Europe Semiconductor Diode Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

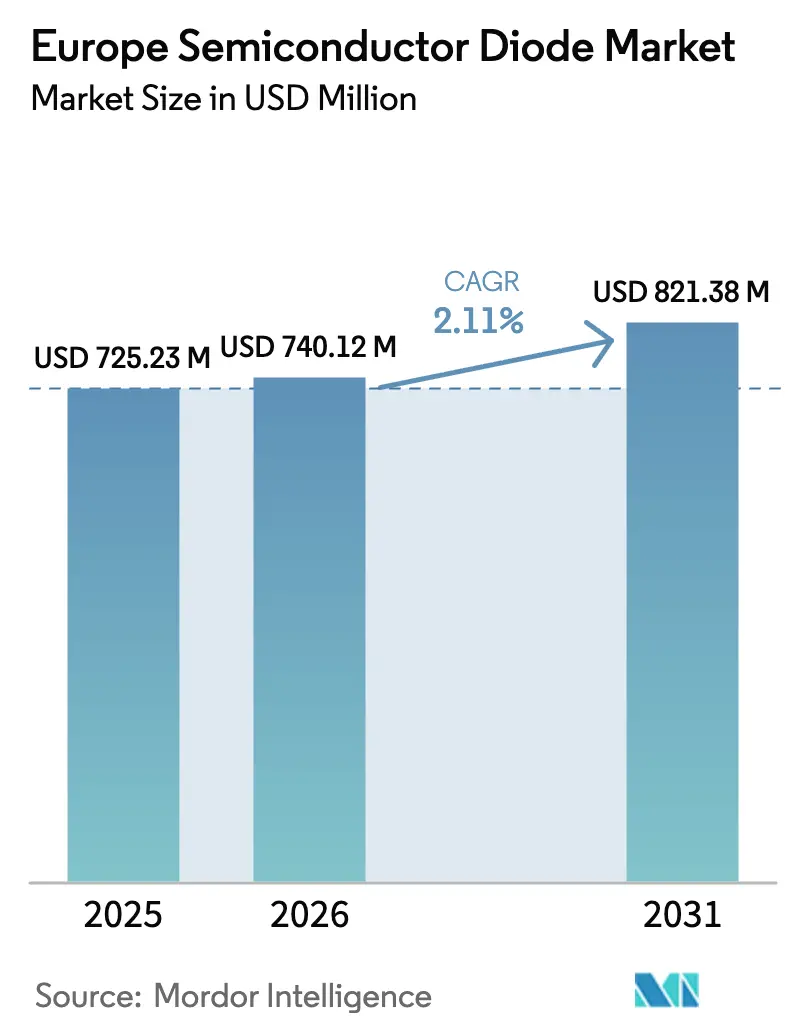

| Base Year Market Size (2025) | USD 725.23 Million |

| Market Size (2026) | USD 740.12 Million |

| Market Size (2031) | USD 821.38 Million |

| Growth Rate (2026 - 2031) | 2.11% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Semiconductor Diode Market Analysis by Mordor Intelligence

The Europe Semiconductor Diode Market size was valued at USD 725.23 million in 2025 and is estimated to grow from USD 740.12 million in 2026 to reach USD 821.38 million by 2031, at a CAGR of 2.11% during the forecast period (2026-2031). A gradual pivot toward wide-bandgap materials is unfolding as silicon carbide (SiC) and gallium nitride (GaN) capture automotive and industrial sockets, while legacy silicon remains entrenched in cost-sensitive consumer and telecom gear. Germany’s public-private megaprojects, including the EUR 10 billion (USD 11.61 billion) ESMC fab and Infineon’s Smart Power Fab, are anchoring regional capacity corridors and stimulating design-in activity for 200 mm SiC wafers. Italy’s Catania cluster, backed by EUR 5 billion (USD 5.80 billion) for STMicroelectronics’ SiC device line and EUR 730 million (USD 847.26 million) for captive substrate output, demonstrates how Chips Act incentives funnel capital toward vertical integration. Schottky rectifiers keep their central role in server power supplies and EV on-board chargers, yet transient-voltage-suppression (TVS) arrays for USB4, Thunderbolt and automotive Ethernet outpace all other device classes. Elevated electricity tariffs 197 EUR/MWh in early 2024 squeeze fab margins, but policy continuity after the September 2025 Semicon Coalition declaration signals further tailwinds for advanced-node and wide-bandgap investment.

Key Report Takeaways

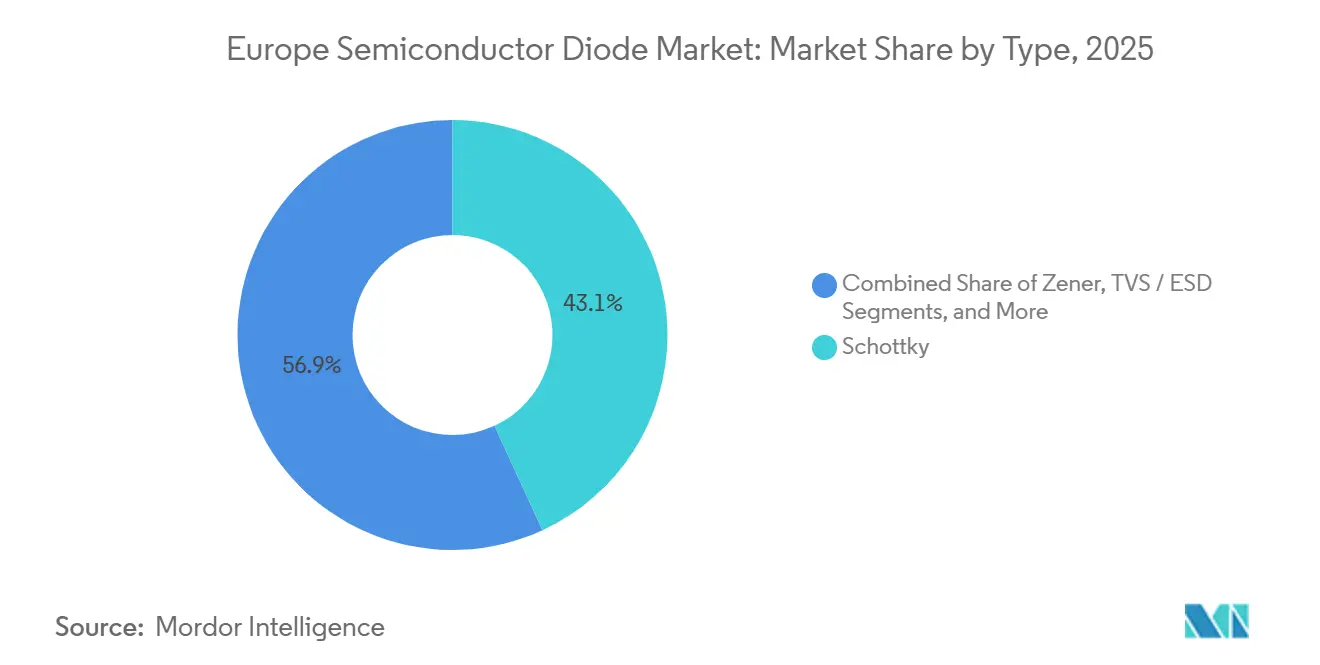

- By type, Schottky diodes led with 43.12% Europe semiconductor diode market share in 2025; TVS and electrostatic-discharge devices are advancing at a 2.36% CAGR through 2031.

- By base material, silicon held 71.43% share of the Europe semiconductor diode market size in 2025, while SiC is rising fastest at 2.44% CAGR.

- By package, surface-mount devices accounted for 64.63% of the Europe semiconductor diode market size in 2025 and are growing at 2.83% CAGR.

- By end-use, automotive and transportation captured 36.51% Europe semiconductor diode market share in 2025 and is expanding at 2.67% CAGR to 2031.

- By geography, Germany dominated with 28.23% revenue share in 2025, whereas Italy is projected to lead growth at 2.71% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Semiconductor Diode Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-Mobility Led SiC-Schottky Pull-Through | +0.6% | Germany, Italy, France, spillover to Spain, UK | Medium term (2-4 years) |

| Expansion of EU Chips Act Funding Pipeline | +0.4% | Germany, Italy, Austria, France, Spain | Long term (≥4 years) |

| Telecom 5G / FTTx Rectifier Renewal | +0.3% | Pan-European | Short term (≤2 years) |

| EV On-Board Charger Design-Wins for GaN TVS | +0.2% | Germany, France, Italy | Medium term (2-4 years) |

| Power-Dense Data-Center PSUs Less Than 3 kW | +0.2% | Frankfurt, London, Amsterdam, Paris, Dublin | Short term (≤2 years) |

| Edge-AI Industrial Drives Less Than 650 V | +0.1% | Germany, Italy | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

E-Mobility Led SiC-Schottky Pull-Through

Battery-electric vehicles moving to 800 V platforms are the prime catalyst for SiC Schottky demand in Europe, as OEMs seek faster charging and lighter copper harnesses. STMicroelectronics logged design wins with Geely and Hyundai for fourth-generation SiC MOSFETs co-packaged with Schottky diodes for SOP-2026 lines.[1]European Commission, “European Chips Act | Shaping Europe’s Digital Future,” EUROPA.EU Infineon’s HybridPACK Drive G3, rolled out in late 2024, integrates CoolSiC MOSFETs and free-wheeling diodes for German premium brands. Transitioning to 200 mm SiC wafers at Catania and Wolfspeed Saarland is expected to trim die cost per ampere by 20-25% by 2027. Yet EU anti-subsidy duties of 17-35.3% on Chinese BEV imports have softened near-term unit pull-through, and AEC-Q101 Grade 0 validation pushes product-launch lead-times out by 12-18 months.

Expansion of EU Chips Act Funding Pipeline

Seven first-of-a-kind fabs approved under the Chips Act have secured EUR 31.5 billion (USD 36.56 billion) in combined spending, with three dedicated to wide-bandgap devices. STMicroelectronics alone commands EUR 5 billion (USD 5.80 billion) for device capacity and EUR 730 million (USD 847.21 million) for substrates in Sicily, while onsemi allocates EUR 1.64 billion (USD 1.90 billion) to Rožnov SiC expansion. Spain’s Imec-backed Málaga center and the EUR 700 million NanoIC pilot line, funded in February 2026, give SMEs 300 mm access and de-risk advanced-node prototyping. The Semicon Coalition’s call for a “Chips Act 2.0” could unlock another EUR 20-30 billion (USD 23.21 -34.82 billion) in private capital by 2028.

Telecom 5G / FTTx Rectifier Renewal

By 2025, European operators covered 81% of the population with 5G and 56% of households with FTTP, starting a retrofit wave for rectifier modules in macro-cells and OLTs. New 3.5 GHz and 26 GHz radios mandate sub-10 ns reverse-recovery Schottkys to hit 95% efficiency, while FTTH infrastructure standardizes on 48 V DC plants that favor low-drop rectification. Nexperia’s automotive-grade GaN FETs released in 2025 offer high-mobility channels that shrink inductors and halve board area in 3 kW rectifiers.[2]Nexperia, “Automotive Qualified Products (AEC-Q100/Q101),” NEXPERIA.COM The upgrade cycle peaks by 2027, after which growth aligns with incremental site deployment.

EV On-Board Charger Design-Wins for GaN TVS

GaN TVS arrays, prized for picofarad-level capacitance, safeguard CAN-FD and Ethernet buses in 11 kW and 22 kW on-board chargers. Infineon shipped CoolGaN 650 V HEMTs with integrated GaN clamping diodes in 2024. German, French and Italian Tier-1s such as Bosch, Valeo and Marelli have design-ins pending AEC-Q101 approval and ZVEI robustness validation. The 48 V mild-hybrid push further expands TAM for low-capacitance TVS arrays.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| SiC Substrate Cost Delta vs. Si Greater Than 6× | -0.3% | Pan-European | Medium term (2-4 years) |

| Automotive OEM PPAP Backlog Less Than 18 Months | -0.2% | Germany, France, Italy | Short term (≤2 years) |

| EU Energy-Price Volatility on Fab OPEX | -0.2% | Germany, France, Spain | Short term (≤2 years) |

| Trade-Remedy Tariffs on Chinese BEV Imports | -0.1% | Pan-European | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

SiC Substrate Cost Delta vs. Si Greater Than 6×

Substrates account for half of finished SiC diode cost and still price out at six times equivalent silicon wafers, hindering broader penetration. Moving from 150 mm to 200 mm cuts cost per square centimeter by roughly 20% by 2027, yet the absolute premium stays quadruple that of silicon through 2031. Vertical integration at STMicro and Infineon remains the chief hedge against volatile spot markets.

Automotive OEM PPAP Backlog Less Than18 Months

AEC-Q101 zero-defect targets and ZVEI robustness validation prolong PPAP cycles for wide-bandgap diodes to 18 months. Incumbents maintain in-house labs to parallel-process lots, but newer vendors such as GeneSiC face liquidity strain while waiting for qualification sign-off.[3]ZVEI, “Handbook for Robustness Validation of Semiconductor Devices in Automotive Applications,” ZVEI.ORG The multi-source penalty also deters OEMs from broadening supplier rosters, reinforcing the incumbents’ moat.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Schottky Dominance Anchored by Rectification Efficiency

Schottky devices represented 43.12% of the Europe semiconductor diode market size in 2025, a share rooted in their sub-0.5 V forward drop that improves synchronous rectifier efficiency in EV chargers and server PSUs. Zener and small-signal diodes serve as references and for switching, while TVS and ESD arrays post the steepest 2.36% CAGR thanks to USB4 and automotive Ethernet rollouts.

More OEMs now specify GaN TVS for 48 V mild-hybrid buses, citing order-of-magnitude lower capacitance than silicon counterparts. Schottky demand also benefits from 5G base-station retrofits that require less than 10 ns of reverse recovery time. Niche laser diodes for LiDAR contribute under 5% of revenue but see solid traction in 905 nm edge-emitting designs, even as VCSEL alternatives loom.

By Base Material: Silicon Carbide Gains Despite Premium

Silicon retained 71.43% Europe semiconductor diode market share in 2025, underpinned by its mature supply chain, abundant wafer capacity and decades-long reliability data favored by consumer, telecom and low-voltage industrial buyers. Silicon carbide, though still a minority material, is pacing a 2.44% CAGR to 2031 as 800 V traction inverters, 650 V servo drives and 350 kW grid-scale battery chargers demand 30-40% lower switching losses than silicon can deliver. STMicroelectronics’ Catania hub targets 15,000 200 mm wafers per week by 2033, while onsemi’s Rožnov line will push 40,000 150 mm wafers annually by 2027, moves that could lift SiC’s slice of the Europe semiconductor diode market size toward 9-10% over the forecast horizon. Gallium nitride, holding barely 3% volume in 2025, is carving footholds in 11 kW on-board chargers and 48 V mild-hybrid DC-DC converters, where 500 kHz switching shrinks inductors and raises power density in cramped engine bays. Emerging ultra-wide-bandgap options such as gallium oxide remain pre-commercial, but EU-funded pilot lines like NanoIC are sampling demonstrator diodes that withstand over 3 kV reverse bias at junction temperatures above 200 °C.

Vertical-integration plays are rewriting cost curves: STMicroelectronics’ EUR 730 million captive-substrate project seeks to internalize 40% of its SiC wafer demand by 2026, cutting exposure to spot-market swings and shaving die cost per ampere by nearly one-quarter. Infineon pursues a similar hedge at Dresden, shifting to 200 mm SiC production today and piloting 300 mm lots for post-2027 ramps. Device makers without in-house boule capacity, including GeneSiC and Littelfuse subsidiaries, increasingly lock multi-year substrate supply contracts or pivot toward GaN where wafer economics are comparatively benign. Silicon will still dominate low-voltage sockets USB power bricks, set-top boxes, home appliances—yet its region-wide share is likely to dip to the high-sixties by 2031 as automotive, renewable-energy and heavy-industry clients standardize on wide-bandgap rectifiers for efficiency mandates and lifetime cost reductions.

By End-Use: Automotive Electrification Accelerates Demand

Automotive and transportation captured 36.51% of the Europe semiconductor diode market size in 2025 and is expanding at a 2.67% CAGR through 2031, confirming that electrification is the single strongest pull-through force for diodes. Demand stems from 800 V traction inverters, 11 kW and 22 kW on-board chargers, 48 V mild-hybrid DC-DC converters, and expanding ADAS feature sets that embed LiDAR, radar, and camera modules, each protected by low-capacitance TVS arrays. Communications infrastructure remains the second-largest buyer, with 5G macro-cell and FTTP rollouts replacing legacy rectifier bricks with sub-10 ns Schottkys that keep base-station efficiency above 95%. Industrial automation follows closely: edge-AI servomotor drives, welding rigs, and uninterruptible power supplies use 650 V SiC rectifiers to meet EU eco-design rules while reducing heat sinks. Data-center operators in Frankfurt, Amsterdam, Paris, London, and Dublin push server power supplies toward 96% efficiency, further reinforcing demand for high-current Schottky diodes.

Consumer electronics, once the highest-volume outlet, now trails overall market growth because smartphone and notebook refresh cycles are lengthening and Chinese ODMs are diversifying assembly to Southeast Asia. Medical imaging, renewable-energy inverters and rail traction combine for a steady 10-12% revenue slice, buffered by multiyear procurement budgets that minimize cyclical swings. Within automotive, the shift from distributed to zonal E/E architectures multiplies high-speed CAN-FD and Ethernet ports per vehicle, elevating the bill of materials for TVS and ESD networks. European Tier-1s such as Bosch, Valeo and Marelli report that every 5 million BEV powertrains they ship adds roughly USD 7 million in incremental diode content, most of it wide-bandgap. As a result, automotive’s share of the Europe semiconductor diode market is projected to edge past 38% by 2031 even if regional BEV production underperforms consensus forecasts.

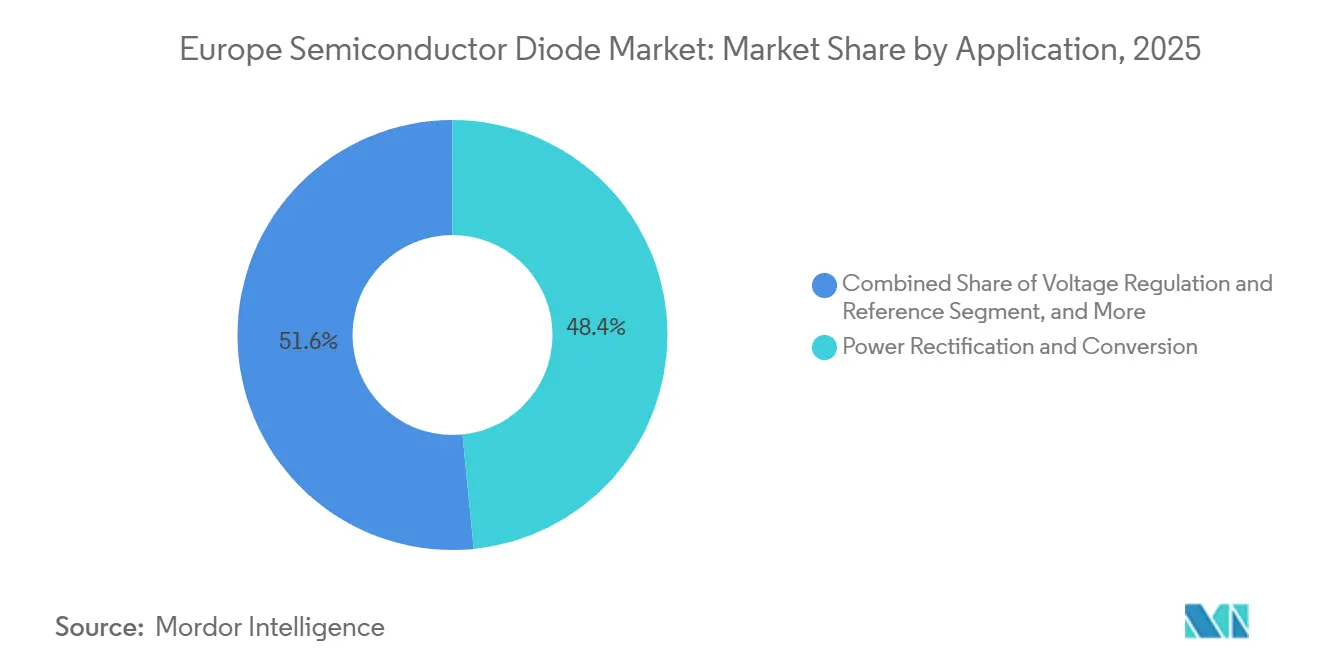

By Application: Power Rectification Leads, Protection Devices Surge

Power rectification and conversion captured 48.42% of the Europe semiconductor diode market size in 2025 and is projected to expand near the overall 2.11% CAGR through 2031, thanks to synchronous buck and totem-pole PFC stages in data-center PSUs, telecom rectifiers and EV fast-charging dispensers that depend on low-drop Schottkys and SiC diodes for 95-98% system efficiency. Voltage-reference and regulation circuits, anchored by Zener architectures, serve precision analog chains in instrumentation amps, tire-pressure monitoring sensors and medical ultrasound probes, keeping a steady single-digit revenue share. Electrostatic-discharge, surge and circuit-protection uses are the fastest riser at 2.61% CAGR, fueled by USB4, Thunderbolt 4 and 1000BASE-T1 Ethernet that need sub-0.3 pF junction capacitance to guard 40 Gbps links without degrading eye diagrams. Renewable-energy inverters and grid-connected battery banks further enlarge the rectification TAM, as 1,500 V utility-scale strings adopt SiC antiparallel diodes to slash gate-charge losses in three-level topologies.

Medical imaging, rail traction and aerospace radar fold into an “other applications” cluster that stays below 5% revenue yet commands premium ASPs due to radiation-hardness and high-temperature requirements. Within consumer electronics, faster-charging GaN USB-C adapters lean on ultra-fast recovery diodes to meet IEC 62368 thermal derating, partially offsetting the slowdown in smartphone refresh cycles. Automotive TVS content rises with the shift to zonal E/E architectures: each additional 10-gigabit GMSL camera link demands four-channel, 20 V clamp arrays that add up to USD 0.45 diode content per vehicle. Likewise, the EU’s data-center energy-efficiency directive, aiming for PUE below 1.3 in new builds after 2027, cements demand for rectifiers that tolerate 175 °C junctions during high-temperature soak tests, ensuring power stages hit 96% plus efficiency without bulky heat sinks.

By Package Type: Surface Mount Outpaces Through-Hole

Surface-mount formats already held 64.63% Europe semiconductor diode market share in 2025 and are growing fastest at 2.83% CAGR, propelled by automotive mandates for side-wettable flanks that enable optical joint-inspection under IPC-A-610 Class 3 guidelines. Nexperia’s DFN2020MD-6, Infineon’s CFP3-CFP15 and onsemi’s DPAK-7 packages integrate copper clips that cut thermal resistance below 1.5 K/W, allowing SiC Schottkys to carry 175 °C junction ratings without external heat spreaders. Flip-chip and wafer-level chip-scale packages are also proliferating in 40 Gbps USB4 and Thunderbolt ports, where parasitic inductance under 0.5 nH is critical for signal integrity. Automotive Tier-1s increasingly specify wettable-flank packages to automate AOI, trimming manual X-ray inspections and saving up to EUR 0.04 per board in rework costs.

Through-hole devices persist only where bolt-down terminations or press-fit pins simplify heat-sink attachment in Greater Than 100A industrial welders and locomotive traction rectifiers, but the segment is contracting 1-2% annually as SiC power modules displace discrete diodes. Panel-level reflow ovens now dominate automotive body-electronics lines in central Europe, and every incremental second of time-above-liquid drives OEMs toward smaller, thinner QFN and DFN outlines. Packaging houses in Malaysia and the Czech Republic report wafer-level chip-scale TVS volumes doubling between 2024 and 2026, primarily for infotainment and ADAS Ethernet PHYs. Looking ahead, surface-mount share should climb to roughly 68% of the Europe semiconductor diode market by 2031, with most of the upside captured by flip-chip TVS arrays and high-current copper-clip Schottkys.

Geography Analysis

Germany generated 28.23% of Europe semiconductor diode market revenue in 2025, powered by Infineon’s Smart Power Fab ramp and the EUR 10 billion (USD 11.61 billion) ESMC JV, yet faces cost headwinds from 197 EUR/MWh electricity prices and complex permitting.[4]Institute for Security and Development Policy, “Challenges Faced by TSMC and Its Suppliers in Expanding to Europe,” ISDP.EU The domestic automotive supply chain, worth 10% of GDP, remains the main off-take channel for SiC Schottkys and GaN TVS arrays.

Italy is the fastest-growing locale at 2.71% CAGR, propelled by STMicroelectronics’ SiC device and substrate complexes in Catania and state-aided advanced-packaging commitments in Novara. Tier-1s such as Marelli embed SiC rectifiers in brake-by-wire and 800 V inverter stacks, pushing volume shipments from 2027 onward.

France, the United Kingdom and Spain jointly accounted for roughly one-third of regional sales in 2025. France benefits from the EUR 7.5 billion (USD 8.70 billion) Crolles FD-SOI line, Spain from the Imec Málaga hub seeded with EUR 615 million (USD 713.75 million), and the UK from design-centric compound-semiconductor R&D rather than high-volume fabs. Austria, Czech Republic, Poland and Nordics fill out the “rest of Europe” cohort, highlighted by onsemi’s Rožnov expansion and ams-OSRAM’s Premstätten CMOS line.

Competitive Landscape

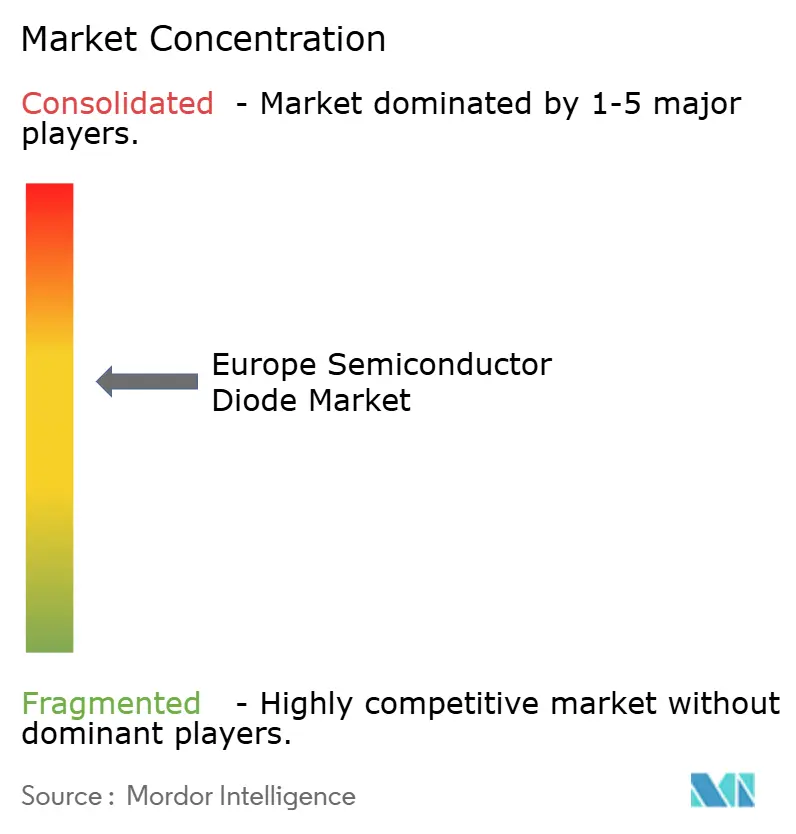

The Europe semiconductor diode market is moderately fragmented, with the top five suppliers controlling about 55-60% of revenue, leaving niches for ultra-low-capacitance ESD arrays and LiDAR-grade laser diodes. Vertical integration is the dominant cost-control lever: STMicro’s EUR 730 million (USD 847.21 million) substrate project aims to internalize 40% of SiC wafer needs by 2026, while Infineon’s Dresden line scales to 200 mm and pilots 300 mm SiC by late 2026.

Nexperia’s trench Schottkys win sockets in 48 V automotive DC-DC boards through improved thermal stability. Infineon’s CoolSiC device family anchors premium German OEM designs, and onsemi’s EliteSiC suite joins traction-inverter and industrial-drive bids. Barriers such as AEC-Q101 zero-defect criteria and 18-month PPAP queues insulate incumbents; newer players like GeneSiC must secure LTAs or pivot to GaN TVS niches.

Fabless disruptors leverage GaN for MHz-class power converters, and foundry partners propose chiplet-based co-packages that integrate SiC diodes with MOSFETs. Moderate consolidation is likely as IDMs scoop substrate specialists and marginal suppliers retreat to aerospace or defense micro-segments.

Europe Semiconductor Diode Industry Leaders

Infineon Technologies AG

STMicroelectronics N.V.

Nexperia B.V.

Vishay Intertechnology, Inc.

onsemi Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: EU invests EUR 700 million (USD 812.44 million) in the NanoIC pilot line for 300 mm diode prototyping aimed at SMEs.

- September 2025: All 27 EU states sign the Semicon Coalition declaration, paving the way for Chips Act 2.0 and expanded R&D funding.

- May 2025: The German government granted final approval for Infineon’s EUR 5 billion (USD 5.80 billion) Smart Power Fab, including EUR 1 billion (USD 1.16 billion) public funding.

- January 2025: Spain approves Imec’s EUR 615 million (USD 713.79 million) Malaga research and manufacturing center, focusing on advanced packaging.

Europe Semiconductor Diode Market Report Scope

The Europe Semiconductor Diode Market is witnessing significant growth, driven by advancements in technology, increasing demand across various end-use industries, and the rising adoption of energy-efficient electronic components. The market's expansion is further supported by the growing focus on renewable energy systems and the integration of semiconductor diodes in electric vehicles and smart devices.

The Europe Semiconductor Diode Market Report is Segmented by Type (Schottky, Zener, TVS/ESD, Laser, Small-Signal Switching, Other Materials), Base Material (Silicon, Silicon Carbide, Gallium Nitride, Other Materials), End-Use Industry (Automotive and Transportation, Consumer Electronics, Communications Infrastructure, Industrial Automation and Power, Computing and Data Centre, Others), Application (Power Rectification and Conversion, Voltage Regulation and Reference, Electrostatic/Surge/Circuit Protection, Other Applications), Package Type (Surface Mount, Through-Hole), and Geography (Germany, United Kingdom, France, Italy, Spain, Rest of Europe). Market Forecasts are Provided in Terms of Value (USD).

| Schottky |

| Zener |

| TVS / ESD |

| Laser |

| Small-Signal Switching |

| Other Types |

| Silicon (Si) |

| Silicon Carbide (SiC) |

| Gallium Nitride (GaN) |

| Other Base Materials |

| Automotive and Transportation |

| Consumer Electronics |

| Communications Infrastructure |

| Industrial Automation and Power |

| Computing and Data Centre |

| Other End-Use Industries |

| Power Rectification and Conversion |

| Voltage Regulation and Reference |

| Electrostatic / Surge / Circuit Protection |

| Other Applications |

| Surface Mount (SMD) |

| Through-Hole |

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Rest of Europe |

| By Type | Schottky |

| Zener | |

| TVS / ESD | |

| Laser | |

| Small-Signal Switching | |

| Other Types | |

| By Base Material | Silicon (Si) |

| Silicon Carbide (SiC) | |

| Gallium Nitride (GaN) | |

| Other Base Materials | |

| By End-Use Industry | Automotive and Transportation |

| Consumer Electronics | |

| Communications Infrastructure | |

| Industrial Automation and Power | |

| Computing and Data Centre | |

| Other End-Use Industries | |

| By Application | Power Rectification and Conversion |

| Voltage Regulation and Reference | |

| Electrostatic / Surge / Circuit Protection | |

| Other Applications | |

| By Package Type | Surface Mount (SMD) |

| Through-Hole | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe |

Key Questions Answered in the Report

What is the forecast value of the Europe semiconductor diode market by 2031?

The market is projected to reach USD 821.38 million by 2031.

Which country will register the fastest growth through 2031?

Italy is expected to grow at a 2.71% CAGR, underpinned by large-scale SiC investments in Catania.

Which diode type commands the largest revenue share?

Schottky diodes led with 43.12% share in 2025 thanks to rectification efficiency.

Why are SiC diodes gaining traction in Europe?

SiC cuts switching losses by 30-40% in 800 V BEV inverters and 650 V industrial drives, justifying its cost premium.

What packaging trend is shaping automotive designs?

Surface-mount packages with side-wettable flanks dominate, covering 64.63% of shipments in 2025 and growing fastest at 2.83% CAGR.

Page last updated on: