Car Sharing Telematics Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

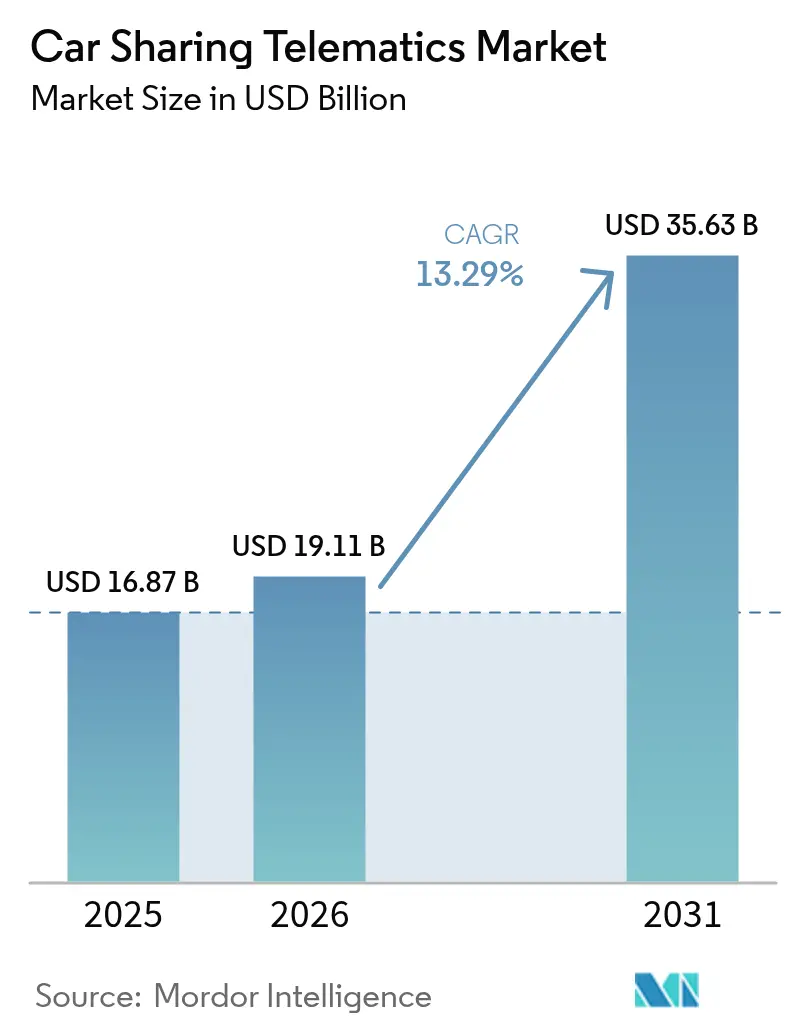

| Market Size (2026) | USD 19.11 Billion |

| Market Size (2031) | USD 35.63 Billion |

| Growth Rate (2026 - 2031) | 13.29% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Europe |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Car Sharing Telematics Market Analysis by Mordor Intelligence

Car Sharing Telematics Market size in 2026 is estimated at USD 19.11 billion, growing from 2025 value of USD 16.87 billion with 2031 projections showing USD 35.63 billion, growing at 13.29% CAGR over 2026-2031.

Expansion is driven by tighter urban congestion policies, mandatory in-vehicle safety regulations, and a rapid infusion of IoT-enabled fleet management architectures, which together redefine urban mobility economics. Europe retains a 37% revenue lead, driven by eCall compliance and long-standing shared-mobility ecosystems, whereas the Asia Pacific registers the fastest pace at 14.51% CAGR, largely due to smart-city spending and autonomous-vehicle pilots. Embedded connectivity, cloud analytics, and battery-electric-vehicle (BEV) proliferation combine to raise telematics complexity and opportunity across all major business models. The resulting data deluge underpins new revenue pathways in usage-based insurance, MaaS aggregation, and energy management, cementing telematics as the core digital spine of shared mobility.

Key Report Takeaways

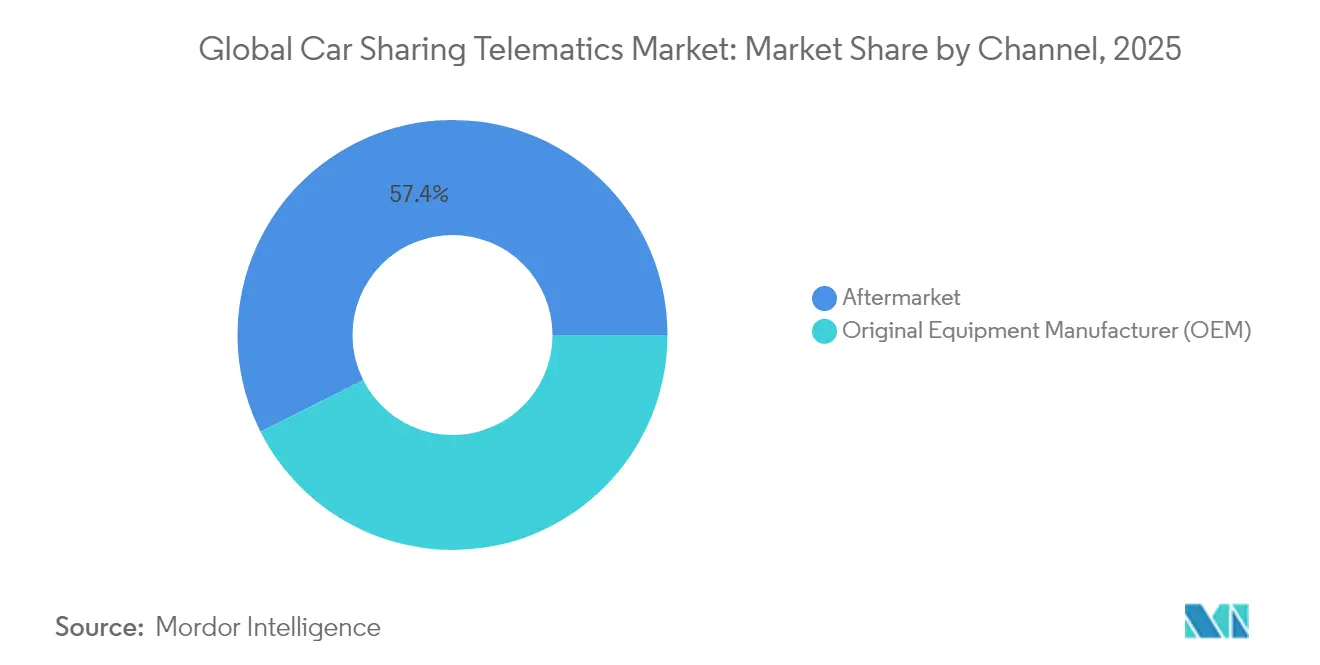

- By channel, the aftermarket segment secured 57.42% of the car sharing telematics market share in 2025, while OEM-embedded solutions are advancing at a 14.92% CAGR through 2031.

- By form factor, integrated telematics platforms are expanding at 16.65% CAGR, overtaking embedded solutions that held 45.48% revenue share in 2025.

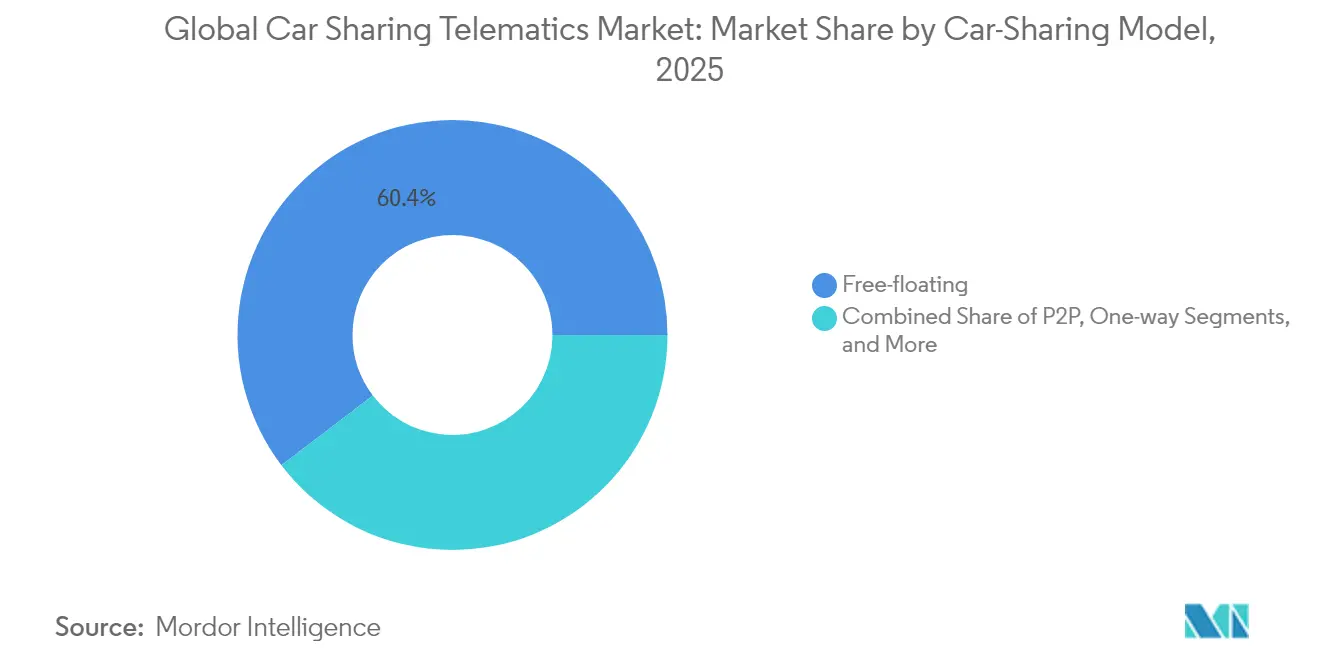

- By car-sharing model, free-floating services commanded 60.35% revenue in 2025; peer-to-peer platforms are projected to grow at 18.74% CAGR to 2031.

- By vehicle propulsion, BEVs accounted for 39.28% of the car sharing telematics market size in 2025 and are growing at 22.38% CAGR through 2031.

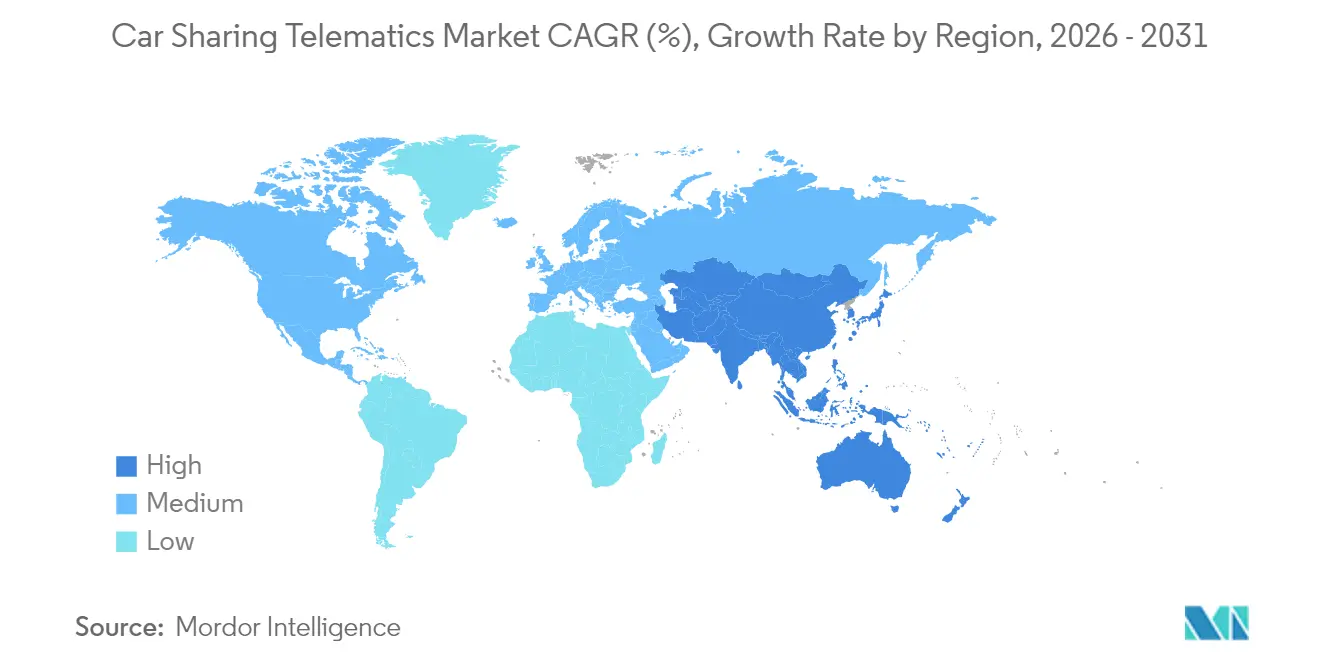

- By region, Europe led with 36.62% revenue in 2025, whereas Asia Pacific is forecast to log the fastest 14.33% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Car Sharing Telematics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing urban preference for shared mobility | +2.8% | Global tier-1 cities | Medium term (2–4 years) |

| Government mandates for vehicle telematics (eCall, safety) | +2.1% | Europe, North America, emerging APAC | Short term (≤2 years) |

| Integration of IoT/AI/ML for fleet optimization | +2.4% | North America and Europe | Medium term (2–4 years) |

| Rapid electrification of car-sharing fleets | +1.9% | Europe, China, California | Long term (≥4 years) |

| Usage-based-insurance partnerships lowering OPEX | +1.6% | North America and Europe | Medium term (2–4 years) |

| API-first telematics platforms enabling MaaS aggregation | +1.4% | Global tech hubs | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Growing Urban Preference for Shared Mobility

Continued densification and escalating congestion-charging schemes are shifting commuter economics toward shared fleets, nudging municipal planners to re-allocate curb space for multimodal mobility hubs that integrate car sharing, micro-mobility, and public transit. Free-floating operators use real-time heat-map telemetry to reposition vehicles in zones of peak demand, cutting customer wait times and trimming fleet idle minutes. In Munich and Berlin, usage clusters align with demographic density and proximity to subway interchanges, confirming location analytics as a core profitability lever. Dynamic-pricing engines, trained on weather feeds and event calendars, optimize vehicle distribution while lowering per-ride emissions footprints. Such urban network effects underscore why investors continue to back car sharing telematics market platforms that internalize both transportation and environmental externalities.

Government Mandates for Vehicle Telematics (eCall, Safety)

Regulators are accelerating adoption by making telematics a legal obligation. Under the EU General Safety Regulation II, all new M1 and N1 vehicles must feature intelligent speed assistance, automatic emergency-braking, and event-data recorders from July 2024.[1]Continental AG, “General Safety Regulation II Explained,” continental-automotive.com Next-Generation eCall shifts the emergency-alert backbone from 2G/3G to 4G/5G, demanding hardware refreshes across car-sharing fleets.[2]Keysight Technologies, “Advancing Automotive eCall Testing,” keysight.comComparable frameworks are rolling out in Russia and Brazil, and the FCC is reviewing a similar mandate, giving scale economies to vendors able to standardize multi-region compliance. Vehicles upgraded for NG-eCall deliver richer crash datasets that operators now monetize through safer-driving programs and refined insurance pricing.

Integration of IoT/AI/ML for Fleet Optimization

AI-enabled telematics platforms process upward of 300 vehicle signals per second to predict component failures, optimize charging windows, and personalize in-app offers. Geotab forecasts industry-wide migration to edge-AI architectures that embed machine-learning accelerators in telematics control units, slashing cloud-compute costs and latency.[3]Geotab, “Top Fleet Trends 2025,” geotab.comV2X interoperability leveraging 5G bandwidth allows shared cars to coordinate lane merges and parking maneuvers, boosting average fleet utilization. HARMAN’s 5G-ready control unit exemplifies the shift from connectivity modules to holistic vehicular computers, a prerequisite for Level-4 autonomy deployment.

Rapid Electrification of Car-Sharing Fleets

Operational math favors BEVs in shared fleets: centralized depots lower charging overhead, regenerative braking cuts wear, and predictable daily mileage eases range anxiety. ChargePoint’s telematics suite co-optimizes route scheduling and charger assignment, reducing per-mile energy costs by double digits. Renault Group’s Utrecht pilot shows Vehicle-to-Grid (V2G) participation earning ancillary revenue while keeping state-of-charge within warranty limits.[4]Renault Group, “Utrecht Vehicle-to-Grid Pilot,” renaultgroup.com The push toward 800-V architectures heightens requirements for thermal-management telemetry and silicon-carbide inverter diagnostics, expanding the bill of materials for car sharing telematics market hardware.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High hardware and installation costs | -1.8% | Global, price-sensitive markets | Short term (≤2 years) |

| Data-privacy and cyber-security concerns | -1.4% | Europe, North America | Medium term (2–4 years) |

| Lack of telematics interoperability standards | -1.1% | Global | Long term (≥4 years) |

| Low utilization in suburban and rural zones | -0.9% | North America suburbs, rural Europe and APAC | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Hardware and Installation Costs

Silicon supply constraints and escalating sensor counts are pushing semiconductor content per vehicle toward USD 1,200 by 2030, doubling 2022 levels, a trend highlighted by NITI Aayog’s component-cost tracking. Upgrading fleets from 4G to 5G radios elevates module prices yet delivers minimal payback until low-latency apps reach scale. Consequently, smaller operators defer refresh cycles or seek subscription models that spread capital outlay across contractual terms. Strategic OEM-tier-one alliances—Geotab with Volkswagen Group, Samsara with Stellantis—are emerging to unlock purchase discounts and shared R&D while ensuring compliance updates flow over-the-air rather than via costly service campaigns.

Data-Privacy and Cyber-Security Concerns

Europe’s GDPR necessitates explicit user consent for location, behavioral, and biometric tracking, forcing developers to adopt privacy-by-design architectures with local data minimization. A 2024 European survey found 67% of drivers trust automakers with their data, but only 33% extend that trust to third-party app providers—placing car-sharing platforms under added scrutiny. Tesla’s documented camera-data leakage underscores reputational stakes and motivates investment in end-to-end encryption and penetration testing. Cyber intrusions ranging from key-relay hacks to CAN-bus injections compel layered defenses, further inflating total cost of ownership for telematics rollouts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Channel: OEM Integration Accelerates Despite Aftermarket Dominance

In 2025, aftermarket retrofits dominated with 57.42% revenue, reflecting the sizeable legacy vehicle pool. Yet OEM-embedded units are advancing at 14.92% CAGR, helped by factory-level compliance with eCall-style mandates and tighter cybersecurity hardening. Automakers now expose on-board APIs that furnish granular battery, ADAS, and climate data, giving operators more levers to drive up fleet utilization. Partnerships such as Geotab’s direct pipeline into Volkswagen Group dashboards exemplify the gravitation toward ecosystem plays that marry hardware, software, and field-updatable firmware in a single lifecycle stack.

The car sharing telematics market size for OEM-integrated deployments is projected to climb sharply as BEV adoption widens, because battery diagnostics demand direct traction-system access that retrofit dongles cannot match reliably. Nonetheless, retrofit vendors still serve mixed-fuel fleets and emerging markets where vehicle ages average above eight years, keeping a two-speed channel landscape intact through the mid-term.

Cost parity between embedded and aftermarket is narrowing as silicon prices climb, while over-the-air provisioning reduces fit-out labor for factory units. Larger operators hedge by blending both strategies: new acquisitions arrive with embedded telematics, but veteran gasoline or hybrid units receive certified third-party devices to unify granular data feeds. This hybrid posture insulates businesses from single-vendor risk and shortens refresh cycles without stranding capital—practices that shape procurement playbooks across the broader car sharing telematics market.

By Form: Integrated Solutions Drive Next-Generation Connectivity

Embedded modules accounted for 45.48% revenue in 2025, but fully integrated connectivity platforms—encompassing 4G/5G modems, edge AI, and secure bootloaders—exhibit a 16.65% CAGR. These units aggregate functions that once required discrete devices, trimming wiring harnesses while expanding compute throughput. Integrated architectures expose open APIs, enabling developers to layer MaaS billing engines, predictive-maintenance dashboards, and carbon-footprint calculators atop the same telemetry backbone.Tethered solutions that depend on smartphone pairing are receding as fleet operators prioritize always-on redundancy for lock/unlock, immobilizer, and remote-disabling commands. The car sharing telematics market size attached to integrated-form deployments is forecast to outstrip tethered revenues by 2027 as 5G coverage proliferates across metropolitan corridors, permitting latency-sensitive applications such as tele-driving and remote-valet services.

Edge-side containerization now allows multiple virtualized applications to coexist securely within one telematics control unit, future-proofing fleets against evolving standards. Standardization drives cross-OEM data fusion, simplifying multi-brand fleet operations and trimming software-integration overhead. As a result, integrated solutions increasingly underpin RFP criteria among both new entrants and incumbent operators, accelerating their momentum within the car sharing telematics market.

By Car-Sharing Model: Free-Floating Dominance Meets P2P Innovation

Free-floating networks captured 60.35% of 2025 revenue by eliminating rigid station networks, boosting car-per-user ratios in densely populated corridors. AI-guided repositioning reduces time-to-vehicle, and transaction streams feed dynamic-pricing engines that fine-tune hourly tariffs against real-time supply. However, peer-to-peer (P2P) networks—leveraging privately owned vehicles—are sprinting ahead at 18.74% CAGR, aligning with asset-light corporate strategies. Telemetry underpins trust, granting hosts and guests access to odometer validation, fuel-level auditing, and driving scorecards. Station-based and round-trip formats now occupy niche roles—corporate motor pools, university campuses, or peri-urban catchments—where parking capacity offsets the fixed-route limitation. Despite slower growth, their predictable booking patterns support long-duration rentals, cushioning revenue volatility. The diversification of business models broadens addressable demand and disperses risk, underpinning sustained expansion of the overall car sharing telematics market.

Regulators increasingly view P2P models as congestion-mitigating rather than competitive to public transit, granting favorable zoning or parking waivers. Yet P2P growth amplifies cybersecurity and privacy obligations because asset ownership and user base are both atomized. Platform operators embed hardened OBD-gateways and biometric authentication to maintain safety while facilitating frictionless handover—a design imperative shaping the next development wave within the car sharing telematics market.

By Vehicle Propulsion: Electric Transformation Reshapes Telematics Requirements

BEVs held 39.28% revenue in 2025 and expand at 22.38% CAGR, propelled by zero-emission zones, plunging battery costs, and predictable shared-fleet duty cycles. Real-time battery-state reporting, charge-session orchestration, and residual-value analytics move from nice-to-have to mission-critical. Operators rely on thermal-management telemetry to avoid asset downtime during fast-charging peaks, while V2G-ready firmware converts parked vehicles into distributed grid storage. Internal-combustion and hybrid powertrains persist where charging deserts remain, but their share will decline steadily as public DC-fast networks proliferate. The car sharing telematics market size linked to BEV fleets therefore outpaces that of hydrocarbons, pushing vendors to integrate charger-availability APIs, energy-tariff look-ups, and route-based range prediction. These software pivots define competitive gaps as electrification pushes deeper into the 2030 horizon.

Emerging silicon-carbide inverters and 800-V battery systems heighten thermal and fault-detection requirements, dictating new sensor arrays and higher-bandwidth CAN gateways. Telemetry vendors transitioning to zonal architectures reduce wire weight while adding redundancy, ensuring resilience for autonomous-ready fleets. Such evolutions anchor long-term cost leadership for platforms that master electric-specific data orchestration within the car sharing telematics market.

Geography Analysis

Europe retains 36.62% revenue leadership owing to mature regulations that mandate advanced safety and connectivity suites on all new vehicles. National incentive schemes bordering Germany, France, and the Nordics subsidize electrified car-sharing fleets, making BEV subscriptions financially compelling for operators. ShareNow’s expansion eastward demonstrates intra-continental knowledge transfer, while Renault’s Utrecht V2G pilot showcases grid-integrated mobility potential. Asia Pacific is scaling fastest at 14.33% CAGR, underwritten by rapid urban migration and sovereign smart-city budgets. Mainland China alone fields robotaxi pilots across more than 50 municipalities, each requiring ultra-low-latency connectivity baked into fleet telematics. The region counts 1.8 billion mobile subscribers, a connectivity bedrock for real-time fleet orchestration and over-the-air updates. Southeast Asian governments are likewise subsidizing telematics-based fleet-management rollouts, cultivating a fertile runway for the car sharing telematics market. North America exhibits mixed momentum: tech-centric metros adopt 5G-enabled tele-driving pilots, whereas suburban sprawl depresses vehicle-turnover metrics. Verizon Business’ Las Vegas partnership with Vay highlights the push toward remote-driven e-vehicles that cut repositioning labor while leveraging mmWave bandwidth. Rural and ex-urban districts, however, remain tethered to LTE or legacy 3G networks, tempering service-expansion economics. Canada and the United States increasingly prioritize cybersecurity alignment with federal standards such as ISO/SAE 21434, adding an additional compliance layer yet reinforcing consumer trust—crucial for sustained car sharing telematics market penetration.

Competitive Landscape

The sector is moderately fragmented: no single vendor controls more than one-fifth of global revenue, yet synergy-driven tie-ups are tightening the field. Platform specialists INVERS, Vulog, and Ridecell compete on configurable software stacks, while Continental, Bosch, and HARMAN battle for the underlying telematics control units. Geotab holds a defensible moat via direct integrations with 157 OEMs, covering nearly 15,000 vehicle variants and granting a data-scale advantage others struggle to match.

Intellectual-property filings underscore strategic priorities—Toyota registered 2,428 telematics and mobility patents in 2024 alone, reinforcing vertical-integration defenses. Start-ups wield API-first architectures to unbundle legacy stacks, but require deep cybersecurity credentials and global SIM provisioning to win enterprise deals. Hardware margins keep tightening due to semiconductor inflation, pivoting revenue toward analytics subscriptions and fleet-efficiency dashboards. These dynamics collectively steer the car sharing telematics market toward a platform-plus-ecosystem structure reminiscent of smartphone operating systems.

OEMs are intensifying in-house software pushes, absorbing telematics layers that aftermarket players once monopolized. Stellantis’ Mobilisights data marketplace feeds raw vehicle signals directly into partner dashboards without external dongles, exemplifying data-monetization moves that squeeze lower-tier suppliers Stellantis. Meanwhile, tier-ones forge EV-specific telemetry modules bundled with over-the-air battery-management firmware, securing annuity revenues long after initial hardware sales. Such maneuvers deepen moats and accelerate consolidation across the car sharing telematics market.

Car Sharing Telematics Industry Leaders

INVERS GmbH

Convadis AG

MoC Sharing

Ridecell, Inc

Vulog

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Gridline INC. acquired Shell’s telematics division to fuse renewable-energy analytics with fleet-management services.

- January 2025: Samsara expanded its collaboration with Stellantis, granting direct cloud access to Mobilisights vehicle data for European fleets.

- November 2024: Renault Group, We Drive Solar, and MyWheels launched Europe’s first V2G-enabled car-sharing service in Utrecht.

- October 2024: Verizon Business partnered with Vay to deploy 5G connectivity for tele-operated shared EVs in Las Vegas.

Global Car Sharing Telematics Market Report Scope

Carsharing Telematics enables the automatic collection of data by understanding the current condition of every car in the fleet. The data assists car-sharing companies in making informed financial decisions.

The study covers original equipment manufacturers (OEM) and aftermarket channel types and tracks the usage of car-sharing telematics across embedded, tethered, and integrated forms. The study also covers demand across various regions and considers the impact of COVID-19 on the car-sharing telematics market.

| Original Equipment Manufacturer (OEM) |

| Aftermarket |

| Embedded |

| Tethered |

| Integrated |

| Round-trip / Station-based |

| Free-floating (One-way) |

| Peer-to-Peer (P2P) |

| Corporate / Fleet |

| Internal-Combustion Engine (ICE) |

| Battery-Electric Vehicle (BEV) |

| Hybrid Electric Vehicle (HEV/PHEV) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN | ||

| Rest of Asia Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| UAE | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Channel | Original Equipment Manufacturer (OEM) | ||

| Aftermarket | |||

| By Form | Embedded | ||

| Tethered | |||

| Integrated | |||

| By Car-Sharing Model | Round-trip / Station-based | ||

| Free-floating (One-way) | |||

| Peer-to-Peer (P2P) | |||

| Corporate / Fleet | |||

| By Vehicle Propulsion | Internal-Combustion Engine (ICE) | ||

| Battery-Electric Vehicle (BEV) | |||

| Hybrid Electric Vehicle (HEV/PHEV) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| ASEAN | |||

| Rest of Asia Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| UAE | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current value of the car sharing telematics market?

The market stands at USD 19.11 billion in 2026 and is projected to grow to USD 35.63 billion by 2031, reflecting a 13.29% CAGR.

Which region leads revenue generation?

Europe accounts for 36.62% of global revenue, driven by stringent safety mandates and mature shared-mobility ecosystems.

Which car-sharing business model is growing fastest?

Peer-to-peer platforms are expected to post a 18.74% CAGR through 2031, despite free-floating models holding the largest current share.

How does electrification influence telematics requirements?

Battery-electric fleets require advanced telemetry for battery health, charge scheduling, and grid interaction, elevating hardware complexity and data-analytics needs.

What regulatory developments are most impactful?

The EU General Safety Regulation II and Next-Generation eCall mandates require advanced connected-safety systems, accelerating telematics penetration globally.

What is the main cost barrier for smaller operators?

Rising semiconductor and 5G-module prices push telematics hardware costs toward USD 1,200 per vehicle, pressuring capital budgets for fleet upgrades.

Page last updated on: