End-of-Line Automation And Integrated Case Handling Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

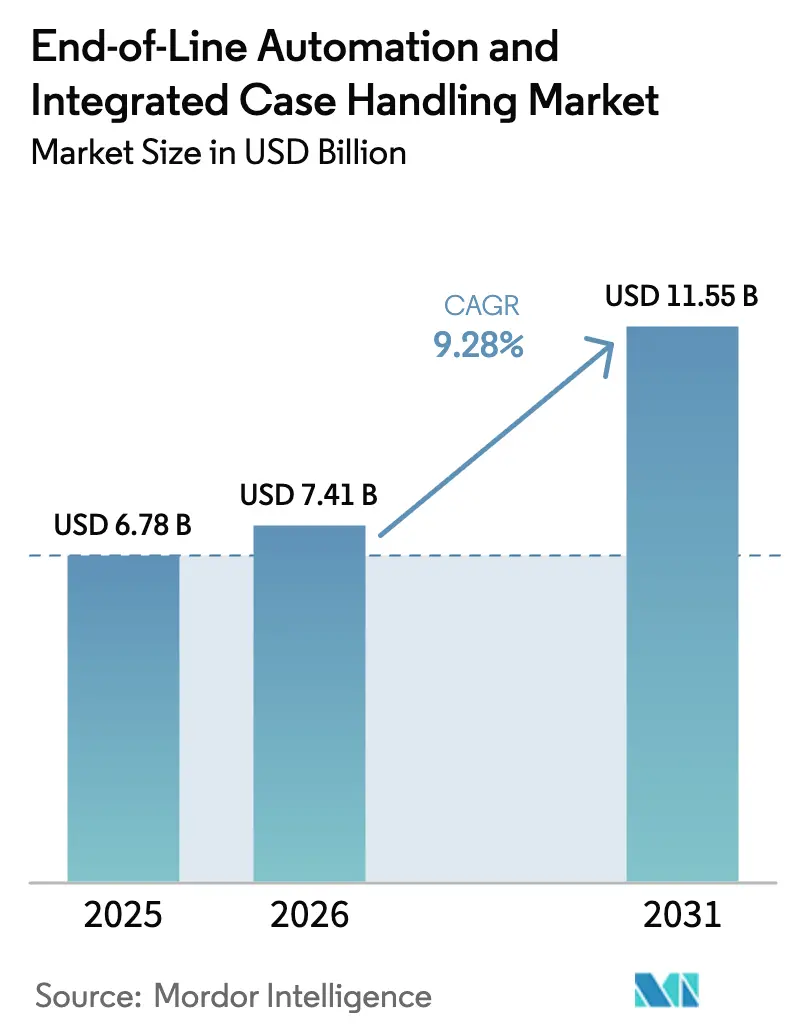

| Market Size (2026) | USD 7.41 Billion |

| Market Size (2031) | USD 11.55 Billion |

| Growth Rate (2026 - 2031) | 9.28% CAGR |

| Fastest Growing Market | Middle East |

| Largest Market | Asia Pacific |

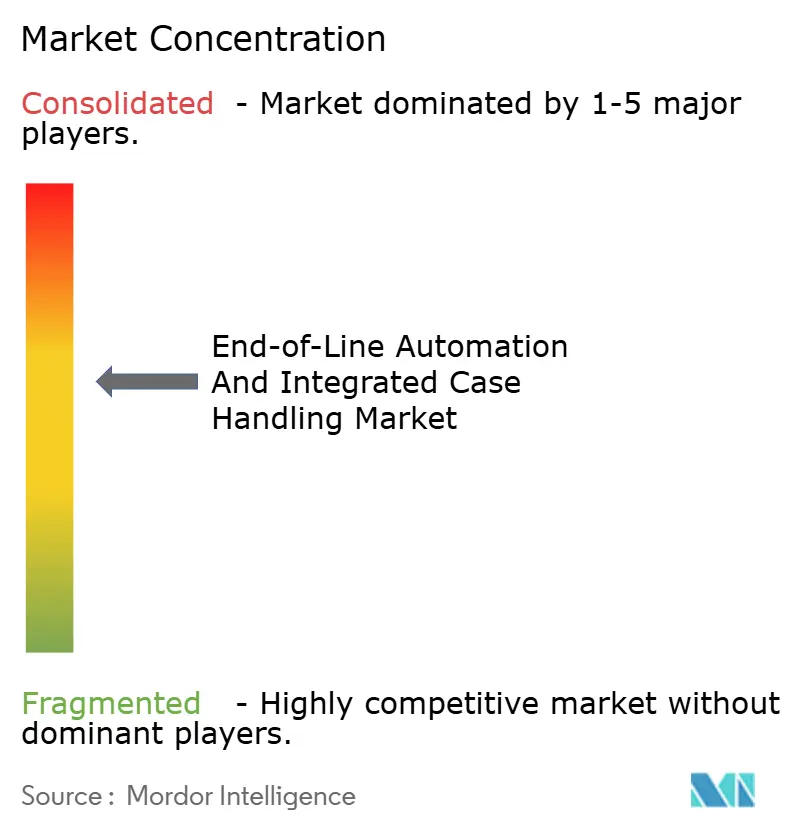

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

End-of-Line Automation And Integrated Case Handling Market Analysis by Mordor Intelligence

The End-of-Line Automation market size in 2026 is estimated at USD 7.41 billion, growing from 2025 value of USD 6.78 billion with 2031 projections showing USD 11.55 billion, growing at 9.28% CAGR over 2026-2031. Recent investment cycles indicate that manufacturers are shifting from point solutions toward integrated, data-centric lines that strike a balance between SKU diversity and high throughput. Demand is underpinned by tight labor markets in warehouses, the rapid expansion of e-commerce fulfillment nodes, and heightened expectations for 24/7, lights-out operations. Equipment builders are responding with modular machines, open software architectures, and pervasive sensor networks that cut unplanned downtime. Capital spending remains strongest in the food, beverage, and personal-care verticals; however, the fastest incremental gains are coming from omnichannel retailers retrofitting brownfield facilities to meet their direct-to-consumer shipping promises.

Key Report Takeaways

- By solution type, case packers captured 26.12% of the End-of-Line Automation and Integrated Case Handling Market share in 2025.

- By automation level, End-of-Line Automation and Integrated Case Handling Market size for fully automated systems is projected to grow at 11.76% CAGR between 2026–2031.

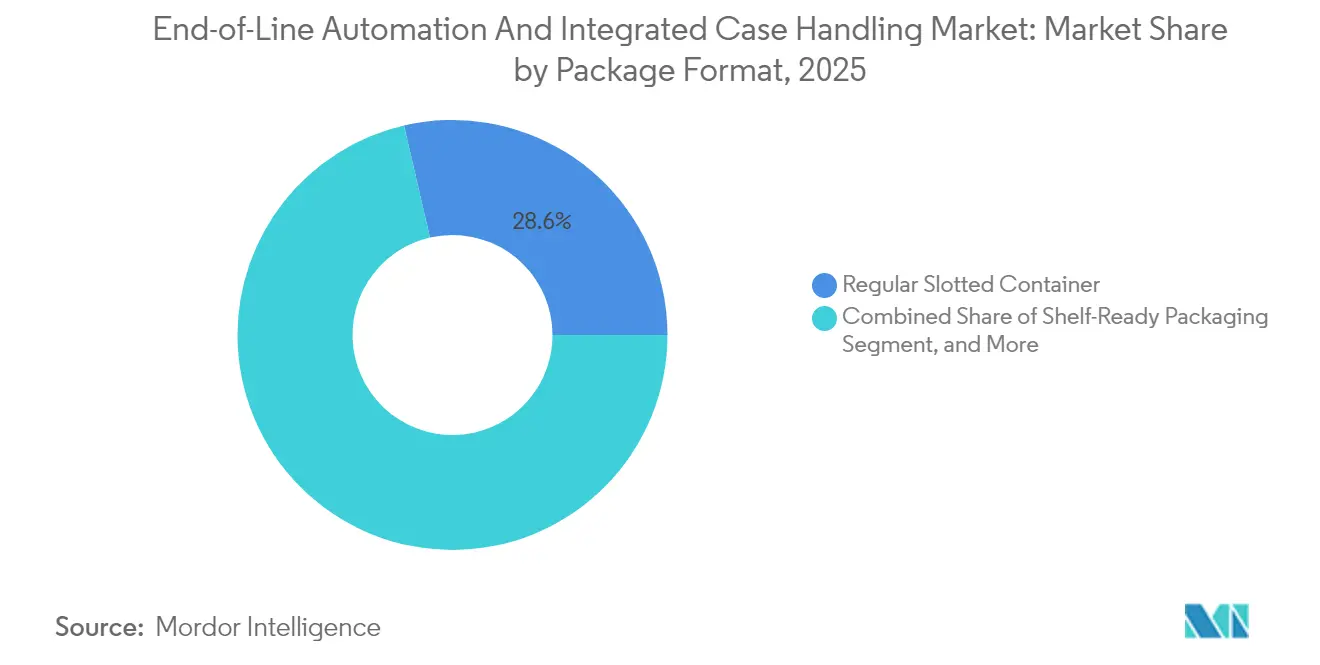

- By package format, regular slotted containers captured 28.62% of the End-of-Line Automation and Integrated Case Handling Market share in 2025.

- By end-user industry, the End-of-Line Automation and Integrated Case Handling Market size for e-commerce and retail is projected to grow at a 10.19% CAGR between 2026–2031.

- By geography, Asia-Pacific captured 37.05% of the End-of-Line Automation and Integrated Case Handling Market share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global End-of-Line Automation And Integrated Case Handling Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in SKU Proliferation Demanding Flexible Case Packing | +2.1% | Global, strongest in North America and Europe | Medium term (2-4 years) |

| Rising Adoption of Vision-Guided Robotic Palletizers | +1.8% | Asia-Pacific core, spillover to North America | Short term (≤ 2 years) |

| E-Commerce Shift Driving High-Mix, Low-Volume Fulfillment | +1.9% | Global, early gains in North America, Europe, China | Medium term (2-4 years) |

| Labor Scarcity and Escalating Wages in Warehouses | +2.3% | North America and Europe, expanding to Asia-Pacific | Short term (≤ 2 years) |

| Integration Of IoT-Based Predictive Maintenance Enhancing Uptime | +1.0% | Global, with early adoption in developed markets | Long term (≥ 4 years) |

| Sustainability Mandates Pushing for End-of-Line Material Reduction | +0.8% | Europe leading, followed by North America and APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

SKU Proliferation Demands Flexible Case Packing

Consumer packaged goods companies report annual SKU growth of nearly 20%, forcing line operators to process vastly different footprints, weights, and protective requirements without lengthy changeovers.[1]Packaging Strategies, “SKU Proliferation and Packaging Line Flexibility,” packagingstrategies.com Modern servo-driven case packers now feature recipe-based adjustments and automated end-effector swaps, which reduce changeover intervals from hours to minutes, making small-batch runs financially viable. Advanced vision systems feed dimensional data into AI-powered motion planners that dynamically adjust collation patterns. Early adopters see line utilization climb beyond 85% despite product complexity, validating flexible automation as a hedge against demand volatility. Capital payback accelerates when flexibility prevents the need for parallel manual packing lanes.

Labor Scarcity Accelerates Automation Adoption

Warehouse vacancy rates exceed 15% across major logistics hubs, while wage inflation topped 8% in 2025, prompting operators to consider fully autonomous palletizing, sealing, and stretch-wrapping cells. Lights-out end-of-line zones reduce overtime reliance and mitigate safety liabilities associated with repetitive lifting. Automation vendors report a sharp uptick in mid-cap firms embracing robotics after calculating sub-two-year paybacks that combine labor savings, reduced workers’ compensation claims, and higher first-pass-yield. Even firms hesitant to overhaul entire lines are installing cobot pack stations on night shifts to stabilize throughput without staffing premiums.

E-Commerce Fulfillment Centers Drive High-Mix Automation

Direct-to-consumer channels force facilities to ship thousands of unique order configurations daily, unlike the predictable pallet loads of traditional retail. Integrated software and controls orchestrate case erecting, void filling, print-and-apply labeling, and mixed-case palletizing in one continuous flow. Real-time order reprioritization leverages AI scheduling engines that weigh carrier cutoff times against machine state, ensuring same-day delivery windows. Grocery and consumer electronics operations report 30% gains in order accuracy after transitioning from siloed equipment to unified control layers that can re-balance workloads on the fly.

Vision-Guided Robotic Palletizers Transform Material Handling

Deployments of 3D-vision robotic palletizers are climbing 35% per year as producers seek to eliminate manual pallet building and accommodate mixed-case loads. Machine-learning algorithms generate optimal stacking recipes for irregular or fragile items, trimming load instability events by 40%. New cobot palletizers integrate onboard safety scanners, allowing human workers to replenish slip sheets without the need for fencing. The technology’s ability to switch patterns instantly supports e-commerce single-parcel orders, seasonal packaging variants, and promotional bundles within the same footprint, widening the addressable market beyond high-volume monotypes.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Initial Capital Expenditure for Customized Lines | -1.4% | Global, highest impact in emerging markets | Short term (≤ 2 years) |

| Limited Skilled Technicians for Complex Integration Projects | -1.1% | Global, sharpest shortages in developed economies | Medium term (2-4 years) |

| Interoperability Issues Between Legacy and Modern Automation Components | -0.9% | North America and Europe | Medium term (2-4 years) |

| Cyber-Security Risks in Connected End-of-Line Systems | -0.6% | Global, higher in critical industries | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Initial Capital Expenditure Constrains Adoption

Custom end-of-line cells cost USD 500,000 to USD 5 million and often require building reinforcements, utility upgrades, and extended commissioning periods. SMEs with volatile order books hesitate to commit, especially when finance teams demand sub-three-year paybacks. Pharmaceutical and food producers face additional validation and documentation charges that double baseline system costs. Leasing models and as-a-service offerings are emerging, yet uptake remains slow outside North America due to risk-averse accounting practices.

Limited Skilled Technicians Restrict Complex Integrations

Brownfield sites rely on legacy PLCs, fieldbus networks, and proprietary SCADA layers that new robots must integrate with, yet the pool of technicians fluent in both generations is dwindling. Integration quotes regularly exceed greenfield project costs by 30% as suppliers schedule scarce specialists months in advance. Companies with strong internal maintenance teams are investing in reskilling programs; however, workforce gaps persist, prolonging project timelines and increasing total installed costs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Solution Type: Integrated Software Catalyzes Digital Transformation

Case packers contributed 26.12% of the End-of-Line Automation market share in 2025, underscoring their position as the primary bottleneck eliminator within high-speed lines. Palletizers ranked second as warehouse automation strategies demanded consistent load quality. The End-of-Line Automation market size for integrated software and controls is forecasted to increase from USD 1.42 billion in 2025 to USD 2.82 billion by 2031, reflecting a 12.14% CAGR as plants transition toward unified dashboards that monitor overall equipment effectiveness. Vendors increasingly bundle advanced analytics modules that flag micro-stoppages, boosting uptime by up to 6 percentage points. Over the forecast horizon, edge-deployed AI models will transition from descriptive alarms to prescriptive adjustment sequences that automatically tune servo paths in real-time.

Second-tier equipment, such as case sealers and pallet wrappers, remains crucial for meeting retailer load integrity standards. Demand for auxiliary inspection systems, including inline X-ray units and vision-based flap detection systems, is expanding in tandem as brand owners raise their quality thresholds. Producers now expect open APIs, allowing these peripherals to feed critical quality characteristics back into centralized historians, enabling closed-loop improvements across the End-of-Line Automation market.

By Automation Level: Fully Autonomous Lines Accelerate

Fully automated configurations held 53.74% of the End-of-Line Automation market in 2025 and are growing at 11.76% CAGR as operators chase 24/7 output with minimal supervision. Lights-out cells employing articulated robots, servo diverters, and smart conveyors demonstrate mean-time-between-failure metrics above 5,000 hours after adopting condition-based maintenance routines. Semi-automated alternatives still dominate applications that handle fragile glass or artisanal goods, where human dexterity yields superior defect rates.

Investment appetite for full autonomy is strongest in pharmaceutical, beverage, and tier-one automotive plants that calculate combined labor and scrap savings topping USD 750,000 annually. The End-of-Line Automation market size attached to fully autonomous lines is predicted to climb by more than USD 2.25 billion between 2026 and 2031, solidifying them as the default choice in new factory blueprints. Integrators now package digital twin simulations with every proposal, giving finance teams clarity on throughput under variable SKU mixes before capex decisions.

By Package Format: Shelf-Ready Designs Gain Ground

Regular slotted containers dominated the market, accounting for 28.62% of revenue in 2025, due to their cost efficiency and compatibility with established erecting and sealing machines. The End-of-Line Automation market size associated with shelf-ready packaging is expected to grow at a 10.93% CAGR, driven by retail chains mandating faster shelf restock cycles. Perforated tear-away windows eliminate the need for manual knife use, reducing in-store merchandising time by 35%. Converters now laminate high-resolution graphics on display panels, enabling brand storytelling without the need for secondary retail trays.

Case packing lines are upgrading end-effectors to handle shelf-ready SKUs while preserving flat crush strength. Early adopters report double-digit sales lifts for high-turnover snacks after adopting display-ready cartons that simplify replenishment. Although trays and wrap-around blanks still serve beverage multipacks efficiently, some bottlers are experimenting with corrugated pads plus overwrap film to shrink corrugated tonnage and meet sustainability pledges.

By End-User Industry: E-Commerce Spurs Rapid Uptake

Food and beverage plants contributed 31.44% of total demand in 2025 owing to stringent hygiene mandates and relentless SKU churn. However, e-commerce and omnichannel retailers are projected to post a 10.19% CAGR as parcel shippers replace manual pack tables with automated void-fill, print-and-apply, and robotic sortation. High-mix orders drive predictive software that reprioritizes tasks based on real-time carrier cutoff windows, illustrating why software-heavy solutions outpace purely mechanical solutions within the End-of-Line Automation industry.

Healthcare adoption is escalating as serialization laws prompt drug manufacturers to close audit loops through integrated case coding and pallet aggregation. Automotive tier suppliers likewise invest, driven by traceability requirements and the shift toward battery-electric powertrains that introduce new pack geometries. Household and personal-care segments capitalize on modular lines that can switch between bulk club formats and precision retail portions without lengthy downtime, reinforcing the flexibility imperative surrounding the End-of-Line Automation market.

Geography Analysis

Asia-Pacific anchored 37.05% of global revenue in 2025, buoyed by China’s manufacturing scale, India’s consumer-goods expansion, and Japan’s early adoption of robotics. Within the End-of-Line Automation market, local governments offer tax credits for smart-factory investments, accelerating the transition from labor-intensive cells to autonomous palletizers. [2]Gulf News, “Automation Projects Under Middle East Diversification Plans,” gulfnews.com . Regional OEMs are increasingly partnering with global brands to co-develop localized solutions that meet price sensitivities while maintaining international safety standards.

North America sustains elevated demand as persistent labor shortages accelerate capital allocation toward full-line retrofits in both greenfield and brownfield facilities. Advanced motion-control ecosystems, widespread IIoT connectivity, and mature distribution infrastructure support large projects, particularly among beverage bottlers aiming for 2-hour delivery windows. Sustainability legislation encouraging the use of recycled corrugate further propels investment in smart case formers capable of handling lighter board grades without warping.

Europe’s End-of-Line Automation market benefits from cross-industry Industry 4.0 programs and strict producer-responsibility directives that thrust energy-efficient, modular machines into the spotlight. The region’s strong food and pharmaceutical clusters adopt closed-system lines to align with rising hygiene expectations, while palletizing robots tuned for warehouse mezzanine deployment gain traction amid real estate constraints.

Competitive Landscape

The End-of-Line Automation market displays moderate concentration. Krones AG and Sidel Group dominate the beverage industry through their vertically integrated case handling, inspection, and stretch-wrapping portfolios. Robotics powerhouses ABB Ltd., FANUC Corporation, and KUKA AG capture market share in palletizing with six-axis and SCARA platforms fine-tuned for lightweight, corrugated payloads.[3]Packaging World, “End-of-Line Equipment Builders Battle for Integration Supremacy,” packworld.com Mid-cap specialists, such as ProMach Inc. and BluePrint Automation, emphasize application-specific expertise, winning contracts where rapid changeovers or space constraints render traditional layouts ineffective.

Competitive dynamics now hinge on software differentiation. Vendors roll out line-level MES connectors, AI-assisted OEE dashboards, and cloud-native predictive maintenance suites that upgrade mechanical installations into data-driven assets. Strategic acquisitions persist: ProMach’s 2025 purchase of Robopac expanded its stretch-wrap footprint, while ABB’s Shanghai plant doubled palletizer output to meet the growth curves in Asia.

Collaborative robotics broadens the field for smaller challengers, such as EndFlex LLC and ITW Hartness. By leveraging plug-and-play vision stacks, these firms integrate cobots into existing pack stations rather than full cage-based cells, appealing to SMEs staging incremental automation. Edge-to-cloud cybersecurity offerings emerge as a competitive moat as customers scrutinize protection of serialized product data feeding national traceability registries.

End-of-Line Automation And Integrated Case Handling Industry Leaders

Krones AG

Sidel Group

Syntegon Technology GmbH

Schneider Packaging Equipment Company, Inc.

ABB Ltd

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Krones AG completed a USD 85 million automation technology center in Neutraubling, Germany, housing digital twin testbeds for AI-driven packaging lines.

- September 2025: ABB Ltd invested USD 120 million to expand Shanghai robotics capacity, doubling palletizer output and unveiling new cobots for end-of-line tasks.

- August 2025: ProMach Inc. acquired Robopac S.p.A. for USD 180 million, reinforcing stretch-film expertise across Europe.

- July 2025: FANUC Corporation launched its CRX-25iA cobot with integrated vision for case packing, targeting SME labor gaps.

Global End-of-Line Automation And Integrated Case Handling Market Report Scope

| Semi-Automated |

| Fully Automated |

| Case Erectors |

| Case Packers |

| Case Sealers |

| Palletizers |

| Pallet Wrappers |

| Integrated Software and Controls |

| Auxiliary Equipment |

| Other Solution Types |

| Food and Beverage |

| Pharmaceutical and Healthcare |

| Household and Personal Care |

| E-commerce and Retail |

| Automotive |

| Logistics |

| Other End-user Industries |

| Regular Slotted Container |

| Tray and Wrap-around |

| Shelf-Ready Packaging |

| Bags and Pouches |

| Kegs and Drums |

| Other Package Formats |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Automation Level | Semi-Automated | ||

| Fully Automated | |||

| By Solution Type | Case Erectors | ||

| Case Packers | |||

| Case Sealers | |||

| Palletizers | |||

| Pallet Wrappers | |||

| Integrated Software and Controls | |||

| Auxiliary Equipment | |||

| Other Solution Types | |||

| By End-user Industry | Food and Beverage | ||

| Pharmaceutical and Healthcare | |||

| Household and Personal Care | |||

| E-commerce and Retail | |||

| Automotive | |||

| Logistics | |||

| Other End-user Industries | |||

| By Package Format | Regular Slotted Container | ||

| Tray and Wrap-around | |||

| Shelf-Ready Packaging | |||

| Bags and Pouches | |||

| Kegs and Drums | |||

| Other Package Formats | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the End-of-Line Automation market in 2026?

The market reached USD 7.41 billion in 2026, with a projected rise to USD 11.55 billion by 2031 at a 9.28% CAGR.

Which region leads the adoption of end-of-line systems?

The Asia-Pacific region commands 37.05% of global revenue, driven by its dense manufacturing bases and government incentives for smart factories.

What segment grows fastest within end-of-line solutions?

The integrated software and controls segment is forecast to expand at a 12.14% CAGR through 2031 as plants prioritize data-driven optimization.

Why are fully automated lines gaining favor?

Labor shortages, rising wages, and the need for 24/7 operations push manufacturers toward lights-out cells that deliver rapid paybacks and consistent quality.

Which driver most influences future investments?

Labor scarcity, carrying a +2.3% impact on CAGR, remains the strongest catalyst for accelerating automation budgets.

What is the biggest barrier to adoption for small manufacturers?

High initial capital costs, often USD 500,000 to USD 5 million per customized line, deter smaller firms and extend payback periods beyond three years.

Page last updated on: