Europe Home Energy Management System Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

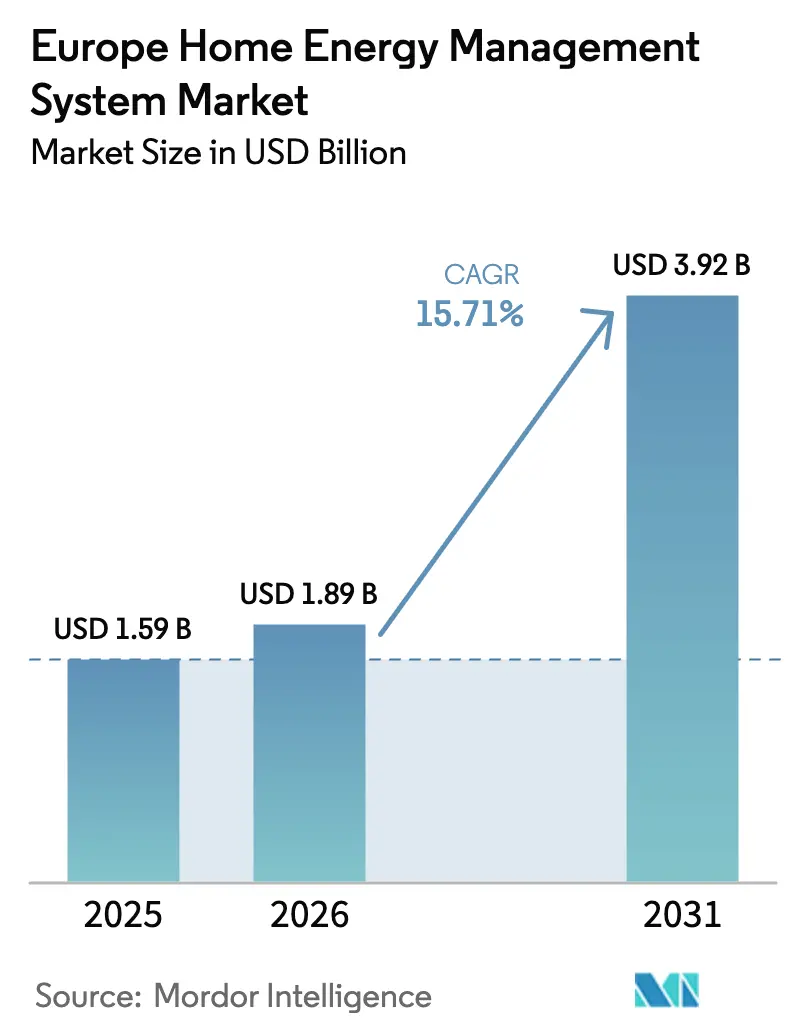

| Base Year Market Size (2025) | USD 1.59 Billion |

| Market Size (2026) | USD 1.89 Billion |

| Market Size (2031) | USD 3.92 Billion |

| Growth Rate (2026 - 2031) | 15.71% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Home Energy Management System Market Analysis by Mordor Intelligence

The Europe home energy management system market size is projected to be USD 1.59 billion in 2025, USD 1.89 billion in 2026, and reach USD 3.92 billion by 2031, growing at a CAGR of 15.71% from 2026 to 2031. Continuing deployment of smart meters is converting passive consumption data into dynamic price signals, which is steering households toward automated load-shifting tools. Persistent post-crisis electricity tariffs keep payback periods attractive for platforms that orchestrate heat pumps, electric vehicle chargers, and batteries. Protocol unification under Matter is reducing vendor lock-in and accelerating multiprotocol device onboarding. Utilities are pivoting beyond hardware toward cloud orchestration that monetizes residential flexibility in wholesale and ancillary-service markets. The confluence of these factors is nurturing an ecosystem in which software aggregation, not device sales, captures the largest share of value.

Key Report Takeaways

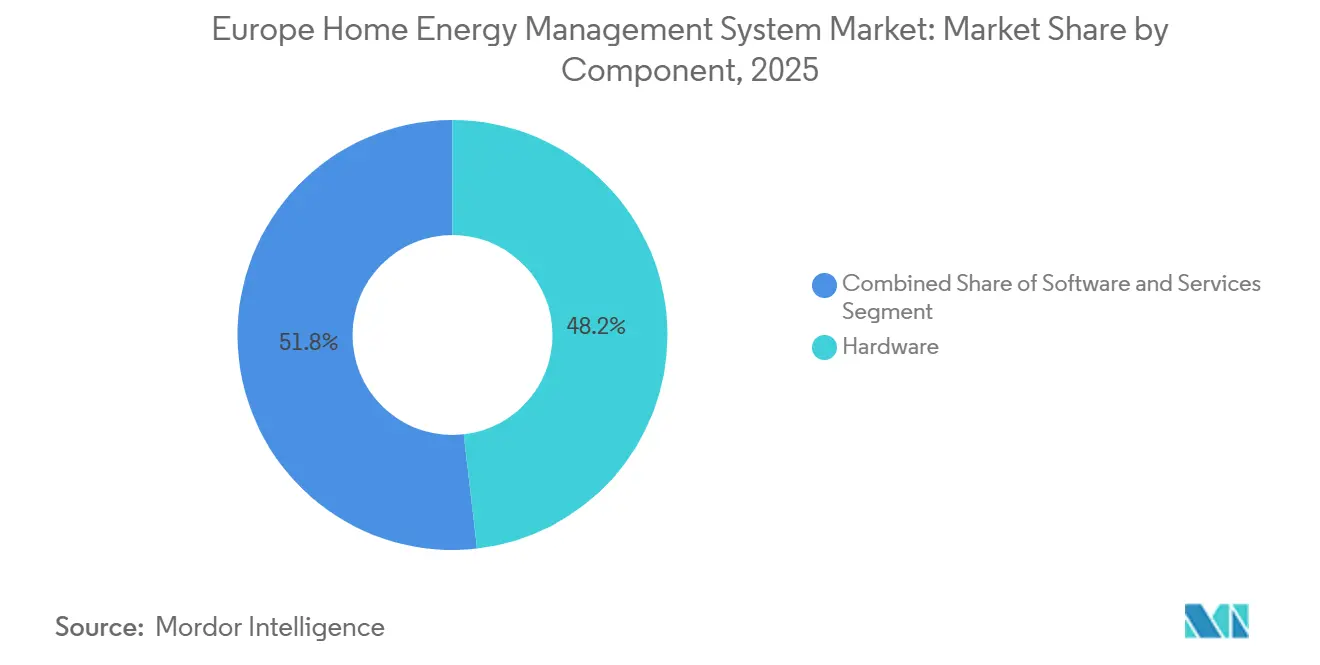

- By component, hardware led with 48.19% of the Europe home energy management system market share in 2025, while software is projected to expand at a 16.23% CAGR through 2031.

- By product type, lighting controls accounted for 37.28% of 2025 revenue, whereas self-monitoring systems and services are advancing at a 16.51% CAGR to 2031.

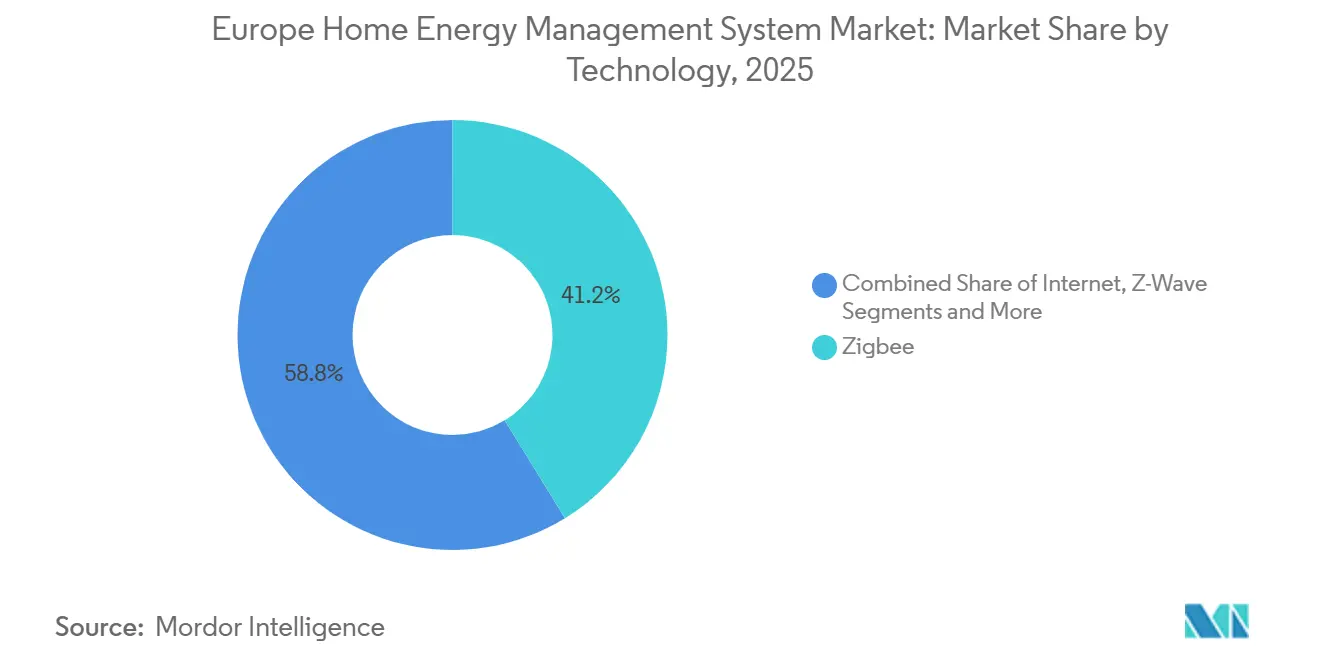

- By technology, Zigbee commanded 41.23% of 2025 revenue, and Thread is forecast to record the fastest growth at 16.67% over 2026-2031.

- By installation type, retrofit integrations represented 62.36% of 2025 deployments, yet new-build installations are poised to grow at a 16.06% CAGR through 2031.

- By geography, the United Kingdom held a 23.39% revenue share in 2025, while Spain is on track for the highest regional growth at 16.16% CAGR during the forecast window.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Home Energy Management System Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mandatory Smart-Meter Rollouts Under EU Clean Energy Package | +3.20% | Pan-European, with accelerated deployment in Germany, United Kingdom, France | Medium term (2-4 years) |

| Soaring Household Electricity Prices Post-Energy Crisis | +2.80% | Germany, United Kingdom, Spain, Italy | Short term (≤2 years) |

| Residential Electrification (Heat Pumps and EV Chargers) Needing Load Orchestration | +2.50% | Northern Europe (Nordics, Germany, Netherlands), expanding to France and United Kingdom | Medium term (2-4 years) |

| Solar plus Battery Bundling Unlocking Behind-the-Meter Optimisation | +2.10% | Spain, Germany, Italy, Southern France | Medium term (2-4 years) |

| Utility-Led Demand-Response Incentive Programmes | +1.90% | United Kingdom, Germany, Netherlands, pilot programs in France | Short term (≤2 years) |

| Retail-Energy Flexibility Trading Revenue Streams for Prosumers | +1.60% | United Kingdom, Germany, Spain (post-2024 regulatory reform) | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Mandatory Smart-Meter Rollouts Under the EU Clean Energy Package

Eighty percent household coverage before 2026 is locking in a digital substrate that transmits half-hourly consumption data over secure backbones, allowing retailers to publish granular tariffs that fluctuate with wholesale prices.[1]European Commission, “Clean Energy for All Europeans Package,” energy.ec.europa.eu Germany crossed the threshold in early 2025, converting smart-meter rollouts into dynamic tariff offers that sharpen consumer demand for automated controllers capable of pre-programmed load shifting. The United Kingdom’s 57 million installations illustrate scale, yet lingering interoperability issues with early SMETS1 devices highlight the value of platform-agnostic software capable of abstracting hardware quirks. France’s Linky meters achieved national coverage in 2024, but the slower uptake of dynamic tariffs left room for challenger suppliers using home energy management bundles to win share. Spain, already above a 70% smart-tariff penetration rate, demonstrates how policy clarity directly correlates with a double-digit growth trajectory in the Europe home energy management system market. Across the region, smart-meter ubiquity is no longer a forecast variable; it is an operational reality that anchors automated flexibility services.

Soaring Household Electricity Prices

German households paid EUR 0.42 per kWh (USD 0.47 per kWh) in Q1 2025, still 60% higher than pre-crisis levels, intensifying consumer focus on cost-saving automation.[2]International Energy Agency, “Heat Pumps,” iea.org British tariff caps reached GBP 0.28 per kWh (USD 0.36 per kWh), and customers on Agile products realized documented annual savings of GBP 180 (USD 230) by aligning device cycles with intraday price valleys.[3]Octopus Energy, “Agile Octopus Half-Hourly Tariff,” octopus.energy Peak-to-off-peak spreads in Spain widened to EUR 0.15 per kWh (USD 0.17 per kWh), amplifying arbitrage opportunities for battery-equipped households. Elevated retail rates compress the payback period for hardware bundles that combine thermostats, circuit-level monitors, and cloud software, converting price pressure into an adoption catalyst across the Europe home energy management system market.

Residential Electrification Requiring Load Orchestration

Europe installed 3.2 million heat pumps in 2024 and counts 2.8 million residential EV charge points by end-2025. Simultaneous peak-time operation strains distribution feeders, motivating distribution system operators to compensate flexible households that allow remote modulation. Germany’s §14a EnWG affords utilities curtailment rights, creating an economic signal for consumers to adopt controllers capable of pre-heating or deferred EV charging. The United Kingdom’s Demand Flexibility Service enrolled 1.4 million homes by winter 2025, paying participants GBP 100 (USD 128) for seasonal curtailment events. Such programs externalize grid value to the residential edge and reinforce the strategic relevance of orchestration software.

Solar plus Battery Bundling Unlocking Behind-the-Meter Optimization

Residential solar additions hit 7.8 GW in 2024, and battery attachment rates climbed to 35%. German feed-in tariffs dropped to EUR 0.082 per kWh (USD 0.092 per kWh), one-fifth of retail pricing, thereby incenting storage plus software combinations that maximize self-consumption margins. Spain’s collective self-consumption rules permit shared generation credits, pushing homeowners toward cloud platforms that calculate optimal charge-discharge allocations among neighbours. Sonnen reports 68% of its battery customers subscribe to a flexibility tariff that trades stored power in wholesale markets. Aggregation business models that monetize beyond-the-meter resources are amplifying demand for interoperable orchestration and are reinforcing the Europe home energy management system market growth outlook.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Hardware Cost vs Traditional Controls | -1.80% | Southern Europe (Spain, Italy, Portugal), Eastern Europe | Short term (≤2 years) |

| Fragmented Device Standards (Zigbee, Thread, Matter, etc.) | -1.30% | Pan-European, particularly affecting retrofit installations | Medium term (2-4 years) |

| Consumer Cyber-Privacy Concerns on Granular Load Data | -0.90% | Germany, France, Netherlands, privacy-conscious Northern Europe | Medium term (2-4 years) |

| Slow Roll-Out of Dynamic Tariffs in Several EU States | -0.70% | Southern Europe (Italy, Portugal, Greece), Eastern Europe | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

High Upfront Hardware Cost vs Traditional Controls

A full home energy management kit costs EUR 800-1,500 (USD 900-1,690), whereas a basic programmable thermostat is EUR 150-250 (USD 169-281). Households in Spain, Italy, and Portugal, with lower disposable income and flatter tariffs, often perceive a five-year payback as too lengthy. A 2025 survey showed 48% of Spanish respondents citing cost as the primary barrier to adoption. Subscription models that waive device payments in exchange for EUR 10-15 (USD 11-17) monthly service fees are emerging, exemplified by tado and Hive bundles, and are broadening penetration but cannot yet neutralize the restraint in the southern tier markets.

Fragmented Device Standards

Zigbee, Z-Wave, Thread, Wi-Fi, and proprietary stacks coexist, generating compatibility headaches that inflate installer labour and inventory costs. Matter 1.3 certification finally includes energy-centric device classes, but legacy sensors are not firmware-upgradable, obliging dual-radio gateways that add EUR 80-120 (USD 90-135) to bill-of-materials. A 2025 alliance survey found 37% of consumers experiencing pairing failures, prompting 29% to retreat into single-vendor ecosystems. Until retrofit gateways reach commodity costs, standards fragmentation will continue to subtract percentage points from the Europe home energy management system market CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Monetizes Flexibility

Hardware retained 48.19% of 2025 spending because sensors, smart plugs, and gateways are prerequisites for data capture, yet growth momentum has pivoted to cloud platforms that orchestrate these assets. Software revenue climbs at 16.23% through 2031 as aggregators bundle algorithms, demand-response enrolment, and wholesale market bidding into monthly subscriptions. This revenue mix shift elevates recurring income, deepening vendor margins and attracting venture capital inflows across the Europe home energy management system market. Services, covering installation and remote monitoring, ride the same vector as households outsource technical complexity.

Early dynamic tariff adopters require software that forecasts price curves and schedules pre-heating cycles thirty minutes before peak events. Octopus processed 2.4 billion half-hourly reads in 2025 and optimized 180,000 distributed batteries, demonstrating how code rather than copper is the locus of differentiation. Schneider Electric reported software and services contributing 34% of its home segment sales in fiscal-2024, underscoring the sector’s monetization advantage.

By Product Type: Self-Monitoring Platforms Outpace Legacy Lighting Systems

Lighting controls kept 37.28% revenue share in 2025 due to early consumer familiarity, yet they deliver limited tariff arbitrage. Self-monitoring platforms, expanding at 16.51% per year, embed circuit-level meters, tariff APIs, and mobile dashboards, enabling prosumers to chase intraday spreads and curtail phantom loads, thereby increasing the Europe home energy management system market size associated with software subscriptions. Thermostats, once the flagship device, now saturate Northern Europe, shifting incremental sales to Southern and Eastern corridors.

Advanced central controllers integrate HVAC, EV charging, and storage, performing as the digital conductor of multi-load households. Tado’s Auto-Assist subscription attracted 42% of its user base, converting a hardware installed base into EUR 18 million (USD 20 million) of recurring revenue in 2025. Netatmo’s Matter-ready thermostat fed 19% year-on-year connected-product sales growth at Legrand, evidencing consumer demand for standards-compliant devices that slot into broader ecosystems.

By Technology: Thread Rises Under Matter Umbrella

Zigbee commanded 41.23% in 2025 after a decade of incumbency, but Thread grows at 16.67% on the back of IPv6 support and Matter endorsement. Border routers embedded in mass-market smart speakers create zero-cost gateways, accelerating Thread household penetration and expanding the Europe home energy management system market share for low-power mesh devices. Z-Wave holds niche security applications owing to its 868 MHz spectrum which avoids Wi-Fi congestion.

Thread Group certified 350-plus products by mid-2025 and saw 12 million border routers ship in 2024, a 140% leap year-on-year. Matter 1.3 brought EV chargers and heat pumps under a common schema, extending interoperability from lighting to high-value loads, a milestone expected to keep Thread on its upward trajectory.

By Installation Type: Retrofit Dominant, New-Build Momentum Builds

Retrofit accounted for 62.36% deployments in 2025; Europe’s aging housing stock lacks built-in data buses and therefore relies on wireless add-ons. Wireless sensors and power-line communication adapters cut installation labour and keep the Europe home energy management system market accessible to existing dwellings. Devolo’s Magic adapters, which exploit existing wiring, garnered 38% retrofit sales share in 2025.

Building codes are turning new-build projects into smart-ready canvases. Germany’s Building Energy Act mandates controllable loads in new homes, while France’s RE2020 regulation accelerates thermostat uptake to meet carbon targets. Pre-installation economies trim gateway costs by up to 40%, and greenfield neighbourhoods increasingly market net-zero credentials that presuppose orchestrated energy controls.

Geography Analysis

The United Kingdom led with 23.39% of 2025 revenue, underwritten by the continent’s deepest smart-meter penetration and a competitive retail landscape where 15 suppliers’ market dynamic tariffs. Agile tariff enrolment exceeded 400,000 households by mid-2025, and a vibrant developer community built third-party apps atop the Kraken API, reinforcing the United Kingdom’s pole position in the Europe home energy management system market. Policy parity arrived via the 2024 Energy Security Bill which obliges every supplier to launch at least one time-varying tariff, cementing future demand for orchestration platforms.

Germany’s growth narrative centers on statutory curtailment rights under §14a EnWG. E.ON added 1.2 million connected-home clients and delivered 180 MW of flexible capacity in winter 2024-2025, equivalent to a mid-sized peaker plant. Deutsche Telekom cross-sold Magenta SmartHome services to 18% of broadband customers by end-2025, confirming that telecoms now rival utilities in home-energy value capture.

Spain, the forecast pacesetter at 16.16% CAGR, benefits from self-consumption legislation and a solar boom that necessitates bidirectional storage controls. Enel X’s JuiceNet platform recruited 35,000 Spanish households by mid-2025, paying EUR 120 (USD 135) per year for grid services and compressing payback periods for hardware. France, the Netherlands, and Nordics post high single-digit growth as tariff reforms and electrification accelerate, while Eastern Europe lags pending regulatory convergence under Fit for 55.

Competitive Landscape

No vendor exceeds 8% share, aligning the Europe home energy management system market with a moderate concentration profile. Legacy automation majors such as Schneider Electric, Honeywell, and Johnson Controls compete with pure-play specialists (tado, Netatmo), retailer platforms (Octopus Kraken, OVO Zero Carbon), and battery aggregators (sonnenCommunity). Differentiation is migrating from device specifications to algorithm-driven flexibility services.

Vertical integration is intensifying utilities scoop up technology assets to retain customer touchpoints, exemplified by E.ON’s 2025 launch of a proprietary cloud optimizer and Schneider Electric’s partnership with Volkswagen for bidirectional EV charging. Horizontal interoperability alliances are equally pivotal; Bosch Smart Home, for instance, collaborates with utilities, device manufacturers, and platform providers to ensure seamless integration across multi-vendor home energy ecosystems.

Honeywell, and ABB all secured Matter certification in 2025, future-proofing device lines and mitigating standards risk. Thermondo’s heat-pump-as-a-service model, funded with EUR 50 million Series C in early 2025, underscores venture appetite for subscription hardware plays that wrap installation, maintenance, and software into one fee, further reshaping competitive boundaries.

Europe Home Energy Management System Industry Leaders

Schneider Electric

Eaton Corporation

ABB Group

GE Electric

Honeywell International Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Carrier Global and Google Cloud formed a partnership to develop AI-powered HEMS that couple Carrier’s battery-enabled HVAC systems with WeatherNext forecasting to enhance grid resilience.

- March 2025: WeaveGrid and Emporia Energy integrated utility-managed EV-charging programs with home energy platforms for automated renewable-aligned charging schedules.

- February 2025: The German Bundesrat approved accelerated smart-meter rollout provisions including installation price caps and expanded consumer choice.

- February 2025: ABB and Samsung Electronics demonstrated SmartThings Pro connectivity with ABB InSite at Integrated Systems Europe 2025, highlighting real-time appliance control.

Europe Home Energy Management System Market Report Scope

The Europe Home Energy Management System Market Report is Segmented by Component (Hardware, Software, Services), Product Type (Lighting Controls, Self-Monitoring Systems and Services, Programmable Communicating Thermostats, Advanced Central Controllers, Intelligent HVAC Controllers), Technology (Zigbee, Wi-Fi, Internet, Z-Wave, Others), Installation Type (New-Build, Retrofit), and Geography (United Kingdom, Germany, France, Spain, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

| Hardware |

| Software |

| Services |

| Lighting Controls |

| Self-Monitoring Systems and Services |

| Programmable Communicating Thermostats |

| Advanced Central Controllers |

| Intelligent HVAC Controllers |

| Zigbee |

| Wi-Fi |

| Internet |

| Z-Wave |

| Others |

| New-Build |

| Retrofit |

| United Kingdom |

| Germany |

| France |

| Spain |

| Rest of Europe |

| By Component | Hardware |

| Software | |

| Services | |

| By Product Type | Lighting Controls |

| Self-Monitoring Systems and Services | |

| Programmable Communicating Thermostats | |

| Advanced Central Controllers | |

| Intelligent HVAC Controllers | |

| By Technology | Zigbee |

| Wi-Fi | |

| Internet | |

| Z-Wave | |

| Others | |

| By Installation Type | New-Build |

| Retrofit | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

How large will residential software revenues become within the Europe home energy management system market by 2031?

Software is on track for the fastest growth at a 16.23% CAGR, making it the primary value pool even though hardware still dominates volumes.

Which technology will replace Zigbee in new European smart-home installations?

Thread is the leading successor, advancing at 16.67% per year due to Matter endorsement and IPv6 compatibility.

What drives Spain's leadership in growth for connected-home energy platforms?

Self-consumption regulations from Royal Decree 244/2019 and rapid solar plus storage adoption propel a 16.16% CAGR, the highest in the region.

Why are utilities investing in virtual power plant models?

Aggregating residential flexibility lets utilities offset peaker capacity and monetize wholesale market opportunities without owning generation assets.

What obstacle most restricts adoption in Southern Europe?

High upfront costs relative to income and slower deployment of dynamic tariffs lengthen payback periods, deterring households from purchasing full HEMS bundles.

How does Matter improve device interoperability?

Matter defines a common application layer across Thread, Wi-Fi, and Ethernet, allowing devices from multiple brands to pair quickly and participate in unified automation routines.

Page last updated on: