Circular Dichroism Spectrometers Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

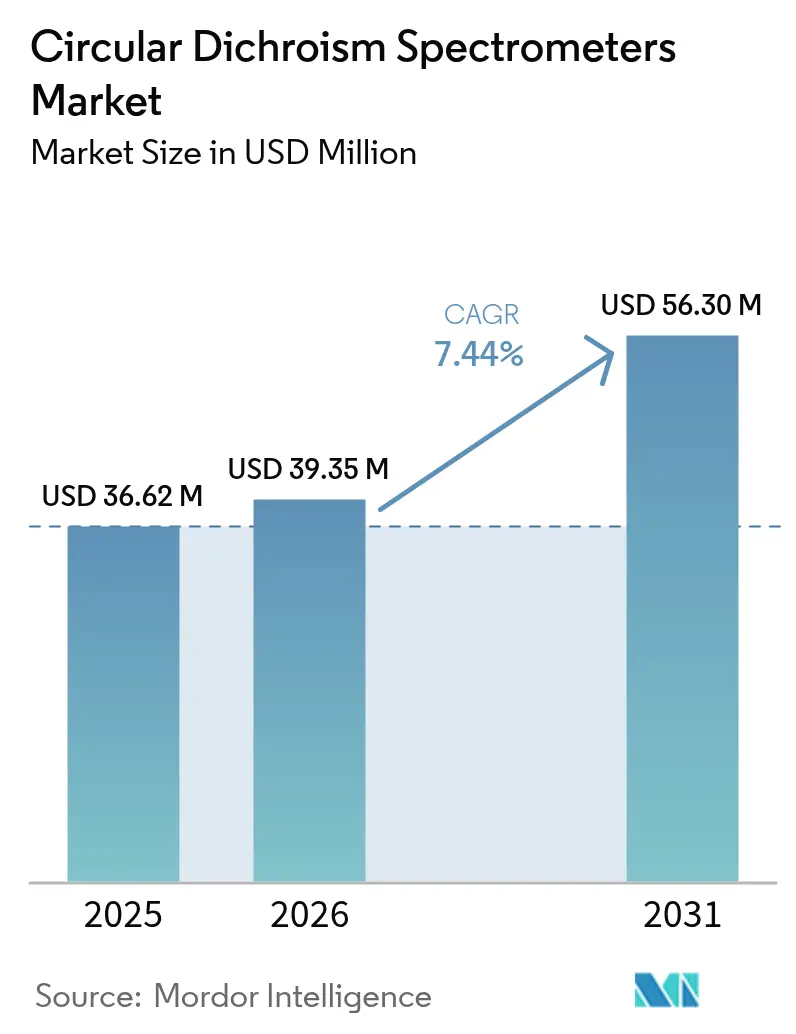

| Market Size (2026) | USD 39.35 Million |

| Market Size (2031) | USD 56.3 Million |

| Growth Rate (2026 - 2031) | 7.44% CAGR |

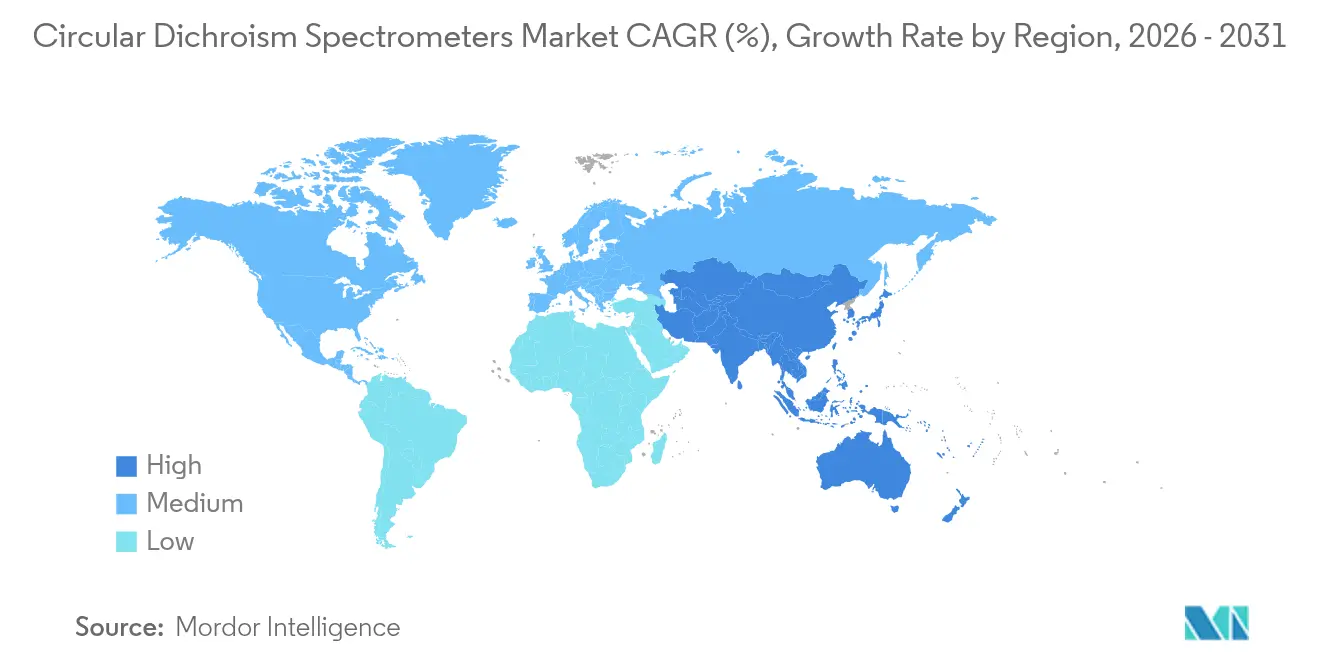

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

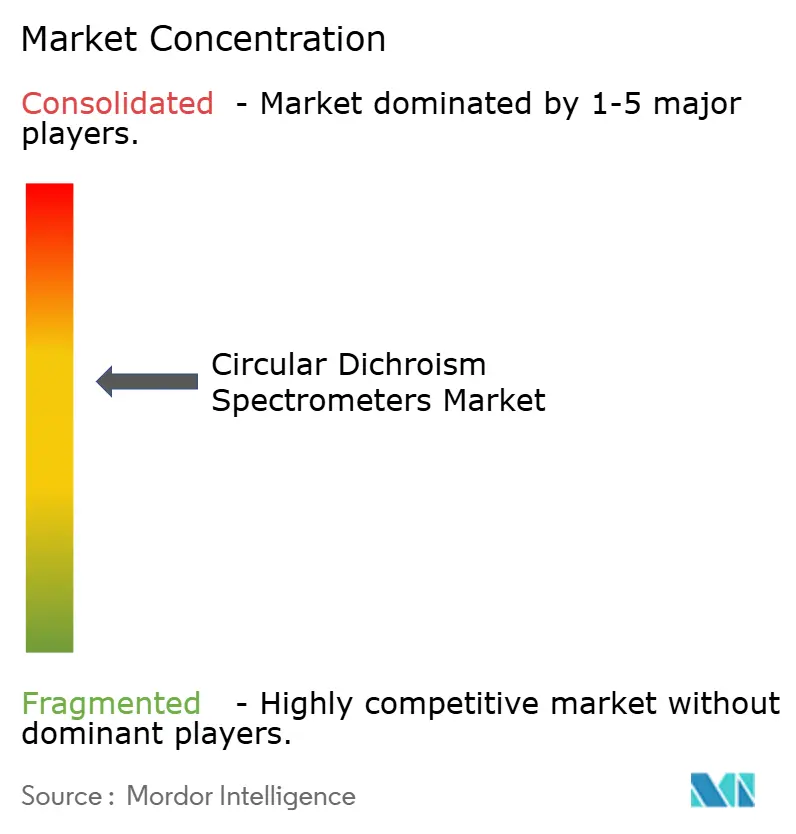

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Circular Dichroism Spectrometers Market Analysis by Mordor Intelligence

The Circular Dichroism Spectrometers market size was valued at USD 36.62 million in 2025 and estimated to grow from USD 39.35 million in 2026 to reach USD 56.3 million by 2031, at a CAGR of 7.44% during the forecast period (2026-2031). In practice, the sector’s momentum is anchored in biopharmaceutical manufacturing scale-up, rising biosimilar pipelines, and tighter FDA-EMA expectations for higher-order protein structure validation[1]U.S. Food and Drug Administration, “Biosimilarity and Interchangeability Guidance,” fda.gov. Demand is additionally supported by NIH and NSF funding streams that keep academic core facilities well capitalized. Supply-side advances—most notably benchtop automation and quantum-cascade-laser vibrational CD—lower per-sample costs and broaden usability. Meanwhile, mid-sized contract research organizations (CROs) increasingly purchase multi-user systems and convert capital outlays into fee-for-service revenues, injecting new volume into the Circular Dichroism Spectrometers market. Technology convergence around process analytical technology further insulates vendors from routine research budget swings, embedding instruments directly into continuous biologics production lines.

Key Report Takeaways

- By product type, benchtop instruments led with 44.78% of Circular Dichroism Spectrometers market share in 2025, while floor-standing systems are poised for the quickest uptake through 2031.

- By technology, electronic CD accounted for 54.88% share of the Circular Dichroism Spectrometers market size in 2025; synchrotron radiation CD is projected to log the fastest CAGR over the same horizon.

- By application, protein secondary-structure determination held 25.21% of the Circular Dichroism Spectrometers market size in 2025, whereas biosimilar comparability testing is on track for the sharpest growth to 2031.

- By end-user, pharmaceutical and biotechnology companies captured 42.15% revenue share of the Circular Dichroism Spectrometers market in 2025; CROs and CMOs are expected to grow at the highest pace.

- By geography, North America retained 38.10% share of the Circular Dichroism Spectrometers market in 2025, but Asia-Pacific is expanding at an 8.41% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Circular Dichroism Spectrometers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Expansion of global biopharmaceutical manufacturing | +1.8% | North America, EU, China | Medium term (2-4 years) |

| Rising R&D expenditure in life sciences instrumentation | +1.2% | North America & EU core; spill-over to APAC | Long term (≥4 years) |

| Technological innovations in circular dichroism hardware | +0.9% | Global | Short term (≤2 years) |

| Growing demand for protein structure analysis in drug discovery | +1.4% | North America, EU, China | Medium term (2-4 years) |

| Increasing academic funding for structural biology research | +0.7% | North America & EU | Long term (≥4 years) |

| Emergence of integrated spectroscopy platforms for process analytical technology | +0.6% | Global | Short term (≤2 years) |

| Source: Mordor Intelligence | |||

Expansion of Global Biopharmaceutical Manufacturing

Biologic plants shifting toward continuous production embed CD probes directly into process lines for real-time folding validation, driving higher-throughput specifications and favoring floor-standing systems. Bruker’s 2024 revenue spike of USD 3.37 billion underscores the instrumentation pull-through tied to these capital projects. Vendors now bundle automated cuvette changers and GMP-ready software, shortening operator intervention time and aligning with 21 CFR Part 11 expectations. Larger batch-release volumes encourage multi-year service contracts that lock in annuity revenue. Together, these factors add a sturdy compliance floor beneath the Circular Dichroism Spectrometers market.

Rising R&D Expenditure in Life Sciences Instrumentation

NIH’s FY 2025 request of USD 50.1 billion keeps grant-backed lab upgrades on pace, while the NSF’s USD 40 million protein-design initiative anchors demand for advanced structure-validation kits[2]National Science Foundation, “Protein Design Initiative,” nsf.gov. Academic consortia consolidate purchasing power, opting for benchtop instruments equipped with AI-driven spectral deconvolution that handles diverse protein libraries. Procurement cycles increasingly specify multi-detector packages, rewarding manufacturers able to ship turn-key systems. These funding dynamics promote steady instrument refresh intervals, buttressing the Circular Dichroism Spectrometers market.

Technological Innovations in Circular Dichroism Hardware

JASCO’s quantum-cascade-laser vibrational CD unit moves routine scans from minutes to seconds, letting formulators identify chiral impurities early in discovery workflows. CRAIC Technologies follows with CD microspectroscopy capable of single-cell resolution, extending utility into cell-therapy quality checks. Such premium instruments push the upper limit of average selling prices even as unit volumes stay modest. At the same time, component miniaturization filters down to entry-level benchtop systems, expanding total addressable installations. Rapid innovation reinforces vendor differentiation and sustains a healthy Circular Dichroism Spectrometers market.

Growing Demand for Protein Structure Analysis in Drug Discovery

FDA biosimilar guidance mandates higher-order structure equivalence, cementing CD as a staple assay across originator and follow-on products. Harvard Medical School’s core facility doubled CD usage hours in 2024 to validate ligand-induced conformational shifts. Fragment-based screening groups appreciate CD’s solution-state readout, which reduces crystal-formation bottlenecks. These laboratory realities translate into predictable reorder cycles for light sources, cells, and nitrogen purifiers, adding service revenue layers that enhance vendor margins inside the Circular Dichroism Spectrometers market.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital and operational costs of CD systems | -1.1% | Global; most acute in emerging markets | Short term (≤2 years) |

| Limited availability of trained spectroscopy professionals | -0.8% | Global; pronounced in APAC | Medium term (2-4 years) |

| Growing preference for high-resolution alternative methods | -0.7% | North America & EU | Long term (≥4 years) |

| Regulatory validation challenges for new CD technologies | -0.4% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital and Operational Costs of CD Systems

Premium systems can exceed USD 250,000 once GMP software and service agreements are added, straining capital budgets for first-time buyers. Supply-chain tariffs risk adding 10–15% to landed costs for U.S. importers of optics sub-assemblies[3]American Chemical Society, “Trade Tariff Impacts on Lab Instruments,” cen.acs.org. Operational expenses include liquid-nitrogen logistics, lamp replacements, and specialized calibrants, lifting total cost of ownership. Shared-facility models relieve part of that burden but produce reservation bottlenecks that deter time-sensitive experiments. These factors collectively temper high-growth optimism for the Circular Dichroism Spectrometers market in price-sensitive regions.

Limited Availability of Trained Spectroscopy Professionals

Undergraduate curricula seldom cover CD spectroscopy, leaving early-career chemists dependent on vendor workshops for method proficiency. Global CROs often recruit internationally to fill skill gaps, which increases onboarding costs and risks turnover. Automated analysis software helps, yet advanced troubleshooting still demands human expertise. This talent bottleneck slows instrument utilization ramp-up, creating latent capacity that masks potential demand in the Circular Dichroism Spectrometers market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Benchtop Systems Drive Routine Applications

Benchtop units delivered a commanding 44.78% share of Circular Dichroism Spectrometers market size in 2025 by meeting everyday protein-fold screening needs of academic labs and mid-tier biotechs. Laboratories choose them for compact footprints, rapid scan modes, and optional automated plate readers. Floor-standing models, although fewer in absolute shipments, record the fastest unit growth because continuous-manufacturing lines require 24/7 reliability and higher s/n ratios. Specialty SRCD beamline configurations, housed at national light-sources, serve niche membrane-protein projects where extended wavelengths matter. The Harvard Medical School installation of dual J-1500s illustrates how benchtops remain central to high-throughput stability studies. Over the forecast, benchtops will continue to dominate replacement cycles, while floor-standing platforms capture green-field plants, keeping a balanced revenue mix inside the Circular Dichroism Spectrometers market.

In parallel, product upgrades blur lines between categories. Vendors now retrofit benchtops with robotic autosamplers once exclusive to large systems, letting smaller labs process 96-well plates overnight. Conversely, floor-standing models incorporate modular optics so users swap in UV, visible, or mid-IR heads without factory service visits. This feature parity compresses the historical price spread yet supports differentiated value propositions around throughput and robustness. Ultimately, evolving lab workflows ensure both product classes expand, reinforcing the broad opportunity base across the Circular Dichroism Spectrometers market.

By Technology: Electronic CD Maintains Dominance Despite Emerging Alternatives

Electronic CD still held 54.88% of Circular Dichroism Spectrometers market share in 2025 because its far-UV range delivers the alpha-helix and beta-sheet fingerprints prized by protein scientists. The method’s mature validation guides ease regulatory submissions, making it the default for batch-release assays. Synchrotron Radiation CD, while confined to beamline access, posts the briskest CAGR as national facilities open industrial queue time and deliver wavelengths down to 170 nm unattainable on conventional optics. Vibrational CD elbows into chiral-small-molecule QA/QC, though current users remain pharma stereochemistry groups ready to pay for quantum-cascade-laser sources. JASCO’s mid-IR quantum-cascade bench system demonstrates that VCD can migrate from niche to daily workflow by shortening acquisition times from hours to minutes.

Cross-pollination among these technologies is growing. Software packages increasingly allow spectral overlay across electronic and vibrational regimes, providing a single-view protein backbone plus side-chain chirality. Portable SRCD add-ons are under evaluation, but beamtime availability stays the gating factor. Over the outlook, Electronic CD will remain the workhorse while SRCD and VCD supply premium margins, preserving a tiered pricing architecture across the Circular Dichroism Spectrometers market.

By Application: Biosimilar Testing Accelerates Growth

Protein secondary-structure determination represented 25.21% of Circular Dichroism Spectrometers market size in 2025 because every new biologic or vaccine candidate passes through early fold confirmation. Yet biosimilar comparability testing outpaces all other uses thanks to the ICH Q6B mandate for higher-order structure matching. CD’s speed and low sample consumption make it a frontline assay before more resource-intensive hydrogen-deuterium exchange or cryo-EM. Creative Proteomics’ expansion of far-UV CD services exemplifies how CROs monetize this regulatory need. Downstream, routine batch-release testing stays steady, and fragment-based drug-discovery screens broaden the customer base to small biotech startups.

Vaccinology projects inject further upside. mRNA platforms depend on correct folding of lipid-nanoparticle encapsulation proteins, a parameter CD reads quickly without extensive purification. Field-deployable CD modules are under pilot in GMP fill-finish suites, where operators verify protein antigens inline during lot release. Such new-use cases diversify revenue channels and support the resilient expansion of the Circular Dichroism Spectrometers market.

By End-User: CRO Outsourcing Transforms Market Dynamics

Pharmaceutical and biotechnology companies together accounted for 42.15% revenue in 2025, purchasing instruments for core R&D and lot release. However, CROs and CMOs record the sharpest volume uptake because they service multiple sponsors, maximizing utilization per capital dollar. Agilent’s Life Sciences segment posted USD 647 million in Q1 2025, attributing part of its 4% rise to outsourced analytical testing growth. Academic and government labs, fueled by NIH block grants, sustain a steady refresh cadence but rarely surge beyond single-digit growth. Hospital diagnostic labs remain experimental users, piloting CD for conformational disease biomarkers, a niche that could mature post-2030.

Outsourcing momentum reorganizes the sales funnel. Vendors increasingly negotiate fleet-level agreements with CRO holding groups, bundling multi-year service plus remote calibration. This shift nudges product-mix toward high-capacity instruments with validated 21 CFR Part 11 audit trails. As these trends evolve, all customer classes benefit from economies of scale, ensuring a well-distributed demand base across the Circular Dichroism Spectrometers market.

Geography Analysis

North America retained 38.10% of Circular Dichroism Spectrometers market share in 2025, buoyed by mature biologics pipelines, FDA’s rigorous analytical expectations, and a well-funded academic ecosystem. The NIH’s 2025 appropriation of USD 50.1 billion guarantees consistent instrument refresh rates at shared facilities. A possible 10-15% tariff on critical optics assemblies could lift short-term prices, but warranty discounts and lease models cushion the blow. Canada’s vaccine-manufacturing build-out amplifies regional procurement, particularly for floor-standing CD lines designed for GMP production floors.

Asia-Pacific is the fastest-expanding arena at an 8.41% CAGR through 2031, propelled by China’s modern biologic clusters, India’s aggressive biosimilar targets, and Japan’s investment in regenerative medicine quality tools. Chinese CD vendors focus on cost-optimized benches, but global players win large-capacity orders at multinational joint-ventures needing FDA-ready validation packages. India’s state-sponsored biotech parks bundle equipment financing, unlocking demand among start-ups. This regional momentum reduces historical dependency on imported second-hand gear and accelerates premium segment penetration across the Circular Dichroism Spectrometers market.

Europe exhibits balanced but slower growth, stabilizing around large pharma refurbishments and Horizon Europe research calls. Germany and Switzerland continue to invest in high-precision CD for membrane-protein drug work, while the UK’s post-Brexit customs shifts require longer planning windows for instrument delivery. Eastern European CROs emerge as price-competitive service hubs, purchasing mid-tier CD units to attract western sponsors. Smaller but notable gains surface in Latin America and the Middle East, where local vaccine initiatives spur pilot lab construction. However, limited spectroscopy talent and sporadic funding cycle volatility temper near-term upside in those regions.

Competitive Landscape

The circular dichroism spectrometers market shows moderate fragmentation. JASCO, Bruker, and Applied Photophysics hold entrenched channel relationships and comprehensive portfolios ranging from entry benches to SRCD systems. Bruker leverages its USD 3.37 billion 2024 revenue base to cross-bundle CD with NMR and FTIR packages, capturing enterprise-wide capital allocations. JASCO differentiates with rapid-scan UV-CD and turnkey pharma-compliance software suites, while Applied Photophysics champions stopped-flow CD for kinetic studies, an under-served niche.

Emerging firms inject disruptive pressure. CRAIC Technologies’ single-cell CD microscope at sub-micron resolution targets cell-therapy QC, a frontier unavailable to incumbent designs. Hinds Instruments integrates CD with plate readers, shortening lead-times for fragment library screens. Broader analytical giants, including Thermo Fisher Scientific, showcase complementary platforms at global expos, signaling potential entry via acquisition or internal R&D.

Strategic rivalry increasingly centers on software ecosystems. Vendors that furnish AI-powered spectral deconvolution and GMP-grade audit trails command higher average selling prices and lock in aftermarket revenue. Service portfolios—spanning preventive maintenance, operator certification, and 24/7 remote diagnostics—serve as tiebreakers in competitive bids. With high technical barriers but visible consolidation pathways, market players actively explore alliances to shrink development costs and broaden geographic reach, knitting an evolving yet stable environment for the circular dichroism spectrometers market.

Circular Dichroism Spectrometers Industry Leaders

JASCO

Bruker

Applied Photophysics

Bio-Logic Science Instruments

Hinds Instruments

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: CRAIC Technologies launched a CD microspectroscopy platform that merges circular dichroism and high-resolution microscopy for single-cell analysis.

- April 2025: Bruker reported Q1 2025 revenue of USD 801.4 million, up 11% year-on-year, citing BioSpin segment strength.

- April 2024: Thermo Fisher Scientific displayed advanced FTIR and diffraction tools that complement CD spectroscopy at Analytica 2024.

- March 2024: JASCO introduced J-1700 and J-1500 CD spectrophotometers with faster scan speeds for high-throughput workflows.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the circular dichroism spectrometers market as all factory-built instruments whose primary function is to quantify differential absorption of left- versus right-hand circularly polarized light for chiral or secondary-structure analysis of biomolecules and small molecules. Only stand-alone benchtop, floor-standing, synchrotron-beamline, and micro-CD units shipped new are counted; software upgrades, service contracts, or CD add-on modules for other spectrometers are not.

Scope exclusion: hybrid multi-tech platforms sold primarily for fluorescence or Raman workflows are outside scope.

Segmentation Overview

- By Product Type

- Benchtop CD Spectrometers

- Floor-Standing CD Spectrometers

- SRCD Beamline Instruments

- CD Microspectrometers

- By Technology

- Electronic CD (ECD)

- Vibrational CD (VCD)

- Synchrotron Radiation CD (SRCD)

- By Application

- Protein Secondary-Structure Determination

- Vaccinology & Antigen Conformation Studies

- Biosimilar & Biologic Comparability Assessments

- Quality Control / Batch Release Testing

- Drug Discovery Screening & Hit Validation

- By End-User

- Pharmaceutical & Biotechnology Companies

- Contract Research / Manufacturing Organizations (CROs/CMOs)

- Academic & Government Research Institutes

- Hospital & Diagnostic Laboratories

- Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Detailed Research Methodology and Data Validation

Primary Research

Analysts interviewed instrument engineers, biopharma analytical-development managers across North America, Europe, and Asia-Pacific, and purchasing leads at contract research organizations. These discussions clarified typical price dispersion, replacement cycles, and emerging demand for low-volume vaccine characterization, enabling us to verify secondary findings and fine-tune model assumptions.

Desk Research

We collated foundational data from open sources such as the National Institutes of Health equipment grant logs, United States International Trade Commission import codes, Eurostat PRODCOM instrument shipments, and peer-reviewed spectroscopy journals, together with company 10-Ks and investor decks that disclose instrument backlogs. Paid databases like D&B Hoovers (company revenues) and Questel (patent velocity on SRCD optics) helped us map vendor activity trends. These materials supplied baseline unit shipments, average selling prices (ASP), and R&D spending cues that frame demand. The sources listed are illustrative; many additional public and proprietary references were reviewed for completeness.

Market-Sizing & Forecasting

We begin with a top-down reconstruction of global demand using production and trade data, which is then cross-checked with bottom-up samples of vendor shipments and ASPs gathered through channel checks. Key variables in our model include installed biopharma clean-room capacity, NIH and Horizon Europe life-science grant totals, average batch-release testing runs per biologic, and ASP compression tied to benchtop automation. Forecasts leverage multivariate regression blended with scenario analysis to capture sensitivity to R&D funding cycles and biosimilar pipeline volumes. Where bottom-up samples are thin, gap-filling relies on normalized replacement-rate curves drawn from expert interviews.

Data Validation & Update Cycle

Outputs pass variance checks against historical import data and published corporate revenues before a two-stage analyst review. Models refresh annually; interim updates trigger when material events, such as a major technology launch or regulatory shift, alter demand signals. A final pre-publication sweep ensures clients receive the latest calibrated view.

Why Mordor's Circular Dichroism Spectrometers Baseline Commands Reliability

Published market values often diverge because publishers apply different scopes, pricing baskets, and refresh cadences.

Other sources place the 2024 global value between USD 40.9 million and USD 790 million.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 36.62 Mn (2025) | Mordor Intelligence | - |

| USD 40.9 Mn (2024) | Global Consultancy A | Includes refurbished systems and bundle discounts not modeled by Mordor |

| USD 39.9 Mn (2023) | Industry Journal B | Uses averaged historical ASPs, overlooking recent price erosion |

| USD 790 Mn (2024) | Research Firm C | Broad scope folds in spectroscopy services and consumables |

The comparison shows that when scope is tightly defined, variables are transparent, and annual refreshes are honored, Mordor Intelligence delivers a balanced, reproducible baseline that decision-makers can trust.

Key Questions Answered in the Report

What is the current size of the Circular Dichroism Spectrometers market?

The market is valued at USD 39.35 million in 2026 and is set to reach USD 56.3 million by 2031, registering a 7.44% CAGR.

Which product category leads the Circular Dichroism Spectrometers market?

Benchtop instruments held 44.78% share in 2025 due to their balance of performance and affordability for routine protein characterization.

Why is Asia-Pacific the fastest-growing region for Circular Dichroism Spectrometers?

Rapid biopharmaceutical expansion in China, India, and Japan, coupled with tightening regulatory standards, drives an 8.41% regional CAGR through 2031.

How do biosimilar programs influence demand for CD spectrometers?

Regulatory guidance requires higher-order structural comparability, making CD an essential assay and accelerating instrument purchases among biosimilar developers.

What technological trend most impacts future instrument design?

Integration of quantum-cascade-laser vibrational CD and microspectroscopy promises faster scans and sub-cellular resolution, opening new application domains.

Are high capital costs a barrier to adoption?

Yes. Upfront prices exceeding USD 250,000 and ongoing operational expenses can delay procurement, especially in emerging markets, although shared facilities and leasing soften the impact.

Page last updated on: