Elemental Analysis Market Size and Share

Market Overview

| Study Period | 2022 - 2031 |

|---|---|

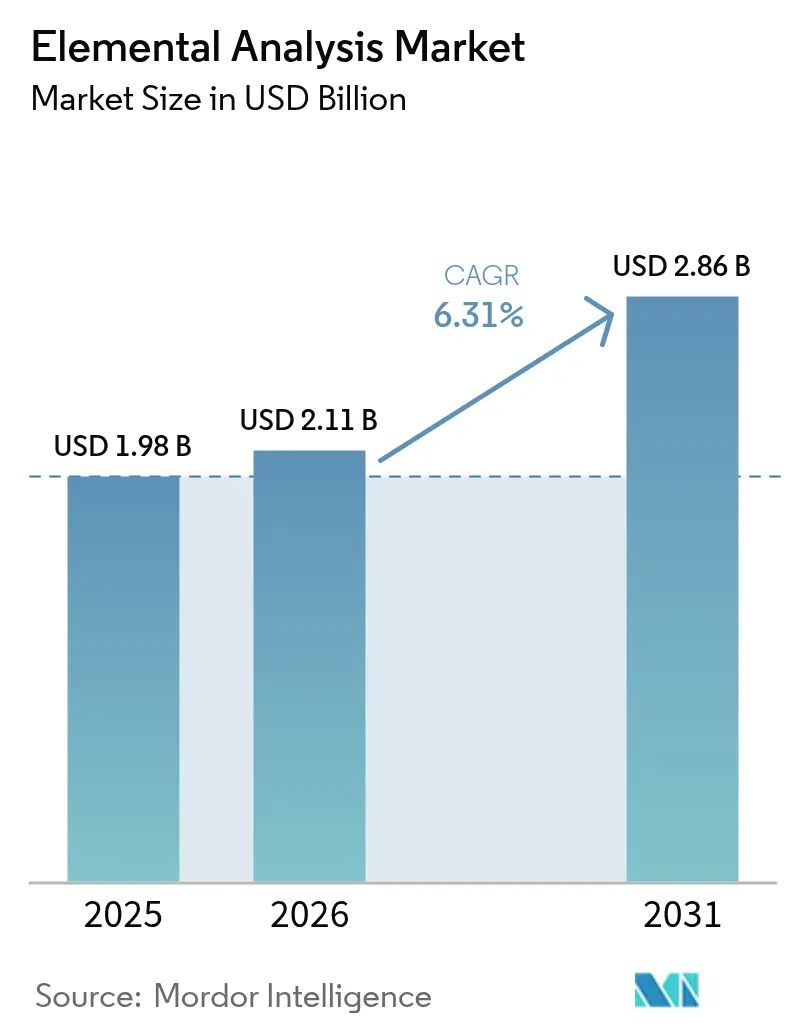

| Market Size (2026) | USD 2.11 Billion |

| Market Size (2031) | USD 2.86 Billion |

| Growth Rate (2026 - 2031) | 6.31% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Elemental Analysis Market Analysis by Mordor Intelligence

The elemental analysis market size was valued at USD 1.98 billion in 2025 and estimated to grow from USD 2.11 billion in 2026 to reach USD 2.86 billion by 2031, at a CAGR of 6.31% during the forecast period (2026-2031). Growth reflects a shift from routine quality control toward ultra-trace characterization demanded by semiconductor fabs, stringent pharmaceutical impurity limits, and widening environmental regulations. Investments in AI-enabled automation, helium-saving workflows, and hybrid multi-technique platforms strengthen vendor differentiation. Rapid semiconductor buildouts across Asia, expanding PFAS and nitrosamine limits, and robust life-science R&D budgets reinforce long-term demand. Meanwhile, capital intensity, skilled-labor shortages, and volatile carrier-gas markets temper near-term momentum.

Key Report Takeaways

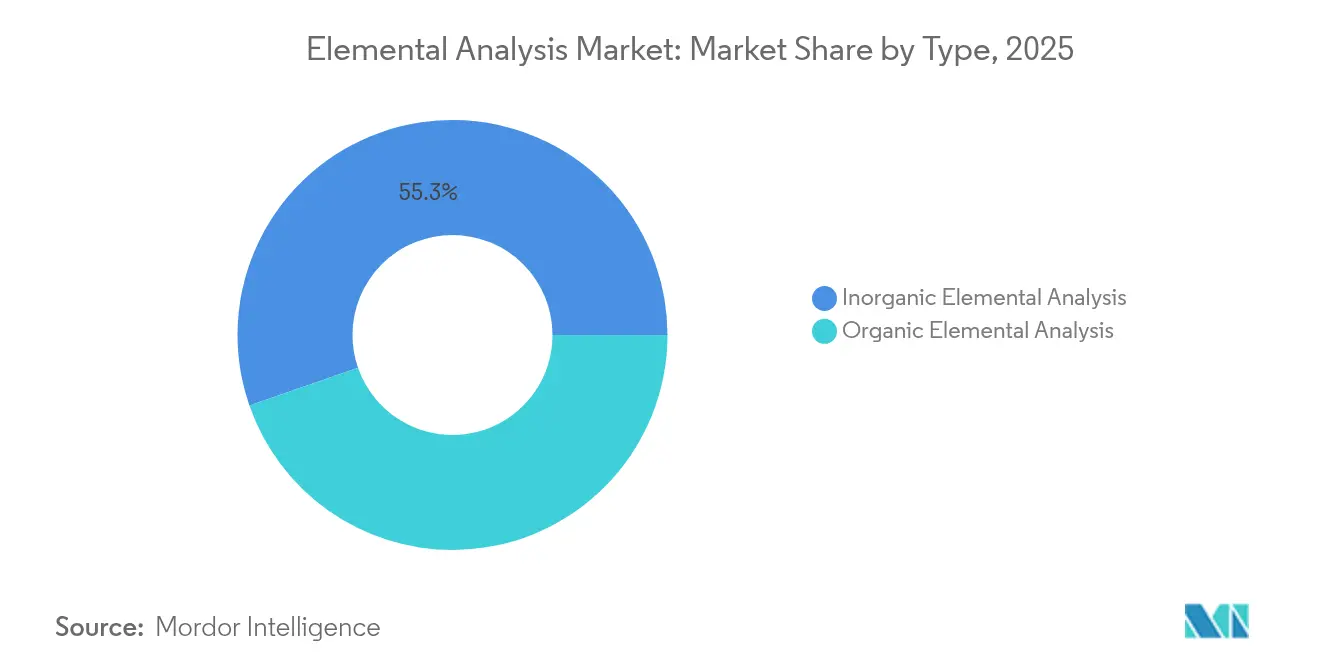

- By type, inorganic analysis led with 55.32% revenue share in 2025; organic analysis posts the fastest 7.55% CAGR to 2031.

- By technology, X-ray fluorescence held 48.85% of the elemental analysis market share in 2025, while ICP-MS is projected to grow at 8.08% CAGR through 2031.

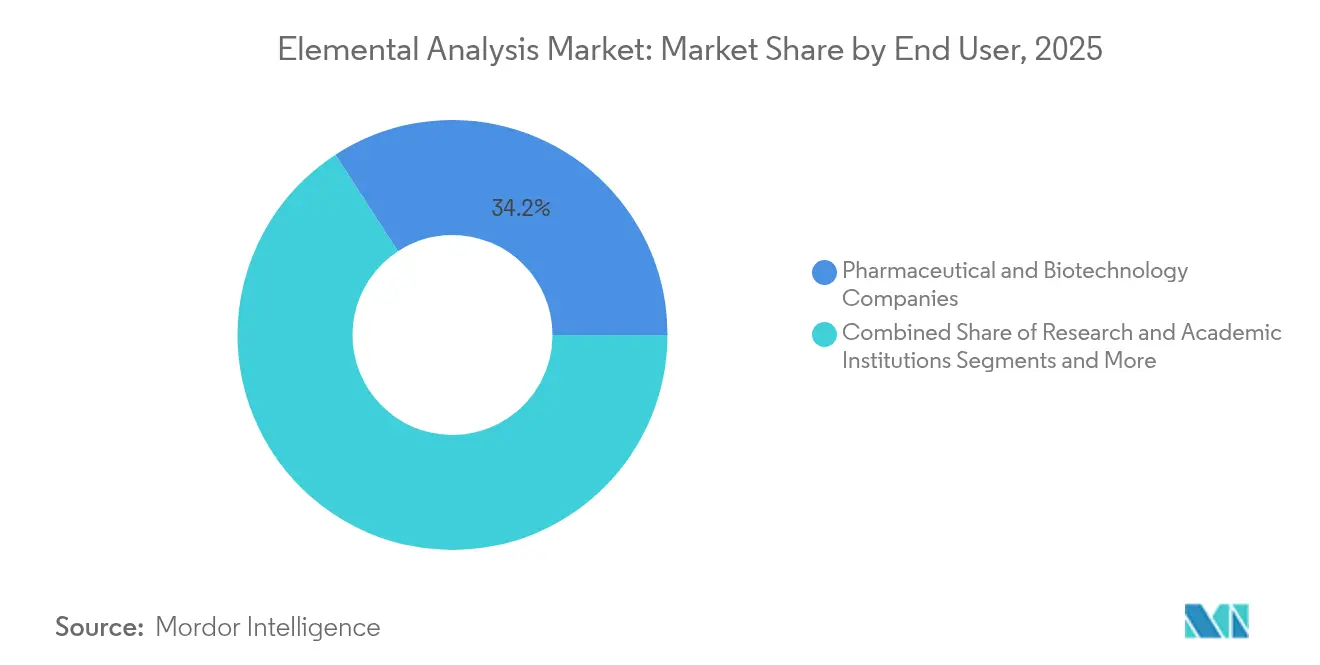

- By end user, pharmaceutical & biotechnology companies accounted for 34.17% of elemental analysis market size in 2025; environmental & food laboratories are advancing at an 8.46% CAGR.

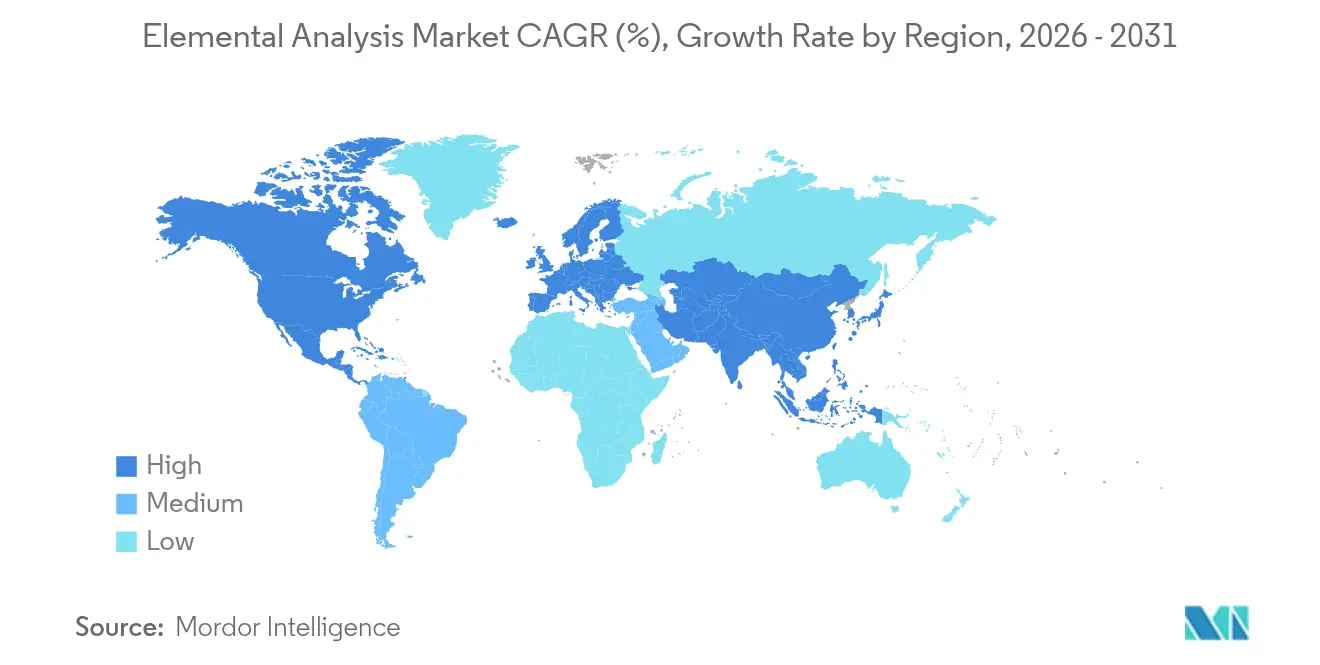

- By geography, North America commanded 35.12% revenue share in 2025; Asia-Pacific is set to deliver the highest 7.18% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Elemental Analysis Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing R&D funding in life sciences | +1.20% | North America, Europe, emerging Asia | Medium term (2-4 years) |

| Stringent elemental-impurity limits | +1.50% | Global, led by US FDA & EMA | Short term (≤ 2 years) |

| Expanding food & environmental rules | +0.80% | Global, strongest acceleration in Asia-Pacific | Medium term (2-4 years) |

| Semiconductor-grade purity demands | +1.10% | Asia-Pacific core; spill-over into North America | Long term (≥ 4 years) |

| AI-based multi-element mapping | +0.70% | Early adoption in developed markets | Medium term (2-4 years) |

| Battery-recycling ultratrace detection | +0.60% | Europe & North America lead; Asia-Pacific following | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing R&D Funding in Life Sciences

Global pharma-biotech R&D spending crossed USD 200 billion in 2024, intensifying demand for elemental impurity testing under ICH Q3D guidelines. Thermo Fisher’s multi-year USD 40-50 billion M&A pipeline underscores vendor confidence in sustained instrumentation demand. The pharmaceutical analytical-testing market itself is projected to rise from USD 9.74 billion in 2025 to USD 14.58 billion by 2030 at 8.41% CAGR, outpacing broader analytical chemistry spending. These investments solidify long-term orders for ICP-MS, ICP-OES, and combustion analyzers. Automation modules that shrink turnaround times and lower per-sample cost are increasingly bundled with spectrometers. Vendors also roll out compliance-ready software that aligns reporting directly with USP 232/233 limits.

Stringent Elemental-Impurity Limits in Global Pharmacopeias

The US FDA’s 2024 nitrosamine update created immediate compliance pressure as it tightened classification systems for trace metals. USP expanded its pharmaceutical analytical impurity library to nearly 1,000 PAIs spanning 300 APIs, compelling laboratories to broaden multi-element panels. In March 2025, the FDA launched the Chemical Contaminants Transparency Tool, signaling a persistent agency focus on metals monitoring in foods.[1]U.S. Food & Drug Administration, “Chemical Contaminants Transparency Tool,” fda.gov Rapid adoption of ready-to-use calibration standards and cloud-based reference libraries has followed. Instrument makers increasingly certify systems per 21 CFR Part 11 to reduce validation overhead for drug manufacturers. These trends keep the elemental analysis market firmly linked to evolving pharmacopeial directives.

Expanding Food & Environmental Safety Regulations

EPA Method 1633 formalized PFAS testing across matrices in 2024, joining Canada’s 30 ng/L drinking-water objective for 25 PFAS and the EU’s pending PFHxA restrictions. Analysts estimate US remediation liabilities exceeding USD 220 billion, creating an unprecedented flow of samples to contract labs. Environmental testing laboratories therefore record the quickest revenue climb at 8.9% CAGR. Technique demand is shifting toward high-throughput ICP-MS equipped with collision/reaction cells to mitigate interferences. Portable XRF and LIBS units are also making inroads in field screening to prioritize samples. Trace-metal screening in fresh produce and rice has expanded in India and Vietnam under new food-code amendments, broadening the addressable elemental analysis market.

Semiconductor-Grade Purity Requirements for Advanced Chips

Government incentives across Japan, India, and the United States continue to accelerate 3-nm and 4-nm fab construction. Achieving 9N to 11N purity in silicon, copper, and process chemicals requires detection limits below 10 ppt. Thermo Fisher’s Vulcan Automated Lab, launched in March 2025, combines robotics with ICP-MS to process 200 wafers nightly at <100 ng/L detection limits. Agilent’s Advanced Valve System adds 100 extra samples per day to the 7850 line, directly addressing fab throughput targets. These innovations feed sustained double-digit spending on ultratrace instrumentation, keeping the elemental analysis market on its current growth trajectory.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital & maintenance costs | −0.9% | Global, pronounced in emerging markets | Short term (≤ 2 years) |

| Shortage of cross-trained analytical chemists | −0.6% | North America & Europe | Medium term (2-4 years) |

| Complex sample-prep workflows | −0.4% | Application-dependent global impact | Short term (≤ 2 years) |

| Global helium shortages | −0.8% | Severe in North America | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High capital & maintenance costs

Single-quadrupole ICP-MS units typically list between USD 100,000 and USD 200,000, while triple-quadrupole or high-resolution models can exceed USD 400,000, placing a heavy upfront burden on mid-size laboratories. Annual operating expenses compound the challenge: gas, power, and consumables push yearly running costs for an ICP-MS to about USD 13,250, more than double the bill for an ICP-OES setup. Vendors generally recommend full-service contracts priced at 10% of the purchase value each year to cover detector replacement, preventive maintenance, and software updates. Even where financing spreads capital outlays, hidden costs such as facility upgrades for exhaust handling and clean power can add another 15-20% to project budgets, slowing adoption in emerging markets. As helium prices rise and supply tightens, labs face further escalation in direct operating expenditures, prompting many to postpone instrument refresh cycles or pivot to rental models.

Global Helium Shortages Inflating ICP-MS Operating Budgets

Helium spot prices climbed to USD 14 per m³ in 2023, with labs receiving only 45-65% of allocations, causing downtime in trace-metal workflows. Peak Scientific reports a 70% rise in helium-generator inquiries as users seek independence from bulk supply. Shimadzu publishes method-translation kits that swap helium for hydrogen or nitrogen, cutting carrier-gas costs by up to 90% without sacrificing detection limits. Vendors are also shipping collision-cell ICP-MS models optimized for argon/hydrogen mixes, mitigating operating risk and sustaining sample throughput.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Inorganic Analysis Dominance Meets Organic Growth Acceleration

Inorganic analysis captured 55.32% of the elemental analysis market share in 2025, buoyed by USP 232/233 compliance and semiconductor contamination control. ICP-MS and ICP-OES platforms dominate this segment, delivering sub-ng/L detection of As, Pb, and Cd in drug products and high-purity chemicals. Semiconductor foundries demand routine certification of 9N-grade process chemicals, further anchoring instrument placements. Vendor emphasis is shifting toward hybrid systems that bundle inorganic metals detection with options for halogen and sulfur mapping, extending platform utility across QA labs. Capital expenditure is sustained by extended service contracts that guarantee <1 ppt baseline drift, assuring fabs of long-term analytical reproducibility.

Organic elemental analysis, while smaller, is growing at 7.55% CAGR—faster than the overall elemental analysis market. Combustion-based CHNSO analyzers address drug-development needs for molecular formula confirmation and are now equipped with 90-position autosamplers offering 5-minute cycle times. Food-safety labs adopt the same platforms to quantify protein, fat, and moisture, expanding the customer base beyond pharma and petrochemicals. Vendors introduce dual oven configurations that measure high-temperature polymers alongside low-temperature agro-samples, reducing idle time. Coupled software allows seamless import of LIMS metadata, trimming post-run validation.

By Technology: XRF Leadership Challenged by ICP-MS Innovation

X-ray fluorescence sustained a 48.85% share of the elemental analysis market in 2025 owing to its non-destructive character and broad matrix tolerance. Petrochemical refineries use benchtop XRF for sulfur in fuels, while art conservators rely on handheld-units for pigment screening. The latest Vanta Element handheld incorporates a graphene window and IP65 sealing for harsh-field deployments. Ongoing advances in silicon-drift detectors now extend sensitivity down to Mg and Al, expanding coverage to light-element geoscience applications.

ICP-MS records the fastest 8.08% CAGR to 2031, pushing elemental analysis market size for ultratrace detection to new records. Collision-cell designs, triple-quadrupole geometries, and new dry-plasma introduction systems drive detection limits below 1 ng/L even in high-matrix samples. Semiconductor customers increasingly bundle robots for unattended overnight runs, boosting daily sample counts above 400. Pharmaceutical QC labs value the technique’s ability to report 24 ICH metals in a single two-minute scan, cutting per-sample reagent costs in half. As helium shortages intensify, vendors add hydrogen mode that maintains low backgrounds, protecting long-term throughput.

By End User: Pharmaceutical Dominance Versus Environmental Testing Surge

Pharmaceutical & biotechnology companies generated 34.17% revenue in 2025, anchored by mandatory elemental-impurity limits and a surging biologics pipeline. This clientele prioritizes 21 CFR Part 11-ready software, instrument uptime guarantees, and service-level agreements aligning with batch-release cycles. Regulatory harmonization across the FDA, EMA, and PMDA accelerates analytic method transfers among global sites, driving multi-instrument roll-outs inside big pharma networks.

Environmental & food laboratories post an 8.46% CAGR as PFAS limits, micro- and nano-plastics surveillance, and heavy-metal scrubbing in baby food expand test menus. Eurofins alone operates 900 labs with 200,000 accredited methods, signaling the scale of outsourced demand. These labs increasingly procure turnkey containerized ICP-MS suites for pop-up deployment near remediation hotspots, minimizing sample hold times. Automated dilution stations and barcode-driven chain-of-custody modules curb labor costs and compliance risks.

Geography Analysis

North America held 35.12% of revenue in 2025 on the strength of FDA impurity guidelines, EPA PFAS mandates, and world-leading pharma output.]US drugmakers account for over 40% of global clinical pipelines, sustaining steady instrument orders, while Canada’s mining sector fuels XRF placements for grade control. Mexico’s rising contract-manufacturing activity, supported by Shimadzu’s new subsidiary, widens the regional user base.

Asia-Pacific is projected to deliver a 7.18% CAGR, the fastest worldwide, as governments subsidize advanced chip fabs and domestic drug production capabilities. Japan’s 2-nm pilot lines and India’s USD 100.2 billion semiconductor roadmap enlarge the addressable elemental analysis market through ultratrace purity specifications. China’s push for materials self-sufficiency drives demand for ICP-MS, while South Korea’s battery gigafactories purchase LIBS systems for inline cathode inspection. Australia’s mining exports sustain XRF sales for bulk-ore screening.

Europe grows steadily on the back of stringent PFAS restrictions and strong vaccine manufacturing clusters in Germany and France. The EU’s battery-recycling directive, targeting a 50-fold capacity increase by 2030, lifts orders for ultratrace metals analyzers. The United Kingdom emphasizes nitrogen-pressurized ICP-MS to mitigate helium volatility, and Nordic nations deploy LIBS for rapid slag monitoring in green-steel pilot plants. Eastern European mining expansions in Poland and Serbia add new sales channels, while Middle East copper projects and South American lithium brine operations open supplementary opportunities.

Competitive Landscape

The elemental analysis market shows moderate concentration, with the top five companies controlling a significant portion of global revenue. Thermo Fisher Scientific, Agilent Technologies, and Bruker Corporation combine scale, broad product portfolios, and embedded software ecosystems to anchor market leadership. ICP-MS innovation and AI-enabled XRF mapping form the core battlegrounds for differentiation.

M&A activity remained brisk in 2024-2025. Thermo Fisher’s USD 4.1 billion acquisition of Solventum’s purification & filtration unit enlarges its bioprocessing reach and cross-sells analytical hardware. Analytik Jena consolidated an ICP-MS line to deepen environmental-lab penetration. Bruker purchased Optimal Group, adding automation software that integrates mass spectrometry and optical spectroscopy on a single control layer.

Strategic roadmaps emphasize helium-free carrier modes, robotic sample preparation, and cloud analytics. Vendors pilot subscription models bundling hardware, consumables, and software, smoothing customer CapEx and unlocking recurring revenue. Portable analyzers gain attention for process industries seeking real-time decision loops. While established players guard IP through aggressive patent filings, niche firms target specific use-cases such as LIBS for battery raw materials or CHNSO analyzers for biofuels, keeping innovation cycles vibrant.

Elemental Analysis Industry Leaders

-

Eurofins Scientific

-

Agilent Technologies, Inc.

-

Rigaku Corporation

-

Verder Scientific GmbH & Co. KG (ELTRA GmbH)

-

PerkinElmer Inc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Bruker launched the timsMetabo platform for PFAS and small-molecule detection.

- March 2025: Thermo Fisher introduced the Vulcan Automated Lab, which targets semiconductor purity workflows.

- February 2025: Thermo Fisher Scientific agreed to acquire Solventum’s Purification & Filtration Business for USD 4.1 billion.

- February 2025: Analytik Jena completed an ICP-MS business acquisition, expanding its elemental analysis portfolio.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study considers the elemental analysis market to include laboratory-grade instruments, associated consumables, and enabling software that determine the qualitative or quantitative elemental composition of organic or inorganic samples through destructive techniques (ICP-OES, ICP-MS, combustion analyzers) as well as nondestructive methods (X-ray fluorescence, FT-IR, LIBS). Equipment sold for metallurgical spectrometry, semiconductor wafer inspection, and field-portable analyzers is counted only when its primary function is elemental quantification.

Scope exclusion: services limited to contract testing or turnkey analytical laboratories are outside the sizing.

Segmentation Overview

-

By Type

- Organic Elemental Analysis

- Inorganic Elemental Analysis

-

By Technology

-

Destructive Technologies

- ICP-Atomic Emission Spectroscopy (ICP-AES)

- ICP-Mass Spectrometry (ICP-MS)

- Combustion Analysis (CHNS/O)

- Others

-

Nondestructive Technologies

- X-Ray Fluorescence Spectroscopy (XRF)

- Fourier Transform Infrared Spectroscopy (FTIR)

- Laser-Induced Breakdown Spectroscopy (LIBS)

- Others

-

Destructive Technologies

-

By End User

- Pharmaceutical & Biotechnology Companies

- Research & Academic Institutions

- Environmental & Food Testing Laboratories

- Industrial & Manufacturing

- Others

-

By Geography

-

North America

- United States

- Canada

- Mexico

-

Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

-

Asia Pacific

- China

- Japan

- India

- South Korea

- Australia

- Rest of Asia Pacific

-

Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

-

South America

- Brazil

- Argentina

- Rest of South America

-

North America

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed quality-control managers in U.S. and German pharma labs, environment-testing directors across India, and process-control engineers at semiconductor fabs in Taiwan and Texas. These conversations validated sample-prep throughput assumptions, current instrument utilization rates, and price erosion curves that the desk work alone could not clarify.

Desk Research

We began by mapping publicly available data sets, using sources such as the US Food & Drug Administration elemental-impurity guidelines, Eurostat's trade codes for spectrometers, the United Nations Comtrade export records, NIH and Horizon Europe R&D budgets, and environmental monitoring statistics from the US EPA and the European Environment Agency. Financial details for listed instrument vendors were retrieved from SEC 10-Ks and annual reports, while scholarly insights were gathered from open-access journals like Spectrochimica Acta and patent families screened via Questel. Our team also screens press releases indexed on Dow Jones Factiva and company profiles on D&B Hoovers to capture product launch cadence and average selling prices. The desk-research sources noted are illustrative, not exhaustive.

A second pass links macro indicators, pharmaceutical capex, semiconductor wafer starts, and global helium prices to elemental analysis demand, ensuring the model mirrors real economy cycles. This is where Mordor Intelligence tightens scope boundaries that some publishers leave vague.

Market-Sizing & Forecasting

We employ a top-down construct anchored on laboratory capital-equipment outlays, import-export flows, and installed-base renewal cycles, which are then cross-checked through selective bottom-up roll-ups of sampled unit shipments and ASPs shared confidentially by channel partners. Variables that feed the model include: 1) pharma elemental-impurity filings, 2) number of accredited environmental labs, 3) 200 mm and 300 mm wafer starts, 4) global helium spot prices, and 5) academic spectroscopy grant awards. Forecasts are generated with a multivariate regression that captures elasticity between these drivers and historical instrument revenues, before scenario analysis adjusts for helium supply shocks and regulatory step-ups.

Data Validation & Update Cycle

Outputs pass variance tests against independent shipment tallies and customs codes; anomalies trigger peer review and re-contact with key informants. Reports refresh each year, and an interim update is released when material events, such as a sudden helium shortage, shift any core variable. A final analyst check ensures clients receive the latest calibrated view.

Why Our Elemental Analysis Baseline Earns Confidence

Published figures often diverge because firms pick different instrument families, apply dissimilar ASP deflators, or update models irregularly. By tying scope strictly to laboratory-grade elemental analyzers and refreshing every twelve months, Mordor keeps variance tight.

Major gap drivers with other publishers include: inclusion of contract testing revenue, extrapolating average prices from narrow regional samples, and adopting a single growth factor instead of variable-level forecasting.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.98 B (2025) | Mordor Intelligence | - |

| USD 1.77 B (2023) | Global Consultancy A | Counts only instrument sales reported by listed firms, omits consumables, older base year |

| USD 1.90 B (2024) | Trade Journal B | Uses flat ASP across regions and rolls forward with uniform 5 % CAGR |

The comparison shows that, by selecting the right scope elements and stress-testing variables each year, Mordor delivers a balanced, transparent baseline that decision-makers can replicate and defend.

Key Questions Answered in the Report

What is the current size of the elemental analysis market?

The elemental analysis market is valued at USD 2.11 billion in 2026 and is forecast to hit USD 2.86 billion by 2031.

Which technology segment is growing fastest?

ICP-MS is projected to post the highest 8.08% CAGR because of ultratrace detection needs in semiconductors and pharmaceuticals.

Why is Asia-Pacific the fastest-growing region?

Aggressive semiconductor investments in Japan, India, and China, coupled with expanding pharma manufacturing, propel a 7.18% CAGR for the region.

How are helium shortages affecting laboratories?

Helium prices have surged, prompting labs to adopt hydrogen or nitrogen carrier gases and invest in gas generators to maintain ICP-MS operations.

Which end-user group dominates spending?

Pharmaceutical and biotechnology companies accounted for 34.17% of 2025 revenue due to mandatory elemental impurity testing requirements.

Page last updated on: