Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.28 Billion |

| Market Size (2026) | USD 1.41 Billion |

| Market Size (2031) | USD 2.31 Billion |

| Growth Rate (2026 - 2031) | 10.36% CAGR |

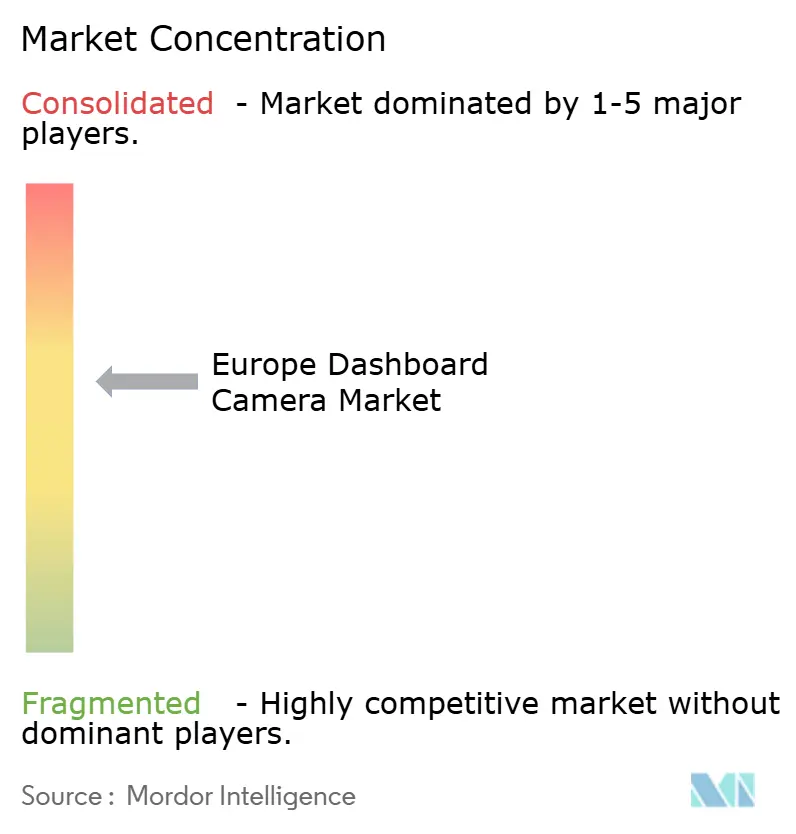

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Dashboard Camera Market Analysis by Mordor Intelligence

The Europe dashboard camera market size is expected to grow from USD 1.28 billion in 2025 to USD 1.41 billion in 2026 and is forecast to reach USD 2.31 billion by 2031 at 10.36% CAGR over 2026-2031. Strong demand stems from insurers granting policy discounts, courts fast-tracking video evidence, and fleets seeking lower accident costs, while component prices fall and EU safety rules tighten. Consumers in mature markets such as the United Kingdom already view dashcams as essential for liability protection, whereas fast-growing Spain benefits from rideshare expansion and fleet-modernization incentives. Hardware-only sales are giving way to subscription analytics, and dual-channel, 4K, and AI-enabled models are displacing entry-level units as fleet managers balance compliance with cost. Original equipment manufacturer (OEM) integration poses a long-term competitive threat, but after-market specialists still address the vast parc of older vehicles across the continent.

Key Report Takeaways

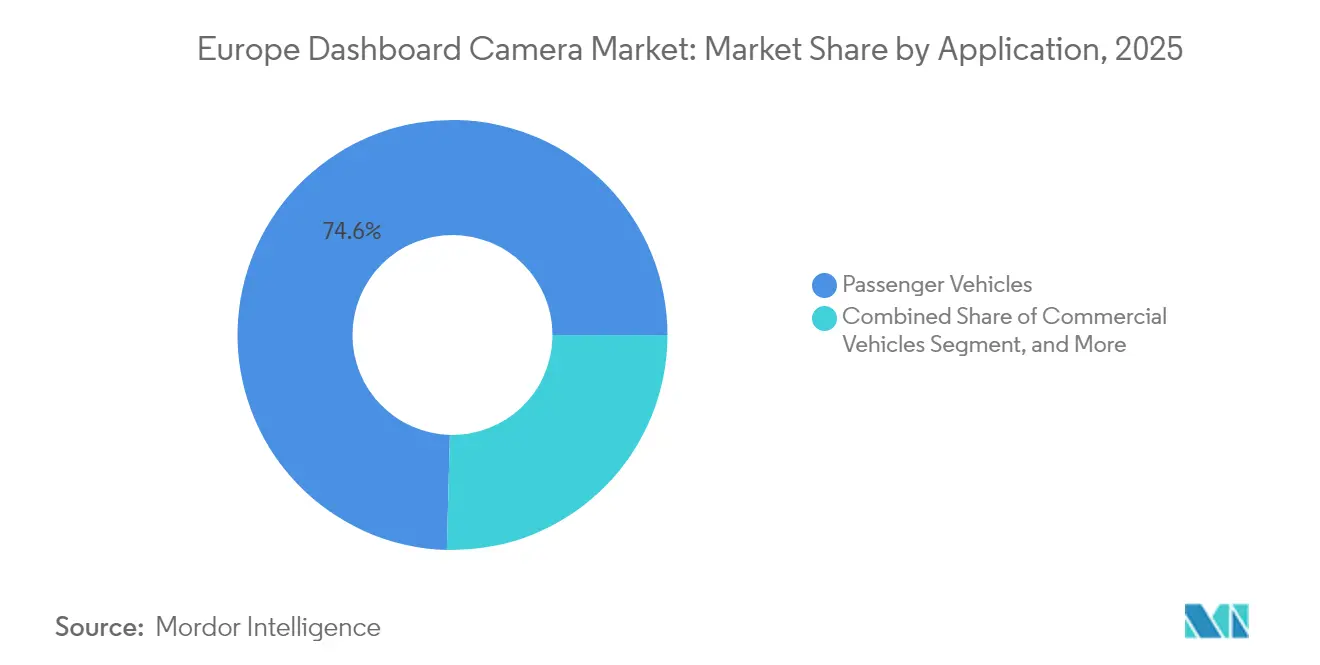

- By application, passenger vehicles accounted for 74.58% of the Europe dashboard camera market share in 2025, while commercial vehicles are on track for an 11.28% CAGR through 2031.

- By country, the United Kingdom led with 28.85% revenue share in 2025; Spain is forecast to post the fastest 13.02% CAGR to 2031.

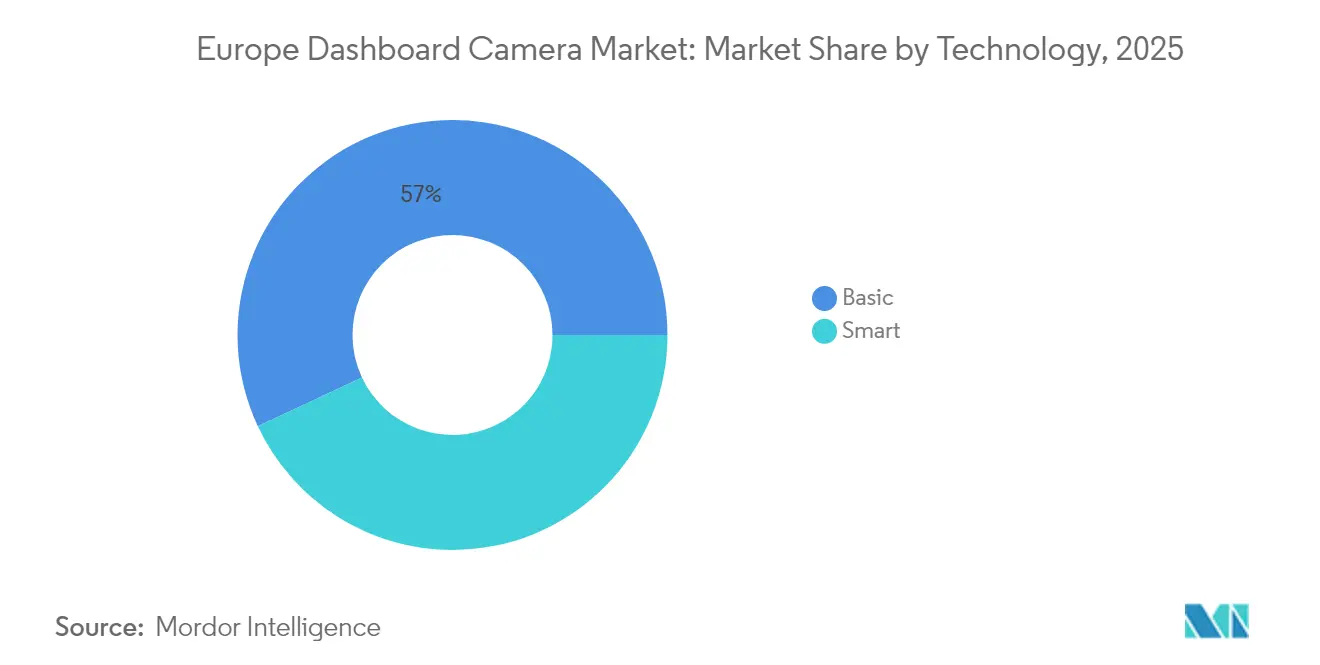

- By technology, basic dashcams held 56.98% of 2025 revenue; smart variants are expected to advance at an 10.95% CAGR to 2031.

- By product type, single-channel units captured 64.25% of 2025 sales, yet dual-channel systems are projected to expand at a 12.18% CAGR to 2031.

- By resolution, Full HD commanded 44.05% of sales in 2025; 4K and above formats will climb at a 12.46% CAGR to 2031.

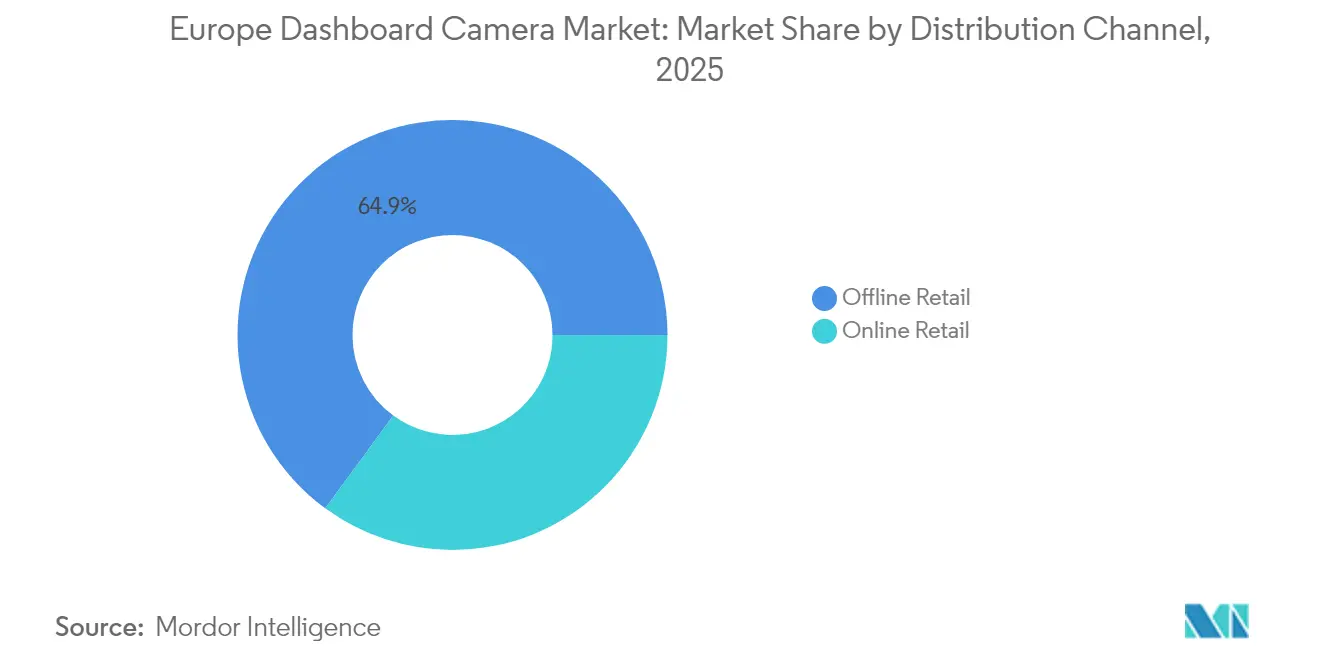

- By distribution channel, offline retail held 64.92% of 2025 revenue; online retail are expected to advance at an 13.10% CAGR to 2031.

- By end-user, private vehicle owners held 77.65% of 2025 revenue; fleet operators are expected to advance at an 12.21% CAGR to 2031..

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Dashboard Camera Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Road-Accident Litigation Evidence Needs | +2.8% | UK, France, Spain, Italy | Short term (≤ 2 years) |

| Insurance Premium Discounts for Dashcam-Equipped Vehicles | +2.4% | UK, Netherlands, Germany | Medium term (2-4 years) |

| EU Mandates for Advanced Driver Monitoring Systems | +2.1% | EU-wide, strongest in France and Germany | Medium term (2-4 years) |

| Proliferation of AI-Enabled Connected Dashcams | +1.9% | UK, Germany, Netherlands, Nordic countries | Long term (≥ 4 years) |

| Fleet Telematics Integration Across Logistics and Rideshare | +1.5% | Spain, France, UK, Italy | Medium term (2-4 years) |

| Declining Cost of High-Resolution Imaging Sensors | +1.2% | Global, with early gains in UK, Germany, Netherlands | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surge in Road-Accident Litigation Evidence Needs

Courts across Europe now accept dashcam video as primary proof in liability disputes, shortening settlement cycles by up to 40% and cutting insurer legal fees. United Kingdom police processed about 125,000 Operation Snap submissions in 2023, with 70% yielding enforcement action.[1]UK Police, “Operation Snap Dashcam Submissions,” police.uk France and Italy allow recordings if retention is limited to seven days unless an incident occurs, reinforcing consumer confidence. Spanish rideshare drivers rely on footage to rebut fraudulent claims, mirroring the country’s 13.44% CAGR. Logistics fleets report accident reductions of 15% and premium cuts of up to 18% after deploying cameras. As video admissibility spreads, cameras shift from optional gadgets to legal safeguards.

Insurance Premium Discounts for Dashcam-Equipped Vehicles

Insurers reward policyholders who share footage or telematics data. Aviva’s smartphone dashcam app yields average annual savings of GBP 170 (USD 215) and peaks at GBP 250 (USD 316) for high-scoring drivers. Jaguar Land Rover and Allianz subsidize Range Rover premiums by GBP 150 (USD 190) monthly in exchange for data feeds. Adoption is advanced, with 31% of motorists owning dashcams and three-quarters believing all drivers should use one. Dutch fleets report safety scores near 100% after adding video, translating into 12%–18% renewal discounts. As commercial carriers with high mileage face tighter underwriting, cameras are increasingly required equipment.

EU Mandates for Advanced Driver Monitoring Systems

The General Safety Regulation 2022/2144 obliges new vehicle types approved after July 2024 to include driver drowsiness and distraction warnings.[2]European Commission, “Safe Vehicles—General Safety Regulation,” europa.eu Retrofitting older fleets with dual-channel dashcams meets these standards at lower cost than OEM systems. UN Regulation 169 further compels heavy trucks to store 30 seconds of pre-crash data. Vendors winning type-approval certifications position themselves as compliance partners, while Germany’s stricter privacy rules force firmware variants that respect local data-retention limits

Proliferation of AI-Enabled Connected Dashcams

Artificial-intelligence engines transform cameras into preventive tools that score driver behavior, trigger in-cab alerts, and stream incidents to the cloud. Samsara’s vision analytics, rolled out across Fraikin’s 60,000 European vehicles, cut crashes by 15% in one year and secured multiyear software contracts. Nextbase embeds What3words geolocation and Alexa voice control in its 622GW 4K model, allowing drivers to send precise coordinates to responders. Thinkware’s T700 offers tamper-proof lock-box mounts to deter fraud. Fleets pay EUR 400–550 (USD 450–620) per unit because the analytics offset costs via lower premiums and downtime.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Stringent GDPR-Driven Data-Privacy Compliance Costs | -1.8% | Germany, Austria, Belgium, France | Medium term (2-4 years) |

| National Restrictions on Public-Space Video Recording | -1.2% | Germany, Austria, Switzerland | Long term (≥ 4 years) |

| Competitive Pressure from OEM-Integrated Camera Systems | -1.0% | EU-wide, strongest in Germany, France, UK | Long term (≥ 4 years) |

| Battery-Drain Concerns During 24-Hour Parking Mode | -0.6% | Urban centers in Germany, Netherlands, UK | Short term (≤ 2 |

| Source: Mordor Intelligence | |||

Stringent GDPR-Driven Data-Privacy Compliance Costs

Germany’s revised Federal Data Protection Act and Telecommunications-Telemedia amendments impose end-to-end encryption and restrict continuous recording, adding EUR 50–80 (USD 56–90) to bill-of-materials costs. France’s Penal Code limits footage retention to seven days, compelling automatic overwrite functions. Vendors must code geofencing to disable recording in sensitive zones and maintain consent logs, complicating firmware and shrinking entry-level margins. Such fragmentation forces makers to maintain multiple software builds, undermining scale economies.

National Restrictions on Public-Space Video Recording

Germany’s courts decide admissibility case by case, creating legal uncertainty for casual users, while Austria and Switzerland enforce strict proportionality tests. Consumers wary of fines or litigation delay purchases, slowing organic penetration. Manufacturers struggle to craft a single legal disclaimer suitable for every jurisdiction, raising support costs and delaying launches.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Smart Variants Capture Fleet Analytics Premium

Smart models, forecast to grow at an 10.95% CAGR, embed AI that coaches drivers and uploads clips instantly, reshaping value from passive to predictive safety. Basic devices held 56.98% of 2025 revenue, yet their share erodes as fleets choose data-rich units that cut accidents by 15% and unlock insurance savings. The Europe dashboard camera market size for smart units is projected to widen most among logistics and rideshare operators that demand compliance dashboards.

Price-sensitive private owners still choose EUR 150 (USD 169) basic models for evidence capture, sustaining volume but pressuring margins. Retail channel promotions clear aging inventory as 4K prices drop. The bifurcation mirrors wider automotive tech adoption: consumers judge cameras as accessories, fleets view them as operational software nodes.

By Product Type: Dual-Channel Growth Driven by Compliance and Fraud Prevention

Single-channel devices held 64.25% revenue in 2025, yet dual-channel units will rise at a 12.18% CAGR because EU rules now require cabin-facing monitoring on new truck types. Rideshare drivers also install cabin cameras to document disputes, accelerating uptake in Spain and France.

Fleet buyers pay EUR 250–400 (USD 281–450) for dual-channel bundles that include secure lock-box mounts, avoiding driver tampering. Rear-only units remain niche, aimed at parking-lot scuffs. As OEMs add multiple lenses, after-market suppliers focus on ease of retrofit and superior analytics to retain share.

By Application: Commercial Fleets Accelerate Adoption Through Telematics Integration

Passenger cars dominated with 74.58% of 2025 revenue, yet commercial vehicles show an 11.28% CAGR as operators integrate cameras with fuel, route, and maintenance dashboards. Berto Group cut accidents 15% and premiums 18% after equipping 180 trucks, underscoring return on investment.

Private-vehicle uptake is mature in the United Kingdom, while Spanish growth is rideshare-led. Commercial buyers demand installation services, cloud storage, and multi-year warranties, encouraging vendors to bundle hardware with software fees.

By Video Quality/Resolution: 4K Adoption Driven by Night-Vision Clarity

Full HD retained 44.05% of 2025 sales due to balanced cost, but 4K units will grow 12.46% annually as Sony STARVIS sensors become cheapen. Garmin’s 1440p Dash Cam 66W sells at GBP 154.95 (USD 196), hitting the mid-market sweet spot.

Nextbase’s 622GW commands EUR 329.99–384 (USD 371–432) for 4K, attracting fleets that need plate legibility in low light. Lower storage costs and cloud compression reduce file-size worries, and insurers increasingly prefer 4K for forensic zoom. Standard Definition quickly fades except in bargain outlets.

By Distribution Channel: Online Retail Gains Share Through Direct-to-Consumer Models

By Distribution Channel, offline retail held 64.92% of 2025 revenue; online retail are expected to advance at an 13.10% CAGR to 2031. E-commerce expands faster than brick-and-mortar as brands sell direct, bundle cloud plans, and capture higher margins. Nextbase offers web-only kits with filters and hard-wire looms, while Halfords pivots to installation services in the United Kingdom.

Fleets bypass retail altogether, signing multiyear contracts with telematics vendors that include hardware, software, and support. Online share gains further as subscription add-ons require account portals, embedding customers in brand ecosystems.

By End-User: Fleet Operators and Rideshare Drivers Lead Commercial Upswing

By End-User, private vehicle owners held 77.65% of 2025 revenue; fleet operators are expected to advance at a 12.21% CAGR to 2031. Private owners remain the largest by units, yet growth slows as the United Kingdom nears 31% penetration. Fleet operators, rideshare drivers, and law enforcement drive the fastest expansion as compliance and insurance clauses become stricter. Fraikin’s 60,000-vehicle rollout with Samsara showcases scale economics in video analytics.

Rideshare drivers in Madrid and Barcelona adopt dual-channel units to protect against false passenger claims, while municipal fleets in France outfit vans to document service disputes. The split forces vendors to address two value propositions: low-cost evidence capture versus high-touch enterprise integration.

Geography Analysis

The United Kingdom captured 28.85% of 2025 revenue, anchored by Operation Snap’s 125,000 video submissions that led to enforcement in 70% of cases. Aviva’s dashcam app saves drivers GBP 170 USD 226.66 annually, and 81% of U.K. motorists know about usage-based insurance, accelerating device uptake. Home-grown leader Nextbase pilots innovations domestically before continental rollout. Despite saturation risk, replacement demand for 4K and dual-channel models sustains incremental gains.

Spain is the fastest climber at a 13.02% CAGR through 2031. Fleet-modernization mandates, rideshare expansion, and permissive evidence rules drive adoption in Madrid, Barcelona, and Valencia. Dual-channel cameras appeal to drivers eager to counter fraudulent claims, and insurers begin offering tiered discounts for 4K uploads.

Germany, France, and Italy jointly hold a roughly 39.80% share, yet grow more slowly owing to privacy and fragmentation. Germany’s April 2025 encryption rules inflate costs and create consumer hesitation. France allows recordings but limits retention to seven days. Italy clarified legality in 2024, boosting modest uptake. Fleets in France still realize 18% premium cuts after adding video, proving ROI can outweigh bureaucracy. Nordic and Eastern European markets start from low bases but will benefit from falling hardware prices and EU safety harmonization.

Regulatory Landscape

Dashcams in Europe sit at the intersection of vehicle safety requirements and data protection rules. Video recorded in public areas can fall under GDPR when use goes beyond a purely personal or household context, which makes many fleet, rideshare, rental, and employer deployments subject to controller obligations such as lawful basis, transparency, security, and data minimization. The European Data Protection Board (EDPB) has repeatedly emphasized that constant recording of traffic and nearby persons is a significant interference with rights and requires strict necessity and proportionality assessment, and it reiterated the compliance focus for in-car video cameras and dashcams in a May 2025 letter.

On the automotive side, EU safety regulation is tightening requirements that influence camera adoption and integration choices. The EU General Safety Regulation (EU) 2022/2144 applies to new vehicle types approved after July 2024 with mandates such as driver drowsiness and distraction warnings, supporting demand for cabin-facing monitoring and dual-channel retrofits in older fleets. In parallel, cybersecurity governance for connected vehicle systems is becoming more prominent via UN Regulation No. 155, and EU rules on secure on-board monitoring data transmission reference cybersecurity measures aligned to that framework, raising compliance expectations for connected, cloud-enabled, and OEM-integrated camera systems.

Value Chain Analysis

The value chain starts upstream with key components such as CMOS image sensors, lens modules, storage, GNSS modules, and application-specific SoCs that enable encoding, AI inference, and connectivity. Brand owners and ODM/OEM electronics manufacturers assemble single- and multi-channel devices, then add differentiating layers such as HDR/low-light tuning, driver-monitoring features, parking-mode power management, and tamper-resistant mounts. As product mix shifts toward connected smart dashcams, software stacks (device management, incident detection, driver coaching) and cloud storage/analytics increasingly shape gross margin and lock-in, particularly for fleet deployments.

Downstream, routes to market split between offline retail (including installers), direct-to-consumer e-commerce, and enterprise or fleet procurement through telematics platforms and integrators. Regulatory compliance is embedded across the chain: GDPR obligations (for commercial deployments) shift operational load onto fleet operators as data controllers, while suppliers respond with features such as encryption, access controls, and configurable retention to match local interpretations. For factory-fit and connected solutions, cybersecurity expectations aligned with UN Regulation No. 155 and secure data transmission requirements reinforce the role of established OEM ecosystems and partners that can document compliance across hardware, firmware, backend services, and support processes.

Competitive Landscape

Europe dashboard camera market competition is moderate, with the top three brands Nextbase, Garmin, and Samsara holding about 35%–40% share. Nextbase’s March 2025 purchase of an AI firm adds cloud analytics that underpin subscription bundles. Samsara’s alliance with Fraikin equips 60,000 trucks and demonstrates how software stickiness locks in fleets. Garmin targets mid-market consumers with 1440p units that integrate smartphone apps and GPS.

Smaller players such as VIOFO and Vantrue undercut on price with EUR 200 dual-channel 4K kits, winning retail share in Spain and Italy but lacking cloud ecosystems. Thinkware differentiates through tamper-proof hardware for insurance fraud defense. encroachment from Tesla, BMW, and Mercedes-Benz threatens after-market demand among new-car buyers, so vendors pivot toward older fleets and richer analytics. Compliance certifications under UN 169 create entry barriers that favor established brands capable of navigating multi-state regulation.

White-space remains in southern and eastern Europe where penetration is under 10%, and in premium aftermarket upgrades for vehicles without OEM systems. Partnerships with insurers and telematics platforms are emerging as the key axis of competition, shifting emphasis from lens quality to data-driven services.

Europe Dashboard Camera Industry Leaders

Pittasoft Co., Ltd.

MiTAC Europe Ltd. (Mio)

Vantrue Inc.

Portable Multimedia Ltd. (Nextbase)

Garmin Ltd.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

The clearest opportunity is in compliance-forward offerings for fleets and other commercial users who function as GDPR data controllers. The EDPB has highlighted the need for careful role assessment and safeguards for in-car video cameras and dashcams (May 2025), which supports demand for privacy-by-design capabilities such as strong encryption, strict retention controls, granular access management, and on-device processing that minimizes cloud transfer. Vendors that package cameras with controller-ready workflows (audit logs, consent/notice toolkits, configurable masking, and jurisdiction-specific firmware settings) align with the operational reality of logistics, rideshare, rental, and municipal fleets that must balance safety evidence needs with privacy restrictions.

A second opportunity is retrofit-grade dual-channel and smart systems that map to EU safety and operational requirements without waiting for full OEM rollouts. The General Safety Regulation (EU) 2022/2144, applicable to new vehicle types after July 2024 for features including driver drowsiness and distraction warnings, has increased attention on cabin-facing monitoring and higher-grade incident capture. Market activity already reflects this shift toward integrated video telematics, including Samsara deployments at scale with Fraikin and insurer-led discount programs such as Aviva, which reward drivers that can share footage and telematics data. These proof points support bundles combining hardware with subscription analytics, installation, and data governance, especially for the large parc of older vehicles across Europe that will not receive factory-fit camera systems quickly.

Recent Industry Developments

- January 2026: Nextbase launched its Vehicle Accessory as a Service (VAaaS) platform and announced a partnership with Mitsubishi Motors North America to offer dash cams through Mitsubishi dealerships. The platform formalizes a dealership-led distribution model that can standardize installation and support subscription attachment, reinforcing the shift from one-time hardware sales toward recurring services.

- December 2025: BlackVue (Pittasoft) launched the ELITE 10-2CH dual-channel 4K dash cam, highlighting fast boot performance and upgraded imaging with Sony STARVIS 2 sensors. This release raises the performance bar in the premium aftermarket and supports higher-ARPU bundles that pair 4K capture with connected features and fleet-grade reliability.

- April 2024: MiTAC Digital Technology announced a strategic collaboration with CANGO Mobility to integrate video telematics (MioEYE K Series) with CANbus vehicle data insights. Linking video with vehicle telemetry strengthens the enterprise value proposition for connected dashcams and positions suppliers closer to fleet-management workflows rather than standalone evidence capture.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers revenue generated in Europe from dashboard cameras (dash cams) that record driving footage, including front-facing units and systems sold as single-channel or dual-channel setups. The sizing reflects sales across passenger and commercial vehicles, across offline and online channels.

Scope exclusions: We exclude embedded ADAS sensing cameras, parking-assist camera modules, and general in-cabin security systems when they are not sold and used as dedicated dash cams.

Segmentation Overview

- By Technology

- Basic

- Smart

- By Product Type

- Single-Channel

- Dual-Channel

- Rear-View

- By Application

- Passenger Vehicles

- Commercial Vehicles

- By Video Quality/Resolution

- Standard Definition (SD)

- High Definition (HD)

- Full High Definition (FULL HD)

- Ultra High Definition (4K and Above)

- By Distribution Channel

- Online Retail

- Offline Retail

- By End-User

- Private Vehicle Owners

- Fleet Operators

- Law Enforcement and Emergency Services

- Rideshare and Taxi Drivers

- By Country

- United Kingdom

- Germany

- France

- Spain

- Italy

- Rest of Europe

Data Sources, Market Sizing, and Validation

Desk Research

Desk work starts with aligning what counts as a dash cam in Europe, and then mapping demand signals that can be checked year over year. We typically refer to public sources such as Eurostat trade and consumer indicators, UNECE vehicle safety and regulatory references, and national transport agencies for road safety statistics that influence adoption.

To keep assumptions grounded, we also review manufacturer product catalogs, public price listings from major retailers, company annual reports, and reputable press coverage on privacy rules and in-car recording acceptance by country. When needed, paid subscriptions are used only for company financials and intelligence, import and export shipment-level checks, and patent databases to sense feature cycles. These examples are not exhaustive, and many other public documents and datasets are also used for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work is used to confirm adoption by country, realistic pricing bands, and how fast features like dual-channel, parking mode, and connected storage are moving into the mass market. We speak with a mix of brands, distributors, retailers, installers, and fleet-oriented buyers across Europe so gaps from desk sources can be closed and assumptions can be rechecked before finalization.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 37% | CXOs: 13% | |

| Mid tier: 48% | Functional/Unit leaders: 33% | |

| Smaller Players: 15% | Managers: 54% |

Market-Sizing & Forecasting

The core sizing is built using a top-down model where vehicle parc and new registrations by country are translated into an addressable demand pool using dash cam penetration and replacement cycles, and then converted to value using blended average selling prices. The inputs are adjusted for practical market fingerprints, like the split between single-channel and dual-channel units, the mix shift toward higher resolution devices (for example 2K and 4K), and typical retail price spreads by channel.

We then corroborate totals using selective bottom-up approximations, such as rolling up sampled brand presence in key retailers, channel checks on unit volumes, and ASP-by-feature comparisons that help us spot overstatement in one country or undercount in another. For forecasting, scenario analysis is used and anchored to a small set of drivers that experts consistently cite, including privacy enforcement intensity, insurance-linked incentives, fleet adoption momentum, and consumer replacement timing. If a country-level variable is missing or inconsistent, it is proxied using a close peer market and then revalidated in follow-up calls.

Data Validation & Update Cycle

Model outputs are checked against independent signals, including trade movement direction, price trend logic, and whether the implied unit volumes match what channels describe as realistic. When a variance looks large, assumptions are reopened, and respondents are re-contacted to confirm if the change is structural, seasonal, or tied to a one-time event.

Before sign-off, the work goes through multiple analyst reviews where formulas, currency conversions, and year alignment are rechecked to avoid accidental drift. The report is refreshed annually, and interim updates are made when material events occur, such as regulatory changes or a sudden pricing reset. Right before delivery, a fresh pass is completed so clients receive the latest updated view.

Mordor Intelligence's Europe Dashboard Camera Market Estimate Compared With Other Published Estimates

Published market sizes for Europe dash cams often do not match, even when the topic sounds identical, because the scope and the counting rules are not consistent across publishers. Differences usually come from what products are included, whether passenger and fleet demand are both counted, and how pricing is treated across online and offline channels.

Some estimates fold in adjacent automotive camera categories or connected telematics services that sit next to dash cams in retail bundles. In Mordor Intelligence sizing, only dedicated dashboard camera hardware sold for continuous recording is counted, and embedded vehicle camera modules are left out, which keeps the value tied to the real dash cam purchase decision.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 1.28 B (2025) | |

| Global Consultancy A | USD 1.30 B (2024) | Uses a different base year and can blend earlier pricing levels with later adoption, so the implied ASP and penetration mix do not line up with the 2025 demand pool used here. |

| Trade Journal B | USD 1.55 B (2025) | Often groups dash cams with other in-car video and driver monitoring add-ons, which can inflate value when service attachments and non-dashcam camera modules are included in the same revenue bucket. |

The spread in the table is mainly explained by year alignment and what gets bundled into the definition of a dash cam sale. By keeping the inputs traceable to vehicle parc, adoption, replacement, and realistic channel pricing, the estimate stays easier to reproduce and easier to challenge when a country assumption changes.

Key Questions Answered in the Report

How large is the Europe dashboard camera market in 2026?

The Europe dashboard camera market size is USD 1.41 billion in 2026.

What is the projected growth rate for dashboard cameras in Europe?

Revenue is expected to rise at a 10.36% CAGR from 2026 to 2031.

Why are dual-channel dashcams gaining popularity?

Dual-channel units meet new EU driver-monitoring mandates and help fleets curb fraud, driving a 12.18% CAGR.

Which country leads European sales of dashboard cameras?

The United Kingdom leads with 28.85% revenue share as of 2025.

How do insurers encourage dashcam adoption?

Discounts such as Aviva’s GBP 170 annual savings incentivize policyholders to install and share dashcam footage.

Which vendors dominate the European dashcam landscape?

Nextbase, Garmin, and Samsara together hold about 35%-40% of market revenue.

Page last updated on: