Europe Less-Than Container Load Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

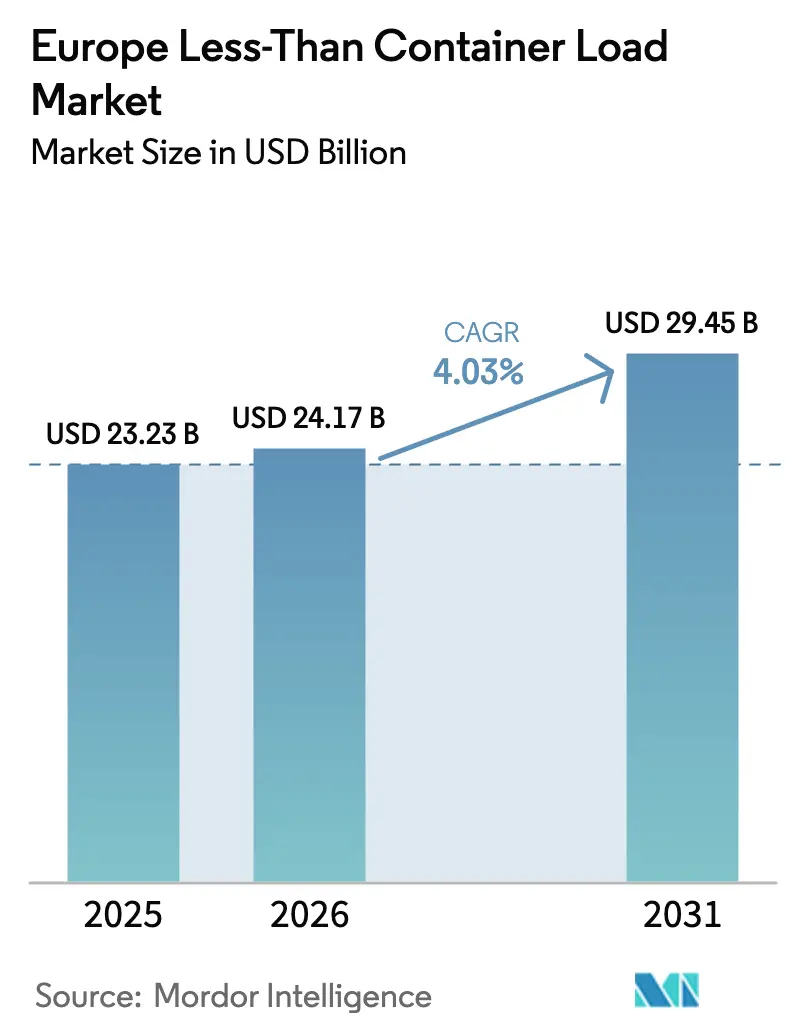

| Base Year Market Size (2025) | USD 23.23 Billion |

| Market Size (2026) | USD 24.17 Billion |

| Market Size (2031) | USD 29.45 Billion |

| Growth Rate (2026 - 2031) | 4.03% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Less-Than Container Load Market Analysis by Mordor Intelligence

The Europe Less-Than Container Load Market size is expected to grow from USD 23.23 billion in 2025 to USD 24.17 billion in 2026 and is forecast to reach USD 29.45 billion by 2031 at 4.03% CAGR over 2026-2031.

The solid growth outlook is underpinned by escalating cross-border e-commerce volumes, digital booking platforms that shrink lead times, and regulatory incentives that make ocean consolidation more attractive than air and road alternatives. A steady pipeline of green shipping corridors and the post-Brexit compliance burden are further tilting European shippers toward flexible LCL solutions that optimize container utilization while easing customs administration. Meanwhile, the sector is learning to manage higher carbon-pricing pass-throughs and port congestion that periodically stretch transit times yet also stimulate demand for inventory-buffering consolidation services.

Key Report Takeaways

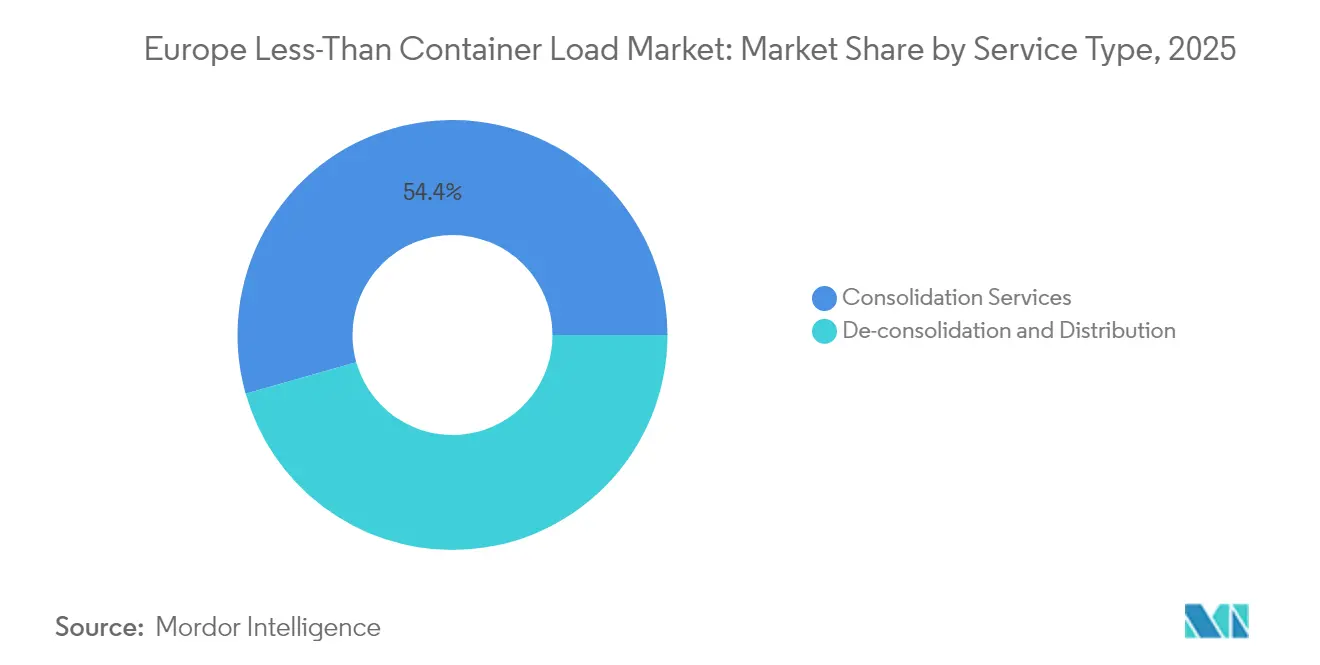

- By service type, consolidation services captured 54.40% of the Europe less than container load (LCL) market share in 2025, while de-consolidation and distribution is projected to expand at a 4.67% CAGR to 2031.

- By destination, international services accounted for 70.55% of the Europe less than container load (LCL) market size in 2025 and are poised to grow at a 4.26% CAGR through 2031.

- By nature of business, freight forwarding dominated with a 89.30% share in 2025 and is advancing at a 3.98% CAGR over the forecast period.

- By end user, retail and e-commerce led with a 31.60% revenue share in 2025; healthcare and pharmaceuticals record the fastest growth at a 5.15% CAGR to 2031.

- By geography, Germany held 15.70% of the Europe less than container load (LCL) market share in 2025, whereas Spain is set to rise at a 4.93% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Less-Than Container Load Market Trends and Insights

Drivers Impact Analysis*

| Driver | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce parcel surge boosts LCL demand | +1.2% | Global, early gains in Germany, Netherlands, UK | Medium term (2-4 years) |

| Digital freight platforms enable instant LCL booking | +0.8% | North & Central Europe, spill-over to Southern Europe | Short term (≤ 2 years) |

| EU ETS / Med-ECA compliance shifts freight from air & road to LCL | +0.9% | EU-wide, pronounced on Mediterranean lanes | Long term (≥ 4 years) |

| Post-Brexit customs complexity diverts UK flows to LCL services | +0.6% | UK-EU corridors, focused on Dover, Calais, Rotterdam | Medium term (2-4 years) |

| Asia-Europe green shipping corridors increase sailing frequency | +0.7% | Northern European ports, Eastern European hinterlands | Long term (≥ 4 years) |

| Resilience strategies after Red-Sea rerouting diversify entry ports | +0.5% | Mediterranean, Atlantic and Baltic gateways | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

E-commerce Parcel Surge Propels LCL Consolidation Demand

European parcel carriers moved 6.2 billion shipments during the 2024 holiday peak, a 9% jump that gave freight forwarders rich opportunities to aggregate smaller orders into containerized loads. Roughly 70% of that volume required direct-to-consumer delivery, encouraging providers to apply algorithmic matching that raises container fill rates and lowers handling costs. Chinese platforms alone sent 4.6 billion packets into Europe in 2024, magnifying the need for reliable LCL consolidation that can clear customs at scale. The EU plan to withdraw the EUR 150 duty-free threshold in 2025 will standardize declarations, strengthening the competitive position of LCL operators that already run integrated brokerage capabilities. Together these forces add structural tailwinds to the Europe less than container load (LCL) market[1]“Changes to the Existing ETS and MRV Applying from 1 January 2024,” European Commission, climate.ec.europa.eu.

Digital Freight Platforms Transform LCL Booking Infrastructure

Platforms such as Cargoboard and Shypple compress traditional quote cycles from several days to a few minutes, giving shippers on-demand price discovery and slot confirmation. Kuehne + Nagel’s myKN expands this capability with CO₂-neutral options and real-time tracking, contributing to the forwarder’s 15% revenue increase in Q1 2025[2]“New Requirements for EU-GB Imports from 31 January,” ICAEW, icaew.com. Algorithmic route design and machine-learning-driven capacity pooling consistently lift container utilization 20-30 percentage points above manual methods. Maersk flags digitalization as a top logistics theme for 2025, highlighting how automated workflows are redefining freight forwarding complexity. These advancements widen adoption of Europe less than container load (LCL) market solutions among small and midsized shippers that previously lacked purchasing leverage.

EU ETS Implementation Accelerates Modal Shift to LCL Services

The addition of maritime transport to the EU Emissions Trading System in 2024 obliges carriers to buy allowances covering 70% of emissions in 2025, climbing to full coverage in 2026. Ocean Network Express responded with an Environment Surcharge that aligns with both EU ETS and FuelEU Maritime rules. CMA CGM estimates the regulation inflates base freight rates by 7-8 EUR per 100 kg, a 75% rise that erodes air-cargo price parity. Because the per-unit carbon cost drops sharply when shipments are consolidated, the Europe less than container load (LCL) industry gains a comparative edge for medium-distance traffic once served by trucks or planes.

Asia-Europe Green Shipping Corridors Enhance Sailing Frequency

Public-private coalitions are building low-carbon corridors linking main Asian export hubs to northern Europe, prompting carriers to schedule more intra-European feeders to synchronize transshipment windows. Higher sailing frequency diminishes dwell times at consolidation points, raising service reliability for the Europe less than container load (LCL) market. The expansion extends hinterland reach into Eastern Europe, widening addressable demand among exporters seeking consistent weekly departures.

Restraints Impact Analysis*

| Restraint | (%) Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Port congestion & container shortages elevate transit variability | -1.1% | Hamburg, Antwerp, Rotterdam, other North European hubs | Short term (≤ 2 years) |

| Fragmented CFS infrastructure in Eastern Europe | -0.7% | Central & Eastern Europe, Balkan corridors | Long term (≥ 4 years) |

| Carbon-compliance surcharges narrow LCL price advantage | -0.8% | EU-wide, heavier on Mediterranean lanes | Medium term (2-4 years) |

| Rising insurance/security costs on high-risk routes | -0.6% | Red Sea, Black Sea, other high-risk corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Port Congestion Crisis Disrupts LCL Transit Reliability

Vessel wait times of 7–10 days at key consolidation hubs reflect yard utilization beyond 92%, pushing container dwell at Rotterdam past 9 days and stretching barge delays in Antwerp to 96-120 hours. Belgian strikes in early 2025 shut port access for 36 hours, cascading backlogs across Northern Europe. End-to-end lanes that once delivered in 45 days now require up to 90 days, pressuring inventory planning for users of the Europe less than container load (LCL) market.

Carbon-Compliance Surcharges Tighten Cost Parity

While consolidated loads dilute carbon fees, some deep-sea carriers levy blanket surcharges that raise all-in LCL rates by 8-10%, trimming but not eliminating the discount versus air freight. On Mediterranean routes the added cost narrows historical differentials, forcing LCL providers to sharpen vessel-space procurement and enhance cargo-mix optimization to preserve their value proposition within the Europe less than container load (LCL) market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Consolidation Services Dominate Market Share

Consolidation services captured 54.40% of 2025 revenue within the Europe less than container load (LCL) market, reflecting the core economics of aggregating multiple consignments into a single container move. Sophisticated matching engines on platforms including Ship4wd raise load factors, allowing forwarders to distribute cost savings to small and midsize exporters. The Europe less than container load (LCL) market size for consolidation is projected to expand steadily as algorithms cut empty slots and reduce manual planning time. De-consolidation and distribution, though smaller, post the fastest 4.67% CAGR thanks to the surge in last-mile e-commerce fulfillment that needs break-bulk capability close to consumption centers.

The segment’s evolution now incorporates AI-driven stowage plans that respect cargo affinity rules while squeezing every cubic meter, a capability especially attractive to high-value healthcare and temperature-sensitive loads. Import Control System 2, rolling to road and rail legs in 2025, raises data-quality thresholds, tilting business toward providers with seamless digital compliance. As carbon pricing tightens, consolidated voyages spread ETS costs across more shippers, strengthening the dominance of consolidation services in the Europe less than container load (LCL) industry.

By Destination: International Services Drive Market Growth

International lanes represented 70.55% of 2025 turnover, underlining Europe’s deep cross-border trade integration. The Europe less than container load (LCL) market size for international moves is forecast to grow at a 4.26% CAGR, buoyed by trade liberalization with Asia-Pacific and corridor diversification around the Red Sea disruption. Post-Brexit customs procedures add documentation layers that make consolidated services more cost-effective on UK-EU corridors.

Longer transit distances embedded in international moves command better margins and support premium add-ons such as CO₂-neutral offerings and time-definite agreements. Domestic LCL retains relevance in feeding hub ports and balancing inland distribution loops, yet its shorter haul and competitive truckload rates restrain expansion. As EU decarbonization turns road transport costlier, some intra-EU freight will convert to short-sea LCL, creating incremental upside for international-style operations inside the Europe less than container load (LCL) market.

By Nature of Business: Freight Forwarding Maintains Market Leadership

Traditional freight forwarders controlled 89.30% of 2025 revenue, validating their expertise in juggling consolidation, customs and multimodal orchestration. Digital layers such as myKN help incumbents scale visibility without losing relationship depth, underpinning a 3.98% growth trajectory. The Europe less than container load (LCL) market share of forwarders is bolstered by the April 2025 closing of DSV’s EUR 14.3 billion (USD 15.78 billion) purchase of DB Schenker, which lifts combined scale to 41.6 billion EUR (USD 45.91 billion) turnover.

NVOCCs play a smaller but strategically important role, offering dynamic pricing tied to spot indices and positioning themselves as neutrality custodians for logistics marketplaces. As compliance burdens rise, cargo owners lean on forwarders’ brokerage licenses and bonded facilities, reinforcing forwarder primacy in the Europe less than container load (LCL) industry. Yet competition heats as digital-native entrants leverage API-driven capacity pooling, compelling legacy players to accelerate tech investment.

By End User: Retail & E-commerce Leads Demand Generation

Retail and e-commerce produced 31.60% of 2025 billings, mirroring shifts toward omnichannel fulfillment that values smaller, more frequent restocks. Cross-border sellers favor consolidation to limit duty exposure while accessing continental delivery networks, a key growth driver for the Europe less than container load (LCL) market. Healthcare and pharmaceuticals top the growth charts at 5.15% CAGR, propelled by demand for GDP-compliant cold-chain services and pandemic-era re-shoring of critical supplies.

Manufacturing and automotive demand remains subdued amid excess capacity and tepid vehicle sales, but tightening working-capital targets motivate original equipment manufacturers to swap full container commitments for flexible LCL arrivals. Agricultural exporters turn to consolidation for seasonal pulses and specialty crops that cannot fill a 20-foot box alone, adding another layer of diversified demand in the Europe less than container load (LCL) market.

Geography Analysis

Germany’s 15.70% share confirms its anchor role in Northern Europe’s freight matrix even as port volumes retreat to 20-year lows because of competitiveness issues and limited digital adoption. The government’s investment push into rail-linked multimodal yards aims to regain momentum, yet in the interim shippers diversify to nearby Dutch and Belgian gateways, spreading Europe less than container load (LCL) market demand across the region. The United Kingdom, despite Brexit complexities, still channels sizeable LCL flows; mandatory safety and security declarations from January 2025 shift many small importers toward forwarders equipped with automated border-compliance engines.

Spain is the breakout performer, on track for a 4.93% CAGR through 2031 as carriers steer Asia-Europe services around Red Sea risks and unload at Mediterranean and Atlantic ports such as Valencia and Algeciras. France and Italy leverage domestic consumption and trans-Alpine feeder networks but wrestle with sporadic labor actions that dent schedule dependability. The Netherlands retains Rotterdam’s mega-hub status, yet dwell times averaging 9 days pressure consolidation timetables and spark modal reassessment for time-sensitive cargo.

Poland commands regional distribution despite a 30,000-50,000 driver deficit that tightens inland trucking capacity. Scandinavian nations advance maritime decarbonization with Denmark’s distance-based heavy-vehicle toll and Sweden’s electrified road pilots, moves that indirectly favor longer-reach sea consolidation solutions. Central & Eastern Europe offers white-space upside, though fragmented CFS standards hinder rapid penetration of the Europe less than container load (LCL) market. Russian participation remains constrained by sanctions that have reshaped continental trade corridors.

Competitive Landscape

Industry concentration is moderate, a level that fuels price competition yet still allows differentiated service niches. The April 2025 DSV-DB Schenker merger crowns a USD 45 billion-plus global heavyweight poised to integrate newly acquired air and sea capacity into its pan-European LCL network. Kuehne + Nagel sustains leadership through continuous tech investment, securing a Leader spot in Gartner’s 2025 3PL Magic Quadrant for its balanced vision and execution.

Digital natives such as Freightos, Shypple and Cargoboard scale rapidly by providing instant rate discovery and API connectivity into e-commerce checkout flows, a model that wins small-parcel merchants now priced out of air solutions. Strategic plays emphasize sustainability, with operators offering biofuel or book-and-claim mechanisms to shippers chasing science-based net-zero targets.

White-space opportunities lie east of the Elbe, where disjointed CFS capacity creates an opening for asset-light players to establish bonded facilities. Insurance premiums up 900% on Red Sea routes push volumes onto Cape of Good Hope rotations or rail-road combinations, requiring agile network redesign. In response, incumbents pilot machine-learning engines that rebuild consolidation plans in near real time, reinforcing technology as the decisive battleground in the Europe less than container load (LCL) market.

Europe Less-Than Container Load Industry Leaders

Vanguard Logistics

DSV

Geodis

CEVA Logistics

ECU Worldwide (Part of All Cargo Logistics)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: DSV completed its EUR 14.3 billion (USD 15.78 billlion) acquisition of DB Schenker, forming the world’s largest freight forwarder with projected DKK 9.0 billion synergy capture by 2028reliable road freight ETAs.

- March 2025: Radiant Logistics acquired Transcon Shipping, adding USD 75 million in coastal forwarding revenue and gateway strength in Los Angeles, New York and Chicago.

- January 2025: Ocean Network Express rolled out a Europe Environment Surcharge that consolidates EU ETS and FuelEU Maritime cost recovery.

- February 2024: AIT Worldwide Logistics purchased Lubbers Logistics Group, expanding European project cargo reach.

Europe Less-Than Container Load Market Report Scope

Less than container load shipping is a cost-effective and flexible form of international cargo shipment as it allows shippers to consolidate shipments with other customers for lower rates rather than ship individual shipments on an independent basis using full container loads or truckload services. It is also known as groupage because it is grouped with other goods. As a result, LCL shipping is designed for goods with a low or moderate volume. As a result, LCL is the popular way of shipping for small firms.LCL is more commonly accessible than FCL during peak season.

The market is segmented By Destination (Domestic and International), By End User (Manufacturing, Retail (Includes E-commerce), Healthcare and Pharmaceuticals, Agriculture, and Other End Users), By Country (Germany, United Kingdom, France, Italy, Spain, Russia, Netherlands, Poland, Rest of Europe)

A full study of the Europe Less-than Container Market, including current market trends, constraints, technical updates, and extensive information on key segments and the industry's competitive landscape. During the research, the influence of COVID-19 was also taken into account.

| Consolidation Services |

| De-consolidation and Distribution |

| Domestic |

| International |

| Freight Forwarding |

| NVOCCs |

| Manufacturing and Automotive |

| Retail and E-commerce |

| Healthcare and Pharmaceuticals |

| Agriculture and Forestry |

| Other End Users |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Netherlands |

| Poland |

| Scandinavia (Denmark, Sweden, Norway, Finland) |

| Central and Eastern Europe (Czechia, Slovakia, Hungary) |

| Russia |

| Rest of Europe |

| By Service Type | Consolidation Services |

| De-consolidation and Distribution | |

| By Destination | Domestic |

| International | |

| By Nature of Business | Freight Forwarding |

| NVOCCs | |

| By End User | Manufacturing and Automotive |

| Retail and E-commerce | |

| Healthcare and Pharmaceuticals | |

| Agriculture and Forestry | |

| Other End Users | |

| Geography | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Netherlands | |

| Poland | |

| Scandinavia (Denmark, Sweden, Norway, Finland) | |

| Central and Eastern Europe (Czechia, Slovakia, Hungary) | |

| Russia | |

| Rest of Europe |

Key Questions Answered in the Report

What is the 2026 value of the Europe less than container load (LCL) market?

The sector is valued at USD 24.17 billion in 2026 and is projected to climb to USD 29.45 billion by 2031.

Which service type leads LCL revenue in Europe?

Consolidation services hold 54.40% of 2025 revenue, far ahead of de-consolidation and distribution.

How will EU ETS affect LCL competitiveness?

Carbon pricing raises all-in ocean freight costs, but consolidation dilutes per-unit fees, making LCL more compelling than air or road.

Which geography is growing fastest?

Spain is forecast to expand at a 4.93% CAGR thanks to rerouted Asia-Europe flows and strong domestic demand.

What end-user segment is expanding quickest?

Healthcare and pharmaceuticals post a 5.15% CAGR due to heightened demand for temperature-controlled, GDP-compliant moves.

How concentrated is the competitive landscape?

With the top five providers controlling about 45% of revenue, the market scores 6 on a 1–10 concentration scale.

Page last updated on: