Ethnic Foods Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

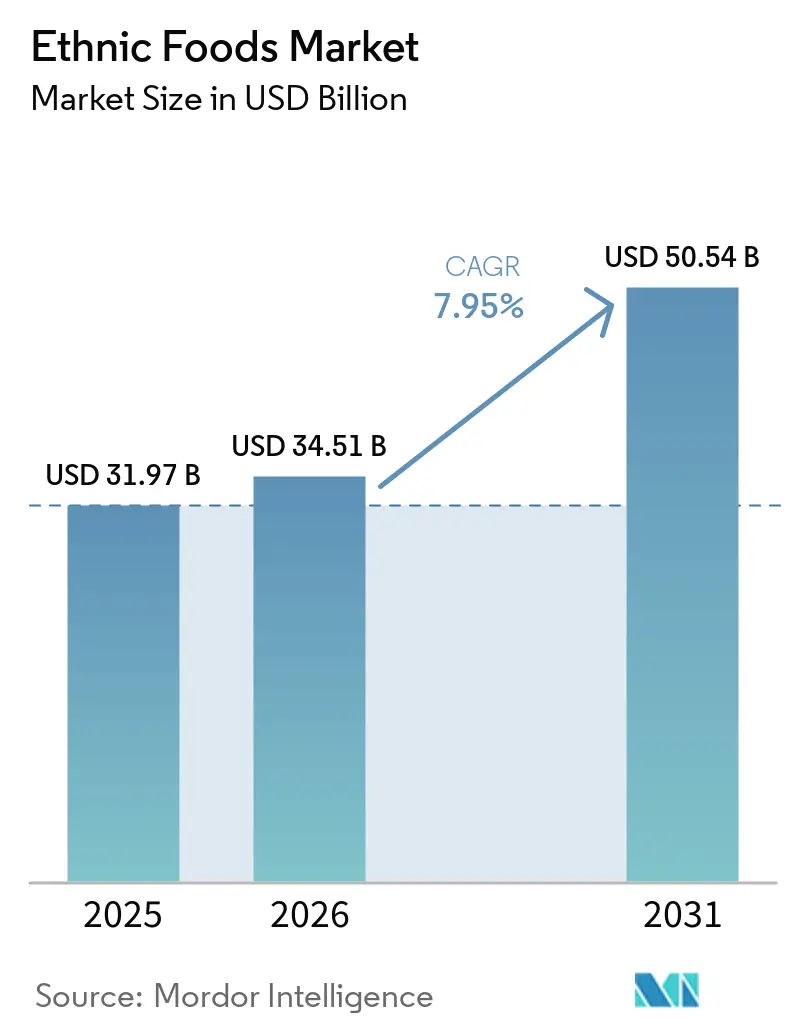

| Market Size (2026) | USD 34.51 Billion |

| Market Size (2031) | USD 50.54 Billion |

| Growth Rate (2026 - 2031) | 7.95% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

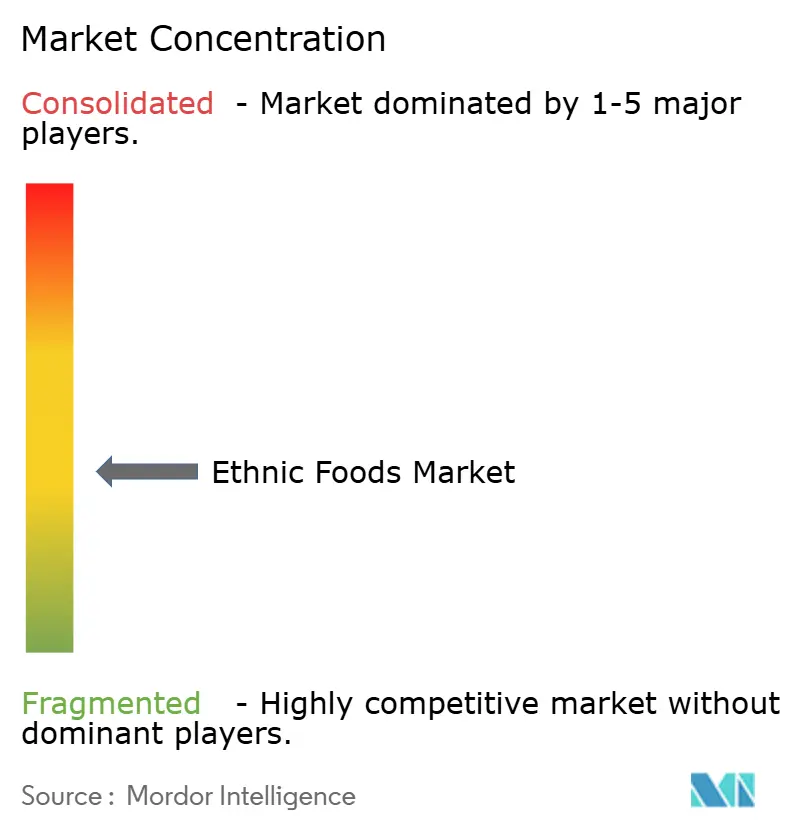

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Ethnic Foods Market Analysis by Mordor Intelligence

Ethnic foods market size in 2026 is estimated at USD 34.51 billion, growing from 2025 value of USD 31.97 billion with 2031 projections showing USD 50.54 billion, growing at 7.95% CAGR over 2026-2031. This trajectory underscores the market's current stature and promising growth outlook. Factors such as rising multicultural populations, increased visibility of global-cuisine SKUs on shelves, and flavor exploration driven by social media are bolstering demand. Concurrently, the expansion of private labels and the surge of e-commerce are intensifying competition. While shelf-stable formats dominate, there's a notable acceleration in frozen innovations as manufacturers address past texture and flavor hurdles. Europe, benefiting from decades of immigration and aligned regulations, leads in revenue. In contrast, the Asia-Pacific region is witnessing the fastest growth, fueled by urbanization and a burgeoning middle class. The competitive landscape is marked by moderate rivalry, with established CPG giants, regional specialists, and digital-first retailers all vying for unique authenticity and distribution approaches.

Key Report Takeaways

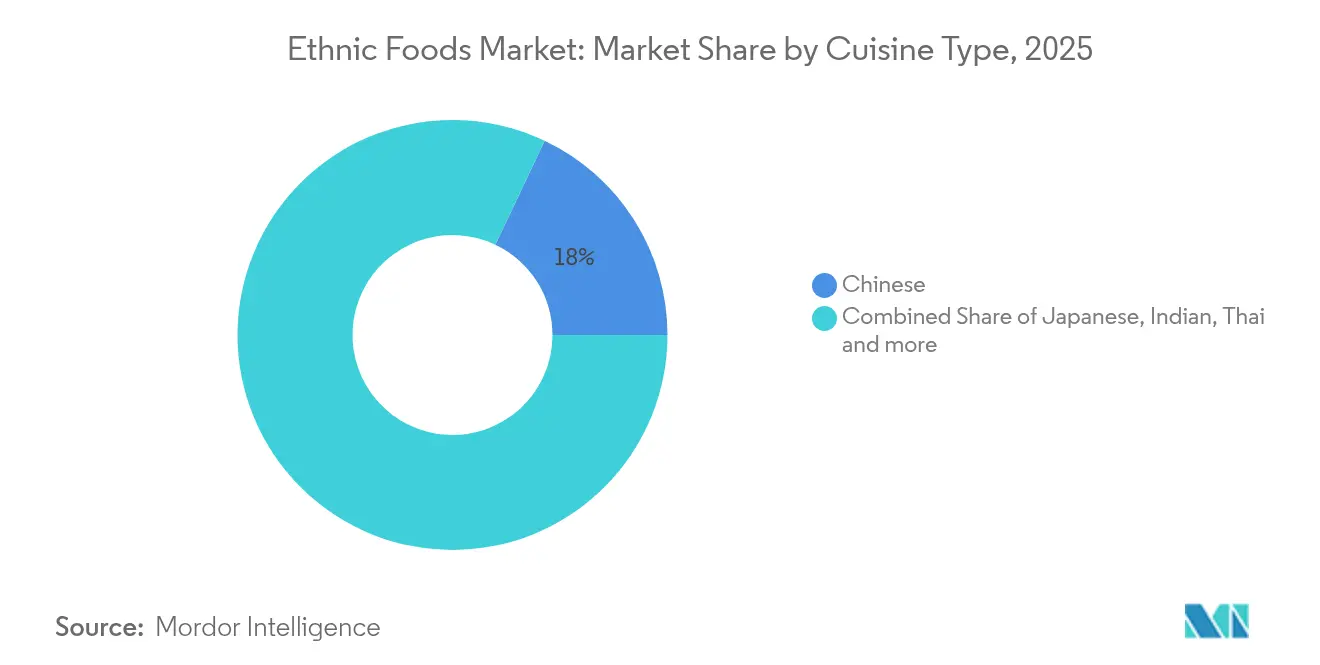

- By cuisine, Chinese food led with an 17.95% market share in the ethnic food market in 2025, while Korean cuisine is forecast to post a 10.30% CAGR through 2031.

- By food type, non-vegetarian products accounted for 67.90% of the ethnic foods market size in 2025, yet vegetarian/vegan lines are expected to expand at an 11.02% CAGR to 2031.

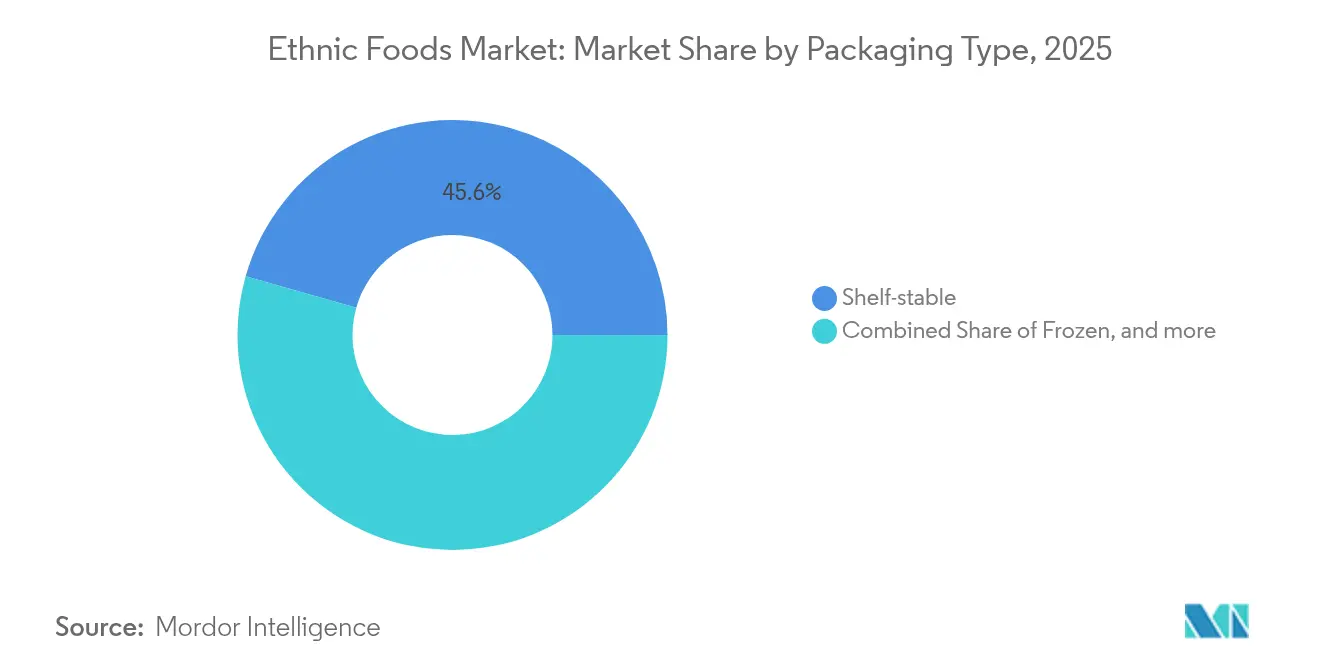

- By packaging, shelf-stable items captured 45.60% share in 2025, and frozen offerings are projected to grow at an 8.35% CAGR over the same period.

- By distribution, supermarkets and hypermarkets held 42.30% revenue share in 2025, whereas online retail is set to rise at a 9.12% CAGR.

- By geography, Europe generated 34.40% of sales in 2025, but Asia-Pacific is on track to advance at a 9.85% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Ethnic Foods Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising multicultural populations in key consuming regions | +2.1% | North America and Europe, with spillover to Australia | Long term (≥ 4 years) |

| Growing penetration of ethnic SKUs on mainstream grocery shelves | +1.8% | Global, with early gains in North America, Western Europe | Medium term (2-4 years) |

| Elevation of flavor exploration via social-media "food tourism" | +1.5% | Global, concentrated in urban markets with high social media penetration | Short term (≤ 2 years) |

| Expansion of private-label global-cuisine lines by big-box retailers | +1.3% | North America and Europe, emerging in Asia-Pacific urban centers | Medium term (2-4 years) |

| Culinary fusion and innovation | +0.9% | Global, led by metropolitan areas and food-forward regions | Medium term (2-4 years) |

| Growth of food festivals and gastronomic events | +0.7% | Global, with concentration in tourism-dependent economies | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rising multicultural populations in key consuming regions

Demographic shifts are fundamentally reshaping food consumption trends in developed markets. Projections from the U.S. Census Bureau indicate that by 2044, minority groups will constitute over half of the U.S. population [1]Source: U.S. Census Bureau, “Projections of the Size and Composition of the U.S. Population”, census.gov. Furthermore, the foreign-born demographic is set to surge by 85%, jumping from 42 million to a projected 78 million by 2060. This demographic evolution isn't merely about numbers; it's fostering a consistent appetite for authentic ingredients and familiar flavors within immigrant communities. At the same time, it's broadening the palate of mainstream consumers, introducing them to a rich tapestry of culinary traditions. Research from the USDA highlights distinct consumption patterns: non-Hispanic Asians have a penchant for fruits and seafood, whereas Hispanics gravitate towards meat. These trends, as noted by the USDA Economic Research Service, are pivotal in driving category expansions. Moreover, immigration trends are cementing a lasting demand for ethnic foods, elevating them from mere luxuries to essential staples, irrespective of economic fluctuations.

Growing penetration of ethnic SKUs on mainstream grocery shelves

Mainstream retailers are broadening their ethnic food selections, moving beyond the confines of traditional specialty aisles. They now view these offerings as key drivers of growth. A case in point is Kroger's debut of the Mercado brand, which showcases over 50 Hispanic-inspired items, ranging from fresh meats to traditional cheeses, underscoring this pivot towards cultural inclusivity. Meanwhile, Walmart's Bettergoods line, boasting 300 products priced between USD 2 and USD 15, highlights how retail giants are making global cuisines more accessible, all while keeping prices competitive. This deeper dive into mainstream retailing sets off a beneficial cycle: as shelf space for ethnic foods expands, non-ethnic consumers are more likely to give them a try. Simultaneously, this heightened visibility draws ethnic shoppers to mainstream retailers, steering them away from niche specialty stores. The approach resonates strongly with younger consumers; data from Intrepid Investment Bankers reveals that 43% prioritize authentic ethnic flavors in their food choices, and 32% are open to paying a premium for them. By integrating ethnic foods into their regular offerings, mainstream retailers are not just diversifying their shelves, they're reshaping consumer habits, turning once-specialty items into everyday staples and significantly broadening their market reach.

Elevation of flavor exploration via social-media "food tourism"

Social media platforms have transformed how consumers discover and engage with ethnic cuisines, birthing a virtual food tourism that influences real-world purchasing decisions. This digitally driven demand surge is underscored by the global Asian food market's leap from USD 154.8 billion in 2023 to a projected USD 268.9 billion by 2032. Hot, spicy, and smoked flavors, as highlighted by Kerry, are at the forefront of consumer preferences. Kerry Group further elucidates this trend, noting measurable market shifts: chili-flavored foods saw a 4% uptick, while spice flavors surged by 5%, underscoring social media's tangible impact on product development and consumer choices. Both Japanese and Korean cuisines are reaping the rewards, with Japanese restaurants outside Japan witnessing a 20% surge and Korean kimchi exports climbing by 10.5%, according to the same source. Social media has elevated ethnic foods from mere sustenance to aspirational lifestyle statements, fostering brand loyalty and a willingness to pay premium prices. This trend isn't limited to individual products; entire cuisine categories are in the spotlight. McCormick's selection of Aji Amarillo as the 2025 Flavor of the Year, predicting a 59% menu growth over four years, serves as a testament to this broader culinary trend [2]Source: McCormick & Company, “Flavor Forecast 25th Edition”, mccormick.com.

Expansion of private-label global-cuisine lines by big-box retailers

Major retailers are reshaping the competitive landscape of ethnic cuisines by adopting private-label strategies, allowing them to boost margins and broaden access. Walmart's launch of "Bettergoods" marks its most significant private-label push in 20 years, aiming at affluent grocery shoppers with a diverse range of products, from culinary delights to plant-based and dietary-specific items. This pivot underscores retailers' realization that ethnic foods can yield better margins than traditional commodities. Moreover, by developing private labels, they can ensure quality and authentic flavors that rival or surpass established brands. The Hispanic grocery market's fragmentation, where leading chains capture just 20-25% of sales, presents a golden opportunity for major retailers to expand their foothold through robust private-label offerings. By introducing private labels, retailers not only make ethnic cuisines more accessible, dispelling the premium pricing of specialty brands, but also enjoy enhanced margins and foster customer loyalty. This trend is gaining momentum as retailers understand that genuine ethnic offerings demand cultural insight and supply chain ties that smaller players find hard to match.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Supply-chain complexity for authentic ingredients | -1.4% | Global, with acute impact in regions distant from ingredient sources | Long term (≥ 4 years) |

| Labelling and regulatory hurdles tied to multi-country ingredient sourcing | -1.1% | North America and Europe, emerging in APAC with stricter standards | Medium term (2-4 years) |

| Maintaining authenticity consistently | -0.8% | Global, particularly challenging in mass-market distribution | Long term (≥ 4 years) |

| Cultural barriers and limited awareness | -0.6% | Regional, concentrated in areas with limited multicultural exposure | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Supply-chain complexity for authentic ingredients

Ethnic food manufacturers, reliant on specific regional ingredients, have found themselves vulnerable amidst global supply chain disruptions, facing ongoing challenges with costs and ingredient availability. The Inquirer reports that the FDA's import alert on Filipino ingredients, such as banana ketchup and bagoong, was triggered by food additives like potassium iodate. This underscores how swiftly regulatory actions can impact entire culinary categories. Roland Foods' market report from March 2025 sheds light on these cascading supply challenges: jasmine rice prices surged by 20% due to droughts in Southeast Asia, and Peruvian anchovy fishing is grappling with a scarcity of raw materials [3]Source: Roland Foods, “March 2025 Regional Market Report”, rolandfoods.com. Manufacturers now face a dilemma: uphold authenticity with costly, limited ingredients or risk consumer backlash by substituting flavors. Adding to the complexity, the FDA's Foreign Supplier Verification Program (FSVP) mandates that importers ensure foreign suppliers align with U.S. safety standards, further straining already challenged supply chains. Roland Foods notes that El Niño weather patterns, impacting key pineapple-producing regions across Indonesia, Thailand, Vietnam, and the Philippines, highlight the challenges posed by climate volatility on the supply of authentic ethnic ingredients.

Labelling and regulatory hurdles tied to multi-country ingredient sourcing

Ethnic food manufacturers face significant compliance challenges due to complex regulatory frameworks across various jurisdictions, especially when sourcing ingredients from diverse geographic origins. The EU mandates, through Regulation (EU) No 1169/2011, that food information be presented in easily understood languages for each member state where products are marketed. Additionally, the European Commission emphasizes specific allergen highlights and nutritional declarations. In the U.S., while FDA regulations stipulate that less than 1% of imported foods undergo physical examination, all are subject to electronic review. However, high-risk ethnic foods face heightened scrutiny and potential delays, as noted by the Association of Food and Drug Officials. From FY2007 to FY2009, the FDA's spice risk profile revealed a 6.6% Salmonella prevalence in imported spices, prompting enhanced testing requirements that drive up costs and extend lead times [4]Source: U.S. Food and Drug Administration, “Risk Profile on Pathogens and Filth in Spices”, fda.gov. The regulatory landscape becomes even more intricate when products incorporate ingredients from multiple countries, each with its own safety standards, labeling mandates, and documentation protocols. This complexity results in an administrative burden that smaller ethnic food companies often find challenging to navigate efficiently.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cuisine Type: Korean Wave Accelerates Global Expansion

In 2025, Chinese cuisine commands a dominant 17.95% market share, thanks to its well-established supply chains and widespread acceptance among diverse demographics. Meanwhile, Korean cuisine is on the rise, boasting the title of the fastest-growing segment with a projected 10.30% CAGR through 2031, a surge largely attributed to the Korean government's "K-Food" initiative. Japanese cuisine enjoys a premium status, bolstered by health-conscious perceptions. In contrast, Thai and Indian cuisines resonate with consumers drawn to authentic spice profiles and vegetarian offerings. North of the border, Mexican cuisine thrives in North American markets, buoyed by demographic trends and robust distribution networks.

Korean cuisine's meteoric rise isn't just a stroke of luck; it's the result of concerted efforts from both the government and private sectors. Notably, these exports saw a 10.5% uptick in recent times, as highlighted by the Kerry Group. The Korean Ministry of Agriculture, under its 4th Food Industry Promotion Basic Plan (2023-2027), is pushing for food tech innovations and bolstering K-Food exports. This institutional backing stands in stark contrast to the support that smaller culinary categories often miss out on. Meanwhile, Brazilian and Lebanese cuisines are emerging as the next big opportunities, especially as younger consumers turn to social media to explore diverse flavor profiles. The performance of the "Others" category underscores a trend: as diners venture beyond mainstream ethnic offerings, there's a burgeoning space for niche cuisine specialists to thrive.

By Food Type: Plant-Based Revolution Transforms Traditional Categories

In 2025, non-vegetarian ethnic foods command a dominant 67.90% market share, underscoring deep-rooted consumer preferences for meat-centric dishes. Meanwhile, vegetarian and vegan ethnic foods are on a rapid ascent, boasting an 11.02% CAGR projected through 2031. This surge, fueled by rising health consciousness, environmental concerns, and the need to cater to dietary restrictions, outpaces the overall market's growth rate, signaling a notable shift in consumer behavior and a pivot in product innovation. The plant-based movement in ethnic cuisine isn't merely about replacing meat; it's a celebration of authentic vegetarian traditions from diverse cultures.

Cuisines like Indian, Thai, and Mediterranean naturally offer these plant-centric options. Looking ahead to 2025, food trend analyses reveal that over 75% of consumers prioritize food seasonality and regional sourcing. Notably, as highlighted by BIOFACH, there's a marked uptick in the consumption of plant-based alternatives. Among these, frozen plant-based ethnic products are particularly surging in popularity. Millennials, with their penchant for sustainability, are at the forefront of this demand, evidenced by companies like Planet Based Foods rolling out innovative offerings like hemp-based taquitos. This segment's robust growth mirrors a broader dietary evolution towards flexitarianism, where consumers are moderating, rather than completely forgoing, meat. This shift ensures a steady appetite for premium plant-based ethnic alternatives.

By Packaging Type: Frozen Segment Gains Momentum Through Innovation

In 2025, shelf-stable packaging commands a dominant 45.60% market share, capitalizing on cost benefits, prolonged shelf life, and a well-established distribution network tailored for the intricate ingredient profiles of ethnic foods. Meanwhile, the frozen packaging segment is on a rapid ascent, projected to grow at an 8.35% CAGR through 2031, fueled by rising demands for convenience and the need to preserve authentic flavors and textures. Refrigerated and chilled packaging caters to premium markets that prioritize fresh ingredients, while the "Others" category highlights emerging packaging innovations tailored to specific ethnic food needs.

Technological advancements in freezing methods now allow for the preservation of authentic textures and flavors, a feat once only possible with fresh preparations. Conagra Brands' Future of Frozen Food 2025 report spotlights global cuisine trends, noting a staggering 375% growth in Asian-inspired frozen appetizers, such as dumplings and wontons, over just four years . Furthermore, with consumers increasingly desiring restaurant-quality results at home, air fryer compatibility has emerged as a pivotal consideration in the development of frozen ethnic foods, leading to a surge in products tailored for air frying, as highlighted by Conagra Brands.

By Distribution Channel: E-Commerce Disrupts Traditional Retail Models

In 2025, supermarkets and hypermarkets command a 42.30% market share, leveraging their expansive shelf space, competitive pricing, and the allure of one-stop shopping. This strategy resonates with mainstream consumers eager to explore ethnic cuisines. Meanwhile, online retail is on a robust trajectory, growing at a 9.12% CAGR and projected to continue through 2031. This surge is fueled by the availability of specialty products, innovative subscription models, and direct-to-consumer relationships—an area where traditional retailers find it challenging to compete. While convenience and grocery stores cater to immediate consumption needs, specialty stores carve out their niche through expertise and a curated selection of authentic products.

The rise of online channels underscores a shift in ethnic food shopping habits, especially among younger consumers who are not only tech-savvy but also on the lookout for products that local stores don't stock. A testament to this trend is Weee!, which has successfully raised over USD 800 million and boasts a portfolio of over 15,000 ethnic products. This underscores the potential of specialized e-commerce platforms in catering to multicultural communities, often outpacing traditional retailers. Adding to Weee!'s momentum is the strategic appointment of former Amazon CEO Jeff Wilke as an advisor, hinting at the platform's aspirations for operational scaling and bolstered supply chain capabilities. In response to these shifts, traditional retailers are not standing still. They're broadening their multicultural offerings and ramping up e-commerce initiatives. Notable moves include Kroger's launch of a Hispanic concept store in Houston and Walmart's introduction of the Bettergoods private label, aimed at attracting a more affluent demographic.

Geography Analysis

In 2025, Europe commands a 34.40% share of the market, a testament to its long-standing multicultural integration and adept food distribution systems catering to diverse ethnic communities. The EU's Regulation (EU) No 1169/2011, which focuses on food information for consumers, establishes unified standards. These standards not only bolster the cross-border trade of ethnic foods but also prioritize consumer safety, mandating allergen labeling and nutritional declarations as directed by the European Commission. Germany, the UK, and France, buoyed by established immigrant communities and a mainstream embrace of ethnic cuisines, lead in consumption. Meanwhile, Eastern European nations are increasingly welcoming global flavors. The region's seasoned market dynamics lean towards premium offerings and authentic ingredient sourcing, presenting avenues for specialized ethnic food enterprises. These companies, adept at navigating intricate regulatory landscapes, also prioritize cultural authenticity.

Asia-Pacific is set to outpace others, boasting a robust 9.85% CAGR through 2031. This surge is fueled by swift urbanization, a burgeoning middle class, and heightened exposure to global cuisines, thanks to digital media and travel. In China, the spotlight is on online retail and venturing into smaller cities. Conversely, India's trajectory is shaped by traditional retail's dominance and rising disposable incomes. Japan, grappling with demographic hurdles and a mature market, showcases slower growth but stands out as a pivotal export hub for genuine Asian ingredients. South Korea's growth narrative is driven by a penchant for convenience and online grocery shopping, bolstered by state-backed initiatives championing K-Food exports. In Indonesia, where traditional trade holds an 80% market share, there's a pronounced potential for organized retail growth and the evolution of the ethnic food segment.

North America's market is buoyed by ongoing demographic diversification. Projections from the U.S. Census Bureau indicate the Hispanic population could touch 22% by 2028. Furthermore, the foreign-born demographic is set to swell from 42 million to a staggering 78 million by 2060. This diversification fuels the multicultural grocery market's annual growth, with Hispanic consumers playing a pivotal role. Not only do they significantly contribute to the GDP, but they also outspend their non-Hispanic counterparts on food, as highlighted by Progressive Grocer. In Canada, government-backed multiculturalism and immigration policies bolster the ethnic food market. Asian consumers, as noted by Alberta Agriculture and Forestry, are gravitating towards tropical fruits, pork, poultry, and fish, while curbing their beef consumption. Meanwhile, Mexico's burgeoning middle class, coupled with its closeness to U.S. markets, presents a dual opportunity: domestic consumption and export-driven ethnic food production. However, emerging tariff policies could reshape the landscape of cross-border trade.

Competitive Landscape

The ethnic foods market remains moderately fragmented. This fragmentation arises from a long tail of regional specialists, which curtails the dominance of major players. Yet, it simultaneously opens avenues for both consolidation and niche expansion. Market leaders, such as Ajinomoto Co., Inc., McCormick & Company, General Mills, ARYZTA AG, and Associated British Foods, adopt varied strategies. Some emphasize authentic ingredient expertise, while others focus on mainstream distribution. Ajinomoto stands out with its innovation-driven approach. In 2023, it expanded gyoza production in Europe by inaugurating a new facility in France. Furthermore, in July 2025, it rolled out the Palate Perfect FL-TM fermented tomato flavor, a move aimed at tackling supply chain hurdles and catering to the rising demand for clean labels.

In this competitive arena, technology adoption emerges as a pivotal strategy for capturing market share. Companies are channeling investments into areas like supply chain transparency, flavor authentication technologies, and direct-to-consumer platforms, effectively sidestepping traditional retail constraints. Meanwhile, emerging disruptors are making waves, positioning themselves as specialists. Their emphasis on cultural authenticity strikes a chord with both ethnic communities and mainstream consumers, all in pursuit of genuine experiences. Notably, there's a surge of private equity interest in family-owned ethnic food brands. This trend underscores a broader recognition: authenticity, a hallmark of these brands, remains elusive for larger CPG companies. Such dynamics present enticing acquisition prospects for established players eager to broaden their ethnic food portfolios, as highlighted by Intrepid Investment Bankers.

Underserved cuisine categories, plant-based ethnic alternatives, and premium frozen offerings that promise restaurant-quality standards present abundant white-space opportunities. These segments remain relatively untapped, offering significant potential for innovation and market expansion. Companies that skillfully blend cultural authenticity with mainstream appeal are gaining an edge in the competitive landscape, as consumers increasingly seek diverse and high-quality food options. However, as these companies grapple with the intricacies of sourcing ingredients from multiple countries, they must prioritize regulatory compliance, particularly with frameworks such as the FDA's Foreign Supplier Verification Program. Ensuring adherence to such regulations is critical to maintaining product integrity and consumer trust.

Ethnic Foods Industry Leaders

Ajinomoto Co. Inc.

McCormick & Company Inc.

General Mills, Inc.

Associated British Foods PLC

ARYZTA AG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Mizkan Corporation launched "鍋THE WORLD" hot pot series, incorporating global cuisine essences including Manhattan clam chowder, Marseille bouillabaisse, and Korean yukgaejang flavors, addressing consumer boredom with traditional options while expanding the hot pot market beyond conventional boundaries.

- July 2025: Ajinomoto Health and Nutrition introduced Palate Perfect FL-TM fermented tomato flavor, designed to replace high-value ingredients like tomato puree while addressing California tomato crop shortages, demonstrating cost-in-use efficiency for food manufacturers.

- January 2025: McCormick unveiled Aji Amarillo as the 2025 Flavor of the Year, launching new seasoning products and hosting Miami Flavor Night Market to promote the Peruvian pepper expected to achieve 59% menu growth over four years.

- October 2024: Nestlé announced strategic expansion into the USD 110 billion global cuisine market through enhanced Mexican and Asian food brand offerings, reflecting the company's commitment to capturing ethnic food growth opportunities.

Global Ethnic Foods Market Report Scope

Ethnic food refers to a wide variety of packaged foodstuffs that can be identified by the public mind as coming from a foreign source.

The ethnic foods market is segmented by distribution channel into hypermarkets/supermarkets, convenience stores, online stores, and other distribution channels. By geography, the market is segmented into North America, Europe, Asia-Pacific, and Rest of the World. For each segment, the market sizing and forecasts have been done in value terms (USD million).

| Chinese |

| Japanese |

| Indian |

| Thai |

| Korean |

| Mexican |

| Brazilian |

| Lebanese |

| Others |

| Vegetarian/Vegan Ethnic Foods |

| Non-Vegetarian Ethnic Foods |

| Shelf-stable |

| Frozen |

| Refrigerated/Chilled |

| Others |

| Supermarkets/Hypermarkets |

| Convenience/Grocery Stores |

| Specialty Stores |

| Online Retail |

| Other Retail Channels |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| Italy | |

| France | |

| Spain | |

| Netherlands | |

| Poland | |

| Belgium | |

| Sweden | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| Indonesia | |

| South Korea | |

| Thailand | |

| Singapore | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Colombia | |

| Chile | |

| Peru | |

| Rest of South America | |

| Middle East and Africa | South Africa |

| Saudi Arabia | |

| United Arab Emirates | |

| Nigeria | |

| Egypt | |

| Morocco | |

| Turkey | |

| Rest of Middle East and Africa |

| By Cuisine Type | Chinese | |

| Japanese | ||

| Indian | ||

| Thai | ||

| Korean | ||

| Mexican | ||

| Brazilian | ||

| Lebanese | ||

| Others | ||

| By Food Type | Vegetarian/Vegan Ethnic Foods | |

| Non-Vegetarian Ethnic Foods | ||

| By Packaging Type | Shelf-stable | |

| Frozen | ||

| Refrigerated/Chilled | ||

| Others | ||

| By Distribution Channel | Supermarkets/Hypermarkets | |

| Convenience/Grocery Stores | ||

| Specialty Stores | ||

| Online Retail | ||

| Other Retail Channels | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| Italy | ||

| France | ||

| Spain | ||

| Netherlands | ||

| Poland | ||

| Belgium | ||

| Sweden | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Indonesia | ||

| South Korea | ||

| Thailand | ||

| Singapore | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Colombia | ||

| Chile | ||

| Peru | ||

| Rest of South America | ||

| Middle East and Africa | South Africa | |

| Saudi Arabia | ||

| United Arab Emirates | ||

| Nigeria | ||

| Egypt | ||

| Morocco | ||

| Turkey | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

How large is the packaged ethnic foods market in 2026?

The ethnic foods market stands at USD 34.51 billion in 2026 and is forecast to reach USD 50.54 billion by 2031.

Which cuisine is growing fastest within packaged ethnic foods?

Korean cuisine is projected to post the quickest growth at a 10.30% CAGR through 2031.

What packaging format is gaining share the fastest?

Frozen ethnic products are expanding at an 8.35% CAGR as technology improvements boost quality and convenience.

Which region offers the strongest growth outlook?

Asia-Pacific is set to advance at a 9.85% CAGR thanks to urbanization, rising incomes, and online grocery adoption.

Page last updated on: