Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

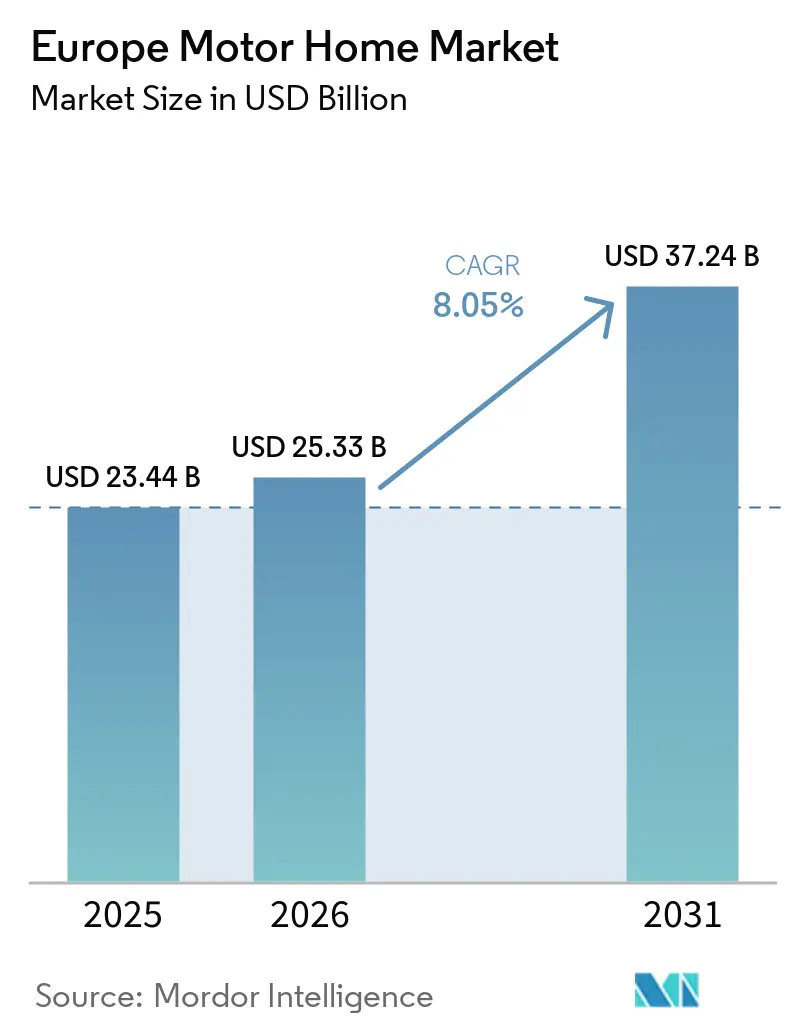

| Base Year Market Size (2025) | USD 23.44 Billion |

| Market Size (2026) | USD 25.33 Billion |

| Market Size (2031) | USD 37.24 Billion |

| Growth Rate (2026 - 2031) | 8.05% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Motor Home Market Analysis by Mordor Intelligence

The European motor homes market size in 2026 is estimated at USD 25.33 billion, growing from 2025 value of USD 23.44 billion with 2031 projections showing USD 37.24 billion, growing at 8.05% CAGR over 2026-2031. Market momentum outpaces the broader automotive landscape because Europeans are blending leisure, work, and mobility, choosing motorhomes over hotels for privacy, flexibility, and cost control. Aging baby boomers with healthy pensions favor comfort on the move, while digital nomads rely on on-board connectivity to extend trips beyond classic holiday windows. Regulatory emphasis on lower-emission transport channels EU funding toward campground electrification and public charging, lifting buyer confidence in emerging battery-electric formats[1]“Transport Infrastructure: Over EUR 352 Million of EU Funding to Boost Greener Mobility,” CINEA, cinea.europa.eu. Competition intensifies as platform-based rentals broaden access without upfront ownership, fueling unit volumes and giving manufacturers recurring fleet orders. The tight interplay between lifestyle shifts, environmental policy and digital retail puts the Europe recreational vehicle market on a structurally higher growth path than conventional passenger cars.

Key Report Takeaways

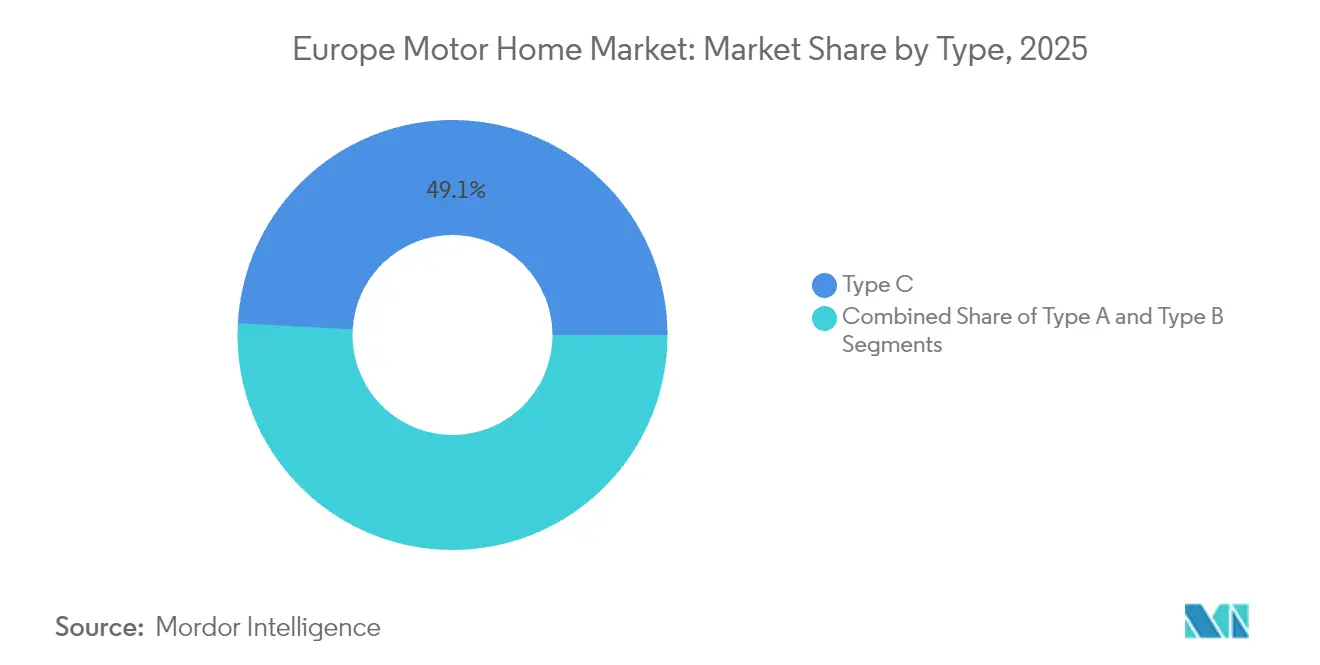

- By type, Class C motorhomes led with 49.12% of the European motor homes market share in 2025, while Class B campervans are forecast to expand at a 13.61% CAGR through 2031.

- By propulsion, diesel engines accounted for 87.65% share of the European motor homes market size in 2025, whereas battery-electric models are advancing at a 13.85% CAGR to 2031.

- By end user, direct individual buyers held a 70.62% of the European motor homes market share in 2025, and rental and sharing fleets record the highest projected CAGR at 11.05% during the outlook period.

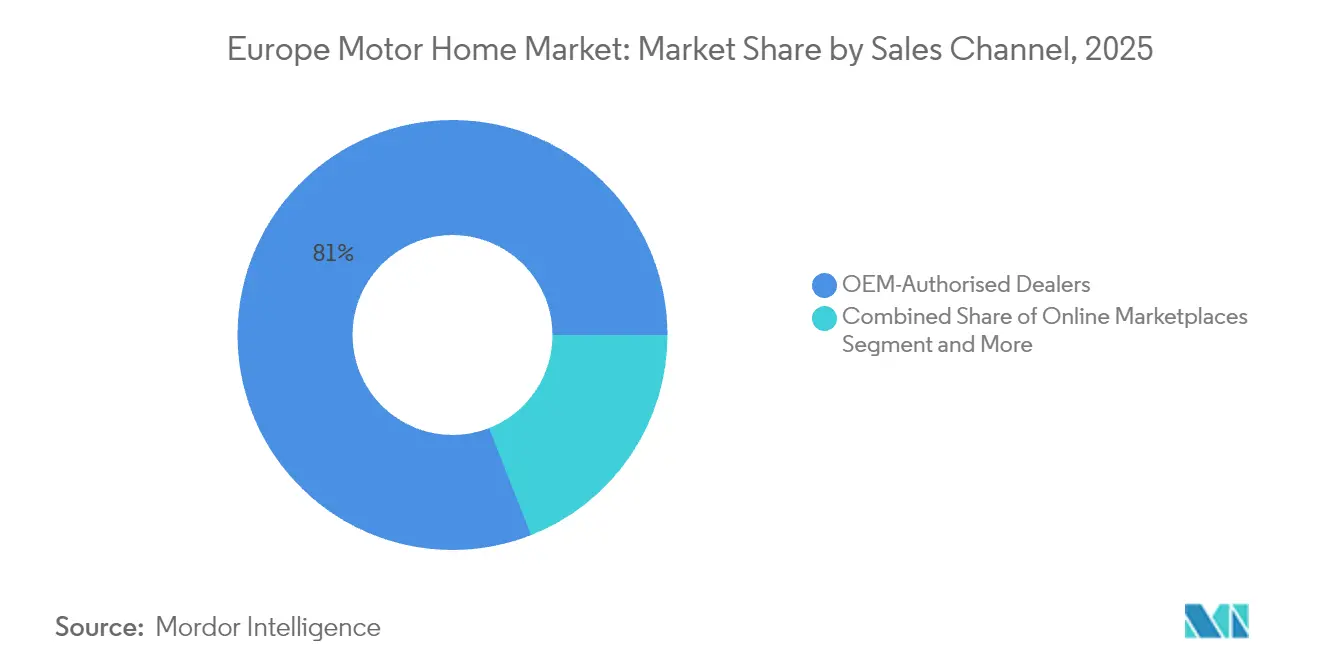

- By sales channel, OEM-authorized dealers controlled 80.95% of the European motor homes market share in 2025, yet online marketplaces are growing at a 10.3% CAGR to 2031.

- By length, units between 6 m and 7.5 m commanded 45.98% of the European motor homes market size in 2025, while sub-6 m formats are expanding at 8.7% CAGR.

- By country, Germany captured 41.90% of the European motor homes market share in 2025; Spain demonstrates the fastest regional CAGR of 8.72% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Motor Home Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Recreational Travel and "Staycation" Culture | +2.1% | Germany, France, Netherlands, United Kingdom | Medium term (2-4 years) |

| Aging Baby-Boomer Demographics | +1.8% | Germany, Italy, France, Spain | Long term (≥ 4 years) |

| Digital RV-Rental Marketplaces | +1.2% | Netherlands, Germany, Nordic countries, France | Short term (≤ 2 years) |

| Remote-Work Lifestyles | +0.9% | Nordic countries, Germany, Netherlands, Austria | Medium term (2-4 years) |

| Campground Infrastructure Upgrades | +0.8% | Southern Europe, Eastern Europe, Portugal, Greece | Medium term (2-4 years) |

| Nordic Wild-Camping Deregulation | +0.7% | Sweden, Norway, Finland, Denmark | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rapid Rise in Recreational Travel And "Staycation" Culture

In 2024, the European Union achieved a record milestone in tourism, with accommodations hosting over 3 billion nights. Higher domestic travel has lengthened average trips, reduced seasonality, and pushed camper demand into the shoulder months. Mediterranean destinations still attract 53% of campers, yet Nordic wild-camping gains traction as deregulation makes remote sites easier to access. Inflation and geopolitical risk redirect discretionary spending toward local journeys, reinforcing the appeal of privately owned or rented motorhomes. These patterns support sustained volume growth even during economic uncertainty.[2]"EU Tourism Hits Record 3 Billion Overnight Stays in 2024", Global Tourism Forum, worldtourismforum.net

Aging Baby-Boomer and Early-Retirement Demographics

Citizens aged 61-79 will represent one-fifth of Europe’s population in 2025, driving predictable demand because retirees prioritize comfort, health and cost control over speed. Seniors already account for nearly one-quarter of all EU tourism nights, frequently choosing vehicles they can drive year-round rather than paying for seasonal rentals. Extended retirement horizons enlarge the addressable base, while multi-generational trips bring younger relatives into the user pool. The demographic tailwind underpins long product cycles and stabilizes resale values, encouraging fresh purchases when pensioners upgrade to larger or electrified models suited for longer stays.

Expansion of Digital RV-Rental Marketplaces

Peer-to-peer apps remove the capital barrier that once narrowed participation to affluent households. Platform volume increases keep fleet utilization high and stimulate repeat bookings, which in turn persuade individual owners to list idle vehicles. Strong rental CAGR also creates bulk orders from fleet operators that negotiate standardized specs, offering manufacturers predictable runs and production scale. Online ecosystems reduce information gaps, streamline booking and elevate transparency on maintenance histories, adding liquidity to the secondary market and boosting overall transaction velocity.

Remote-Work Lifestyles Enabling Long-Term Mobile Living

Employees who can log in virtually choose vans that blend workstations, connectivity, and leisure amenities. Campervan registrations rose sharply after 2020 as urban professionals realized the flexibility to combine weekday work with weekend exploration, accelerating momentum in the recreational vehicle market. However, continuous connectivity and ergonomic design are essential to sustain adoption; thus, suppliers integrate 5G routers, solar arrays, and fold-out desks. Governments still finalize tax and residency frameworks for mobile workers, but initial ambiguity has not deterred trial adoption, showing that policy clarity could unleash additional latent demand.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Purchase and Maintenance Costs | -1.5% | Eastern Europe, Southern Europe, Portugal, Greece | Short term (≤ 2 years) |

| City-Level Diesel Bans | -0.8% | Germany, France, Netherlands, Italy | Medium term (2-4 years) |

| Limited Campsite Availability | -0.6% | Western Europe, Mediterranean regions, Alpine countries | Short term (≤ 2 years) |

| Oversupply-Led Price Depreciation | -0.4% | Germany, France, United Kingdom, Netherlands | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Upfront Purchase and Maintenance Costs

Pandemic-era supply constraints forced sticker prices up to one-third above pre-2020 levels, and though dealer negotiations soften the hit, affordability remains an acute barrier for first-time buyers. Running expenses climb as models add lithium batteries, heat pumps and driver-assist technology requiring specialized service tools. Eastern and Southern Europe feel the impact most because disposable incomes lag Western standards. Financing options are improving, yet fragmented across borders, leaving potential owners reliant on general automotive loans that rarely match RV depreciation curves.

City-Level Diesel Bans and LEZ Expansion Curbing Access

More than 300 European municipalities now restrict older diesels. Germany’s green sticker scheme and France’s Crit’Air vignette are emblematic. The diesel fleet, therefore, faces route planning headaches, especially when spontaneous detours run through restricted zones. Those constraints accelerate powertrain transition yet risk stranding owners whose vehicles still have useful life. Manufacturers able to homologate Euro VI or electric variants seize advantage, but resale prices of non-compliant units drop, weighing on new-buyer confidence.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Compact Campervans Challenge Traditional Dominance

Class C motorhomes represented 49.12% of Europe's motorhome market size in 2025, illustrating continued appetite for spacious interiors that meet family needs. However, Class B campervans are projected to post a 13.61% CAGR, reflecting rising urbanization and user desire for a single vehicle that can serve as both commuter and holiday home. Parking regulations and road-width limits in historic European centers tilt momentum to compact vans that fit standard spaces. Manufacturers leverage existing light-commercial platforms, reducing production cost and enabling faster electrification rollouts. The European motor homes market thus pivots toward versatility, drawing younger buyers who value maneuverability and smartphone-like digital interfaces.

Large Class A units still command premium pricing but confront infrastructure barriers: few campsites host >8 m rigs, and LEZ rules often exclude heavy chassis. To hedge, builders experiment with self-driving caravan axles that let towable units reposition autonomously within cramped plots. Across all categories, integrated solar, lithium storage, and app-based diagnostics shift buyer focus from raw square meters to energy autonomy and user experience, further blurring traditional type distinctions.

By Propulsion: Electric Transition Accelerates Despite Diesel Dominance

Diesel retains 87.65% of the European motor homes market share in 2025, explained by abundant refueling, torque, and proven reliability, yet battery-electric models show the fastest commercialization path with a 13.85% CAGR. EU plans for 3.5 million public chargers by 2030, plus campground-level grants, directly target the European motor homes market. Thor Industries’ hybrid Class A concept demonstrates 500-mile combined range, signaling impending breakthroughs in weight-to-energy ratios.

Gasoline remains a niche alternative for users wary of diesel bans but unwilling to commit to full electrification. Hybrid-electric drive trains bridge gaps, giving rural travelers charging flexibility without sacrificing payload. Designers shorten rear overhangs and lower floor height as battery density improves, correcting historic compromises that limited interior layouts on early electric prototypes. The propulsion mix is therefore poised for rapid rebalancing once residual-value confidence firms and public fast-charge coverage mature.

By End User: Rental Fleets Reshape Market Dynamics

Direct individual buyers dominated with a 70.62% of the European motor homes market share in 2025, yet rentals and sharing fleets expand at 11.05% CAGR, underscoring a shift from ownership to access. Platforms match idle assets with demand spikes, smoothing seasonal cycles and improving ROI for owners. For manufacturers, fleet ordering means large, repeat contracts and predictable specifications. Rental operators prioritize durability, standardization, and quick-turn maintenance, leading OEMs to design simplified interiors with wipe-clean surfaces and modular components.

Corporate, event, and hospitality fleets create specialized niches- mobile offices, VIP shuttles, and pop-up medical clinics diversify revenue streams and showcase technological features such as telematics and energy-independent HVAC. Over time, fleet units enter the secondary market, offering affordable entry points that cultivate new private owners. The segment’s virtuous cycle makes rental ecosystems an essential catalyst for Europe's motor homes market penetration.

By Sales Channel: Digital Platforms Disrupt Traditional Distribution

OEM dealers still account for 80.95% of the European motor homes market share in 2025, but online marketplaces post a 10.3% CAGR as shoppers demand price transparency and inventory breadth. COVID-era restrictions normalized virtual walk-throughs, 360° videos, and remote paperwork, making many first-time owners comfortable finalizing high-ticket purchases online. Dealers respond with omnichannel models that combine click-to-reserve with in-store handovers, turning showrooms into experience centers rather than inventory depots.

Direct-to-consumer programs surface mainly in luxury builds where factory visits and customization merit travel. Some manufacturers pilot AI chatbots that recommend layouts, options, and financing, guiding prospects through the configuration journey. Dealer consolidation accelerates because investments in diagnostic equipment, charging infrastructure, and training scale better across larger footprints, leaving smaller independents to specialize in service or retrofit.

By Length/Size: Compact Formats Gain Urban Advantage

RVs between 6 m and 7.5 m held 45.98% of the European motorhomes market size in 2025, balancing living space with highway handling. Units below 6 m grow at 8.7% CAGR because they slot into most municipal parking bays and incur lower ferry tariffs. Electric powertrains amplify the advantage: smaller bodies need fewer kilowatt-hours to achieve an acceptable range, freeing payload for passengers and gear.

Conversely, rigs over 7.5 m confront low bridge clearances, weight-class license hurdles, and campsite plotting fees. Norway’s proposal to let regular licenses cover up to 4,250 kg would ease barriers, yet adoption hinges on pan-European harmonization. For now, OEMs hedge by offering modular slide-outs that expand interior volume when parked, allowing shorter driving footprints without sacrificing comfort.

Geography Analysis

Germany captured 41.90% of Europe's motor homes market share in 2025, thanks to high household incomes, dense dealer networks, and mature campground infrastructure. Federal tax incentives and robust financing options support year-round usage beyond holiday peaks, while local production clusters shorten lead times and customize specs for regional preferences. Yet volume growth shows early signs of tapering because replacement rather than first-time purchases now drive sales. Southern neighbors France and Italy follow, leveraging Mediterranean coastlines and well-publicized domestic tourism campaigns. French operators benefit from 23,200 campsites, the continent’s largest network, keeping travel distances short and encouraging multi-stop itineraries that maximize daily spend.

Spain is the breakout story with a projected 8.72% CAGR to 2031. Post-pandemic infrastructure upgrades, relaxed overnight parking policies, and aggressive regional marketing reposition the country from a winter haven for Northern retirees to a year-round destination for domestic families. Nordic countries illustrate policy-led demand. Norway, Sweden, and Finland integrate wild-camping rights with high disposable incomes, pushing per-capita RV density above EU averages. Harsh winters constrain usage to seasonal windows, but advanced insulation, heated tanks and all-wheel-drive platforms extend practical itineraries.

Eastern Europe remains nascent yet promising. Poland, the Czech Republic and the Baltics upgrade highways and align vehicle taxation with EU norms, laying groundwork for volume expansion once disposable incomes rise. Consumers currently favor imported used inventory; nevertheless, domestic assembly plants could spawn as both labor advantage and local content rules appeal to global OEMs. Brexit complications dampen U.K. export flows to the continent, inadvertently reinforcing intra-EU supply chains and giving mainland producers a logistical edge.

Competitive Landscape

The European motor homes market shows moderate concentration. Trigano SA and Thor Industries lead, forming a duopoly at the top tier. Below them, family-owned brands and regional assemblers supply niche formats ranging from alpine-grade campervans to retro-inspired micro trailers. Leadership hinges on scale, distribution reach, and the ability to absorb electrification costs. Thor’s acquisition of Erwin Hymer Group elevated its European sales, lifting its share of motorcaravans and campervans and underscoring acquisition-driven growth.

Technology differentiates incumbents. Market leaders introduce hybrid drivetrains, 48-volt house systems, and over-the-air software updates that manage battery health, security, and predictive maintenance. Smaller rivals concentrate on bespoke cabinetry, thematic interiors, and locally sourced materials to stand out. Dealer consolidation accelerates because servicing high-voltage systems demands capital only larger groups can invest, squeezing independent outlets.

Partnerships with energy providers and telematics firms illustrate evolving ecosystem strategies. OEMs sign memoranda to equip campgrounds with brand-specific chargers that dispense loyalty points, subtly steering users to preferred networks. Subscription models covering maintenance, connectivity and insurance emerge, transforming one-time transactions into multi-year revenue streams. Manufacturers with balanced portfolios across diesel, hybrid and fully electric will likely capture share as policy pressure intensifies.

Europe Motor Home Industry Leaders

-

KnausTabbert GmbH

-

Thor Industries Inc.

-

Swift Group

-

Dethleffs GmbH & Co. KG

-

Trigano SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Thor Industries restructured Heartland Recreational Vehicles under Jayco Inc. to streamline costs and improve dealer support.

- September 2024: Thor Industries and Harbinger unveiled a hybrid Class A motorhome with a 140-kWh battery, rooftop solar and 500-mile range, targeting commercial launch in 2025.

- September 2024: Outdoorsy Group announced European expansion after surpassing USD 3 billion in platform sales, projecting USD 8 billion by 2029.

Europe Motor Home Market Report Scope

Motorhomes are used for vacation activities and festivals, concerts, and multi-day events. Motorhomes have the added advantage of reducing vacation costs by an average of 55% over other conventional vacation activities.

The European motorhomes market is segmented by type, end user, and country. By type, the market is segmented into class A, class B, and class C. By end user, the market is segmented into fleet owners, direct buyers, and other end users. By country, the market is segmented into Germany, United Kingdom, France, Italy, Spain, and Rest of Europe. The report covers the market size and forecast in value (USD) for all the above segments.

By Type

| Class A |

| Class B (Camper Van) |

| Class C (Alcove/Semi-integrated) |

By Propulsion

| Diesel |

| Gasoline |

| Hybrid |

| Battery-Electric |

By End User

| Direct Individual Buyers |

| Rental and Sharing Fleets |

| Corporate / Event and Hospitality Fleets |

By Sales Channel

| OEM-Authorized Dealers |

| Online Marketplaces |

| Direct-to-Consumer (Factory Delivery) |

By Length/Size

| Up to 6 m |

| 6 to 7.5 m |

| Above 7.5 m |

By Country

| Germany |

| France |

| United Kingdom |

| Italy |

| Spain |

| Netherlands |

| Sweden |

| Norway |

| Rest of Europe |

| By Type | Class A |

| Class B (Camper Van) | |

| Class C (Alcove/Semi-integrated) | |

| By Propulsion | Diesel |

| Gasoline | |

| Hybrid | |

| Battery-Electric | |

| By End User | Direct Individual Buyers |

| Rental and Sharing Fleets | |

| Corporate / Event and Hospitality Fleets | |

| By Sales Channel | OEM-Authorized Dealers |

| Online Marketplaces | |

| Direct-to-Consumer (Factory Delivery) | |

| By Length/Size | Up to 6 m |

| 6 to 7.5 m | |

| Above 7.5 m | |

| By Country | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Netherlands | |

| Sweden | |

| Norway | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe motor homes market in 2026?

The market is valued at USD 25.33 billion and is projected to reach USD 37.24 billion by 2031.

Which vehicle class is growing the fastest?

Class B campervans are advancing at a 13.61% CAGR due to compact size and urban drivability.

What share do diesel engines hold?

Diesel propulsion accounts for 87.65% of 2025 registrations, though electric variants are gaining traction.

Why is Spain the fastest-growing geography?

Infrastructure upgrades, relaxed parking policies and surging domestic tourism push Spain toward a 8.72% CAGR through 2031.

How are digital platforms changing sales?

Online marketplaces grow at 10.3% CAGR, fostering transparent pricing and cross-border inventory access that complement dealer showrooms.

What impact do Low Emission Zones have?

City diesel bans restrict older vehicles, pressuring owners to upgrade and accelerating the shift to hybrid and electric powertrains.

Page last updated on: