Elemental Fluorine Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

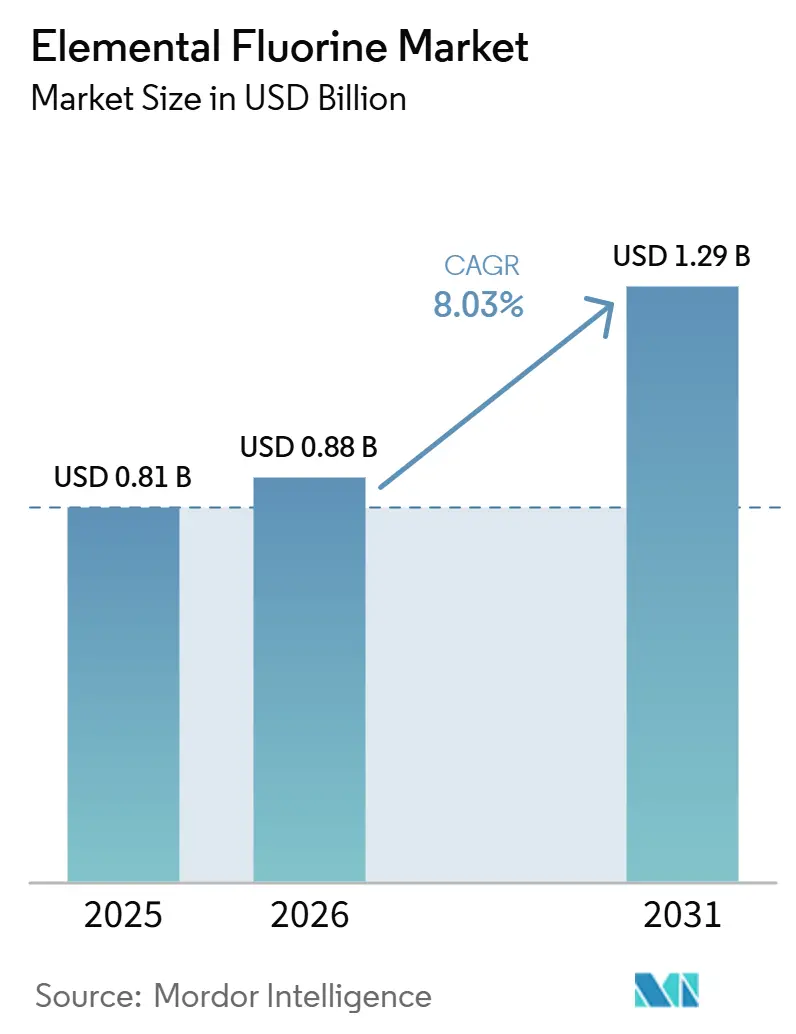

| Market Size (2026) | USD 0.88 Billion |

| Market Size (2031) | USD 1.29 Billion |

| Growth Rate (2026 - 2031) | 8.03% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Elemental Fluorine Market Analysis by Mordor Intelligence

The Elemental Fluorine Market size is projected to be USD 0.81 billion in 2025, USD 0.88 billion in 2026, and reach USD 1.29 billion by 2031, growing at a CAGR of 8.03% from 2026 to 2031. Expansions in uranium-enrichment capacity, aggressive chip-fab buildouts, and stricter regulations phasing down high-GWP gases are driving baseline demand for high-purity fluorine. Producers are increasingly focusing on on-site generation to reduce transport risks, which shortens supply timelines and supports just-in-time manufacturing at semiconductor fabs and pharmaceutical plants. Asia-Pacific remains the leader in new capacity announcements, while North American incentives under the CHIPS Act and nuclear-fuel grants are encouraging partial re-shoring of demand. In Europe, high energy tariffs and stricter climate regulations are fostering tolling partnerships with Asian suppliers instead of initiating greenfield projects within the region.

Key Report Takeaways

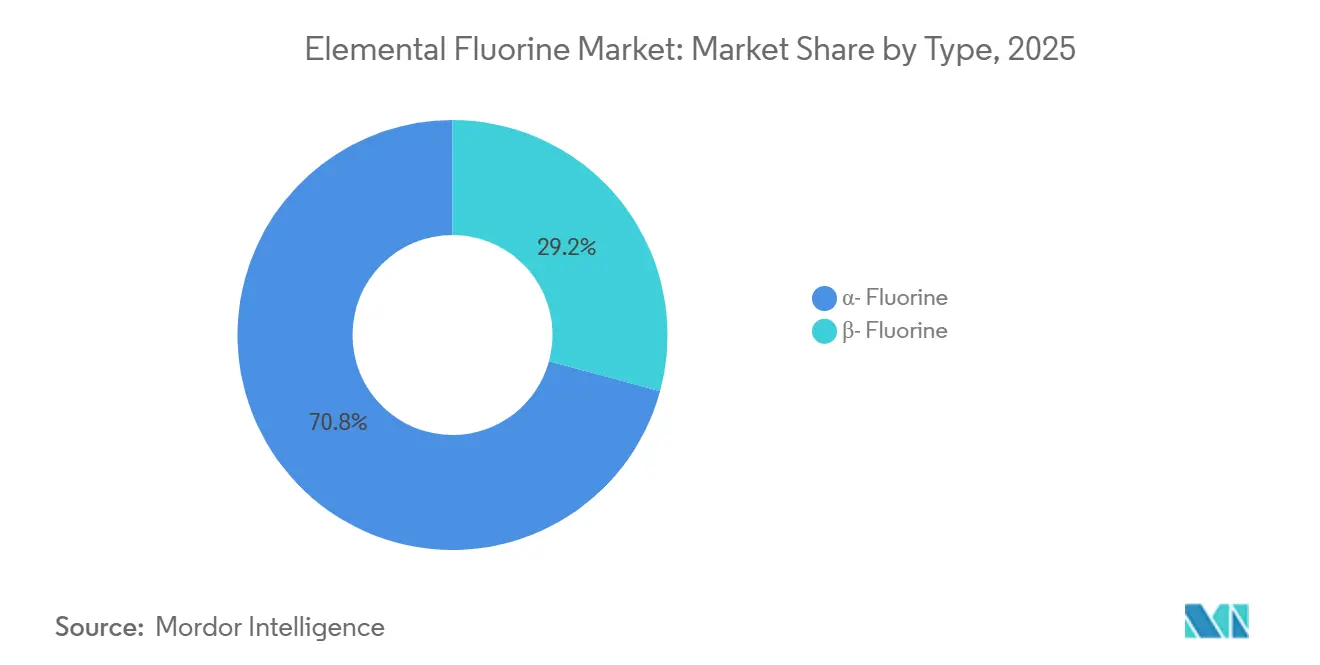

- By type, α-Fluorine led with 70.78% of the elemental fluorine market share in 2025, while β-Fluorine is advancing at an 8.24% CAGR through 2031.

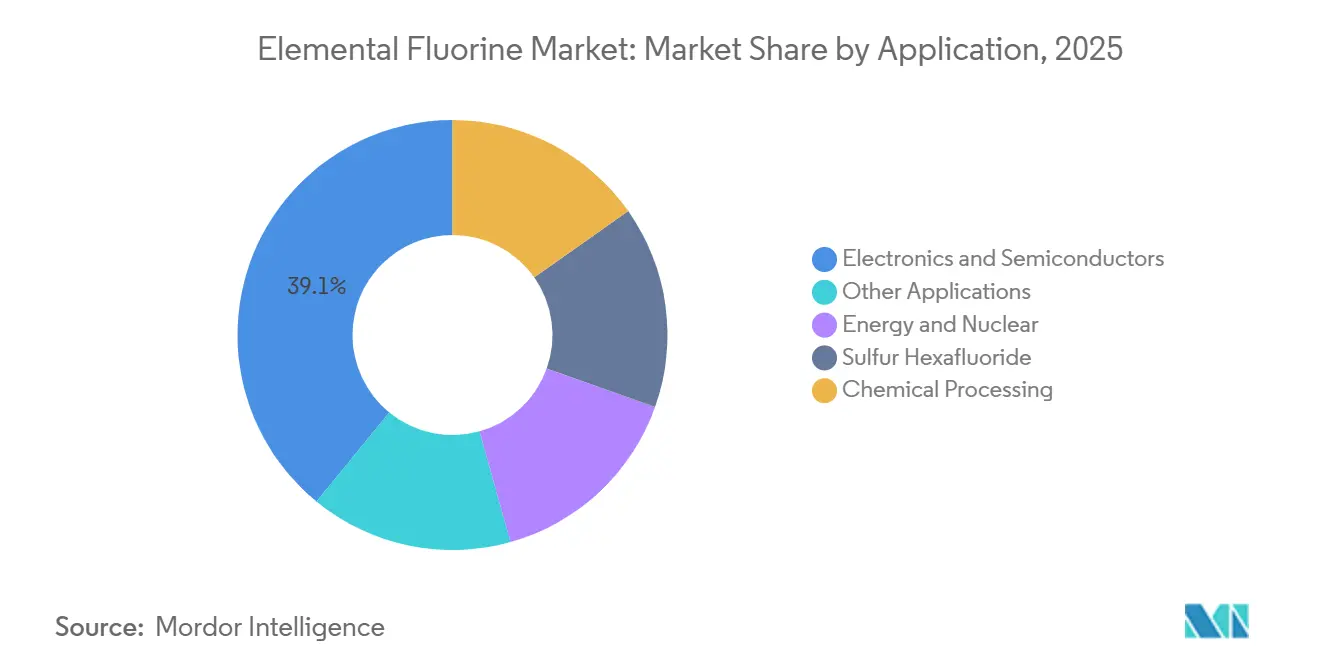

- By application, electronics and semiconductors captured 39.11% of the elemental fluorine market share in 2025, while energy and nuclear is advancing at an 8.78% CAGR through 2031.

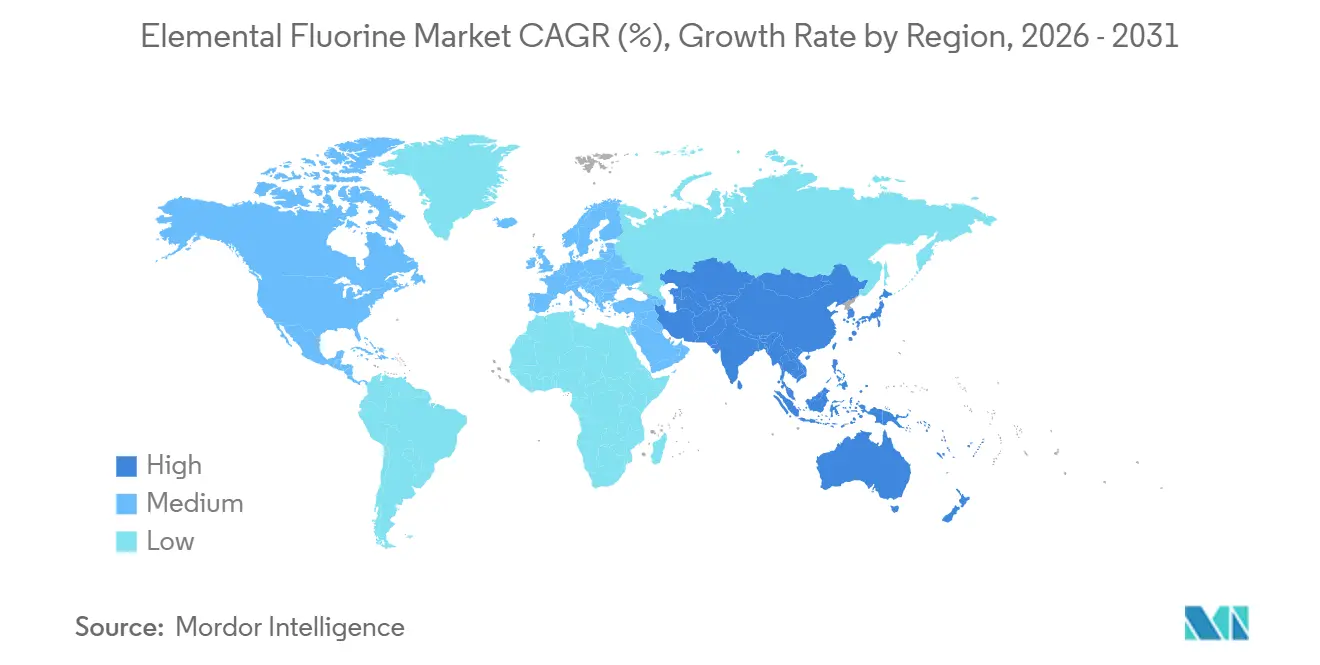

- By geography, Asia-Pacific accounted for 54.45% of the elemental fluorine market share in 2025 and is advancing at an 8.95% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Elemental Fluorine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of UF₆ conversion/enrichment capacity for nuclear fuel | +1.8% | North America, Europe, APAC (China, India) | Medium term (2–4 years) |

| Growth in plastics, LCD and OLED display etching/cleaning uses | +2.1% | APAC core (China, South Korea, Taiwan), spill-over to North America | Short term (≤2 years) |

| Regulatory phase-down of high-GWP NF₃ favouring F₂ adoption | +1.5% | Global, led by EU and North America | Long term (≥4 years) |

| On-site modular fluorine generators reducing logistics risk | +1.2% | Global, with early adoption in APAC and North America semiconductor hubs | Medium term (2–4 years) |

| Emerging use of high-purity F₂ as lithium-ion battery electrolyte additive | +0.9% | APAC (China, South Korea), North America (EV gigafactory clusters) | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Expansion of UF₆ Conversion/Enrichment Capacity for Nuclear Fuel

Government-supported enrichment projects are increasing fluorine consumption as advanced reactors transition from pilot phases to early commercial deployment. Centrus Energy’s Piketon, Ohio site is expanding with thousands of centrifuges under a multi-year engineering contract awarded in 2026, positioning the facility as the West’s only licensed source of high-assay LEU fuel. Each kilogram of LEU requires elemental fluorine during the UF₄-to-UF₆ conversion process, directly linking nuclear capacity to fluorine demand. Similar capacity expansions in France and India are further strengthening mid-term demand visibility. Suppliers offering nuclear-qualified purity grades are securing decade-long offtake agreements, which support investments in new electrolyzers.

Growth in Plastics, LCD and OLED Display Etching/Cleaning Uses

OLED penetration accounted for 61% of LG Display’s revenue in 2025, with the company investing USD 970 million to expand panel production lines through 2027. Advanced display technologies require multiple dry-etch processes, where fluorinated gases remove polymeric residues without damaging underlying layers. Semiconductor fabs operating below the 5 nm node are adopting elemental fluorine for chamber cleaning due to its zero-GWP properties, which help meet Scope 1 emissions targets. These trends are particularly concentrated in the Asia-Pacific region, where over 80% of new display and semiconductor capacity is under construction, representing the largest near-term growth driver for the elemental fluorine market.

Regulatory Phase-Down of High-GWP NF₃ Favoring F₂ Adoption

The European Union’s Regulation 2024/573 imposes stricter quotas, reporting requirements, and leak-detection rules for fluorinated greenhouse gases[1]European Union, “Regulation (EU) 2024/573 on Fluorinated Greenhouse Gases,” eur-lex.europa.eu. Similarly, California and New York have implemented parallel frameworks, increasing the cost of using NF₃, which has a global warming potential (GWP) of nearly 17,000. Elemental fluorine, with a GWP of zero, avoids these regulatory constraints and qualifies for corporate net-zero accounting. Industrial gas companies report double-digit growth in on-site "Generation F" systems as semiconductor fabs transition away from cylindered NF₃. This displacement trend is expected to continue beyond 2030.

On-Site Modular Fluorine Generators Reducing Logistics Risk

Transporting compressed fluorine involves stringent hazmat and security regulations, significantly increasing delivery costs. Companies like Linde and Air Liquide are offering skid-mounted systems that electrolyze anhydrous HF at customer sites, maintaining only 2 kg of fluorine in line compared to 500 steel cylinders annually for equivalent NF₃ supply. These systems achieve payback in less than four years for fabs operating continuously, with safety records showing zero incidents over fifteen years. Adoption is particularly strong in South Korea and Arizona, where new fabs often lack legacy cylinder infrastructure.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capex/opex for fluorine electrolysis production plants | -1.1% | Global, acute in regions with high electricity costs (Europe, Japan) | Medium term (2–4 years) |

| Limited global supply of battery-grade anhydrous HF feedstock | -0.8% | Global, with supply concentrated in China; acute in North America and Europe | Short term (≤2 years) |

| Shortage of certified fluorine-handling technicians | -0.5% | Global, most acute in North America and Europe | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Capex/Opex for Fluorine Electrolysis Production Plants

Electrolyzer cells require specialized materials such as nickel-copper alloys, double-walled piping, and continuous gas monitoring systems, driving installed costs above USD 10 million for large facilities. In Europe, high electricity tariffs further increase variable costs compared to Asian plants, limiting domestic expansion and encouraging the tolling of semi-finished intermediates back to Asia.

Limited Global Supply of Battery-Grade Anhydrous HF Feedstock

China accounts for over half of global anhydrous HF production, with moisture-spec grades below 20 ppm commanding a premium. While North American investments aim to address this bottleneck, new acid plants face lengthy permitting processes, making near-term shortages likely as electric vehicle (EV) gigafactories begin operations in 2027.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: α-Fluorine Maintains Scale Advantage, β-Fluorine Gains in Niche Purity Windows

α-Fluorine accounted for 70.78% of the elemental fluorine market share in 2025, supported by long-established infrastructure used for nuclear fuel conversion and semiconductor chamber cleaning. This segment benefits from a stable customer base, proven passivation protocols, and readily available analytical standards.

β-Fluorine is projected to grow at a CAGR of 8.24% through 2031, albeit from a smaller base. Its unique reactivity for selective fluorination is increasingly valued by battery and pharmaceutical innovators. As production scales up, β-Fluorine’s contribution to the elemental fluorine market size is expected to increase, though α-Fluorine is likely to retain its dominance through the forecast period.

By Application: Electronics and Semiconductors Lead, Energy and Nuclear Outpace Growth

Electronics and semiconductors contributed 39.11% of 2025 revenues, driven by advancements in 3 nm and 2 nm fabrication technologies in Taiwan, South Korea, and the United States. On-site Generation F systems enable fabs to reduce Scope 1 emissions and adopt pay-as-you-grow models, strengthening supplier relationships.

The energy and nuclear segment is expected to achieve the highest CAGR of 8.78% between 2026 and 2031. Investments in enrichment facilities in Ohio and planned HALEU capacity in France are shifting long-term contracts toward Western suppliers. These developments are increasing demand for ultra-dry fluorine, surpassing earlier market size projections for nuclear fuel applications.

Geography Analysis

Asia-Pacific controlled 54.45% of global revenue in 2025 thanks to the clustering of display, semiconductor, and EV supply chains. Chinese producers such as Dongyue are redirecting HK$191.9 million into high-purity PTFE for chip fabs and pilot tetrafluoropropylene lines that enable low-GWP refrigerants[2].Dongyue Group Ltd., “Change in Use of Proceeds,” dongyue.com South Korean OLED expansions and Japanese fine-gas investments further strengthen the region's position, keeping Asia-Pacific on an 8.95% CAGR trajectory through 2031.

North America is regaining strategic weight as the CHIPS Act subsidizes fabs in Arizona and Texas, while the Inflation Reduction Act anchors battery-material projects in the Southeast. Centrus Energy’s Piketon HALEU project alone creates a multiyear fluorine feed for nuclear fuel blending. Domestic fluorspar scarcity persists, so most anhydrous HF feedstock still ships from Mexico and China, nudging producers toward co-located HF plants on the Gulf Coast.

Europe faces the twin pressures of elevated electricity pricing and stringent F-gas quotas. Industrial-gas majors prefer brownfield expansions in Germany and Ireland, but many refrigerant and PVDF expansions are moving to Kentucky or Jiangsu to cap opex exposure. High anhydrous HF import costs place Europe at a structural disadvantage, keeping its Elemental fluorine market growth below the global mean despite regulatory incentives for low-GWP chemistries.

Competitive Landscape

The elemental fluorine market is moderately concentrated. Five leading players account for roughly 61% of installed capacity in 2025. Linde operates more than 30 Generation F units across 11 countries with a perfect safety record over 15 years, offering unmatched process data that satisfies SEMI S2 audits. Air Liquide’s EUR 250 million Dresden complex, operational in 2027, ties the firm into a long-term supply contract with a top-three logic foundry.

Specialty chemical companies Arkema, Daikin, Solvay, and Chemours integrate backward into monomers and downstream fluoropolymers, balancing stable electronics demand against more cyclical refrigerants. Chemours’ 56% year-over-year Opteon sales growth in 2025 demonstrates the benefit of differentiated IP in a quota-tight refrigerant landscape.

Mid-tier challengers such as Kanto Denka Kogyo target a 25% share of semiconductor etching gases by 2030 through regional hubs in Xuancheng and Pyeongtaek. Smaller innovators, such as F2 Chemicals Ltd. and Valliscor, pursue high-purity organofluorine molecules for pharma APIs, but scale and certification hurdles limit near-term threat to incumbents.

Elemental Fluorine Industry Leaders

Solvay

Linde PLC

Air Products and Chemicals, Inc.

KANTO DENKA KOGYO CO., LTD.

Navin Fluorine International Limited

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Rcapital Partners LLP acquired F2 Chemicals Ltd., a United Kingdom-based manufacturer of fluorinated compounds, from Resonac Corporation, its former parent. F2 Chemicals produces elemental fluorine, which melds with organic compounds to create perfluorinated fluids.

- March 2024: Deepak Chem Tech Limited (DCTL), a wholly-owned subsidiary of Deepak Nitrite Limited, inaugurated its first fluorination plant in Dahej, Gujarat. This facility marked the group's entry into fluorine chemistry, catering to applications in pharmaceuticals, agrochemicals, and materials science.

Global Elemental Fluorine Market Report Scope

Elemental fluorine is the most reactive and electronegative chemical element. Under standard conditions, it exists as a pale yellow, highly toxic diatomic gas with a pungent, biting odor. It is the strongest known oxidizing agent, capable of causing materials such as water, glass, and asbestos to spontaneously ignite or burn with a bright flame.

The Elemental Fluorine Market is segmented into type, application, and geography. By type, the market is segmented into α-fluorine and β-fluorine. By application, the market is segmented into electronics and semiconductors, energy and nuclear, sulfur hexafluoride, chemical processing, and other applications. The report also covers the market size and forecasts for elemental fluorine in 17 countries across major regions. For each segment, the market sizing and forecasts have been done on the basis of value (USD).

| α- Fluorine |

| β- Fluorine |

| Electronics and Semiconductors |

| Energy and Nuclear |

| Sulfur Hexafluoride |

| Chemical Processing |

| Other Applications |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| NORDIC Countries | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle-East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle-East and Africa |

| By Type | α- Fluorine | |

| β- Fluorine | ||

| By Application | Electronics and Semiconductors | |

| Energy and Nuclear | ||

| Sulfur Hexafluoride | ||

| Chemical Processing | ||

| Other Applications | ||

| By Geography | Asia-Pacific | China |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| NORDIC Countries | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle-East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle-East and Africa | ||

Key Questions Answered in the Report

What is the size of the elemental fluorine market?

The elemental fluorine market stands at USD 0.88 billion in 2026 and is projected to reach USD 1.29 billion by 2031.

Which type holds the largest market share in 2025?

Α-Fluorine commanded 70.78% of revenue in 2025.

Which application is growing the fastest through 2031?

Energy and nuclear is projected to expand at an 8.78% CAGR between 2026 and 2031.

Which region dominates consumption in 2025?

Asia-Pacific accounted for 54.45% of 2025 sales and maintains the highest regional growth outlook.

Page last updated on: