Epichlorohydrin Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

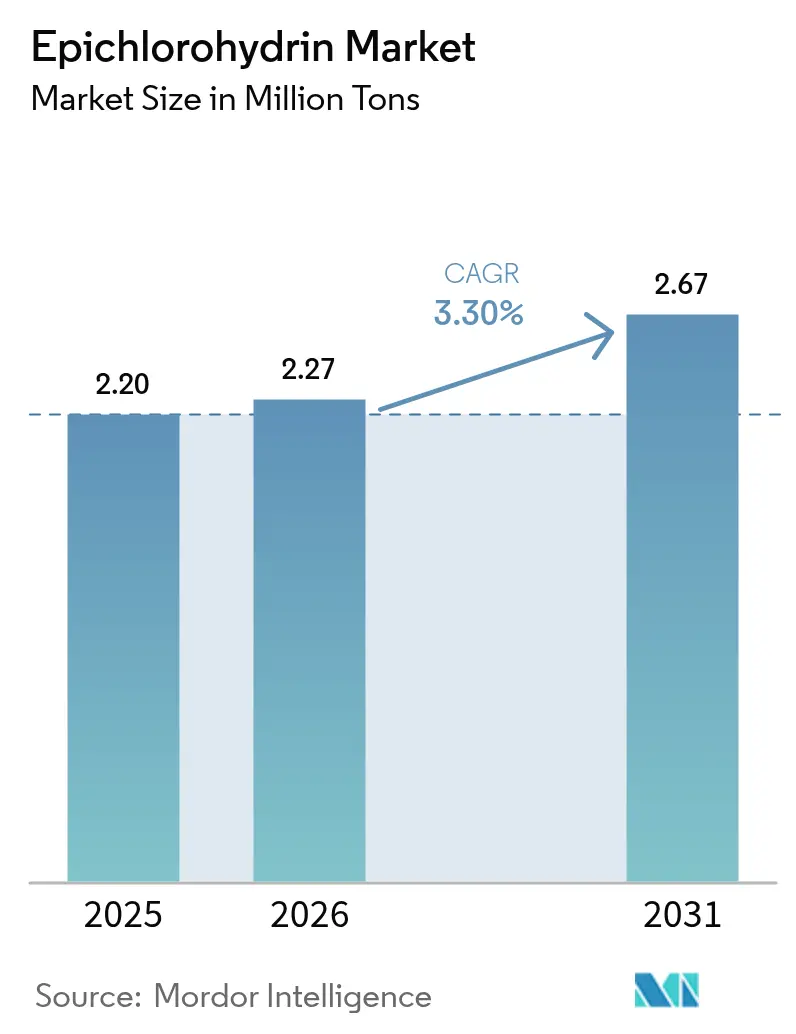

| Market Volume (2026) | 2.27 Million tons |

| Market Volume (2031) | 2.67 Million tons |

| Growth Rate (2026 - 2031) | 3.30% CAGR |

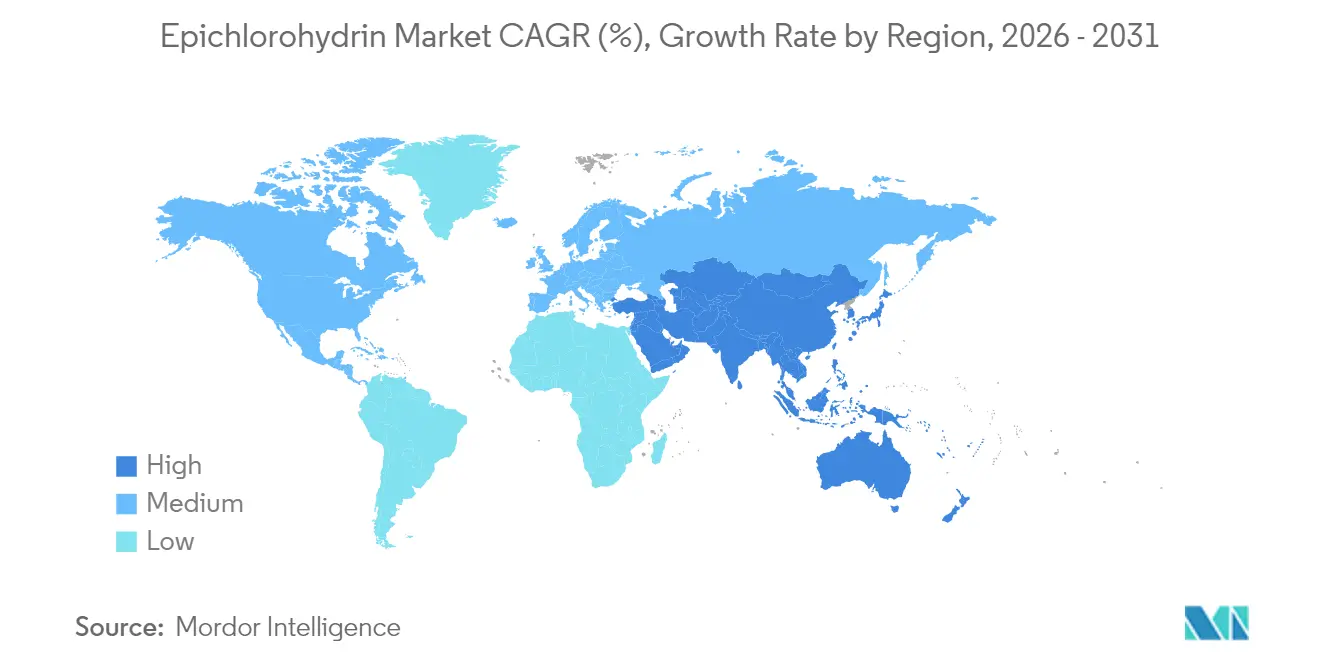

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

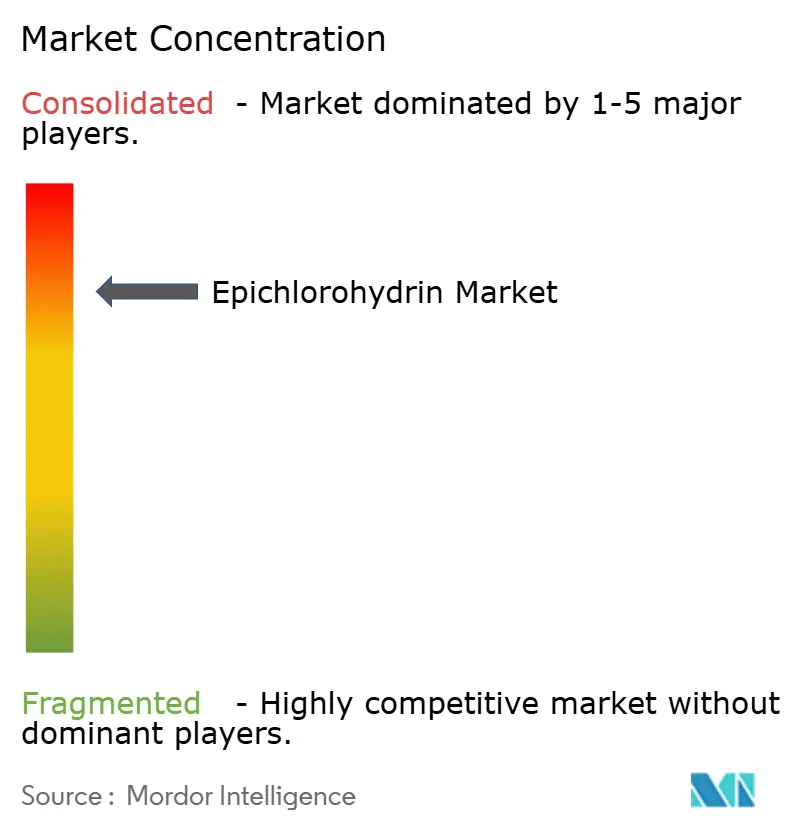

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Epichlorohydrin Market Analysis by Mordor Intelligence

Epichlorohydrin Market size in 2026 is estimated at 2.27 Million tons, growing from 2025 value of 2.20 Million tons with 2031 projections showing 2.67 Million tons, growing at 3.30% CAGR over 2026-2031. Volume growth stems mainly from the expanding epoxy resin sector, new capacity additions in Asia-Pacific, and increasing substitution of petroleum routes with glycerin-based processes. Industry participants are extending vertical integration into downstream epoxy resins to buffer raw-material swings, while investments in renewable feedstock technologies reduce compliance costs in regions tightening emission limits. Although North America and Europe contend with higher energy costs and stricter air-pollution rules, global construction activity, renewable-energy installations, and semiconductor device miniaturization continue to widen application breadth and sustain long-term demand for epichlorohydrin.

Key Report Takeaways

- By type, oil-based grades retained an 87.78% epichlorohydrin market share in 2025; bio-based grades are poised to advance at a 3.96% CAGR through 2031, outpacing the overall market.

- By application, epoxy resins captured 86.20% of the epichlorohydrin market size in 2025 and are set to expand at a 3.92% CAGR to 2031.

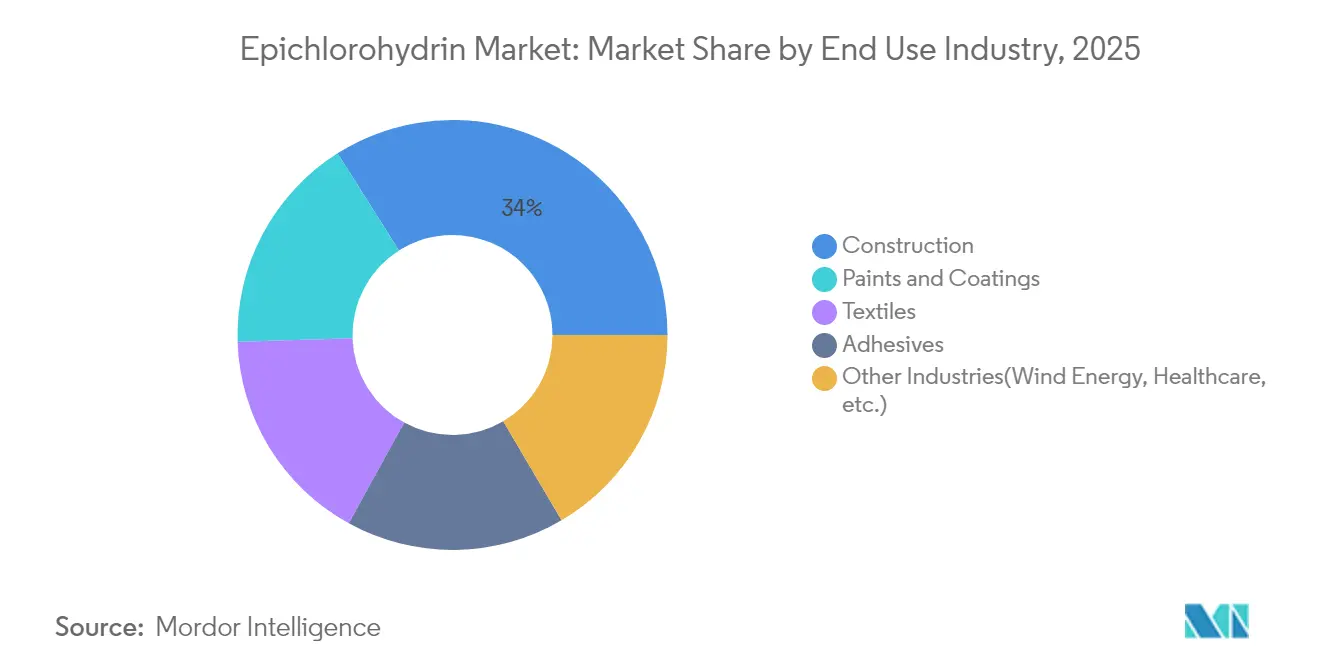

- By end-use, construction accounted for 33.98% of epichlorohydrin demand in 2025, while wind-energy and healthcare uses together register the swiftest 4.04% CAGR to 2031.

- By geography, Asia-Pacific commanded 58.72% of global demand in 2025 and is projected to grow the fastest at 4.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Epichlorohydrin Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Bio-based feedstock shift | +0.7% | Global; early gains in Asia-Pacific | Medium term (2-4 years) |

| Rising epoxy resin demand | +1.2% | Global | Short term (≤ 2 years) |

| Construction activity rebound | +0.5% | Asia-Pacific; North America | Medium term (2-4 years) |

| Wind-turbine blade manufacturing | +0.4% | Europe; North America; China | Medium term (2-4 years) |

| Growing investment in semiconductor encapsulation | +0.3% | Asia-Pacific, North America | Short term (≤2 yrs) |

| Source: Mordor Intelligence | |||

Bio-based Feedstock Availability Spurs Sustainable Growth

A widening surplus of crude glycerin from biodiesel has bolstered the economic case for glycerin-to-epichlorohydrin production. Plants using Epicerol technology cut CO₂ emissions by 60% and wastewater generation by up to forty-fold compared with propylene routes, meeting tightening carbon regulations and qualifying for green-chemistry incentives. Production costs around EUR 1,697 / ton are now within striking distance of prevailing market prices, narrowing the profitability gap as glycerin prices soften. AGC Chemicals Europe commercialized EPINITY in 2024, and Epigral Limited entered domestic manufacturing in India using the same technology, underlining accelerated adoption. As more jurisdictions impose lifecycle-carbon disclosures, bio-based epichlorohydrin gives producers a credible pathway to secure long-term offtake agreements with sustainability-focused customers.

Escalating Epoxy Resin Consumption Amplifies Core Demand

Epoxy resins absorb over 86% of global epichlorohydrin output, anchoring baseline growth for the epichlorohydrin market. Infrastructure upgrades, protective industrial coatings, and advanced composites for automotive and aerospace continue to widen epoxy use, while electronics miniaturization demands high-purity, low-chlorine resin grades. DCM Shriram’s USD 120 million epoxy resin complex in Gujarat exemplifies regional backward integration designed to secure captive epichlorohydrin supply. As coating manufacturers introduce water-borne and solvent-free lines to meet volatile-organic-compound rules, epoxy demand per square meter rises, lengthening the growth runway through 2030.

Construction Sector Expansion Underpins Volume Uptake

Although higher interest rates moderated Western housing starts in 2024, stimulus programs in China, India, and the United States keep large-scale transportation, commercial, and residential projects moving forward. Durable flooring, corrosion-resistant rebar coatings, and epoxy-bonded structural adhesives all rely on epichlorohydrin-derived resins. Government mandates for longer design lives and lower maintenance costs push builders toward epoxy systems with certified environmental product declarations, reinforcing steady consumption even during cyclical downturns. The segment retains the single-largest share of end-use demand, ensuring that construction activity remains a dependable load for future capacity expansions.

Wind-Energy Blade Manufacturing Extends Application Scope

Global targets for renewable power have accelerated wind-farm deployments, boosting composite-blade demand. Epichlorohydrin-based epoxy matrices deliver the high glass-transition temperature and fatigue resistance required for ever-longer blades. Recent laboratory results show that disulfide epoxy additives create covalent-adaptable networks, enabling blade sections to be reprocessed while retaining structural integrity. Such recyclability addresses growing concern over blade landfill waste, and regulatory pressure for end-of-life solutions is expected to channel additional volumes toward next-generation epoxy systems.

Restraint Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Raw-material price volatility | -0.6% | Global | Short term (≤ 2 years) |

| Environment-related compliance costs | -0.8% | North America; Europe | Long term (≥ 4 years) |

| Rising adoption of non-epoxy aliphatic resins | -0.3% | Europe, North America | Long term (≥5 yrs) |

| Source: Mordor Intelligence | |||

Feedstock Price Fluctuations Pressure Margins

Propylene and caustic soda prices continued to swing widely in 2024, reflecting global energy-price uncertainty and periodic outages in chlor-alkali units. While Asian suppliers temporarily benefited from lower production costs, European producers grappled with high electricity tariffs, compressing spreads. Firms with integrated chlor-alkali assets have partially offset volatility, yet unhedged producers face margin squeeze that can delay debottlenecking plans. Bio-based units provide an alternate cost base but remain exposed to glycerin pricing tied to biodiesel policies. Hedging strategies and diversified sourcing therefore stay at the forefront of procurement practices during 2025-2026.

Tightening Environmental Regulations Elevate Compliance Burden

The US EPA’s 2024 amendments to NESHAP and NSPS mandate additional vent controls that collectively shave 1,372 tons per year of hazardous air pollutant emissions from chemical facilities[1]Environmental Protection Agency, “Regulatory Impact Analysis for the Final New Source Performance Standards for the Synthetic Organic Chemical Manufacturing Industry and National Emission Standards for Hazardous Air Pollutants for the Synthetic Organic Chemical Manufacturing Industry and Group I & II Polymers and Resins Industry,” epa.gov . Similar provisions in Canada now require notification for consumer-product uses exceeding 0.1% epichlorohydrin w/w [2]Government of Canada, “Order 2024-87-20-01 Amending the Domestic Substances List,” gazette.gc.ca. Capital expenditures for scrubbers, flare systems, and leak-detection upgrades raise operating costs and favor plants with modern, low-emission designs or renewable feedstock pathways. While these rules improve community health outcomes, they can weigh on near-term profitability and nudge marginal production toward regions with lighter regulatory footprints.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Bio-Based Grades Gain Momentum

Oil-derived epichlorohydrin retained an 87.78% share of global consumption in 2025, equating to 1,931.16 kilotons, yet bio-based volumes grew faster, closing the year at 268.84 kilotons. The epichlorohydrin market size attributable to bio-based production is expected to expand at 3.96% CAGR, lifted by policy incentives for low-carbon chemicals and expanding glycerin availability from biodiesel streams. In contrast, the oil-based route is projected to trail the overall epichlorohydrin market by nearly 70 basis points in growth due to escalating carbon fees in Europe and the gradual shift of multinational customers toward greener supply chains.

Producers employing Epicerol technology consistently report 60% lower greenhouse-gas footprints and up to forty-fold reductions in wastewater discharge relative to the allyl-chlorination pathway. Early adopters in Asia, most notably in Thailand and India, demonstrate that bio-based units can reach economies of scale above 50 ktpa, encouraging other chlor-alkali firms to license similar technology. Over the forecast horizon, incremental efficiency gains and potentially lower glycerin prices may compress the cost premium, enabling bio-based grades to penetrate niche electronic encapsulation lines where ultra-low chlorine is pivotal.

By Application: Epoxy Resins Preserve Dominance

Epoxy resins absorbed 1,896.4 kilotons in 2025, translating to 86.20% of total demand. Their 3.92% CAGR through 2031 ensures that the epichlorohydrin market continues to track epoxy sector growth. Construction, protective coatings, and electrical laminates lead volume uptake, while advanced composites in aerospace and wind energy supply higher-value grades. The epichlorohydrin market share associated with water-treatment flocculants remains modest but stable, as stringent potable-water standards limit allowable monomer residues.

Semiconductor encapsulation represents a fast-growing, premium niche. Patent filings describing low-ppm-chlorine epoxy systems underscore the industry’s quest for higher thermal conductivity and minimal warpage during reflow soldering. Although volumes are comparatively small, their elevated margins influence producers to maintain dedicated purification trains. Meanwhile, regulatory scrutiny over potential monomer migration in potable water spurs continuous R&D into ultra-low-residual processes, preserving the epichlorohydrin industry’s relevance in safety-critical applications.

By End-Use Industry: Construction Retains Lead despite Headwinds

The construction sector drew down 747.56 kilotons of epichlorohydrin-derived products in 2025, or 33.98% of global demand. Urban infrastructure projects in India and Southeast Asia offset softer residential spending in Europe, allowing the segment to post modest year-on-year growth. Interior floor coatings, chemical-resistant grout, and epoxy-bonded concrete overlays anchor baseline consumption, while government mandates for green building materials promote low-VOC, high-solids formulations that intensify epichlorohydrin usage per finished surface.

Paints and coatings ranked second and benefited from a swift rebound in automotive OEM production and defense spending. Adhesives for engineered wood and structural assemblies maintained mid-single-digit growth, illustrating ongoing substitution of solvent-borne systems. Emerging sectors—wind-energy composites, medical devices, and specialty elastomers, together tally the fastest 4.04% CAGR. Manufacturers targeting these niches deploy grade differentiation strategies such as ultrapure or elastomer-modified epoxies to secure higher contribution margins, thereby diversifying revenue streams beyond cyclical construction trends.

Geography Analysis

Asia-Pacific led global demand with 1,291.84 kilotons in 2025, equating to 58.72% of the epichlorohydrin market. Continued 4.12% CAGR growth arises from robust downstream epoxy resin expansion, capacity investments in India, and Chinese industrial policy emphasizing self-reliance in advanced materials. Regional producers benefit from access to competitively priced propylene and supportive infrastructure investment, enhancing supply-chain agility. The epichlorohydrin market size in Asia-Pacific is therefore expected to widen its lead over other regions by 2031.

North America retains significant high-value consumption in aerospace composites, semiconductor encapsulation, and specialty coatings. However, emission-control retrofits mandated under revised EPA rules introduce capital expenditures that may encourage incremental imports of bio-based grades produced in Asia. Europe confronts parallel challenges: high energy costs, slower GDP growth, and stringent carbon-pricing schemes compress margins, prompting consolidation of smaller epoxy formulators. Nevertheless, EU funding for offshore-wind build-outs and battery gigafactories ensures selective demand pockets for premium epichlorohydrin derivatives.

Latin America, the Middle East, and Africa collectively account for less than 10% of global volumes but present long-term potential. Brazil’s infrastructure concessions and Saudi Arabia’s chemical diversification agendas create localized demand clusters. While per-capita consumption is currently low, rising urbanization and renewable-energy targets promise incremental growth that global suppliers may capture by deploying import terminals and regional blending hubs.

Competitive Landscape

The global epichlorohydrin market is concentrated, with key players leveraging vertical integration to mitigate feedstock cost volatility and secure captive outlets. AGC’s chlor-alkali network in Southeast Asia supports domestic and export markets, while its EPINITY line enhances sustainability. Indian producers like Epigral are expanding rapidly, as the company has approved a 100 ktpa capacity increase at Dahej to meet domestic and export demand. Technology licensors like Technip Energies drive sustainability with glycerin-based processes. Strategic priorities include optimizing brownfield assets, co-locating near renewable energy hubs, and using biogenic feedstock to meet targets, while partnerships with downstream sectors boost demand and cross-selling opportunities.

Epichlorohydrin Industry Leaders

Solvay

Sumitomo Chemical Co., Ltd.

Olin Corporation

Shandong Haili Chemical Industry Co., Ltd.

Grasim Industries Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2024: Epigral's Board greenlit a plan to double the Epichlorohydrin capacity at its Dahej facility in Gujarat. The capacity will be boosted by 50,000 TPA, bringing the total to 100,000 TPA, anticipating a surge in demand in the coming years.

- February 2024: DCM Shriram Chemicals invested USD 120 million in an epoxy resin plant, complementing its integrated epichlorohydrin (ECH) plant. The ECH plant is scheduled for completion in 2025.

Global Epichlorohydrin Market Report Scope

Epichlorohydrin is a highly reactive chemical intermediate. In its pure form, epichlorohydrin is a clear, colorless liquid. The presence of an epoxide ring and a chlorine atom in the molecule allows epichlorohydrin to readily undergo various chemical reactions with many types of compounds, earning its widespan use as a chemical intermediate. The epichlorohydrin market is segmented by product, type, application, and geography. By product, the market is segmented into epichlorohydrin. By type, the market is segmented into oil-based epichlorohydrin and bio-based epichlorohydrin. By application, the market is segmented into epoxy resins, synthetic glycerin, epichlorohydrin elastomers, specialty water treatment chemicals, and other applications. The report also covers the market size and forecasts for the epichlorohydrin market in 13 countries across major regions. For all the above segments, market sizing and forecasts have been done on the basis of volume (kiloton).

| Oil-based epichlorohydrin |

| Bio-based epichlorohydrin |

| Epoxy Resins |

| Specialty Water Treatment Chemicals |

| Synthetic Glycerin |

| Epichlorohydrin Elastomers |

| Other Applications(Pharmaceuticals, etc.) |

| Construction |

| Paints and Coatings |

| Adhesives |

| Textiles |

| Other Industries(Wind Energy, Healthcare, etc.) |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Type | Oil-based epichlorohydrin | |

| Bio-based epichlorohydrin | ||

| By Application | Epoxy Resins | |

| Specialty Water Treatment Chemicals | ||

| Synthetic Glycerin | ||

| Epichlorohydrin Elastomers | ||

| Other Applications(Pharmaceuticals, etc.) | ||

| By End-Use Industry | Construction | |

| Paints and Coatings | ||

| Adhesives | ||

| Textiles | ||

| Other Industries(Wind Energy, Healthcare, etc.) | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected growth rate for the epichlorohydrin market between 2026 and 2031?

The epichlorohydrin market is expected to expand at a 3.30% CAGR, rising from 2.27 million tons in 2026 to 2.67 million tons in 2031.

Which application will drive the largest epichlorohydrin volume through 2031?

Epoxy resins will remain the dominant application, accounting for more than 86% of demand and growing at 3.92% CAGR.

Why is Asia-Pacific the leading regional consumer of epichlorohydrin?

Rapid industrialization, substantial construction spending, and expanding epoxy resin capacity give Asia-Pacific a 58.72% share of global demand, the highest worldwide.

What regulatory trends are shaping future supply strategies?

Tighter air-pollutant limits in North America and Europe and Canada’s new-activity reporting requirements are pressing producers to adopt cleaner technologies and bio-based feedstocks.

Page last updated on: