Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2019 - 2024 |

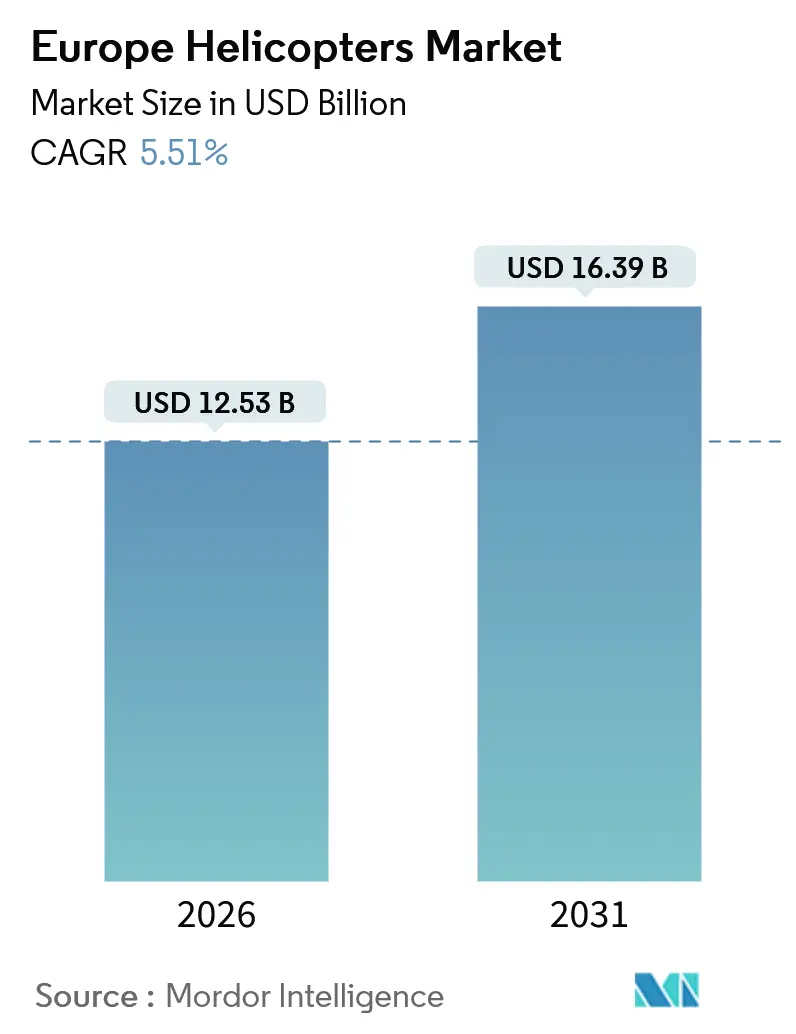

| Market Size (2026) | USD 12.53 Billion |

| Market Size (2031) | USD 16.39 Billion |

| Growth Rate (2026 - 2031) | 5.51% CAGR |

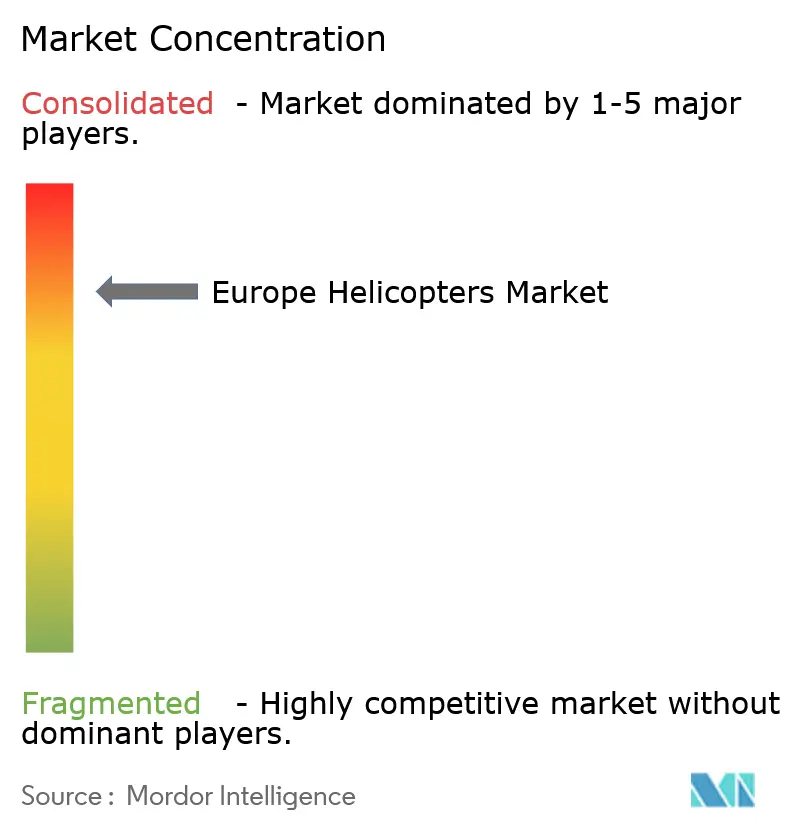

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Helicopters Market Analysis by Mordor Intelligence

The Europe helicopters market size stood at USD 12.53 billion in 2026 and is projected to reach USD 16.39 billion by 2031, advancing at a 5.51% CAGR. The European helicopters market's expansion reflects synchronized defense recapitalizations, rising offshore wind farm traffic, and scaled emergency medical services frameworks, all of which reinforce near-term demand even as operating cost headwinds persist. Medium-lift twin-turbine platforms dominate procurement because they satisfy EASA ditching rules and deliver the endurance required for North Sea shuttle networks. Civil and commercial activity is now showing the steepest ascent, partly because EU structural funds are accelerating air-ambulance awards in Central and Eastern Europe, and partly because coastal tourism in Italy and Spain has returned to pre-pandemic flight-hour volumes. Tier-one manufacturers are responding with lighter, quieter models and with power-train roadmaps that can ingest higher blends of sustainable aviation fuel, thereby aligning fleet economics with ReFuelEU Aviation mandates. Competitive dynamics remain intense, yet switching costs, shared training pipelines, and local industrial work-share agreements continue to favor incumbents offering common cockpits across multiple weight classes.

Key Report Takeaways

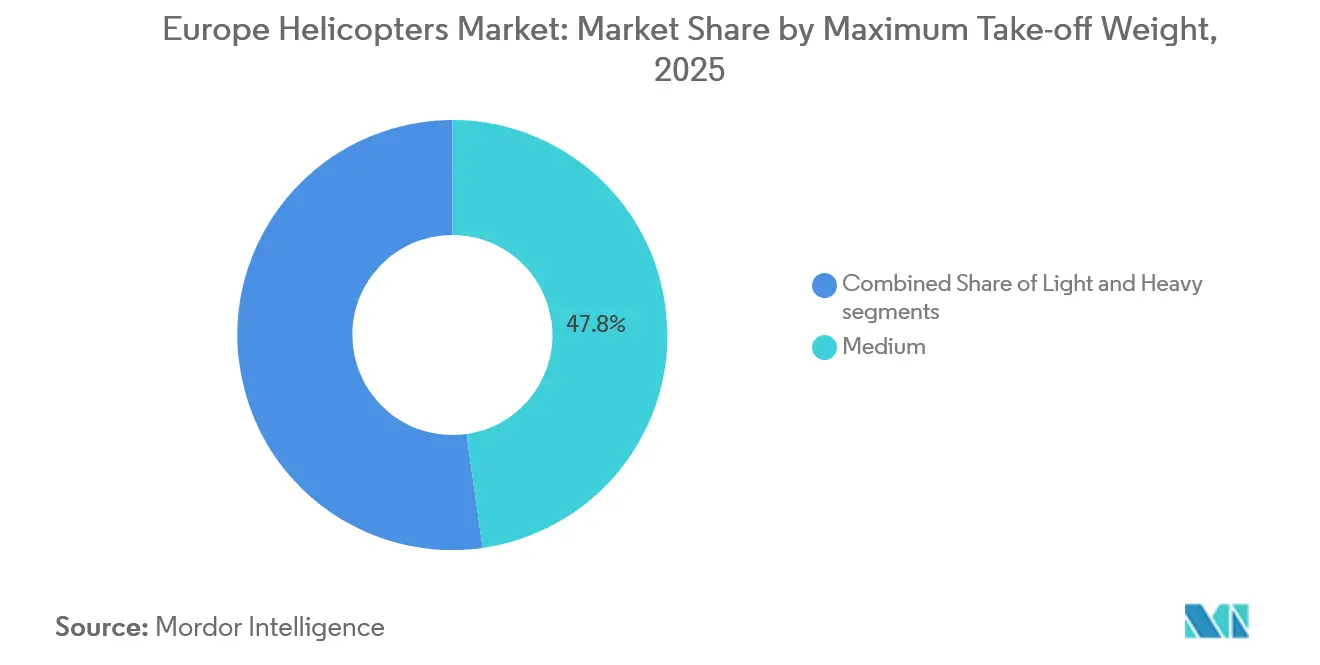

- By maximum take-off weight, medium helicopters led the European helicopter market with a 47.76% share in 2025, while the light category is advancing at a 6.89% CAGR toward 2031.

- By application, military utilization accounted for 60.77% of the European helicopter market size in 2025; civil and commercial demand is forecast to expand at a 7.32% CAGR through 2031.

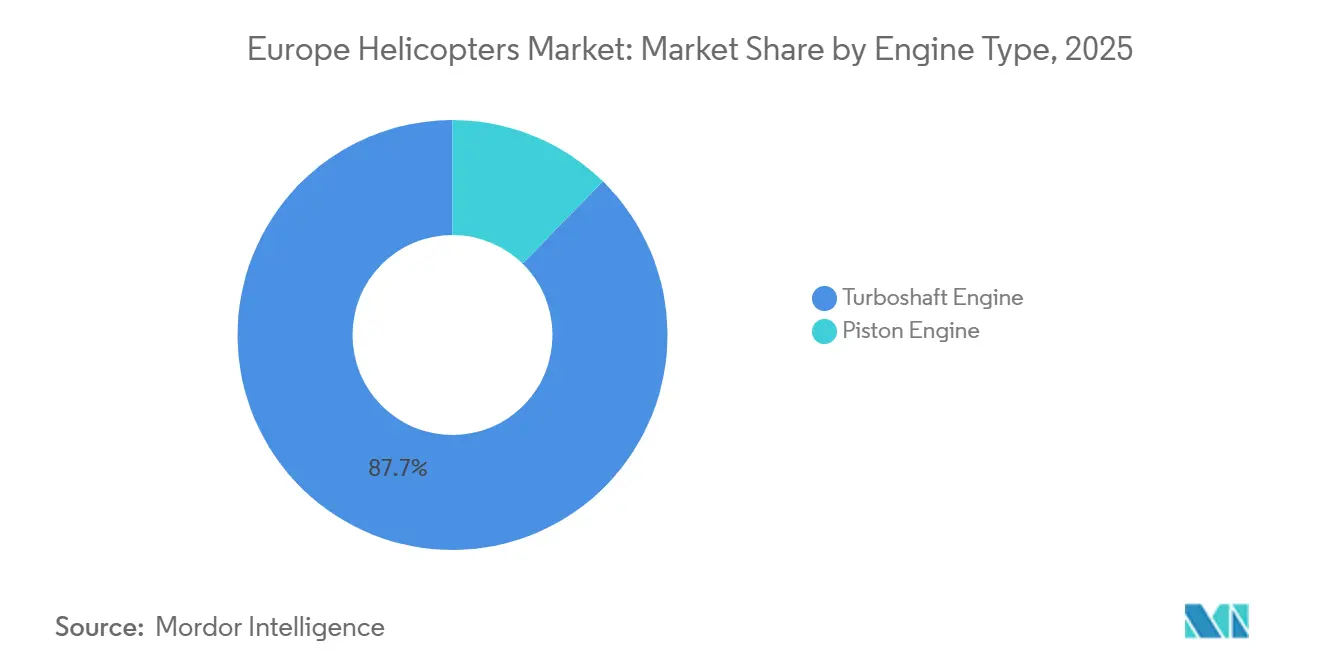

- By engine type, turboshaft platforms captured 87.67% of the European helicopter market share in 2025 and are projected to grow at a 6.43% CAGR through 2031.

- By end-use sector, intelligence, surveillance, and reconnaissance accounted for 28.38% of the European helicopter market size in 2025, while emergency medical services are expected to increase at a 7.19% CAGR between 2026 and 2031.

- By geography, the United Kingdom held 19.91% of Europe's helicopter market share in 2025, whereas Italy exhibited the fastest growth of 6.73% CAGR over the forecast horizon.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Helicopters Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fleet modernization to meet EU Stage 3/4 rules | +0.8% | Western Europe (UK, France, Germany, Netherlands) | Medium term (2-4 years) |

| Surge in HEMS contracts and EU-funded medevac | +1.2% | Central and Eastern Europe | Short term (≤ 2 years) |

| Offshore wind-farm build-out | +1.0% | North Sea littoral, Baltic Sea | Medium term (2-4 years) |

| Defense rotorcraft replacement cycles | +1.5% | France, Spain, UK, Germany | Long term (≥ 4 years) |

| Hybrid-electric rotorcraft R&D grants | +0.4% | EU-wide with concentration in France, Germany, Italy | Long term (≥ 4 years) |

| Border-security and SAR requirements | +0.6% | Poland, Baltic states, Romania | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fleet Modernization to Meet EU Stage 3/4 Noise and Emission Rules

EASA CS-36 noise standards and Stage 3/4 emission thresholds are accelerating the retirement of older rotorcraft in urban HEMS and offshore routes where community noise complaints intensify.[1]EASA, “CS-36 Noise Certification Standards,” easa.europa.eu ReFuelEU Aviation mandates a 2% sustainable aviation fuel blend from 2025, which increases to 6% by 2030 and 70% by 2050, resulting in fuel bills that are two to five times higher than those of Jet A-1. Operators therefore gravitate toward twin-engine types such as the H145 and H160, whose five-blade bearingless rotors and Fenestron tails reduce external noise by up to 50%. NHV validated the feasibility by flying 40% SAF blends on North Sea sectors during 2025, proving that energy clients absorb higher logistics tariffs to hit carbon targets. Germany embedded low-acoustic signatures in its 82-unit H145M order, underscoring how compliance is now a key consideration in request-for-proposal criteria, rather than being treated as retrofit work.

Surge in HEMS Contracts and EU-Funded Medevac Programs

Central and Eastern Europe utilized structural funds to bridge trauma-care gaps, where sparse road networks lengthen response times. Bulgaria signed a EUR 50.8 million (USD 59.26 million) nationwide air-ambulance package in 2024, which is expected to reach full service by mid-2026. The rescEU framework earmarked EUR 140 million (USD 163.32 million) for a pooled fleet serving Slovakia, Czechia, and Romania, an early example of asset sharing that trims life-cycle costs across borders. Commission Regulation 2023/1020 harmonized crew training and medical-equipment baselines, eliminating patchwork compliance hurdles and enlarging tender pools for private operators.

Offshore Wind-Farm Build-out in North Sea and Baltic Sea

More than 20 GW of offshore wind capacity entered construction or commissioning between 2024 and 2026, each requiring continuous helicopter lift for turbine assembly, maintenance, and crew transfers. RWE’s Thor wind farm achieved commercial operation in spring 2026 using dedicated shuttle flights that covered up to 120 km from shore. Ørsted awarded CHC Helicopter a multi-year contract under which H175 and AW139 aircraft support Hornsea 3, reinforcing demand for medium twins that satisfy EASA ditching rules.[2]Ørsted, “Hornsea 3 Helicopter Logistics Contract,” orsted.com Offshore energy, therefore, grows at a 6.1% CAGR even as operators face margin erosion from fixed-price logistics clauses and obligatory SAF adoption.

Defense Rotorcraft Replacement Cycles

France and Spain injected EUR 4 billion (USD 4.67 billion) into the Tiger MkIII mid-life upgrade covering 60 units, with first deliveries slated for 2029 and 2030. Germany diverted instead to 82 H145M light combat helicopters, of which the first entered training service in 2024. The United Kingdom will award its New Medium Helicopter contract in 2025 for 36-44 aircraft to replace Puma HC2 fleets. Combined, these programs increase the forecast CAGR by 1.5 percentage points and expand the industrial footprint at the Donauwörth, Yeovil, and Yeovilton assembly hubs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising operating costs from SAF mandates | -0.9% | EU-wide, most acute in offshore energy and HEMS | Short term (≤ 2 years) |

| Persistent pilot and technician shortage | -0.7% | Western Europe | Medium term (2-4 years) |

| Civil airspace congestion | -0.3% | Major urban centers | Medium term (2-4 years) |

| Export restrictions on Russian components | -0.5% | Eastern Europe with legacy Soviet fleets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising Operating Costs from SAF Blending Mandates

Sustainable aviation fuel prices ran two to five times higher than Jet A-1 during 2025. High-utilization offshore fleets consume thousands of liters per day, incurring annual cost increases of EUR 0.5-2 million (USD 0.58-2.33 million) per aircraft, which squeezes margins under fixed-price service contracts. HEMS operators cannot fully pass costs through to health ministry budgets, forcing route consolidation. While oil majors subsidized NHV’s 40% SAF flights in the North Sea, civil clients without carbon budgets resist similar premiums.

Persistent Pilot and Technician Shortage in Western Europe

EASA forecasts a need for 35,000 new European helicopter pilots by 2032; however, training programs cost EUR 100,000-150,000 (USD 116,656.50 to USD 174,984.75) and last up to two years. The retirement of seasoned captains is accelerating the gap; more than 40% of Europe’s existing pilot cohort is over 50 years old. Maintenance backlogs are lengthening as Part-145 shops report workforce deficits, which can ground aircraft for months and dilute fleet utilization. Germany included eight simulators within the H145M package to mitigate the instructor bottleneck, while the UK CAA streamlined military-to-civil license conversions; however, fewer than 200 transitions per year materialized.[3]UK Civil Aviation Authority, “Military-to-Civil Pilot Transition Programs,” caa.co.uk

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Maximum Take-Off Weight Light Helicopters Gain on Training and Tourism

Light helicopters captured training and leisure recovery tailwinds, expanding at a 6.89% CAGR through 2031. The medium class retained the single most significant slice of the European helicopters market share at 47.76% in 2025, anchored by defense lift and offshore contracts that value payload and twin-engine redundancy. The absolute European helicopter market size for light models is expected to expand as Mediterranean sightseeing operators refresh their fleets and schools add lower-cost aircraft to accelerate pilot throughput. Robinson’s R66 remains the best-selling turbine single in Spain and Italy due to acquisition pricing of EUR 900,000 (USD 1.04 million), while Leonardo’s AW09 targets the same niche but faces certification delays. Germany’s 3.7-tonne H145M blurs the light-medium lines by offering modular weapon kits, as illustrated by its adoption by special forces.

Demand for heavy rotorcraft remains tied to specialized North Sea platforms such as H225 and AW189. Growth lags at 4.2% CAGR, constrained by waning oil production and the pivot to fixed-wing crew change flights on ultra-long routes. Medium twins, especially the AW139 and H175, maintain outsized contract visibility because they can satisfy 300-nautical-mile round-trip operating envelopes and integrate 40% SAF blends without requiring hardware modifications.

By Application Civil and Commercial Surge Outpaces Military Baseline

Military programs controlled 60.77% of Europe's helicopter market share in 2025, as deliveries of the Tiger MkIII, H145M, and New Medium Helicopter reached their early run-rate. The civil and commercial sectors, however, are projected to post a 7.32% CAGR, surpassing defense growth after 2029. Emergency medical services, offshore energy, and tourism reopenings underpin the uplift. Offshore logistics dependence rises in tandem with wind farm capacity; contractual clauses now incorporate the use of SAF and carbon accounting. Tourism charter hours in Italy and Spain increased by 25% year-over-year in 2025, restoring pre-pandemic traffic levels amid the expansion of coastal helipads. Law enforcement frameworks in the UK, France, and Germany are shifting toward H145 and AW169 platforms, featuring sensor suites that integrate seamlessly with secure ground networks. Utility and aerial work operators are introducing unmanned systems for routine inspections, reserving manned sorties for complex lifts, thereby flattening demand curves in that sub-segment.

By Engine Type Turboshaft Dominance Reflects Safety and Regulation

Turboshaft powerplants commanded 87.67% of the European helicopter market share in 2025 and will climb at a 6.43% CAGR, driven by ditching regulations and the twin-engine redundancy ethos within defense, HEMS, and offshore spheres. Safran’s Arriel 2E and Pratt & Whitney Canada’s PT6C-67E feature dual FADEC channels, delivering a sub-0.32 lb/hp/hr fuel burn, an advantage as SAF surcharges take effect.[4]Safran, “Arriel 2E Turboshaft Engine,” safran-group.com Piston models decline at a 2.1% CAGR because Stage 3 acoustic limits erode urban access rights. Hybrid-electric demonstrators are gathering momentum, yet certification and battery-energy hurdles push entry into service beyond 2032, prolonging the turboshaft hegemony.

By End-Use Sector Emergency Medical Services Grow with Highest CAGR

Intelligence, surveillance, and reconnaissance (ISR) accounted for 28.38% of Europe's helicopter market in 2025. The segment's growth is fueled by an intensified focus on bolstering defense capabilities, increased procurement of military helicopters, and escalating warfare situations across Europe. The EMS segment is expected to be the fastest-growing sector at a 7.19% CAGR. Bulgaria reduced rural response times to 18 minutes after introducing three H145 helicopters across five bases, showcasing tangible public health dividends. Ireland specified night-vision, dual-pilot, and twin-stretcher layouts in its 2025 tender, reflecting harmonized EU medical-interior norms. Offshore energy accounts for 18% of end-use and grows at a 6.1% CAGR despite squeezed operator margins. Law-enforcement missions account for 12% of end-use and tend to gravitate toward common cockpit fleets for training efficiency. Tourism and VIP charter stands at 15% as Mediterranean resort demand rebounds. Search and rescue operations remain at 10%, concentrated in coastal states with obligations in the Baltic and North Seas. In comparison, utility tasks account for 17% but are facing gradual substitution by unmanned platforms.

Geography Analysis

The United Kingdom retained a 19.91% share of the European helicopter market in 2025, as North Sea legacy oil infrastructure, expansive HEMS grids, and the pending New Medium Helicopter award underpinned volume. Long-term contracts held by CHC and Bristow feature the H175, AW139, and AW189 types, while the National Police Air Service has ordered ten H145s to unify its fleet training. Post-Brexit dual-certification requirements have created additional administrative costs, yet they have not deterred major offshore operators from continuing their operations.

France and Germany are running parallel modernization agendas worth more than EUR 6 billion (USD 7 billion) through 2031. France completed delivery of 63 NH90 Caïman transports in February 2025 and initiated Tiger MkIII upgrades in 2022. Germany received its first H145M within eleven months of contract signature and will field 82 units by 2029, financed by the EUR 100 billion (USD 116.66 billion) defense fund. Airbus Donauwörth produces up to 80 H145-family units annually, solidifying Germany's position as both the lead customer and manufacturing hub.

Italy records the highest 6.73% CAGR to 2031, driven by Leonardo’s domestic lines shortening lead times and the generation of new shuttle demand from Adriatic and Tyrrhenian offshore wind sites. Spain follows at 5.8% on tourism recovery and Tiger MkIII participation. Eastern Europe, comprising Poland, the Baltics, and Scandinavia, is expected to advance 5.2% as border-security budgets rise and Baltic Sea wind-farm activity accelerates. However, sanctions have curtailed Russia’s participation, leaving legacy Soviet fleets stranded.

Competitive Landscape

Airbus Helicopters and Leonardo together accounted for more than 70% of civil and parapublic deliveries in 2025, a level that signals high concentration. Airbus posted 450 net orders and 361 deliveries in 2024, resulting in a 57% global market share in the civil sector. Leonardo leverages AW139, AW169, and AW189 success in the UK and Italy while courting the light-single segment with the AW09. Textron’s Bell line faces a sliding share as European customers consolidate on Airbus and Leonardo cockpits. NH Industries struggles with NH90 supportability; availability shortfalls below 40% have prompted Norway and Germany to either exit or limit their fleets, leaving space for the H175M and AW149. Defense acquisition policy divergence widens the opportunity for newer entrants; Sikorsky competes for the S-70i in the UK's New Medium Helicopter tender, while smaller OEMs, such as Robinson and MD Helicopters, sustain niche law enforcement and utility footprints. Technological differentiators now include hybrid-electric readiness and crewed-uncrewed teaming: Airbus’s VSR700 completed frigate trials in 2024, hinting at future requirement sets that integrate optionally piloted assets.

Europe Helicopters Industry Leaders

Leonardo S.p.A

Airbus SE

Rostec

The Boeing Company

Textron Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: In December 2023, Germany sealed a deal for 62 H145M light combat helicopters (Leichter Kampfhubschrauber, or LKH), with an option to purchase 20 additional units. Recently, Germany exercised that option, raising the total to 82 helicopters. Of these, 72 will serve the German Army, while the remaining 10 are designated for the Luftwaffe's special forces.

- March 2025: Airbus introduced the H140 light twin at VERTICON, positioning the 3-ton model between the H135 and H145 with entry into service slated for 2028.

- December 2024: Spain has accepted its first NH90 Standard 3 helicopter as part of its fleet modernization roadmap.

- November 2024: Airbus delivered the first H145M to the Bundeswehr less than one year after contract award, enabling pilot training at Bückeburg ahead of 2026 operational deployment.

Europe Helicopters Market Report Scope

The European helicopters market report covers the latest trends and technological developments, providing analysis on various aspects of the market, including development and revenue generation from different types of helicopters.

The Europe helicopters market is segmented by maximum take-off weight, application, engine type, end-use sector, and geography. By maximum take-off weight, the market is segmented into light, medium, and heavy. By application, the market is categorized into military, civil, and commercial segments. By engine type, the market is classified into piston engines and turboshaft engines. By end-use sector, the market is segmented into combat, offshore energy, emergency medical services, law enforcement and public safety, tourism and VIP charter, search and rescue, ISR, and utility and aerial work.

The report also covers the market sizes and forecasts for the Europe helicopters market across major countries. The market sizing and forecasts have been provided in value (USD billion).

By Maximum Take-off Weight

| Light |

| Medium |

| Heavy |

By Application

| Military |

| Civil and Commercial |

By Engine Type

| Piston Engine |

| Turboshaft Engine |

By End-Use Sector

| Combat |

| Offshore Energy |

| Emergency Medical Services |

| Law Enforcement and Public Safety |

| Tourism and VIP Charter |

| Search and Rescue |

| Utility and Aerial Work |

| Intelligence, Surveillance, and Reconnaissance (ISR) |

By Geography

| Europe | United Kingdom |

| France | |

| Germany | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe |

| By Maximum Take-off Weight | Light | |

| Medium | ||

| Heavy | ||

| By Application | Military | |

| Civil and Commercial | ||

| By Engine Type | Piston Engine | |

| Turboshaft Engine | ||

| By End-Use Sector | Combat | |

| Offshore Energy | ||

| Emergency Medical Services | ||

| Law Enforcement and Public Safety | ||

| Tourism and VIP Charter | ||

| Search and Rescue | ||

| Utility and Aerial Work | ||

| Intelligence, Surveillance, and Reconnaissance (ISR) | ||

| By Geography | Europe | United Kingdom |

| France | ||

| Germany | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

Key Questions Answered in the Report

What is the current value of the Europe helicopters market?

The market is valued at USD 12.53 billion in 2026 and is forecast to reach USD 16.39 billion by 2031.

Which segment holds the highest Europe helicopters market share?

Medium-lift helicopters led with 47.76% share in 2025.

Which sector is growing fastest within European helicopter applications?

Emergency medical services expand at a 7.19% CAGR through 2031, the fastest among all end-use sectors.

Why do turboshaft engines dominate Europe’s helicopter fleet?

They meet twin-engine safety rules for over-water and urban operations and already hold an 87.67% share in 2025.

Which country shows the quickest growth in helicopter procurement?

Italy registers the highest 6.73% CAGR through 2031, driven by domestic production and offshore wind projects.

How do sustainable aviation fuel mandates affect operators?

ReFuelEU rules raise fuel costs two to five times, cutting margins in offshore and HEMS missions unless operators secure subsidies or fleet upgrades.

Page last updated on: