Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

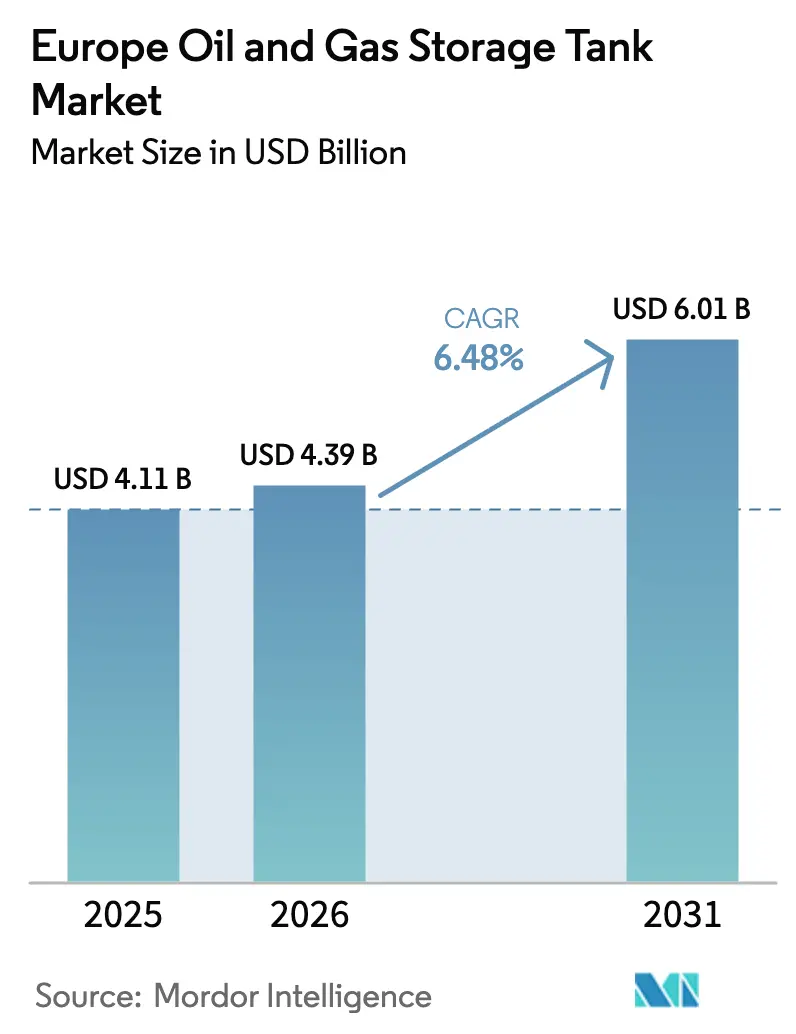

| Base Year Market Size (2025) | USD 4.11 Billion |

| Market Size (2026) | USD 4.39 Billion |

| Market Size (2031) | USD 6.01 Billion |

| Growth Rate (2026 - 2031) | 6.48% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Oil And Gas Storage Tank Market Analysis by Mordor Intelligence

The Europe Oil And Gas Storage Tank Market size is projected to be USD 4.11 billion in 2025, USD 4.39 billion in 2026, and reach USD 6.01 billion by 2031, growing at a CAGR of 6.48% from 2026 to 2031.

This growth reflects steady capital spending on multi-fuel tank farms that can accommodate liquefied natural gas (LNG), hydrogen, and advanced biofuels in addition to crude oil and refined products. Floating-roof replacements mandated by tighter volatile-organic-compound (VOC) limits, the commissioning of LNG import terminals in Germany and the Netherlands, and rising strategic-reserve targets across the European Union are the principal revenue drivers. Conversely, declining petroleum demand, stringent environmental compliance costs, and persistent community opposition extend payback horizons for newbuild projects. Competitive intensity remains moderate because the top five independent operators control about 40% of third-party storage capacity, leaving room for regional specialists that emphasize digital-twin maintenance and modular tank solutions.

Key Report Takeaways

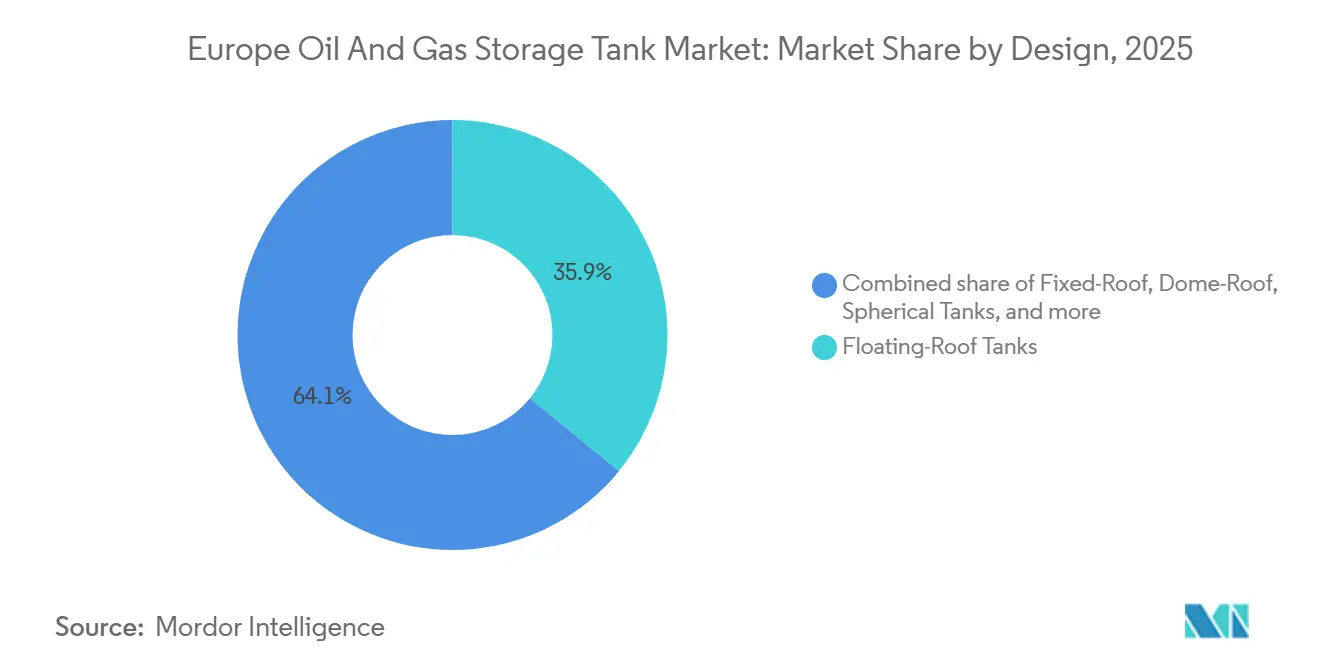

- By design, floating-roof tanks captured 35.9% revenue share in 2025; the segment is forecast to expand at a 7.5% CAGR through 2031.

- By tank type, above-ground vessels held 70.2% of Europe's oil & gas storage tank market share in 2025, while mobile and modular units are expected to post the fastest 8.9% CAGR to 2031.

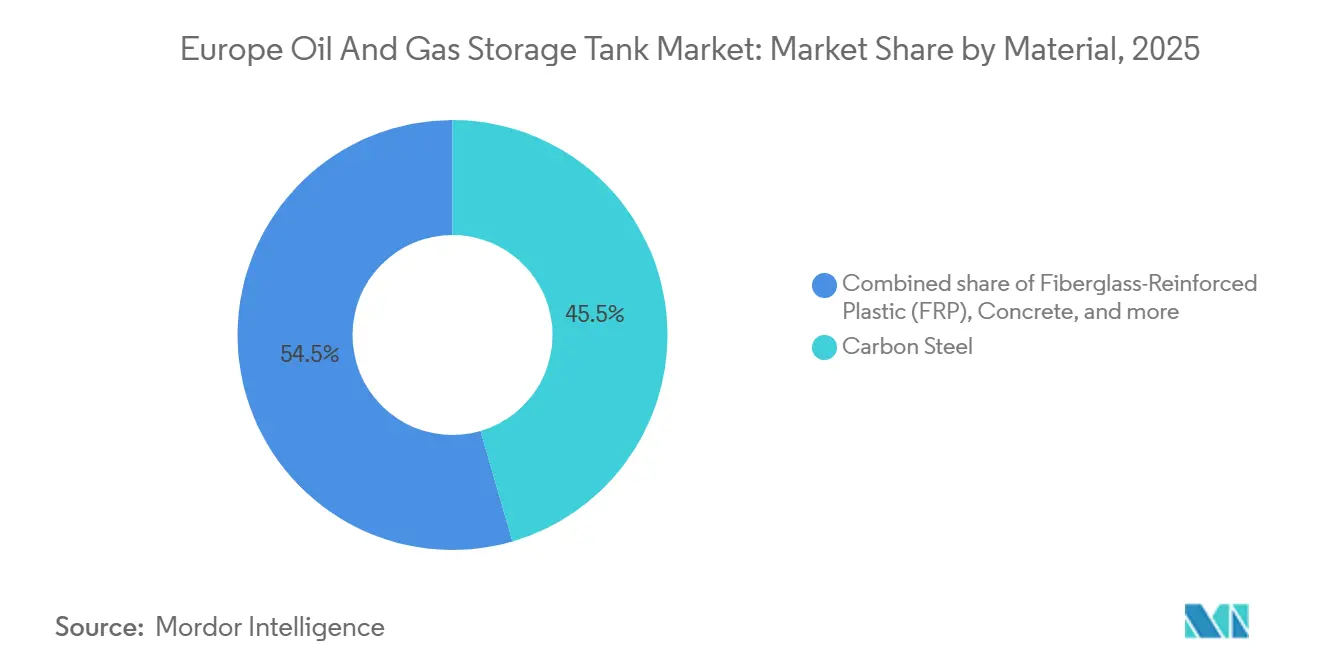

- By material, carbon steel accounted for 45.5% of Europe's oil & gas storage tank market size in 2025, whereas fiberglass-reinforced plastic (FRP) led growth at a 9.7% CAGR.

- By capacity range, the 50,000–150,000 m³ band commanded 32.7% revenue share in 2025 and is projected to rise at a 6.9% CAGR.

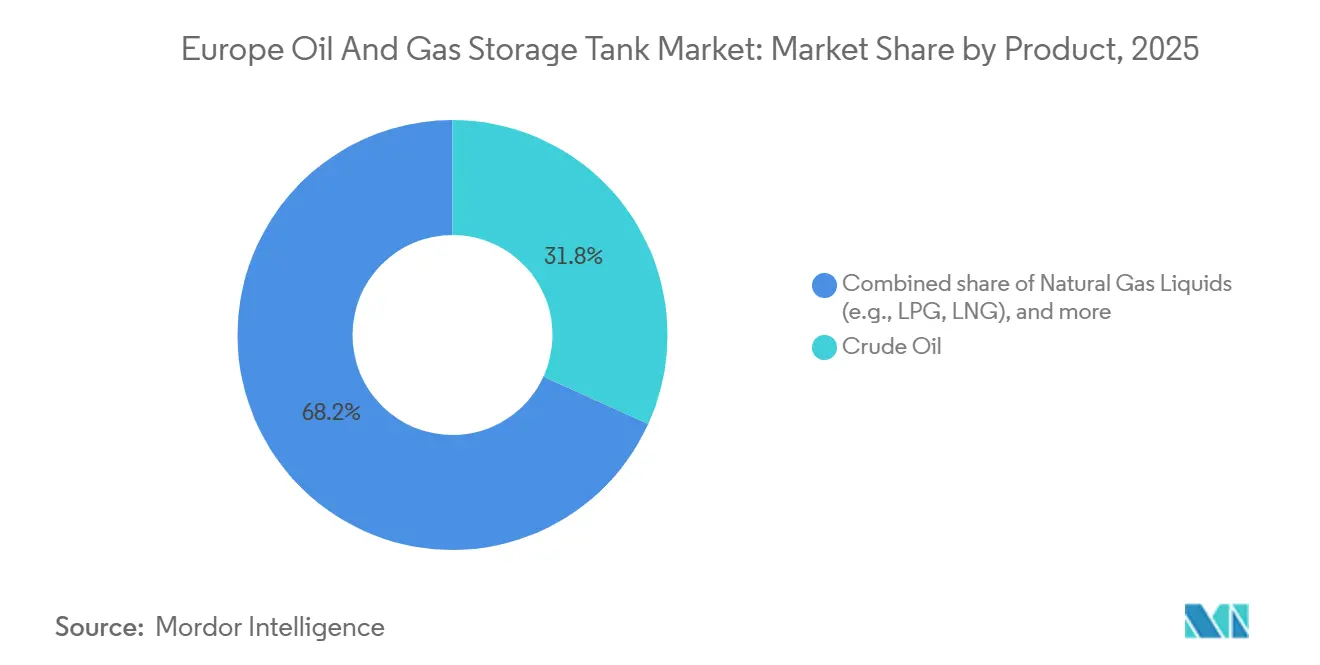

- By product, crude oil remained the largest category at 31.8% share in 2025; natural gas liquids, covering LPG and LNG, are poised for the highest 8.2% CAGR.

- By end user, refineries and petrochemical plants contributed 33.3% of demand in 2025 and are advancing at a 7.1% CAGR on the back of sustainable-aviation-fuel investments.

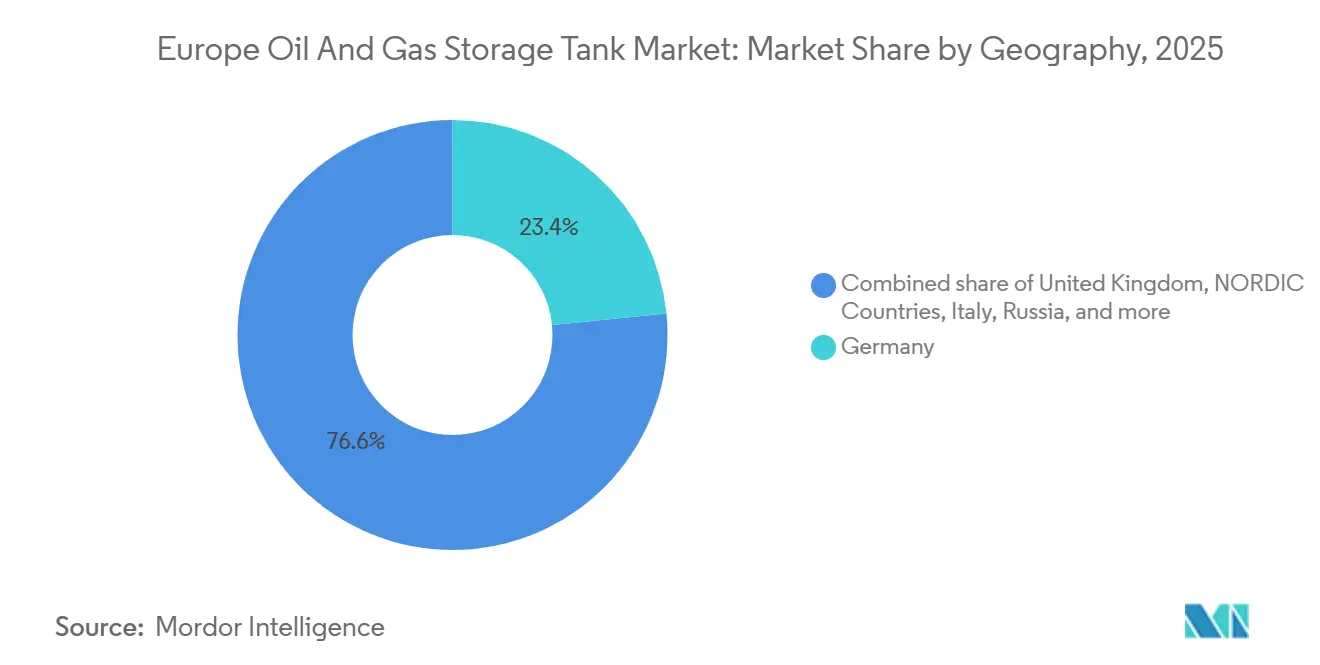

- By geography, Germany led with a 23.4% revenue share in 2025, whereas Russia is expected to record the fastest 7.6% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Oil And Gas Storage Tank Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising need for strategic petroleum reserves | +1.2% | Germany, France, Spain, Italy | Medium term (2–4 years) |

| Expansion of LNG import terminals & cryogenic tanks | +1.8% | Germany, Netherlands, Nordic Countries | Short term (≤2 years) |

| Aging storage infrastructure replacement demand | +1.0% | United Kingdom, France, Germany | Long term (≥4 years) |

| Growth in biofuels & hydrogen storage tanks | +0.9% | Nordic Countries, Germany, Netherlands | Medium term (2–4 years) |

| Repurposing decommissioned tanks for CCS storage | +0.5% | United Kingdom (North Sea), Norway, Netherlands | Long term (≥4 years) |

| Digital-twin-driven predictive maintenance retrofits | +0.7% | Global (concentrated in Germany, UK, Netherlands) | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Rising Need for Strategic Petroleum Reserves

European Union members collectively held 90 days of net import cover in December 2025, yet several governments now target 120 days by 2028.[1]European Commission, “Energy Security Report 2025,” ec.europa.eu Germany added 3.2 million m³ of new capacity in 2025, commissioning tanks in Wilhelmshaven and Lower Saxony that primarily fall in the 50,000–150,000 m³ sweet spot.[2]German Federal Office for Economic Affairs and Export Control, “Strategic Reserve Expansion 2025,” bafa.de Spain awarded EUR 180 million (USD 195 million) in above-ground tank contracts near Cartagena and Tarragona, specifying corrosion-resistant coatings that extend inspection intervals to 15 years. France’s SAGESS tendered for 1.8 million m³ during 2024, reinforcing consistent demand for large-diameter carbon-steel tanks even as gasoline consumption plateaus. The resulting offtake stabilizes fabrication pipelines for regional steel shops and lifts per-unit profitability despite muted refined-product throughput.

Expansion of LNG Import Terminals & Cryogenic Tanks

Germany commissioned four floating storage and regasification units (FSRUs) between 2023 and 2025, which together required 480,000 m³ of onshore minus-162 °C storage. In May 2025, the Gate terminal in Rotterdam finished a third 180,000 m³ tank built from 9-percent-nickel steel that meets EN 14620.[3]Gate Terminal, “Third LNG Tank Completion Press Release,” gateterminal.com Finland’s Inkoo facility added a 50,000 m³ bullet tank in September 2025, illustrating Nordic preference for modular, incremental capacity. Cryogenic construction costs of USD 1,200–1,800 per m³, roughly triple crude-oil equivalents, are nevertheless justified by the strategic imperative to displace Russian pipeline gas. This LNG surge underpins the 8.2% CAGR forecast for natural-gas-liquid tank demand.

Aging Storage Infrastructure Replacement Demand

Roughly 35% of Europe’s above-ground petroleum tanks predate 1985, and many exceed their 40-year design life, triggering mandatory API 653 fitness assessments. The United Kingdom’s Health and Safety Executive issued 127 improvement notices in 2024 related to floor corrosion, accelerating replacement at PetroIneos and Navigator sites. Royal Vopak launched a EUR 450 million program in 2025 to replace 22 tanks in Amsterdam, Rotterdam, and Antwerp, opting for duplex stainless steel and FRP where biofuels prevail. Modern floating-roof designs simultaneously expand capacity and cut VOC emissions, enabling compliance while limiting downtime.

Growth in Biofuels & Hydrogen Storage Tanks

The ReFuelEU Aviation regulation obliges 6% sustainable-aviation-fuel (SAF) blending by 2030, climbing to 70% by 2050. Neste installed a 25,000 m³ 316L-stainless-steel HEFA tank in March 2025 to accommodate the acidic renewable feedstock. Germany allocated EUR 1.2 billion to hydrogen refueling infrastructure in 2024, including four liquid-hydrogen depots with composite-overwrapped pressure vessels rated at 350 bar. Spanish refiners Repsol and Cepsa announced EUR 200 million each in 2025 for FRP biodiesel tanks to mitigate galvanic corrosion. FRP’s 9.7% CAGR mirrors this pivot toward corrosion-proof, lightweight vessels.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Declining petroleum demand in Europe | -1.1% | Western Europe (Germany, UK, France, Italy, Spain) | Long term (≥4 years) |

| Stringent environmental regulations & compliance costs | -0.8% | EU member states, Norway | Medium term (2–4 years) |

| Community opposition & permitting delays | -0.6% | Germany, Netherlands, Belgium (high-density corridors) | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Declining Petroleum Demand in Europe

Regional demand fell to 12.4 million b/d in 2025, shaving 2.1% year-on-year as electric-vehicle uptake hit 22% of new car registrations.[4]International Energy Agency, “Oil Market Report Dec 2025,” iea.org Germany’s gasoline and diesel consumption slipped 3.8% and 2.9%, respectively, depressing refinery utilization below 80%. Gunvor idled 400,000 m³ of middle-distillate capacity in Rotterdam early 2025, citing weak contango that no longer funds storage arbitrage. Unless crude tanks are repurposed, an estimated 1.2 million m³ will risk stranding in France by 2030.

Stringent Environmental Regulations & Compliance Cost

The 2024 update to the Industrial Emissions Directive halves allowable VOC emissions to 0.15 g/L and mandates optical-gas-imaging cameras. Upgrading a 100,000 m³ floating-roof tank costs EUR 1.2–1.8 million, and operators with multi-tank sites can face bills above EUR 20 million. Spain’s Catalonia region now mandates double-bottoms for tanks within 500 m of aquifers, adding 12–18% to capex. The Netherlands introduced a EUR 5/m³ decommissioning levy in 2024 to fund soil cleanup, further discouraging speculative builds.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Design: Floating-Roof Dominance Rises with Emission Rules

Floating-roof vessels accounted for 35.9% of Europe's oil & gas storage tank market revenue in 2025 and are on track for a 7.5% CAGR through 2031. The 2024 EEA directive compels internal or external floating roofs for liquids above 10 kPa Reid vapor pressure by December 2027, forcing the retrofit or replacement of roughly 1,800 fixed-roof tanks. Royal Vopak converted 14 tanks at Rotterdam in 2025, cutting VOC releases by 1,450 t/yr and avoiding ETS penalties. Fixed-roof vessels still serve low-volatility fuels, while dome-roof designs handle high snow-load sites in Finland, and bullet tanks support modular LNG satellite stations in Spain.

Dome roofs resist 5 kPa snow loads, demonstrated by Neste's 60,000 m³ Porvoo biodiesel tank engineered for –20 °C operations. Bullet tanks, typically 200 m³ each, support distributed LNG demand; Enagás deployed 18 in rural Spain during 2025. The convergence of emission compliance and inventory efficiency cements floating roofs as the default for volatile liquids through 2031.

By Tank Type: Above-Ground Leads, Mobility Accelerates

Above-ground tanks dominated with a 70.2% market share in 2025, reflecting lower construction costs and inspection ease. Underground newbuilds decline due to groundwater-protection rules; the Netherlands banned such tanks within 100 m of drinking-water wells in 2024. Mobile and modular tanks grow at an 8.9% CAGR as disaster-response agencies and LNG peak-shaving operators favor 50–1,000 m³ trailer-mounted units. Germany’s Federal Agency for Technical Relief bought 24 in 2025 for refinery turnarounds. Finland’s Gasgrid leased six 500 m³ LNG tanks from HOYER in early 2025, deferring capital while securing supply.

Above-ground vessels fit the 50,000–150,000 m³ capacity band favored at coastal terminals, whereas underground options require favorable geology and face costlier excavation. Mobility offers asset-light flexibility, enabling operators to redeploy capacity within 48 hours to seasonal hotspots.

By Material: FRP Outpaces Traditional Metals

Carbon steel retained a 45.5% share in 2025 owing to its USD 800–1,200 /m³ cost and well-defined API 650 guidelines. Stainless steel held 22% for high-purity and acidic products, but FRP is the fast-growing material with a 9.7% CAGR through 2031. Decal Spain delivered 38 FRP biodiesel tanks in 2025, each warrantied for 25 years without recoating. Alkion installed eight FRP units on reclaimed land near Venice, saving EUR 1.2 million in deep-pile foundations. EU renewable-energy mandates favor corrosion-proof materials, bolstering FRP adoption.

Stainless 316L vessels dominate SAF and renewable-diesel storage, as shown by TotalEnergies’ 180,000 m³ La Mède installation in 2024. Concrete tanks remain niche at 8% share for low-value liquids due to incompatibility with leak-detection standards.

By Capacity Range: Mid-Tier Tanks Optimize Economics

Tanks between 50,000 and 150,000 m³ represented 32.7% of the market in 2025 and will grow 6.9% annually. A 100,000 m³ tank buffers 7–10 days of crude for a 200,000 bbl/d refinery, balancing working-capital cost with operational resilience. Germany’s PCK Raffinerie added two 120,000 m³ crude vessels in 2024, reducing pumping energy by 18% after consolidating four smaller tanks. Sub-5,000 m³ tanks serve airport hydrant systems; Aéroports de Paris installed 14 for SAF segregation in 2025. Mega-tanks above 150,000 m³, although cheapest per m³, face tougher seismic and permitting hurdles, concentrated in Rotterdam and Antwerp.

By Product: LNG Storage Expands Fastest

Crude oil held a 31.8% share in 2025, yet LNG and LPG collectively post an 8.2% CAGR to 2031 as import hubs proliferate. Gate terminal’s fourth truck-loading bay now serves 180 industrial customers across Northwest Europe. Spain plans to add 400,000 m³ across Barcelona and Cartagena by 2028. Conventional refined products lose ground to SAF and renewable diesel, which require dedicated stainless or FRP segregation tanks. Specialty petrochemicals such as methanol and BTX maintain an 8% niche, anchored in Rotterdam’s Botlek and Antwerp’s chemical clusters.

By End User: Refinery Demand Persists Despite Rationalization

Refineries and petrochemical complexes delivered 33.3% of 2025 demand and are forecast to grow 7.1% yearly, propelled by SAF and hydrogen co-processing lines. Traders like Vitol commissioned proprietary capacity, 250,000 m³ in Rotterdam in June 2025, to capture blending margins and reduce counterparty risk. Strategic-reserve agencies offer 15-year take-or-pay leases, exemplified by Spain’s 400,000 m³ commitment to Rubis in 2024. Logistics firms HOYER and LBC diversify into chemicals to offset petroleum volume declines, sustaining a 6.3% CAGR.

Geography Analysis

Germany led the European oil & gas storage tank market with a 23.4% share in 2025, underpinned by four FSRUs totaling 30 bcm/year and 480,000 m³ of cryogenic storage commissioned between 2023 and 2025. Strategic-reserve additions of 3.2 million m³ and SAF infrastructure investments sustain a 6.7% CAGR through 2031 despite lower refinery throughput. Russia is forecast to have the fastest 7.6% CAGR as Transneft’s 1.2 million m³ Ust-Luga expansion and Gazprom Neft’s 300,000 m³ product tanks at Omsk bolster export-oriented capacity. Regulatory cycles of 15 years reduce lifecycle compliance cost, favoring carbon-steel mega-tanks.

The United Kingdom, France, Italy, and Spain collectively accounted for 38% of 2025 revenue. UK LNG storage grew 120,000 m³ in 2024, with another 200,000 m³ planned by 2028. France’s La Mède biorefinery added 80,000 m³ SAF capacity in 2025. Italy’s Saras replaced six fixed roofs with four floating roofs, cutting VOCs 1,100 t/yr. Spain’s Repsol and Cepsa each invested EUR 200 million in biofuel terminals using FRP tanks in 2025.

Nordic markets, Norway, Sweden, Finland, Denmark, represent 9% share and grow 6.8% annually, led by LNG imports and hydrogen pilots. Norway inaugurated a 50,000 m³ CO₂ tank at Øygarden in June 2025, showcasing reuse potential for decommissioned crude infrastructure. Finland’s modular LNG bullet tanks underscore the region’s preference for incremental capacity that avoids multiyear permitting.

Competitive Landscape

The European oil & gas storage tank market competition is moderate, with Royal Vopak, Oiltanking, VTTI, Odfjell, and Rubis holding 40% of third-party capacity. Royal Vopak’s EUR 450 million renewal program targets a 30% Scope 1 reduction by 2030, focusing on floating roofs and stainless steel. VTTI’s 250,000 m³ Europoort expansion, finished in November 2025, integrates 98% VOC-capture vapor-recovery and secured a 10-year Shell Trading SAF contract. Odfjell delayed a Rotterdam chemical-tank project 14 months due to permitting uncertainty, illustrating regulatory risk.

Hydrogen, CCS, and modular emergency tanks represent white-space niches. Germany’s hydrogen roadmap implies 300,000–400,000 m³ of new compressed or liquid tanks by 2030. BP’s and Equinor’s CCS plans open retrofit orders for supercritical CO₂ tanks. Challenger firms like Dyer Gas and Virtor Oy leverage skid-mounted LNG and hydrogen vessels to undercut incumbents on lead time, delivering 22 modular LNG tanks in Germany during 2025. Technology adoption increasingly separates leaders; ROSEN’s twin system on 340 tanks extends API 653 intervals from five to seven years.

Europe Oil And Gas Storage Tank Industry Leaders

Royal Vopak N.V.

Oiltanking GmbH

Vitol Tank Terminals International BV (VTTI)

HES International BV

Rubis Terminal

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: ORLEN Paliwa has wrapped up a significant investment at its Liquefied Petroleum Gas (LPG) Terminal in Szczecin. With the expansion, the terminal's storage capacity has doubled, and its handling volume surged by nearly 65%, now reaching an annual capacity of 400 thousand tonnes of LPG. Valued at over PLN 150 million, the project bolsters the security and reliability of ORLEN's LPG supply chain, benefiting both its clientele and network of fuel stations. A consortium of Polish firms spearheaded the entire project.

- April 2025: Mervielde marked a pivotal milestone in its logistics expansion. The company welcomed eight sizable shore tanks at its Seveso site, located in the North Sea Port. These liquid storage tanks, transported via pontoon from Antwerp, signify a substantial enhancement to the site's existing infrastructure.

- February 2025: Tepsa Netherlands completed a significant expansion in Rotterdam. The company added nine new tanks, increasing capacity by 28,000 m³. These tanks are designated for petrochemicals, Sustainable Aviation Fuel (SAF), and Liquid Waste Plastic (LWP) for Neste. Additionally, Tepsa acquired the GES Rotterdam terminal in Europoort, which boasts a capacity of 212,000 m³.

- February 2024: In response to the rising demand for chemical storage in northwestern Europe, LBC Tank Terminals has greenlit a significant expansion at its Rotterdam terminal. By 2026, the terminal's storage capacity will swell to 280,000 cubic meters, thanks to an addition of 98,000 cubic meters. This expansion is a pivotal step in the terminal's ongoing multi-year growth initiative.

Europe Oil And Gas Storage Tank Market Report Scope

Oil and gas storage tanks are used throughout the oil and gas industry to bulk-contain fluids at different stages of the refinery process. Products are often stored for a short time before being transported for further processing.

The European oil and gas storage tank market is segmented by design, tank type, material, capacity range, product, end user, and geography. By design, the market is segmented into fixed-roof, floating-roof, dome-roof, spherical, bullet, and other tank designs. By tank type, the market is categorized into aboveground, underground, and mobile/modular storage tanks. By material, the market is segmented into carbon steel, stainless steel, fiber-reinforced plastic (FRP), concrete, and other materials. By capacity range, the market is segmented into tanks with capacities up to 5,000 m³, 5,000–50,000 m³, 50,000–150,000 m³, and above 150,000 m³. By product, the market is segmented into crude oil, refined petroleum products, natural gas liquids (NGL), aviation fuel, and specialty hydrocarbons. By end user, the market is segmented into producers, refineries, traders, strategic petroleum reserves (SPRs), and logistics providers. For each segment, the market size and forecasts are provided on the basis of value (USD).

By Design

| Fixed-Roof Tanks |

| Floating-Roof Tanks |

| Dome-Roof Tanks |

| Spherical Tanks |

| Bullet Tanks and Others |

By Tank Type

| Aboveground Storage Tanks (ASTs) |

| Underground Storage Tanks (USTs) |

| Mobile/Modular Tanks |

By Material

| Carbon Steel |

| Stainless Steel |

| Fiberglass-Reinforced Plastic (FRP) |

| Concrete |

| Others |

By Capacity Range

| Up to 5k m³ |

| 5 to 50k m³ |

| 50 to 150k m³ |

| Above 150k m³ |

By Product

| Crude Oil |

| Refined Petroleum Products |

| Natural Gas Liquids (e.g., LPG, LNG) |

| Aviation Fuel and Middle Distillates |

| Specialty Hydrocarbons/Petrochemicals |

By End-User

| Oil and Gas Producers |

| Refineries and Petrochemical Plants |

| Traders and Distributors |

| Strategic Petroleum Reserve Agencies (SPRs) |

| Logistics/Transportation companies |

By Geography

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| NORDIC Countries |

| Russia |

| Rest of Europe |

| By Design | Fixed-Roof Tanks |

| Floating-Roof Tanks | |

| Dome-Roof Tanks | |

| Spherical Tanks | |

| Bullet Tanks and Others | |

| By Tank Type | Aboveground Storage Tanks (ASTs) |

| Underground Storage Tanks (USTs) | |

| Mobile/Modular Tanks | |

| By Material | Carbon Steel |

| Stainless Steel | |

| Fiberglass-Reinforced Plastic (FRP) | |

| Concrete | |

| Others | |

| By Capacity Range | Up to 5k m³ |

| 5 to 50k m³ | |

| 50 to 150k m³ | |

| Above 150k m³ | |

| By Product | Crude Oil |

| Refined Petroleum Products | |

| Natural Gas Liquids (e.g., LPG, LNG) | |

| Aviation Fuel and Middle Distillates | |

| Specialty Hydrocarbons/Petrochemicals | |

| By End-User | Oil and Gas Producers |

| Refineries and Petrochemical Plants | |

| Traders and Distributors | |

| Strategic Petroleum Reserve Agencies (SPRs) | |

| Logistics/Transportation companies | |

| By Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| NORDIC Countries | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current and projected value for Europe oil & gas storage tank market?

The market size stood at USD 4.39 billion in 2026 and is forecast to reach USD 6.01 billion by 2031, reflecting a 6.48% CAGR.

Which tank design captures the largest revenue share across Europe?

Floating-roof vessels hold 35.9% of 2025 revenue and are advancing at a 7.5% CAGR because VOC rules favor this low-emission architecture.

How fast is demand for LNG and other natural-gas-liquid storage expanding?

LNG and LPG tank capacity posts the region’s quickest 8.2% CAGR through 2031, driven by new FSRUs and cryogenic terminals in Germany, the Netherlands, and Finland.

What role do digital twins play in maintaining European tank farms?

Platforms from ROSEN and Siemens Energy cut unplanned downtime by up to 22% and trim annual inspection costs 15% by shifting to condition-based maintenance.

How do new EU environmental standards affect capital costs?

Upgrading a 100,000 m³ floating-roof tank to meet 2024 VOC limits requires EUR 1.2–1.8 million in seal, vapor-recovery, and monitoring systems.

Page last updated on: