Europe Air Ambulance Services Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2019 - 2023 |

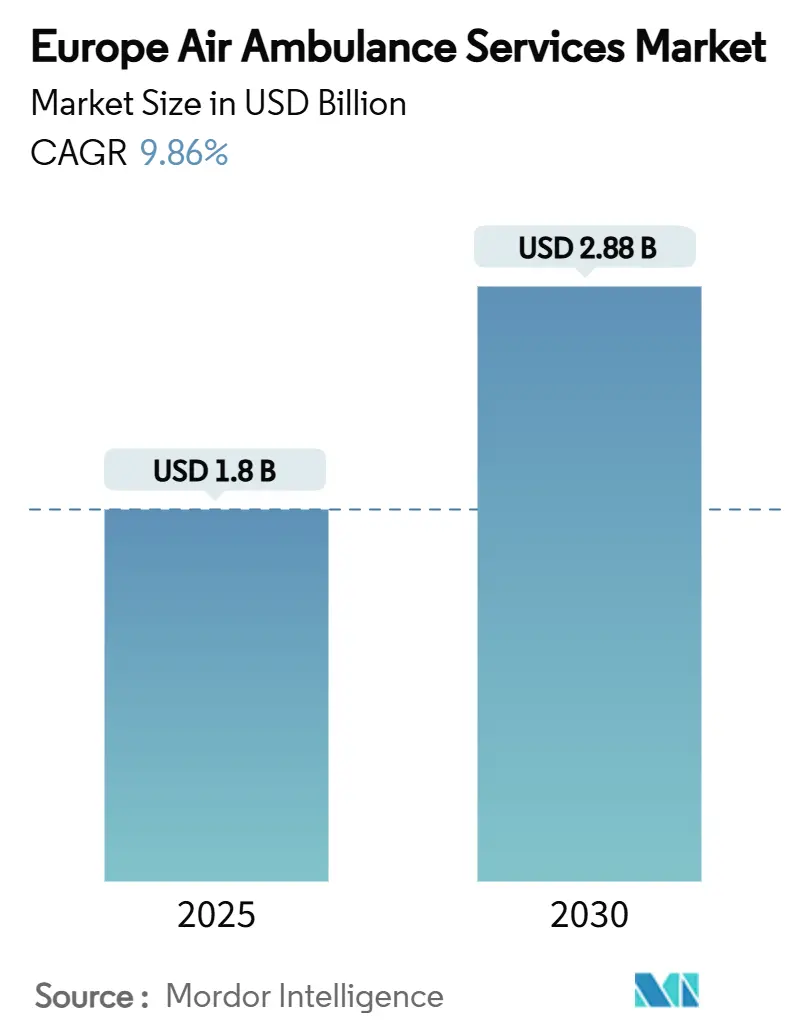

| Market Size (2025) | USD 1.8 Billion |

| Market Size (2030) | USD 2.88 Billion |

| Growth Rate (2025 - 2030) | 9.86% CAGR |

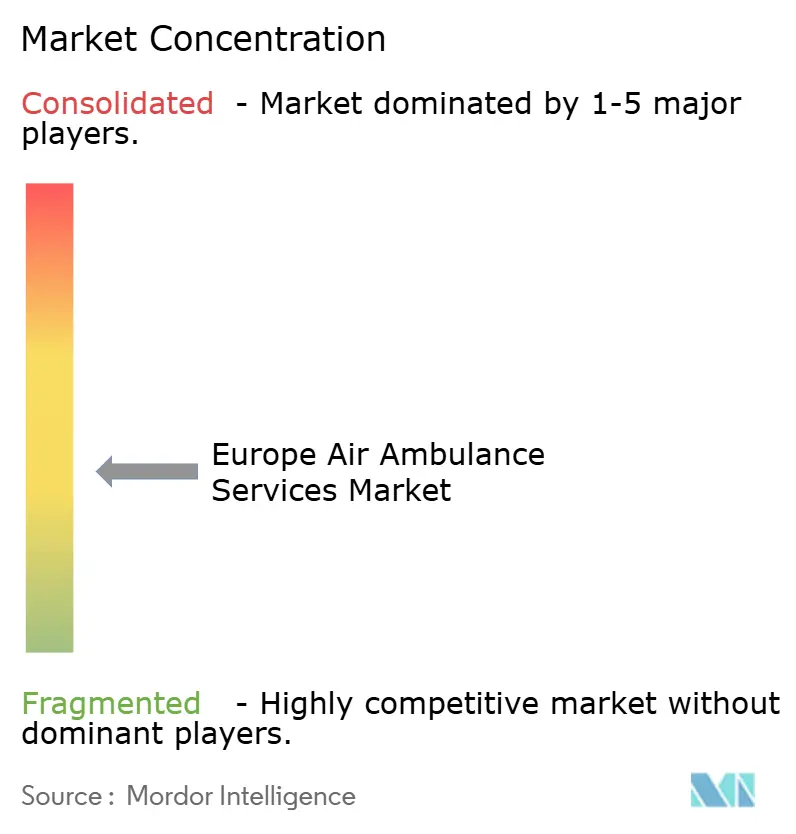

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Air Ambulance Services Market Analysis by Mordor Intelligence

The Europe air ambulance services market size stands at USD 1.8 billion in 2025 and is forecast to reach USD 2.88 billion by 2030, expanding at a 9.86% CAGR. Market momentum is anchored by the frailty of aging populations, steady escalation in cardiovascular and cerebrovascular events, and a wave of fleet modernization that includes eVTOL trials. A strong reimbursement environment in Switzerland, Germany, and the Netherlands continues to reduce payment risk. At the same time, France’s push to link offshore-wind installations with dedicated evacuation corridors creates fresh route density. Intensifying pilot shortages, higher rotorcraft upkeep, and noise-litigation risks in metropolitan zones temper the outlook but are unlikely to derail growth given the scale of unmet demand. Consolidation remains modest; leading incumbents are modernizing fleets and expanding pan-European partnerships rather than relying on outright mergers. The interplay between hospital-based, government, and independent models encourages operator specialization, protecting service quality, and promoting cross-border medical mobility.

Key Report Takeaways

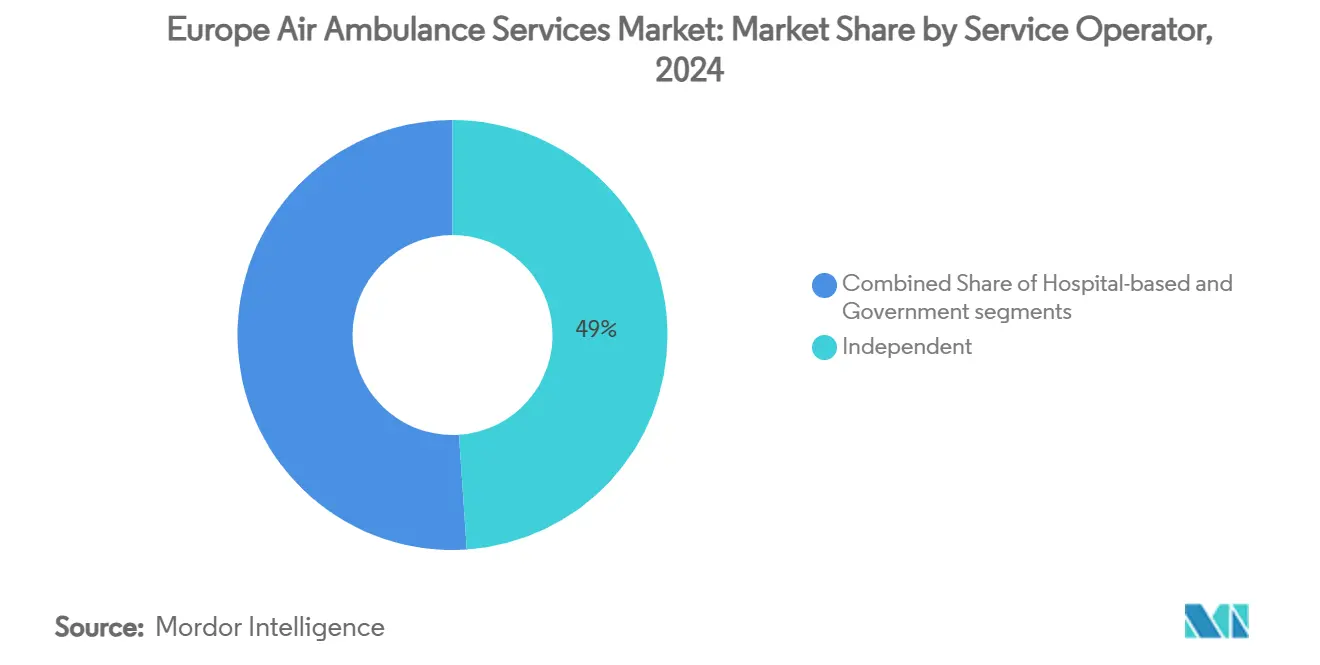

- By service operator, independent companies commanded 48.95% of the Europe air ambulance services market share in 2024; hospital-based units will be the quickest climbers with an 11.54% CAGR to 2030.

- By aircraft type, fixed-wing platforms controlled a 66.51% share of the Europe air ambulance services market in 2024; rotary-wing fleets are on course for a 10.4% CAGR through 2030.

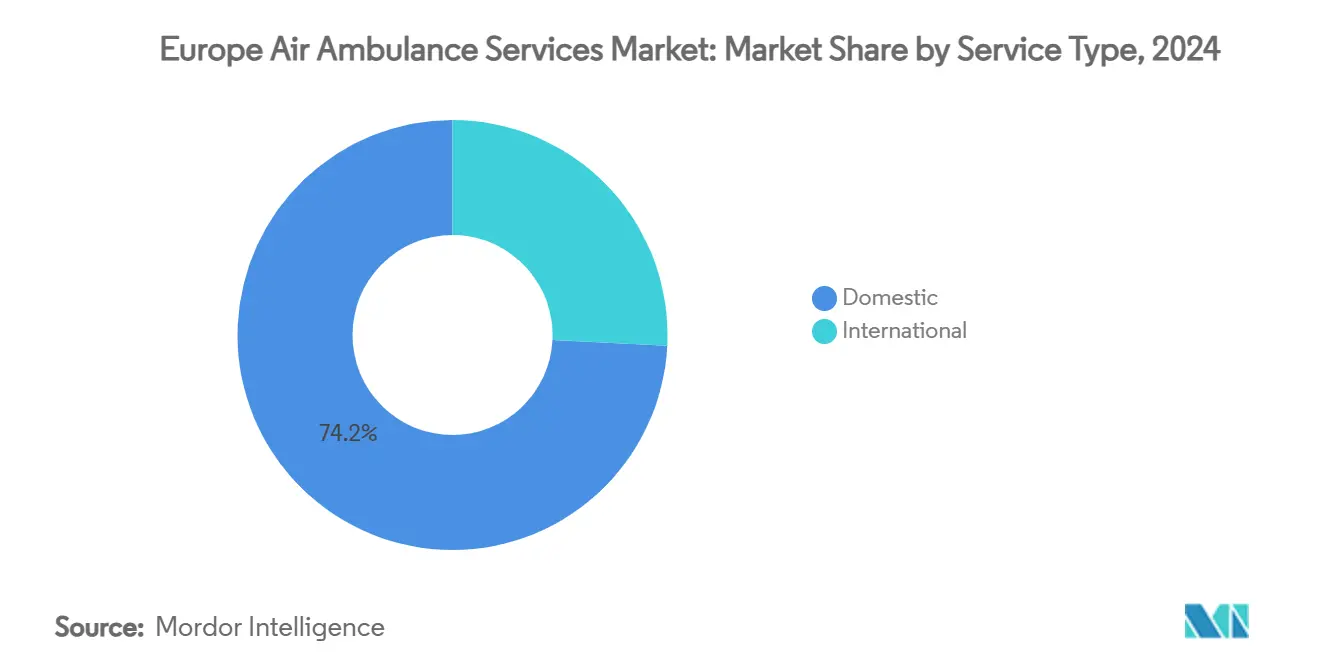

- By service type, domestic missions accounted for 74.21% of the Europe air ambulance services market size in 2024, whereas international flights are forecasted to grow at 9.89% CAGR during the same horizon.

- By geography, Switzerland held 40.26% of the Europe air ambulance services market share in 2024, while France is projected to compound at 12.45% CAGR from 2025 to 2030.

Worldwide, activity is shaped by contributions from multiple regions, with Europe representing one of the more structurally developed among them. The global report on air ambulance service market by Mordor Intelligence reflects how these regional layers combine into a single system.

Europe Air Ambulance Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising incidents of cardiovascular and cerebrovascular emergencies | +1.80% | Germany, France, UK | Long term (≥ 4 years) |

| Growing geriatric population requiring specialized medical transport | +2.10% | Western Europe | Long term (≥ 4 years) |

| Integration of helicopter EMS with national trauma networks | +1.20% | DACH, Nordics | Medium term (2-4 years) |

| Favorable reimbursement frameworks for HEMS in key EU nations | +1.50% | Switzerland, Germany, Netherlands, Austria | Short term (≤ 2 years) |

| Offshore-wind-farm expansion fuelling offshore medevac contracts | +0.90% | North Sea states | Medium term (2-4 years) |

| Emerging eVTOL medical fleets opening new capacity corridors | +0.70% | Urban EU hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Incidents of Cardiovascular and Cerebrovascular Emergencies

European emergency departments logged 304.5 visits per 1,000 inhabitants in 2024, and between 70% and 80% of admissions originated in those units.[1]European Society for Emergency Medicine, “European Emergency Medicine in Numbers,” eusem.org Elderly residents generated 42.6% of all call-outs, yet their response requirement of 223 per 1,000 inhabitants dwarfed the 76 per 1,000 rate among younger adults. Primary percutaneous coronary intervention coverage ranges from 5% to 92% across the region, making rapid air transfers to cardiac centers essential. Swiss data reveal that 87% of air missions fell into the “non-urgent but specialized” class, indicating latent demand for clinical capabilities inside the cabin. Three-quarters of European helicopter EMS providers already embed point-of-care ultrasound, yet two-thirds lag on standardized training, highlighting an upskilling gap.

Growing Geriatric Population Requiring Specialized Medical Transport

Europe’s median age now surpasses 44 years, and home-based emergencies among seniors require longer on-scene times that ground units cannot absorb without compromising coverage elsewhere. Nursing-home residents are twice as likely to generate physician-attended calls, pushing air crews to develop geriatric-specific protocols, including frailty scoring and fall-injury stabilization.[2]Journal of Clinical Medicine, “Epidemiology of Pre-Hospital EMS Treatment of Geriatric Patients,” jcm.ac German community paramedic audits indicate more than half of low-acuity elder cases still escalate to transport, illustrating the latent flight demand embedded in demographic trends. Operators investing in cabin layouts that accommodate bariatric stretchers and portable dialysis equipment gain a competitive edge. Policymakers, meanwhile, view air assets as a lever to maintain equitable access in rural regions where hospital consolidation is accelerating.

Integration of Helicopter EMS with National Trauma Networks

The European Governance Alliance in HEMS standardizes protocols and peer reviews, creating interchangeability among crews and fleets. Germany fields one of the densest rotorcraft grids worldwide through DRF Luftrettung and ADAC, enabling sub-12-minute dispatch in most regions. Norway estimates its base network covers 73.60% of incidents within 30 minutes, and GIS optimization studies indicate potential to lift coverage above 90% with minor relocations. Cross-border frameworks within the EU accelerate transfers without customs or immigration bottlenecks, expanding addressable demand for the Europe air ambulance services market.

Favourable Reimbursement Frameworks for HEMS

Switzerland reimburses nearly the full cost of air rescue, a factor that underpins its 40.26% market share. Germany’s tariffs vary two-and-a-half-fold by state, yet recent bundling reforms aim to narrow the gap and improve cost predictability. The United Kingdom illustrates an alternate path: charitable donations raise GBP 200 million (USD 260 million) annually to keep 40+ bases airborne, with Airbus supplying two-thirds of the fleet. Cross-border healthcare directives secure payment flows for international missions, encouraging operators to expand into high-acuity specialist transfers that command premium rates.

Restraints Impact Analysis*

| Restraint | ( ~ ) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High operating and maintenance costs of rotorcraft fleets | -1.40% | EU-wide | Short term (≤ 2 years) |

| Stringent aviation-safety compliance expenditures | -0.80% | EU-wide | Medium term (2-4 years) |

| Acute pilot shortage amplified by drone-logistics demand | -1.10% | Germany, UK, France, Nordics | Medium term (2-4 years) |

| Urban noise-pollution litigation curbing night-time flights | -0.60% | Major metros | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Operating and Maintenance Costs of Rotorcraft Fleets

Simulation studies from rural Germany reveal that per-hour costs fall only after missions exceed specific thresholds; below that, subsidies or philanthropy remain essential.[3]Health Economics Review, “Costing of Helicopter Emergency Services,” biomedcentral.com UK charities collectively spend GBP 200 million (USD 260 million) each year to keep their helicopter fleets mission-ready. Germany’s inter-state tariff divergence further complicates route planning, forcing operators to base higher-performance aircraft in regions where payment ceilings offset upkeep costs. Predictive maintenance tools and single-type fleets are emerging counter-measures, yet capital-intensive overhauls still limit entry for smaller providers.

Stringent Aviation-Safety Compliance Expenditures

DRF Luftrettung allocates notable budget lines to hoist-rescue symposiums and runs a purpose-built training academy, illustrating the relentless investment required for regulatory alignment. February 2025 EASA amendments add new competency syllabi and extend record-keeping duties, raising administrative overheads, especially for multi-country operators. While such frameworks enhance patient safety, they extend payback periods for new aircraft and deter prospective entrants lacking deep capital reserves.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Operator: Independent Operators Drive Market Leadership

Independent providers accounted for 48.95% of the European air ambulance services market in 2024, leveraging multi-payer contracting and cross-border flexibility. Hospital-based operators are forecast to log an 11.54% CAGR, outpacing the overall market size, as health systems internalize aviation to tighten care-continuity loops.

Independent firms such as SAF Aerogroup, now running 43 helicopters from 30 bases, illustrate how geographic clustering and lean governance deliver scale advantages.[4]FlightGlobal, “SAF Aerogroup Plans Growth Path,” flightglobal.com Government fleets remain vital in Nordic welfare states but face budget caps that confine fleet modernization, whereas hospital-linked units access donor capital earmarked for patient-outcome improvements.

By Aircraft Type: Rotary Momentum Builds

Fixed-wing assets held 66.51% of the Europe air ambulance services market share in 2024 by servicing repatriation corridors from the Middle East and Africa. Rotary-wing platforms, however, will record the segment-leading 10.4% CAGR through 2030, narrowing the gap within the Europe air ambulance services market as urbanization and offshore energy demand escalate.

DRF Luftrettung's February 2024 order for up to ten H145s underscores the turn toward versatile, low-noise helicopters.[5]Airbus, “DRF Luftrettung Orders Up to 10 Additional H145s,” airbus.com Airbus's H140 EMS variant and Leonardo's AW169 payload upgrade reinforce OEM focus on medical payloads and cabin re-configurability. Fixed-wing specialists counter by marketing long-range ICU modules and reduced door-to-door travel times for intercontinental transfers.

By Service Type: International Missions Gain Traction

Domestic flights represented 74.21% of activity in 2024, reflecting national trauma-network reliance. International missions will expand at a 9.89% CAGR as EU patient-mobility directives and medical-tourism corridors deepen, adding incremental value to the Europe air ambulance services market size.

Swiss Rega’s 305 repatriations spanning 34 countries show how legacy domestic operators monetise overseas demand. Cross-border tele-consults and multilingual dispatch platforms reduce coordination friction, positioning operators to capture elective oncology and transplant transports within Schengen.

Geography Analysis

Switzerland’s leadership stems from its Alpine topography, which renders ground evacuation impractical in many cantons. Its single-payer reimbursement ensures that every medically necessary flight is compensated, protecting operator margins. The country also fields Europe’s highest helicopter-per-capita ratio, allowing rapid dispatch even in adverse weather. Its standardised clinical governance protocols feed continuous quality loops that reinforce brand trust.

France, by contrast, is scaling quickly as the state modernises SAMU dispatch algorithms and funds offshore-wind SAR capacity from Normandy to Nouvelle-Aquitaine. The pre-hospital “scoop-and-treat” doctrine widens the scope for in-flight medical acts, pushing demand for twin-engine cabins equipped with ultrasound and blood warmers. Government co-financing lowers capital risk, enticing private entrants to regional concession tenders.

Germany remains Europe’s most complex reimbursement environment, with EMS tariffs ranging from EUR 660 (USD 729) in Berlin to EUR 1,530 (USD 1,690) in Schleswig-Holstein. Nevertheless, ADAC and DRF Luftrettung operate nearly 80 helicopters combined, ensuring 12-minute average response times nationwide. The UK balances reliance on charity fundraising with Ministry of Defence surplus aircraft grants, creating a hybrid ecosystem where public goodwill offsets fiscal constraints. Nordic states leverage sovereign wealth funds to run technically advanced AW139 and H145 fleets that can reach Arctic communities within the 60-minute trauma window.

Competitive Landscape

Europe’s provider matrix is moderately fragmented: the top five groups hold roughly 55% of combined flight hours, assigning a middle-tier concentration profile to the Europe air ambulance services market. Swiss Rega dominates its domestic turf yet seldom competes abroad, whereas DRF Luftrettung and ADAC pursue multi-state alliances to extend buying power on new-build helicopters. Babcock Scandinavian AirAmbulance leads the Nordic theatre, capitalising on cross-border contracts that bundle Sweden, Norway, and Finland into a contiguous service zone.

Strategic moves focus on fleet renewal and digital integration. DRF’s 2024 H145 order improves lift capacity by 150 kg per sortie, enabling ECMO missions previously assigned to military assets. SAF Aerogroup’s April 2025 private-equity buy-out earmarks expansion into Spain and Italy via base-acquisition deals. Leonardo’s 2025 Verticon event logged AW169 EMS orders from the UK’s Gama Aviation, reflecting operator appetite for single-type, multi-mission airframes.

Technology adoption is equally decisive. Frequentis secured a EUR 427.5 million (USD 501.5 million) ATC-comms upgrade that underpins seamless HEMS flight-following across Norway’s Avinor network. Operators embed ultrasound, NVGs, and predictive-maintenance analytics to improve uptime and patient outcomes, while eVTOL prototypes position early adopters for urban slot allocations once vertiports come online. Talent acquisition remains a gating factor, with companies offering sign-on bonuses and career-progression pathways to mitigate Europe-wide pilot shortages.

Europe Air Ambulance Services Industry Leaders

DRF Stiftung Luftrettung gemeinnützige AG

ADAC Luftrettung

Babcock Scandinavian AirAmbulance (SAA)

Swiss Air-Rescue Rega

Norwegian Air Ambulance Foundation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: During Verticon 2025 in Dallas, Gama Aviation and Leonardo bolstered their partnership, securing an order for five additional helicopters. These helicopters are designated for emergency medical service (EMS) and energy support operations in the UK.

- March 2025: ADAC Luftrettung and ÖAMTC Flugrettung, both German and Austrian helicopter emergency medical services operators, inked a deal with Airbus Helicopters to procure ten H140 helicopters, five of which will be distributed to each operator.

- June 2024: ADAC SE, the German automobile association, ordered a Bombardier Challenger 650 aircraft via its subsidiary, Aero-Dienst. Configured as a dedicated air ambulance, the aircraft will be delivered to Aero-Dienst, ADAC's primary aircraft operator, in 2026.

- May 2024: Midlands Air Ambulance Charity (MAAC) awarded Babcock a new contract, bolstering the charity's pre-hospital emergency care flight operations with added long-term resilience.

Europe Air Ambulance Services Market Report Scope

| Hospital-based |

| Independent |

| Government |

| Fixed-Wing |

| Rotary-Wing |

| Domestic |

| International |

| United Kingdom |

| France |

| Germany |

| Switzerland |

| Sweden |

| Denmark |

| Norway |

| Rest of Europe |

| By Service Operator | Hospital-based |

| Independent | |

| Government | |

| By Aircraft Type | Fixed-Wing |

| Rotary-Wing | |

| By Service Type | Domestic |

| International | |

| By Geography | United Kingdom |

| France | |

| Germany | |

| Switzerland | |

| Sweden | |

| Denmark | |

| Norway | |

| Rest of Europe |

Key Questions Answered in the Report

How large is the Europe air ambulance services market in 2025?

The market stands at USD 1.8 billion in 2025 and is forecasted to grow to USD 2.88 billion by 2030 at a CAGR of 9.86%.

Which geography currently leads in market share?

Switzerland holds the lead with 40.26% share, driven by its Alpine terrain and robust reimbursement.

What aircraft type is growing fastest?

Rotary-wing services are expected to post a 10.4% CAGR between 2025-2030, the highest among platform categories.

Why are hospital-based operators expanding rapidly?

Health-system integration and the push for seamless trauma networks give hospital fleets an 11.54% projected CAGR.

How are offshore wind farms influencing demand?

New North Sea turbines require 24/7 med-evac coverage, generating specialised contracts for helicopter operators.

Will eVTOL aircraft impact future capacity?

Yes, EASA’s 2024 regulations pave the way for electric VTOL medical flights, promising quieter urban operations from 2027 onward.

Page last updated on: