Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

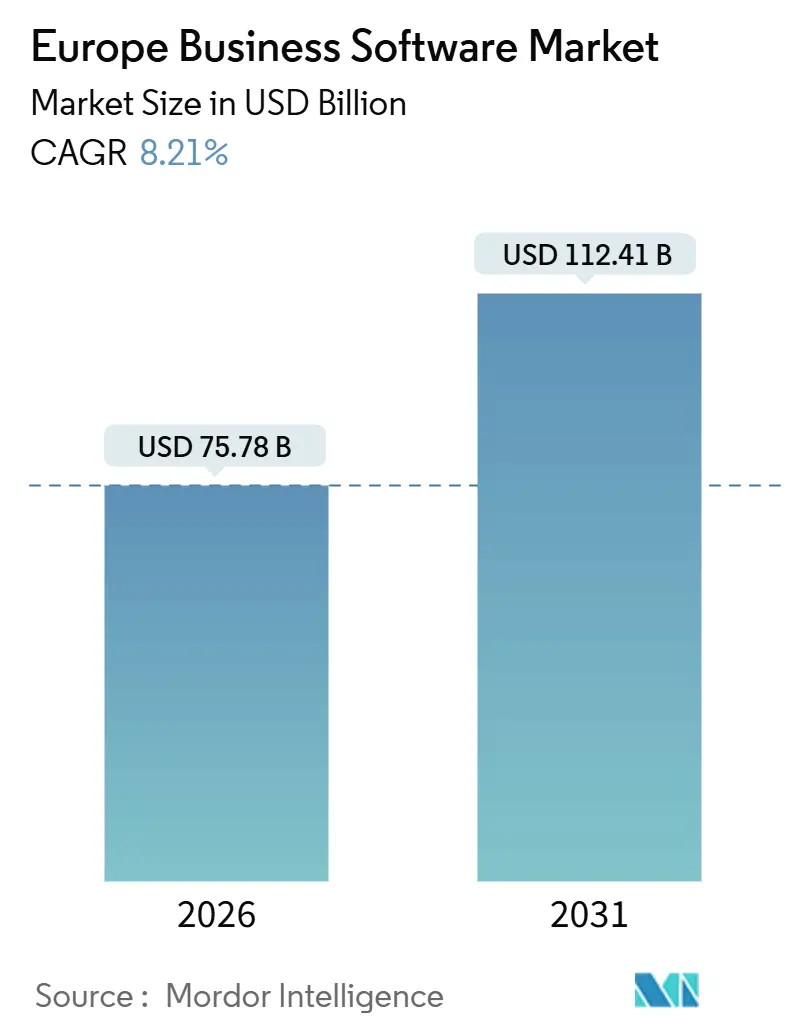

| Market Size (2026) | USD 75.78 Billion |

| Market Size (2031) | USD 112.41 Billion |

| Growth Rate (2026 - 2031) | 8.21% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Business Software Market Analysis by Mordor Intelligence

The Europe Business Software market size stood at USD 75.78 billion in 2026 and is projected to register an 8.21% CAGR, lifting revenue to USD 112.41 billion by 2031. Growth rests on three pillars: rapid migration to cloud-native architectures, regulatory mandates that embed compliance into everyday workflows, and the steady infusion of generative AI into enterprise resource planning, customer relationship management, and supply chain management applications. Cloud deployments already dominate spending, yet sovereignty rules are forcing vendors to host data inside the bloc, reshaping procurement criteria. Interoperability clauses in the EU Data Act are simultaneously lowering switching costs, while the Corporate Sustainability Reporting Directive is turning ESG reporting into a software buying trigger. Competitive intensity is rising as hyperscalers pour capital into new data centers and regional providers pitch sovereign alternatives, giving enterprises more bargaining power.

Key Report Takeaways

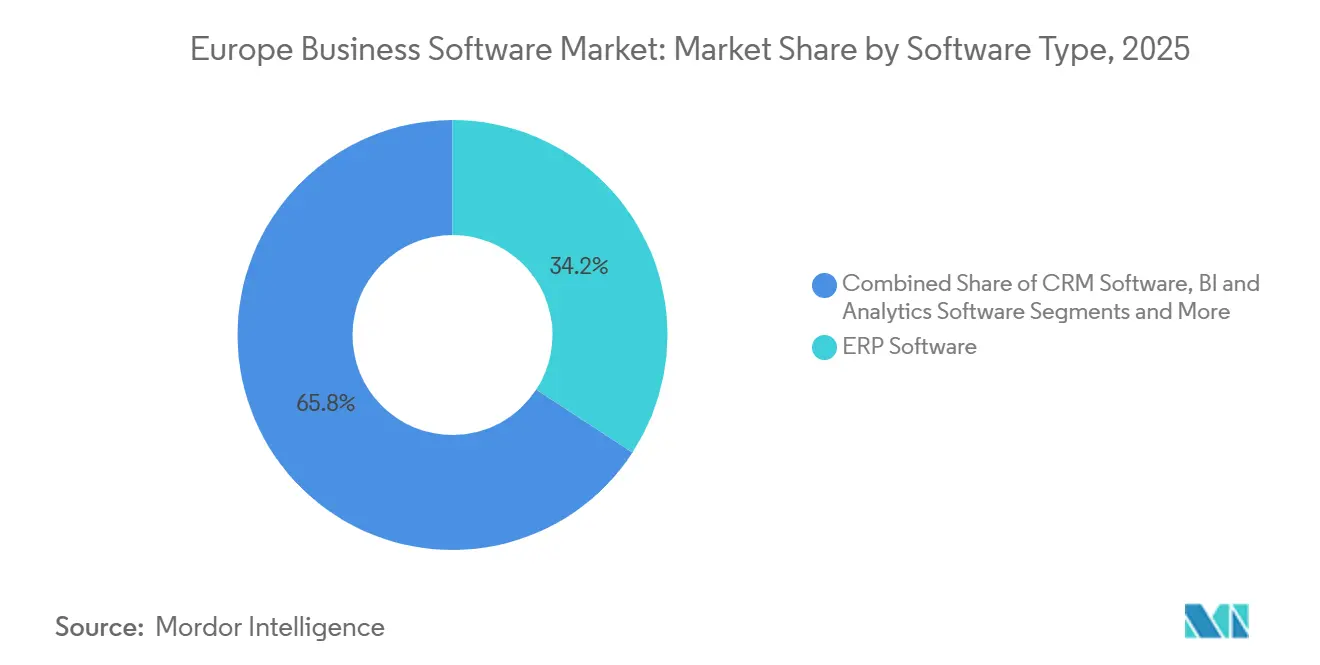

- By software type, enterprise resource planning accounted for 34.19% of 2025 revenue, while business intelligence and analytics platforms are forecast to grow at a 9.43% CAGR through 2031.

- By deployment model, cloud installations captured 72.34% share in 2025 and are expected to advance at a 9.85% CAGR through 2031.

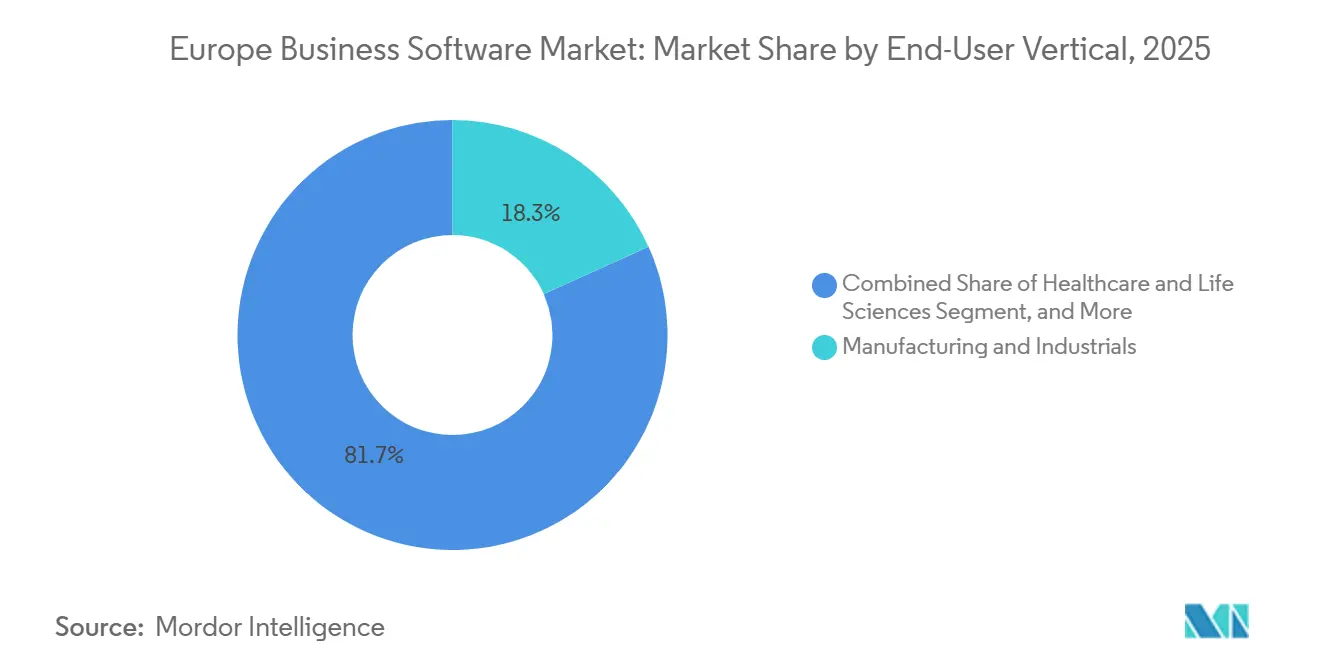

- By end-user vertical, manufacturing held 18.27% of 2025 spending, whereas healthcare and life sciences are set to expand at an 8.92% CAGR over the forecast horizon.

- By enterprise size, large organizations controlled 51.94% of 2025 revenue, yet the mid-sized cohort is projected to post an 8.56% CAGR to 2031.

- By geography, Germany led with a 22.27% share in 2025, while Spain is poised for the fastest 8.84% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Business Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cloud-First Shift Across European Mid-Market Firms | +2.10% | Pan-European, with strongest uptake in Germany, UK, France, and Nordic countries | Medium term (2-4 years) |

| AI-Enabled Decisioning Embedded in ERP and SCM Suites | +1.80% | Global, with early adoption in manufacturing hubs (Germany, Italy) and financial centers (UK, France) | Short term (≤ 2 years) |

| Post-BREXIT Compliance Push for Multi-Entity Finance Suites | +0.60% | UK and EU27 cross-border operations, particularly financial services and retail | Medium term (2-4 years) |

| EU Data Act Spurring SaaS Analytics Modernization | +1.30% | EU27, with compliance mandates affecting all cloud service providers | Short term (≤ 2 years) |

| Green-Taxonomies Driving ESG Reporting Modules Uptake | +1.00% | EU27, with highest demand in Germany, France, Netherlands, and Nordic countries | Medium term (2-4 years) |

| Manufacturing Renaissance Funds (IPCEI) Favouring Vertical ERP | +0.90% | Germany, France, Italy, Spain, and Central European manufacturing corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Cloud-First Shift Across European Mid-Market Firms

Recovery and Resilience Facility grants are lowering capital barriers, allowing mid-sized enterprises to decommission aging servers and adopt subscription licenses. Eurofound and Cedefop found in 2025 that 73% of small and medium-sized enterprises had reached basic digital intensity, yet regional disparities persist, especially in Southern Europe.[1]European Commission, “Data Act,” digital-strategy.ec.europa.eu United Kingdom studies suggest that a 1% productivity uplift from digital tools could add GBP 94 billion (USD 119 billion) to GDP, encouraging policymakers to underwrite CTO-as-a-service programs. PwC reported that 94% of organizations plan to redesign cloud architecture to reflect geopolitical realities.[2]PwC, “EMEA Cloud Survey 2025,” pwc.com Hyperscaler revenue is therefore climbing, yet German and French enterprises increasingly trial sovereign platforms from OVHcloud and Scaleway to keep sensitive data inside the bloc. Because only one-third of European firms have migrated more than half of their workloads, a substantial runway remains for workload re-platforming.[3]McKinsey, “Cloud’s Trillion-Dollar Prize is Up for Grabs,” mckinsey.com

AI-Enabled Decisioning Embedded in ERP and SCM Suites

Generative AI is moving from pilot to production across core business suites, trimming cycle times and reducing manual effort. SAP infused Business AI into S/4HANA, while Microsoft launched Copilot inside Dynamics 365 Supply Chain Management, claiming up to 30% forecast-error reductions.[4]Microsoft, “Dynamics 365 Supply Chain Management,” microsoft.com BCG estimates that generative models can cut ERP implementation labour by 20-40%. Oracle, Salesforce, and regional vendors are racing to match these capabilities, shifting buyer expectations so that predictive analytics becomes a baseline requirement. European manufacturers are early adopters, using AI-driven visibility tools to offset semiconductor shortages; Apollo Tyres’ European division saved GBP 9.2 million (USD 11.7 million) through route optimization. Vendors unable to release credible AI roadmaps risk commoditization as procurement teams bake intelligent automation into request-for-proposal templates.

EU Data Act Spurring SaaS Analytics Modernization

The EU Data Act obliges software providers to offer data portability and open APIs, dismantling long-standing lock-in practices. Analytics vendors are rebuilding around open standards so clients can federate queries across AWS, Azure, on-premises clusters, and sovereign clouds. Microsoft already merged Power BI with its Fabric platform and OneLake data lake, giving customers single-copy analytics in regionally compliant instances. Tableau and QlikTech are following suit, reflecting growing pressure to support data mesh topologies. The act’s liability provisions heighten financial exposure for non-compliance, encouraging risk-averse sectors such as healthcare, banking, and utilities to prioritize vendors with proven governance controls. Over time, enforced openness is expected to erode incumbent switching barriers and foster best-of-breed adoption patterns that boost demand for integration middleware.

Green-Taxonomies Driving ESG Reporting Module Uptake

The Corporate Sustainability Reporting Directive forces roughly 50,000 European companies to disclose double materiality metrics under European Sustainability Reporting Standards. PwC’s 2024 readiness survey showed 58% of firms were unprepared, signalling a sizable compliance gap. SAP, Workiva, and several niche players have released pre-built ESG modules that collect, validate, and audit carbon, water, and social data. Because ISO 14001 and ISO 26000 references are now standard in tenders, embedded sustainability functionality is shifting from nice-to-have to license-must. The EU Taxonomy Regulation compounds complexity by requiring real-time tracking of revenue, capital expenditure, and operating expenditure linked to taxonomy-eligible activities. Vendors offering automated classification and disclosure workflows can therefore command price premiums and accelerate renewals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Unresolved EU-Wide Skills Shortage in Low-Code Platforms | -1.20% | Pan-European, with acute shortages in Germany, UK, France, and Nordic countries | Long term (≥ 4 years) |

| Mounting Sovereignty Concerns over US-Hosted SaaS | -0.90% | EU27, with strongest sentiment in Germany, France, and Netherlands | Medium term (2-4 years) |

| Fragmented VAT Regimes Complicating Multi-Country Rollouts | -0.50% | EU27 cross-border operations, particularly retail, e-commerce, and logistics | Medium term (2-4 years) |

| Rising Total-Cost-of-Ownership for Hyperscaler Consumption | -0.70% | Global, with highest impact in cloud-intensive verticals (financial services, healthcare, SaaS providers) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Unresolved EU-Wide Skills Shortage in Low-Code Platforms

The European Commission reported that 77% of enterprises struggled to hire ICT specialists in 2024, hindering low-code uptake despite the promise of citizen development. Only 54% of the population has basic digital skills, while advanced competencies such as API design and cybersecurity remain scarcer. OECD analysis of Czech SMEs showed just 16% invest in ICT training, a pattern mirrored across several Central and Eastern European markets. This talent gap bifurcates the market: large enterprises deploy low-code to accelerate backlog reduction, whereas mid-market firms remain stuck at proof-of-concept. Vendors are responding with academy programs, but progress is slow, placing a drag on license growth forecasts.

Mounting Sovereignty Concerns over US-Hosted SaaS

Schrems II and the extraterritorial reach of the US CLOUD Act amplified fears that foreign authorities could access European citizen data without due process. A 2025 KPMG survey found 58% of German companies regard sovereign cloud as non-negotiable and 98% are willing to pay a premium for it. SAP, Microsoft, and Oracle have responded with sovereign regions operated by European partners, but limited feature parity and higher pricing complicate value propositions. Meanwhile, the Important Projects of Common European Interest initiative directed EUR 1.2 billion (USD 1.3 billion) toward a federated cloud, yet production readiness is years away. Until native EU alternatives reach scale, enterprises must juggle compliance, capability, and cost, lengthening sales cycles and tempering market expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Software Type: ERP Anchors Spending, Analytics Accelerates Fastest

Enterprise resource planning applications accounted for 34.19% of 2025 revenue, confirming their role as the transactional backbone for finance, procurement, and human capital across Europe Business Software market deployments. Business intelligence and analytics suites are poised to record the fastest 9.43% CAGR, helped by EU Data Act mandates that require open data models and the proliferation of agent-based dashboarding. Vendors are embedding natural language interfaces and predictive logic that surface insights without manual SQL, which shortens decision loops for line-of-business managers.

In the decision stack, customer relationship management remains crucial, especially in financial services, while supply chain management gains urgency as manufacturers localize sourcing to manage geopolitical risk. The Europe Business Software market size for emerging niches such as environmental, social, and governance reporting has grown rapidly following the Corporate Sustainability Reporting Directive, giving pure-play providers an entry wedge. Competitive positioning is shifting toward composable architectures, allowing customers to assemble best-of-breed combinations from SAP, Microsoft, Salesforce, and a growing roster of mid-market specialists.

By Deployment Model: Cloud Dominance Entrenches Despite Sovereignty Frictions

Cloud installations comprised 72.34% of total revenue in 2025, and the segment is likely to outpace overall Europe Business Software market growth at a 9.85% CAGR through 2031. Hyperscalers are expanding data-center footprints from Dublin to Warsaw, ensuring sub-20-millisecond latency for most users. Yet sovereignty clauses in public tenders oblige providers to guarantee in-region processing and European legal jurisdiction, spawning a new tier of protected instances that balance compliance and innovation.

On-premises remains relevant for critical infrastructure, defense, and certain bank workloads, but even these users are adopting containerized platforms that can shift between private and public environments. Multi-cloud configurations dominate architecture roadmaps, giving enterprises flexibility to arbitrage pricing and resilience. As reserved-instance contracts proliferate, finance teams are sharpening FinOps practices to limit unbudgeted consumption, moderating the Europe Business Software market share gains of hyperscalers but solidifying cloud as the default deployment choice.

By End-User Vertical: Manufacturing Leads, Healthcare Surges on Interoperability Mandates

Manufacturing contributed 18.27% of 2025 spending, reflecting Germany’s automotive clusters, Italy’s machinery exports, and pan-European Industry 4.0 subsidies. Digital twins, predictive maintenance, and automated quality inspection modules are mainstreaming inside plants, creating durable demand for real-time ERP and supply chain visibility. Conversely, healthcare and life sciences are on track for the highest 8.92% CAGR, driven by European Health Data Space rules that enforce cross-border electronic health record sharing. Hospitals are moving to cloud-based EHRs and analytics to enable integrated care pathways and clinical research.

Financial services, retail, and logistics each represent sizeable slices of the Europe Business Software market, underpinned by risk management reform and omnichannel commerce imperatives. Public sector agencies are leaning on Recovery and Resilience Facility grants to upgrade legacy payroll, permitting, and tax systems. Telecom and media operators continue to deploy customer data platforms as 5G monetization strategies pivot toward subscription bundles. Each vertical’s digital road map reinforces the importance of modular compliance engines that can adapt to divergent regulations without full-scale rewrites.

By Enterprise Size: Large Firms Dominate Spending, Mid-Market Drives Growth

Large enterprises generated 51.94% of 2025 revenue, confirming their outsize influence on vendor product road maps. These organizations run multi-entity structures that require consolidated financials, automated intercompany eliminations, and global supply chain orchestration. Consequently, they purchase integrated suites and premium support, lifting average contract values across the Europe Business Software market.

Mid-sized companies will contribute the fastest 8.56% CAGR as government subsidies, freemium models, and simplified onboarding shrink adoption barriers. Vendors such as Sage, Zoho, and Odoo are tailoring pre-configured workflows that lower implementation time to weeks rather than months. Still, skills shortages persist, and many firms depend on partner networks for customization. Small businesses lag due to budget constraints and limited in-house IT capacity, yet policy targets that call for 90% digital intensity by 2030 suggest accelerated uptake later in the decade.

Geography Analysis

Germany retained a 22.27% share of the Europe Business Software market in 2025, underpinned by a strong manufacturing sector and proactive adoption of Industry 4.0 practices. KPMG surveys indicate that 62% of German enterprises now follow a cloud-first doctrine, while 58% require sovereign hosting, forcing both global and local vendors to invest in domestic data centers. The national contribution of EUR 750 million (USD 825 million) to the federated European cloud underscores Berlin’s strategic intent to future-proof industrial competitiveness.

Spain is expected to be the fastest-growing geography, registering an 8.84% CAGR through 2031. Recovery and Resilience Facility grants and the Kit Digital voucher program underpin the rapid digitization of small and medium-sized enterprises. This policy stance, together with rising venture capital inflows into Barcelona and Madrid, creates fertile ground for SaaS adoption. The post-Brexit United Kingdom remains an attractive market due to its banking and insurance concentration, although dual reporting frameworks add compliance overhead that favours modular ERP.

France leverages the Gaia-X initiative and public investment banks to foster a sovereign data ecosystem, boosting native providers such as OVHcloud. Italy channels Transizione 4.0 incentives and PNRR funds into public sector modernization, while Nordic nations lead on digital skills, accelerating adoption cycles. Central and Eastern European markets present mixed readiness; Poland and the Czech Republic continue to draw foreign direct investment into manufacturing, whereas Bulgaria and Romania lag on cloud skill metrics but show potential upside as connectivity improves.

Collectively, geographic demand patterns highlight the importance of localization, language support, and in-region compliance modules, reinforcing the Europe Business Software market’s preference for modular platforms that can be parameterized rather than heavily customized.

Competitive Landscape

The Europe Business Software market is moderately concentrated. SAP, Microsoft, and Oracle anchor the top tier with comprehensive ERP, database, and productivity suites, yet their hold is tempered by sovereignty stipulations and pricing scrutiny. Salesforce remains the CRM reference point, but HubSpot and Zoho are eroding share in the mid-market with lower cost of ownership. Workday is capitalizing on demand for unified human capital and financial management among large enterprises, particularly those with complex payroll and multi-GAAP reporting needs.

Regional specialists thrive in domain-specific niches. Sage and Unit4 focus on professional services, IFS dominates field service management, and Dassault Systèmes supplies manufacturing product lifecycle management. Low-code contenders such as Out Systems, Mendix, and Microsoft Power Platform are vying for developer mindshare, while ESG reporting startups position themselves as plug-ins for compliance gaps. The EU Data Act’s push for interoperability is fostering a composable mindset, encouraging best-of-breed purchasing and opening doors for challenger brands.

Strategic moves intensified in 2025. Microsoft launched Copilot across European Dynamics 365 instances, SAP promoted Business AI within its S/4HANA Cloud, and Oracle expanded German data centers to bolster sovereign propositions. Meanwhile, IFS’s acquisition of a predictive maintenance specialist and Sage’s integration with Microsoft Power Platform illustrate how vendors blend inorganic and partnership tactics to extend functionality. The race is now centered on embedding generative intelligence, ensuring data residency, and delivering out-of-the-box compliance kits.

Europe Business Software Industry Leaders

Accenture Plc

Cisco Systems Inc.

Microsoft Corporation

SAP SE

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Workday reported Q1 FY2026 revenue of USD 2.24 billion and expanded UK operations to pursue EMEA uptake.

- March 2025: Aletiq raised USD 6.5 million to scale its SaaS PLM platform for European manufacturers.

- February 2025: Microsoft finalized its EU sovereign cloud, reinforcing its alignment with regional data-sovereignty mandates.

- January 2025: The virt8ra project launched Europe’s first sovereign edge cloud with EUR 3 billion in IPCEI funding.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the Europe business software market as all paid ERP, CRM, BI/analytics, supply-chain, and adjacent process-automation suites sold to private and public organizations, measured at vendor invoice value in USD. Solutions focused purely on basic office productivity, infrastructure security, or custom coding platforms fall outside this boundary.

Scope Exclusion: tooling aimed only at personal productivity (e.g. email clients, word processors) and system-level middleware is not counted.

Segmentation Overview

- By Software Type

- ERP Software

- CRM Software

- BI and Analytics Software

- Supply-Chain Management Software

- Other Software Type

- By Deployment Model

- Cloud

- On-premise

- By End-User Vertical

- BFSI

- Healthcare and Life Sciences

- Public Sector and Institutions

- Retail and E-commerce

- Transportation and Logistics

- Manufacturing and Industrials

- Telecom and Media

- By Enterprise Size

- Large Enterprises

- Mid-sized

- Small Businesses

- By Country

- United Kingdom

- Germany

- France

- Italy

- Spain

- Rest of Europe

Detailed Research Methodology and Data Validation

Primary Research

Discussions with regional CIOs, system integrators, procurement heads, and national regulators across Germany, the UK, France, Italy, Poland, and the Nordics helped us verify license price corridors, cloud migration cadence, and compliance cost impacts, thereby plugging data gaps flagged during secondary review.

Desk Research

Our analysts collate granular spending and adoption statistics from tier-1 public datasets such as Eurostat's "ICT Usage in Enterprises," the European Commission's DESI index, ECB currency databases, OECD Digital Economy Outlook tables, and patent insight from Espacenet. Company filings, 10-Ks, and investor decks complement these sources, while news sweeps through Dow Jones Factiva and revenue splits in D&B Hoovers help validate vendor-level signals. Industry position papers from bodies such as DIGITALEUROPE or BSA provide additional regulatory context. The sources cited above illustrate our desk work; many more repositories were consulted for cross-checks and clarification.

Market-Sizing & Forecasting

We begin with a top-down reconstruction of enterprise application outlays reported by Eurostat and national statistic offices, convert them to USD, and then adjust for non-covered categories before distributing spend across software types, deployment models, and countries. Supplier roll-ups (sampled ASP × active seats gleaned from public contracts and channel checks) provide a bottom-up reasonableness test. Key variables shaping the model include (i) ERP and CRM penetration rates by firm size, (ii) public-cloud workload share, (iii) average subscription discount curves, (iv) GDP-linked IT spending elasticity, and (v) regulatory spend triggers tied to the EU Data Act. Forecasts through 2030 employ multivariate regression blended with scenario analysis to capture macro swings and policy shocks; elasticities were vetted with interviewees before being locked. Any blind spots in bottom-up counts are bridged by weighting vendor cohorts to known regional revenue disclosures.

Data Validation & Update Cycle

Outputs pass a three-layer review: automated anomaly flags, peer analyst scrutiny, and senior sign-off. Divergences above preset thresholds trigger re-contact of key respondents. The dataset is refreshed annually, with interim updates issued when material events, such as major policy enactments or mega vendor mergers, shift underlying drivers.

Why Mordor's Europe Business Software Baseline Holds Up

Published numbers often differ because firms vary scope breadth, pricing assumptions, and refresh cadence.

Key gap drivers center on whether infrastructure tools are bundled, if estimates rely on global ratios prorated to Europe, and how swiftly cloud discounts or euro-dollar movements are incorporated. Mordor's base sticks to business-application suites only, reports constant-currency 2025 dollars, and pulls live adoption ratios twice a year; differences that materially reset totals elsewhere.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 69.56 B (2025) | Mordor Intelligence | - |

| USD 70.60 B (2025) | Regional Consultancy A | Excludes supply-chain modules and public-sector demand |

| USD 72.39 B (2024) | Global Consultancy B | Bundles infrastructure software and uses 2023 exchange rates |

Taken together, the comparison shows that while headline values cluster, scope tweaks and currency timing create visible gaps. Mordor's disciplined variable selection and dual validation steps offer decision-makers a balanced, transparent baseline they can trace back to public metrics and on-ground sentiment.

Key Questions Answered in the Report

How big is the Europe Business Software market in 2026?

It reached USD 75.78 billion in 2026 and is forecast to climb to USD 112.41 billion by 2031 at an 8.21% CAGR.

Which software category is expanding fastest?

Business intelligence and analytics platforms are projected to grow at a 9.43% CAGR through 2031, the highest among all categories.

Why is healthcare seeing accelerated software investment?

The European Health Data Space regulation enforces interoperability across electronic health records, driving hospitals and life-science companies to modern, cloud-based platforms.

How are sovereignty concerns affecting vendor choice?

Many enterprises require data to remain inside the bloc, leading global vendors to launch sovereign regions and boosting demand for Europe-domiciled providers.

What are the main barriers to adoption for mid-sized firms?

Skills shortages, limited IT budgets, and fragmented vendor landscapes slow implementation despite policy grants and freemium pricing.

Which geography will post the fastest growth through 2031?

Spain is set to record an 8.84% CAGR, propelled by Recovery and Resilience Facility grants and small business voucher programs.

Page last updated on: