Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

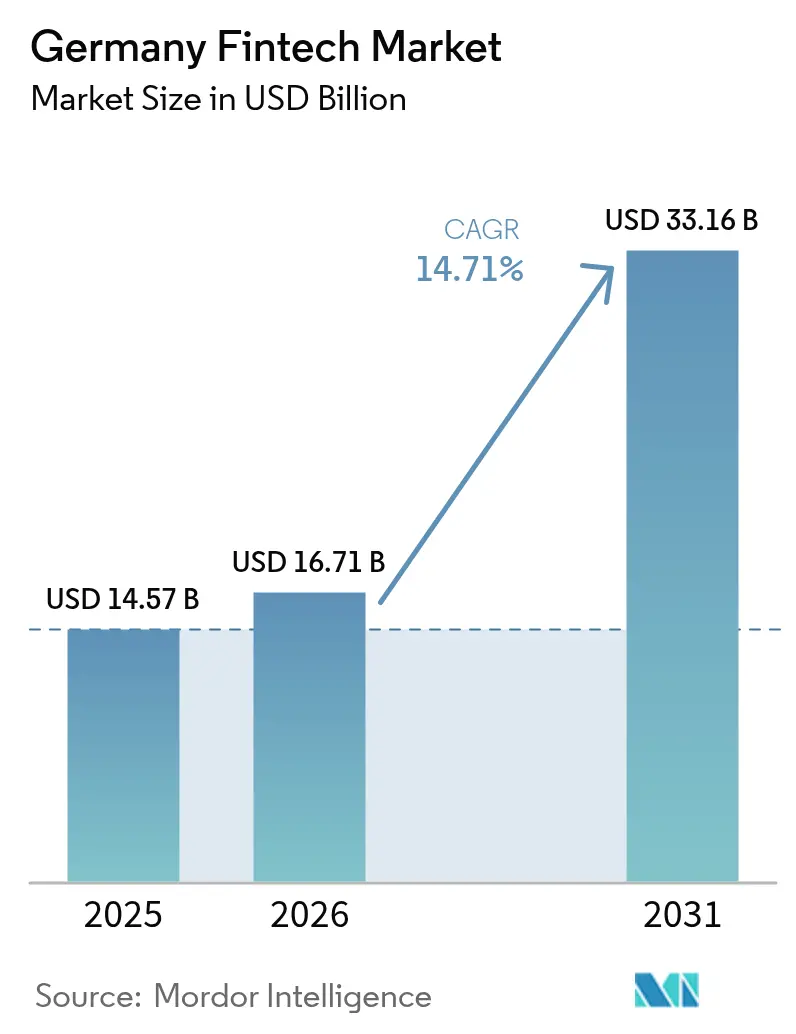

| Base Year Market Size (2025) | USD 14.57 Billion |

| Market Size (2026) | USD 16.71 Billion |

| Market Size (2031) | USD 33.16 Billion |

| Growth Rate (2026 - 2031) | 14.71% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Germany Fintech Market Analysis by Mordor Intelligence

Germany Fintech Market size in 2026 is estimated at USD 16.71 billion, growing from 2025 value of USD 14.57 billion with 2031 projections showing USD 33.16 billion, growing at 14.71% CAGR over 2026-2031.

Continued investment in open-banking rails, rapid smartphone penetration, and enterprise digitalization keeps momentum high even as funding conditions tighten. Digital payments retain headline status by combining contactless acceptance, one-click checkout, and buy-now-pay-later options, while insurtech earns the growth spotlight through parametric products that automate claims and cut loss-adjustment expenses. Competitive strategies reflect a three-tier structure: scale neobanks—led by N26 and Trade Republic—drive brand awareness, mid-sized specialists such as Solaris and Wefox monetize specific rails, and new entrants attack underserved niches through vertical-first platforms. German regulation, although lengthy, supplies a moat that favors well-capitalized innovators and forces disciplined unit economics. Ecosystem collaboration is maturing banks monetize APIs rather than resist them, insurers co-create underwriting engines with cloud-native partners, and industrial conglomerates embed finance inside supply-chain software.

Key Report Takeaways

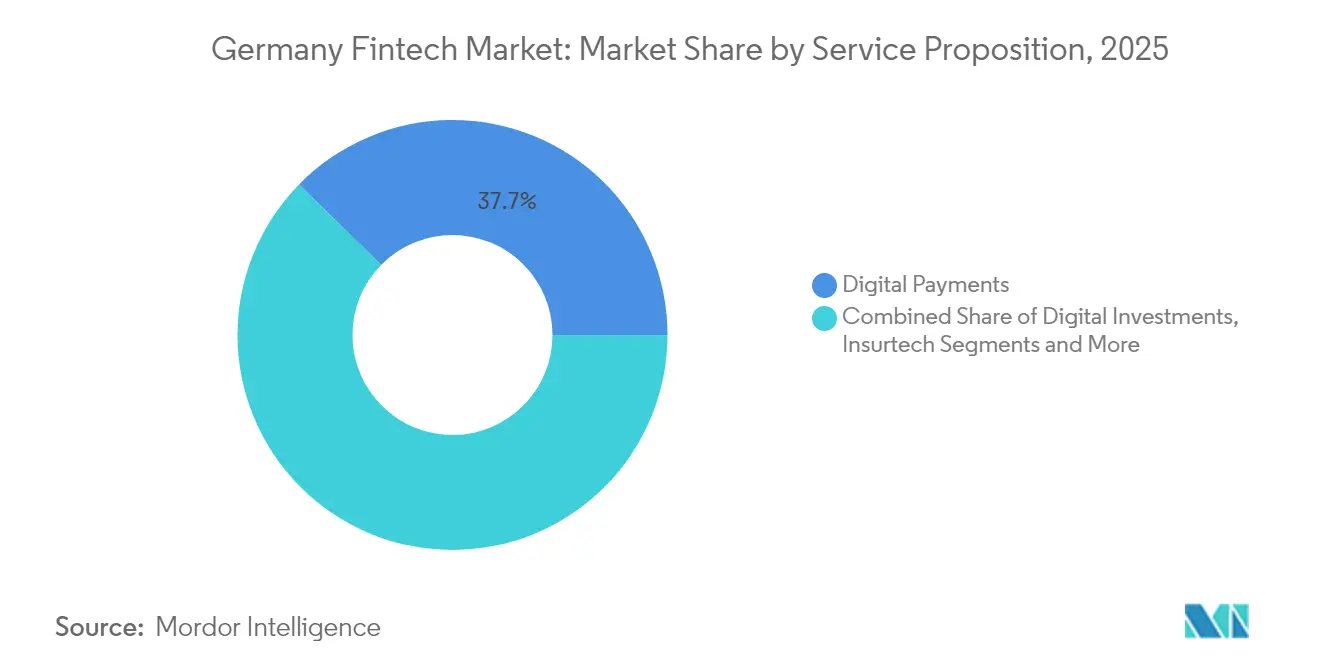

- By service proposition, digital payments led with 37.65% of Germany's fintech market share in 2025, while insurtech is forecasted to expand at an 17.98% CAGR through 2031.

- By end-user, retail dominated with 64.10% Germany fintech market share in 2025; the businesses segment is projected to grow at a 16.4% CAGR to 2031.

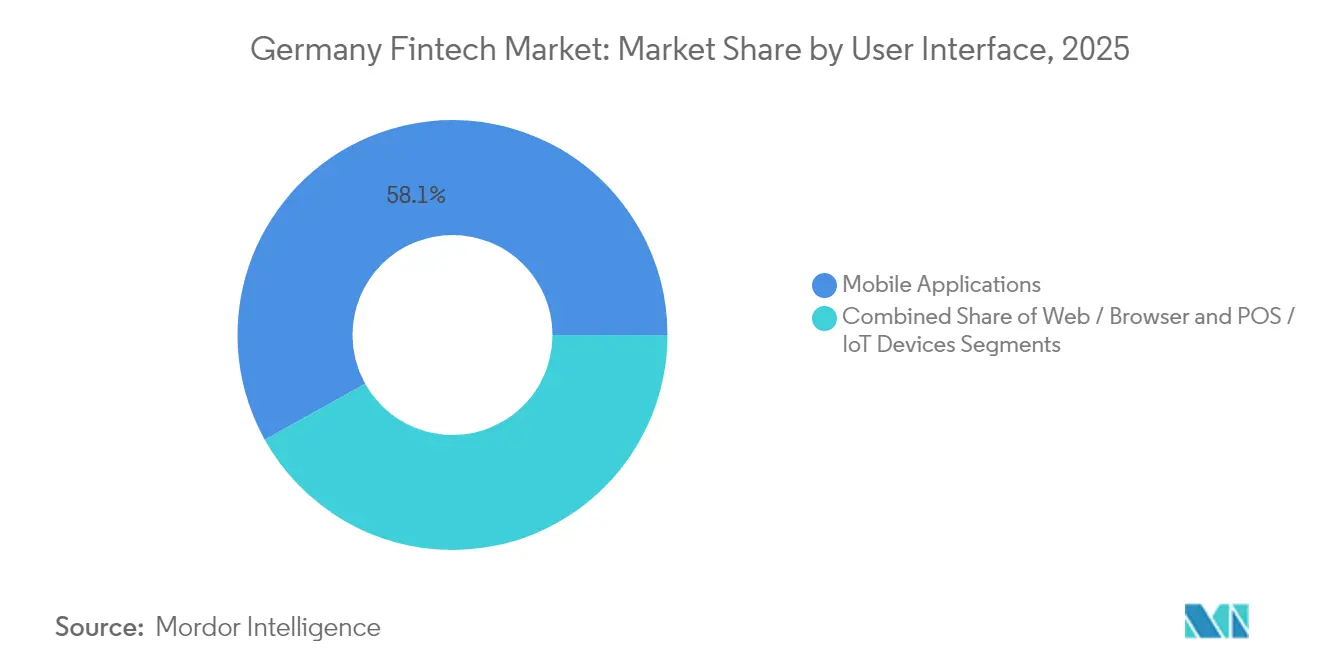

- By user interface, mobile applications accounted for 58.10% of the Germany fintech market size in 2025, and POS/IoT devices are expected to advance at a 20.55% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Germany Fintech Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| PSD2-driven open banking adoption | +3.0% | National, early gains in urban centers | Medium term (2-4 years) |

| Demographic shift toward mobile-first banking | +2.5% | National, stronger in urban areas | Medium term (2-4 years) |

| Surge in e-commerce volumes | +2.0% | National | Short term (≤ 2 years) |

| Digital treasury modernization | +1.5% | National, industrial regions | Medium term (2-4 years) |

| Instant payment settlement | +1.0% | National | Short term (≤ 2 years) |

| EU green finance policies | +0.8% | National, eco-conscious regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

PSD2-driven open banking accelerates API innovation

Mandatory API gateways introduced under PSD2 have moved German banks from resistance to monetization. BaFin’s secure-API mandate spawned 187 registered third-party providers in 2024, a 23% jump year-on-year[1]European Banking Authority, “Register of Payment and E-Money Institutions,” eba.europa.eu. Institutions now compete on developer experience: Deutsche Bank’s XS2A sandbox underpins account aggregation, and savings-bank groups package real-time payment initiation for e-commerce checkouts. Strong customer authentication, once viewed as friction, reduces fraud exposure and standardizes security, allowing fintechs to scale without bespoke integrations. The shift from compliance to commercial API portfolios positions open banking as a durable growth rail for the Germany fintech market.

Demographic shift toward mobile-first banking among urban Gen Z and millennials

Consumers under 35 rarely visit branches and expect instant onboarding, account insights, and investment execution on a smartphone. Urban adoption rates translate into usage rather than just downloads: active mobile-bank users log in 15-20 times a month, double 2022 levels. This mobile bias extends to investing, where fractional-share platforms eclipse traditional advisors for first-time investors. Providers that pair sleek UX with deposit protection win share, while slower incumbents risk brand relevance.

Surge in German e-commerce volumes fuels embedded payment solutions

Digital wallet share hit a considerable share of online checkouts in 2024, gaining 4.7 percentage points year-on-year. Retailers integrate one-click payments, instant credit, and delivery insurance at checkout, turning payment APIs into customer-acquisition levers. Embedded finance now extends to B2B marketplaces that connect buyers, suppliers, and working-capital engines on a single screen, broadening addressable revenue pools for fintech providers.

Digital treasury modernization expands B2B fintech demand

Around 68% of German CFOs rank treasury automation as a top-three priority. Real-time liquidity dashboards and API connectivity with ERP suites let mid-market exporters hedge FX risk within minutes instead of days. Longer sales cycles are offset by higher lifetime value and 95% renewal rates, anchoring predictable revenue streams for providers that master corporate onboarding.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent cash preference among older consumers | -2.0% | National, stronger in rural areas | Long term (≥ 4 years) |

| Stringent BaFin licensing process | -1.5% | National | Short term (≤ 2 years) |

| VC funding contraction in Series B+ | -1.0% | National, early-stage startups | Short term (≤ 2 years) |

| Legacy IT fragmentation at incumbent banks | -0.8% | National | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Persistent cash preference among older Germans

Cash still accounts for a significant portion of transactions, with the 65+ cohort driving most usage[2]Deutsche Bundesbank, “Payment Behaviour in Germany 2023,” bundesbank.de. Rural merchants reinforce habits by offering cash discounts. Fintechs respond with hybrid rails: Paysafe and Deutsche Bank co-develop cash-in/cash-out at post offices, while G+D pilots a CBDC that mimics banknotes offline. Yet acquisition costs rise when digital onboarding must coexist with in-store education, capping the upside for fully cashless propositions.

Stringent BaFin licensing extends time-to-market

Payment-institution approval requires 12-18 months, audited governance plans, and minimum capital far above EU averages[3]BaFin, “Payment Services Supervision Act (ZAG) – Open Banking Requirements,” bafin.de. While the framework underpins stability, it delays revenue and forces start-ups to raise bridge rounds. Well-capitalized entrants treat the process as a competitive moat, but smaller founders often relocate to passport-friendly domiciles, diluting domestic innovation density.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Proposition: Insurtech unlocks the fastest runway

Digital payments held a 37.65% share of Germany fintech market. Merchant adoption of contactless POS, QR codes, and embedded checkout APIs has made payment services the default monetization rail. Insurtech, in contrast, captures a modest slice today yet is forecasted to grow at an 17.98% CAGR, reflecting parametric crop cover, usage-based auto policies, and AI-driven claims. Payment specialists defend share through loyalty add-ons, while insurance challengers bundle underwriting, distribution, and policy administration on cloud cores.

Neobanking, lending, and wealth-tech form the middle ranks. Lending moves from consumer instalments to working-capital lines scored on real-time ERP data. Wealth-tech democratizes ETFs and fractions, but fee pressure forces platforms to upsell crypto custody, ESG filters, and tax optimization. The Germany fintech market, therefore, tilts from horizontal “finance-super-apps” toward vertical leaders that monetize a single profit pool deeply.

By End-User: Businesses close the gap

Retail users commanded 64.10% of Germany fintech market share in 2025, reflecting early consumer focus and rapid mobile adoption. Yet business users record the sharper trajectory, expanding to 16.4% CAGR as treasurers digitize payables, receivables, and liquidity dashboards. German SMEs—3.1 million entities—seek cloud bookkeeping with built-in payments, credit, and cash-flow forecasting, converting software subscriptions into multi-product revenue streams.

While household demand remains the volume anchor, business demand raises average revenue per user and shrinks churn. Fintechs that integrate fiscal reporting, point-of-sale data, and credit-insights APIs deepen business stickiness, adding cross-sell potential in foreign-exchange hedging and embedded insurance. The interplay of high-volume retail and high-value business segments diversifies revenue and cushions cyclical shocks for the Germany fintech market.

By User Interface: IoT devices shape the next wave

Mobile applications owned 58.10% of the Germany fintech market share in 2025, mirroring the smartphone’s role as a financial command center. POS/IoT devices, however, are forecast to climb at a 20.55% CAGR to 2031, driven by smart terminals that auto-sync inventory and enable biometrics. Retailers deploy Android-based POS that beam item-level data to cloud ERPs, unlocking financing offers at checkout. Web dashboards retain a foothold in complex investment and corporate treasury tasks, but mobile and IoT set the UX standard.

Voice assistants, in-car payments and connected-appliance re-ordering open adjacent interfaces. Fintech providers that design adaptive experiences—recognizing a customer on phone, kiosk or smart-watch—gain data richness and engagement time, reinforcing the competitive flywheel within the Germany fintech market.

Geography Analysis

Berlin hosts roughly one-third of German fintechs and attracted 88% of national venture funding in H1 2024, cementing its role as the experimentation lab. The capital’s talent density and English-speaking culture lure global engineers, while a local sandbox eases early testing. Munich leverages proximity to Allianz and Munich Re to specialize in insurtech collaborations, advancing white-label products that incumbents distribute at scale. Frankfurt’s heritage as bank headquarters underpins B2B fintech, especially treasury APIs and crypto-asset custody seeking regulatory clarity.

Hamburg focuses on retail finance, pairing port-city trade data with credit engines. Cologne builds consumer-lending and banking-as-a-service clusters, aided by university pipelines. This hub-and-spoke model diffuses innovation but complicates national network effects: founders travel between cities for partnerships more than in single-center markets. Rural areas lag in digital skills—48% basic-skill attainment versus 63% urban—creating room for hybrid distribution via postal outlets and regional savings banks. Payment-account penetration in rural Germany remains 91%, signaling near-universal bank access yet lower uptake of value-added digital services. Providers that localize interfaces and blend cash touch-points can unlock incremental growth without extensive branch build-outs.

Regulatory Landscape

Germanys fintech regulation is anchored in BaFin supervision and EU rulebooks that have recently reset compliance baselines for payments, open banking, and crypto-asset services. DORA has applied since 17 January 2025, expanding operational resilience duties such as ICT incident reporting and tighter oversight of critical third-party providers. FinmadiG implemented MiCA in Germany with effect from 30 December 2024, bringing crypto-asset service providers into a harmonized authorization and conduct framework.

BaFin sharpened supervisory priorities in 2026 by publishing its Risks in Focus 2026 agenda, highlighting cybersecurity, ICT concentration risk, and consumer protection topics including buy-now-pay-later. In parallel, the Federal Ministry of Finance advanced tax-transparency measures for crypto by progressing DAC8-related and Crypto-Asset Reporting Framework information-exchange initiatives, including a 24 March 2026 draft on exchanging information on crypto-assets, increasing reporting and data-governance requirements for platforms that intermediate digital assets.

Value Chain Analysis

Germanys fintech value chain starts with regulated access and controls (BaFin licensing under ZAG for payments, and MiCA-aligned authorization for crypto-asset services). It then extends into core infrastructure such as API connectivity for PSD2-style account access and payment initiation, identity and AML tooling, and cloud/ICT providers operating under DORA-style third-party risk disciplines. Product builders including neobanks, payment specialists, wealth-techs, and insurtechs layer customer experience, underwriting, and data analytics on top of these rails, then distribute via mobile apps, web portals, and merchant POS/IoT endpoints.

Monetization centers on transaction fees and merchant service charges (payments), spreads and risk-based pricing (lending and BNPL), platform and custody fees (investments and crypto), and commissions plus automation-driven cost takeout (insurtech). Bottlenecks cluster around compliance-intensive onboarding, outsourcing governance, and audit-ready controls, which elevates the role of regtech, standardized APIs, and resilient ICT operations as fintechs expand from consumer acquisition into B2B infrastructure and institutional-grade services.

Competitive Landscape

Germany Fintech Market structure resembles a barbell: at one pole, scale neobanks and payment giants fight for deposits, trading, and interchange; at the other, early-stage verticalists weaponize domain expertise. Payments approach a consolidation phase, with few players clearing a large portion of mobile-payment volume, while lending and wealth remain fragmented among tens of niche apps. Partnership replaces disruption rhetoric: Deutsche Bank backs Mambu for core-lending revamp, and Allianz’s digital factory co-develops underwriting logic with Wefox.

Technology differentiation concentrates in AI: fraud algorithms cut false positives by 40%, and chatbots handle 80% of inbound support within seconds. Data ownership is strategic currency; platforms embed analytics to upsell risk, credit, and insurance. The European Central Bank’s digital euro pilot looms as a structural wildcard, potentially resetting settlement economics and wallet architectures. Firms that can integrate CBDC rails early will reinforce competitive moats in the Germany fintech market.

Germany Fintech Industry Leaders

N26 GmbH

Solaris SE

Trade Republic Bank GmbH

Raisin DS GmbH

Penta Bank GmbH (Qonto Group)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Compliance-driven modernization under EU frameworks is creating whitespace for fintechs that package DORA-ready operational controls, auditable outsourcing governance, and incident response into sellable B2B capabilities for banks, insurers, and regulated partners. BaFins 2026 supervisory focus on cybersecurity, ICT concentration risk, and BNPL consumer protection supports demand for tooling that improves transaction monitoring, SCA-aligned risk scoring, and third-party risk visibility, especially for platforms running payment initiation, embedded lending, and merchant checkouts.

Crypto and tokenization infrastructure also opens room for regulated, bank-partnered offerings as MiCA-aligned authorization timelines move the market from national regimes toward an EU passporting model under FinmadiG, while Germany advances DAC8 and CARF-style tax reporting for crypto transactions. This combination favors players that can operationalize reporting, Travel Rule style data handling, and custody/execution workflows, including through partnerships with incumbents and financial groups integrating digital-asset services into existing distribution.

Recent Industry Developments

- June 2026: N26 published its fiscal year 2025 results, reporting over EUR 500 million in revenue and its first full year of net profitability. The milestone reinforces N26s positioning with regulators and partners by showing a path to sustainable unit economics while continuing to broaden its product suite.

- March 2026: Solaris SE announced a strategic transformation to become an AI-native banking platform, supported by a partnership with SBI Group. The initiative targets greater automation across banking-as-a-service operations, which can improve scalability for embedded-finance clients that rely on Solaris APIs.

- December 2024: Mambu partnered with Deutsche Bank to modernize the banks digital lending stack. The collaboration highlights incumbents shifting core lending workflows toward cloud-native architectures, creating integration opportunities for fintechs providing credit decisioning, onboarding, and data connectivity layers.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers the revenue earned in Germany from technology-enabled financial services delivered through digital channels, including payment, lending, investment, insurance-related fintech activity, and digital banking style offerings.

Scope exclusions: We exclude core bank IT outsourcing and pure back-office banking software revenue when it is not sold as a fintech service proposition.

Segmentation Overview

- By Service Proposition

- Digital Payments

- Digital Lending and Financing

- Digital Investments

- Insurtech

- Neobanking

- By End-User

- Retail

- Businesses

- By User Interface

- Mobile Applications

- Web / Browser

- POS / IoT Devices

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started with building a clear picture of Germanys financial services baseline and the digital adoption context, then mapping what share can reasonably be tied to fintech-led business models. Public and official references were used for this, such as Deutsche Bundesbank publications, BaFin releases and registers, Destatis statistics, ECB payments and banking indicators, and European Commission materials on PSD2 and related rule updates, which helped anchor the macro assumptions.

We also checked reputable ecosystem and innovation signals, including government trade and investment briefs, peer-reviewed papers on digital finance adoption, and association and industry websites that track payments, lending, and digital identity themes. Company annual reports, investor presentations, and trusted press were used to understand how revenues get recorded (fees, interest-related income, subscriptions) and to sanity-check the direction of change. When needed, a paid subscription source for company financials and a patent database were used to fill gaps around private company scale and product intensity. These are illustrative sources only, and we referred to other public materials as well to collect data points, validate assumptions, and clarify unclear items.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with fintech operators, regulated financial institutions partnering with fintechs, payment and lending intermediaries, and advisors who track product pricing and adoption. Since this is a Germany-only report, we emphasized national demand signals and regulation-led constraints, then used the discussions to pressure-test desk assumptions on take rates, monetization paths, and realistic growth speeds.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 26% | CXOs: 12% | |

| Mid tier: 60% | Functional/Unit leaders: 34% | |

| Smaller Players: 14% | Managers: 54% |

Market-Sizing & Forecasting

We sized the market using the top-down and bottom-up mix. The primary structure is a top-down demand reconstruction that starts from Germanys financial activity pools and digital usage signals, then filters into fintech-addressable revenue streams (for example, payment fee pools and digitally originated lending and investment flows). To keep totals realistic, the model was corroborated with selective bottom-up checks, such as rolling up a sample of provider revenues, channel checks on pricing, and simple ASP x volume approximations where volumes are observable.

Inputs used in the model included payment transaction activity trends, digital banking and wallet adoption indicators, credit origination and SME financing momentum, product level take rates (such as payment processing fees), and the mix shift toward app-first distribution. Where direct revenue visibility is limited for private firms, we used a conservative gap-handling step that ties implied scale to licensing status, customer traction signals, and known monetization structures, then adjusts based on what interviewees consider feasible.

For forecasting, scenario analysis was used so growth can be expressed as a base case with clear drivers, then flexes under tighter funding conditions or faster product adoption. Variables were projected with desk series first and then tuned using primary consensus, particularly around pricing pressure, regulatory timelines, and the pace of embedded finance expansion.

Data Validation & Update Cycle

Validation happened in layers, with model outputs compared against independent indicators like digital payment penetration direction, financing activity, and observable product pricing bands. When unusual jumps appeared, the assumptions were re-checked, and respondents were re-contacted if the variance could not be explained by a definitional change or a known one-off event.

Before sign-off, the work is reviewed in multiple analyst passes so inputs, conversions, and year alignment errors are caught early. The report is refreshed annually, and interim updates are made when material events occur, such as a major regulatory change or a sharp shift in funding and consumer activity. Right before delivery, a final update pass is performed so clients receive the latest market view.

Mordor Intelligence's Germany Fintech Market Size Versus Other Published Estimates

Published market sizes for Germany fintech can differ quite a lot because the term fintech gets used in different ways, and because some estimates mix ecosystem value, funding, or transaction volumes into what is presented as revenue. Differences also show up when the base year is not the same, or when exchange rates and inflation adjustments are applied in different time windows.

By tracking monetized fee and interest revenue streams and then refreshing take rate assumptions through re-contacts, Mordor Intelligence keeps the model tied to what fintech services actually earn in Germany, rather than counting company valuations or broad IT spend.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 14.57 B (2025) | |

| Global Research Publisher A | USD 17.55 B (2026) | Uses a later year and a wider service bucket that folds more open banking and embedded finance enablement revenue into the total, which can lift the number even if end-demand is similar. |

| Industry Data Blog B | USD 59.40 B (2024) | Reports ecosystem valuation in euros as of August 2024 (converted to USD here), so it reflects company value rather than annual fintech service revenue. |

The main takeaway from the comparison is that a revenue-based sizing and a valuation-based ecosystem snapshot will not reconcile, even if they describe the same country. Once scope is kept to annual fintech service revenue and the year is aligned, the market size can be traced back to adoption, pricing, and activity signals in a repeatable way.

Key Questions Answered in the Report

What is driving the rapid growth of the Germany fintech market?

Strong PSD2-enabled open banking, mobile-first consumer behavior, rising e-commerce volumes, and corporate treasury modernization together add roughly 10.8 percentage points to the market’s 14.71% CAGR.

Which fintech segment shows the highest revenue share today?

Digital payments held 37.65% Germany fintech market share in 2025, supported by pervasive contactless acceptance and embedded checkout rails.

Why is Insurtech expected to outpace other segments?

Automated claims, usage-based pricing and cloud-native underwriting push insurtech toward an 17.98% CAGR between 2026-2031, the fastest among all service propositions.

How do regulatory factors affect market entry?

BaFin’s licensing process can stretch to 18 months and subtract 1.5 percentage points from market CAGR, but it also builds a competitive moat for well-capitalized entrants.

Which regions in Germany act as fintech hubs?

Berlin dominates venture funding and start-up density, Munich specializes in insurtech collaborations, Frankfurt anchors B2B finance, while Hamburg and Cologne nurture retail-finance niches.

How are fintech providers addressing Germany’s cash-centric older population?

Hybrid solutions such as cash-in/cash-out partnerships and CBDC pilots allow providers to maintain cash accessibility while onboarding users to digital channels, mitigating the –2.0 percentage-point restraint on growth.

Page last updated on: