Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

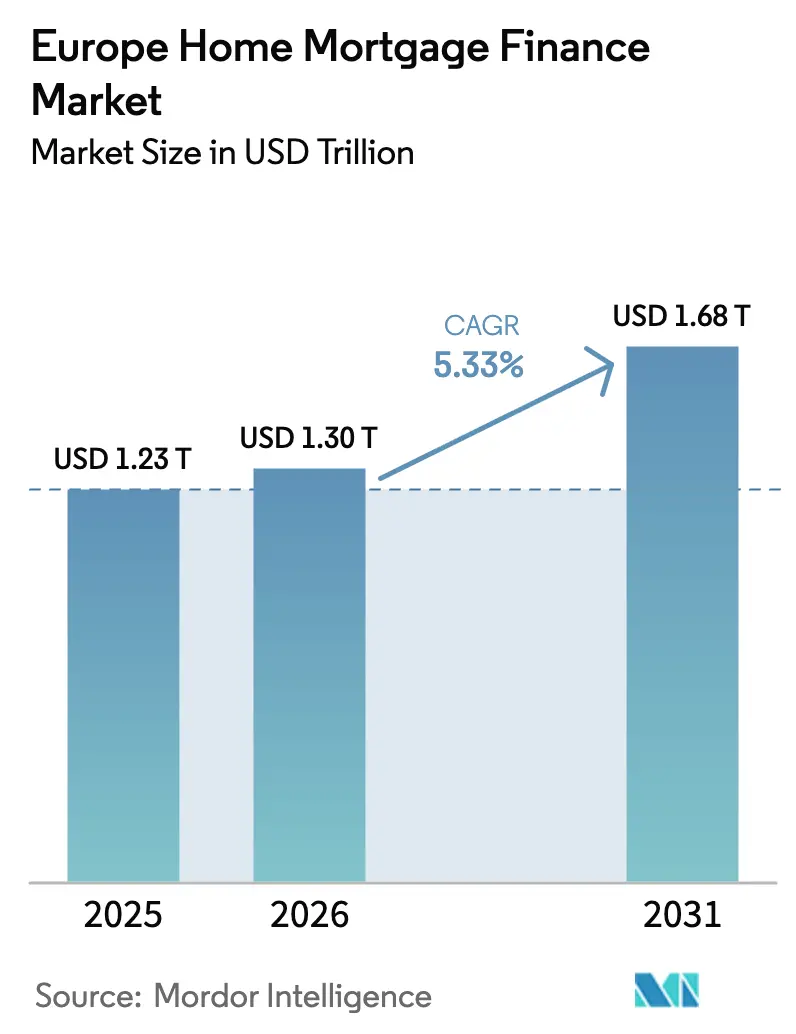

| Base Year Market Size (2025) | USD 1.23 Trillion |

| Market Size (2026) | USD 1.3 Trillion |

| Market Size (2031) | USD 1.68 Trillion |

| Growth Rate (2026 - 2031) | 5.33% CAGR |

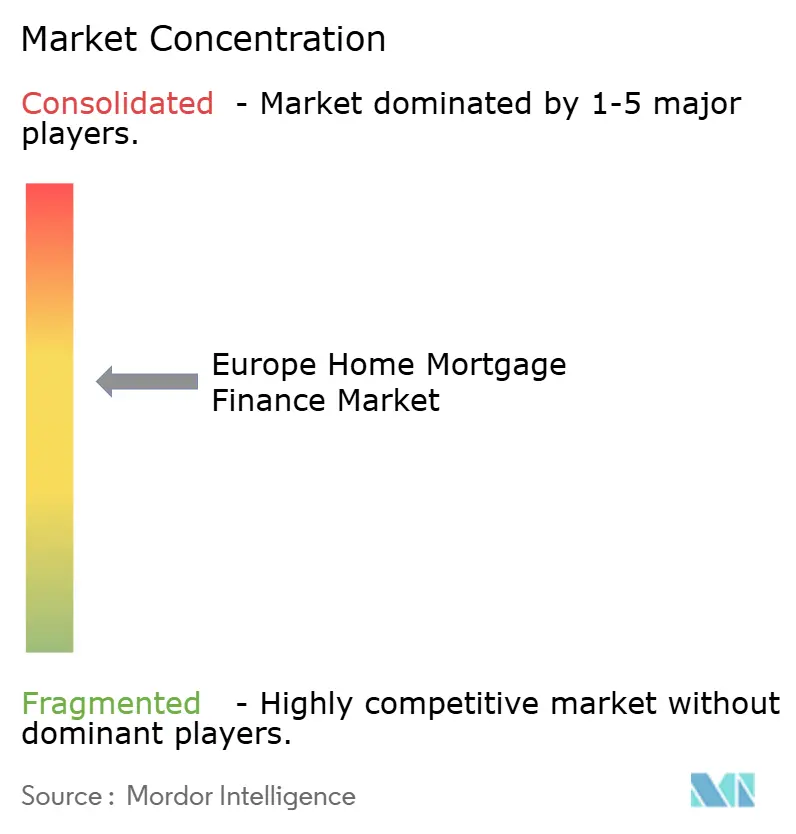

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Home Mortgage Finance Market Analysis by Mordor Intelligence

The Europe home mortgage finance market size is expected to grow from USD 1.23 trillion in 2025 to USD 1.30 trillion in 2026 and is forecast to reach USD 1.68 trillion by 2031 at 5.33% CAGR over 2026-2031. Relaxation in European Central Bank (ECB) policy, expanding green-mortgage incentives, and persistent housing-supply shortages underpin this steady growth[1]European Central Bank, “Monetary Policy Decisions Press Release,” ecb.europa.eu. Divergent monetary transmission across member states produces mixed rate environments: variable-rate borrowers in Italy and Spain feel rapid cost adjustments, whereas fixed-rate borrowers in France and Germany experience a slower pass-through. Government-backed guarantees such as Poland’s Bezpieczny Kredyt 2% or Germany’s KfW climate-retrofit loans continue to buffer affordability shocks and stimulate niche segments. Consolidation—illustrated by Santander’s pending takeover of TSB—reshapes competitive dynamics, while fintech entrants leverage open-banking rails to compress underwriting times and attract digitally savvy borrowers. Tighter climate-risk rules simultaneously restrict lending in flood-prone regions and unlock pricing advantages of 10–25 basis-point discounts for high-efficiency properties.

Key Report Takeaways

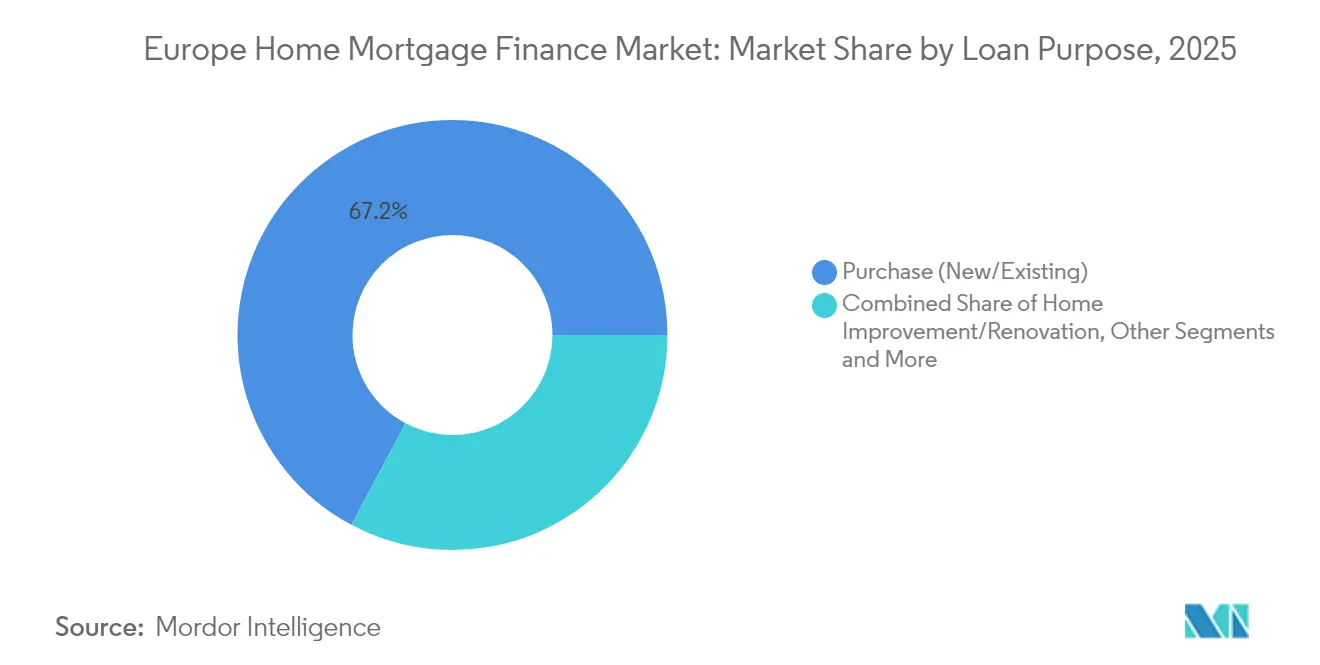

- By loan purpose, Purchase (New/Existing) held 67.21% of the European home mortgage finance market share in 2025, while Home Improvement/Renovation is projected to grow at a 6.55% CAGR through 2031.

- By provider, Banks accounted for 83.05% of the European home mortgage finance market size in 2025; Housing Finance Companies are expected to record the highest projected CAGR at 7.14% to 2031.

- By interest rates, Fixed Interest Rates led with a 77.02% share of the European home mortgage finance market in 2025, whereas Floating Interest Rates are forecasted to expand at 6.92% CAGR over 2026-2031.

- By loan tenure, mortgages exceeding 20 years represented 46.01% of the European home mortgage finance market size in 2025 and will advance at a 5.82% CAGR.

- By country, the United Kingdom captured 22.74% of the European home mortgage finance market share in 2025; Rest of Europe is the fastest-growing region, at a 6.28% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Home Mortgage Finance Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Low-interest-rate environment prior to ECB tightening | +1.2% | Eurozone core, UK spillover | Short term (≤ 2 years) |

| Government-backed mortgage guarantee schemes | +0.8% | Poland, Germany, UK | Medium term (2-4 years) |

| Rising household disposable income in core EU economies | +0.9% | Germany, France, Netherlands, Nordics | Medium term (2-4 years) |

| Housing-supply shortage in key urban centres | +1.1% | London, Paris, Amsterdam, Stockholm, Munich | Long term (≥ 4 years) |

| Growth of green mortgages tied to energy-efficient homes | +0.6% | Netherlands, Germany, France | Long term (≥ 4 years) |

| Open-banking-enabled instant underwriting | +0.4% | UK, Netherlands, Nordics | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Low low-interest-rate environment prior to the ECB tightening

Originated sub-2% loans still cover about 60% of outstanding balances, creating a two-tier borrower pool in the European home mortgage finance market. Households locked into ultra-cheap debt maintain spending power even as new entrants face rates near 4%. Borrowers in Italy and Spain with shorter fixed periods confront payment jumps of 150–200 basis points, whereas 77% of French mortgages carry fixed rates exceeding 15 years[2]Banque de France, “Retail Banking Survey 2025,” banque-france.fr. Lenders offset margin compression by repricing new loans and accelerating hedging strategies. Portfolio optimization—selling seasoned fixed-rate blocks and originating hybrids—strengthens risk-adjusted returns while preserving presence in the European home mortgage finance market.

Government-backed mortgage guarantee schemes

Poland’s Bezpieczny Kredyt 2% lowers effective rates from 8.46% to 2% for a decade, halving monthly payments and invigorating first-time-buyer demand. Germany’s KfW allocates EUR 762 million in 2025 toward energy-retrofit mortgages that blend fiscal support with climate goals. The United Kingdom’s scheme backed 39,000 purchases after its 2024 expansion, though proposed 99% LTV loans invite overheating concerns. Such programs narrow risk spreads, catalyze construction in eligible brackets, and inject countercyclical stability into the European home mortgage finance market.

Rising household disposable income in core EU economies

Spain posted an 8.2% jump in household disposable income for 2024 on broad wage gains. German inflation moderated to 1.3%, keeping real earnings positive despite construction-sector headwinds. Denmark’s 3.6% GDP growth, fueled by pharmaceuticals, lifted Nordic income trajectories. Debt-to-income ratios thus stabilized, anchoring sustainable origination volumes and underpinning growth across the European home mortgage finance market.

Housing supply shortage in key urban centers

German permits fell 31.9% year-on-year to 21,200 in April 2024, deepening a projected 700,000-unit deficit by 2025. London and Amsterdam see median first-time-buyer ages touching 34 and a tight rental vacancy, respectively. Lenders respond by stretching tenures beyond 25 years and rolling out income-stretch products that meet prudent affordability tests. Persistent scarcity keeps property values firm, enlarging collateral buffers and supporting asset-quality metrics across the European home mortgage finance market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| ECB interest-rate hikes raising borrowing costs | -1.8% | Eurozone; Italy & Spain variable-rate pools | Short term (≤ 2 years) |

| Tighter mortgage-affordability stress tests | -0.7% | UK, Netherlands, Nordics | Medium term (2-4 years) |

| Housing-price overvaluation risk in select markets | -0.5% | London, Amsterdam, Stockholm, Munich | Medium term (2-4 years) |

| Climate-risk regulations limiting lending in flood zones | -0.3% | Netherlands, Germany, UK coastal regions | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

ECB interest-rate hikes are raising borrowing costs

Average Italian payments climbed EUR 200–300 on EUR 150,000 loans in 2024, pushing 46% of mortgagors to cut consumption[3]BNP Paribas, “Italian Mortgage Outlook 2024,” group.bnpparibas. Floating-rate uptake reached 60.9% in Italy as fixed-rate premiums widened to 96 bps. As the ECB trims policy rates through 2025, refinancing appetites return yet remain above the ultra-low era’s benchmarks, re-anchoring price expectations across the European home mortgage finance market.

Tighter mortgage-affordability stress tests

Dutch rules capping loan-to-income upset decades-high demand even amid wage growth. UK lenders now stress at 300 bps above prevailing rates[4]Bank of England, “Mortgage Lender Statistics Q4 2024,” bankofengland.co.uk. Nordic supervisors monitor debt at 235% of disposable income in Norway. These prudential screens suppress marginal approvals but lift portfolio resilience, tempering expansion of the European home mortgage finance market without jeopardizing stability.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Loan Purpose: Renovation Finance Accelerates Energy Goals

Purchase (New/Existing) mortgages accounted for 67.21% of the European home mortgage finance market in 2025. The share reflects entrenched owner-occupation culture and a steady resale pipeline. Home Improvement/Renovation, however, carries a 6.55% CAGR outlook, outpacing all other purposes as EU energy-efficiency mandates channel households toward retrofits. The European home mortgage finance market size for renovation finance is poised to rise materially over 2026-2031, supported by EUR 150 billion yearly investment requirements under the Energy Performance Building Directive.

Demand for retrofit loans reshapes underwriting. Lenders must evaluate both future energy savings and collateral uplift. The EIB–Deutsche Bank program, worth EUR 600 million, illustrates how concessional capital crowd-in narrows borrowing costs for qualifying projects. Bundling renovation loans with subsidies underpins risk-adjusted returns, further embedding sustainability into the European home mortgage finance market.

By Provider: Agile Housing Finance Companies Erode Bank Hegemony

Banks retained 83.05% of the European home mortgage finance market size in 2025, leveraging deposit funding and multi-product cross-selling. Yet Housing Finance Companies eye a 7.14% CAGR thanks to specialized underwriting and digital origination. AI-powered platforms cut cost-to-income ratios and improve risk segmentation, letting newcomers capture niche borrowers overlooked by universal banks.

Incumbents counter with partnerships and core-banking upgrades. Santander’s cloud-native origination stack, deployed after the TSB integration, aims to process applications in under 48 hours. Fintech alliances provide speed and customer experience gains that help incumbent volumes grow alongside rising competition in the European home mortgage finance market.

By Interest Rates: Floating-Rate Revival Reflects Monetary Cycle Expectations

Fixed-rate mortgages commanded a 77.02% share of the European home mortgage finance market size in 2025. As traders price sequential ECB cuts, floating-rate loans forecast a 6.92% CAGR. The European home mortgage finance market share for floating products surged in Italy, moving from 15.8% to 60.9% in 12 months as spreads between fixed and variable widened to almost 100 bps.

Borrowers hedge via capped-rate options that limit upside risk while preserving downside participation. French culture still favors long fixed terms, maintaining stability within the European home mortgage finance market. Lenders manage basis risk through dynamic hedging and loan covenants that permit later rate conversions once policy easing materializes.

By Loan Tenure: Longer Terms Offset Affordability Strains

Loans beyond 20 years hold 46.01% of 2025 volumes and outpace other buckets at a 5.82% CAGR. Extended amortization pushes monthly payments down, supporting entry-level ownership even as prices climb. In costly capitals such as London, the median price-to-income exceeds 9x, making 30-year schedules commonplace.

Lengthening terms raises lifetime interest expense and duration risk. Supervisors now scrutinize borrowers’ retirement-age repayment capacity. Lenders adopt staged repayment features—stepped escalations or balloon options—to align cash-flows with life-cycle income, safeguarding credit quality across the European home mortgage finance market.

Geography Analysis

The United Kingdom leads with a 22.74% slice of the European home mortgage finance market. A diverse product landscape—tracker, offset, lifetime—supports granular segmentation, while mergers such as Santander–TSB augment scale. Regulatory reforms post-Brexit harmonize capital charges with Basel III, giving large lenders balance-sheet flexibility. Despite 2024 affordability stress testing, UK origination volumes remain resilient due to robust labor markets and pent-up housing demand.

Germany and France are structural pillars. Germany’s supply bottleneck, evidenced by permit collapse, intensifies competition for scarce stock and prolongs price appreciation. French markets benefit from a progressive decline in average mortgage rates—from 4.21% to 3.60% through 2024—stimulating refinancing even amid cautious consumer sentiment. Nordic lenders grow volumes despite subdued price rises; Nordea posted 6% growth in Q1 2025 mortgages, proving the region’s appetite for digitally enabled lending.

Spain and Italy provide cyclical upside. Spain’s 3.2% GDP expansion in 2024 bolstered house sales by 15% year-on-year. Italian credit conditions soften as banks deploy consolidation synergies; Intesa Sanpaolo facilitated EUR 30 billion medium/long-term lending over nine months of 2024, spurring mortgage growth. Rest of Europe, spanning Central and Eastern states, is the fastest growing at a 6.28% CAGR through 2031. Guarantee programs and EU funds accelerate formal credit penetration, widening the European home mortgage finance market reach. EIB-backed schemes in Latvia and large cross-border takeovers—like Erste Group’s stake in Santander Polska—provide capital and technology essential for rapid expansion.

Competitive Landscape

The European mortgage market exhibits moderate concentration with intensifying competitive dynamics driven by strategic consolidation and technological disruption. Santander’s USD 2.65 billion TSB deal lifts its UK mortgage assets to USD 45 billion, granting a 6% local share and better funding diversification. Nationwide’s proposed Virgin Money purchase would vault the mutual to second in deposits and mortgages, indicating that consolidation remains a favored route to cost efficiency. Cross-border acquisitions such as Erste Group’s EUR 6.8 billion stake in Santander Polska emphasize regional convergence aimed at digital infrastructure alignment.

Fintech challengers intensify pressure. Revolut intends to launch AI-assisted mortgages in 2025, combining open-banking data pulls with instant decision-making that undercuts incumbents on user experience. Traditional banks answer with internal buildouts: Legal & General Home Finance’s API rollout streamlines lifetime-mortgage processing, while ING’s granular green-pricing tool differentiates on sustainability.

White-space innovation also shapes rivalry. Lifetime and equity-release products address aging demographics, green mortgages command premium LTV pricing, and instant underwriting attracts younger borrowers. Institutions able to integrate ESG analytics and machine learning into credit models stand to gain a share of the European home mortgage finance market.

Europe Home Mortgage Finance Industry Leaders

Lloyds Banking Group

Banco Santander

BNP Paribas

Crédit Agricole

Barclays plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Santander completed its USD 2.65 billion acquisition of TSB, creating the UK’s fourth-largest mortgage provider and lifting combined mortgage assets to USD 45 billion.

- May 2025: Erste Group bought 49% of Santander Bank Polska for EUR 6.8 billion, enlarging its Central European mortgage book to EUR 131 billion.

- May 2025: ING launched tiered energy-label mortgage pricing in the Netherlands, linking rates to property efficiency from G through A++++.

- April 2025: The ECB’s lending survey showed 7% of banks eased housing-loan standards while net demand rebounded on lower rates.

Europe Home Mortgage Finance Market Report Scope

Housing finance is a type of lending service that offers money to purchase new properties, such as a home or land, to the end users. This helps individuals and businesses to purchase these housing properties without giving the entire buying price at once. The person borrowing this money repays the loan amount and interest up to the specified number of years.

The Europe home mortgage finance market is segmented by application (home purchase, refinance, home improvement, and others), by providers (banks, housing finance companies, and real estate agents), and by interest rate (fixed rate mortgage loan and adjustable rate mortgage loan). The report offers market size and forecasts for Europe Home Mortgage Finance Market in value (USD Million) for all the above segments.

By Loan Purpose

| Purchase (New/Existing) |

| Home Improvement/Renovation |

| Loan Against Property |

| Others (Construction, Refinance, etc.) |

By Provider

| Banks |

| Housing Finance Companies |

| Others |

By Interest Rates

| Fixed Interest Rates |

| Floating Interest Rates |

By Loan Tenure

| ≤ 10 Years |

| 11 – 20 Years |

| More than 20 Years |

By Country

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| Benelux (Belgium, Netherlands, and Luxembourg) |

| Nordics (Sweden, Norway, Denmark, Finland, and Iceland) |

| Rest of Europe |

| By Loan Purpose | Purchase (New/Existing) |

| Home Improvement/Renovation | |

| Loan Against Property | |

| Others (Construction, Refinance, etc.) | |

| By Provider | Banks |

| Housing Finance Companies | |

| Others | |

| By Interest Rates | Fixed Interest Rates |

| Floating Interest Rates | |

| By Loan Tenure | ≤ 10 Years |

| 11 – 20 Years | |

| More than 20 Years | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| Benelux (Belgium, Netherlands, and Luxembourg) | |

| Nordics (Sweden, Norway, Denmark, Finland, and Iceland) | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current value of the European home mortgage finance market?

The market is valued at USD 1.30 trillion in 2026 and is projected to reach USD 1.68 trillion by 2031.

Which country holds the largest share of the European home mortgage finance market?

The United Kingdom leads with a 22.74% share as of 2025.

Why are renovation loans growing faster than purchase loans?

EU energy-efficiency mandates and green-mortgage discounts of up to 25 basis points drive a 6.55% CAGR for Home Improvement/Renovation loans.

How do government guarantee schemes influence mortgage affordability?

Programs like Poland’s Bezpieczny Kredyt 2% cut effective rates from 8.46% to 2%, reducing monthly payments by about 50% for qualifying borrowers.

What technological changes are reshaping mortgage underwriting?

Open-banking integration and AI-powered platforms lower approval times from weeks to hours, improving borrower experience and risk assessment accuracy.

Are floating-rate mortgages becoming more popular?

Yes, as borrowers expect ongoing ECB rate cuts, floating-rate products are forecast to grow at 6.92% CAGR through 2031, particularly in Italy and Spain.

Page last updated on: