North America Almond Milk Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

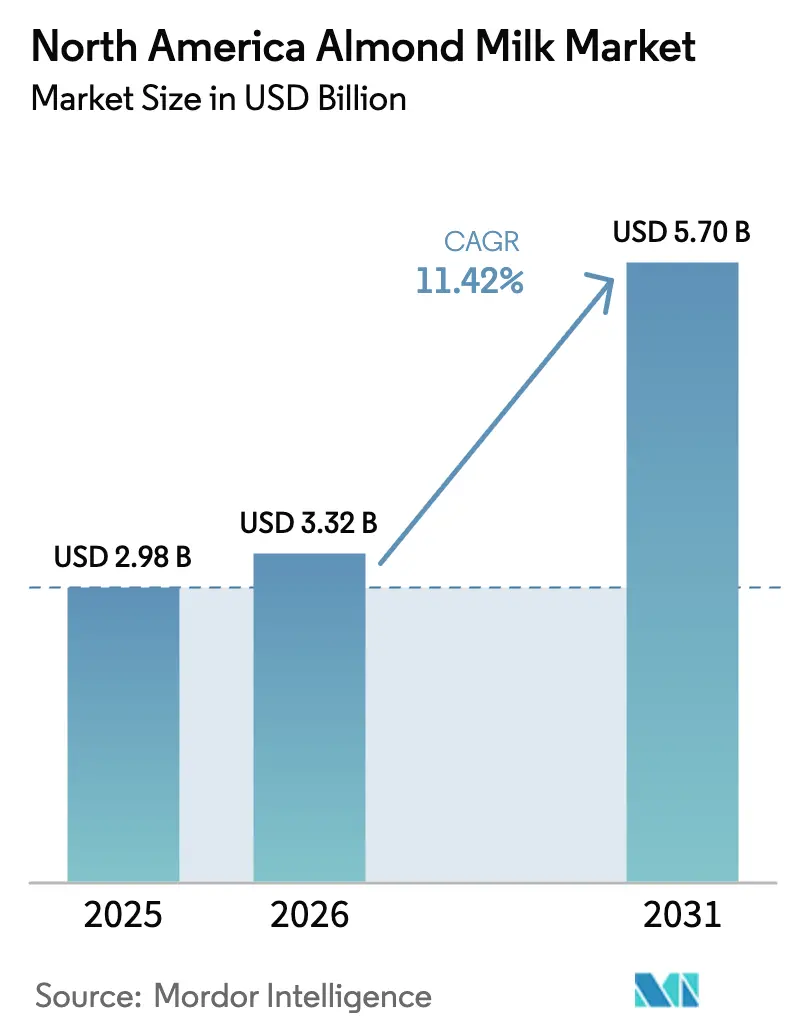

| Base Year Market Size (2025) | USD 2.98 Billion |

| Market Size (2026) | USD 3.32 Billion |

| Market Size (2031) | USD 5.70 Billion |

| Growth Rate (2026 - 2031) | 11.42% CAGR |

| Market Concentration | High |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

North America Almond Milk Market Analysis by Mordor Intelligence

The North American almond milk market size was valued at USD 2.98 billion in 2025 and estimated to grow from USD 3.32 billion in 2026 to reach USD 5.71 billion by 2031, at a CAGR of 11.42% during the forecast period (2026-2031). The market is driven by increasing lactose intolerance, rising adoption of plant-based products, and clearer regulatory guidance on labeling. Lactose intolerance affects 36% of the population in the United States, according to the National Institutes of Health [1]Source: National Institutes of Health, “Lactose Intolerance,” nih.gov. This has naturally steered consumers towards lactose-free beverages. Furthermore, with 47% of American adults now identifying as flexitarians, almond milk is witnessing a sustained boost as households shift from traditional dairy to plant-based alternatives, a trend highlighted by the Centers for Disease Control and Prevention[2]Source: Centers for Disease Control and Prevention, “National Health and Nutrition Examination Survey,” cdc.gov . Health-conscious consumers are fueling demand for both unsweetened variants and indulgent flavored options, reflecting a segmented consumption trend. Robust retail penetration continues to support sales, while foodservice adoption, accelerated by the removal of non-dairy surcharges by major coffee chains, has enhanced mainstream acceptance. Key players, including Blue Diamond, Danone (Silk), and Califia Farms, dominate the distribution network.

Key Report Takeaways

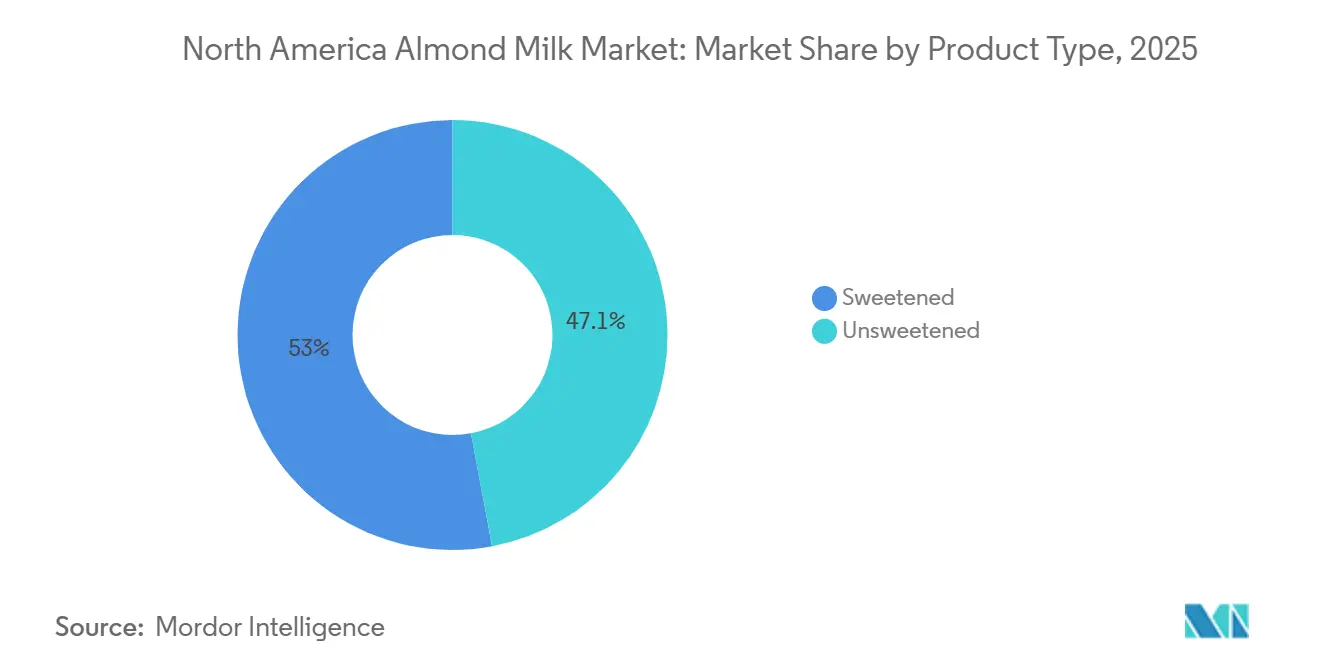

- By product type, unsweetened variants captured 47.05% revenue in 2025; sweetened products are advancing at a 12.66% CAGR to 2031.

- By packaging, cartons retained 37.12% of market share in 2025, while glass bottles are expanding at a 13.35% CAGR through 2031.

- By flavor, unflavored options commanded 67.05% of market share in 2025, whereas flavored SKUs are rising at a 12.07% CAGR over the same horizon.

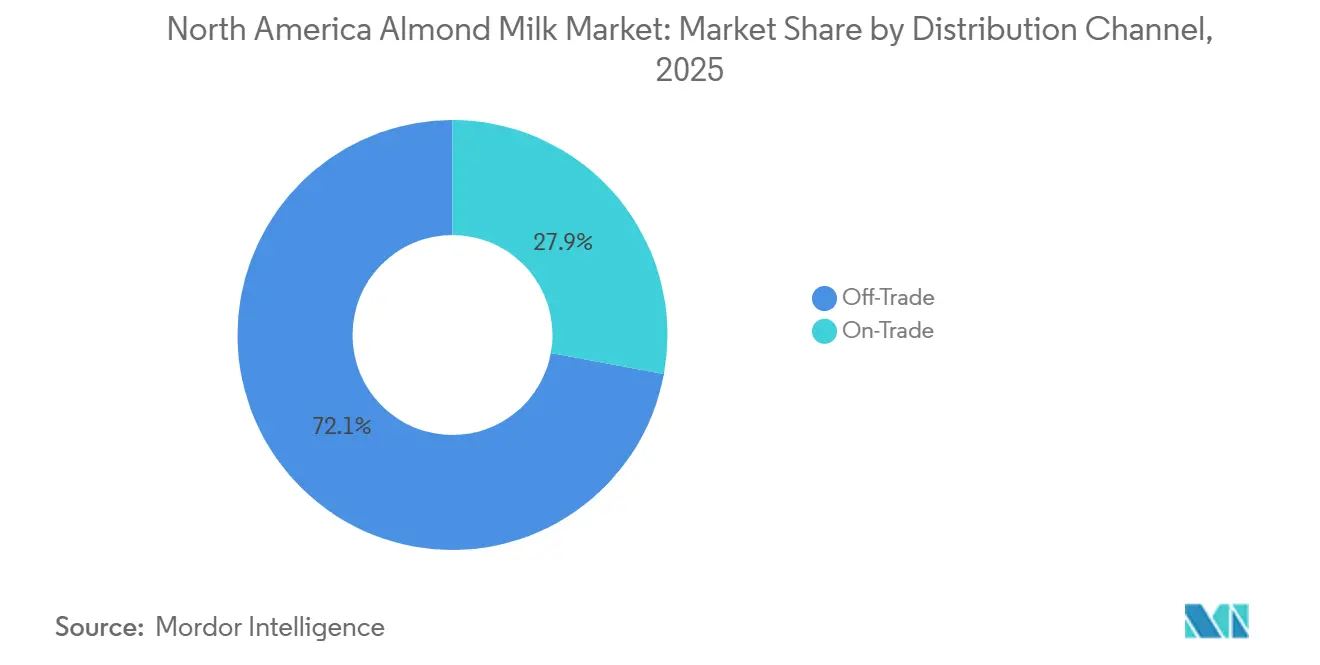

- By channel, off-trade accounted for 72.10% of the 2025 market share; on-trade is climbing at a 13.56% CAGR to 2031.

- By geography, the United States held 79.10% of 2025 revenue, while Canada is the fastest-growing market at a 13.24% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Almond Milk Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of lactose-intolerance and dairy allergies | +2.1% | United States, Canada, with higher incidence in Hispanic and Asian-American communities | Medium term (2-4 years) |

| Expanding vegan and flexitarian consumer base | +2.5% | United States urban centers, Canada metropolitan areas, emerging in Mexico | Long term (≥ 4 years) |

| Product innovation in flavors, fortification and barista blends | +1.8% | North America, with premium adoption in coastal United States markets and Toronto, Vancouver | Short term (≤ 2 years) |

| Food-service shift toward plant-based coffee creamers | +1.6% | United States, Canada, driven by coffee chains and quick-service restaurants | Medium term (2-4 years) |

| Retail private-label expansion enhancing price accessibility | +1.4% | United States mass-market retailers, Canada grocery chains | Short term (≤ 2 years) |

| Protein-fortified almond milks targeting sports-nutrition users | +1.2% | United States, Canada, concentrated in fitness-oriented demographics | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising prevalence of lactose intolerance and dairy allergies

The increasing prevalence of lactose intolerance and dairy allergies across North America is driving sustained demand for almond milk, particularly among ethnically diverse demographics and children with diagnosed sensitivities. This health-driven trend is further supported by updated regulatory frameworks in the United States and Canada, which mandate clearer nutrient equivalency and fortification standards for plant-based beverages. These regulations are prompting manufacturers to enhance the calcium, vitamin D, and protein content of their products. As a result, brands are repositioning almond milk from a basic dairy substitute to a functional wellness beverage, exemplified by protein-enriched innovations from companies such as Califia Farms. The category is expanding its reach beyond medically driven consumption to include health-conscious households seeking clean-label, fortified, and proactively healthy alternatives. Additionally, increasing awareness of digestive health, clean eating, and plant-based diets is bolstering almond milk’s appeal among flexitarian and wellness-focused consumers. Pediatric recommendations, fitness trends, and the growing demand for minimally processed ingredients are collectively reinforcing almond milk’s position as a mainstream, lifestyle-oriented dairy alternative, moving it beyond its niche status.

Expanding vegan and flexitarian consumer base

The North American almond milk market is experiencing significant growth, driven by the expanding vegan and flexitarian consumer base. A growing segment of consumers is actively reducing dairy consumption without fully eliminating animal products. This shift is primarily motivated by health optimization, protein diversification, and a preference for natural, plant-based products rather than strict adherence to veganism. Health remains the key driver for plant-based milk purchases, followed by demand for higher protein content and avoidance of highly processed products. These factors position almond milk as a clean-label, lifestyle-oriented alternative. Manufacturers are responding to this demand by reformulating products to balance fortification with minimal ingredients. For instance, Danone’s Silk brand offers organic and fortified almond milk with alternative calcium sources to meet both nutritional and clean-label expectations. Growth opportunities are particularly strong among younger, urban consumers in the United States and Canada, where the adoption of plant-based products is outpacing the overall growth of the food category, creating substantial potential for increased almond milk market penetration.

Product innovation in flavors, fortification, and barista blends

In North America, product innovation in flavors, fortification, and barista-grade formulations is driving growth in the almond milk market. These advancements are expanding consumption occasions and enhancing competitiveness against other plant-based alternatives. Improvements in foam stability and heat resistance have strengthened almond milk’s adoption in food-service and specialty coffee chains, with companies such as Blue Diamond optimizing their Barista Blend offerings. Flavor innovation has progressed beyond traditional vanilla and chocolate to include café-inspired and indulgent variants, targeting snacking and ready-to-drink segments, thereby increasing usage beyond breakfast. Additionally, evolving regulatory guidance on voluntary nutrient comparisons with dairy is accelerating fortification strategies, reinforcing almond milk’s positioning as a functional and nutritionally competitive product within the broader plant-based beverage market.

Protein-fortified almond milks targeting sports-nutrition users

In North America, the almond milk market is witnessing a surge, driven by a growing consumer preference for protein-fortified variants. As health and fitness take center stage, consumers are gravitating towards plant-based beverages that align with their active lifestyles. For instance, according to the Health and Fitness Association, in 2024, 77 million Americans were engaged with fitness facilities[3]Source: Health & Fitness Association "US Health & Fitness Consumer Report", healthandfitness.org. Traditionally, almond milk has been perceived as having lower protein content compared to dairy and soy alternatives. To address this gap, manufacturers are enhancing formulations with plant-based proteins to strengthen nutritional value and position almond milk as a viable option for post-workout recovery and on-the-go consumption. Leading brands such as Silk have introduced protein-enriched almond milk, while Blue Diamond’s Almond Breeze Protein line offers higher protein content without compromising on taste or texture. This fortification strategy enables almond milk to compete more effectively in the sports-nutrition and performance beverage market, supporting premiumization and attracting health-conscious consumers seeking dairy-free protein solutions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Intensifying competition from oat, soy and pea milks | -1.8% | North America, with oat milk gaining share in United States urban markets and Canada | Short term (≤ 2 years) |

| Premium price gap versus dairy milk | -1.5% | United States mass-market, Mexico price-sensitive segments, rural Canada | Medium term (2-4 years) |

| Water-footprint backlash against California almond farming | -0.9% | United States West Coast, environmentally conscious consumer segments | Long term (≥ 4 years) |

| Yield volatility and supply-chain risk in United States almond crop | -1.2% | North America, with acute impact during California drought cycles | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Intensifying competition from oat, soy, and pea milks

The North American almond milk market is encountering heightened competition from oat, soy, and pea milks, each leveraging unique advantages that challenge almond milk's market position. Oat milk has gained a competitive edge with its superior texturing properties, highly favored by baristas, and a sustainability narrative that strongly appeals to environmentally conscious consumers. While soy milk's popularity has plateaued, it continues to attract fitness-focused consumers due to its higher protein content. Pea milk, meanwhile, emphasizes allergen-free formulations, although it faces ongoing challenges with consumer taste acceptance. This competitive landscape is driving shifts in consumer preferences, with oat milk's premium positioning and the expansion of private-label offerings eroding almond milk's market share. In response, almond milk brands are focusing on barista-grade formulations and blended product variants to maintain their competitive position. However, the rapid pace of innovation and increasing market fragmentation are exerting pressure on mid-tier players with limited research and development capabilities, further constraining overall market growth.

Water-footprint backlash against California almond farming

The North American almond milk market is encountering reputational and operational challenges due to increasing scrutiny over the water footprint of California's almond farming practices. With the majority of orchards located in drought-prone regions, stakeholders argue that almond cultivation imposes unsustainable pressure on aquifers, particularly during prolonged dry periods. Although micro-irrigation advancements have improved water efficiency per unit, the expansion of acreage has sustained high overall water demand, drawing criticism from environmental advocates. Recent droughts have exacerbated these concerns, leading to production declines and raising questions about the long-term cost competitiveness of almond milk compared to alternatives such as oat and soy milk, which emphasize water efficiency in their value propositions. However, California’s dominant role in the global almond supply chain limits diversification opportunities, compelling producers to balance environmental accountability with the need to maintain market share against competitors leveraging sustainability-focused narratives more effectively.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Sweetened Variants Gain as Health Halo Fades

In 2025, unsweetened almond milk accounted for 47.05% of the market, driven by early adopters seeking low-calorie, low-sugar options aligned with ketogenic and paleo diets. However, the sweetened almond milk segment is projected to grow at a 12.66% CAGR through 2031, as mainstream consumers increasingly prioritize taste. To address this demand, brands are incorporating functional sweeteners such as monk fruit, stevia, and allulose, enabling indulgence without causing glucose spikes. Blue Diamond launched its Almond and Oat Blend in January 2024, strategically positioning it within the "better-for-you indulgence" market by offering 4 grams of sugar per cup. In food-service channels, sweetened almond milk is gaining traction as baristas report that unsweetened variants can impart chalky or bitter notes in espresso beverages. Coffee chains are responding by stocking lightly sweetened options that enhance coffee flavor profiles.

Unsweetened almond milk continues to dominate in health-food stores, retail outlets, and among fitness-focused consumers who closely monitor macronutrient intake. Brands such as MALK Organics and Elmhurst 1925 emphasize minimal-ingredient, unsweetened formulations to appeal to consumers prioritizing clean labels and organic certifications. PLANTSTRONG entered the market in February 2024, launching an Unsweetened Almond SKU free from gums or oils across 500 Whole Foods stores. The unsweetened segment benefits from growing consumer awareness of the health risks associated with added sugars. To address perceptions of nutritional inferiority compared to dairy, manufacturers are fortifying unsweetened variants with calcium, vitamin D, and vitamin B12, aligning their offerings with dairy's nutritional profile.

By Packaging Type: Glass Bottles Signal Premium Positioning

In 2025, carton packaging accounted for a 37.12% market share, driven by aseptic technology that enhances shelf life and meets the convenience demands of mainstream consumers. However, glass bottles are experiencing significant growth, with a projected CAGR of 13.35% through 2031. Companies are leveraging glass packaging to emphasize sustainability, artisanal quality, and premium positioning. For example, Mooala Organic's offerings highlight authenticity and appeal to environmentally conscious consumers. Plastic bottles continue to play a role, particularly in private-label segments, though the shift toward recycled materials reflects increasing environmental, social, and governance (ESG) commitments. Additionally, niche formats such as pouches and bag-in-boxes are gaining traction in food-service channels, offering solutions for bulk dispensing and reducing packaging waste.

Packaging is increasingly being utilized as a strategic tool to communicate brand positioning: glass represents premium offerings, carton targets mainstream consumers, and plastic caters to value-driven segments. Innovations like resealable caps in cartons address consumer concerns about freshness. At the same time, logistical challenges and regulatory developments, such as state-level extended producer responsibility laws, are influencing production and distribution strategies. This evolving hierarchy is shaping the market landscape, driving line extensions and product launches across various price tiers.

By Flavor: Matcha and Chai Drive Premiumization

In 2025, unflavored almond milk held a commanding 67.05% share of the North American market. Its adaptability in cooking, baking, and coffee applications, particularly within food-service channels that prioritize neutral taste profiles, has reinforced its market dominance. For example, Blue Diamond’s Barista Blend, an unflavored and unsweetened almond milk, is specifically designed for espresso-based beverages. Concurrently, flavored almond milk variants are gaining traction, with a projected CAGR of 12.07% through 2031. Brands are expanding into snacking and dessert categories, leveraging innovations such as vanilla, chai, matcha, caramel, and seasonal flavors to drive consumer trials and repeat purchases. However, chocolate-flavored almond milk, while targeting children, faces challenges in balancing taste appeal with health-conscious positioning due to its sugar content.

Flavor innovation is increasingly employed as a strategic differentiator in a competitive market. Ready-to-drink formats and alternative sweeteners, including monk fruit and stevia, are aligning indulgent offerings with clean-label consumer preferences. Despite the growth of flavored options, brands are carefully managing SKU proliferation to optimize operational efficiency and maintain marketing focus. The objective remains to ensure relevance across diverse consumption occasions while sustaining a streamlined product portfolio.

By Distribution Channel: On-Trade Rebounds as Surcharges Disappear

In 2025, off-trade channels accounted for 72.10% of almond milk sales, with supermarkets and hypermarkets driving mainstream distribution. Online retail emerged as the fastest-growing sub-channel, supported by subscription models and direct-to-consumer strategies. Convenience and specialty stores maintained a strategic role, focusing on grab-and-go formats and premium or organic product positioning. Private-label initiatives from major retailers, such as Walmart’s Bettergoods line and Costco’s Kirkland Signature almond milk, intensified market competition by offering cost-effective alternatives, exerting pressure on mid-tier brands lacking comparable economies of scale.

The on-trade sector is projected to grow at a 13.56% CAGR through 2031. Coffee chains and quick-service restaurants are driving this growth by eliminating non-dairy surcharges and reformulating menus, thereby increasing almond milk adoption in espresso-based and customized beverages. Brands are capitalizing on evolving consumer preferences for plant-based options and their willingness to pay for premium experiences, with urban independent coffee shops reporting notable demand growth. While supermarkets continue to hold the largest market share, growth is increasingly concentrated in channels that enable premium positioning, differentiation, and direct consumer engagement, reshaping the distribution landscape.

Geography Analysis

In 2025, the United States captured 79.10% of regional revenue, driven by extensive distribution networks, high rates of lactose intolerance, and early adoption of plant-based diets. However, market penetration remains uneven, with urban coastal regions demonstrating strong adoption, while rural and Southern areas lag due to income disparities, educational gaps, and cultural preferences. California plays a dual role as a key production hub and a major consumption market, enhancing supply-chain efficiencies. Nevertheless, climate-related risks, such as droughts, expose the region to environmental vulnerabilities.

Canada is projected to achieve a 13.24% CAGR through 2031, supported by regulatory clarity and urban demographics that are accelerating almond milk adoption. Health Canada’s updated standards, which promote nutrient-comparison labeling and fortification to dairy-equivalent levels, favor established brands capable of reformulating their products. Urban centers like Toronto, Vancouver, and Montreal are driving growth, fueled by younger, health-conscious consumers. Additionally, provincial subsidies and federal dietary guidelines create a more favorable growth environment compared to certain United States regions.

Mexico and other North American markets, while smaller, hold strategic importance. Mexico’s high lactose-intolerance rates drive demand; however, limited income levels and dairy subsidies restrict almond milk’s reach to affluent urban areas such as Mexico City, Monterrey, and Guadalajara. Food certification regulations under NOM-251-SSA1-2009 increase compliance costs for imported almond milk, creating a price disadvantage. In the broader North American region, including the Caribbean and Central America, demand is emerging due to tourism, expatriates, and the growth of the urban middle class. However, weak distribution networks and cold-chain limitations hinder market expansion. To address these challenges, brands are testing shelf-stable formats to bypass refrigeration requirements. SunOpta’s aseptic carton production is well-positioned to capitalize on this opportunity.

Competitive Landscape

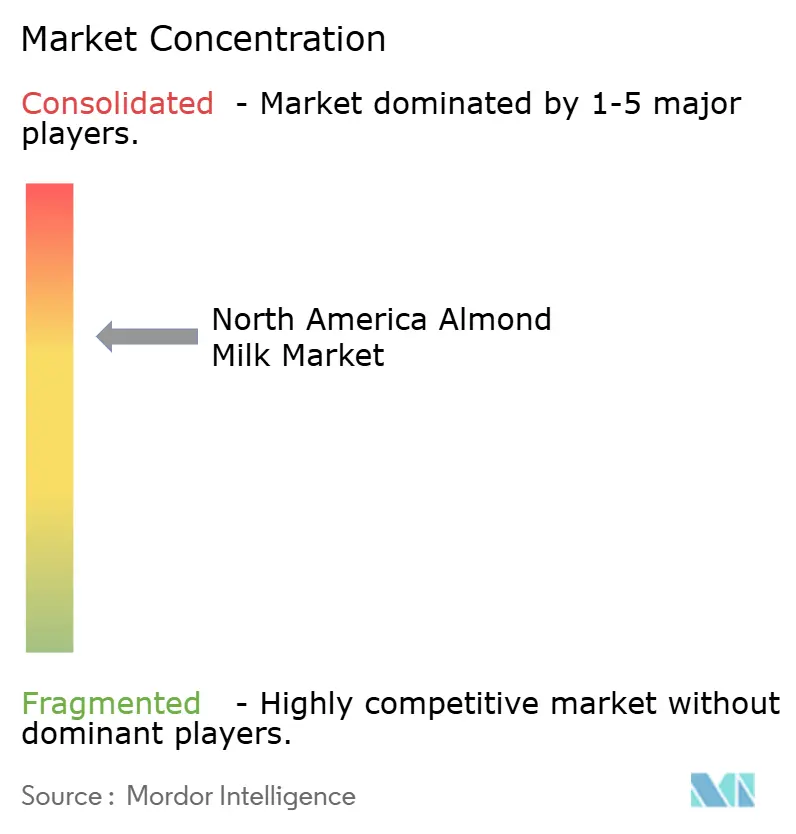

The North American almond milk market is moderately concentrated, with Blue Diamond Growers, Danone (Silk, Alpro), and Califia Farms holding a significant share of supermarket shelf space. However, private-label offerings from major retailers like Costco and Walmart are exerting pressure on margins. Leading brands are prioritizing barista-grade formulations, protein fortification, and hybrid blends to address functional gaps and align with consumer expectations. They are also exploring growth opportunities in sports nutrition channels and bulk formats for the food-service sector. Emerging disruptors are differentiating themselves by leveraging sustainability narratives, utilizing glass packaging, and adopting direct-to-consumer subscription models to stand out from mainstream competitors.

Technological advancements and formulation capabilities are increasingly influencing competitive dynamics. Key players are investing in advanced processing technologies, such as micro-encapsulation for nutrient stability and high-pressure processing to extend shelf life. These innovations enable clean-label fortification, which mid-tier brands find difficult to replicate. For example, Danone’s organic Silk line demonstrates this advantage by maintaining calcium fortification without the use of gums or oils, achieved through proprietary processes. This highlights the competitive edge provided by scale and in-house research and development capabilities.

Regulatory and market pressures are also shaping strategic positioning. The United States Food and Drug Administration (FDA) guidance on nutrient statements favors vertically integrated companies that can meet the criteria for “Healthy” claims. At the same time, the growing penetration of private-label products in the United States and Canada is compressing the pricing power of branded players. To counter this, brands are focusing on differentiation through functional claims, organic certifications, and premium packaging. These strategies support higher price points compared to store brands and emphasize the importance of innovation and operational sophistication to maintain competitiveness in the market.

North America Almond Milk Industry Leaders

-

Blue Diamond Growers

-

Califia Farms LLC

-

Danone SA

-

The Hain Celestial Group Inc.

-

SunOpta Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: MALK Organics, a United States-based brand specializing in milk alternatives, introduced its new shelf-stable product: Vanilla Almond. This plant-based milk features a straightforward ingredient list, comprising only four components: filtered water, organic almonds, vanilla extract derived from real vanilla beans, and Himalayan pink salt. This launch expands MALK Organics' existing shelf-stable product portfolio, which currently includes the Unsweetened Almond variant.

- July 2024: Califia Farms introduced Organic Vanilla Almondmilk. This United States Department of Agriculture (USDA) Certified Organic plant-based milk is formulated without the use of gums or oils. Designed to cater to diverse consumer needs, it is ideal for applications such as coffee, cereal, and cooking. Califia Farms' Organic Vanilla Almondmilk is produced using only water, organic almonds, pure vanilla extract, and a touch of sea salt.

- April 2024: HP Hood LLC announced a USD 83.5 million expansion at its Winchester, Virginia, facility, upgrading production and packaging equipment for Blue Diamond Almond Breeze and Planet Oat. The facility employs more than 600 people and manufactures extended-shelf-life fluid milk and non-dairy products. The investment underscores the capital intensity of co-manufacturing partnerships, which enable brands to scale capacity without greenfield construction, and reflects rising demand for plant-based milk in the Mid-Atlantic and Southeast regions.

North America Almond Milk Market Report Scope

Almond milk is a plant-based, dairy-free beverage made by blending almonds with water and straining out solids. It is naturally lactose-free, low in calories, and often fortified with vitamins and minerals. The North American almond milk market is segmented by product type, packaging type, flavor, distribution channel, and country. By product type, the market is segmented into sweetened and unsweetened. By packaging type, the market is segmented into carton, plastic bottle, glass bottle, and others. By flavor, the market is segmented into flavored and unflavored. By distribution channel, the market is segmented into on-trade and off-trade. By geography, the market is segmented into the United States, Canada, Mexico, and the rest of North America. The market forecasts are provided in terms of value (USD).

| Sweetened |

| Unsweetened |

| Carton |

| Plastic Bottle |

| Glass Bottle |

| Others |

| Flavored |

| Unflavored |

| On-Trade | |

| Off-Trade | Supermarket/Hypermarket |

| Convenience Store | |

| Specialist Stores | |

| Online Retail Store | |

| Other Distribution Channels |

| United States |

| Canada |

| Mexico |

| Rest of North America |

| Product Type | Sweetened | |

| Unsweetened | ||

| Packaging Type | Carton | |

| Plastic Bottle | ||

| Glass Bottle | ||

| Others | ||

| Flavor | Flavored | |

| Unflavored | ||

| Distribution Channel | On-Trade | |

| Off-Trade | Supermarket/Hypermarket | |

| Convenience Store | ||

| Specialist Stores | ||

| Online Retail Store | ||

| Other Distribution Channels | ||

| Geography | United States | |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

Market Definition

- Dairy Alternatives - Dairy alternatives are foods that are made from plant-based milk/oils instead of their usual animal products, such as cheese, butter, milk, ice cream, yogurt, etc. Plant-based or non-dairy milk alternative is the fast-growing segment in the newer food product development category of functional and specialty beverage across the globe.

- Non-Dairy Butter - Non dairy butter is a vegan butter alternative that is made from a mixture of plant oils. With an increase in alternative diets like vegetarianism, veganism, and gluten intolerance, plant butter is a healthy non-dairy substitute for normal butter.

- Non-Dairy Ice Cream - Plant based ice cream is a growing category. Non-dairy ice cream is a type of dessert made without any animal ingredients. This is typically considered a substitute for regular ice cream for those who cannot or do not eat animal or animal-derived products, including eggs, milk, cream, or honey.

- Plant-Based Milk - Plant based milks are milk substitutes that are made from nuts (e.g., hazelnuts, hemp seeds), seeds (e.g., sesame, walnuts, coconuts, cashews, almonds, rice, oats, etc.) or legumes (e.g., soy). Plant-based milk such as soy milk and almond milk have been popular in East Asia and the Middle East for centuries.

| Keyword | Definition |

|---|---|

| Cultured Butter | Cultured butter is prepared by having the raw butter go through chemical processing and has been added with certain emulsifiers and foreign ingredients. |

| Uncultured Butter | This type of butter is one which has not been processed in any way |

| Natural Cheese | The type of cheese in its most natural form. It is made from natural and simple products and ingredients, including fresh and natural salts, natural colors, enzymes, and high-quality milk. |

| Processed Cheese | Processed cheese undergoes the same processes as natural cheese; however, it requires more steps and many different forms of ingredients. Making processed cheese involves melting natural cheese, emulsifying it, and adding preservatives and other artificial ingredients or colorings. |

| Single Cream | Single cream contains around 18% fat. It’s a single layer of cream that appears over boiled milk. |

| Double Cream | Double cream contains 48% fat, more than double the amount of fat of single cream. It’s heavier and thicker than single cream |

| Whipping Cream | This has a much higher fat percentage than single cream (36%). Used to top cakes, pies, and puddings and as a thickener for sauces, soups, and fillings. |

| Frozen Desserts | Desserts that are meant to be eaten in frozen condition. E.g., sherbets, sorbets, frozen yogurts |

| UHT Milk (Ultra-high temperature milk) | Milk heated at a very high temperature. Ultra-high-temperature processing (UHT) of milk involves heating for 1–8 sec at 135–154°C. which kills the spore-forming pathogenic microorganism, resulting in a product with a shelf-life of several months. |

| Non-dairy butter/Plant-based butter | Butter made from plant-derived oil such as coconut, palm, etc. |

| Non-dairy Yogurt | Yogurt made from typically made from nuts, like almonds, cashews, coconuts, and even other foods like soybeans, plantains, oats, and peas |

| On-trade | It refers to restaurants, QSRs, and bars. |

| Off-trade | It refers to supermarkets, hypermarkets, on-line channels, etc. |

| Neufchatel cheese | One of the oldest kinds of cheese in France. It is a soft, slightly crumbly, mold-ripened, bloomy-rind cheese made in the Neufchâtel-en-Bray region of Normandy. |

| Flexitarian | It refers to a consumer preferring a semi-vegetarian diet, that is centered on plant foods with limited or occasional inclusion of meat. |

| Lactose Intolerance | Lactose intolerance is a reaction in digestive system to lactose, the sugar in milk. It causes uncomfortable symptoms in response to the consumption of dairy products. |

| Cream Cheese | Cream cheese is a soft and creamy fresh cheese with a tangy taste made from milk and cream. |

| Sorbets | Sorbet is a frozen dessert made using ice combined with fruit juice, fruit purée, or other ingredients, such as wine, liqueur, or honey. |

| Sherbet | Sherbet is a sweetened frozen dessert made with fruit and some sort of dairy product such as milk or cream. |

| Shelf stable | Foods that can be safely stored at room temperature, or "on the shelf," for at least one year and do not have to be cooked or refrigerated to eat safely. |

| DSD | Direct Store Delivery is the process in supply chain management wherein the product is delivered from manufacturing plant directly to the retailer. |

| OU Kosher | Orthodox Union Kosher is a kosher certification agency based in New York City. |

| Gelato | Gelato is a frozen creamy dessert made with milk, heavy cream and sugar. |

| Grass-fed Cows | Grass-fed cows are allowed to graze in pastures, where they eat a variety of grasses and clover. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period for each country.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms