Europe Almond Milk Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

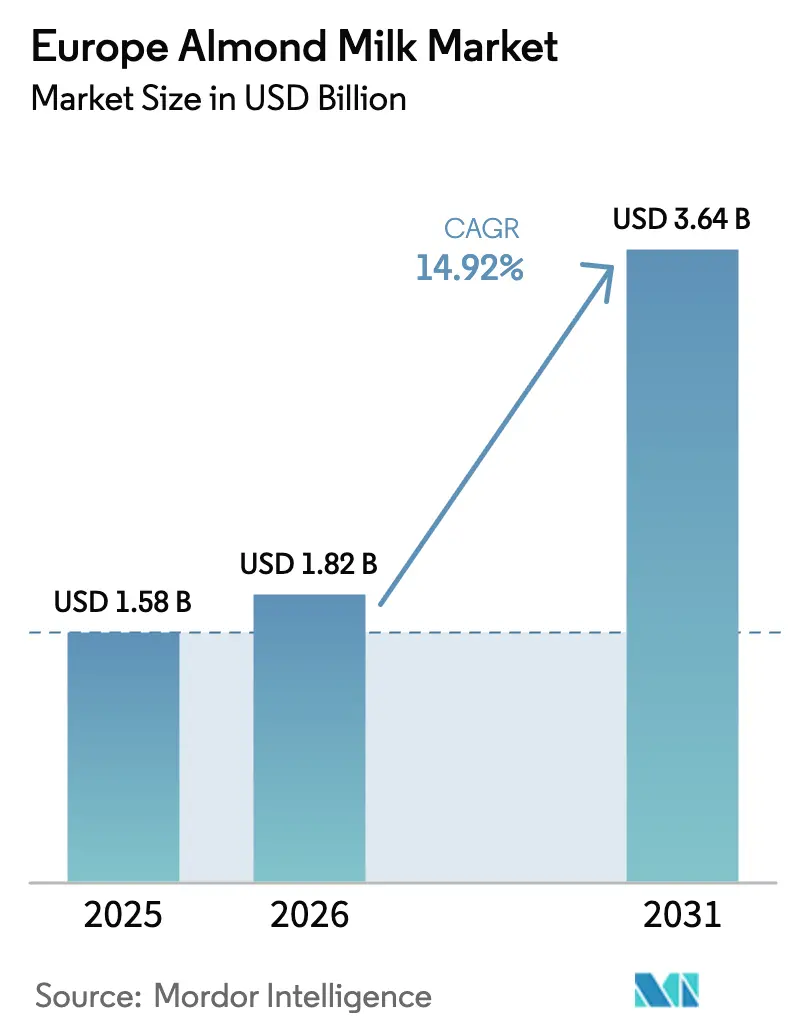

| Base Year Market Size (2025) | USD 1.58 Billion |

| Market Size (2026) | USD 1.82 Billion |

| Market Size (2031) | USD 3.64 Billion |

| Growth Rate (2026 - 2031) | 14.92% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Almond Milk Market Analysis by Mordor Intelligence

The Europe almond milk market size is expected to grow from USD 1.58 billion in 2025 to USD 1.82 billion in 2026 and is forecast to reach USD 3.64 billion by 2031 at 14.92% CAGR over 2026-2031. Consumers are increasingly driving demand due to heightened awareness of lactose intolerance, the growing adoption of vegan and flexitarian diets, and continuous product innovations that successfully replicate the taste and functionality of dairy products. Manufacturers are enhancing consumer appeal by introducing premium glass packaging, fortified formulations, and barista-grade products. Additionally, companies are integrating these products into food services, which expands their usage beyond retail shelves and into diverse consumption occasions. Germany leads the market with strong brand acceptance, while the Netherlands is experiencing the fastest unit expansion. Meanwhile, a consolidated competitive landscape ensures pricing discipline, even as VAT disparities persist.

Key Report Takeaways

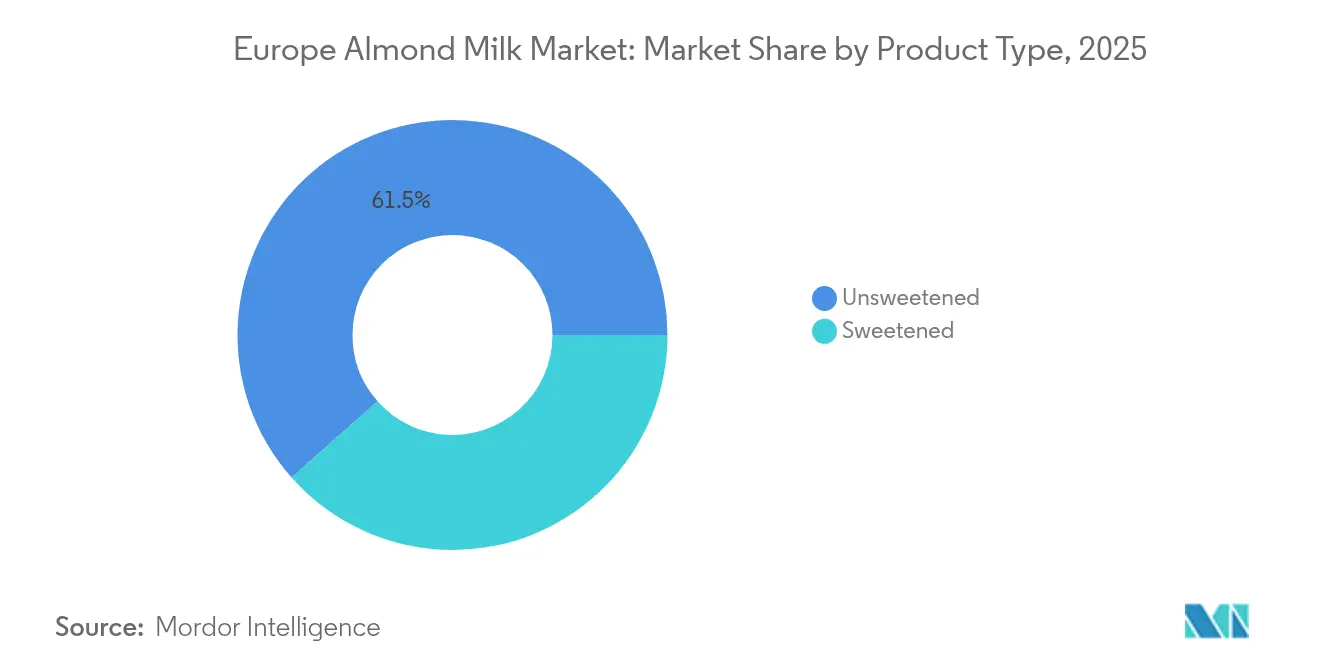

- By product type, unsweetened variants commanded 61.54% of Europe almond milk market share in 2025; sweetened products are forecast to expand at a 15.12% CAGR to 2031.

- By packaging type, carton formats led with 57.76% share of the Europe almond milk market size in 2025, while glass bottles are advancing at a 15.34% CAGR through 2031.

- By flavor, unflavored products captured 67.93% of the Europe almond milk market in 2025; flavored options are poised to grow at a 15.98% CAGR to 2031.

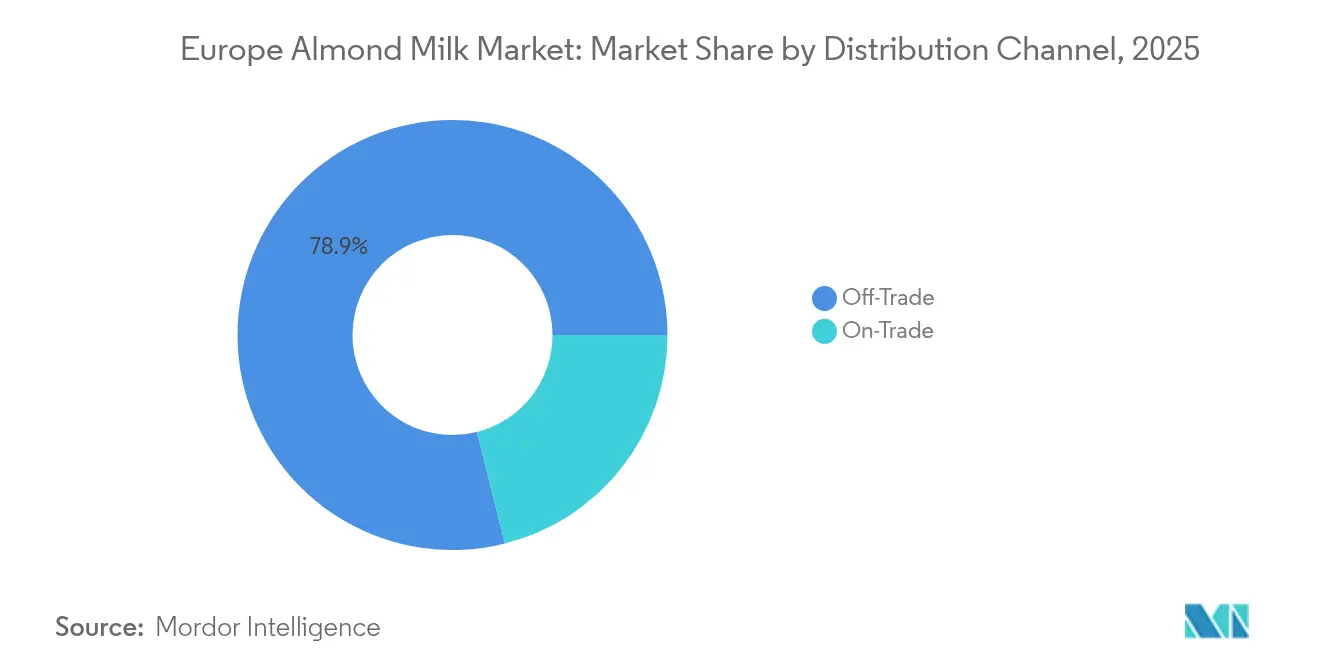

- By distribution channel, off-trade outlets held 78.92% of Europe almond milk market share in 2025, whereas on-trade channels are projected to register a 15.46% CAGR to 2031.

- By geography, Germany accounted for 23.41% share of the Europe almond milk market size in 2025 and the Netherlands is set to expand at a 15.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Almond Milk Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing cases of lactose intolerance and dairy allergies | +2.8% | Regional, with higher prevalence in Northern Europe | Long term (≥ 4 years) |

| Growing vegan population and adoption of plant-based diets | +3.2% | Germany, Netherlands, United Kingdom core markets | Medium term (2-4 years) |

| Continuous product innovations, flavors, fortified/functional options | +2.1% | Western Europe, spill-over to Eastern Europe | Short term (≤ 2 years) |

| Strong marketing and brand activity by leading almond milk companies | +1.9% | Germany, United Kingdom, France primary markets | Medium term (2-4 years) |

| Endorsement by nutritionists and fitness influencers | +1.4% | Urban centers across Europe | Short term (≤ 2 years) |

| Inclusion of almond milk in foodservice, cafés, and specialty drinks | +2.7% | Germany, Netherlands, United Kingdom, with expansion to Southern Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Growing cases of lactose intolerance and dairy allergies

The Europe almond milk market is significantly driven by the growing prevalence of lactose intolerance and dairy allergies, which compel consumers to seek dairy-free alternatives. In particular, lactose intolerance leads many to avoid conventional dairy, while milk protein allergies—including in countries like Finland where an estimated 1 in 60,000 newborns are affected [1]Source: Medline Plus, "Lactose Intolerance", www.medlineplus.gov—increase demand for hypoallergenic, plant-based options such as almond milk. This demographic shift toward health-conscious and allergy-aware consumers is complemented by rising veganism and environmental concerns, positioning almond milk as a favored choice for its low calorie, lactose-free, and nutrient-rich profile. The market is also fueled by expanding product innovation, wider retail and online availability, and a move toward sustainable consumption. Increased consumption among fitness-oriented and conscious-eating consumers, alongside endorsements from nutrition experts, further strengthens market growth, making almond milk a staple in beverages, breakfast foods, and dairy-free culinary applications across the region.

Growing vegan population and adoption of plant-based diets

The growing adoption of plant-based diets and the rising vegan population are significant drivers of the Europe almond milk market. Countries such as Finland, Sweden, Germany, and the UK have substantial percentages of their populations embracing vegan or flexitarian lifestyles, motivated by health, environmental, and ethical concerns. This trend encourages increased consumption of almond milk due to its perception as a nutritious, sustainable, and delicious alternative to dairy. Complementing this, the Nordic Nutrition Recommendations 2023 explicitly support a daily intake of 20-30 grams of nuts, underscoring the health benefits linked to nut consumption such as reduced risk of cardiovascular disease and certain cancers [2]Source: NORDIC NUTRITION RECOMMENDATIONS 2023, "Nuts and Seeds", www.pub.norden.org. This guidance strengthens regulatory and nutritional backing for almond-derived products, especially across Scandinavian markets, boosting consumer confidence and market acceptance. Such official endorsements enhance the appeal of almond milk, positioning it as a health-promoting, sustainable choice aligned with evolving dietary recommendations and lifestyle preferences in northern Europe.

Continuous product innovations, flavors, fortified/functional options

Continuous product innovations, including the development of new flavors, fortified, and functional almond milk options, are a key driver of the Europe almond milk market. Brands are actively expanding their portfolios with flavored variants such as vanilla, chocolate, and coffee, catering to diverse consumer tastes and attracting younger demographics. Additionally, fortified almond milks enriched with essential nutrients like calcium, vitamin D, and omega-3 fatty acids cater to health-conscious consumers seeking enhanced nutritional benefits. These innovations align with consumers’ growing demand for plant-based products that offer both taste and functional advantages. Moreover, sustainability efforts through eco-friendly packaging and clean-label certifications further elevate almond milk’s appeal. Market leaders are leveraging these product innovations to differentiate themselves and drive growth, making almond milk a mainstream choice for beverages, cooking, and specialized dietary needs across Europe.

Strong marketing and brand activity by leading almond milk companies

Strong marketing and brand activity by leading almond milk companies significantly drives the Europe almond milk market. Major players like Blue Diamond Growers (Almond Breeze), Danone S.A., Oatly AB, and Nestlé leverage extensive marketing campaigns emphasizing health benefits, sustainability, and lifestyle alignment to enhance brand visibility and consumer trust. These companies invest heavily in digital advertising, influencer partnerships, and cultural marketing that resonates with environmentally conscious and health-aware consumers. Their positioning of almond milk as a premium, nutritious, and sustainable alternative to dairy helps differentiate products in a crowded market. Additionally, strategic retail partnerships and sponsorships within coffee chains and foodservice outlets facilitate consumer trials and frequent usage. This active brand engagement fosters strong consumer loyalty, supports premium pricing strategies, and expands market reach, making marketing a decisive factor in the rapid growth and acceptance of almond milk across diverse European markets.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Higher price point compared to regular dairy milk | -2.4% | Price-sensitive markets: Eastern Europe, Southern Europe | Long term (≥ 4 years) |

| Allergen concerns—almonds are tree nut, limiting market for some | -1.1% | Northern Europe with higher tree nut allergy prevalence | Long term (≥ 4 years) |

| Difficulty in replicating dairy milk's texture and functional characteristics | -1.8% | Traditional dairy markets: France, Italy, Germany | Medium term (2-4 years) |

| Taste and texture acceptance issues in certain consumer segments | -1.6% | Rural and older demographic segments across Europe | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Higher price point compared to regular dairy milk

The higher price point of almond milk compared to regular dairy milk remains a significant market restraint in Europe. Despite its growing popularity due to health benefits, sustainability, and dietary restrictions like lactose intolerance, almond milk typically costs more—often 10-30% higher—than conventional cow’s milk in retail settings. This price difference is driven by factors such as the cost of almonds, processing, and fortified or flavored variants, which increase manufacturing expenses. Consumer price sensitivity, especially amid economic inflation and rising food prices, limits wide adoption among budget-conscious segments. Consequently, the premium pricing can hinder mass-market penetration, particularly in price-sensitive regions or among lower-income groups. While the demand continues to grow, the elevated price remains a barrier for some consumers, challenging almond milk brands to balance quality, innovation, and affordability to sustain long-term growth in Europe's competitive landscape.

Allergen concerns- almonds are a tree nut, limiting market for some

Almond milk’s growth in the European market is restrained by allergen concerns, as almonds are a common tree nut allergen. Adult tree nut allergy prevalence ranges from 1% to 2%, with risks of severe reactions, including anaphylaxis, which create absolute boundaries in market expansion that cannot be overcome through product innovation or marketing efforts [3]Source: NORDIC NUTRITION RECOMMENDATIONS 2023, "Nuts and Seeds", www.pub.norden.org. Strict EU regulations mandate clear allergen labeling of tree nuts like almonds to protect sensitive consumers. This allergenic limitation excludes a segment of consumers with nut allergies from almond milk use, effectively bounding its total addressable market. Consequently, while almond milk enjoys popularity among a broad audience, these allergen issues represent a critical, non-negotiable restraint in Europe’s almond milk market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Sweetened Variants Drive Premium Growth

The segment with the largest market share in the Europe almond milk market is the unsweetened almond milk category, which held approximately 61.54% of the market in 2025. This segment dominates due to the growing preference among health-conscious consumers who prioritize natural, low-calorie, and low-sugar options. Unsweetened almond milk is favored for its clean label appeal and compatibility with vegan and lactose-intolerant diets. It is commonly used as a dairy substitute in beverages, cereals, and cooking. The widespread availability of unsweetened almond milk in supermarkets and health food stores across Europe supports its substantial market share. Consumer education around the benefits of unsweetened products, such as lower sugar intake and fewer additives, further reinforces its lead. Despite its large share, this segment faces increasing competition from flavored and specialty almond milk variants that cater to evolving consumer tastes.

The fastest-growing segment is the sweetened almond milk category, accelerating at a compound annual growth rate (CAGR) of 15.12% through 2031. This rapid growth indicates a consumer willingness to pay a premium for almond milk products with enhanced taste profiles that address traditional barriers to adoption, such as blandness or lack of flavor. Sweetened almond milk appeals especially to younger consumers and those new to plant-based alternatives who prefer a more indulgent flavor. Its growth is driven by innovation in sweeteners, such as natural sugars, and the introduction of a variety of flavors like vanilla, chocolate, and berry blends. Manufacturers are capitalizing on this trend by expanding their product ranges and incorporating functional ingredients like vitamins and minerals. The increasing availability of sweetened almond milk in both retail and foodservice sectors fuels its expansion, as consumers seek convenient and enjoyable plant-based options.

By Packaging Type: Glass Bottles Signal Premium Positioning

The largest segment in the Europe almond milk market by packaging type is the carton format, which commanded a dominant share of approximately 57.76% in 2025. This package type is favored for its sustainability, bulk storage capacity, and convenience, making it the preferred choice for consumers and retailers alike. Cartons are widely accessible across supermarkets and specialty stores, bolstering their market dominance. They also align with the increasing consumer preference for eco-friendly packaging solutions, emphasizing recyclable and biodegradable materials. The extensive presence of carton packaging in retail outlets further consolidates its leading position. With the growing consumer focus on sustainability and convenience, carton formats are expected to retain their large market share in upcoming years.

The fastest-growing packaging segment is glass bottles, with a CAGR of 15.34%. This growth is driven by consumers’ increasing willingness to pay premiums for high-quality, aesthetically appealing packaging that reinforces perceived product value and differentiation. Glass bottles are associated with premium positioning, perceived as more sustainable, and are often used for flavored and specialty almond milk variants. The appeal of glass bottles in premium retail outlets and specialty cafes is accelerating demand, especially among environmentally conscious consumers who favor reusable and recyclable packaging. The trend toward functional and artisanal branding also boosts glass bottle sales, as brands seek to capitalize on their premium and sustainable image. This segment's structure suggests a strategic shift toward packaging that enhances brand perception and aligns with growing eco-conscious consumption behaviors.

By Flavor: Innovation Drives Flavored Segment Expansion

The segment with the largest market share in the Europe almond milk market is the unflavored almond milk category, which held approximately 67.93% of the market in 2025. This dominant share reflects strong consumer preference for the natural and versatile taste profile of unflavored almond milk, making it suitable for a wide range of uses from drinking plain to adding into recipes and beverages. The unflavored variant appeals particularly to health-conscious consumers who prioritize minimal ingredients and lower sugar content, aligning well with clean-label trends. Its broad availability in major supermarkets, specialty health stores, and online platforms further solidifies its position. Despite its high market share, this category remains resilient through consistent innovation, such as fortification with vitamins and minerals.

In contrast, the fastest-growing segment is flavored almond milk, which is expected to grow at a CAGR of 15.98% through 2031. This rapid growth highlights consumers’ increasing willingness to try almond milk variants with enhanced taste profiles that include natural fruit, vanilla, chocolate, and other flavor infusions. Flavored almond milk appeals to younger demographics and those new to plant-based alternatives who may prefer sweeter, more indulgent options. Manufacturers capitalize on this trend with extensive product line expansions and creative flavor launches aimed at diversifying consumer choice and capturing new market segments. The availability of flavored almond milk in foodservice outlets and cafes also helps drive growth as consumers enjoy these products in a variety of out-of-home settings.

By Distribution Channel: On-Trade Expansion Transforms Market Access

The off-trade distribution channel holds the largest market share in the Europe almond milk market, commanding approximately 78.92% of the market in 2025. This dominance is largely due to the extensive availability of almond milk products in supermarkets, hypermarkets, convenience stores, and online retail platforms. These outlets offer consumers easy and frequent access to almond milk as part of their regular grocery shopping, driving sustained high sales volumes. The convenience and variety provided by off-trade channels support consumer loyalty and repeated purchases. Major retailers in key markets such as Germany, the UK, and France have developed dedicated plant-based sections, further boosting off-trade penetration. The wide reach, competitive pricing, and promotional activities in these channels help maintain their stronghold.

Conversely, the on-trade channel is the fastest-growing segment, accelerating at a CAGR of 15.46% through 2031. This segment includes cafes, restaurants, bars, and other foodservice outlets that are increasingly incorporating almond milk into their beverage and food offerings. On-trade growth is powered by strategic penetration into the foodservice sector where consumers are introduced to almond milk in coffee, smoothies, and specialty drinks, expanding overall market exposure. Leading coffee chains such as Starbucks, Costa Coffee, and Caffè Nero widely offer almond milk as a non-dairy option to meet consumer demand for plant-based alternatives outside the home. This channel’s growth reflects a shift in consumer consumption patterns toward out-of-home occasions and experiential purchases. Foodservice venues also act as trial points, converting new consumers who may later purchase almond milk through retail channels.

Geography Analysis

Germany’s market leadership with a 23.41% share in 2025 underscores its high level of consumer acceptance and the presence of a favorable regulatory environment. The country’s sophisticated consumer base values product quality, health benefits, and sustainability, which give established players a competitive advantage. Germany’s strong market position is further reinforced by supportive policies and regulations that promote organic and eco-friendly products. The country's well-developed retail infrastructure and widespread awareness about plant-based diets create a conducive environment for ongoing growth. Local brands and international players alike are leveraging the country’s reputation for quality to sustain their market dominance.

Meanwhile, the Netherlands is experiencing rapid growth at a CAGR of 15.22% through 2031. This dynamic expansion is fueled by the country’s robust innovation ecosystem, which continuously introduces new product formulations and variants. Regulatory frameworks in the Netherlands are progressive and supportive of plant-based development, allowing companies to experiment and optimize their offerings. The country’s progressive mindset towards sustainability and innovation makes it an attractive market for emerging brands and established players seeking to capitalize on consumer preferences for functional, health-oriented, and sustainable products. The regulatory environment encourages Research and development investments and product diversification, driving the accelerated market expansion.

Other European countries are also contributing to the market's overall growth. For example, the UK, France, and Spain are witnessing increasing consumer shifts towards plant-based and organic dairy options, supported by rising health awareness and sustainability concerns. Countries like Sweden and Belgium are gaining traction due to their high environmental consciousness and supportive regulations for plant-based foods. Overall, Europe’s almond milk market is characterized by diverse regional dynamics, with mature markets like Germany setting the pace while emerging markets like the Netherlands surge through innovation and supportive policies. The collective growth across these regions reflects Europe’s expanding appetite for sustainable, healthy, and innovative plant-based dairy alternatives.

Competitive Landscape

The European almond milk market exhibits a moderately high competitive intensity, rated at 7 out of 10, driven largely by the dominance of established multinational corporations. These global players leverage considerable scale advantages across manufacturing, distribution, and marketing investment capabilities, allowing them to maintain strong footholds in key markets. Their established manufacturing infrastructures enable cost efficiencies and high-volume production, while vast distribution networks ensure broad geographic penetration from major western European hubs to emerging markets in the east. Significant marketing budgets facilitate strong brand recognition and enable extensive promotional campaigns, reinforcing consumer loyalty and barrier to entry for smaller players.

Among the leading multinational companies, strategic innovation and diversification play crucial roles in maintaining competitive advantage. Companies continuously invest in research and development to introduce new almond milk variants with added health benefits, fortified nutrition, and innovative flavors, appealing to increasingly sophisticated consumer preferences. Product portfolio expansion also includes premium and specialty almond milk lines, such as barista formulations and organic options, solidifying their appeal across various customer segments.

Moreover, many players are focussing on sustainability throughout the value chain, aligning with rising consumer expectations related to eco-friendly sourcing, packaging, and production practices. Additionally, private label almond milk offerings by grocery chains intensify competition by providing cost-effective alternatives to branded products. The overall industry is dynamic, with mergers, acquisitions, and strategic alliances shaping market structure as players seek to optimize scale and innovation synergy. To remain competitive, companies must continuously innovate, sustain strong retailer relationships, and adopt sustainable practices that resonate with the evolving tastes and values of European consumers.

Europe Almond Milk Industry Leaders

-

Britvic PLC

-

Calidad Pascual SAU

-

Danone S.A.

-

Blue Diamond Growers

-

Nestlé S.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2024: Califia Farms launched Barista Blend range for United Kingdom, including Organic Oat Barista Blend and Almond Barista Blend at GBP 2.35 per liter, formulated specifically for at-home coffee applications with enhanced frothing and steaming capabilities. The launch targets growing demand for organic and almond drinks in professional and home barista segments.

- April 2024: Alpro launched protein-enhanced product lines and 500ml pack sizes across European markets, addressing consumer demand for convenient portion sizes and improved nutritional profiles in plant-based milk alternatives including almond-based formulations.

- December 2023: Blue Diamond Growers extended its Almond Breeze line with the launch of the Almond Breeze Original Almond & Oat Blend. This new plant-based milk blends almonds and oats, delivering 45 calories, 450 mg of calcium, and 4 grams of sugar per 1-cup serving. The product is designed to offer a healthier and creamier version of traditional oat milk.

- February 2023: Danone inaugurated Daniel Carasso Research and Innovation center in Paris-Saclay dedicated to fresh dairy and plant-based products, with specialized plant-based centers in Belgium and USA supporting increased investment in product superiority and innovation launches. This facility expansion demonstrates continued commitment to European plant-based market leadership.

Europe Almond Milk Market Report Scope

Off-Trade, On-Trade are covered as segments by Distribution Channel. Belgium, France, Germany, Italy, Netherlands, Russia, Spain, Turkey, United Kingdom are covered as segments by Country.| Sweetened |

| Unsweetened |

| Carton |

| Plastic Bottle |

| Glass Bottle |

| Others |

| Flavored |

| Un-Flavored |

| Off-Trade | Convenience Stores |

| Online Retail | |

| Specialist Retailers | |

| Supermarkets and Hypermarkets | |

| Others | |

| On-Trade |

| Germany |

| United Kingdom |

| Italy |

| France |

| Spain |

| Netherlands |

| Poland |

| Belgium |

| Sweden |

| Rest of Europe |

| By Product Type | Sweetened | |

| Unsweetened | ||

| By Packaging Type | Carton | |

| Plastic Bottle | ||

| Glass Bottle | ||

| Others | ||

| By Flavor | Flavored | |

| Un-Flavored | ||

| By Distribution Channel | Off-Trade | Convenience Stores |

| Online Retail | ||

| Specialist Retailers | ||

| Supermarkets and Hypermarkets | ||

| Others | ||

| On-Trade | ||

| By Geography | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

Market Definition

- Dairy Alternatives - Dairy alternatives are foods that are made from plant-based milk/oils instead of their usual animal products, such as cheese, butter, milk, ice cream, yogurt, etc. Plant-based or non-dairy milk alternative is the fast-growing segment in the newer food product development category of functional and specialty beverage across the globe.

- Non-Dairy Butter - Non dairy butter is a vegan butter alternative that is made from a mixture of plant oils. With an increase in alternative diets like vegetarianism, veganism, and gluten intolerance, plant butter is a healthy non-dairy substitute for normal butter.

- Non-Dairy Ice Cream - Plant based ice cream is a growing category. Non-dairy ice cream is a type of dessert made without any animal ingredients. This is typically considered a substitute for regular ice cream for those who cannot or do not eat animal or animal-derived products, including eggs, milk, cream, or honey.

- Plant-Based Milk - Plant based milks are milk substitutes that are made from nuts (e.g., hazelnuts, hemp seeds), seeds (e.g., sesame, walnuts, coconuts, cashews, almonds, rice, oats, etc.) or legumes (e.g., soy). Plant-based milk such as soy milk and almond milk have been popular in East Asia and the Middle East for centuries.

| Keyword | Definition |

|---|---|

| Cultured Butter | Cultured butter is prepared by having the raw butter go through chemical processing and has been added with certain emulsifiers and foreign ingredients. |

| Uncultured Butter | This type of butter is one which has not been processed in any way |

| Natural Cheese | The type of cheese in its most natural form. It is made from natural and simple products and ingredients, including fresh and natural salts, natural colors, enzymes, and high-quality milk. |

| Processed Cheese | Processed cheese undergoes the same processes as natural cheese; however, it requires more steps and many different forms of ingredients. Making processed cheese involves melting natural cheese, emulsifying it, and adding preservatives and other artificial ingredients or colorings. |

| Single Cream | Single cream contains around 18% fat. It’s a single layer of cream that appears over boiled milk. |

| Double Cream | Double cream contains 48% fat, more than double the amount of fat of single cream. It’s heavier and thicker than single cream |

| Whipping Cream | This has a much higher fat percentage than single cream (36%). Used to top cakes, pies, and puddings and as a thickener for sauces, soups, and fillings. |

| Frozen Desserts | Desserts that are meant to be eaten in frozen condition. E.g., sherbets, sorbets, frozen yogurts |

| UHT Milk (Ultra-high temperature milk) | Milk heated at a very high temperature. Ultra-high-temperature processing (UHT) of milk involves heating for 1–8 sec at 135–154°C. which kills the spore-forming pathogenic microorganism, resulting in a product with a shelf-life of several months. |

| Non-dairy butter/Plant-based butter | Butter made from plant-derived oil such as coconut, palm, etc. |

| Non-dairy Yogurt | Yogurt made from typically made from nuts, like almonds, cashews, coconuts, and even other foods like soybeans, plantains, oats, and peas |

| On-trade | It refers to restaurants, QSRs, and bars. |

| Off-trade | It refers to supermarkets, hypermarkets, on-line channels, etc. |

| Neufchatel cheese | One of the oldest kinds of cheese in France. It is a soft, slightly crumbly, mold-ripened, bloomy-rind cheese made in the Neufchâtel-en-Bray region of Normandy. |

| Flexitarian | It refers to a consumer preferring a semi-vegetarian diet, that is centered on plant foods with limited or occasional inclusion of meat. |

| Lactose Intolerance | Lactose intolerance is a reaction in digestive system to lactose, the sugar in milk. It causes uncomfortable symptoms in response to the consumption of dairy products. |

| Cream Cheese | Cream cheese is a soft and creamy fresh cheese with a tangy taste made from milk and cream. |

| Sorbets | Sorbet is a frozen dessert made using ice combined with fruit juice, fruit purée, or other ingredients, such as wine, liqueur, or honey. |

| Sherbet | Sherbet is a sweetened frozen dessert made with fruit and some sort of dairy product such as milk or cream. |

| Shelf stable | Foods that can be safely stored at room temperature, or "on the shelf," for at least one year and do not have to be cooked or refrigerated to eat safely. |

| DSD | Direct Store Delivery is the process in supply chain management wherein the product is delivered from manufacturing plant directly to the retailer. |

| OU Kosher | Orthodox Union Kosher is a kosher certification agency based in New York City. |

| Gelato | Gelato is a frozen creamy dessert made with milk, heavy cream and sugar. |

| Grass-fed Cows | Grass-fed cows are allowed to graze in pastures, where they eat a variety of grasses and clover. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms