Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

| Base Year Market Size (2025) | USD 23.19 Billion |

| Market Size (2026) | USD 23.74 Billion |

| Market Size (2031) | USD 26.69 Billion |

| Growth Rate (2026 - 2031) | 2.37% CAGR |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Korea Pharmaceutical Market Analysis by Mordor Intelligence

The Korea pharmaceutical market size is expected to grow from USD 23.19 billion in 2025 to USD 23.74 billion in 2026 and is forecast to reach USD 26.69 billion by 2031 at 2.37% CAGR over 2026-2031. This modest rise sits at the intersection of a super-aged society, export-oriented biologics capacity, and pricing rules that favor value-based care. Government funding for biomedical R&D climbs 15% in 2025, signaling sustained political will to back novel therapies even as the actual-transaction-price scheme continues to restrain reimbursement ceilings. Biologics plants in Songdo now supply leading multinationals and drive record pharma exports, while data-protection reforms grant 4–10 years of exclusivity depending on drug class. Cardiovascular drugs dominate scripts because 45.2% of middle-aged and senior Koreans have hypertension. Oncology lines, benefitting from accelerated MFDS review and aggressive R&D tax credits, post the fastest growth through 2030. Digital health laws and the coming debate on tele-pharmacy hint at longer-term channel disruption that could reshape the Korea pharmaceutical market.

Key Report Takeaways

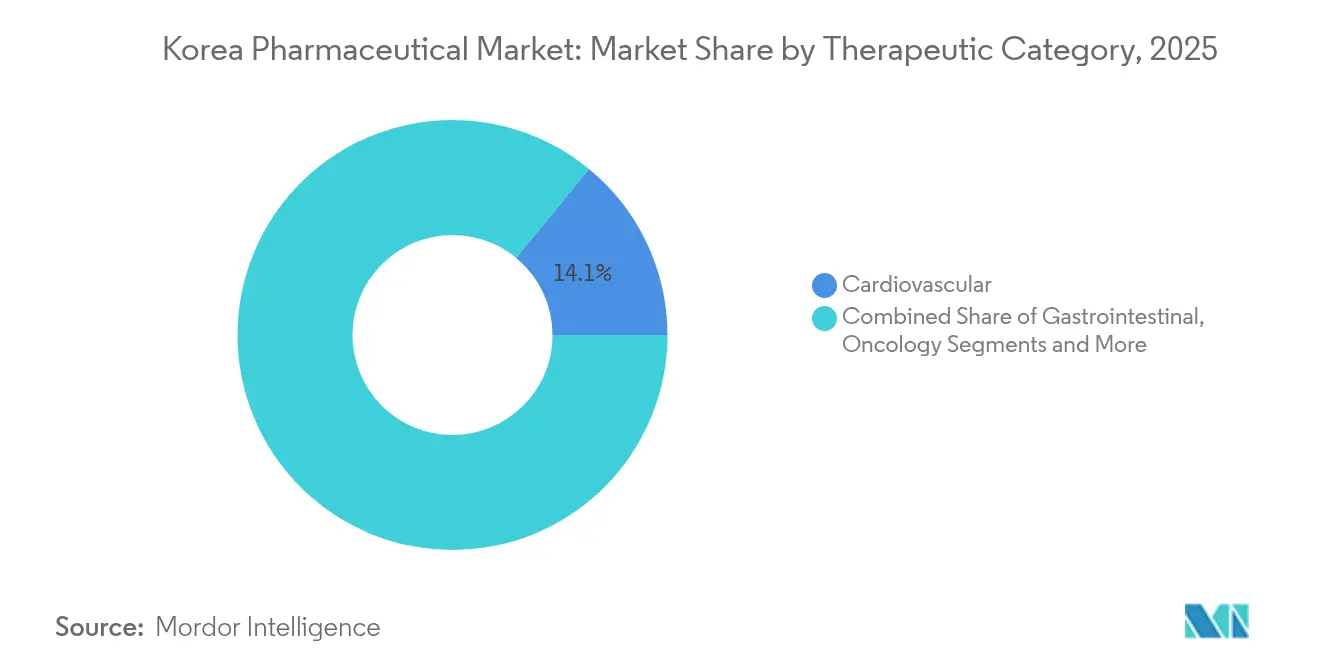

- By therapeutic category, cardiovascular therapies held 14.05% of the Korea pharmaceutical market share in 2025; oncology is projected to expand at a 4.24% CAGR to 2031.

- By drug type, prescription medicines represented 86.88% of the Korea pharmaceutical market size in 2025, while OTC products advance at a 3.04% CAGR through 2031.

- By technology, small molecules accounted for 67.42% of the Korea pharmaceutical market size in 2025; biologics are moving at a 3.72% CAGR to 2031.

- By formulation, tablets commanded 51.55% share of the Korea pharmaceutical market size in 2025, and injectables are climbing at a 2.86% CAGR through 2031.

- By distribution channel, hospital pharmacies controlled 45.62% of the Korea pharmaceutical market size in 2025; online pharmacies register the quickest 3.81% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Korea Pharmaceutical Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supportive government policy framework for biopharma industrialization | +0.7% | National and export markets | Medium term (2-4 years) |

| Aging population and rising chronic disease burden | +0.6% | Nationwide, urban hubs | Long term (≥4 years) |

| Surge in biosimilar adoption backed by domestic manufacturing scale | +0.5% | Domestic and EU/US export corridors | Medium term (2-4 years) |

| Growing export-oriented CDMO contracts from NA & EU clients | +0.3% | North America and Europe | Short term (≤ 2 years) |

| Universal national health insurance coverage driving drug consumption | +0.2% | Nationwide | Long term (≥ 4 years) |

| Duty-free access to the EU and United States | +0.4% | Nationwide | Short term (≤ 2 years |

| Source: Mordor Intelligence | |||

Supportive Government Policy Framework for Biopharma Industrialization

The 2023 “Bio Economy 2.0” plan lifts biopharma funding to 36.7 billion won in 2025, trims approval-to-reimbursement lag via an MFDS linkage system, and cements Seoul’s position as the world’s top city for industry-sponsored trials. These levers fuel pipeline expansion across antibody-drug conjugates, RNA therapeutics, and cell therapies, enhancing export competitiveness for the Korea pharmaceutical market.

Aging Population and Rising Chronic Disease Burden

With citizens 65+ passing the 20% threshold in 2025, chronic illness prevalence soars. Out-of-pocket medical costs for seniors managing multiple conditions average USD 1,163.8 versus USD 456.1 for peers without comorbidities [1]Soojin Park, “Effects of Changes in Multiple Chronic Conditions on Medical Costs among Older Adults in South Korea,” Healthcare, mdpi.com.Government “Essential Healthcare” packages that bolster local clinics and telemonitoring expand long-term demand for antihypertensives, statins, and antidiabetics across the Korea pharmaceutical market.

Surge in Biosimilar Adoption Backed by Domestic Manufacturing Scale

Samsung Biologics’ fifth plant raises capacity to 784,000 liters. Korea now ranks second worldwide in FDA-approved biosimilars and develops 1.5 new entries per year. This scale advantage underpins brisk export wins for trastuzumab and adalimumab copies and cements the Korea pharmaceutical market as a global biosimilar hub.

Growing Export-Oriented CDMO Contracts from NA & EU Clients

Contracts exceeding USD 13 billion link Korean plants with 16 of the top-20 multinational drug makers. Celltrion alone targets USD 2.1 billion in annual CDMO sales by 2031. These deals fortify supply chains for European and U.S. launches, elevating the Korea pharmaceutical market in global value networks.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Drug re-pricing policy compresses margins | -0.4% | Nationwide, stronger on innovators | Medium term (2-4 years) |

| Risk-sharing agreements delay ultra-orphan launches | -0.3% | National specialty segments | Short term (≤ 2 years) |

| Heavy reliance on imported API | -0.3% | Global supply chains | Short term (≤ 2 years) |

| GMP-qualified workforce shortage | -0.2% | Nationwide manufacturing hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Drug Re-pricing Policy Compresses Margins

Actual-transaction-price audits and tougher volume caps cut list prices after market launch. Generics still lack decisive price gaps versus originals, curbing competition [2]Da Hye Lee, “International Comparison of Generic Competition, Prices, and Usage Trends: South Korea and G20 Countries,” Frontiers in Public Health, frontiersin.org. Oncology absorbs 46.2% of new-drug spending, squeezing funds for other areas and heightening pressure to renegotiate rebates within the Korea pharmaceutical market.

Risk-Sharing Agreements Delay Ultra-Orphan Launches

Sixty-eight products sit under Korea’s RSA list, but complex rebate models extend negotiations beyond the statutory 30 days [3]MedPath, “South Korea Accelerates Drug Reimbursement Process with New Pilot Program,” MedPath, trial.medpath.com. Although rare-disease drugs can bypass cost-effectiveness proofs, definitional disputes over “innovative new drug” stall approvals. These delays moderate near-term uptake for ultra-orphan therapies in the Korea pharmaceutical market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Therapeutic Category: Chronic Diseases Reshape Treatment Paradigms

Cardiovascular drugs delivered 14.05% of the Korea pharmaceutical market size in 2025, driven by high hypertension prevalence and strong compliance with combination pills. Oncology outpaces all others at a 4.24% CAGR, backed by accelerated MFDS reviews and robust venture funding for antibody-drug conjugates showcased at AACR 2025.

Anti-diabetic segments gain traction as DPP4 and SGLT2 inhibitors secure guideline status, while GI therapies rebound on new acid-blocker launches such as Fexuclue, whose sales jumped 57% in early 2024. Respiratory products stabilize post-COVID, and rare-disease portfolios benefit from strengthened data exclusivity, increasing their viability inside the Korea pharmaceutical market.

By Drug Type: Prescription Leadership Amid OTC Acceleration

Prescription products held 86.88% Korea pharmaceutical market share in 2025, cemented by universal insurance and strict physician-dispense separation. Branded drugs survive list-price erosion through line-extension reformulations, while generics struggle to win volume due to identical pricing rules.

OTC medicines, though smaller, clock a 3.04% CAGR, helped by a 2012 law that lets convenience stores sell select analgesics. Consumer self-care apps guide dosing and refill alerts, deepening penetration of vitamins and digestive aids within the Korea pharmaceutical market.

By Technology: Biologics Gain Momentum Against Small Molecules

Small molecules still represent 67.42% of the Korea pharmaceutical market size in 2025 thanks to cost advantages and oral convenience. Process intensification and continuous manufacturing keep margins stable.

Biologics rise at a 3.72% CAGR, propelled by mega-capacity in Songdo and the Advanced Regenerative Medicine Act that sets clear CMC and follow-up rules. Biosimilars unlock hospital savings, freeing budgets for breakthrough checkpoint inhibitors and cell therapies, reinforcing the Korea pharmaceutical market as a biologics powerhouse.

By Formulation: Tablets Dominate While Injectables Advance

Tablets made up 51.55% of 2025 volume, favored for low cost and stability. Continuous-tableting lines and taste-mask coatings extend product life cycles across chronic care.

Injectables gain a 2.86% CAGR due to biologics and long-acting depots. Pre-filled syringes and auto-injectors reduce clinic time, while nanoparticle suspensions improve solubility for poorly absorbed APIs . Formulators also explore cyclodextrin complexes such as KLEPTOSE® for antibody stabilization.

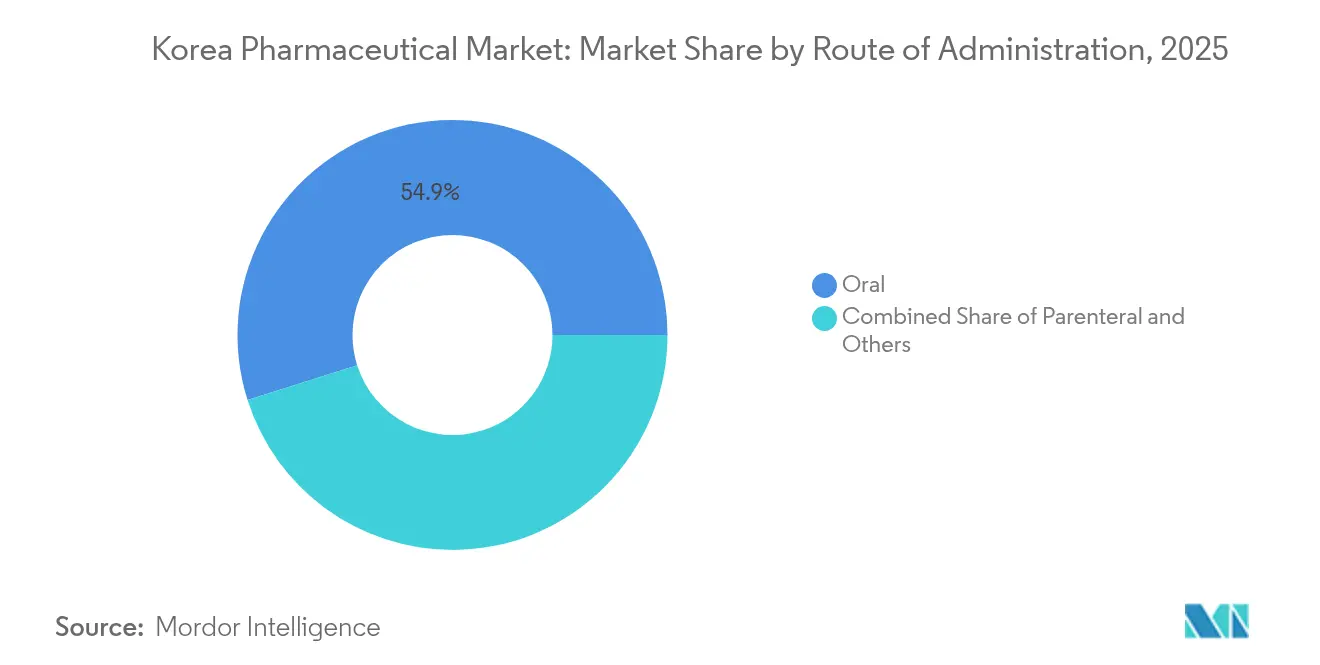

By Route of Administration: Oral Dominance with Parenteral Growth

Oral drugs account for 54.88% of prescriptions, reflecting 73.1% patient preference for pills. Nanotechnology now tackles peptide absorption hurdles, widening the future oral pipeline.

Parenterals grow at 2.94% CAGR as biologics, vaccines, and gene therapies demand direct bloodstream delivery. Dual-chamber syringes and mRNA-ready cold-chains spread quickly, reinforcing the Korea pharmaceutical market’s readiness for next-wave therapies.

By Distribution Channel: Hospital Dominance Amid Digital Transformation

Hospital pharmacies controlled 45.62% of 2025 spending, aided by bundled tenders and embedded e-procur¬ement systems. Retail pharmacies focus on chronic-care counseling but face thinner margins after convenience stores entered OTC sales.

Online pharmacies, though currently restricted, deliver a 3.81% CAGR for wellness lines, previewing significant upside once tele-pharmacy rules evolve. The Digital Medical Products Act, effective January 2025, sets cybersecurity and performance standards for digital therapeutics, laying groundwork for future virtual dispensing inside the Korea pharmaceutical market.

Geography Analysis

Metropolitan clusters-Seoul, Busan, Incheon-absorb most prescriptions due to dense hospital networks and earlier adoption of innovative drugs. Seoul hosts the world’s highest tally of industry trials, letting firms gauge real-world effectiveness quickly and target formulary inclusion faster than in secondary cities. Smart-hospital projects, with AI-assisted dosing and robotics, fortify big-city lead in the Korea pharmaceutical market.

Rural districts, facing depopulation, record lower cancer-screening uptake. Older adults prefer to age in familiar settings despite travel barriers, pressing wholesalers to refine cold-chain logistics and community pharmacies to expand home-delivery services. Government tele-health pilots aim to close monitoring gaps, improving chronic-disease medication adherence across the Korea pharmaceutical market.

Special economic zones, led by Songdo Bio Cluster, concentrate manufacturing and R&D. Tax breaks, bonded warehouses, and streamlined customs speed biologic exports to the EU and U.S. Additional 17 bio-clusters under development will spread this model nationwide, diversifying geographic contribution and enlarging the Korea pharmaceutical market footprint.

Competitive Landscape

Competition blends rising domestic giants with entrenched multinationals. Samsung Biologics runs the planet’s largest single-site biologics facility and secures CDMO contracts with 16 of the top-20 pharma producers. Celltrion funnels biosimilar profits into 13 novel candidates and eyes a 2027 Nasdaq listing. Yuhan Corporation’s EGFR-targeting Lazertinib is Korea’s first home-grown oncology product to clear the FDA, unlocking a USD 750 million global sales horizon.

Multinationals defend territory with checkpoint inhibitors and cardiometabolic blockbusters, partnering with local CROs for streamlined development and co-promotion. Mid-tier firms pivot toward dermatology, metabolic, or ophthalmology niches, reducing direct collision with bigger players.

Digital innovation becomes the new divider. AI-driven discovery start-ups compress lead-optimization cycles, and drug-delivery ventures attract USD 19.9 million VC funding since 2024. Manufacturing plants deploy predictive maintenance, minimizing downtime and reinforcing Korea pharmaceutical market quality credentials.

Korea Pharmaceutical Industry Leaders

AbbVie Inc.

AstraZeneca plc

Bayer AG

SAMSUNG PHARM. Co., LTD.

GlaxoSmithKline plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Celltrion discloses plans to buy a health-food maker and targets a 2027 Nasdaq listing.

- May 2025: Korean pharma groups earmark KRW 60 trillion for M&A, spotlighting biosimilars and innovative assets.

- April 2025: The amended Pharmaceutical Affairs Act introduces data-protection windows of 4–10 years.

Korea Pharmaceutical Market Report Scope

As per the scope of this report, pharmaceuticals are referred to as prescribed and non-prescription drugs. These medicines can be bought by an individual with or without the doctor's prescription and are safe for consumption for various illnesses with or without the doctor's consent.

The Korean pharmaceutical market is segmented by therapeutic category (anti-infectives, cardiovascular, gastrointestinal, anti-diabetic, respiratory, and others) and drug type (prescription drugs (branded drugs and generic drugs) and over-the-counter drugs). The report offers the value (in USD million) for the above segments.

By Therapeutic Category

| Anti-infectives |

| Cardiovascular |

| Gastrointestinal |

| Anti-diabetic |

| Respiratory |

| Oncology |

| Others |

By Drug Type

| Prescription Drugs | Branded |

| Generics | |

| OTC Drugs |

By Technology

| Small Molecules |

| Biologics |

| Biosimilars |

By Formulation

| Tablets |

| Capsules |

| Injectables |

| Others (Topicals, Patches, etc.) |

By Route of Administration

| Oral |

| Parenteral |

| Others (Inhalational, Transdermal) |

By Distribution Channel

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Pharmacies |

| By Therapeutic Category | Anti-infectives | |

| Cardiovascular | ||

| Gastrointestinal | ||

| Anti-diabetic | ||

| Respiratory | ||

| Oncology | ||

| Others | ||

| By Drug Type | Prescription Drugs | Branded |

| Generics | ||

| OTC Drugs | ||

| By Technology | Small Molecules | |

| Biologics | ||

| Biosimilars | ||

| By Formulation | Tablets | |

| Capsules | ||

| Injectables | ||

| Others (Topicals, Patches, etc.) | ||

| By Route of Administration | Oral | |

| Parenteral | ||

| Others (Inhalational, Transdermal) | ||

| By Distribution Channel | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Pharmacies | ||

Key Questions Answered in the Report

How big is the Korea Pharmaceutical Market?

The Korea Pharmaceutical Market size is expected to reach USD 23.74 billion in 2026 and grow at a CAGR of 2.37% to reach USD 26.69 billion by 2031.

Which therapy area is expanding fastest?

Oncology posts the highest trajectory with a 4.24% CAGR, buoyed by accelerated MFDS approvals and robust domestic R&D funding.

Who are the key players in Korea Pharmaceutical Market?

AbbVie Inc., AstraZeneca plc, Bayer AG, SAMSUNG PHARM. Co., LTD. and GlaxoSmithKline plc are the major companies operating in the Korea Pharmaceutical Market.

Why are biosimilars central to Korea’s export growth?

Domestic plants rank second globally in FDA-approved biosimilars and offer cost-competitive monoclonal antibodies that drive shipments to Europe and the U.S.

Page last updated on: