Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

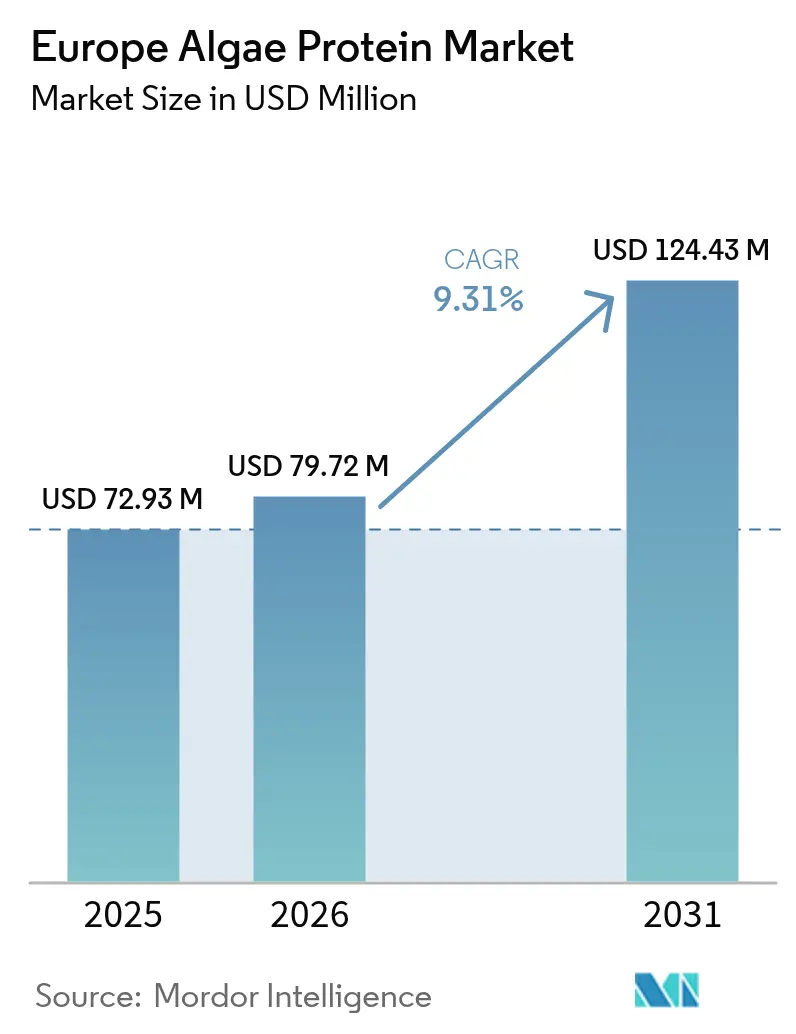

| Base Year Market Size (2025) | USD 72.93 Million |

| Market Size (2026) | USD 79.72 Million |

| Market Size (2031) | USD 124.43 Million |

| Growth Rate (2026 - 2031) | 9.31% CAGR |

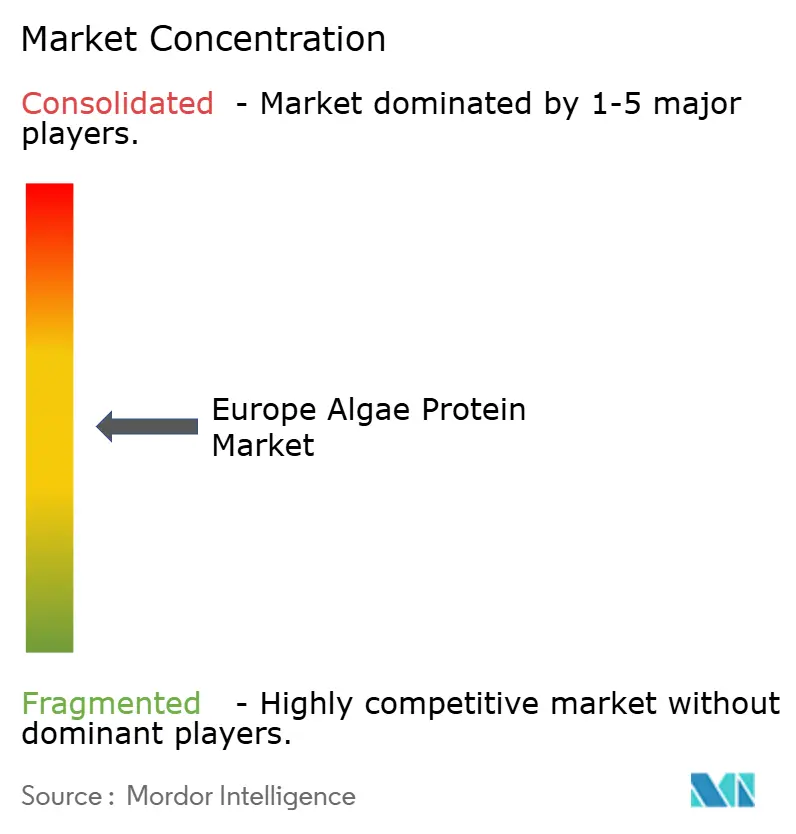

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Europe Algae Protein Market Analysis by Mordor Intelligence

The European algae protein market size in 2026 is estimated at USD 79.72 million, growing from 2025 value of USD 72.93 million with 2031 projections showing USD 124.43 million, growing at 9.31% CAGR over 2026-2031. In February 2024, the European Commission approved more than 20 algae species for food use, reducing commercial timelines and industry costs [1]Source: European Commission: Directorate-General for Maritime Affairs and Fisheries, "More Than 20 Algae Species Can Now Be Sold as Food or Food Supplements in the EU", oceans-and-fisheries.ec.europa.eu. This regulatory nod is propelling the adoption of algae protein across diverse sectors. Meanwhile, innovations in photobioreactor designs and cell-wall disruption methods are further driving down production expenses. As consumers increasingly gravitate towards low-carbon diets, demand for algae protein is surging, especially in bakery items, dairy alternatives, and meat substitutes. This trend is prompting manufacturers to integrate algae protein into a wide array of products, from foods and beverages to supplements and dairy alternatives. Germany, with its robust ingredient manufacturing base, leads regional sales, while Spain, benefiting from Mediterranean cultivation, showcases the most rapid growth.

Key Report Takeaways

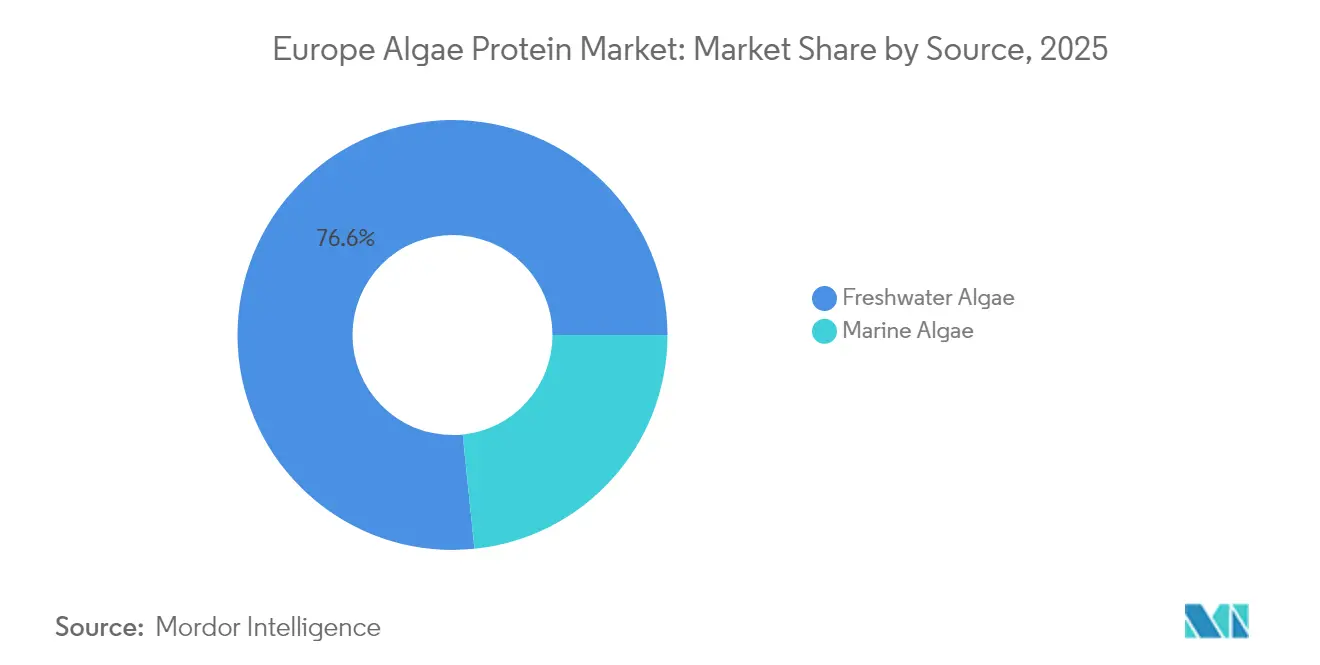

- By source, freshwater algae led with 76.63% of the European algae protein market share in 2025; marine algae is projected to grow at a 9.96% CAGR through 2031.

- By type, spirulina held 56.02% revenue share in 2025, while chlorella is expected to expand at a 10.08% CAGR by 2031.

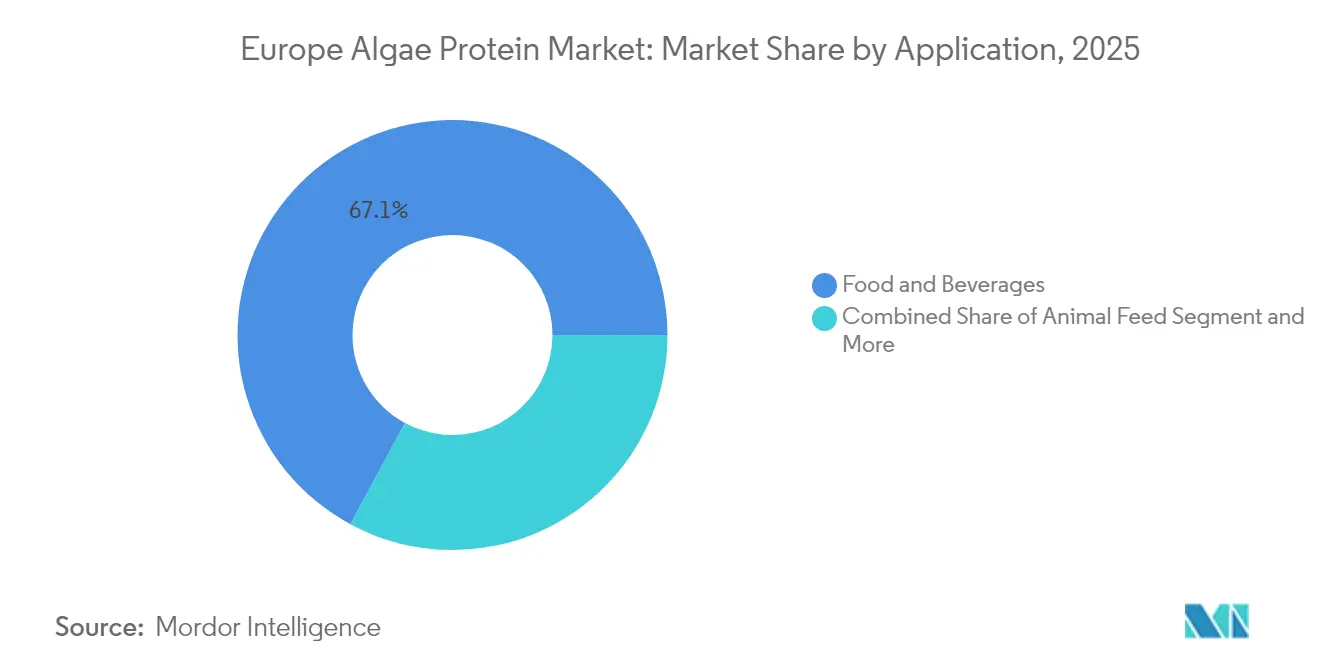

- By application, food and beverage accounted for 67.12% of the European algae protein market size in 2025 and is forecast to advance at a 10.28% CAGR.

- By geography, Germany commanded an 18.05% share of the European algae protein market size in 2025; Spain is set to register a 9.56% CAGR by 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe Algae Protein Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High demand for plant-based food and supplement | +2.1% | Germany, Netherlands, France | Medium term (2-4 years) |

| Technological advancements in algae cultivation | +1.8% | Netherlands, Denmark, Germany | Long term (≥ 4 years) |

| Expansion in functional foods and nutraceuticals | +1.5% | Germany, France, Spain | Medium term (2-4 years) |

| Rising adoption of sustainable proteins | +1.3% | European Union-wide, strongest in Nordic countries | Long term (≥ 4 years) |

| Regulatory approvals for novel food ingredients | +1.0% | European Union-wide regulatory harmonization | Short term (≤ 2 years) |

| Rise of vegan sports-nutrition powders | +0.8% | Germany, United KIngdom, Netherlands | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High demand for plant-based food and supplements

Europe's surging appetite for plant-based foods and supplements is propelling the algae protein market, with applications spanning various industries. As consumers pivot towards sustainable, allergen-free, and nutrient-dense substitutes for animal protein, algae, especially spirulina and chlorella, are emerging as favorites. These algae boast a rich profile, packed with protein, essential amino acids, vitamins, and antioxidants. This rising preference dovetails with Europe's overarching sustainability and climate objectives, given that algae demand significantly less land, water, and energy than conventional crops or livestock. Furthermore, a surge in investments in alternative protein sources across Europe bolsters this market's expansion. Highlighting this trend, the Good Food Institute reported investments in alternative proteins in Germany amounted to EUR 134 million in 2024 [2]Source: Good Food Institute, "European Alternative Protein 2024 Investment Figures Mark Return to Growth, but Show Need for Better Funding Options," gfieurope.org. Reflecting this burgeoning demand, the food and beverage sector is weaving algae protein into an array of products, from meat alternatives and protein bars to dairy-free yogurts, snacks, and beverages, tapping into the expanding vegan and flexitarian demographic.

Technological advancements in algae cultivation

The algae protein market is expanding through innovations in cultivation methods that focus on increasing yields, reducing production costs, and scaling operations. The implementation of closed-loop photobioreactor systems represents a significant technological advancement. These systems provide controlled environments that optimize light exposure, CO₂ levels, and nutrient distribution, resulting in higher biomass productivity compared to traditional open pond methods. The compact design of these systems enables efficient production for food, animal feed, and nutraceutical applications. In Germany, CellDEG GmbH's ultra-high-density thin-layer PBRs, with membrane-mediated CO₂ delivery, achieve impressive biomass concentrations over 30 g/L and daily productivity of around 10 g/L. Moreover, techniques in genetic engineering and strain selection have led to the cultivation of high-protein microalgae, such as Chlorella and Spirulina, boasting enhanced nutritional profiles and quicker growth. The rise of artificial intelligence (AI) and sensor-based monitoring further refines this process, enabling real-time adjustments for peak efficiency. Such advancements bolster the appeal of algae protein, making it a preferred choice over traditional proteins and paving the way for its broader acceptance in European food, aquafeed, and nutraceutical markets.

Expansion in functional foods and nutraceuticals

European consumers prioritize health, making them receptive to algae proteins, particularly those derived from Chlorella and Spirulina. These algae are packed with essential amino acids, antioxidants, omega-3 fatty acids, and bioactive compounds. As the demand for functional foods, known for their immune-boosting, anti-inflammatory, and detoxifying benefits, grows, these algae-based ingredients find their way into protein bars, smoothies, supplements, and fortified drinks. The market's expansion is further fueled by a surge in companies venturing into food supplement production. This momentum is bolstered by the European Union's regulatory endorsement of clean-label and novel foods, streamlining the introduction of algae-based products with health claims. Moreover, Europe's vegan and flexitarian movements, coupled with rising concerns over the environmental impact of animal protein, spotlight algae as a sustainable, low-carbon protein alternative.

Rising adoption of sustainable proteins

In Europe, the algae protein market is gaining momentum, driven by a collective push from consumers, manufacturers, and policymakers toward sustainable and eco-friendly alternatives to traditional proteins. Algae proteins stand out for their sustainability: they demand far less land, water, and energy than conventional crops or livestock. Moreover, advanced production systems, such as closed-loop photobioreactors, can harness waste CO₂ and reclaimed water, further minimizing their environmental footprint. With growing awareness of climate change and biodiversity concerns, European consumers are gravitating towards proteins that champion a low-carbon, circular economy, positioning algae as a prime contender. Highlighting this trend, a 2024 survey by the Food Standards Agency revealed that about 27% of respondents in England, Wales, and Northern Ireland expressed significant concern over sustainable food production [3]Source: Food Standards Agency, "Level of concern among consumers about food being produced sustainably in the United Kingdom", food.gov.uk. On the regulatory front, both governments and the EU are championing sustainable protein innovations. Initiatives like the Farm to Fork Strategy and the European Green Deal underscore the importance of alternative protein development and bolster funding for algae-centric research. This backing has catalyzed a surge in investments and product innovations, spanning from meat substitutes and dairy alternatives to functional food ingredients, all integrating algae protein for its sustainability and nutritional benefits.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sensory acceptance gap such as odor, flavor, and texture | -1.7% | European Wide-wide, particularly Northern Europe | Medium term (2-4 years) |

| High production costs | -1.4% | Germany, Netherlands, France | Long term (≥ 4 years) |

| Limited consumer awareness | -1.1% | Eastern Europe, Southern Europe | Short term (≤ 2 years) |

| Competition from more established plant protein sources | -0.9% | Germany, France, United Kingdom | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Sensory acceptance gap such as odor, flavor and texture

The sensory characteristics of algae protein present significant barriers to consumer acceptance, particularly its earthy, marine-like odor, bitter or grassy taste, and chalky or gritty texture. These attributes are particularly problematic in beverages, snacks, and dairy alternatives. European consumers generally prefer milder, neutral protein sources such as soy or pea, making the adoption of algae protein challenging in the functional food and sports nutrition markets, where taste and texture directly impact consumer repurchase decisions. European food technology companies are investing in solutions including deodorization technologies, microencapsulation, and blending techniques to address these sensory issues. However, these methods show variable results and increase production costs. Despite the technological advances, the persistent sensory issues continue to limit algae protein's integration into mainstream food products, affecting its growth in the European protein market.

High production costs

Algae offer sustainability and nutritional benefits, but converting them into protein-rich ingredients requires expensive technologies, including photobioreactors, controlled harvesting, and energy-intensive drying and extraction processes. These high costs result in more expensive algae protein compared to established plant proteins like soy or pea, limiting its market competitiveness. For instance, CellDEG employs high-density thin-layer photobioreactors, requiring significant capital investment in construction and maintenance. While their technology improves biomass yield, its complexity increases energy and operational costs, impacting overall production expenses. Additionally, strict quality control requirements, specialized infrastructure needs, and skilled workforce demands further increase costs. The financial impact is heightened by current production facilities' limited scale, preventing them from achieving the economies of scale that traditional protein producers benefit from. As a result, manufacturers transfer these costs to consumers, restricting algae protein primarily to premium and niche markets. Without technological advancements and improved scale efficiencies to reduce production costs, algae protein's high price point will continue to hinder its broader adoption in European markets.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Source: Freshwater species dominates while marine algae gains momentum

Freshwater species dominated the European algae protein market with 76.63% share in 2025, primarily through spirulina and chlorella cultivation. Marine microalgae, including Nannochloropsis, are growing at a 9.96% CAGR, driven by European Union authorization of edible seaweeds and increased demand for bioactive polysaccharides. In controlled freshwater environments such as ponds and photobioreactors, species like Spirulina and Chlorella thrive under carefully managed conditions, including nutrient levels, temperature, and light exposure. This controlled cultivation has established freshwater algae as a primary source for commercial protein products, supported by established supply chains and regulatory frameworks in Europe.

Marine algae, including seaweed and microalgae, are emerging as significant protein sources. Their nutritional composition features bioactive compounds like omega-3 fatty acids, antioxidants, and polysaccharides, making them valuable for functional foods and nutraceutical applications. Marine species cultivation in coastal or offshore locations offers scalability benefits and reduces freshwater usage, aligning with European environmental priorities. Advancements in farming and processing techniques are improving yields and product quality. These developments position marine algae to expand their market presence, complementing freshwater algae production and contributing to the growth of Europe's algae protein market.

By Type: Chlorella accelerates despite spirulina leadership

Spirulina held a 56.02% share of the European algae protein market in 2025, supported by its complete amino acid profile and prominence in sports nutrition products. Chlorella is experiencing faster growth, with a projected CAGR of 10.08%. Spirulina contains 65-70% protein concentration and includes essential amino acids, B-vitamins, and antioxidants such as phycocyanin. Its versatility in various food applications, including dietary supplements, smoothies, and energy bars, has strengthened its position in European health food products. Additionally, Spirulina's cultivation in controlled freshwater environments produces high biomass, making it more cost-effective and scalable compared to other algae varieties.

Chlorella is gaining prominence in Europe due to technological advancements in processing that address its limitations. With protein content comparable to Spirulina and higher chlorophyll levels, Chlorella is increasingly used in clean-label and vegan products for its detoxification and immune system benefits. For instance, Allmicroalgae – Natural Products S.A. produces premium Chlorella vulgaris strains in photobioreactors, achieving protein concentrations above 60%. Their processing techniques enhance digestibility and reduce the natural bitter taste, expanding their applications in food products and supplements.

By Application: Food and Beverage drives dual leadership

Food and beverage manufacturers dominated the European algae protein market with a 67.12% share in 2025, with growth projected at a CAGR of 10.28% through 2031. European consumers increasingly seek plant-based, high-protein, and clean-label products, making algae protein an attractive option due to its complete amino acid profile, natural origin, and reduced environmental footprint compared to animal and other plant proteins. In March 2025, the European Algae Biomass Association, through EU4Algae Fora, implemented a "Protocol to Apply for a Novel Food Dossier" to simplify the regulatory process for algae-based foods within the EU's Novel Food framework. This regulatory advancement has enhanced the integration of algae protein into functional foods, including protein bars, meal replacements, snacks, and dairy alternatives.

Furthermore, food manufacturers are harnessing advancements in flavor masking, encapsulation, and texturizing technologies. These innovations have addressed past challenges related to the taste and texture of algae protein, enhancing its appeal and versatility in processed and ready-to-eat items. With the European Union's backing on novel foods and the rising recognition of algae as a sustainable protein, requiring minimal land and water, its integration into food and beverage offerings is gaining momentum.

Geography Analysis

Germany held an 18.05% share of Europe's algae protein market in 2025, supported by its established ingredient supply chains and substantial public funding for alternative proteins. Spain, projected to grow at a 9.56% CAGR during 2026-2031, benefits from its outdoor pond systems with low energy requirements. Germany's research institutions and startups specializing in alternative proteins, particularly algae, receive support through government sustainability programs and EUropean Union funding for advancement in biotechnology, food innovation, and sustainable agriculture. In May 2025, six Fraunhofer Institutes (IME, IVV, IGB, and others) launched 'FutureProteins', implementing specialized photobioreactor systems for continuous algae cultivation throughout the year. The initiative develops new food products, including burgers, milk alternatives, and seaweed beer, by combining algae with plant and fungal proteins while focusing on integrated production and processing.

The Netherlands has emerged as a pivotal scale-up hub. Here, modular photobioreactors, set up in repurposed greenhouse bays, facilitate year-round algae cultivation under controlled lighting. Additionally, Rotterdam's port logistics ensure swift distribution across Europe. Corbion's strategic equity investments further bolster the market position of smaller Dutch innovators.

Spain is emerging as a key player in Europe's algae protein market. The country's climate, particularly in coastal and southern regions, provides optimal conditions for large-scale algae cultivation. Spanish companies are increasing their algae farming operations across marine and freshwater species, supported by government and EU funding initiatives focused on circular bioeconomy and aquaculture development. In a significant development, Spanish biotech startup Microalgas Future established Europe's largest microalgae R&D and production facility in Navarra. The project, with initial funding of EUR 4 million and a planned total investment of EUR 30 million, will span 50,000 m². The facility aims to produce 60 t/year of spirulina, along with haematococcus and Schizochytrium biomass for food, cosmetics, and omega-3 markets. This facility demonstrates Spain's growing influence in the algae protein industry. The country's position is further strengthened by increasing algae incorporation in Mediterranean diets, expanding export-focused production, and growing investments in food technology.

Competitive Landscape

The European algae protein market structure is moderately fragmented, providing opportunities for new entrants. Companies like Corbion and Roquette have adopted vertical integration strategies, controlling operations from photobioreactors to downstream texturizing processes. This integration encompasses cultivation, harvesting, extraction, and protein isolation steps. This strategy allows these companies to maintain quality control across the supply chain. Additionally, it helps them achieve cost efficiencies and strengthen their competitive position in the market.

Companies are forming strategic partnerships to increase production capacity and enhance market presence. These collaborations often involve sharing technological expertise, research facilities, and distribution networks. MicroHarvest's continuous-harvest system at its Hamburg demonstration plant, which processes 10 tons daily, demonstrates the focus on operational efficiency and cost reduction. The system incorporates advanced monitoring systems, automated harvesting mechanisms, and quality control protocols to maintain consistent production standards.

Research and development efforts concentrate on improving product quality and reducing production costs. The increase in patents for vortex photobioreactors, enzymatic dechlorophyllization, and high-pressure homogenization indicates the industry's efforts to commercialize algae protein production. These technological advancements aim to address challenges in protein extraction efficiency, taste profile enhancement, and scalability of production processes. Companies are also investing in developing specialized strains of microalgae with higher protein content and improved nutritional profiles.

Europe Algae Protein Industry Leaders

-

Corbion Biotech, Inc.

-

Roquette Klotze GmbH & Co. KG

-

Phycom BV

-

Duplaco BV

-

Algama Foods

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: SimpliiGood, a subsidiary of AlgaeCore Technologies, Ltd., has commenced commercial production of a plant-based smoked salmon alternative using spirulina microalgae. The company launched its industrial manufacturing line for texturized fresh spirulina, marketed as Simplii Texture. This expansion enables the company to produce hundreds of tons of the ingredient annually.

- December 2024: Algenuity, a United Kingdom-based biotechnology company that develops algae-based ingredients, opened its European commercial headquarters in Rotterdam. The company established this location to expand its presence in Europe's biotech and food-tech markets. While maintaining its research and development facility in the United Kingdom, Algenuity's Rotterdam office will manage the manufacturing, sales, and distribution of its algae ingredients.

- August 2024: Spanish biotech startup Microalgas Future established Europe's largest microalgae R&D and production facility in Navarra. The project, with initial funding of EUR 4 million and a planned total investment of EUR 30 million, will span 50,000 m². The facility aims to produce 60 t/year of spirulina, along with haematococcus and Schizochytrium biomass for food, cosmetics, and omega-3 markets.

Europe Algae Protein Market Report Scope

Europe algae protein market is segmented by type into spirulina, chlorella, and other types. By application, the market is classified into food & beverages, dietary supplements, pharmaceuticals, and others. The market is also segmented on a country basis as the United Kingdom, France, Germany, Netherlands, Italy, and the rest of Europe.

By Source

| Freshwater Algae |

| Marine Algae |

By Type

| Spirulina |

| Chlorella |

| Others |

By Application

| Food and Beverages | Bakery |

| Dairy and Dairy Alternative Products | |

| Meat/Poultry/Seafood and Meat Alternative Products | |

| Sport/Performance Nutrition | |

| Elderly Nutrition and Medical Nutrition | |

| Animal Feed |

By Geography

| United Kingdom |

| Germany |

| France |

| Italy |

| Netherlands |

| Spain |

| Rest of Europe |

| By Source | Freshwater Algae | |

| Marine Algae | ||

| By Type | Spirulina | |

| Chlorella | ||

| Others | ||

| By Application | Food and Beverages | Bakery |

| Dairy and Dairy Alternative Products | ||

| Meat/Poultry/Seafood and Meat Alternative Products | ||

| Sport/Performance Nutrition | ||

| Elderly Nutrition and Medical Nutrition | ||

| Animal Feed | ||

| By Geography | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Netherlands | ||

| Spain | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the current size of the Europe algae protein market?

The market stands at USD 79.72 million in 2026 and is projected to hit USD 124.43 million by 2031.

Which country leads sales?

Germany leads with an 18.05% share, supported by robust food-processing capabilities and strong R&D infrastructure.

What segment grows the fastest?

Food and beverage applications grow the quickest at a 10.28% CAGR, reflecting wider use in meat substitutes, bakery and dairy-alternative products.

Why are marine algae gaining traction?

European Union regulatory clearance for seaweed species and their richer portfolio of bioactives such as fucoidan are driving a 9.96% CAGR for marine algae.

Page last updated on: