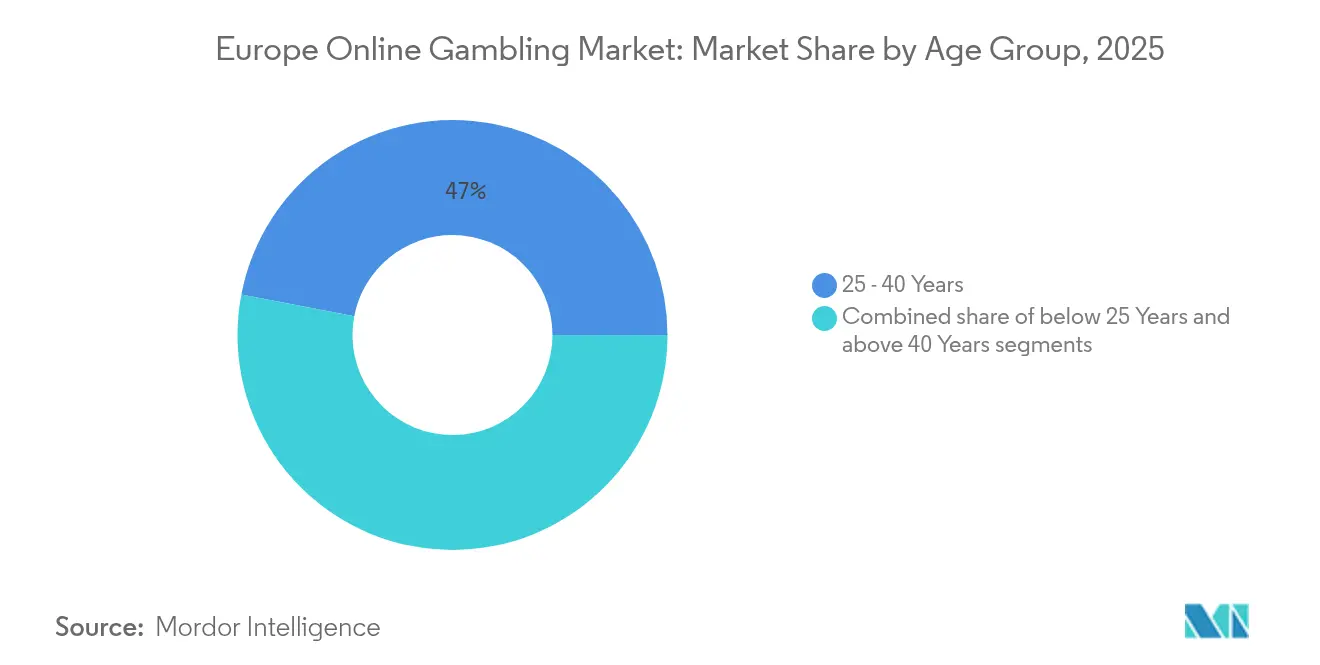

- By age group, the 25-40 cohort held 46.98% share of the Europe online gambling market size in 2025, whereas the below-25 segment is set to grow at 8.06% CAGR through 2031.

- By gender, male players dominated with a 66.35% share in 2025; female participation is advancing at an 7.92% CAGR, particularly via mobile channels.

- By geography, the United Kingdom led with a 24.78% share in 2025, while Italy is forecast to post the fastest 7.41% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Online Gambling Market Trends and Insights

Drivers Impact Table*

| DRIVER | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| 5G and smartphones fuel the market | +1.2% | United Kingdom, Germany, Nordic markets | Medium term (2-4 years) |

| Increased consumer demand for interactive and mobile-friendly experiences | +1.8% | Southern Europe and other emerging markets | Short term (≤ 2 years) |

| Integration of artificial intelligence and virtual reality enhances the overall user experience | +0.9% | United Kingdom, Germany, Netherlands, Sweden | Long term (≥ 4 years) |

| National and regional tournaments boost betting activity by increasing opportunities and consumer engagement | +1.1% | Pan-European, with spikes during major sporting events | Short term (≤ 2 years) |

| Availability of diverse gaming options helps attract a broader consumer base | +0.8% | Mature, well-regulated European markets | Medium term (2-4 years) |

| Strategic marketing initiatives and sponsorship programs increase gambling brand visibility | +0.6% | United Kingdom, Spain, Italy, Germany, France | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

5G and smartphones fuel the market

Europe's online gambling market is growing rapidly, driven by smartphone adoption and 5G networks. In 2024, 94% of European households had internet access, according to the European Union [1]Source: European Union, "Digital economy and society statistics - households and individuals," ec.europa.eu. Operators like Bet365, LeoVegas, and Unibet are focusing on mobile-friendly platforms to attract users. Progressive web apps (PWAs) are gaining popularity, allowing users to access gambling sites via browsers, bypassing app-store restrictions. The rollout of 5G has enhanced mobile gaming with better live streaming, faster response times, and real-time interactions. By the end of 2024, 5G adoption in Europe grew by 87%, as per Connect Europe [2]Source: Connect Europe, "State of Digital Communications 2025," connecteurope.org. Platforms like Bwin have leveraged this to introduce live leaderboards, multiplayer betting rooms, and chat integrations, appealing to younger, experience-focused users. These advancements enable features like voice-activated betting and interactive chat rooms, making the experience more engaging.

Technological advancements and immersive gaming enhance user experience

Europe's online gambling market is growing rapidly, driven by technological advancements and a rising gamer base. Companies like Entain and Flutter Entertainment use AI to customize odds, promotions, and risk alerts, boosting engagement and ensuring responsible gambling. Virtual reality (VR) is reshaping the market with live-casino experiences that mimic physical casinos, appealing to tech-savvy younger users. Blockchain ensures transparent transactions, building trust in regions with strict regulations. Cloud-based systems enable operators to expand across countries and support cross-border liquidity pooling for pan-European operations. Millennials and Gen Z are increasingly drawn to features like missions, leaderboards, and social interactions, aligning with their gaming habits.

National and regional tournaments boost betting activity

Sports tournaments, both national and regional, drive growth in Europe’s online gambling market by increasing betting activity and user engagement. Events like the UEFA Champions League and EuroLeague see spikes in betting, especially when operators like bet365 offer features such as special odds, live betting, and streaming. Operators are also targeting smaller, fast-growing sports, as seen with Betsson’s sponsorship of the International Padel Federation tour. In 2024, Europe welcomed 747 million international arrivals, according to UN Tourism, with many visitors participating in betting during major tournaments [3]Source: UN Tourism, "International tourism recovers pre-pandemic levels in 2024," unwto.org. These collaborations help operators connect with fans, making sports-related engagement a key strategy in a competitive market.

Integration of artificial intelligence and virtual reality enhances overall user experience

AI-driven personalization and immersive technologies like virtual reality (VR) are transforming online gambling in Europe, making it more engaging and user-focused. Operators such as Entain and Kindred Group use machine-learning tools to offer tailored content, recommend bets, and identify risky gambling behaviors to promote safer practices. Platforms like PokerStars VR and Evolution Gaming are introducing VR casino lounges and holographic dealers, creating interactive and immersive experiences that appeal to younger, tech-savvy audiences. However, stricter regulations are emerging alongside these advancements. The EU AI Act, expected by 2026, will require operators to ensure algorithm transparency, detect biases, and undergo independent audits to protect consumers.

Restraints Impact Analysis*

| RESTRAINT | (~) % IMPACT ON CAGR FORECAST | GEOGRAPHIC RELEVANCE | IMPACT TIMELINE |

|---|---|---|---|

| Consumer protection and responsible gambling concerns | -1.4% | United Kingdom, Germany, Netherlands leading regulatory scrutiny | Medium term (2-4 years) |

| High taxation reduces operator profitability | -0.9% | Germany (5.3% stake tax), Sweden (22% GGR tax), France (proposed increases) | Short term (≤ 2 years) |

| Growing concerns over gambling addiction lead to tighter controls | -1.1% | Nordic countries, United Kingdom, Netherlands with strictest measures | Long term (≥ 4 years) |

| Competition from unregulated and black market operators | -0.7% | Eastern Europe, markets with restrictive licensing | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High taxation reduces operator profitability

Europe's online gambling market grapples with high taxation on stakes and gross gaming revenue (GGR), a challenge that weighs heavily on smaller and mid-sized operators. Take Germany, for instance: a 5.3% tax on stakes has drawn criticism for dampening the competitiveness of odds, particularly affecting the allure of online slots and poker. Over in Sweden, a hefty 22% GGR tax is squeezing operators' profit margins, pushing some to scale back marketing or exit the scene altogether. France's tax reforms loom large, with projections indicating a EUR 45 million hit to FDJ’s earnings in 2025, underscoring the tangible impact of tax policies, even on industry giants. Italy's licensing landscape poses its own hurdles: a EUR 7 million fee for a nine-year license, coupled with other revenue-based taxes, sets a daunting barrier for newcomers [4]Source: European Betting and Gaming Association, "EGBA Expresses Concern Over New Italian Decree Reorganising Online Gambling License Fees," egba.eu. Such challenges often leave smaller operators gasping for breath, paving the way for market consolidation as larger entities either absorb them or push them out.

Consumer protection and responsible gambling concerns

Operators in Europe’s online gambling market face challenges due to stricter consumer protection and responsible gambling regulations. Many countries now mandate measures like affordability checks, deposit limits, and self-exclusion tools. For instance, 27 countries require players to set gambling limits during registration. In the UK, proposed reforms aim to tighten controls on high-spending players, targeting VIP programs and financial risk assessments, which could significantly reduce revenues from high-value customers. To comply while maintaining a smooth user experience, operators are investing in advanced compliance systems. However, failure to balance these requirements may push players to unregulated platforms, risking player safety and reducing regulated operators' market share. Balancing compliance and customer satisfaction is now critical for sustainable growth in the sector.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Game Type: Casino innovation narrows the gap

Sports betting continues to dominate as the largest revenue contributor in 2025, with a share of 53.62%, but casino games like roulette, blackjack, and baccarat are rapidly gaining popularity. These games, streamed from professional studios in locations such as Riga and Malta, offer an immersive experience that attracts more players. Casino operators are increasingly collaborating with content studios to create branded tables, while cross-border jackpots significantly boost prize pools, making these games even more appealing. The market for casino games in Europe is expected to grow steadily, with the live-casino segment alone projected to achieve a robust CAGR of 7.78% during the forecast period.

Slot games remain a favorite among players due to their engaging graphics and the allure of multi-currency progressive jackpots. Meanwhile, virtual poker rooms are focusing on building loyal communities by offering shared liquidity pools across countries like Spain, France, and Portugal, enhancing the gaming experience. The digitalization of lotteries is gaining momentum, helping state governments generate revenue while competing with private platforms that provide innovative features like syndicate play. Innovations such as syndicate play, instant draws, and app-based ticketing are helping lotteries stay relevant while driving revenue for governments. These trends highlight the evolving preferences of players and the efforts of operators to adapt to changing market dynamics.

By Device: Smartphone leadership deepens

In 2025, mobile devices contributed to 58.74% of the revenue in the online gambling market and are growing at the fastest rate, with a CAGR of 8.18%. Features like one-hand gameplay, integrated in-app wallets, and biometric login have made mobile gaming more user-friendly and accessible. While desktop platforms still attract high-volume players who prefer advanced tools like multi-screen options and detailed analytics, their market share is gradually shrinking. Operators are also experimenting with new platforms, such as smart TVs and gaming consoles, to reach a broader audience. Virtual reality (VR) headsets are beginning to offer immersive casino experiences, but this technology is still in its early stages and appeals to a smaller group of users.

Cross-platform cloud profiles are becoming increasingly popular, allowing players to switch between devices without losing their progress, which enhances the overall gaming experience. This seamless transition across devices is helping operators build stronger customer loyalty. As mobile gaming continues to dominate, marketing strategies are shifting to focus more on app-store optimization and partnerships with influencers, especially through short-form video content. Combined, these innovations in technology and marketing are positioning mobile devices as the central hub for online gambling, reshaping how operators attract, engage, and retain their player base.

By Age Group: Digital natives reshape demand

Players aged 25-40 currently account for the largest share of revenue at 46.98%, as they typically have stable incomes and a good understanding of sports betting. This group is a primary target for operators because they frequently engage with traditional betting options and show consistent spending patterns. Meanwhile, the under-25 age group is growing rapidly, with a CAGR of 8.06%. Younger players are particularly drawn to modern trends like esports, micro-betting, and interactive challenges that are often integrated with social media platforms. To attract this audience, operators are focusing on creating user-friendly onboarding processes and providing educational tools to help them understand the games and betting systems better. These efforts aim to make the betting experience more accessible and appealing to younger users.

To maintain the interest of younger players, operators are also introducing features like gamified loyalty programs, reward systems similar to loot boxes, and live-streamed content featuring popular influencers. These additions cater to tech-savvy players who value interactive and community-driven experiences. However, this age group is more vulnerable to gambling-related risks, prompting regulators to take action. Authorities are implementing early intervention systems and launching awareness campaigns in schools to educate young players about responsible gambling practices. These measures aim to ensure the market continues to grow while prioritizing the safety and well-being of players, especially those at higher risk.

By Gender: Inclusion widens participation

Male bettors currently dominate the Europe online gambling market, accounting for 66.35% of the total share. However, the participation of female users is growing rapidly, with a compound annual growth rate (CAGR) of 7.92%. To attract more women, companies are focusing on improving platform designs by adding features like social interaction tools, quick-bet options, and markets that align with lifestyle interests, such as entertainment and reality TV betting. These changes aim to make online gambling platforms more inclusive and appealing to female users. As platforms continue to enhance their user experience and diversify their offerings, the share of women in the market is expected to increase significantly in the coming years.

Studies using eye-tracking technology have shown that men and women navigate gambling platforms differently, prompting companies to test and refine design elements such as color schemes and the way information is displayed. These adjustments are helping to create interfaces that cater to the preferences of both genders. Responsible gambling tools are being updated with gender-specific messaging, as research indicates that men and women have different triggers for risky behaviors like chasing losses. By addressing these behavioral differences, operators aim to promote safer gambling practices while expanding their reach to a broader audience. This approach not only supports responsible gambling but also ensures balanced growth in the market.

Geography Analysis

The United Kingdom contributed 24.78% of the revenue in 2025, supported by its strong licensing system, effective consumer protection policies, and a long-standing passion for sports. The market is appealing to gambling operators due to the availability of white-label solutions and advanced payment systems, which make operations smoother and more efficient. However, new affordability checks could reduce spending by high-value players, potentially affecting overall revenues. Companies that adopt advanced compliance technologies are better equipped to handle these changes and maintain their competitive position in this well-regulated market.

Italy is currently the fastest-growing market in Europe, with an expected growth rate of 7.41% CAGR. This growth is driven by the upcoming license renewal process in 2025-2026 and the potential easing of the Dignity Decree advertising ban, which could allow operators to reach a wider audience. The high entry fee of EUR 7 million for a nine-year license favors larger, well-funded operators, giving them an advantage in this expanding market. Additionally, improved channelization is expected to boost tax revenues, making Italy an attractive destination for established gambling companies looking to grow their presence in Europe. These factors position Italy as a key market for future growth in the online gambling industry.

Germany’s regulated market has issued 30 sports-betting, 39 slot, and 5 poker permits as of late 2024, but the 5.3% stake tax has created challenges by limiting operators’ marketing budgets. Despite this, some companies have managed to improve their performance by using pooled liquidity across different states, which helps optimize their operations. Meanwhile, France is exploring the legalization of online casinos, which could create significant opportunities for the European online gambling market if concerns from stakeholders are resolved. Other regions, such as the Nordic countries, are focusing on strict harm-prevention measures to ensure responsible gambling. At the same time, Spain, the Netherlands, and Belgium continue to grow steadily under clear rules for sponsorships and bonuses.

Competitive Landscape

The competition in the European online gambling market is moderately fragmented, where no single player dominates. To scale operations and meet cross-border compliance requirements, companies are pursuing mergers and acquisitions. For instance, FDJ acquired Kindred, while Allwyn secured a majority stake in Novibet. Similarly, Superbet expanded its presence in the Benelux region by acquiring Napoleon Sports & Casino for EUR 350-400 million. These consolidations are helping operators strengthen their market positions and streamline operations across multiple regions.

Technology is playing a crucial role in shaping the competitive landscape of the market. Leading companies like Flutter are leveraging advanced tools such as single-wallet systems and real-time risk engines to enhance their offerings and ensure quick rollouts of new features. Entain, on the other hand, is heavily investing in artificial intelligence to provide personalized betting odds and improve customer engagement. Meanwhile, newer players like BC.GAME, which focuses on cryptocurrency payments, and ComeOn, an esports specialist, are targeting younger audiences who prefer innovative payment methods and integrated gaming experiences. These technological advancements are helping operators cater to diverse customer preferences and stay ahead in the market.

Partnerships with sports teams are proving to be a valuable marketing strategy for gambling operators. Deals such as front-of-jersey sponsorships in leagues like the Premier League, Serie A, and La Liga provide significant brand visibility. For example, Juventus’ sleeve sponsorship with WhiteBIT highlights the growing collaboration between cryptocurrency platforms and mainstream sports clubs. Operators that combine data from both retail kiosks and online platforms gain a comprehensive understanding of customer spending habits. This omnichannel approach allows them to make better lifetime-value predictions and tailor their services to meet customer needs more effectively.

Europe Online Gambling Industry Leaders

-

Betsson AB

-

Entain PLC

-

Bet365 Group Ltd

-

Flutter Entertainment PLC

-

Evoke PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: AS Monaco and VBET have renewed their partnership agreement, which will now run until 2029. This extended collaboration strengthens their association within Ligue 1, allowing both parties to enhance their brand visibility and engage with a broader audience.

- January 2025: Astralis and ComeOn Group have announced a partnership focused on esports betting, set to begin in 2025. This collaboration aims to combine Astralis' expertise in esports with ComeOn Group's experience in online betting, offering fans an enhanced and engaging betting experience tailored to the growing esports market.

- January 2025: Superbet has acquired Napoleon Sports & Casino in a deal valued between EUR 350-400 million. This acquisition represents Superbet's largest international expansion to date, strengthening its presence in the European gaming market and enhancing its portfolio with Napoleon's established operations.

- October 2024: FDJ has completed its USD 2.8 billion acquisition of Kindred, creating a major gaming company with a strong presence across Europe. This merger is expected to enhance their market position and expand their offerings in the gaming and betting industry.

Europe Online Gambling Market Report Scope

Online gambling is a type of betting on sports like casinos, poker, and other sports that are played over the internet. Online gambling is becoming popular due to its multi-layer taxation environment. The market has been segmented by game type, end-user, and geography. The market studied is segmented by game type into sports betting, casino, lottery, and bingo. By sports betting, the market studied is segmented into football, horse racing, e-sports, and others. By casino, the market studied is segmented into live casinos, slots, baccarat, blackjack, and others. By the end use, the market studied is segmented into desktop and mobile. The report covers major countries of Europe, including the United Kingdom, Italy, France, Spain, Germany, Netherlands, Sweden, and Rest of Europe. For each segment, the market sizing and forecasts have been done on the basis of value in USD million.

By Game Type

| Sports Betting | Football |

| Horse Racing | |

| Tennis | |

| Other Game Types | |

| Casino | Live Casino |

| Baccarat | |

| Blackjack | |

| Poker | |

| Slots | |

| Other Casino Games | |

| Lottery | |

| Bingo |

By Device

| Desktop |

| Mobile |

| Others |

By Age Group

| Below 25 Years |

| 25 – 40 Years |

| Above 40 Years |

By Gender

| Male |

| Female |

By Geography

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| Sweden |

| Rest of Europe |

| By Game Type | Sports Betting | Football |

| Horse Racing | ||

| Tennis | ||

| Other Game Types | ||

| Casino | Live Casino | |

| Baccarat | ||

| Blackjack | ||

| Poker | ||

| Slots | ||

| Other Casino Games | ||

| Lottery | ||

| Bingo | ||

| By Device | Desktop | |

| Mobile | ||

| Others | ||

| By Age Group | Below 25 Years | |

| 25 – 40 Years | ||

| Above 40 Years | ||

| By Gender | Male | |

| Female | ||

| By Geography | United Kingdom | |

| Germany | ||

| France | ||

| Spain | ||

| Italy | ||

| Sweden | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the current size of the Europe online gambling market?

The market is valued at USD 50.19 billion in 2026 and is projected to reach USD 68.19 billion by 2031.

Which game type generates the most revenue?

Sports betting leads with 53.62% of 2025 revenue, while casino games show the fastest 7.78% CAGR growth.

How dominant is mobile gambling in Europe?

Mobile channels captured 58.74% of 2025 revenue and are forecast to account for more than 60% in upcoming years.

Which country is growing fastest?

Italy is poised for the highest growth at a 7.41% CAGR due to new licensing rules and potential advertising reforms.

Page last updated on: