Automated Capping And Closure Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

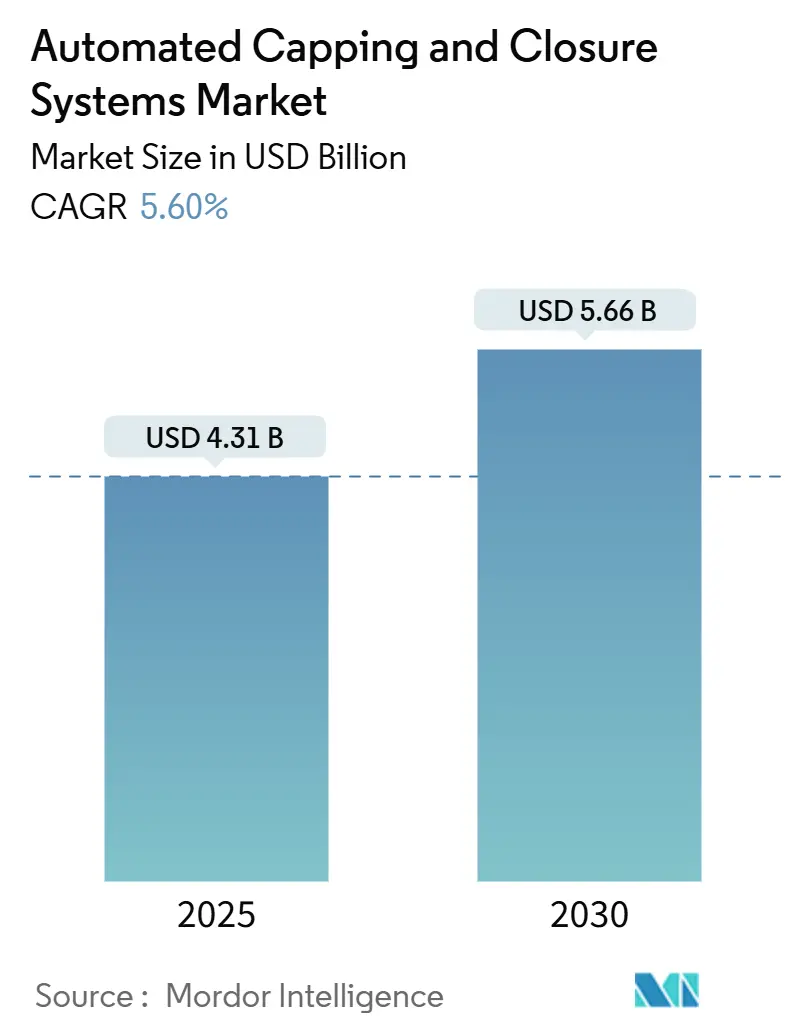

| Market Size (2025) | USD 4.31 Billion |

| Market Size (2030) | USD 5.66 Billion |

| Growth Rate (2025 - 2030) | 5.60% CAGR |

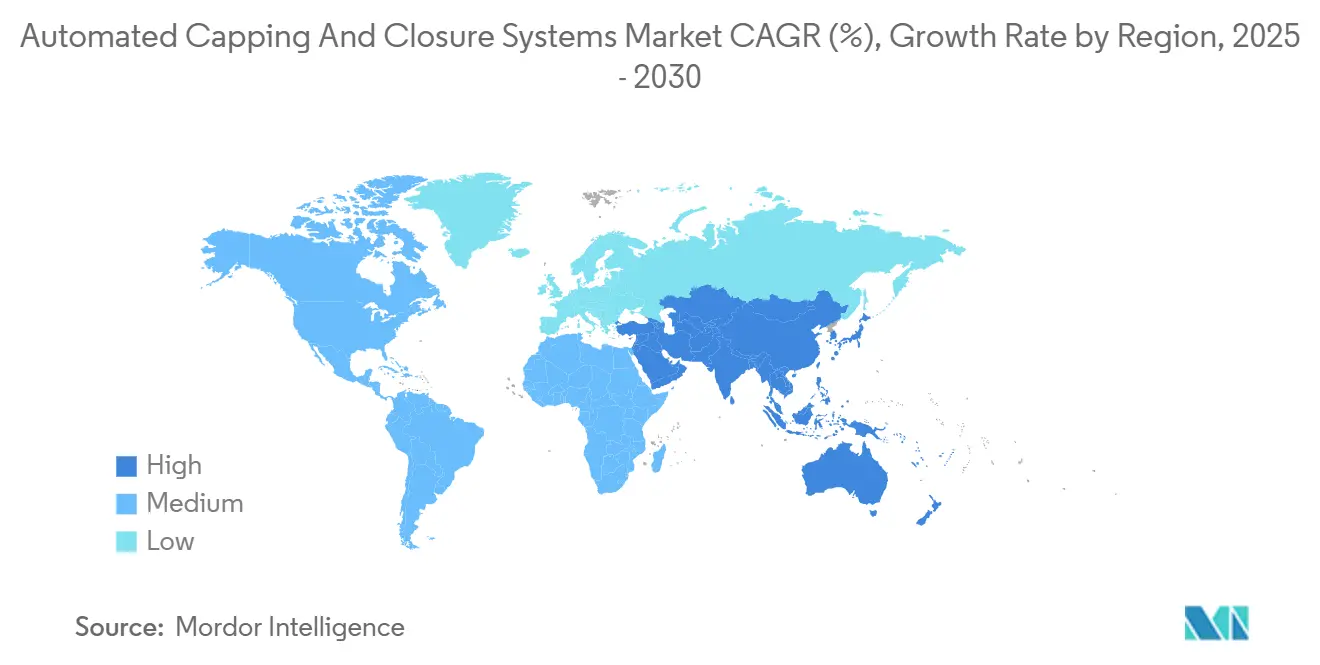

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Automated Capping And Closure Systems Market Analysis by Mordor Intelligence

The automated capping and closure systems market was valued at USD 4.31 billion in 2025 and is projected to reach USD 5.66 billion by 2030, growing at a 5.60% CAGR. Rising regulatory scrutiny, rapid technological upgrades, and consumer demand for safe and convenient packaging are driving this expansion. Pharmaceutical serialization rules are steering equipment specifications toward precise torque control and data capture, while beverage producers are investing in high-speed rotary platforms to keep pace with volume growth.[1]European Medicines Agency, “Falsified Medicines,” EMA.europa.eu Connectivity features, such as predictive maintenance and real-time performance dashboards, are now standard, enhancing overall equipment effectiveness and reducing life-cycle costs. Sustainability programs in Europe and North America are accelerating the shift to lightweight closures, which in turn require tighter application tolerances that automated solutions can reliably deliver. Competitive rivalry remains moderate, as established European suppliers compete with lower-cost Asian manufacturers that are scaling quickly and offering localized service packages.

Key Report Takeaways

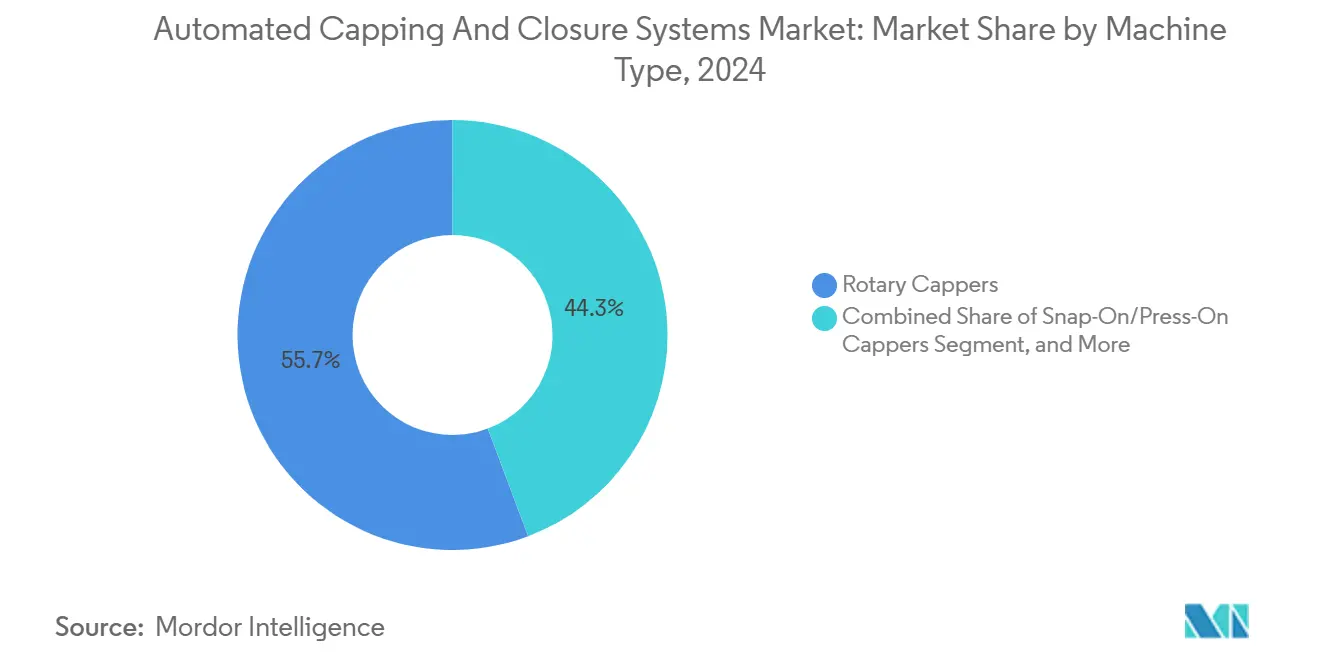

- By machine type, the Rotary Cappers segment captured 55.74% of the Automated Capping and Closure Systems Market share in 2024.

- By closure type, the Automated Capping and Closure Systems Market size for vial stoppers is projected to grow at a 6.84% CAGR between 2025–2030.

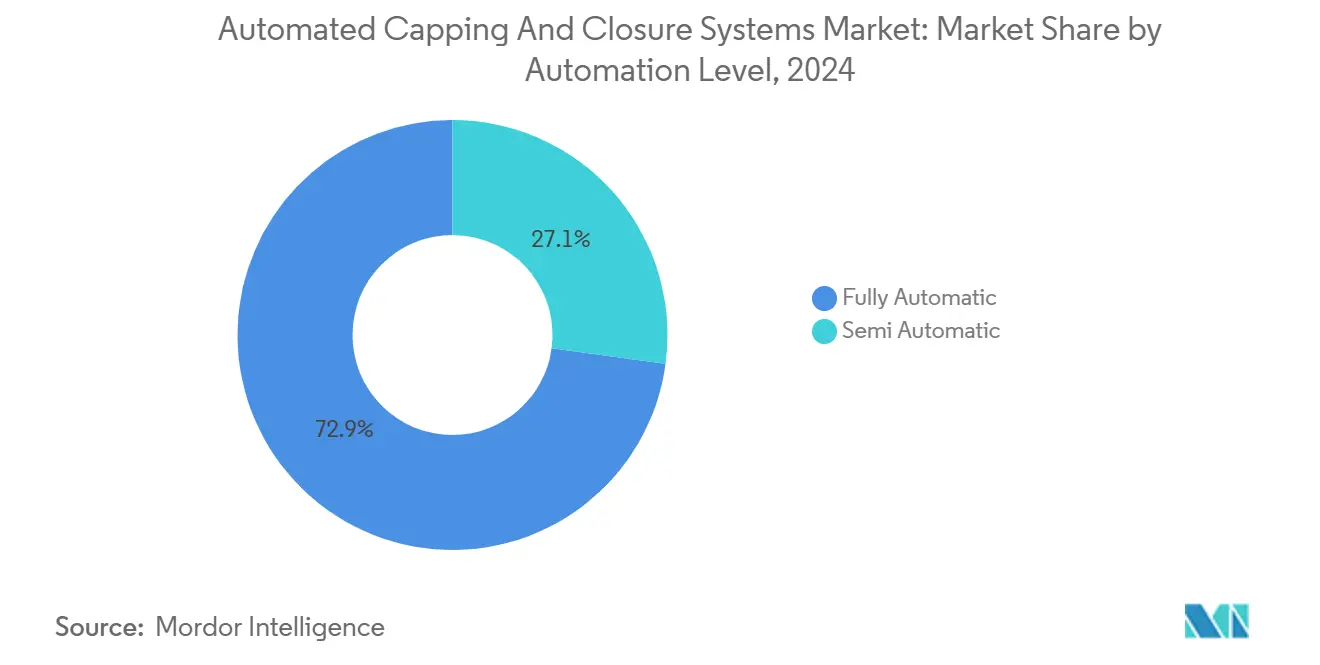

- By automation level, the Automated Capping and Closure Systems Market size for Fully Automatic systems is projected to grow at a 6.93% CAGR between 2025–2030.

- By end-user industry, the food and beverage segment captured 52.83% of the Automated Capping and Closure Systems Market share in 2024.

- By geography, the Automated Capping and Closure Systems Market size for the Asia-Pacific is projected to grow at a 7.07% CAGR between 2025–2030.

Global Automated Capping And Closure Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising demand for tamper-evident packaging | +1.2% | Global, with concentration in North America and EU | Medium term (2-4 years) |

| Regulatory push for pharmaceutical serialization and secure closures | +1.5% | Global, led by FDA and EMA jurisdictions | Long term (≥ 4 years) |

| Shift toward high-speed rotary cappers in beverage lines | +0.9% | APAC core, spill-over to North America | Short term (≤ 2 years) |

| Growth of single-dose nutraceutical formats | +0.8% | North America and EU, expanding to APAC | Medium term (2-4 years) |

| Incorporation of smart torque-feedback systems in machines | +0.7% | Global, early adoption in developed markets | Long term (≥ 4 years) |

| Sustainability-driven lightweight closures | +0.6% | EU-led, expanding globally | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Demand for Tamper-Evident Packaging

Tamper-evident solutions have moved from optional to mandatory in many regulated sectors. The EU Falsified Medicines Directive and the Drug Supply Chain Security Act mandate the use of visible breach indicators and digital traceability, prompting the wide adoption of vision-guided inspection units that verify band integrity with 99.9% accuracy. Pharmaceutical producers are increasingly specifying multi-head systems that apply both primary caps and secondary safety seals in a single pass, which reduces contamination risk and speeds up changeovers. Blockchain interfaces now connect capping equipment to enterprise resource planning platforms, enabling real-time authentication of every closure applied, a feature that also allows machine builders to create new recurring-service revenue streams.

Regulatory Push for Pharmaceutical Serialization and Secure Closures

Global serialization mandates require unit-level track-and-trace, integrating optical character recognition and barcode validation into capping stations. Leading equipment records closure torque, imprint code, and unit identifier in under 100 milliseconds per package, sustaining line speeds above 600 units per minute while remaining in full compliance with FDA and EMA guidance. Equipment suppliers have responded with modular software that supports multiple regional coding formats without hardware overhaul, lengthening asset life cycles and reducing validation costs

Shift Toward High-Speed Rotary Cappers in Beverage Lines

Continuous-motion rotary machines are replacing intermittent-motion linear systems on high-volume drink lines. Throughput can exceed 2,000 bottles per minute at consistent torque values, cutting fill-and-seal cycle time by half compared with legacy configurations. Predictive maintenance sensors measure bearing vibration and motor temperature every second, enabling users to schedule service windows and avoid unexpected stoppages that can cost more than USD 50,000 per hour in lost production.

Growth of Single-Dose Nutraceutical Formats

Personalized nutrition trends have increased demand for portion-controlled vials, sticks, and blisters. These formats require precise, lower-torque application to balance seal integrity with consumer ergonomics. Servo-controlled heads provide dynamic torque adjustment within ±1 % of setpoint, achieving changeovers in under 15 minutes between product runs, an essential feature for contract packers managing diverse SKU portfolios.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Capital-intensive equipment costs for SMEs | -0.8% | Global, particularly impacting emerging markets | Short term (≤ 2 years) |

| Downtime risk from complex multi-head changeovers | -0.6% | Global, concentrated in high-mix production environments | Medium term (2-4 years) |

| Limited standardization across closure types | -0.4% | Global, with regional variations in standards | Long term (≥ 4 years) |

| Supply-chain volatility in specialty polymers | -0.5% | Global, acute in regions dependent on imports | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Capital-Intensive Equipment Costs for SMEs

New high-speed automated lines often exceed USD 100,000, and the total cost of ownership increases once specialized maintenance, spare parts, and facility retrofits are included. SMEs producing fewer than 500 units per hour struggle to reach payback within typical three-year investment windows, which delays modernization plans and sustains manual processes with higher defect rates.

Downtime Risk from Complex Multi-Head Changeovers

Multi-head rotary systems can require two to four hours for a full format change when closures, bottles, and labels all vary. Even with Single Minute Exchange of Die principles, frequent switches depress overall equipment effectiveness below the 70% benchmark in many contract-packing environments.[2]Packaging Machinery Manufacturers Institute, “Packaging Machinery Shipments,” PMMI.org Quick-change tooling and automatic recipe recall reduce time lost, but such options add up-front cost that small operators may find prohibitive.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Machine Type: Rotary Systems Drive High-Volume Applications

Rotary equipment contributed 55.74% revenue in 2024 within the automated capping and closure systems market and is favored for lines exceeding 1,000 containers per minute. The automated capping and closure systems market size for rotary machines is expected to continue its leadership as global beverage brands and pharmaceutical fillers increase their capacity. Continuous-motion design eliminates stop-start stress, enhancing uptime and extending component life. Snap-on and press-on machines remain the fastest-growing class, with a 6.64% CAGR, serving single-dose nutraceutical and over-the-counter drug packs that rely on tamper-evident rings rather than threaded engagement. Inline, chuck, and spindle variants remain relevant for niche tasks that demand torque precision or container-shape flexibility. Servo technology is spreading across all designs, enabling a single platform to handle multiple closure profiles without requiring mechanical retooling.

Rotary cappers are increasingly integrating self-diagnostic software that flags running parameters drifting beyond specifications, guiding operators through corrective steps. Snap-on systems are being outfitted with integrated cap feeders that align lightweight closures without scuffing, a critical factor for clear pharmaceutical vials. New spindle heads can now process press-on tethers for sustainable drink closures, keeping the closure attached to the bottle to meet European Union regulations. Chuck units, although slower, deliver the ±0.5 Nm torque repeatability required in biologics vial sealing. This breadth of technology ensures end users can match pack format, volume requirement, and budget to the most effective machinery.

By Closure Type: Screw Caps Maintain Dominance Amid Specialized Growth

Screw caps accounted for 54.69% revenue in 2024. Their universal compatibility across beverage, personal care, and household chemical lines sustains volume demand and simplifies procurement. The automated capping and closure systems market size for screw-cap lines is expected to expand steadily, despite moderating growth. Vial stoppers are projected to grow at a 6.84% CAGR, driven by the expansion of injectable drug pipelines. Smart closures, which embed near-field communication chips, enable brand owners to combine consumer engagement with anti-counterfeiting assurance. Capping equipment now includes antenna-safe jaws to prevent damage to in-mold electronics.

Roll-on pilfer-proof tops remain popular in the wine and spirits industry, supported by aluminum’s recyclability. Snap-fit solutions win in household cleaners for ease of reseal. Regulations such as ISO 8536 are shifting design priorities toward barrier performance and steam sterilization tolerance. Machine builders now offer modular application stations that handle desiccant-integrated plugs within the same turret, reducing line length and lowering contamination risk. As brands adopt lightweight formats, closure thread profiles are becoming thinner, which necessitates even tighter torque windows during application.

By Automation Level: Full Automation Dominates Quality-Critical Applications

Fully automatic machinery generated 72.87% of 2024 revenue and will grow fastest at 6.93% through 2030. Pharmaceutical lines see the greatest benefit because closed-loop controllers ensure each seal meets validated torque targets, with deviation alarms logged automatically for audit trails. Semi-automatic setups are viable where batch sizes are small and manual supervision still provides value. Collaborative robots have begun to blur traditional lines, feeding caps to semi-automated stations and reducing the need for operator lifting. This hybrid approach allows phased investment, preserving cash flow while sustaining future upgrade paths.

Full automation platforms now ship with cloud-ready gateways that stream machine health data into plant management systems. Machine learning models detect wear patterns days before failure, cutting unplanned downtime. Clean-in-place modules accelerate product changeovers and support sterile operations, while recipe management software automatically scales torque set-points to accommodate lightweight closures. For brand owners, these features translate into lower scrap, reduced recalls, and faster regulatory submissions.

By End-user Industry: Pharmaceuticals Lead Growth Amid Regulatory Pressures

Food and beverage retained 52.83% of 2024 revenue, while pharmaceutical fillers are advancing at the fastest rate, with a 7.11% CAGR. Drug producers face rigorous GMP protocols and must document every seal, which favors fully enclosed, servo-controlled machinery with in-line inspection. Personalized medicine and cell-and-gene therapies rely on smaller batch runs packaged in vials or syringes, pushing demand for adaptable capping heads that apply both stoppers and aluminum overseals in sequence. The automated capping and closure systems market share of pharmaceutical applications is poised to climb as injectable pipelines expand.

Cosmetics players are shifting to premium dispensing closures and airless pumps, which require delicate torque control to avoid scuffing and achieve a matte finish. Industrial chemical packagers require flameproof enclosures and anti-sparking components to reduce workplace hazards while lowering the cost of lifting equipment. Nutraceutical brands, propelled by e-commerce, value fast changeover over absolute speed, creating an opening for flexible, mid-range servo cappers that can switch from gummies to softgels within minutes. Across all segments, heightened sustainability targets are prompting companies to adopt recyclable mono-material closures.

Geography Analysis

Asia-Pacific’s 37.42% share in 2024 reflects cost-competitive labor, a deep supplier ecosystem, and state-backed automation subsidies. In 2025, Chinese pharmaceutical producers upgraded more than 50 filling lines, each equipped with integrated torque feedback and vision inspection systems. Indian generics plants pursued similar modernization to secure U.S. FDA approvals, often partnering with European OEMs that supply validation documentation. Japanese nutraceutical firms adopted ultra-clean snap-on systems for probiotic drinks, boosting regional spending.

North American buyers prioritize technology leadership. Beverage fillers commissioned high-speed rotary cappers capable of exceeding 2,000 bottles per minute to meet demand for convenience packs. Pharmaceutical sites installed cloud-connected work cells that integrate capping with laser coding, aggregation, and palletizing. Sustainability also drives capital plans, with lightweight tethered closures gaining traction following draft U.S. recycling mandates.

Europe faces a 2026 deadline for the use of tethered beverage closures. Equipment retrofits are underway, with a focus on redesigning the spindle head and recalibrating the torque map. Serialization upgrades remain in progress after Brexit created dual coding requirements for lines exporting to the United Kingdom and European Union. Eastern European contract packers are tapping EU funds to install first-time fully automatic lines, widening addressable demand.

Competitive Landscape

The automated capping and closure systems market exhibits a moderate level of concentration. Krones AG and Sidel Group retain technology leadership through patented torque management and quick-change turrets. Both firms supplement machinery with IIoT service subscriptions that remotely monitor vibration and seal quality. Asian newcomers, including several China-based firms, undercut prices by up to 30% and offer on-site service hubs in India and Southeast Asia, eroding European share in price-sensitive tiers.

Strategic moves center on integrating Industry 4.0. Krones AG introduced an AI-driven torque optimizer in October 2024, which self-adjusts every 50 cycles. Sidel Group expanded its Italian plant in September 2024, increasing annual rotary head output by 40% and reducing lead times. Syntegon Technology acquired a specialist in sterile equipment in July 2024, broadening its vial closure capabilities. Patent filings at the United States Patent and Trademark Office reveal an uptick in machine-learning quality-control algorithms and non-contact torque sensors.[3]United States Patent and Trademark Office, “Patents Search,” USPTO.gov

Capital intensity limits new entrants, but service-based competition is on the rise. Vendors now bundle remote diagnostics, parts forecasting, and operator e-learning, converting one-time equipment sales into multi-year contracts. Sustainability is another battleground, with SACMI’s lightweight closure press unveiled in August 2024 achieving 15% resin reduction without compromising seal strength. GEA Group’s IoT-enabled SmartCap platform introduced in May 2024 reduces energy draw by 12%, appealing to carbon-footprint reduction programs.

Automated Capping And Closure Systems Industry Leaders

Krones AG

Sidel Group

Syntegon Technology GmbH

SIG Combibloc Group AG

Coesia S.p.A.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Krones AG launched its ModulCap system featuring AI torque optimization and integrated vision inspection for pharmaceutical serialization compliance.

- September 2024: Sidel Group invested EUR 25 million (USD 27.5 million) to expand production of high-speed rotary equipment in Italy.

- August 2024: SACMI introduced the CCM64MD cap press at PACK EXPO, enabling lightweight closure production with reduced energy consumption.

- July 2024: Syntegon Technology acquired a pharmaceutical packaging specialist, adding sterile capping solutions to its portfolio.

Global Automated Capping And Closure Systems Market Report Scope

| Inline Cappers |

| Rotary Cappers |

| Chuck Cappers |

| Snap-On/Press-On Cappers |

| Spindle Cappers |

| Other Machine Types |

| Screw Caps |

| Roll-On Pilfer-Proof (ROPP) |

| Snap-Fit |

| Vial Stoppers |

| Other Closure Types |

| Semi Automatic |

| Fully Automatic |

| Food and Beverage |

| Pharmaceuticals |

| Cosmetics and Personal Care |

| Industrial and Household Chemicals |

| Other End-User Industries |

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Rest of Africa | ||

| By Machine Type | Inline Cappers | ||

| Rotary Cappers | |||

| Chuck Cappers | |||

| Snap-On/Press-On Cappers | |||

| Spindle Cappers | |||

| Other Machine Types | |||

| By Closure Type | Screw Caps | ||

| Roll-On Pilfer-Proof (ROPP) | |||

| Snap-Fit | |||

| Vial Stoppers | |||

| Other Closure Types | |||

| By Automation Level | Semi Automatic | ||

| Fully Automatic | |||

| By End-user Industry | Food and Beverage | ||

| Pharmaceuticals | |||

| Cosmetics and Personal Care | |||

| Industrial and Household Chemicals | |||

| Other End-User Industries | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Chile | |||

| Rest of South America | |||

| Europe | United Kingdom | ||

| Germany | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the automated capping and closure systems market in 2025?

It reached USD 4.31 billion in 2025.

What CAGR is forecast for automated capping equipment through 2030?

The market is projected to grow at 5.60% annually to 2030.

Which machine type holds the largest share of global demand?

Rotary cappers led with 55.74% market share in 2024.

Why is Asia-Pacific the fastest-growing region?

Rapid pharmaceutical expansion and government automation incentives support a 7.07% CAGR through 2030.

What is the main growth driver in pharmaceuticals?

Serialization and tamper-evident rules are pushing producers toward fully automatic, data-rich capping lines.

Page last updated on: