Bearing Isolators Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

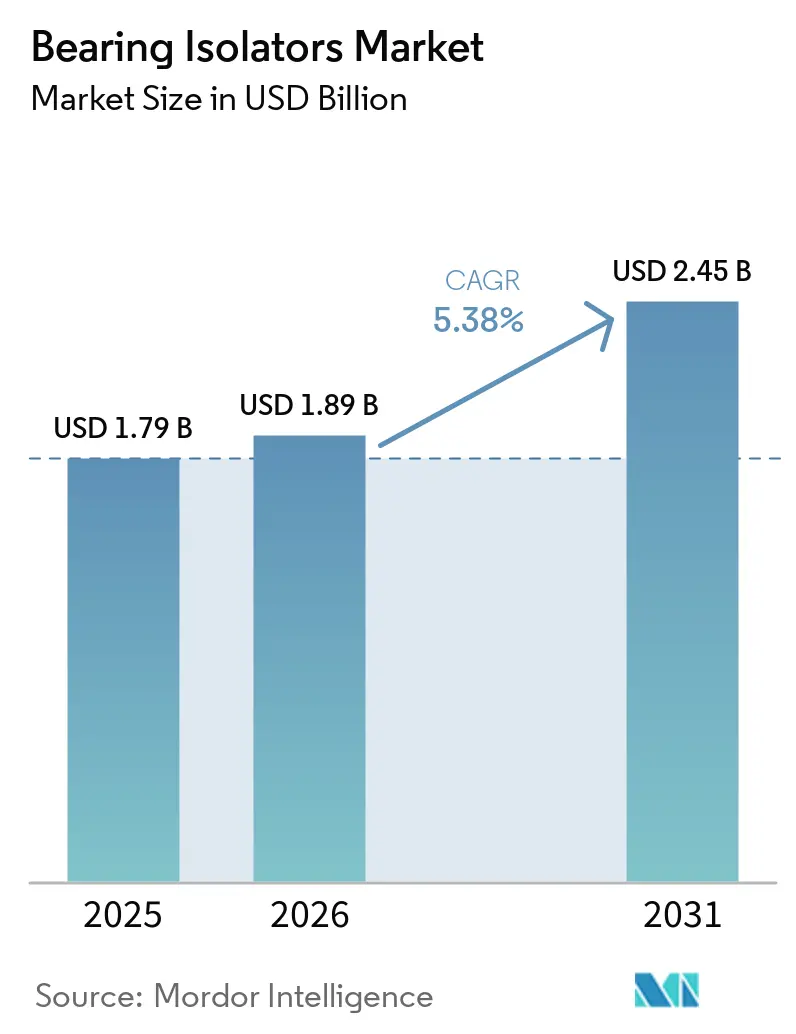

| Market Size (2026) | USD 1.89 Billion |

| Market Size (2031) | USD 2.45 Billion |

| Growth Rate (2026 - 2031) | 5.38% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

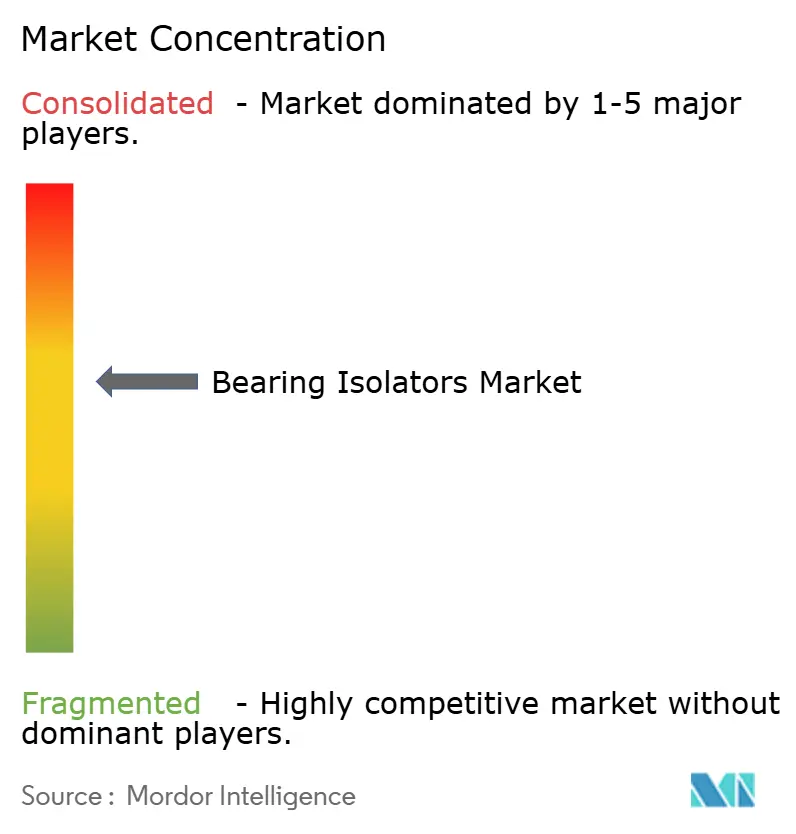

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Bearing Isolators Market Analysis by Mordor Intelligence

The Bearing Isolators Market size is projected to be USD 1.79 billion in 2025, USD 1.89 billion in 2026, and reach USD 2.45 billion by 2031, growing at a CAGR of 5.38% from 2026 to 2031. Demand is strengthening as variable-frequency drives expose legacy motors to shaft-voltage damage, making non-contact and shaft-grounding designs the preferred replacement choice. In ASEAN, a 147% manufacturing-FDI surge in 2024 is translating into greenfield pump, compressor, and turbine installations that specify labyrinth or magnetic protection from day one. Material innovation is reshaping value propositions: additive-manufactured composite isolators that weigh 35% less than bronze are now viable for offshore wind nacelles. Competitive intensity is rising as tier-one bearing makers add seal portfolios through acquisition, while niche houses launch hybrid designs that tolerate misalignment yet maintain zero-wear operation.

Key Report Takeaways

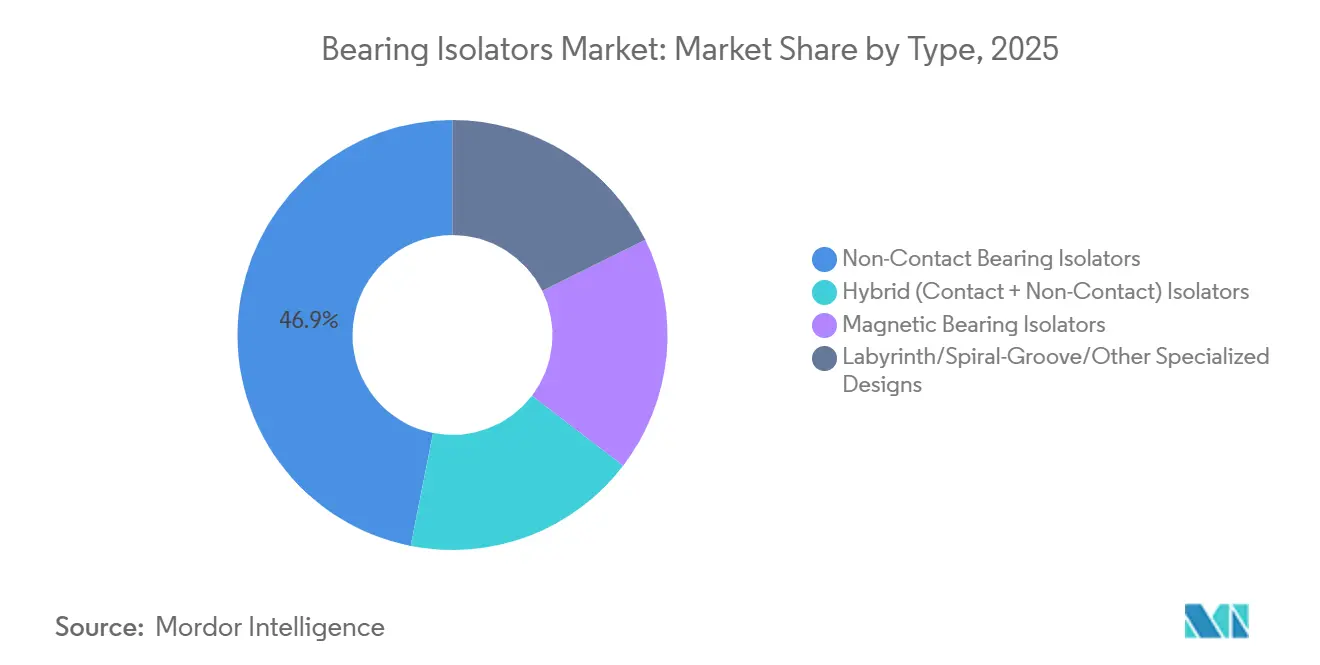

- By type, non-contact bearing isolators held 46.89% of the Bearing Isolators market share in 2025, whereas magnetic bearing isolators posted the highest projected CAGR at 5.90% through 2031.

- By material, metallic (bronze, stainless, and aluminum) accounted for 50.87% of the bearing isolators market size in 2025, while composite/hybrid materials are forecast to advance at a 6.34% CAGR to 2031.

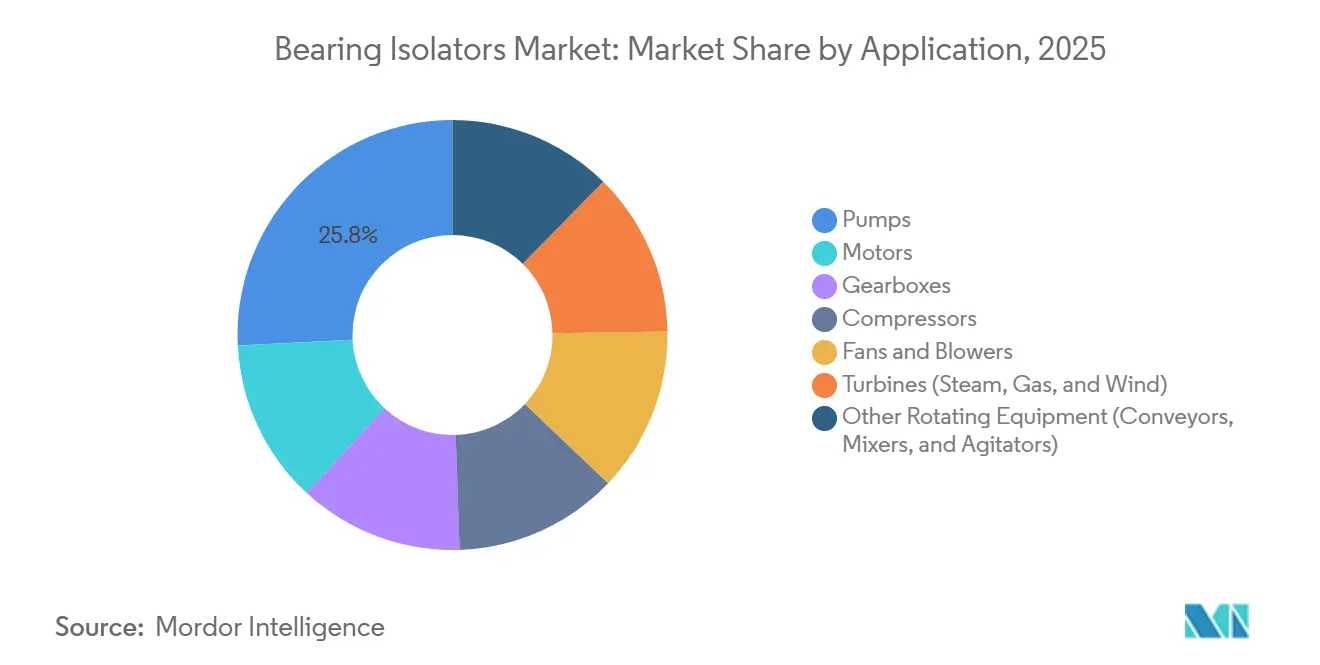

- By application, pumps led with 25.77% revenue share in 2025; turbines (steam, gas, and wind) are slated to expand at a 6.33% CAGR through 2031.

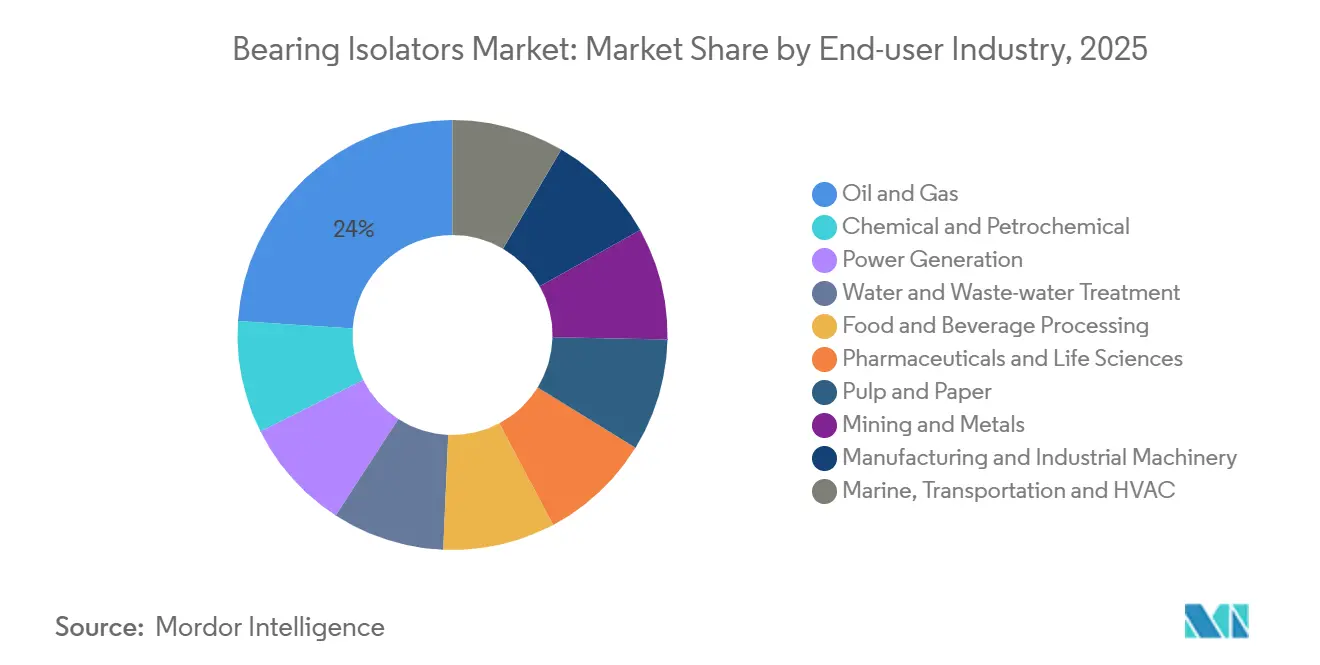

- By end-user industry, oil and gas commanded 23.96% of demand in 2025, but power generation exhibits the quickest growth at 6.45% CAGR over the forecast period (2026-2031).

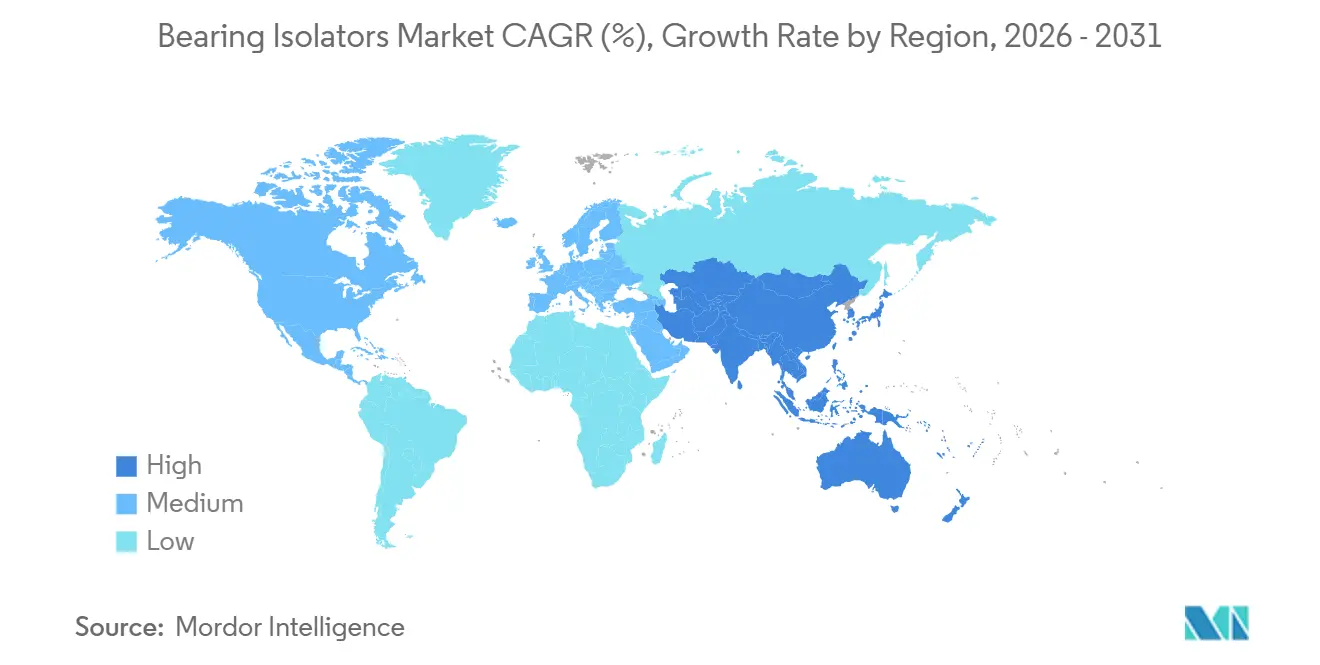

- By region, Asia-Pacific accounted for the largest share of 40.78% in 2025, and is projected to grow at a CAGR of 6.39% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Bearing Isolators Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing demand for maintenance-free bearing protection | +1.2% | North America & Europe core, global spillover | Medium term (2-4 years) |

| Increasing equipment uptime and reliability requirements | +1.0% | Oil & gas, power generation worldwide | Long term (≥ 4 years) |

| Expansion of manufacturing and heavy industries in emerging markets | +1.5% | APAC core with Middle East & Africa spillover | Short term (≤ 2 years) |

| Stricter workplace safety and machinery regulations | +0.8% | North America, EU, early Japan / Korea | Medium term (2-4 years) |

| Integration of shaft-grounding bearing isolators | +0.7% | Motor-intensive sectors worldwide | Short term (≤ 2 years) |

| Additive-manufactured composite isolators for renewables | +0.4% | Europe offshore wind, North America onshore, APAC emerging | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Demand for Maintenance-Free Bearing Protection

Industrial buyers now prioritize total cost of ownership. Liebherr’s 2024 solid-lubrication system set expectations for 10-15-year service life without re-greasing. Armstrong followed by launching circulators in 2025 that pair permanent seals with NSF/ANSI 61 compliance, further validating the value narrative. A USD 300 non-contact isolator averts pump teardowns that cost USD 15,000, paying for itself at the first avoided failure. Schaeffler’s induction-heating tools, released in 2025, let crews install isolators during planned outages, cutting downtime in half. Water-treatment operators, facing USD 50,000-per-day penalties for service interruptions, are therefore standardizing on labyrinth or magnetic formats[1]U.S. Environmental Protection Agency, “Water Infrastructure Needs Survey 2024,” epa.gov.

Increasing Equipment Uptime and Reliability Requirements

Digital-twin adoption is deepening. Siemens Energy’s Omnivise suite began ingesting bearing-housing vibration data in 2025 to predict seal-face wear 90 days ahead, reducing forced outages by 40%. Penalty clauses in power-purchase agreements make each 1% availability shortfall worth USD 2 million in lost revenue on a 500 MW station. John Crane’s Type 93AX coaxial seal, launched mid-2025, holds contact pressure over 0.5 mm of shaft runout, preventing leaks that would otherwise trip turbines. An EASA (European Union Aviation Safety Agency) 2024 study found that over-greasing causes 36% of electric-motor failures, intensifying the pivot toward grease-free isolators.

Expansion of Manufacturing and Heavy Industries in Emerging Markets

ASEAN’s USD 226 billion FDI (Foreign Direct Investment) influx in 2024 is driving new plant builds that specify non-contact solutions from inception. India’s machinery imports jumped 22% in fiscal 2025, with pumps and compressors outpacing all other categories. China’s 1.8 billion-unit 2024 motor output offers a massive installed base for shaft-grounding isolators. Export-oriented factories increasingly treat ISO 7544:2024 contamination-test compliance as a procurement prerequisite, boosting premium isolator demand.

Stricter Workplace Safety and Machinery Regulations

OSHA (Occupational Safety and Health Administration)’s updated 1910.212 standard became effective January 2025, compelling food and pharma plants to block lubricant migration, which elevates demand for NSF H1-certified bearing isolators. The 2024 amendment to Europe’s Machinery Directive now requires bearing-failure risk reviews above 3,000 RPM, penalizing elastomeric lip seals. Japan’s 2025 safety guideline caps contamination-ingress rates, effectively mandating non-contact architectures in high-uptime equipment.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher initial cost versus contact seals | -0.9% | Emerging markets globally | Short term (≤ 2 years) |

| Technical limits in high-speed or misaligned applications | -0.5% | Aerospace, motorsports niches | Medium term (2-4 years) |

| OEM shift to fully sealed “maintenance-free” motors | -0.7% | North America & Europe first, APAC later | Long term (≥ 4 years) |

| Raw-material price volatility for copper-/nickel alloys | -0.6% | Global, strongest in bronze supply chain | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Higher Initial Cost Versus Contact Seals

Non-contact bearing isolators typically command a 3-5× price premium over elastomeric lip seals, a gap that procurement teams in cost-constrained markets struggle to justify despite superior total cost of ownership. A bronze labyrinth isolator for a 100 HP motor retails at USD 250-350, whereas a nitrile lip seal costs USD 60-80, creating a USD 190-270 upfront delta that requires multi-year payback modeling to rationalize[2]Parker Hannifin, “Labyrinth vs Lip Seal Cost Comparison,” parker.com. Timken’s EcoTurn, priced at USD 180 since 2025, narrows the gap, yet split incentives between procurement and maintenance still slow adoption in India and Southeast Asia.

Technical Limits in High-Speed or Misaligned Applications

Non-contact isolators rely on tight clearances, typically 0.2-0.5 mm, to exclude contaminants, yet shaft runout from misalignment or bearing wear can compromise this gap, allowing ingress. Marathon Electric's technical documentation for its sealed motor line, updated in 2025, specifies maximum shaft deflection of 0.15 mm for labyrinth-seal effectiveness, a tolerance that many legacy installations cannot meet without costly realignment. High-speed limits remain: Isomag’s VFD-rated unit tops out at 7,200 RPM, below turbomolecular pump needs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Magnetic Isolators Gain Traction in High-Reliability Sectors

Non-contact labyrinth formats, while still representing the 46.89% of the Bearing Isolators market in 2025, now serve mainly pumps and standard-speed motors. Compliance with ISO 16281:2025, which more harshly derates lip seals under contamination, is hastening the pivot toward magnetic forms. Magnetic architectures are advancing at a CAGR of 5.90% for the forecast period (2026-2031) and are increasingly preferred for high-speed turbines that demand zero wear. Combined-cycle gas-turbine operators find that Isomag’s hybrid ceramic models extend service intervals to 60,000 hours.

Labyrinth, spiral-groove, and other specialized niches remain essential for cryogenic pumps and subsea drives where magnetic fluids or elastomers cannot survive extreme conditions. For misalignment-prone shafts, hybrid O-ring plus PTFE concepts such as John Crane’s 8628VL tolerate 1.0 mm runout, broadening addressable installations.

By Material: Composite Innovation Challenges Metallic Incumbents

Metallic (Bronze, Stainless, and Aluminum) designs held 50.87% share of the Bearing Isolators market size in 2025, led by bronze and stainless steel in corrosive oil-and-gas or pharma wash-down situations. Yet the composite/hybrid materials segment is on a 6.34% expansion trajectory for the forecast period (2026-2031). PEEK-reinforced PTFE achieved 60% lower wear in 2025 lab tests, accelerating wind-turbine adoption where nacelle weight savings translate to cost per kilowatt.

Bronze will remain the default for sour-gas or sulfuric-acid exposure until polymer chemistry matures further. Stainless 316L gained momentum after Parker Hannifin introduced an FDA (Food and Drug Administration)-compliant version that survives 150°C steam-sterilization cycles. Aluminum, 65% lighter than bronze, now replaces heavier units in ceiling-mounted HVAC retrofits.

By Application: Turbines Drive Fastest Growth

Pump installations represented 25.77% of 2025 demand, but turbines (steam, gas, and wind) are the fastest-growing slot at 6.33% CAGR for the forecast period (2026-2031) as plant operators stretch overhaul intervals from 24,000 to 60,000 hours. GE Vernova’s 2025 bulletin explicitly recommends composite isolators for HA-class gas turbines, cementing specification momentum.

In offshore wind, Vestas now specifies IP68-rated hybrid metal-PTFE units that handle 1.5 bar differentials during flooding events. Motors, gearboxes, and compressors together form a mature segment where adoption exceeds 60%; additional volume, therefore, stems mostly from VFD (Variable Frequency Drive) retrofits rather than first-time installs.

By End-user Industry: Power Generation Leads Growth

Oil and gas remained the single-largest customer base at 23.96% in 2025, yet power generation outpaced at 6.45% CAGR for the forecast period (2026-2031) as digital-twin tools quantify downtime savings. Siemens Energy’s Omnivise platform covers 120 GW of turbines and now treats isolator health as a key variable.

Municipal water treatment follows closely, buoyed by a USD 625 billion U.S. infrastructure backlog that flags pump reliability as a top-10 concern. Food-processing plants, spurred by NSF requirements, and pulp-and-paper mills aiming to cut grease consumption round out the mid-tier adopters.

Geography Analysis

Asia-Pacific held 40.78% of the Bearing Isolators market share in 2025 and will grow at 6.39% through 2031. China’s output of 1.8 billion motors in 2024 provides both OEM (Original Equipment Manufacturer) and retrofit pull. India’s 22% machinery-import rise and ASEAN’s USD 226 billion FDI wave reinforce a pattern of design-stage isolator specification. ISO 17956:2025 adoption in Japan and South Korea further penalizes contact seals, accelerating regional transitions.

In North America, OSHA’s 2025 guarding rule is nudging food and pharma plants to swap lip seals for NSF H1-rated isolators. Canadian oil-sands trials showed an 80% cut in bearing swaps after VBMag installations. Near-shoring in Mexico is fueling labyrinth-seal demand for cleanroom assembly conveyors.

Europe’s market share in 2025 was anchored by offshore-wind uptake. System Seals’ composite units now appear in 60% of new North Sea turbines. The revised 2006/42/EC directive’s higher-speed trigger levels catalyze upgrades across Germany and France. Russia pivots to in-house designs amid supply-chain rifts. South America and MEA together represent less than 10% but show pockets of demand in mining, petrochemicals, and desalination.

Competitive Landscape

The Bearing Isolators market is moderately concentrated. Margin pressure from bronze and nickel swings spurs materials R&D, while regulatory certifications, NSF H1, FDA 21 CFR 178.3570, ISO 21469, allow certified suppliers to price at 15-25% premiums in contamination-sensitive sectors. Smaller firms specializing in magnetic or shaft-grounding formats, including Inpro/Seal and Isomag, retain outsized pricing power because they mitigate VFD-induced failures that cost operators far more than the isolator itself.

Bearing Isolators Industry Leaders

InproSeal

Garlock, an Enpro Inc.

AESSEAL

John Crane

The Timken Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: At CES 2025, Schaeffler highlighted its expanded motion technology portfolio, showcasing advanced bearing solutions. The company enhanced its expertise in battery technology and industrial automation to address the rising demand for bearing isolators in electric vehicle powertrains and automated manufacturing systems.

- August 2024: SKF acquired the Lubrication and Flow Management divisions of John Sample Group to strengthen its lubrication management expertise and expand its presence in India and Southeast Asia. It reduced premature bearing failures caused by inadequate lubrication, improved the performance of bearing isolators, and influenced market demand.

Global Bearing Isolators Market Report Scope

Bearing isolators are non-contacting, two-part labyrinth seals (stator and rotor) that provide permanent protection for rotating equipment by preventing lubrication loss and contaminating ingress.

The Bearing Isolators market is segmented by type, material, application, end-user industry, and geography. By type, the market is segmented into non-contact bearing isolators, hybrid (contact + non-contact) isolators, magnetic bearing isolators, and labyrinth/spiral-groove/other specialized designs. By material, the market is segmented into metallic (bronze, stainless, and aluminum), non-metallic (PTFE, UHMWPE, and elastomers), and composite/hybrid materials. By application, the market is segmented into pumps, motors, gearboxes, compressors, fans and blowers, turbines (steam, gas, and wind), and other rotating equipment (conveyors, mixers, and agitators). By end-user industry, the market is segmented into oil and gas, chemical and petrochemical, power generation, water and waste-water treatment, food and beverage processing, pharmaceuticals and life sciences, pulp and paper, mining and metals, manufacturing and industrial machinery, and marine, transportation and HVAC. The report also covers the market size and forecasts for bearing isolators in 17 countries across major regions. The market sizes and forecasts are provided in terms of value (USD).

| Non-Contact Bearing Isolators |

| Hybrid (Contact + Non-Contact) Isolators |

| Magnetic Bearing Isolators |

| Labyrinth/Spiral-Groove/Other Specialized Designs |

| Metallic (Bronze, Stainless, and Aluminum) |

| Non-Metallic (PTFE, UHMWPE, and Elastomers) |

| Composite/Hybrid Materials |

| Pumps |

| Motors |

| Gearboxes |

| Compressors |

| Fans and Blowers |

| Turbines (Steam, Gas, and Wind) |

| Other Rotating Equipment (Conveyors, Mixers, and Agitators) |

| Oil and Gas |

| Chemical and Petrochemical |

| Power Generation |

| Water and Waste-water Treatment |

| Food and Beverage Processing |

| Pharmaceuticals and Life Sciences |

| Pulp and Paper |

| Mining and Metals |

| Manufacturing and Industrial Machinery |

| Marine, Transportation and HVAC |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Non-Contact Bearing Isolators | |

| Hybrid (Contact + Non-Contact) Isolators | ||

| Magnetic Bearing Isolators | ||

| Labyrinth/Spiral-Groove/Other Specialized Designs | ||

| By Material | Metallic (Bronze, Stainless, and Aluminum) | |

| Non-Metallic (PTFE, UHMWPE, and Elastomers) | ||

| Composite/Hybrid Materials | ||

| By Application | Pumps | |

| Motors | ||

| Gearboxes | ||

| Compressors | ||

| Fans and Blowers | ||

| Turbines (Steam, Gas, and Wind) | ||

| Other Rotating Equipment (Conveyors, Mixers, and Agitators) | ||

| By End-user Industry | Oil and Gas | |

| Chemical and Petrochemical | ||

| Power Generation | ||

| Water and Waste-water Treatment | ||

| Food and Beverage Processing | ||

| Pharmaceuticals and Life Sciences | ||

| Pulp and Paper | ||

| Mining and Metals | ||

| Manufacturing and Industrial Machinery | ||

| Marine, Transportation and HVAC | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the Bearing Isolators market?

The Bearing Isolators Market size is projected to be USD 1.79 billion in 2025, USD 1.89 billion in 2026, and reach USD 2.45 billion by 2031, growing at a CAGR of 5.38% from 2026 to 2031.

Which segment will post the fastest growth through 2031?

Magnetic isolators are forecast to grow at 5.90% CAGR as power-generation and VFD-driven assets demand zero-wear protection.

Why are composite materials gaining ground over bronze isolators?

Additive-manufactured PEEK-PTFE designs cut weight 35% and dissipate heat better, which matters in offshore wind and high-speed compressors.

How do shaft-grounding isolators improve motor reliability?

They divert VFD-induced shaft currents that can flute bearings and cut life by 80%, preventing USD 8,000-12,000 repair events.

Page last updated on: