Technology, Media and Telecom

5th MayAccelerating Additive Manufacturing Adoption in India

3 Min Read

Sweden Data Center Rack Market is Segmented by Rack Size (Quarter Rack, Half Rack, Full Rack), by Rack Height (42U, 45U, 48U, Other Heights (≥52U and Custom), Rack Type (Cabinet (Closed) Racks, Open-Frame Racks, Wall-Mount Rack), Data Center Type (Colocation Facilities and More), Material (Steel and More). The Market Sizes and Forecasts are Provided in Terms of Value (USD) for all the Segments.

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Base Year For Estimation | 2025 |

| Forecast Data Period | 2026 - 2031 |

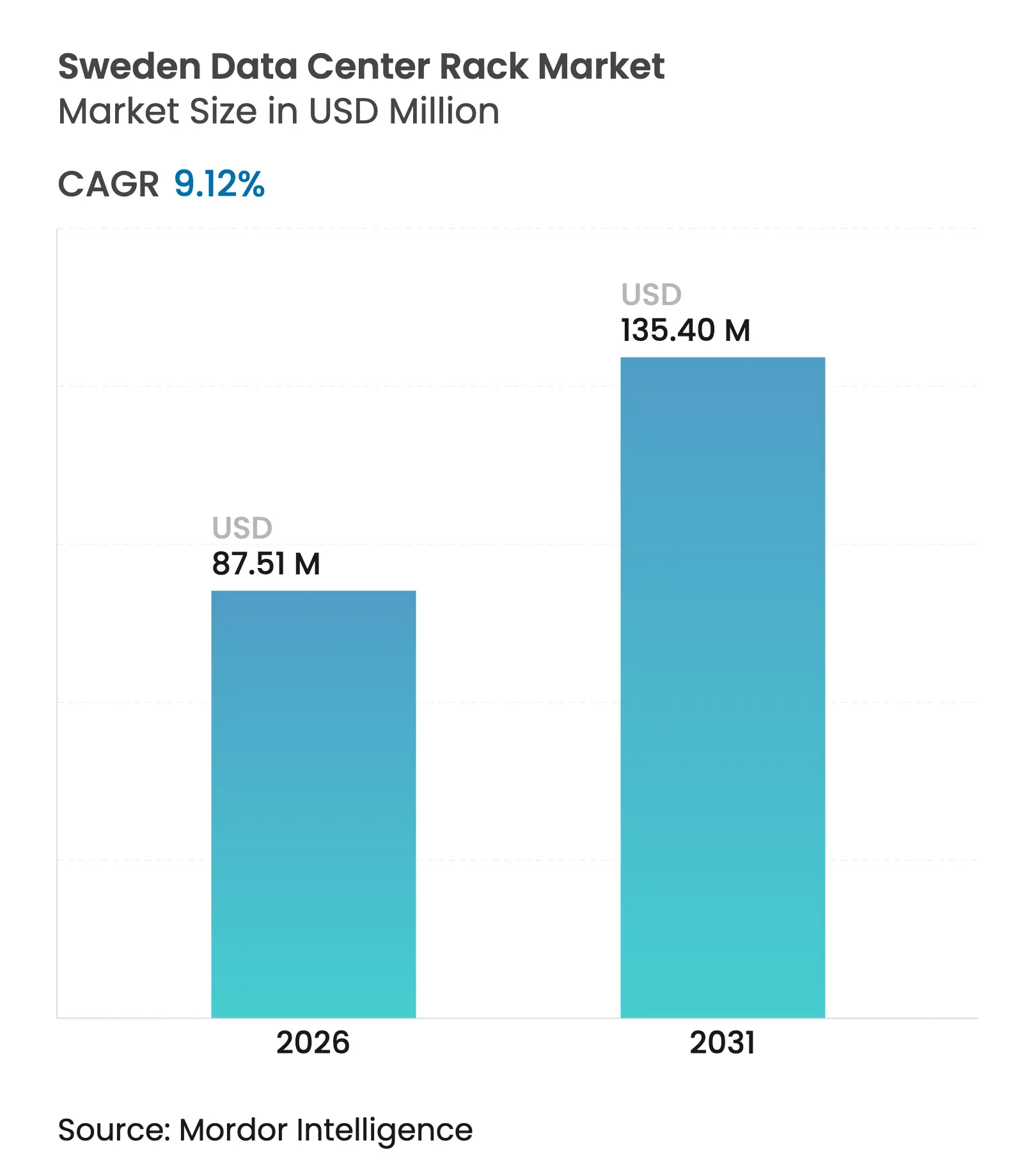

| Market Size (2026) | USD 87.51 Million |

| Market Size (2031) | USD 135.4 Million |

| Growth Rate (2026 - 2031) | 9.12 % CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

Sweden data center rack market size in 2026 is estimated at USD 87.51 million, growing from 2025 value of USD 80.2 million with 2031 projections showing USD 135.4 million, growing at 9.12% CAGR over 2026-2031. Sweden’s abundant renewable-energy mix, political stability and reliable connectivity position it as the Nordic region’s principal hosting location for hyperscale, colocation and edge facilities. Hyperscale operators are scaling rapidly to support artificial-intelligence training and inference workloads, pushing rack densities higher and accelerating the uptake of liquid-cooling-ready enclosures. At the same time, corporate net-zero mandates favor Sweden’s low-carbon electricity profile, giving operators a cost edge versus many Tier-1 European markets. Grid-reinforcement projects, streamlined planning rules outside Stockholm and institutional capital inflows underpin additional build-outs, even as the 2023 removal of electricity-tax incentives tightens near-term margins.

Key Report Takeaways

Note: Market size and forecast figures in this report are generated using Mordor Intelligence's proprietary estimation framework, updated with the latest available data and insights as of 2026.

Drivers Impact Analysis

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Rapid adoption of e-commerce

Rapid adoption of e-commerce

| +2.1% | National, with concentration in Stockholm, Gothenburg, Malmö | Medium term (2-4 years) |

% Impact on CAGR Forecast

:

+2.1%

|

Geographic Relevance

:

National, with concentration in Stockholm,

Gothenburg, Malmö

|

Impact Timeline

:

Medium term (2-4 years)

|

Significant growth in data generation

Significant growth in data generation

| +1.8% | Global with Sweden-specific AI/IoT applications | Long term (≥ 4 years) | |||

Expansion of hyperscale & colocation facilities

Expansion of hyperscale & colocation facilities

| +2.4% | Stockholm region, expanding to northern Sweden | Short term (≤ 2 years) | |||

Extended data-center electricity-tax incentives

Extended data-center electricity-tax incentives

| +0.7% | National (note: incentives abolished July 2023) | Short term (≤ 2 years) | |||

Circular-economy push for modular recyclable racks

Circular-economy push for modular recyclable racks

| +1.2% | EU-wide with Sweden leadership in sustainability | Long term (≥ 4 years) | |||

HPC clusters for AI & quantum research

HPC clusters for AI & quantum research

| +1.6% | Stockholm, Linköping (MIMER AI Factory location) | Medium term (2-4 years) | |||

| Source: Mordor Intelligence | ||||||

Rapid adoption of e-commerce

Almost 99% of Swedish households have internet access, and domestic e-commerce is expanding into B2B verticals, creating steady demand for low-latency, high-density processing nodes hosted in full racks across multiple metro zones.[1]International Energy Agency, “Sweden 2024 Energy Policy Review,” iea.org Retailers embed recommendation engines and dynamic-pricing models that require GPU-accelerated servers, reinforcing the shift toward enclosed, liquid-ready cabinets for thermal control. Fintech firms in Stockholm mirror these needs for algorithmic trading and real-time payments, cementing full-rack supremacy. Sustainability mandates then drive merchants to specify energy-efficient modular designs that can scale with workload surges while minimizing embodied carbon.

Significant growth in data generation

Industrial IoT rollouts in forestry, automotive and precision manufacturing pump out structured data flows that must be stored, filtered and analyzed locally before transfer to core clouds . Smart-city deployments also generate continuous telemetry for traffic, power and environmental systems. Under the EU Energy Efficiency Directive, Swedish operators must log and publish energy and water usage, inflating data volumes that in turn call for ruggedized rack inventories at both edge and core facilities [3]Data Center Knowledge, “EcoDataCenter Converts Borlänge Mill Into 240MW Campus,” datacenterknowledge.com. Quantum-research consortia such as the MIMER AI Factory at Linköping University tighten performance envelopes further; racks there need electromagnetic shielding, high-bandwidth fiber routing and adaptive cooling. [2]EuroHPC Joint Undertaking, “AI Factories Programme Factsheet,” eurohpc.europa.eu

Expansion of hyperscale & colocation facilities

EcoDataCenter’s 240 MW Borlänge campus is engineered for AI and cloud services with standardized cabinets supporting liquid cooling and >50 kW per rack densities. Vertiv’s acquisition of E+I Engineering enhances its integrated power busway offering aimed at prefabricated modular halls where racks must arrive factory-wired and test-certified vertiv.com. Fresh funding from the Nordic Investment Bank validates the investment thesis that Nordic sites can outcompete continental peers on green-power availability and land cost . New Stockholm 4 South capacity from Conapto underscores persistent urban demand even amid grid congestion.

HPC clusters for AI & quantum research

EuroHPC’s AI Factory program designates Sweden as a host for mid-range supercomputers, prompting procurement of racks capable of housing GPU blades with >100 kW thermal budgets, hot-aisle containment and direct-to-chip liquid loops. Use cases in life sciences, gaming and autonomous-vehicle modeling run best on tightly coupled nodes requiring low-latency interconnects, so cabinets integrate high-density fiber patch fields. Quantum-classical hybrids add vibration isolation and magnetic shielding layers, nudging suppliers toward aluminum frames and composite panels that damp interference.

Restraints Impact Analysis

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||||

|---|---|---|---|---|---|---|---|---|

Increasing data-security breaches

Increasing data-security breaches

| -1.3% | Global with Sweden-specific GDPR enforcement | Short term (≤ 2 years) |

:

|

% Impact on CAGR Forecast

:

-1.3%

|

Geographic Relevance

:

Global with Sweden-specific GDPR enforcement

|

Impact Timeline

:

Short term (≤ 2 years)

| |

Stringent GDPR-aligned data-protection laws

Stringent GDPR-aligned data-protection laws

| -0.9% | EU-wide with Sweden as enforcement leader | Medium term (2-4 years) | |||||

Grid-capacity constraints in Stockholm region

Grid-capacity constraints in Stockholm region

| -1.7% | Stockholm metropolitan area | Short term (≤ 2 years) | |||||

Rising steel prices inflating rack costs

Rising steel prices inflating rack costs

| -0.8% | Global supply chain with Nordic delivery premiums | Medium term (2-4 years) | |||||

| Source: Mordor Intelligence | ||||||||

Increasing data-security breaches

High-profile incidents spur Sweden’s Data Protection Authority to levy multimillion-euro penalties, pushing operators to adopt zero-trust zoning down to rack level with biometric locks and tamper sensors. These extras raise acquisition and integration costs. Facilities hosting AI-factory workloads enhance segmentation so that a compromised blade can be quarantined without shutting adjacent compute clusters, further complicating rack design and cable routing.

Grid-capacity constraints in Stockholm region

Rapid hyperscale build-outs have outpaced substation upgrades, creating connection moratoriums and forcing operators to scout northern municipalities with surplus hydropower. Svenska kraftnät’s 2024-2033 plan earmarks 1,500 km of new lines but many projects only come online late in the forecast window. Interim solutions include on-site battery storage and demand-response systems housed in custom rack enclosures, which raise capex and extend deployment cycles.

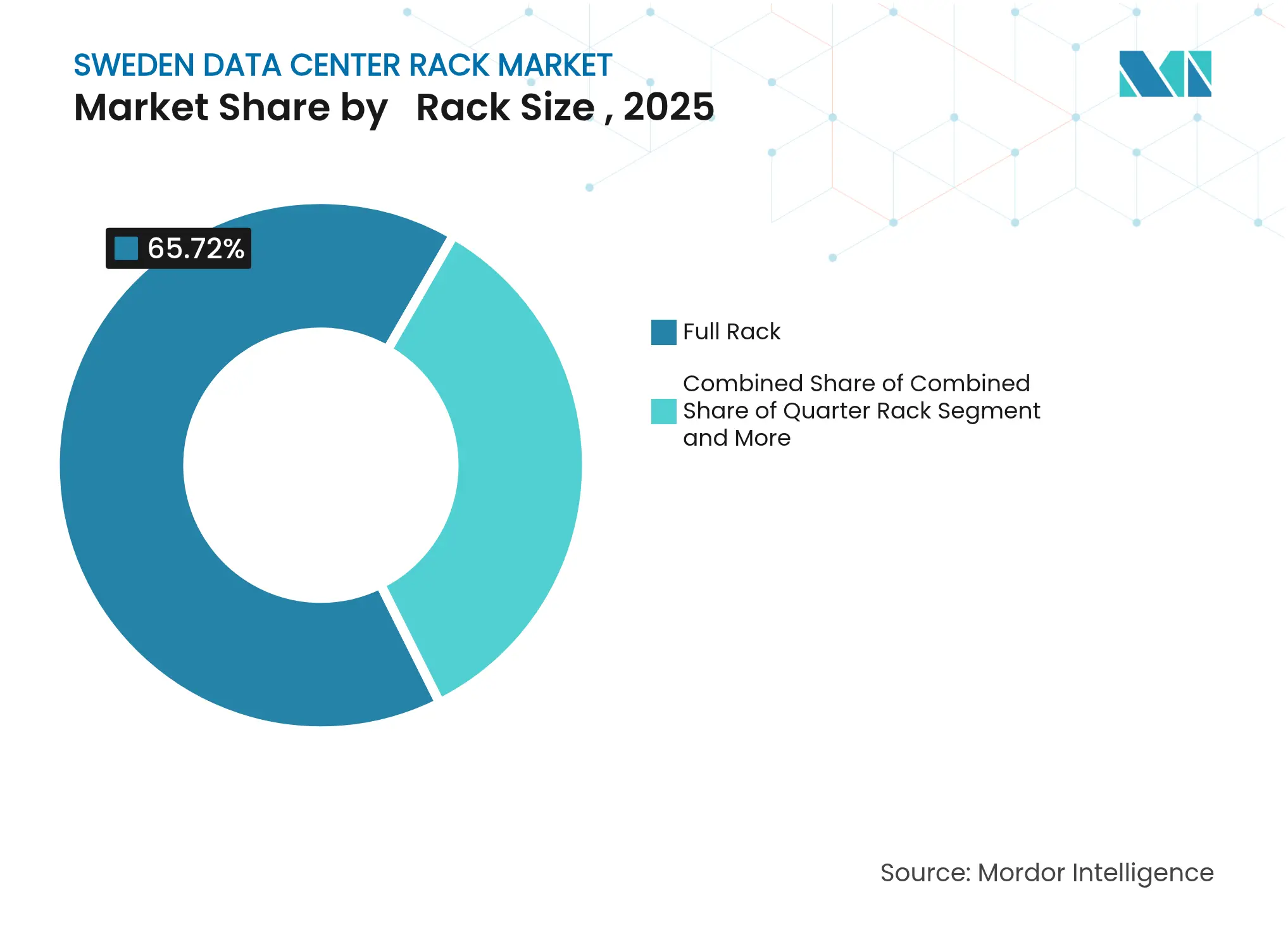

By Rack Size: Full Rack Dominance Driven by AI Workloads

Full racks own 65.72% of Sweden data center rack market share in 2025, reflecting hyperscale preference for dense nodes per cabinet. The Sweden data center rack market size for this format is projected to expand at 11.84% CAGR to 2031. AI training clusters benefit from high-bandwidth, low-latency backplanes best delivered when servers, switches and accelerators sit in contiguous slots. Quarter and half racks remain relevant at far-edge sites such as cellular base stations but their growth trails aggregated deployments where power and cooling can be centralized.

Concentrated compute loads elevate average rack power draw above 30 kW, making liquid cooling trays and rear-door heat exchangers standard. Academic research clusters, including MIMER, specify full frames for deterministic airflow and ease of adding shielding. As hyperscale tenants lock in long-term leases, colocation landlords adopt pay-per-rack pricing tiers calibrated to such power envelopes, reinforcing the model.

Note: Segment shares of all individual segments available upon report purchase

By Rack Height: 42U Standard Faces 48U Innovation Push

Legacy white-space still hosts predominately 42U enclosures which commanded 52.55% revenue in 2025. Operators value mechanical familiarity, abundant accessories and predictable cable paths. Yet 48U cabinets—forecast to grow 10.98% CAGR—offer 14% more vertical slots without lengthening rows, a critical advantage as Stockholm real-estate rates rise. The Sweden data center rack market size attributed to 48U solutions will climb steadily as new halls standardize on taller frames that still fit below 3 m clearance limits.

Thermal designs now place cooling manifolds atop or beneath servers, and the extra 2U eases integration. Sustainability teams also find fewer steel kilograms per installed compute watt when racks host more gear, improving embodied-carbon metrics. French-door models at 48U enable narrower cold aisles, an ergonomic gain when hot-aisle containment is mandatory.

By Rack Type: Cabinet Security Meets Open-Frame Efficiency

Cabinet racks achieved 68.75% of total 2025 revenue, a share that mirrors Sweden’s strict data-protection climate where physical isolation aligns with GDPR risk assessments. The category also registers the fastest 13.12% CAGR. Doors with multi-factor locks, environmental sensors and smart PDUs make cabinets an integrated compliance tool. Open-frame styles persist in test labs and telecom shelters that rely on ambient airflow but growth is single-digit.

Continuous reporting duties under Sweden’s energy-usage decree motivate operators to embed metering at PDU and device level; cabinets simplify this by housing sensors in a sealed ecosystem. Hardware OEMs bundle calibrated airflow-baffle kits that only fit enclosed frames, accelerating the shift. Edge-site wall-mounts serve retail branches yet constitute a low-value slice of Sweden data center rack market revenue.

Recognized by Experts. Trusted by Leaders.

A trusted intelligence partner to global decision-makers across 90+ countries.

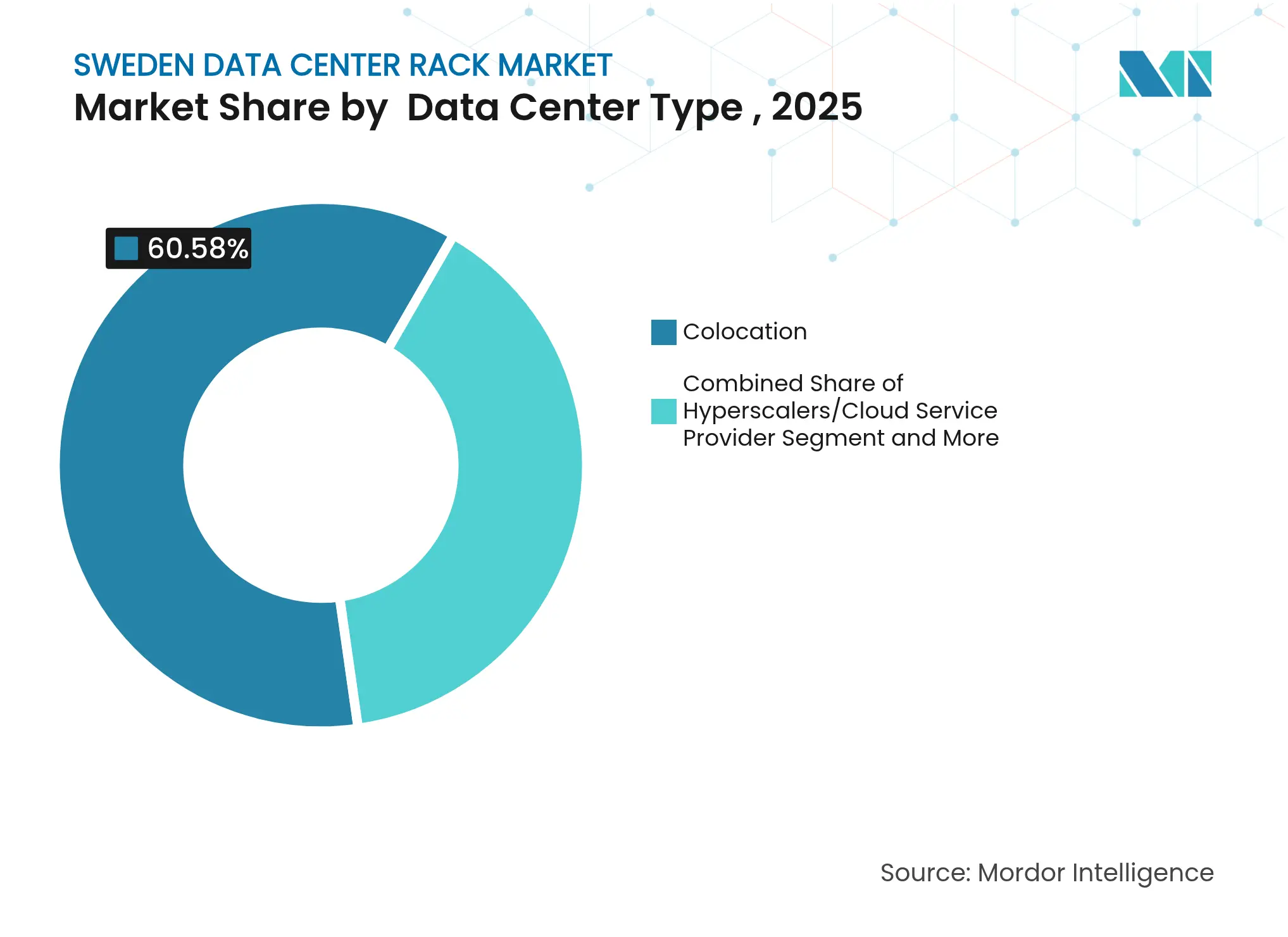

By Data Center Type: Colocation Stability Versus Hyperscale Innovation

Colocation halls controlled 60.58% of Sweden data center rack market size in 2025, buoyed by enterprises seeking OPEX flexibility and latency to domestic users. However, hyperscale and cloud players will log 13.55% CAGR, reaching parity toward decade-end as GPU-intensive AI projects demand purpose-built shells. Operators such as CoreWeave contract entire data suites, influencing rack specifications around immersion-ready frames and 100 Gbit/s fabric terminations.

Government and financial tenants keep colocations resilient by mandating dual-site diversity within Sweden to satisfy data-residency laws. Meanwhile, edge micro-modules sprout along rail corridors and logistics hubs, enabling content caching and IoT aggregation. Their cabinets arrive factory-integrated, reducing on-site labour yet growing more slowly than cloud megacampus orders.

Note: Segment shares of all individual segments available upon report purchase

By Material: Steel Dominance Challenged by Aluminum Innovation

Steel frames retained 77.62% share in 2025 thanks to cost, rigidity and global supply. Rising commodity premiums and circular-economy goals nonetheless propel aluminum to a 11.93% CAGR. Weight savings simplify upper-level installs inside multi-story halls, while corrosion resistance appeals to coastal deployments. The Sweden data center rack market expects aluminum to gain share whenever operators quantify lifecycle carbon.

Suppliers now tout snap-in joints and reversible panels for aluminium models that enable refurbishment rather than scrappage. Composite inserts imbued with electromagnetic shielding protect quantum-research racks. Although alloys carry higher ticket prices, total cost of ownership narrows when factoring recyclability credits, a metric many Swedish institutional investors track in due-diligence screens.

Sweden’s data-center footprint gravitates around Stockholm where 70 MW of commissioned power underpins latency-sensitive finance, gaming and media workloads. The capital enjoys submarine-cable diversity and a dense corporate customer base, keeping occupancy high despite land scarcity. Grid queues, however, compel new entrants to explore Mälardalen and Gävleborg counties, regions within courier reach yet with available capacity and local-government incentives.

Northern provinces such as Dalarna and Norrbotten supply low-cost hydropower and ambient temperatures conducive to free-air cooling, luring hyperscale and AI farms that prize power pricing over milliseconds of latency. EcoDataCenter’s 240 MW campus in Borlänge typifies this shift, converting industrial brownfields into carbon-negative compute parks whose racks exhaust heat into adjacent district-heating grids. Scandinavian Data Centers’ ScandiDC I in Eskilstuna—inside a WWII bunker—adds physical hardening plus a thermal-loop capable of warming 6,000 homes.

Svenska kraftnät’s decade-long expansion of 1,500 km of high-voltage lines and 30 substations will redistribute load and open further corridors, encouraging multicloud operators to adopt a hub-and-spoke model: master campuses in the north feed edge POPs closer to end users. Academic centres at Linköping and Luleå deepen regional diversity by hosting AI Factories, spawning specialist suppliers for shielded aluminum cabinets. Collectively, these moves keep the Sweden data center rack market on a steady northern migration while sustaining core-metro refurbishments.

Market Concentration

Global OEMs such as Schneider Electric, Vertiv and Rittal anchor tender lists with portfolio breadth, integrated power paths and worldwide logistics. Vertiv’s 2024 buyout of E+I Engineering boosts its ability to ship busway+cabinet packages pre-certified for 50+ kW loads, a differentiator when hyperscalers demand six-month delivery windows vertiv.com. Schneider bundles EcoStruxure software with racks to give operators instantaneous energy-intensity dashboards, an advantage under Sweden’s new reporting rules.

Nordic boutiques compete on sustainability nuance. Scandinavian Data Centers designs bunker-derived halls with waste-heat recovery; its cabinets incorporate quick-connect district-heating exchangers, resonating with municipal utilities seeking decarbonization offsets. Conapto markets 100% renewable-powered colocation suites and selects recyclable aluminum frames as standard, carving share among ESG-focused enterprises.

Investor appetite intensifies rivalry. Brookfield Asset Management’s pledge to fund 750 MW of Swedish capacity over 10–15 years gives its operating affiliates bulk-purchasing clout, letting them negotiate frame prices and bespoke features. Areim’s EUR 450 million sustainable data-center fund chases similar deals, often specifying circular-economy scorecards that favour modular, refurbishable rack lines. The Sweden data center rack market consequently rewards vendors that deliver carbon accounting, rapid deployment and robust security in a single SKU.

*Disclaimer: Major Players sorted in no particular order

1. INTRODUCTION

2. RESEARCH METHODOLOGY

3. EXECUTIVE SUMMARY

4. MARKET LANDSCAPE

5. MARKET SIZE AND GROWTH FORECASTS (VALUE)

6. COMPETITIVE LANDSCAPE

7. MARKET OPPORTUNITIES and FUTURE OUTLOOK

Market Definitions and Key Coverage

Our study defines the Sweden data center rack market as the annual invoice value of newly manufactured steel or aluminum enclosures, quarter, half, and full racks between 42 U and ≥52 U, deployed inside colocation, hyperscale, enterprise, and edge data centers nationwide, together with factory-supplied cable management kits and blanking panels.

Scope exclusion: Refurbished racks, aisle containment frames sold without cabinets, and rack-mounted power distribution units are excluded.

Segmentation Overview

Detailed Research Methodology and Data Validation

Primary Research

To close gaps, we interviewed rack OEM design engineers, Stockholm-based colocation facility managers, Nordic electrical design consultants, and regional utility grid planners. Their insights on average selling price shifts, preferred rack heights for liquid-ready servers, and delivery lead times were pivotal in validating secondary indications and calibrating scenario assumptions.

Desk Research

Mordor analysts first mapped the installed and planned white floor footprint using public filings from operators on the Swedish Companies Registration Office portal, energy consumption releases by the Swedish Energy Agency, import codes for HS 9403 metal furniture in the Swedish Customs database, tender notices on Tenders Info, and market commentaries from the Swedish Data Center Industry Association. Supplementary context came from Eurostat ICT datasets, academic papers on Nordic free air cooling, and press archives curated on Dow Jones Factiva.

Financial sanity checks drew on D&B Hoovers for vendor revenue splits, while patent trends for high-density enclosures were sampled through Questel. The sources listed illustrate the spectrum consulted; many additional open and subscription references informed data point verification.

Market-Sizing & Forecasting

A top-down model converts Sweden's planned IT load additions (MW) into rack counts through density coefficients observed in primary calls, then multiplies by weighted ASPs for 42 U, 48 U, and >48 U cabinets. Bottom-up cross-checks use sampled supplier shipments and channel checks to reconcile totals. Key variables include hyperscale capacity pipelines, rack-level power density migration, steel price indices, SEK-USD currency trends, and Stockholm grid connection timelines. Forecasts rely on a multivariate regression with ARIMA overlay that ties rack demand growth to MW additions, e-commerce traffic, and 5G subscriber expansion. Where shipment evidence is thin, linear gap fills are anchored to historical procurement cycles observed in earlier build phases.

Data Validation & Update Cycle

Model outputs pass three rounds of analyst review: variance scans against macro indicators, peer cross-checks, and senior sign-off. Reports refresh annually, and interim reruns are triggered by material events such as hyperscale site announcements or sharp steel cost swings, ensuring clients receive the latest calibrated view.

Why Mordor's Sweden Data Center Rack Baseline Commands Reliability

Benchmark comparison

Published estimates often diverge because firms pick differing rack types, replace cycle assumptions, or currency treatments.

Key gap drivers: some publishers fold mechanical infrastructure bundles into rack totals, others count only new full racks, and a few convert Nordic krona values at list day rates without hedging. Mordor's scope isolates cabinet value only, applies shipment weighted ASPs, and refreshes the model each year, producing a balanced baseline.

| Market Size | Anonymized source | Primary gap driver | ||

|---|---|---|---|---|

USD 80.2 M (2025) | Mordor Intelligence | - | Anonymized source:Mordor Intelligence | Primary gap driver:- |

USD 90 M (2024) | Global Consultancy A | Blends replacement and maintenance kits, inflating value | ||

USD 14 M (2025) | Trade Journal B | Counts only open frame racks shipped, excludes cabinets |

Accelerating Additive Manufacturing Adoption in India

3 Min Read

Pricing Strategy for Semiconductor Components

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.