Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

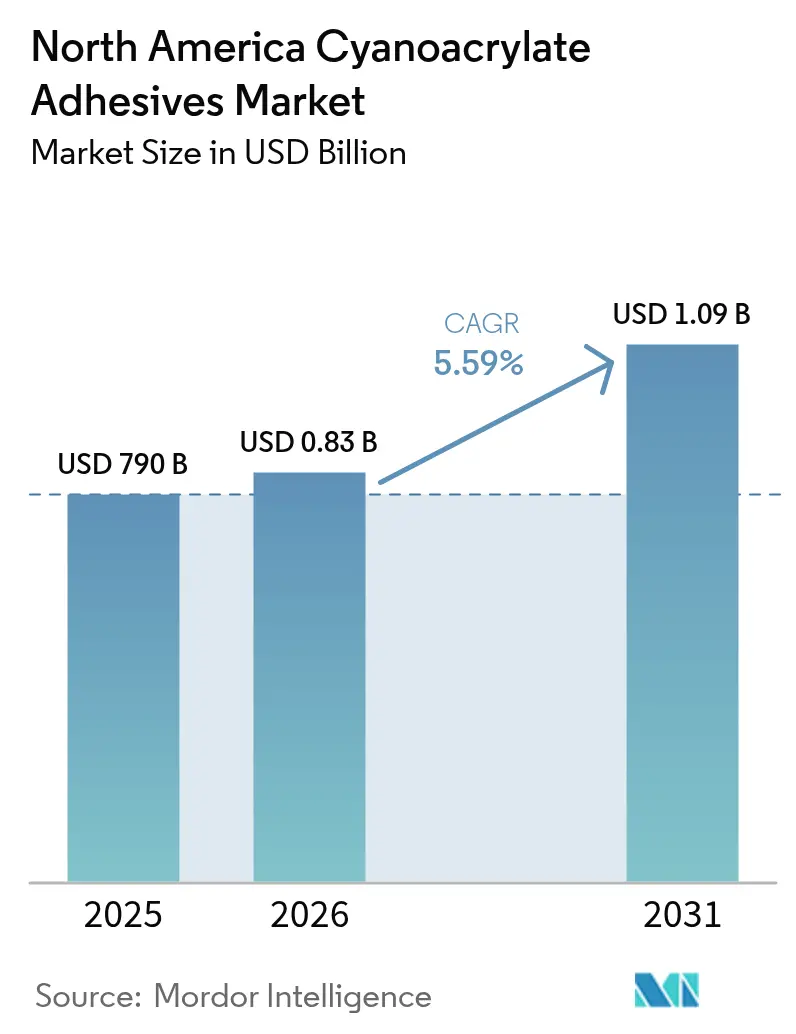

| Base Year Market Size (2025) | USD 790 Billion |

| Market Size (2026) | USD 0.83 Billion |

| Market Size (2031) | USD 1.09 Billion |

| Growth Rate (2026 - 2031) | 5.59% CAGR |

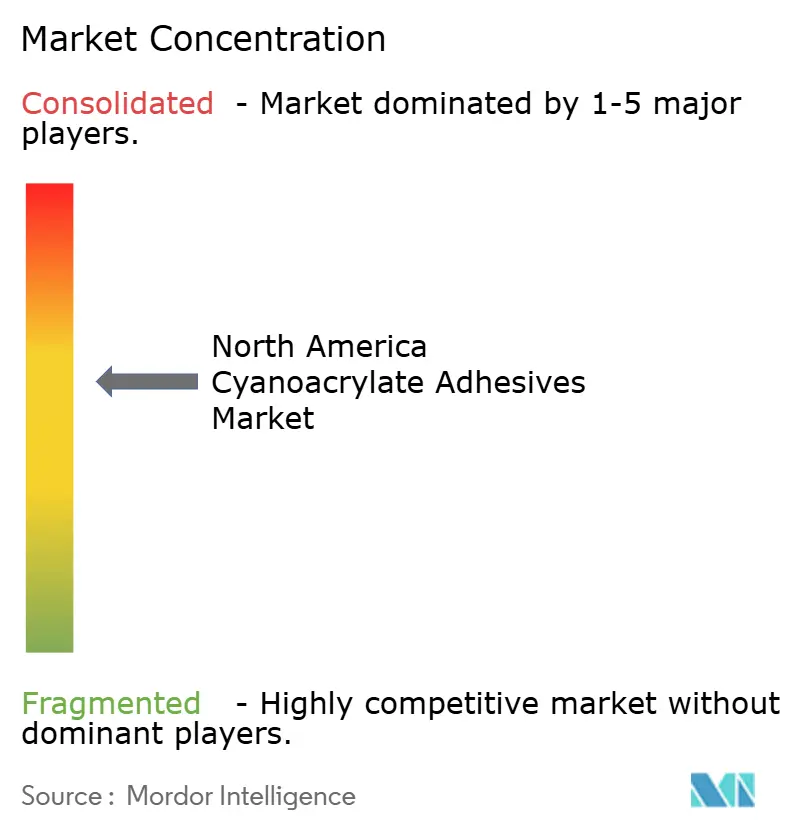

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Cyanoacrylate Adhesives Market Analysis by Mordor Intelligence

The North America Cyanoacrylate Adhesives Market size is expected to grow from USD 790 million in 2025 to USD 830 million in 2026 and is forecast to reach USD 1.09 billion by 2031 at 5.59% CAGR over 2026-2031. This outlook underscores the adhesive sector’s ability to grow even as many specialty chemicals struggle with price pressures and stricter environmental rules. Robust electronics miniaturization, medical device innovation and lightweighting programs in transportation underpin demand. Regulatory moves that restrict solvent-based chemistries are steering buyers toward instant-curing alternatives, while supply-chain shifts closer to end-markets favour production hubs in North America and Mexico. Competition centres on formulation speed, biocompatibility and sustainability, and firms that combine global scale with application-specific know-how continue to capture share.

Key Report Takeaways

- By product type, Ethyl Ester-based grades led with 46.52% of cyanoacrylate adhesives market share in 2025, whereas Other Product Types are projected to achieve the fastest 6.49% CAGR through 2031.

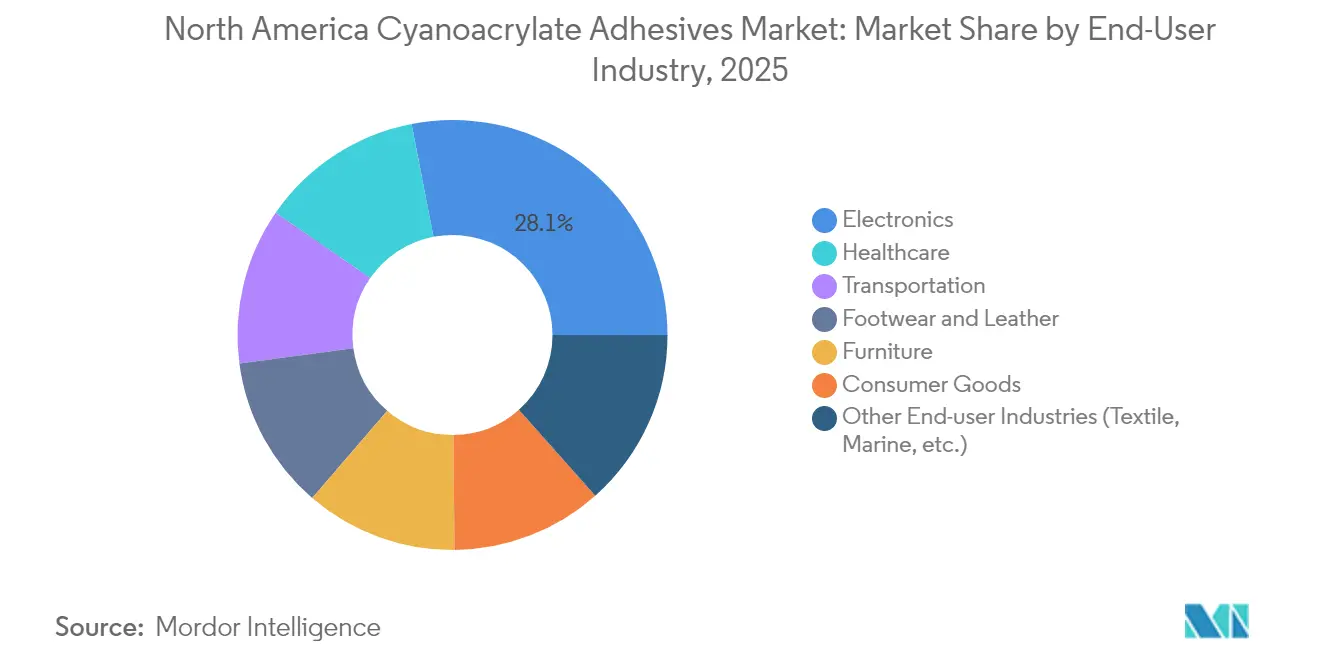

- By end-user industry, Electronics held 28.05% revenue share in 2025, while Healthcare is poised for the highest 6.55% CAGR to 2031.

- By geography, the United States commanded 68.02% share of the cyanoacrylate adhesives market size in 2025; Mexico is the fastest-growing territory with a 5.86% CAGR during 2026-2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Cyanoacrylate Adhesives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging demand from miniaturised consumer-electronics assembly | +1.2% | Global, with concentration in Asia-Pacific manufacturing hubs | Medium term (2-4 years) |

| Rapid adoption in medical device adhesives and wound closure | +1.8% | North America & EU, expanding to emerging markets | Long term (≥ 4 years) |

| Lightweighting initiatives in automotive and e-mobility | +0.9% | Global, led by North America and Europe | Medium term (2-4 years) |

| Expanding DIY and consumer repair culture | +0.6% | North America & EU, with growth in urban centers | Short term (≤ 2 years) |

| Growing demand from furniture industry | +0.4% | Global, particularly in Asia-Pacific production centers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Demand from Miniaturised Consumer-Electronics Assembly

Rapid device shrinkage forces manufacturers to abandon screws and clips in favour of low-viscosity cyanoacrylates that flow into micron-scale gaps and cure within seconds, eliminating added heat cycles that can warp delicate substrates. Growth is amplified by heterogeneous integration in advanced chip packaging, where adhesives must secure multi-material stacks while preventing conductive pathways. Wearables, IoT sensors and automotive infotainment modules replicate these constraints, extending the driver’s global reach. OEMs value the chemistry’s ability to bond plastics, metals and composites with minimal surface preparation, streamlining throughput in high-volume Asian plants. The result is consistent pull-through of premium-grade cyanoacrylates into every new generation of smart devices.

Rapid Adoption in Medical Device Adhesives and Wound Closure

Medical-grade cyanoacrylates are gaining on sutures thanks to faster procedure times, smaller scars and reduced infection rates; the Dermabond Prineo mesh system cut post-operative complications by double-digit margins in multi-centre trials. Long-chain butyl and octyl variants show lower tissue toxicity and maintain tensile strength under bodily fluids, fostering approvals for internal and external applications. H.B. Fuller’s acquisition of Medifill and pending GEM deal expands European supply, illustrating how suppliers race to clear strict ISO 10993 and FDA hurdles. As global surgical volumes rise alongside ageing populations, hospitals continue switching to single-use tissue adhesives that simplify training and shorten recovery, pushing healthcare demand above all other sectors.

Lightweighting Initiatives in Automotive and E-Mobility

Electric vehicles rely on mixed-material architectures—aluminium skins, magnesium castings and carbon-fibre reinforcements—that challenge mechanical fastening. Cyanoacrylates meet this need with universal substrate compatibility and cycle times that match stamping presses, supporting high-speed body-in-white lines projected to exceed 95 million units by 2030 [1]Henkel, “Structural Adhesives for EV Platforms,” henkel.com. New formulations integrate flexibilizers and heat-resistant crosslinkers, letting bonds survive thermal shocks from –40 °C to 120 °C without peeling. Automakers report weight savings of 5 kg per vehicle by swapping rivets for adhesive dots, contributing directly to range gains that comply with tighter CAFE and EU CO2 targets.

Expanding DIY and Consumer Repair Culture

Right-to-repair laws and social media “fix-it” movements are boosting retail glue sales across Europe and North America. Products such as Super Glue Ultra+ replace 60% of petroleum feedstock with castor oil yet keep the trademark 15-second set time, addressing consumer calls for greener chemistries. Lighter odour, anti-clog packaging and colourless joints make the category a home-improvement staple. EU Green Deal circularity goals and retailer eco-labels already favour bio-based tubes on store shelves. With households attempting everything from sneaker restoration to phone-screen fixes, volumes entering the consumer channel are growing faster than GDP.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict VOC and occupational-health regulations | -0.8% | Global, with stricter enforcement in North America & EU | Long term (≥ 4 years) |

| Limited shear or thermal resistance in comparison to alternatives | -0.5% | Global, particularly affecting high-temperature applications | Medium term (2-4 years) |

| Feedstock price-volatility | -0.3% | Global, with higher impact in regions dependent on imports | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Strict VOC and Occupational-Health Regulations

EPA aerosol-coating limits, Canada’s VOC caps on 130 product categories and Australia’s draft toxicology findings compel formulators to strip out solvents and add warning labels, raising compliance costs by up to 12% of sales for small producers [2]United States Environmental Protection Agency, “Aerosol Coating Final Rule Update,” epa.gov. Upgraded ventilation, personal protective equipment and mandatory workplace monitoring further inflate operating expenses in developed regions. While low-odour lines gain traction, they often require costly stabilizers that squeeze margins. Multinationals with dedicated regulatory teams absorb these burdens, but smaller regional brands risk exit or acquisition, nudging sector consolidation.

Limited Shear or Thermal Resistance

Even modified ethyl cyanoacrylates soften near 100 °C and crack under prolonged shear loads above 10 MPa, disqualifying them from engine bays, jet turbines and outdoor structural joints. Researchers adding 6-hydroxyhexyl acrylate improved heat resistance but doubled raw-material costs, delaying commercial scale-up. UV and thermal ageing generate irritant by-products, shortening service life in solar-exposed assemblies. Epoxy, polyurethane and acrylic hybrids therefore retain the high-temperature niche, limiting cyanoacrylate penetration until cost-effective co-monomer blends reach the market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Ethyl Ester Leads as Bio-Based Grades Surge

Ethyl Ester-based formulations retained a commanding 46.52% share of the cyanoacrylate adhesives market size in 2025, buoyed by decades of process optimization that deliver low cost and broad substrate compatibility. Sales into electronics sub-assemblies and automotive harnesses keep throughput high, and incremental tweaks—such as anti-bloom additives—preserve competitiveness. In parallel, “Other Product Types” that bundle bio-based or specialty grades are set to climb at a 6.49% CAGR through 2031, reflecting corporate climate pledges and end-user quests for differentiated performance.

Renewed interest in Methyl Ester grades persists where micro-bonding speed outranks final strength, yet volume dips as engineers chase tougher bonds for impact-laden plastics. Alkoxy Ethyl variants, while niche, win projects demanding cyclic thermal stability beyond 120 °C. University labs are publishing routes to ethoxyethyl α-cyanoacrylate with 24% higher peel strength, signalling potential disruptive entrants should scale economics line up. Over the forecast horizon, suppliers will likely hedge portfolios by balancing legacy Ethyl Ester tonnage with high-margin green or high-temperature offerings in response to procurement scorecards.

By End-User Industry: Electronics Still on Top, Healthcare Gaining Ground

Electronics captured 28.05% of the cyanoacrylate adhesives market share in 2025, thanks to relentless demand for instant-curing materials that bond sensors, displays and antennae without heat distortion. The segment’s depth is evident in fine-pitch semiconductor work that cannot tolerate screws or long oven cycles. Yet Healthcare is speeding ahead with a 6.55% CAGR to 2031, propelled by surgical sealants that shorten operating times and cut infection risk.

Transport OEMs continue to dip into cyanoacrylates for lightweight trim clips and battery modules, while furniture plants swap nails for fast-set drops to meet rapid assembly targets. DIY-friendly consumer goods cement brand loyalty as hobbyists repair toys and footwear at home. Elsewhere, marine and textile sectors adopt flexible cyanoacrylates in niche waterproofing and seam-bonding roles. Looking forward, a richer device mix in outpatient care—delivering drug micro-patches and catheter port seals—presents the next wave of Healthcare volume upside.

Geography Analysis

Under this market, the United States will control 68.02% of regional sales in 2025. The concentration mirrors the dominance of domestic electronics contract manufacturers, Detroit-based e-mobility programmes, and a mature medical-device cluster that demands FDA-cleared instant adhesives. Close proximity to R&D consortia and a robust patent ecosystem sustains innovation, cementing the US as the reference market for specification standards. Nevertheless, manufacturers must navigate overlapping federal and state emissions rules that add layer upon layer of testing and paperwork.

Mexico is the standout growth story, predicted to log a 5.86% CAGR through 2031 as nearshoring re-routes supply chains from Asia to the US-Mexico corridor. Incentives under USMCA slash tariffs on intermediate components, making Monterrey and Queretaro attractive sites for electronics and auto assembly. Adhesive vendors are already setting up local blending operations to trim freight costs and expedite just-in-time deliveries. Economic obstacles—such as subdued GDP expansion and occasional policy shifts—temper enthusiasm, but the structural re-orientation of North American production keeps investment momentum solid.

Canada completes the triad as a steady, highly regulated market. New VOC caps on adhesives oblige importers to maintain accredited test results for every batch, a hurdle easily cleared by global multinationals yet onerous for small specialty importers. Customers lean on suppliers for compliance guidance, reinforcing long-term partnerships and favouring established distributors. Growth pockets reside in Toronto’s med-tech corridor and Western Canada’s composites fabricators, each willing to pay premiums for certifiable clean chemistry.

Regulatory Landscape

In the United States, cyanoacrylate adhesives are governed by workplace chemical-safety and chemical-inventory requirements. OSHA covers occupational exposure and hazard communication for substances such as ethyl 2-cyanoacrylate and methyl 2-cyanoacrylate (including measurement methods referenced by OSHA), while EPA oversight under TSCA requires substances used in formulations to maintain compliant inventory status. EPA PBT rules also include a specific manufacturing-context exclusion for cyanoacrylate glue when used as an intermediate in a closed system.

In Canada, consumer and workplace products face different compliance layers. Consumer cyanoacrylate products fall under Health Canada consumer chemical controls (Consumer Chemicals and Containers Regulations), while workplace products must comply with WHMIS-aligned labeling and Safety Data Sheet requirements under the Hazard Products Act and Hazardous Products Regulations. This setup increases documentation and labeling discipline for importers, private-label brands, and distributors operating across the United States, Canada, and Mexico.

Value Chain Analysis

The value chain starts with upstream feedstocks and monomer synthesis, where supply concentration for ethyl cyanoacrylate monomers and dependence on key chemical precursors heighten sensitivity to price volatility and logistics disruptions. Manufacturing depends on controlled, moisture-managed operations (including nitrogen-blanketed equipment) and specialized formulation talent to maintain consistent viscosity, cure speed, and stability, particularly for medical and electronics specifications.

On the downstream side, regional production and blending shorten lead times for North American OEMs and reduce exposure to tariff-related cost swings across chemicals and packaging components. Players typically combine direct technical sales for regulated or high-spec accounts (medical device, automotive, electronics) with distributor networks and retail hardware channels for consumer-grade volumes. Established manufacturing footprints, including Toagosei America in West Jefferson, Ohio, and H.B. Fuller capacity in Bowling Green, Kentucky, support faster sampling, qualification, and just-in-time replenishment for major end users.

Competitive Landscape

The cyanoacrylate adhesives market includes major players such as Henkel AG and Co. KGaA, 3M, H.B. Fuller Company, Arkema, and Sika AG. Henkel leads with its closed-loop carbon initiative, producing adhesives from captured industrial CO2 streams, offering low-emission options. H.B. Fuller expanded in 2024 by acquiring Medifill and GEM, establishing a medical-technology hub in Europe, and enhancing its tissue-sealant offerings. Arkema’s Bostik Fast Glue Ultra+ advances bio-content in consumer retail, shifting sustainability messaging to DIY markets. Competitive advantages now focus on addressing application challenges, such as thermal shock and odor control, rather than production volume.

North America Cyanoacrylate Adhesives Industry Leaders

3M

Henkel AG & Co. KGaA

H.B. Fuller Company

Sika AG

Arkema

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Medical and healthcare specifications create a clear whitespace for suppliers that can pair cyanoacrylate performance with regulatory-ready documentation. In the United States, topical skin-approximation tissue adhesives are regulated by the FDA as Class II devices under 21 CFR 878.4010 and supported by special controls, which raises the value of suppliers that can offer traceability, biocompatibility packages (commonly aligned to ISO 10993), and consistent manufacturing controls. This framework also shapes supplier selection for contract manufacturers and brand owners serving North American hospitals and outpatient procedures.

Sustainability-led reformulation is another opportunity area, with visible commercial movement toward higher bio-content and solvent-free positioning in consumer and light-industrial channels. Arkema subsidiary Bostik has already commercialized a bio-based cyanoacrylate (Fast Glue Ultra+), which provides a proof point for retail adoption and a benchmark for competing brands seeking lower-odor, lower-emission, and packaging-friendly claims, while still meeting the instant-cure productivity needs that dominate electronics and general assembly use cases.

Recent Industry Developments

- June 2026: Biesterfeld and Bostik (Arkema) entered into a distribution agreement expanding access to Bostik medical adhesive lines, including cyanoacrylates and UV-curing cyanoacrylates, for the medical device industry. The agreement strengthens channel reach for regulated, high-specification applications where supplier qualification, documentation, and continuity of supply influence purchasing decisions.

- December 2024: Late 2024 saw a strategic expansion by acquiring Medifill Ltd., expanding its medical-grade adhesive footprint and signaling emphasis on validated materials for healthcare applications. The acquisition supports broader offerings for customers seeking validated materials and tighter supplier integration.

- February 2024: Henkel rolled out a next-generation instant-adhesives line aimed at medical device applications, highlighting ongoing product development around performance and application safety in healthcare assembly. The expansion aligns with validation requirements and repeatable processes for premium formulations.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of cyanoacrylate (instant) adhesives sold for bonding use across North America, counted at the point where the adhesive is supplied into end-use applications across industries.

Scope exclusions: We exclude non-cyanoacrylate chemistries and we do not count downstream assembled product value where the adhesive is only a small input.

Segmentation Overview

- By Product Type

- Alkoxy Ethyl-based

- Ethyl Ester-based

- Methyl Ester-based

- Other Product Types (Bio-based, etc.)

- By End-user Industry

- Transportation

- Footwear and Leather

- Furniture

- Consumer Goods

- Healthcare

- Electronics

- Other End-user Industries (Textile, Marine, etc.)

- By Geography

- United States

- Canada

- Mexico

Data Sources, Market Sizing, and Validation

Desk Research

Desk work started by grounding the demand story for instant-bonding adhesives in North America, then mapping what drives consumption in the main end-use industries. For directional volume and activity signals, we referred to public sources such as US Census manufacturing and trade tables, US International Trade Commission import export statistics, and statistics agencies in Canada and Mexico.

To keep assumptions realistic, technical and regulatory context was also reviewed through sources such as US FDA pages for medical device and biocompatibility related guidance, OSHA hazard communication references, and peer reviewed chemistry and materials journals that discuss cyanoacrylate performance and curing behavior. We also used company filings, investor presentations, association websites, and trusted business press to confirm capacity additions, channel strategy, and product positioning, then supplemented this with paid subscriptions for company financials and intelligence, patent landscapes, and shipment level trade checks where it helped remove ambiguity. These sources are illustrative and not exhaustive, and many other public references were used for data collection, validation, and clarification during the study.

Primary Interviews and Surveys

Primary work was used to test the desk assumptions that most influence value, especially pricing bands by grade, channel markups, and where cyanoacrylates are being substituted by other fastening methods. Interviews and surveys were run across manufacturers, distributors, and large end users, with coverage balanced across the United States, Canada, and Mexico so country-level demand differences did not get averaged out too aggressively.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 14% | |

| Mid tier: 56% | Functional/Unit leaders: 32% | |

| Smaller Players: 16% | Managers: 54% |

Market-Sizing & Forecasting

Sizing was built using top-down and bottom-up logic, where the demand pool is reconstructed from end-use activity in North America and then reconciled back to supply side signals. On the top-down side, we linked cyanoacrylate consumption to indicators such as transportation production and repair activity, electronics assembly output, healthcare device manufacturing trends, and furniture plus consumer goods production. We then adjusted for adhesive intensity and substitution effects by application.

To keep the model practical, a few inputs were treated as the main value drivers, including average selling price by product type (ethyl, alkoxy ethyl, methyl, and other types), the mix shift toward higher value medical and electronics grades, channel structure (direct versus distributor heavy sales), and the pace of lightweight materials adoption that changes bonding needs. Select bottom-up approximations were then used as a check, including sampling supplier revenue exposure to cyanoacrylates, comparing implied regional demand against trade flows for relevant adhesive preparations, and verifying plausible price bands from interviews. When bottom-up coverage had gaps, totals were not force-filled by company rollups and were instead calibrated using the demand indicators and validated pricing ranges.

Forecasting was done using scenario analysis supported by a simple multivariate regression, where growth is linked to the strongest explanatory variables from the history, then stress tested with interview-based expectations on pricing and end use momentum. This approach helped separate real demand growth from price-led expansion, which matters in reactive adhesives where grade mix can shift quickly.

Data Validation & Update Cycle

Outputs were cross checked against independent signals, and any large variance by country or end-use was reviewed before finalizing totals. We also ran consistency checks so that implied pricing, mix shares, and growth by application stayed aligned with what respondents described in the fieldwork.

Before sign off, the model went through multi step analyst review, where assumptions are re-tested and outliers trigger follow-up questions with contacts when needed. Reports are refreshed annually, and interim updates are made when material events occur such as regulatory changes, large capacity moves, or abrupt demand shifts in key end uses. Right before delivery, a fresh final pass is done so clients receive the latest updated view.

Mordor Intelligence's North America Cyanoacrylate Adhesives Market Sizing Compared With Other Published Estimates

Published market values for North America cyanoacrylate adhesives can differ across sources, even when the coverage sounds like it is targeting the same topic. In most cases, the gaps come from how each study treats scope, the year used as the starting point, and the way pricing and end-use demand are translated into a single revenue number.

The main gap usually comes from what is counted inside the cyanoacrylate label. Some estimates blend broader instant adhesive chemistries or include adjacent adhesive and sealant categories, which expands the reported number quickly. Mordor Intelligence counts only cyanoacrylate adhesives and keeps the product type mix (ethyl, alkoxy ethyl, methyl, and others) tied to end-user demand signals across the United States, Canada, and Mexico. Differences can also be driven by aggressive or conservative price progression, currency timing, and whether the model is refreshed to reflect recent shifts in healthcare and electronics grade demand.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 0.79 B (2025) | |

| Trade Journal A | USD 0.86 B (2024) | Uses a different base year and can reflect a broader revenue capture that is closer to supplier reported sales timing, which can lift the value when pricing moved up or when higher value grades gained share. |

| Industry Data Provider B | USD 7.41 B (2023) | Likely includes a wider set of adhesive categories beyond cyanoacrylates and may roll up multiple chemistries or applications under one bucket, which inflates the total compared with a cyanoacrylate-only scope. |

Looking at the spread, scope discipline is the biggest driver, followed by base year alignment and how price and mix shifts are treated. By keeping the inputs traceable to end-use activity and realistic pricing bands, the final number stays easier to replicate and explain during planning and budgeting.

Key Questions Answered in the Report

What is the current size of the cyanoacrylate adhesives market?

The North America Cyanoacrylate Adhesives Market size is at USD 830 million in 2026 and is projected to climb to USD 1.09 billion by 2031.

Which product type dominates cyanoacrylate adhesive sales?

Ethyl Ester-based grades held 46.52% of global revenue in 2025, owing to all-round performance across industrial sectors.

Why are cyanoacrylates gaining popularity in medical procedures?

Medical-grade variants shorten surgery times, reduce infection risk and improve cosmetic results compared with sutures, driving a 6.55% CAGR in healthcare demand

How do VOC regulations affect cyanoacrylate producers?

Stricter emissions caps in the US, Canada and Australia force formulators to develop low-VOC versions and invest in compliance testing, raising production costs.

Which region is expected to grow fastest through 2031?

Mexico leads with a forecast 5.86% CAGR, buoyed by nearshoring and manufacturing expansions serving North American supply chains.

Page last updated on: