Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

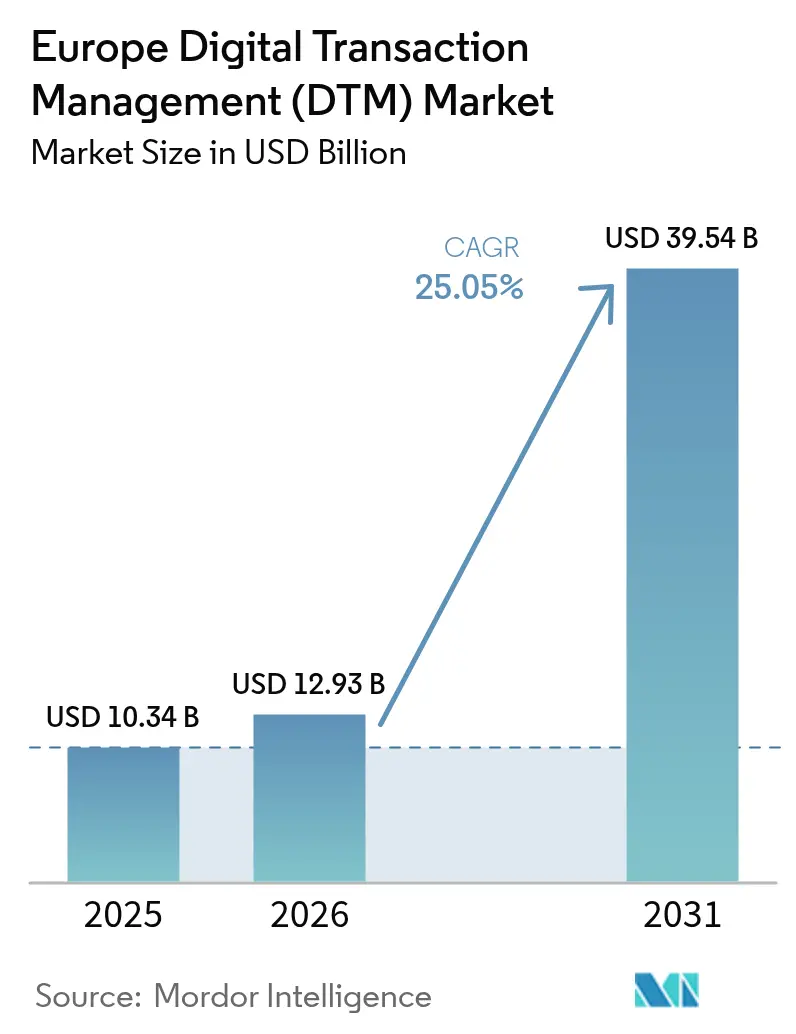

| Base Year Market Size (2025) | USD 10.34 Billion |

| Market Size (2026) | USD 12.93 Billion |

| Market Size (2031) | USD 39.54 Billion |

| Growth Rate (2026 - 2031) | 25.05% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Digital Transaction Management (DTM) Market Analysis by Mordor Intelligence

Europe Digital Transaction Management market size in 2026 is estimated at USD 12.93 billion, growing from 2025 value of USD 10.34 billion with 2031 projections showing USD 39.54 billion, growing at 25.05% CAGR over 2026-2031. This growth reflects the synchrony of stringent EU-level mandates and a work culture that now defaults to remote, paper-free interactions. Continuous regulatory pushes such as eIDAS 2.0, the January 2025 instant-payment rule, and phased B2B e-invoicing deadlines are steering every corporate workflow toward fully digital rails. Enterprises view compliance readiness, real-time processing speed, and pan-European identity interoperability as strategic, not optional, thereby sustaining double-digit spending momentum on platform modernisation. Competitive intensity is rising as European specialists inject local trust-service expertise into a landscape long dominated by a few global providers, while private equity interest signals confidence in decades-long secular adoption. Cyber-risk, funding gaps among smaller firms, and fragmented national eID schemes could temper the upward trajectory, yet they are unlikely to derail it because most new legislation embeds non-negotiable digital requirements into daily trade.

Key Report Takeaways

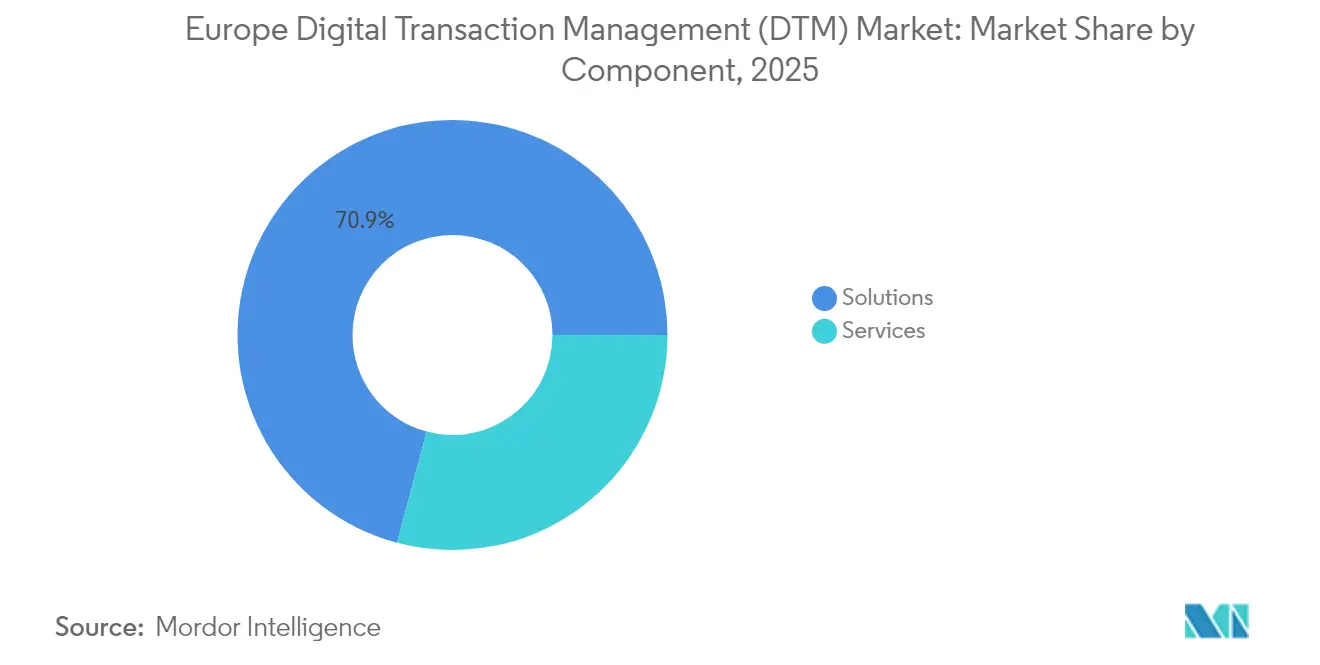

- By component, solutions captured 70.85% of the Europe Digital Transaction Management market share in 2025; services are projected to grow at 23.15% CAGR through 2031.

- By deployment mode, cloud maintained 78.15% share of the Europe Digital Transaction Management market size in 2025 and is advancing at a 27.95% CAGR to 2031.

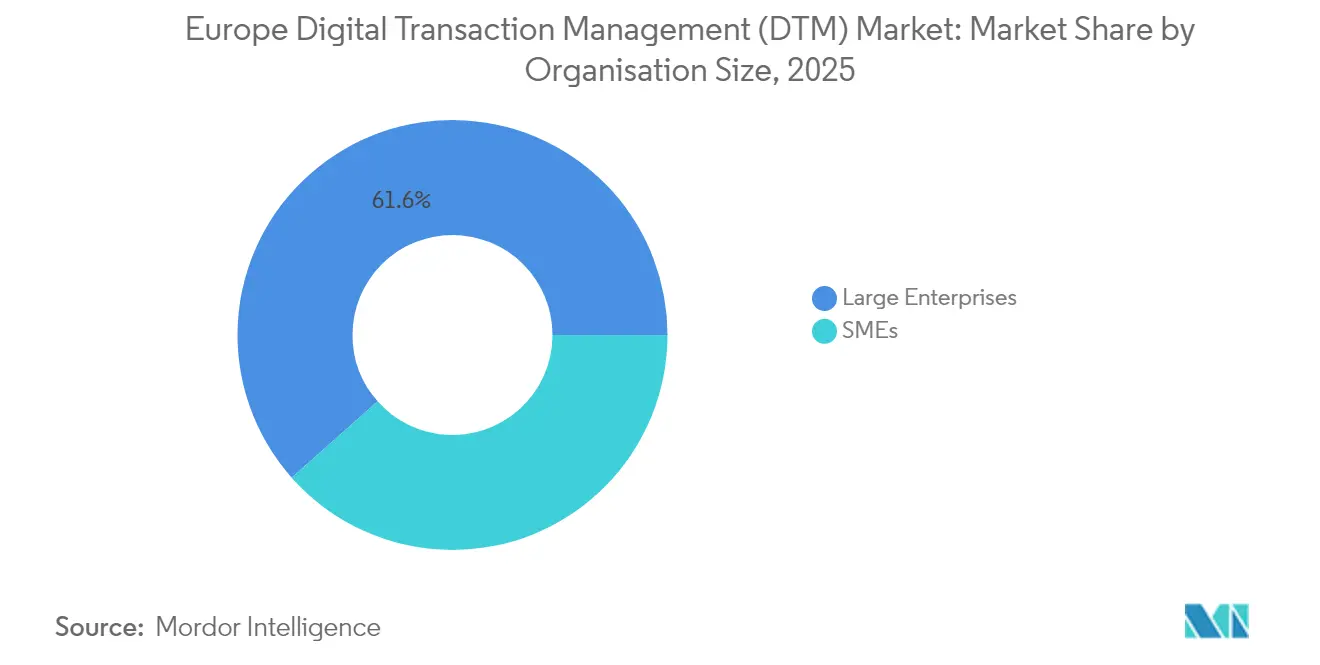

- By organisation size, large enterprises held 61.55% revenue share in 2025, while SMEs are forecast to expand at 25.95% CAGR between 2026-2031.

- By end-user industry, BFSI led with 28.35% share of the Europe Digital Transaction Management market size in 2025; automotive and mobility exhibit the quickest pace at 27.65% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Digital Transaction Management (DTM) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rise in e-signatures and cloud adoption | +6.2% | Global, with Nordic leadership | Short term (≤ 2 years) |

| SME push for end-to-end workflow automation | +5.8% | EU core, spill-over to UK | Medium term (2-4 years) |

| EU eIDAS 2.0 and PSD3 accelerating trust services | +4.9% | EU member states, EEA countries | Long term (≥ 4 years) |

| Post-COVID permanent shift to digital workflows | +3.7% | Global, with Western Europe focus | Short term (≤ 2 years) |

| Mandatory B2B e-invoicing roll-outs across EU | +3.1% | EU member states | Medium term (2-4 years) |

| Instant-payment rails driving real-time DTM demand | +2.4% | Eurozone, expanding to non-Euro EU | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rise in e-signatures and cloud adoption

European legislators project stable 25% yearly revenue gains for e-signature services, propelling cloud models that already hold 77.70% of transactions and register the fastest CAGR through 2030. Nordic governments showcase near-paperless public services, with Denmark eliminating hard-copy options for most citizen interactions and Sweden nearing a cash-free economy. eIDAS 2.0 removes cross-border friction by recognising remote signatures issued under any qualified EU trust service. BFSI stakeholders also depend on cloud scalability to authenticate instant payments within the mandated 10 seconds, cementing cloud architecture as the de facto backbone of pan-European trust services[1]European Parliament, “Electronic signatures,” europarl.europa.eu .

SME push for end-to-end workflow automation

SMEs account for over 99% of European businesses yet carry a EUR 53 billion digital-compliance burden. Targeted EU Digital Europe funds partially offset those costs and are catalysing 26.50% CAGR uptake among smaller firms. Consolidators such as Visma have responded by acquiring niche platforms that package KYC, invoicing and signing features into turnkey bundles. As 72% of SMEs now rely on data-driven decision tools, the demand for subscription-based, no-code automation has evolved from a convenience to a survival requirement [2]OECD, “SME Digitalisation to Manage Shocks and Transitions,” oecd.org .

EU eIDAS 2.0 and PSD3 accelerating trust services

The May 2024 adoption of eIDAS 2.0 obliges every member state to issue a European Digital Identity wallet by December 2026, covering 360 million citizens. Parallel PSD3 verification rules mandate real-time “confirmation of payee” checks from October 2025, driving banks to integrate certified trust-service providers capable of sub-second identity resolution. European firms such as InfoCert are leveraging acquisitions to scale these regulated services and reduce reliance on non-EU technology while maintaining sovereignty over personal data.

Post-COVID permanent shift to digital workflows

Remote operations introduced during lockdowns have outlasted the pandemic. Cloud collaboration suites now embed native signing options that eliminate the document “print-scan-send” loop, opening recurring revenue streams for providers. Healthcare transformation through the European Health Data Space further embeds digital authentication into patient record systems, and connected-car commerce requires continuous transaction checks. These permanent behavioural shifts sustain double-digit demand even as macroeconomic conditions fluctuate.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Persistent data-privacy and cyber-risk concerns | -3.8% | Global, with GDPR compliance focus | Long term (≥ 4 years) |

| High integration and change-management costs | -4.2% | EU SME segment, Eastern Europe | Medium term (2-4 years) |

| Fragmented national eID schemes hinder interoperability | -2.1% | EU member states, varying adoption | Long term (≥ 4 years) |

| Tight SME financing slows tech refresh cycles | -1.9% | Southern and Eastern Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Persistent data-privacy and cyber-risk concerns

Real-time payments demand 10-second clearing and yet must honour GDPR data-minimisation rules that often require data residency within national borders. The NIS2 directive widens breach-notification duties and raises fines, leading many banks to deploy AI-based anomaly detection that can handle rising fraud attempts without infringing privacy constraints. Smaller firms particularly struggle to finance specialist security skills, underscoring the need for vendor-provided compliance capabilities baked into platforms.

High integration and change-management costs

For SMEs, linking older ERP stacks to modern DTM platforms may take up to 12 months and absorb scarce developer budgets. Simultaneous compliance with eIDAS 2.0, PSD3, mandatory e-invoicing, and GDPR forces parallel project tracks, inflating consulting costs. The burden is heaviest in cash-constrained Southern and Eastern member states despite EU grants, slowing conversion from paper to digital in those regions[3]European Parliament, “Impact of EU Legislation on SMEs,” europarl.europa.eu .

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Solutions Maintain Scale Advantage

Solutions accounted for 70.85% of the Europe Digital Transaction Management market share in 2025 on the back of platforms that bundle signing, identity, workflow and audit functions under one licence. The services slice is smaller but rising at 23.15% CAGR as organisations outsource complexity to managed providers, especially for eIDAS wallet integration and instant-payment obligations. Vendors embed AI to auto-classify documents, verify identities and trigger alerts, reducing staff overheads and ensuring that solutions revenue continues to dominate absolute spend even while services expand faster.

Demand for consulting peaks during regulation roll-outs, after which recurring platform fees drive sustained revenue. Healthcare projects funded under the European Health Data Space allocate budget specifically to qualified trust-service integration, thereby locking in multi-year platform contracts. European software majors are consequently acquiring niche service firms to secure implementation talent and defend platform primacy.

By Deployment Mode: Cloud Supremacy Deepens

Cloud solutions held 78.15% of the Europe Digital Transaction Management market size in 2025 and are growing at 27.95% CAGR, reinforcing the architectural pivot away from on-premise. Providers offer real-time compliance updates, geo-fenced data centres and latency guarantees that on-premise installs find costly to replicate. Regulatory requirements for 24/7 instant-payment uptime further tilt adoption toward elastic cloud resources that can auto-scale during volume spikes.

Hybrid remains a transition path for financial institutions that wish to retain core-ledger data locally while routing customer-facing activity to the cloud. Nevertheless, even in these cases audit trails and signature verification often reside in managed environments. Nordic government portals, built completely in the cloud, supply proof points that nationwide digital services can run at scale with strong privacy safeguards, causing lagging countries to follow suit.

By Organisation Size: SME Momentum Rises

Large enterprises still represent 61.55% of revenue, yet SME uptake is expanding at 25.95% CAGR, changing the revenue pyramid. Subsidies under Digital Europe and local tax incentives soften upfront costs, and low-code interfaces reduce technical hurdles. SMEs are also compelled by fiscal authorities to adopt e-invoicing, and failure to comply risks invoice rejection or late-payment penalties.

Subscription pricing lowers entry barriers so that smaller firms bypass multi-year licence commitments. Regional software houses integrate DTM microservices into accounting suites, giving SMEs a single pane of glass for payroll, invoicing and compliance. As these firms scale cross-border, wallet-based identity schemes will reduce onboarding friction, further accelerating SME penetration.

By End-user Industry: BFSI Holds Lead, Automotive Surges

BFSI carried 28.35% share in 2025, justified by the sector’s stringent KYC, AML and instant-payment duties. PSD3 and real-time clearing reinforce the need for tokenised signatures tied to verified identities. At the same time, the automotive and mobility vertical is growing at 27.65% CAGR, buoyed by in-vehicle commerce ranging from charging payments to usage-based insurance. Each driver action can trigger micro-transactions that must be signed and audited automatically.

Healthcare adoption benefits from the European Health Data Space and electronic prescription mandates, whereas retail leverages DTM to curb chargeback risk in cross-border e-commerce. Government portals supply an additional catalyst, as tender bids, grant applications and payroll attestations increasingly require qualified electronic signatures rather than physical stamps.

Geography Analysis

The United Kingdom remains pivotal despite no longer being an EU member. Banks such as Lloyds and Santander invest heavily in open-banking APIs that require end-to-end digital identity proofing, ensuring that cross-border flows with the Single Market remain seamless. London’s fintech cluster continues to attract venture funding for real-time verification services that plug directly into EU eIDAS frameworks.

Germany is the region’s largest single market. January 2025 B2B e-invoicing obligations compel the Mittelstand to embed structured invoice and signature modules into legacy ERP systems, fuelling licence sales into manufacturing supply chains. Germany’s automotive OEMs then extend DTM capabilities into connected-car platforms, creating adjacent revenue streams for provider ecosystems.

Italy offers a mature reference case after mandating B2B e-invoicing in 2019. Its Sistema di Interscambio platform processes millions of invoices daily, and public procurement now requires qualified electronic signatures as standard. Spain and France follow on staggered timetables but mirror Italy’s legislation. Nordic countries demonstrate what fully digital public services deliver in efficiency gains: Denmark’s “digital by default” model and Sweden’s cash-less trajectory display usage benchmarks that other member states are keen to replicate.

Competitive Landscape

DocuSign remains the global brand leader and enjoys unrivalled name recognition among enterprise buyers, yet European specialists such as Visma, Signicat and InfoCert are eroding share by emphasising deep compliance alignment with eIDAS and national eID schemes. The top five suppliers collectively control roughly 68% of regional revenue, signalling a moderately concentrated field where challenger gains can still impact incumbent positioning.

M&A has intensified. InfoCert’s acquisition of Ascertia broadens qualified trust footprints into the UK, while Visma’s spree of four purchases in 18 months bundles KYC, expense and signing functions for two million SME subscribers. Large cloud vendors integrate leading signature engines into productivity suites, locking platforms into daily workflows and raising switching costs.

Private-equity suitors evaluating DocuSign at USD 12 billion highlight conviction that secular digital-workflow adoption has room to run. Smaller entrants target sector-specific gaps, such as electronic notarisation or real-estate escrow, leveraging API-first designs to embed quickly into niche applications. Strategic partnerships between global hyperscalers and local trust-service providers are emerging as the mechanism to reconcile pan-European coverage with country-specific rule nuances.

Europe Digital Transaction Management (DTM) Industry Leaders

DocuSign Inc.

Adobe Inc.

ZorroSign Inc.

Nintex Group Pty Ltd

Namirial SpA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Namirial, a European provider of Digital Transaction Management (DTM) software, and Signaturit, another key player in the sector, have entered exclusive negotiations for Signaturit to join the Namirial Group. The deal, subject to regulatory approvals and employee consultations, will see PSG exit its investment via the PSG Europe I fund.

- July 2025: Mastercard and Pay4You, a self-service payment portal, have partnered to offer a robust tail spend management solution for businesses across Europe. This collaboration utilizes Mastercard's Virtual Card Network (VCN) technology to ensure card acceptance, simplifying tail spend management for corporations.

- February 2025: Legitify partnered with DocuSign to embed secure digital notarisation into financial-services and real-estate flows.

- April 2024: Microsoft added native Adobe and DocuSign signing to SharePoint, cementing DTM inside Microsoft 365.

Europe Digital Transaction Management (DTM) Market Report Scope

Digital transaction management (DTM) is about moving from paper-based document processes to fully digital ones to enable the digital execution of transaction processes. DTM includes e-signatures, document transfer and certification, data and forms integration and management, and a variety of meta-processes around managing electronic transactions and the associated documents.

The European digital transaction management (DTM) market is segmented by component (solutions and services), organization size (small and medium enterprises and large enterprises), end-user industry (BFSI, healthcare, retail, IT and telecommunication, and other end-user industries), and country (United Kingdom, Germany, France, Spain, Italy, Nordics, and Rest of Europe [Eastern Europe, Benelux, etc.]) The market size and forecasts are provided in terms of value (USD) for all the above segments.

By Component

| Solutions |

| Services |

By Deployment Mode

| Cloud |

| On-premise |

| Hybrid |

By Organisation Size

| Small and Medium Enterprises |

| Large Enterprises |

By End-user Industry

| BFSI |

| Healthcare and Life Sciences |

| Retail and E-commerce |

| IT and Telecommunication |

| Government and Public Sector |

| Real-Estate and Construction |

| Automotive and Mobility |

By Country

| United Kingdom |

| Germany |

| France |

| Spain |

| Italy |

| Rest of Europe |

| By Component | Solutions |

| Services | |

| By Deployment Mode | Cloud |

| On-premise | |

| Hybrid | |

| By Organisation Size | Small and Medium Enterprises |

| Large Enterprises | |

| By End-user Industry | BFSI |

| Healthcare and Life Sciences | |

| Retail and E-commerce | |

| IT and Telecommunication | |

| Government and Public Sector | |

| Real-Estate and Construction | |

| Automotive and Mobility | |

| By Country | United Kingdom |

| Germany | |

| France | |

| Spain | |

| Italy | |

| Rest of Europe |

Key Questions Answered in the Report

What is the 2026 value of the Europe Digital Transaction Management market?

The Europe Digital Transaction Management market is valued at USD 12.93 billion in 2026.

How fast will the market grow through 2031?

It is forecast to expand at a 25.05% CAGR, reaching USD 39.54 billion by 2031.

Which deployment model leads adoption across Europe?

Cloud deployment accounts for 78.15% of usage and posts the fastest 27.95% CAGR.

Why are SMEs accelerating their uptake of digital transaction tools?

Driver % Impact on CAGR Forecast Geographic Relevance Impact Timeline Rise in e-signatures and cloud adoption +6.2% Global, with Nordic leadership Short term (≤ 2 years) SME push for end-to-end workflow automation +5.8% EU core, spill-over to UK Medium term (2-4 years) EU eIDAS 2.0 and PSD3 accelerating trust services +4.9% EU member states, EEA countries Long term (≥ 4 years) Post-COVID permanent shift to digital workflows +3.7% Global, with Western Europe focus Short term (≤ 2 years) Mandatory B2B e-invoicing roll-outs across EU +3.1% EU member states Medium term (2-4 years) Instant-payment rails driving real-time DTM demand +2.4% Eurozone, expanding to non-Euro EU Short term (≤ 2 years)

Page last updated on: