Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

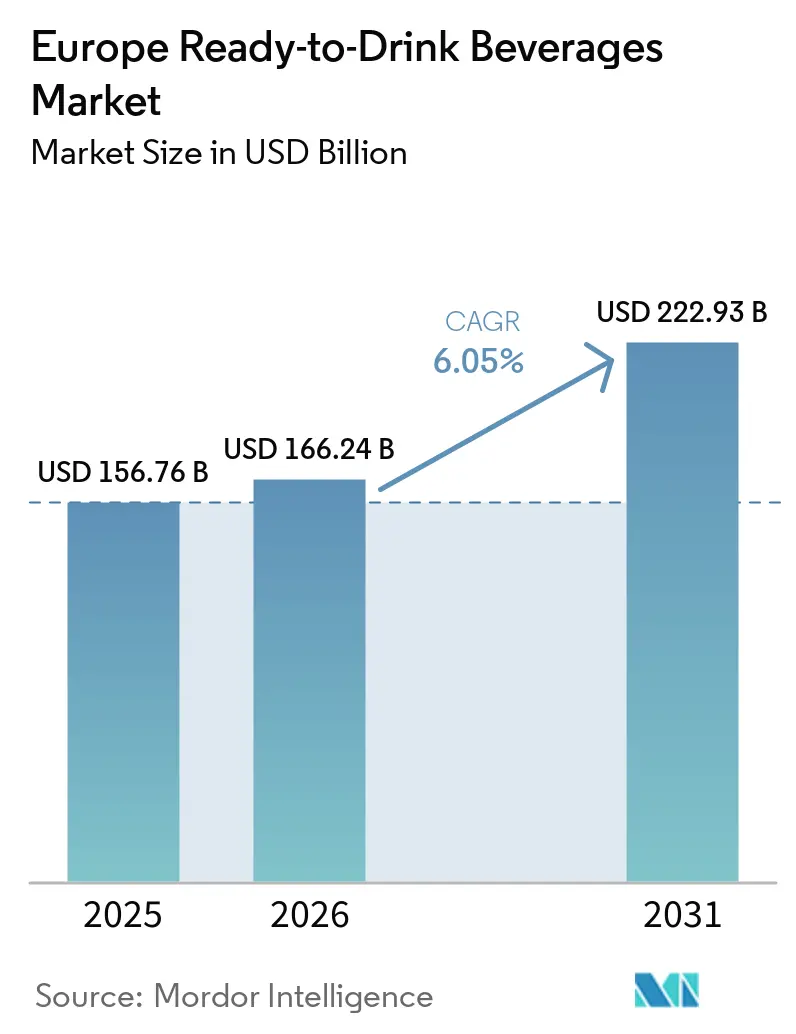

| Base Year Market Size (2025) | USD 156.76 Billion |

| Market Size (2026) | USD 166.24 Billion |

| Market Size (2031) | USD 222.93 Billion |

| Growth Rate (2026 - 2031) | 6.05% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Ready-to-Drink Beverages Market Analysis by Mordor Intelligence

Europe Ready-to-Drink Beverages Market size in 2026 is estimated at USD 166.24 billion, growing from 2025 value of USD 156.76 billion with 2031 projections showing USD 222.93 billion, growing at 6.05% CAGR over 2026-2031. This trajectory reflects a fundamental shift in consumer behavior toward convenience-driven consumption patterns, where traditional beverage preparation gives way to grab-and-go solutions that align with increasingly mobile lifestyles. The market's resilience stems from its ability to adapt to evolving wellness priorities while maintaining the convenience factor that initially drove adoption. Expansion is underpinned by consumers’ preference for grab-and-go formats that fit mobile lifestyles, growing willingness to trade up for functional benefits, and the sector’s quick adaptation to EU sustainability rules that favor recyclable packaging. Multinational bottlers are raising factory investments to localize output and shorten supply chains, cushioning the Ready-to-Drink beverages market from import-related volatility. Spain's accelerated growth trajectory correlates with tourism sector expansion and increased consumer spending on premium beverage categories [1]Source: U.S Department of Agriculture, "Spain: Exporter Guide Annual", fas.usda.gov. Packaging innovation drives segment transformation, with PET/glass bottles holding 50.43% market share in 2024, yet aseptic cartons/Tetra Packs recording the fastest growth at 8.30% CAGR through 2030. This shift reflects regulatory pressure from the EU's Packaging and Packaging Waste Regulation, effective February 2025, which mandates recyclability standards and minimum recycled content requirements [2]Source: European Commission, "New EU regulation promotes the procurement of sustainable packaging", green-forum.ec.europa.eu.

Key Report Takeaways

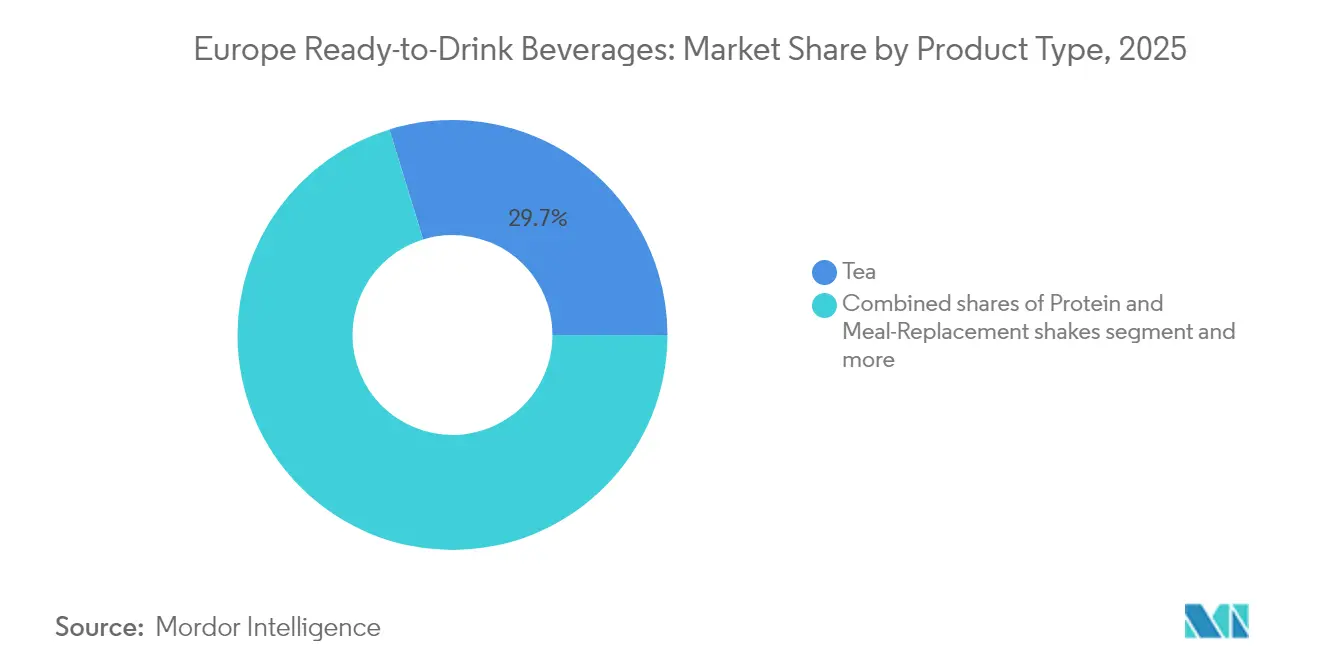

- By product type, tea led with 29.74% of Ready-to-Drink beverages market share in 2025 while protein and meal-replacement shakes advanced at a 7.05% CAGR through 2031.

- By packaging type, PET/glass bottles commanded 49.62% of the Ready-to-Drink beverages market size in 2025; aseptic cartons/Tetra Packs are forecast to grow at 7.92% CAGR to 2031.

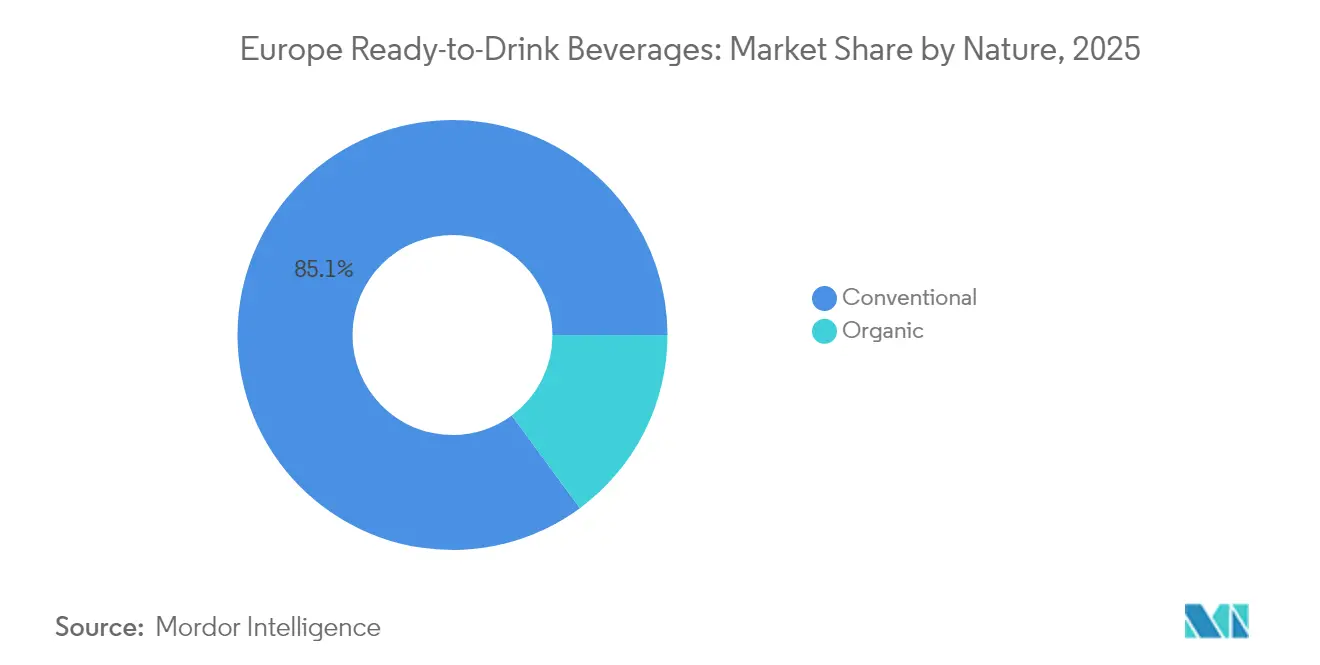

- By nature, conventional lines held 85.10% share of the Ready-to-Drink beverages market size in 2025 and organic variants are tracking a 6.55% CAGR over the same span.

- By distribution, supermarkets/hypermarkets captured 64.85% share in 2025, whereas online retail stores are set to expand at 7.18% CAGR to 2031.

- By geography, the United Kingdom accounted for 25.10% of the Ready-to-Drink beverages market size in 2025; Spain exhibits the fastest growth at 8.43% CAGR for 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Ready-to-Drink Beverages Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Consumer Preference for Convenient, On-The-Go Beverages | +1.2% | Global, with highest impact in UK, Germany, France | Medium term (2-4 years) |

| Increasing Demand for Functional and Wellness-Based RTD Drinks | +1.5% | Europe-wide, particularly strong in Nordic countries and Netherlands | Long term (≥ 4 years) |

| Product Innovation with New Flavors and Ingredients | +0.8% | Germany, UK, France leading innovation adoption | Short term (≤ 2 years) |

| Growing Popularity of Organic and Natural Beverages | +0.9% | Germany, Sweden, Netherlands, with spillover to Central Europe | Medium term (2-4 years) |

| Sustainability Trends Driving Eco-Friendly Packaging Adoption | +1.1% | EU-wide due to PPWR regulation, strongest in Germany and Nordics | Long term (≥ 4 years) |

| Expansion of Modern Retail and E-commerce | +0.7% | Western Europe mature markets, Eastern Europe emerging | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing Consumer Preference for Convenient, On-The-Go Beverages

European consumers increasingly prioritize convenience over traditional beverage preparation methods, driving fundamental changes in consumption patterns across demographic segments. The convenience channel is growing rapidly, with European markets showing particularly strong adoption. France exemplifies this trend with convenience stores recording 48% sales increases, while major retailers like Asda, Waitrose, and Marks & Spencer expand convenience formats to capture shifting shopping behaviors. This transformation reflects urbanization patterns where time-pressed consumers seek immediate gratification solutions, particularly among younger demographics who view convenience as a premium service worth paying for. The trend accelerates in metropolitan areas where commuting patterns and extended working hours create demand for portable nutrition solutions. Mobile consumption occasions now represent the fastest-growing segment within the broader RTD category, suggesting that convenience transcends mere product availability to encompass consumption context optimization.

Increasing Demand for Functional and Wellness-Based RTD Drinks

Functional beverage adoption reaches critical mass across European markets, with 39% of British consumers regularly consuming functional drinks, indicating mainstream acceptance beyond niche health segments. The European functional beverage market, demonstrates sustained momentum with energy drinks commanding a significant market share while RTD coffees and teas grow at a substantial CAGR. Consumer motivations center on health and wellness priorities, with 58% prioritizing natural ingredients over synthetic alternatives, reflecting post-pandemic consciousness shifts toward preventive health measures. The meal replacement segment projects exceptional growth, driven by integration with weight-loss medications like GLP-1 and demand for plant-based, high-protein formulations. Regulatory frameworks like EFSA's nutrition application guidelines ensure product safety while enabling innovation in functional ingredient incorporation. The trend extends beyond traditional sports nutrition into cognitive enhancement, digestive health, and immunity support, creating opportunities for brands to differentiate through targeted health benefits.

Product Innovation with New Flavors and Ingredients

Innovation cycles accelerate across European RTD markets, with companies introducing novel flavor profiles and functional ingredients to capture consumer attention in saturated categories. PepsiCo's launch of prebiotic cola represents breakthrough innovation in traditional cola segments, combining familiar taste profiles with gut health benefits to appeal to health-conscious consumers. Tea-based innovations demonstrate creativity, with brands like Twinings introducing sparkling tea lines featuring functional vitamins and minerals while maintaining under 50 calories per serving. The RTD tea segment positions itself as a healthier alternative to bottled water, with Asian-inspired formulations gaining traction across European markets. Herbal tisanes like hibiscus and rooibos gain popularity for their antioxidant properties, while cross-category innovations blend protein with traditional tea formats to create hybrid products. Innovation success increasingly depends on balancing taste expectations with functional benefits, as consumer testing shows 90% willingness to recommend products that deliver on both dimensions.

Growing Popularity of Organic and Natural Beverages

Organic beverage consumption demonstrates resilience despite economic pressures, with the European organic coffee market stabilizing at 133,000 tonnes in 2023, led by Germany's 44% import share [3]Source: CBI (Centre for the Promotion of Imports from developing countries), "European market potential for organic coffee", cbi.eu. Spain's organic imports surge 134% since 2018, indicating emerging market appetite for premium organic products despite price sensitivity concerns. Consumer preference for clean label formulations intensifies, with a smaller share of RTD beverage consumers prioritizing clean ingredients when making purchase decisions. The clean label movement evolves beyond ingredient simplicity to encompass environmental responsibility and supply chain transparency, creating competitive advantages for brands that communicate sustainability credentials effectively. Natural food additives market growth supports this trend, driven by EU regulations favoring natural alternatives over synthetic options and consumer focus on transparency. Organic certification requirements become more stringent under EU Regulation 2018/848, effective from 2025, potentially creating barriers for smaller producers while benefiting established organic brands with robust compliance systems.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply Chain Disruptions Impacting Availability of Raw Materials and Packaging | -0.8% | Global impact, particularly affecting Eastern Europe and supply-dependent markets | Short term (≤ 2 years) |

| Strict Regulatory Requirements on Ingredients, Labeling, And Advertising Limiting Product Formulations | -0.6% | EU-wide, with varying compliance costs across member states | Medium term (2-4 years) |

| Consumer Skepticism Around Additives and Preservatives Deterring Some Buyers | -0.4% | Northern Europe and Germany leading skepticism, spreading to other markets | Long term (≥ 4 years) |

| Challenges In Preserving Product Freshness and Shelf-Life Without Compromising Quality | -0.5% | Particularly challenging in Southern Europe due to climate, affecting distribution | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply Chain Disruptions Impacting Availability of Raw Materials and Packaging

Supply chain vulnerabilities intensify across European RTD beverage manufacturing, with aluminum can costs increasing 15-20% due to tariff implementations effective April 2025. Coffee bean prices face potential increases up to 46% under new tariff structures, directly impacting RTD coffee segment profitability and forcing manufacturers to consider reformulation or price adjustments. Mid-single-digit food inflation projections create consumer price sensitivity, leading to increased private-label preference and demand for value justification from premium brands. Supply chain complexities extend beyond cost pressures to include longer lead times and quality inconsistencies, particularly affecting smaller manufacturers with limited supplier diversification capabilities. The European beverage industry responds through supply chain fortification strategies, including ingredient localization, supplier diversification, and strategic inventory management to mitigate disruption impacts. Raw material availability challenges intensify during peak demand periods, creating potential stockout situations that benefit competitors with more resilient supply networks.

Strict Regulatory Requirements on Ingredients, Labeling, And Advertising Limiting Product Formulations

European regulatory frameworks create increasingly complex compliance landscapes for RTD beverage manufacturers, with Regulation (EC) No 1333/2008 establishing stringent food additive approval processes that limit formulation flexibility. EFSA's nutrition application guidelines require extensive scientific documentation for health claims, creating barriers for smaller companies lacking regulatory expertise and financial resources for clinical studies. The Union list of novel foods restricts ingredient innovation, requiring pre-market authorization for new functional ingredients that could differentiate products in competitive markets. Labeling requirements under EU food law mandate comprehensive ingredient disclosure and nutritional information, increasing packaging costs while limiting marketing message space. Advertising restrictions particularly impact functional beverage claims, requiring substantiation that may not align with consumer perception or marketing objectives. The regulatory burden disproportionately affects innovative formulations, potentially stifling product development cycles and favoring established ingredients with proven regulatory pathways.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Tea Dominance Meets Protein Innovation

Tea maintains commanding market leadership with 29.74% share in 2025, reflecting European consumers' historical preference for traditional beverage categories and growing appreciation for functional tea formulations. Protein and meal-replacement shakes emerge as the fastest-growing segment at 7.05% CAGR for 2026-2031, driven by mainstream adoption beyond traditional sports nutrition demographics and integration with weight management programs. Coffee products capture significant market presence through RTD innovations. Energy and sports drinks maintain steady performance despite regulatory scrutiny over caffeine content and marketing practices targeting younger consumers. Fruit and vegetable juice segments face pressure from sugar reduction initiatives while benefiting from clean label trends and premium positioning strategies.

The tea segment undergoes significant transformation through functional ingredient incorporation and innovative packaging formats, with brands like Twinings launching sparkling tea lines that deliver vitamins and minerals while maintaining under 50 calories per serving. Dairy-based RTD products benefit from protein trend convergence, while others category including functional waters and isotonics captures growth through specialized hydration solutions. The protein segment's exceptional growth trajectory reflects consumer shift toward convenient nutrition solutions, with Starbucks partnering with Arla to launch high-protein iced coffee containing 20 grams of protein per 330ml serving. Market dynamics suggest continued premiumization across all product categories, with innovation focusing on functional benefits rather than traditional taste differentiation.

By Packaging Type: Sustainability Drives Carton Growth

PET and glass bottles command 49.62% market share in 2025, benefiting from consumer familiarity and premium positioning advantages, yet face increasing pressure from sustainability regulations and environmental consciousness. Aseptic cartons and Tetra Packs record the fastest growth at 7.92% CAGR for 2026-2031, driven by the EU's Packaging and Packaging Waste Regulation requiring recyclability standards and consumer preference for environmentally sound packaging options. Tetra Pak advocates for carton adoption over traditional tin cans, emphasizing sustainability benefits while majority of food and beverage companies accept cost-related trade-offs for sustainable practices. Cans maintain market presence through aluminum's recyclability advantages, though face cost pressures from 15-20% price increases due to tariff implementations. Others category including pouches and paperboard packaging gains traction through innovative formats that address convenience and sustainability simultaneously.

The packaging landscape transformation accelerates through regulatory mandates requiring 30% recycled content for PET food packaging by 2030, rising to 50% by 2040, fundamentally altering supply chain economics and material sourcing strategies. Consumer research indicates cartons receive the most favorable environmental perception compared to plastic alternatives, with 42% willing to pay premium prices for environmentally sound packaging. The regulation's requirement for 10% reusable beverage packaging creates opportunities for innovative packaging solutions while challenging traditional single-use models. Deposit return systems become mandatory by 2029, targeting 90% collection rates and fundamentally altering consumer interaction with packaging across all formats.

By Nature: Organic Growth Accelerates Despite Premium Pricing

Conventional products maintain overwhelming dominance with 85.10% market share in 2025, reflecting price sensitivity and established consumer habits, yet organic alternatives capture accelerating growth at 6.55% CAGR for 2026-2031. Consumer willingness to pay premium prices for organic certification creates sustainable profit margins that justify higher production costs and complex supply chain requirements. The clean label movement extends beyond organic certification to encompass natural ingredients, environmental responsibility, and supply chain transparency, creating competitive advantages for brands that effectively communicate sustainability credentials.

Regulatory frameworks become more stringent under EU Regulation 2018/848, effective from 2025, potentially creating barriers for smaller producers while benefiting established organic brands with robust compliance systems. The organic segment benefits from health-conscious consumer trends and post-pandemic awareness of preventive health measures, with 29% of RTD beverage consumers prioritizing clean ingredients when making purchase decisions. Premium positioning strategies enable organic products to maintain higher margins despite lower volumes, creating sustainable business models for specialized producers. Market expansion depends on education efforts that communicate organic benefits beyond environmental impact to include health advantages and taste differentiation.

By Distribution Channel: E-commerce Disrupts Traditional Retail

Supermarkets and hypermarkets maintain dominant position with 64.85% market share in 2025, leveraging established consumer shopping patterns and comprehensive product assortments, yet face increasing pressure from convenience-focused alternatives. Online retail stores emerge as the fastest-growing channel at 7.18% CAGR for 2026-2031, driven by subscription models, bulk purchasing options, and convenience-seeking consumer behaviors accelerated by digital transformation. Convenience and grocery stores benefit from changing shopping patterns, with the convenience channel growing significantly at global level and France recording 48% sales increases in convenience formats. Other distribution channels including vending machines and foodservice outlets adapt to post-pandemic consumption patterns while capturing impulse purchase opportunities.

The digital transformation reveals significant opportunities for market expansion, with European e-commerce reaching more than 67% penetration among individuals aged 16-74 in 2023, representing continued growth potential. PepsiCo's European digital strategy analysis reveals untapped potential, with only 19% of Spanish food delivery platforms listing PepsiCo products compared to 38.5% in France, indicating substantial room for digital distribution expansion. Major European retailers including Asda, Waitrose, and Marks & Spencer expand convenience store offerings to capture changing consumer preferences for immediate access and smaller basket sizes. The integration of online and offline channels creates omnichannel experiences that enhance customer engagement while providing valuable data insights for targeted marketing and inventory optimization strategies.

Geography Analysis

The United Kingdom maintains its position as Europe's largest RTD beverage market with 25.10% share in 2025 yet faces growth deceleration as market maturity limits expansion opportunities compared to emerging European markets. British consumers demonstrate sophisticated preferences for functional beverages, with 39% regularly consuming energy drinks, protein shakes, or probiotic beverages, indicating mainstream acceptance beyond niche health segments. The UK market benefits from advanced retail infrastructure and high e-commerce penetration rates, supporting omnichannel distribution strategies that enhance consumer accessibility according to the International Trade Administration. Brexit continues reshaping supply chain dynamics and regulatory frameworks, creating both challenges through increased compliance costs and opportunities through regulatory flexibility that may enable faster product innovation cycles.

Spain emerges as Europe's fastest-growing RTD beverage market at 8.43% CAGR for 2026-2031, driven by economic recovery with projected 1.9% GDP growth in 2024 and tourism sector revitalization that enhances consumption opportunities. The market benefits from strategic investments like Nestlé's new coffee factory, reflecting confidence in long-term growth prospects and local production capabilities. Consumer behavior shifts toward prioritizing value while maintaining interest in premium categories, creating opportunities for brands that balance quality with affordability. Spain's packaging regulations through the Real Decreto de Envases create compliance requirements that may favor larger manufacturers with resources to adapt quickly to changing standards.

Germany, Italy, France, Netherlands, Poland, Belgium, Sweden, and other European markets contribute diverse growth patterns reflecting varying economic conditions, consumer sophistication, and regulatory environments. France demonstrates the highest beverage penetration rate, with convenience stores recording significant sales increases, indicating strong consumer adoption of on-the-go consumption patterns. The collective European market benefits from regulatory harmonization through the EU's Packaging and Packaging Waste Regulation, effective February 2025, which creates consistent sustainability standards while potentially favoring larger manufacturers with compliance resources. Regional consolidation trends continue reshaping competitive landscapes, with cross-border acquisitions and partnerships enhancing distribution capabilities and market access across multiple European territories.

Competitive Landscape

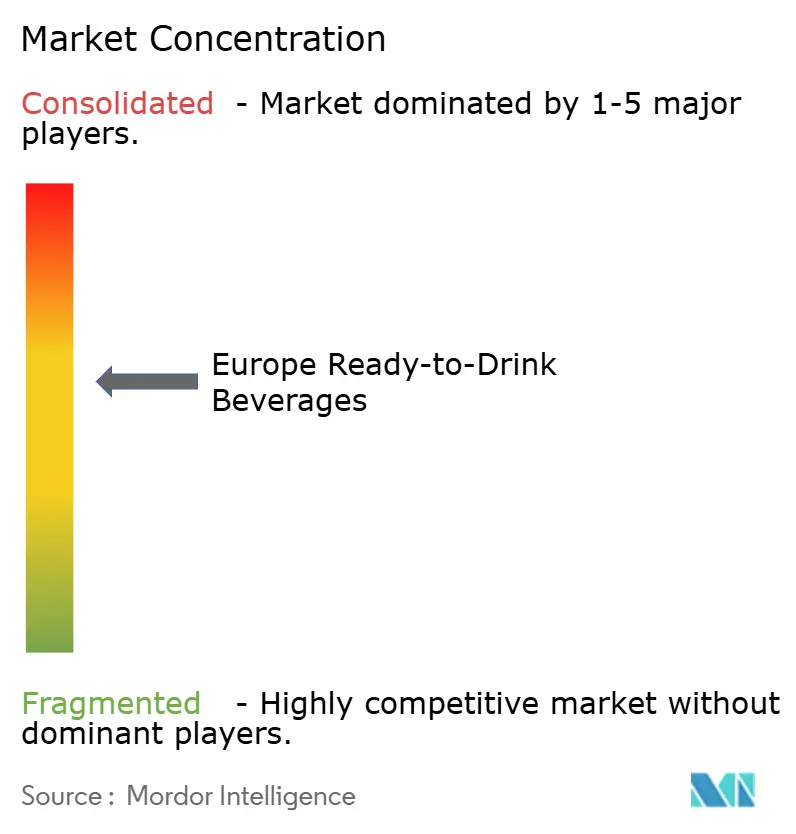

The European RTD beverage market exhibits moderate concentration rating, indicating sufficient competitive intensity to drive innovation while allowing established players to maintain strategic advantages through scale economies and distribution networks. Market leaders including PepsiCo, Nestlé S.A., The Coca-Cola Company, Starbucks, etc. pursue differentiation strategies focused on functional innovation, premium positioning, and sustainable packaging solutions rather than traditional price competition. PepsiCo's launch of prebiotic cola demonstrates breakthrough innovation in mature categories, while Coca-Cola's partnership with illycaffé for premium RTD coffee targets the nearly USD 10 billion global market through joint venture structures. Consolidation activities reshape competitive dynamics, with Carlsberg's GBP 3.3 billion Britvic acquisition creating enhanced multi-beverage capabilities and potential cost synergies of GBP 100 million over five years.

Technology adoption focuses on digital distribution optimization, with significant gaps in platform presence creating opportunities for market share gains through improved online availability. Opportunities emerge in functional beverage segments where traditional players lack expertise, enabling specialized companies to capture growth through targeted health benefits and clean label positioning. The meal replacement segment projects exceptional expansion exceeding GBP 19 billion by 2030, attracting new entrants with plant-based formulations and personalized nutrition approaches.

Emerging disruptors leverage direct-to-consumer models and subscription services to bypass traditional retail gatekeepers while building brand loyalty through personalized experiences. Regulatory compliance under the EU's Packaging and Packaging Waste Regulation creates competitive advantages for companies with advanced sustainability capabilities, potentially disadvantaging smaller players lacking resources for compliance investments. Innovation cycles accelerate through bioscience applications for natural preservation and functional ingredient development, requiring continuous R&D investment to maintain competitive positioning in rapidly evolving market segments.

Europe Ready-to-Drink Beverages Industry Leaders

-

Monster Beverage Corporation

-

Nestlé S.A.

-

SUNTORY HOLDINGS LIMITED

-

PepsiCO

-

The Coca‑Cola Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Rémy Cointreau’s Metaxa brand rolled out a duo of canned cocktails across Europe. The Peach Spritz and Ginger and Lime Long Drink variants hit the shelves in 25cl cans, boasting an ABV of 5%. The launch coincided with a new marketing push titled ‘Get your cocktails ON’.

- May 2025: Müller Yogurt and Desserts and Myprotein expanded their collaboration, launching a ready-to-drink (RTD) protein shake alongside two high-protein yogurts. The RTD protein shakes, available in 385ml, were offered in chocolate and strawberry flavours, each delivering 25g of protein with a low-fat, no-added-sugar formulation. The new products were made available across various retailers in the UK.

- February 2025: Emmi launched Caffè Latte Zero, a ready-to-drink coffee devoid of added sugar or sweeteners, marking what it touted as a first for the UK market. Crafted solely from coffee and milk, the new product aims at health-conscious consumers, responding to the rising demand for lower-sugar alternatives. Caffè Latte Zero hit the shelves exclusively at Tesco on 3 March 2025, retailing at an RRP of GBP 1.85 for a 230 ml bottle.

- January 2025: Through a new partnership, Dilmah Craft Iced Tea became available to consumers across the Netherlands in a convenient 330ml can format. Renowned for its refreshing and natural taste, Dilmah Craft Iced Tea delivers the benefits of Ceylon tea. It is crafted from handpicked tea leaves sourced from Sri Lanka's tea gardens and brewed on-site to preserve its freshness, flavor, and antioxidant properties.

Europe Ready-to-Drink Beverages Market Report Scope

Ready-to-drink beverages are single-use beverages that are packaged ready for immediate consumption upon purchase. There are different types of RTD beverages, each serving a different purpose. As per our study scope, we have considered all the prominent product categories like Tea, Coffee, Energy Drinks, Fruit & Vegetable Juice, etc.

The Europe ready-to-drink beverages market is segmented by product type, distribution channel, and country. By product type, the market is segmented into tea, coffee, energy drinks, fruits & vegetable juice, dairy-based beverages, and others, By distribution channel, the market is segmented into supermarkets/hypermarkets, convenience stores, online retail stores, and other distribution channels. Also, the study analyzes the RTD beverages market in emerging and established markets across Europe, including the United Kingdom, Germany, France, Russia, Italy, Spain, and the Rest of Europe. The report offers market size and forecasts for Europe ready-to-drink-beverages market in value (USD million) for all the above segments.

By Product Type

| Tea |

| Coffee |

| Energy/Sports Drinks |

| Fruit and Vegetable Juice |

| Dairy-based RTD |

| Protein and Meal-Replacement Shakes |

| Others |

By Packaging Type

| PET/Glass Bottles |

| Cans |

| Aseptic Cartons/Tetra Packs |

| Others |

By Nature

| Conventional |

| Organic |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Convenience/Grocery Stores |

| Online Retail Stores |

| Other Distribution Channels |

By Geography

| Germany |

| United Kingdom |

| Italy |

| France |

| Spain |

| Netherlands |

| Poland |

| Belgium |

| Sweden |

| Rest of Europe |

| By Product Type | Tea |

| Coffee | |

| Energy/Sports Drinks | |

| Fruit and Vegetable Juice | |

| Dairy-based RTD | |

| Protein and Meal-Replacement Shakes | |

| Others | |

| By Packaging Type | PET/Glass Bottles |

| Cans | |

| Aseptic Cartons/Tetra Packs | |

| Others | |

| By Nature | Conventional |

| Organic | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Convenience/Grocery Stores | |

| Online Retail Stores | |

| Other Distribution Channels | |

| By Geography | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current value and growth outlook for Europe’s Ready-to-Drink beverages?

The Ready-to-Drink beverages market size is USD 166.24 billion in 2026 and is forecast to hit USD 222.93 billion by 2031 at a 6.05% CAGR.

Which product segment shows the strongest growth momentum?

Protein and meal-replacement shakes lead with a 7.05% CAGR through 2031, fueled by mainstream demand for convenient high-protein nutrition.

How will EU packaging rules influence beverage formats?

The 2025 regulation requires all packs to be recyclable by 2030 and 30% recycled content in PET, driving rapid adoption of cartons and reusable systems.

Which sales channel is expanding fastest?

Online retail stores are projected to grow at 7.18% CAGR thanks to high internet penetration and subscription models that encourage repeat purchasing.

Page last updated on: