Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

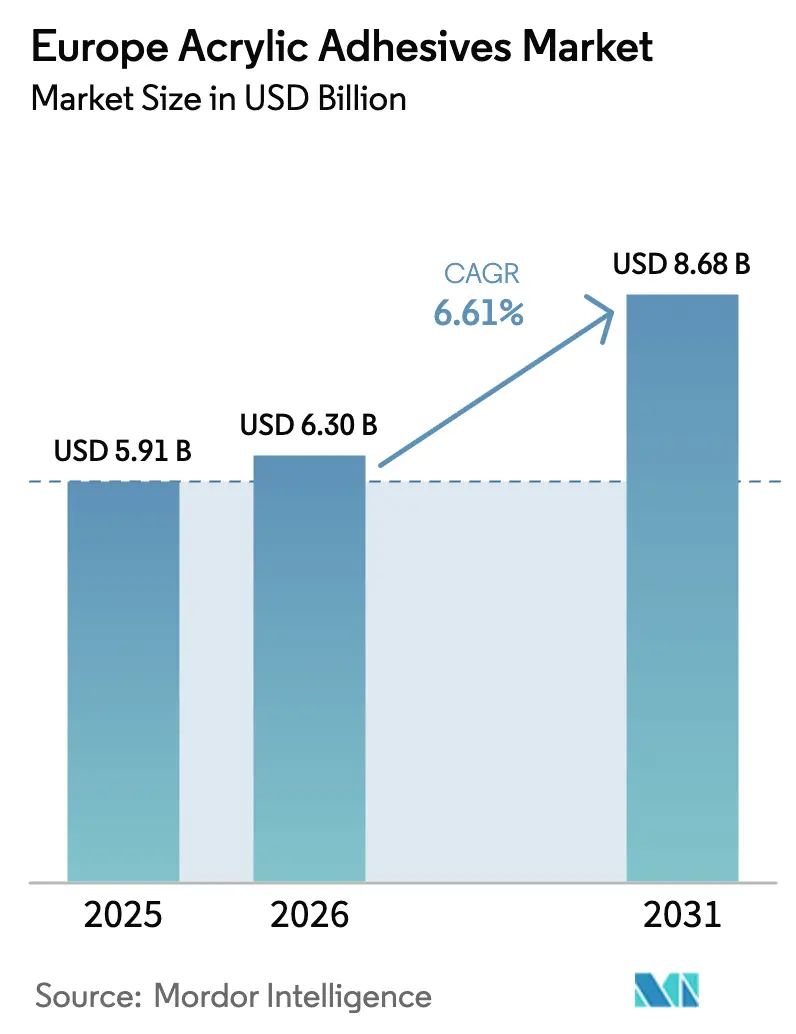

| Base Year Market Size (2025) | USD 5.91 Billion |

| Market Size (2026) | USD 6.30 Billion |

| Market Size (2031) | USD 8.68 Billion |

| Growth Rate (2026 - 2031) | 6.61% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe Acrylic Adhesives Market Analysis by Mordor Intelligence

The Europe Acrylic Adhesives Market size is expected to increase from USD 5.91 billion in 2025 to USD 6.30 billion in 2026 and reach USD 8.68 billion by 2031, growing at a CAGR of 6.61% over 2026-2031. Product demand benefits from e-commerce packaging, vehicle lightweighting, and retrofit construction incentives that collectively lift volumes and improve average selling prices. Regulatory changes that tighten volatile-organic-compound (VOC) thresholds accelerate the switch to low-VOC water-borne chemistries, prompting suppliers to re-engineer supply chains for compliant monomers and emulsifiers. Integrated producers with backward linkages into methyl-methacrylate and butyl-acrylate feedstocks retain a cost edge, while mid-tier converters win volume with tailored formulations for niche substrates. Portfolio rationalization, technical-service support, and rapid scale-up capacity remain decisive competitive factors as buyers consolidate supplier bases to secure on-time deliveries and regulatory documentation.

Key Report Takeaways

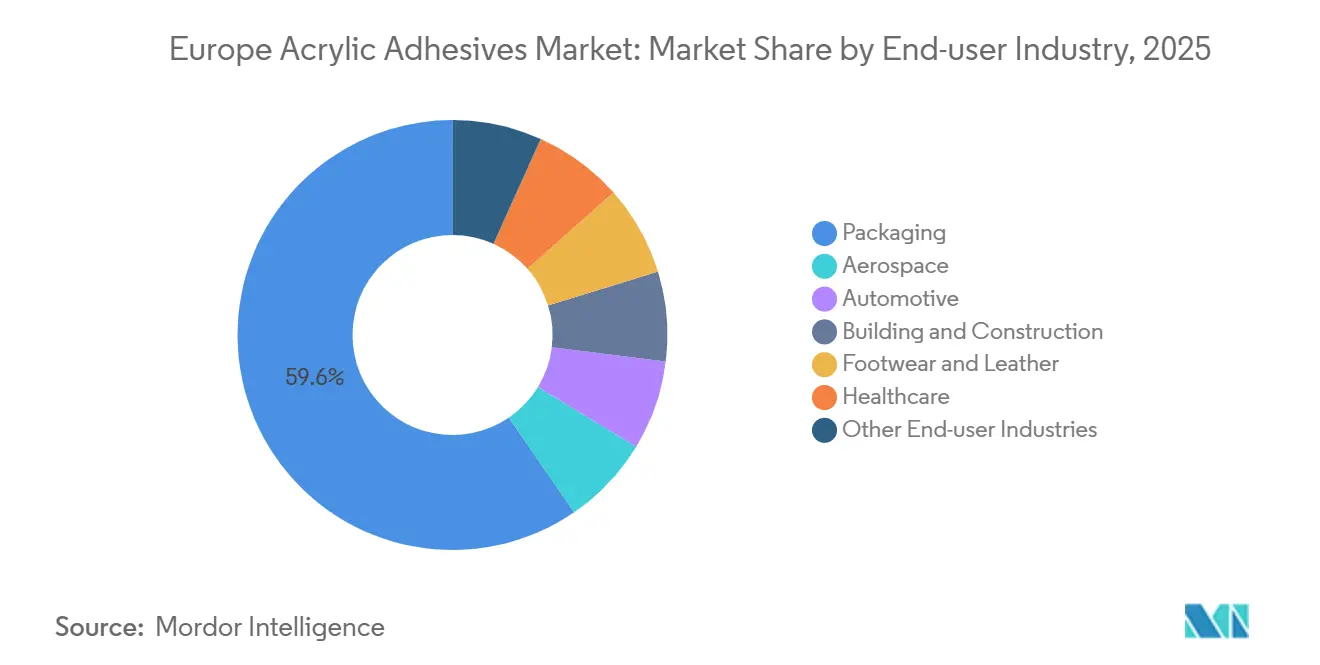

- By end-user industry, packaging led with 59.56% revenue share in 2025; automotive is advancing at a 6.72% CAGR through 2031.

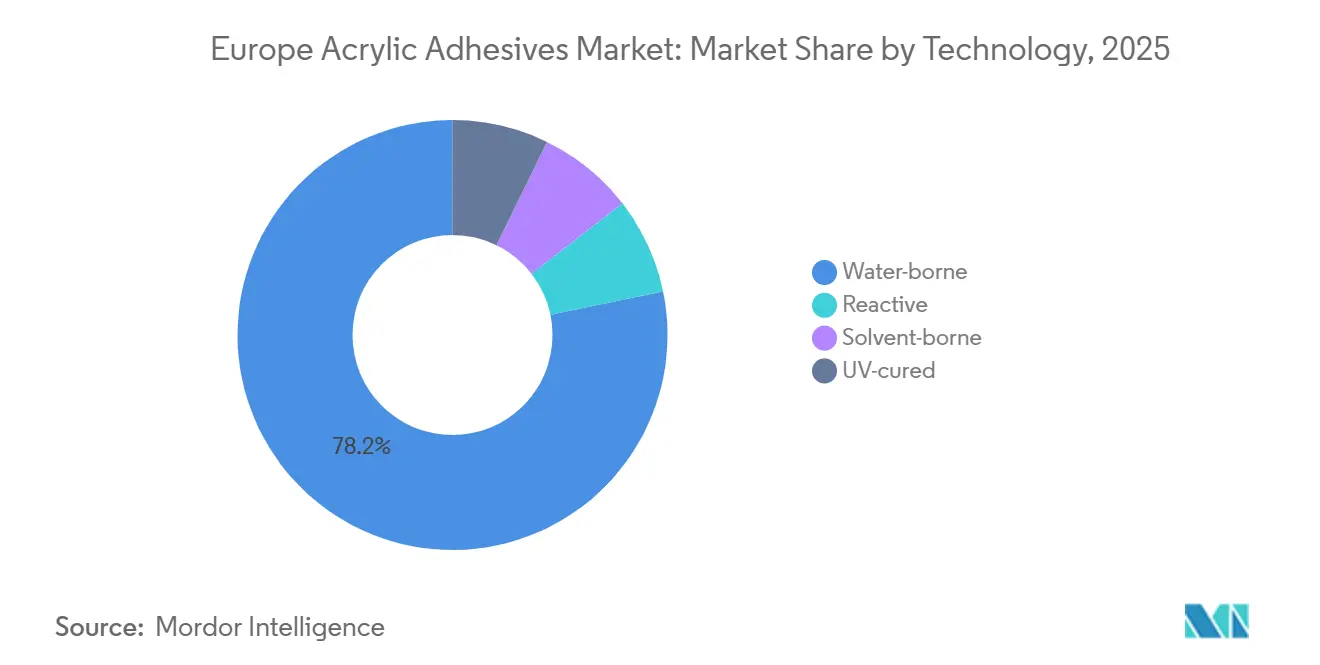

- By technology, water-borne formulations held 78.24% share in 2025 and are expanding at 7.15% CAGR to 2031.

- By country, Germany commanded 23.11% share in 2025, while the United Kingdom is projected to post the fastest 6.78% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Europe Acrylic Adhesives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Shift toward water-borne acrylics under EU VOC limits | +1.8% | EU-wide, strongest in Germany, France, Benelux | Short term (≤ 2 years) |

| E-commerce packaging boom driving PSA demand | +1.5% | Germany, UK, France, Nordic countries | Medium term (2-4 years) |

| Automotive lightweighting and mixed-material bonding | +1.2% | Germany, Italy, Spain, UK | Medium term (2-4 years) |

| EU Renovation Wave spurring façade-insulation adhesives | +0.9% | DACH, France, Southern Europe | Long term (≥ 4 years) |

| Wind-turbine blade refurbishment using structural acrylics | +0.6% | Nordic countries, German and UK offshore zones | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift Toward Water-Borne Acrylics Under European Union VOC Limits

Revised EU VOC ceilings, announced late 2025 and effective mid-2026, compel formulators to audit every solvent-borne stock-keeping unit, accelerate pilot runs of compliant water-borne grades, and certify new raw-material supply chains[1]Directorate-General for Environment, “Revision of EU VOC Limits for Building Products,” environment.ec.europa.eu. Early movers that publish third-party life-cycle assessments secure preferential scores in public tenders and hospitality refurbishments that weight low-emission products higher. Installers need retraining because emulsion systems exhibit longer open time and altered rheology, yet their near-zero odor profile reduces indoor-air re-occupancy delays. Packaging groups have already trialed hybrid acrylic UV-emulsion chemistries that meet both productivity and compliance targets. Collectively, the legislative push adds a visible 1.8 percentage-point uplift to the forecast CAGR of the Europe Acrylic Adhesives market.

E-Commerce Packaging Boom Driving PSA Demand

Online retail migration propels demand for corrugated labels, flexible films, and resealable pouches that rely on pressure-sensitive acrylic emulsions for consistent tack across cardboard, polyethylene, and metallized substrates[2]Avery Dennison, “Capacity Expansion in France to Meet E-commerce Label Demand,” averydennison.com. RFID tags and smart-label sensors increasingly specify low-migration acrylics that remain stable through multi-temperature logistics cycles. Brand owners favor water-borne grades that facilitate fiber-to-fiber recycling and reduce de-inking steps, aligning with EU circular-economy directives. European converters report line-speed gains of up to 12% after switching to next-generation emulsion PSAs, supporting a 1.5 percentage-point boost to overall growth in the Europe Acrylic Adhesives market.

Automotive Lightweighting and Mixed-Material Bonding

Battery-electric platforms adopt multi-material architectures, aluminum, high-strength steel, and glass-fiber composites, that reward structural acrylics and performance tapes for stress-distribution and corrosion mitigation. Tesa ACXplus tapes and SikaFast acrylic two-part systems cut weld points, lower NVH levels, and shorten takt time by curing within minutes. Supply agreements with German OEMs anchor baseline volumes, while contract manufacturing in Spain and Italy scales capacity for export builds. The shift displaces mechanical fasteners and raises acrylic content per vehicle, adding about 1.2 percentage-points to the long-term CAGR of the Europe Acrylic Adhesives market.

EU Renovation Wave Spurring Façade-Insulation Adhesives

The Renovation Wave targets energy upgrades in 35 million buildings by 2030, unlocking subsidies that favor low-VOC acrylic adhesive tapes for vapor-barrier laminates and exterior insulation composite systems. Contractors in Germany and Austria cite 30% labor-time savings when using peel-and-stick acrylic membranes versus cementitious bonding methods. Premium moisture-tolerant acrylic mastics also comply with stricter fire-performance classes introduced in the 2025 amendments to national building codes. This structural demand underpins a 0.9 percentage-point CAGR lift for the Europe acrylic adhesives market over the forecast horizon.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Acrylic-monomer price volatility | -0.8% | EU-wide, Antwerp and Rhine production hubs | Short term (≤ 2 years) |

| VOC-compliance costs for solvent systems | -0.5% | Germany, France, Benelux | Medium term (2-4 years) |

| Bio-based polyurethane dispersions cannibalizing share | -0.4% | Germany, France, Nordic premium niches | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Acrylic-Monomer Price Volatility

Scheduled cracker turnarounds and spot acetone tightness have historically triggered double-digit quarterly swings in methyl-methacrylate pricing. Although late-2025 oversupply cooled quotations, buyers remain wary and shift toward formula-based contracts or dual sourcing from fully integrated suppliers. Feedstock swings of ±10% compress formulators’ margins, delaying discretionary investments and shaving 0.8 percentage-points off the Europe acrylic adhesives market growth potential in the near term.

VOC-Compliance Costs for Solvent Systems

Solvent-borne grades used for automotive refinish and specialty coatings require expensive abatement investments to meet revised emission ceilings. Smaller converters either retrofit incineration units or exit the segment, consolidating demand toward larger players that can amortize compliance upgrades. The incremental capital burden trims 0.5 percentage-points from the projected CAGR of the Europe Acrylic Adhesives market across the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-user Industry: Packaging Dominance Anchors Volume Growth

Packaging accounted for 59.56% of the Europe Acrylic Adhesives market share in 2025, supported by escalating parcel volumes and flexible-film lamination lines running at record utilization. The segment is expected to retain leadership through 2031 as brand owners migrate to mono-material structures that rely on high-clarity acrylic emulsions. Arkema’s late-2024 acquisition of Dow’s flexible-packaging adhesive assets immediately lifted Bostik’s European footprint and secured backward integration into performance resins. Medical packaging and pharmaceutical blister labels further reinforce baseline demand, ensuring the Europe Acrylic Adhesives market size for packaging expands steadily across the forecast years.

Automotive, while contributing a smaller base, is forecast to grow fastest at 6.72% CAGR on the back of battery module assembly, lightweight body-in-white bonding, and electromobility investments. Vehicle platforms aggressively cut weight to extend driving range, and OEMs (Original Equipment Manufacturers) validate acrylic tapes for mixed-metal joints that tolerate differential thermal expansion. Strategic sourcing arrangements signed by German automakers secure multi-year capacity reservations, creating a visible growth pipeline for the Europe acrylic adhesives market within the mobility value chain.

By Technology: Water-Borne Formulations Lead Regulatory Shift

Water-borne systems held 78.24% of the Europe Acrylic Adhesives market size in 2025 and are projected to log the fastest segmental CAGR at 7.15% to 2031. The February 2026 enforcement of revised EU Ecolabel thresholds accelerates the pivot, pushing converters to qualify low-VOC emulsions and UV-acrylic hybrids. Avery Dennison’s EUR 60 million French expansion ramps high-speed hot-melt emulsion capacity, while Henkel retrofits its Bopfingen site for next-generation water-borne lines. The structural uplift cements water-borne dominance and limits solvent-grade demand to niche metal-bonding and maintenance coatings where performance outliers justify higher VOC budgets.

UV-cured and reactive two-component methyl-methacrylate (MMA) formulations continue to capture share in electronics encapsulation, rail rolling stock, and composite panel assemblies. Faster line speeds and energy-efficient LED curing drive a healthy 8-plus CAGR, complementing the broader water-borne surge.

Geography Analysis

Germany generated 23.11% of total revenue in the Europe Acrylic Adhesives market during 2025, underpinned by its automotive export base, renovation incentives tied to the Gebäudeenergiegesetz upgrade, and a dense network of formulators clustered along the Rhine. Local OEM validation protocols favor suppliers with domestic pilot lines and on-site technical support; consequently, global majors operate multi-technology plants near Stuttgart and Düsseldorf. Federal hydrogen-hub funding also trickles into new trailer-body assembly plants that specify low-temperature-curing acrylics to maximize cycle time.

The United Kingdom is projected to record the highest national CAGR of 6.78% through 2031. Post-Brexit trade realignment drives domestic investments in corrugated packaging, prefabricated housing, and offshore wind logistics, each of which consumes PSA labels, insulation tapes, and structural acrylic cartridges. Regulatory divergence from REACH presents extra documentation for importers, yet parallel registration pathways introduced in 2025 preserve supply-chain continuity, preventing shipment delays and sustaining momentum in the Europe Acrylic Adhesives market.

France, Italy, and Spain collectively add resiliency by balancing sector exposure: France hosts Arkema’s technical center that spearheads bio-based monomer trials, Italy houses newly acquired flexible-lamination assets now fully integrated into Bostik, and Spain accelerates façade-retrofit programs subsidized under the EU Renovation Wave. Nordic countries, though smaller by value, outpace the regional average owing to wind-blade maintenance and strict VOC caps that mandate high-performance water-borne grades. Across these geographies, local application norms and building codes shape formulation preferences, yet the overarching compliance trajectory drives convergence toward low-emission chemistries in the Europe Acrylic Adhesives market.

Competitive Landscape

The Europe Acrylic Adhesives market is moderately consolidated. Automation, data-rich technical dossiers, and traceable supply chains now act as tie-breakers in sourcing decisions. Suppliers that merge real-time production data with digital customer portals shorten qualification cycles, translating into a higher share-of-wallet with multinational brand owners. Collectively, these moves pull industry boundaries upward, but with sufficient space for niche specialists, sustaining a balanced yet competitive Europe Acrylic Adhesives market.

Europe Acrylic Adhesives Industry Leaders

3M

Arkema Group

H.B. Fuller Company

Henkel AG & Co. KGaA

Sika AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Arkema transitioned its entire range of acrylic thickeners, commonly utilized for viscosity control in adhesives, to bio-based variants at its European facilities. This move not only integrates up to 30% bio-based content but also achieves a reduction of up to 25% in the product's carbon footprint when juxtaposed with standard grades.

- June 2024: Meridian Adhesives Group (Meridian), a manufacturer and innovator of high-performance adhesives, announced the acquisition of Bondloc UK Ltd, a specialty adhesive manufacturer based in the United Kingdom.

Europe Acrylic Adhesives Market Report Scope

Acrylic adhesive is a fast-curing, high-strength structural adhesive, often known as methyl methacrylate (MMA), designed for bonding diverse materials, including metals, plastics, and composites. It is known for its resistance to weathering, moisture, UV light, and chemicals, making it ideal for both structural indoor and outdoor applications.

The Europe Acrylic Adhesives market report is segmented by end-user industry, technology, and country. By end-user industry, the market is segmented into aerospace, automotive, building and construction, footwear and leather, healthcare, packaging, and other end-user industries. By Technology, the market is segmented into reactive, solvent-borne, UV-cured adhesives, and water-borne. The report also covers market sizes and forecasts for 6 countries across the region. The market sizes and forecasts are provided in terms of value (USD).

By End-user Industry

| Aerospace |

| Automotive |

| Building and Construction |

| Footwear and Leather |

| Healthcare |

| Packaging |

| Other End-user Industries |

By Technology

| Reactive |

| Solvent-borne |

| UV-cured |

| Water-borne |

By Country

| Germany |

| United Kingdom |

| France |

| Italy |

| Spain |

| Russia |

| NORDIC Countries |

| Rest of Europe |

| By End-user Industry | Aerospace |

| Automotive | |

| Building and Construction | |

| Footwear and Leather | |

| Healthcare | |

| Packaging | |

| Other End-user Industries | |

| By Technology | Reactive |

| Solvent-borne | |

| UV-cured | |

| Water-borne | |

| By Country | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe |

Market Definition

- End-user Industry - Building & Construction, Packaging, Automotive, Aerospace, Woodworking & Joinery, Footwear & Leather, Healthcare, and Others are the end-user industries considered under the acrylic adhesives market.

- Product - All acrylic adhesive products are considered in the market studied

- Resin - Under the scope of the study, different kinds of acrylate monomers, like 2-Ethylhexyl acrylate and butyl acrylate are considered

- Technology - For the purpose of this study, Water-borne, Solvent-borne, Reactive, Hot Melt, and UV Cured adhesive technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms