Contract Management Software Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

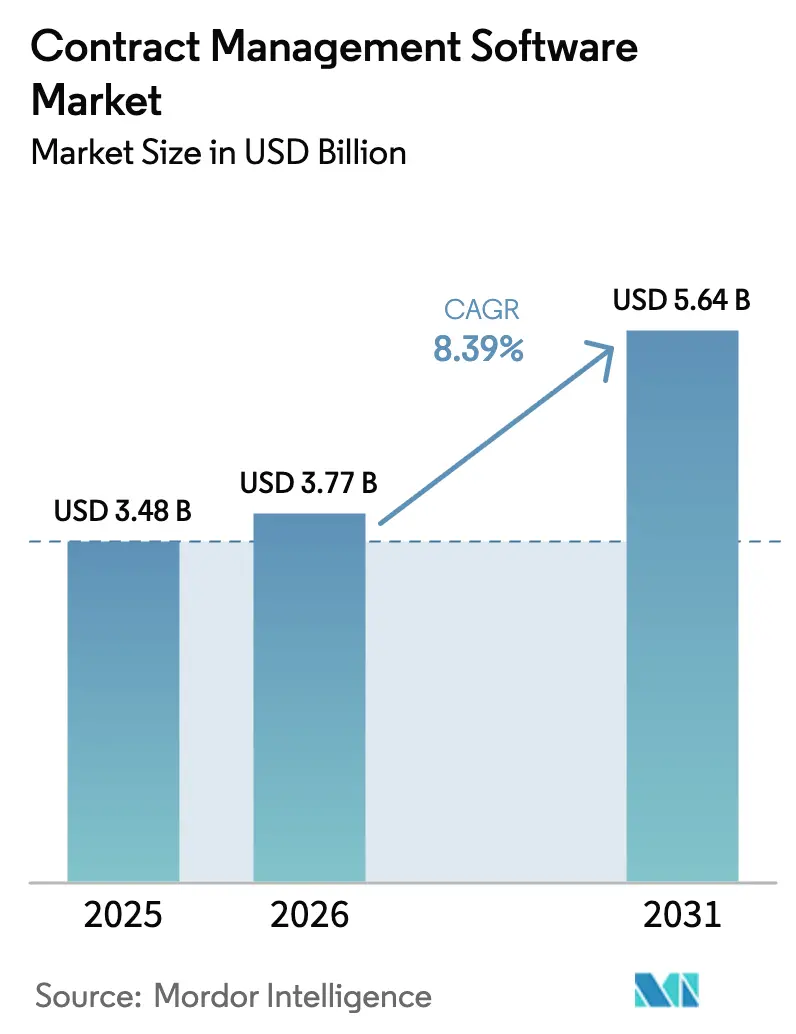

| Market Size (2026) | USD 3.77 Billion |

| Market Size (2031) | USD 5.64 Billion |

| Growth Rate (2026 - 2031) | 8.39% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Contract Management Software Market Analysis by Mordor Intelligence

Contract management software market size in 2026 is estimated at USD 3.77 billion, growing from 2025 value of USD 3.48 billion with 2031 projections showing USD 5.64 billion, growing at 8.39% CAGR over 2026-2031. The upward trajectory stems from enterprises digitizing the entire contract lifecycle to meet tightening regulatory demands, integrate AI analytics, and support remote-first workforces that expect e-signature-native workflows. Growth is further propelled by ESG-linked supplier mandates, the mainstreaming of generative AI for risk scoring, and regulatory measures such as the EU Data Act that lower switching barriers for cloud adoption. Competitive dynamics favor vendors able to embed contract data inside wider ERP, CRM, and SCM ecosystems, as firms race to eliminate silos and surface actionable insights in real time.

Key Report Takeaways

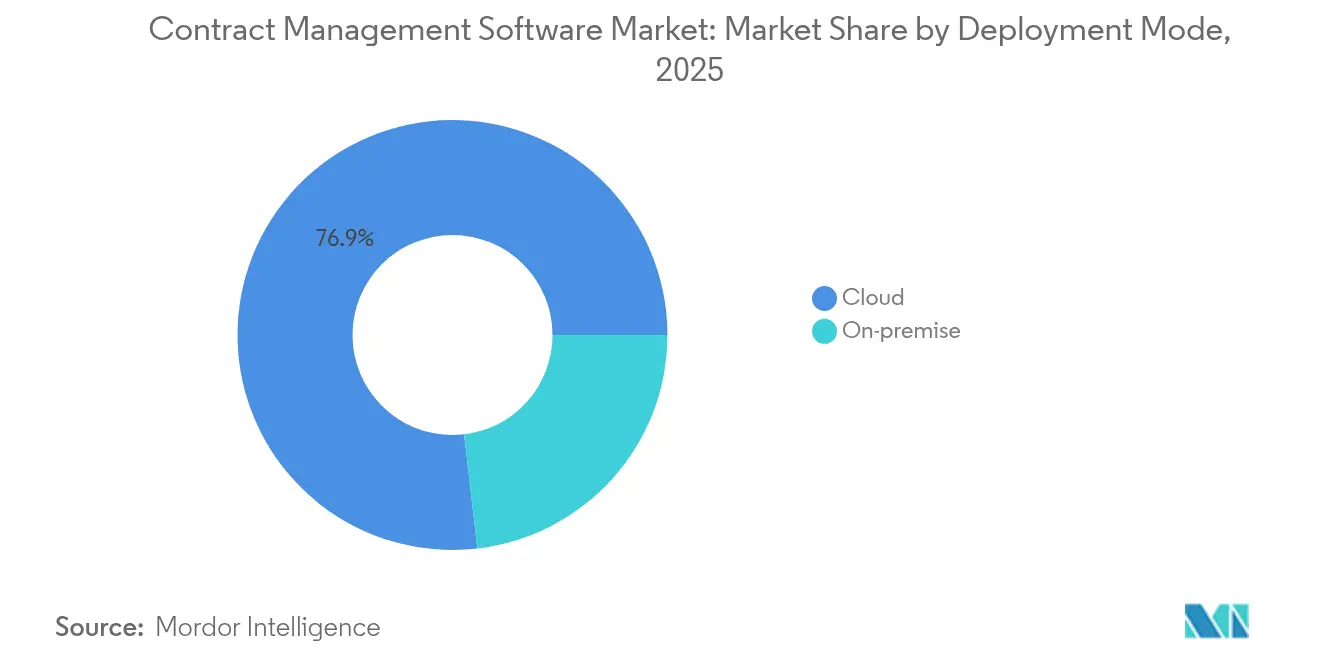

- By deployment mode, cloud solutions held 76.85% of contract management software market share in 2025, while on-premise platforms are forecast to expand at a slower 4.05% CAGR to 2031.

- By component, software accounted for 62.75% revenue in 2025; services are advancing at a 12.02% CAGR through 2031.

- By contract type, buy-side agreements commanded 55.12% share of the contract management software market size in 2025, whereas non-commercial contracts are rising at a 9.12% CAGR.

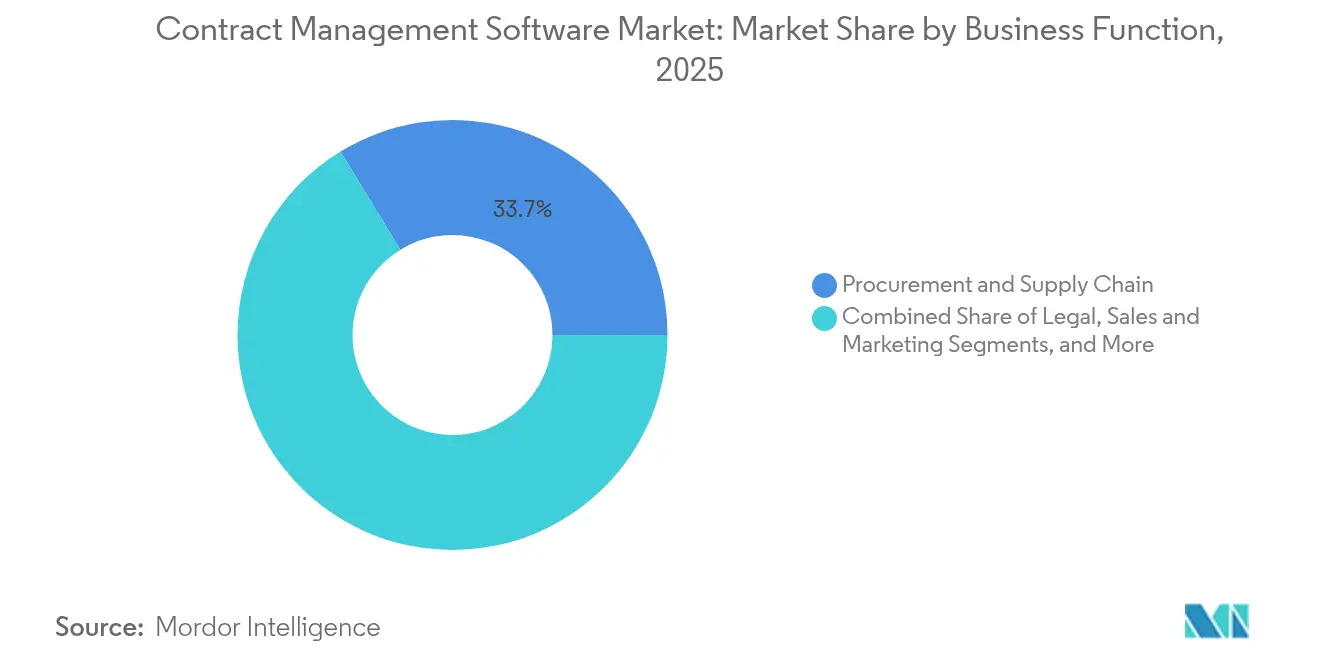

- By business function, procurement and supply chain led with 33.72% share in 2025; legal departments record the fastest 9.48% CAGR to 2031.

- By pricing model, subscription plans captured 92.08% of contract management software market size in 2025 and continue at a 9.05% CAGR.

- By integration level, standalone systems retained 66.05% share in 2025, yet integrated suites are growing at a 13.78% CAGR.

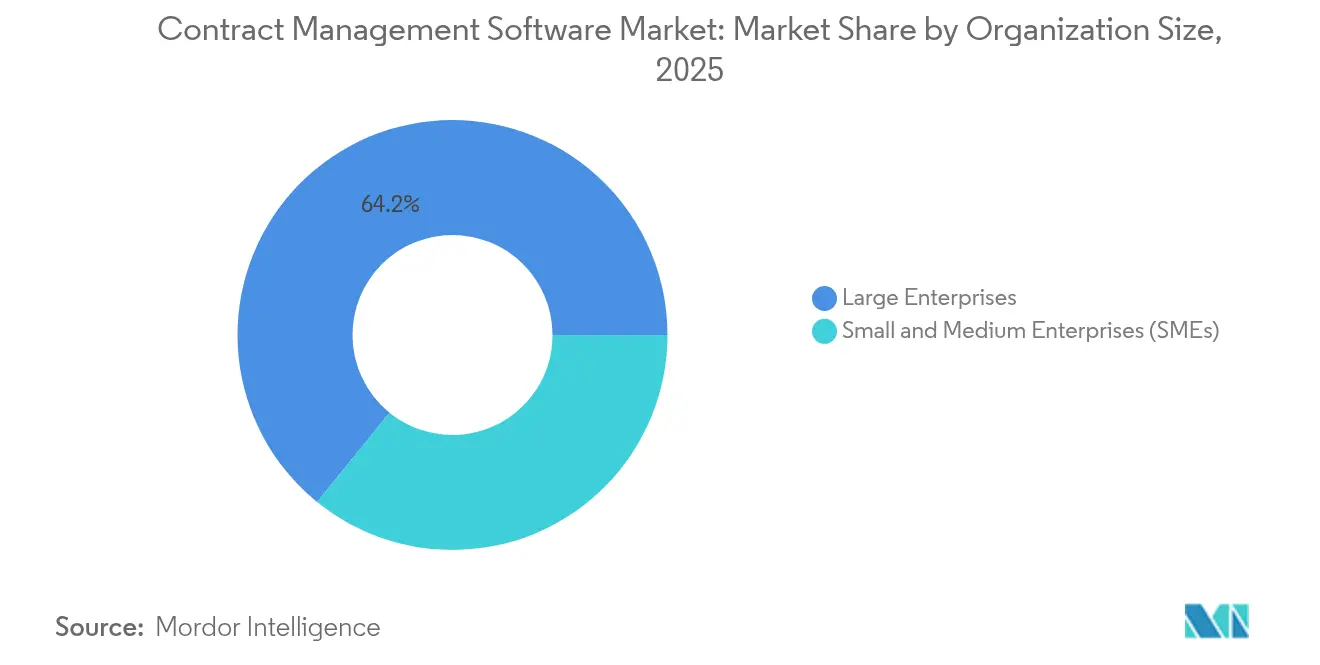

- By organization size, large enterprises represented 64.15% share in 2025, but SMEs are expanding at a 13.02% CAGR.

- By end-user industry, IT & telecom generated 18.22% revenue in 2025; healthcare and life sciences show the highest 10.76% CAGR.

- By geography, North America contributed 41.05% of contract management software market share in 2025, while Asia-Pacific posts a 9.18% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Contract Management Software Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging enterprise demand for unified buy-side and sell-side CLM across regulated industries | +1.8% | Global, with concentration in North America & EU | Medium term (2-4 years) |

| Rapid shift to AI-enabled contract analytics for risk and obligation management in North America | +1.5% | North America core, spill-over to APAC | Short term (≤ 2 years) |

| Acceleration of remote and hybrid work models driving e-signature-native CLM adoption | +1.2% | Global | Short term (≤ 2 years) |

| Vendor push toward verticalised CLM templates boosting uptake in Europe | +0.9% | Europe core, expanding to other regions | Medium term (2-4 years) |

| Rising pressure from ESG-linked supplier compliance mandates in global procurement | +0.8% | Global, with early adoption in EU & North America | Long term (≥ 4 years) |

| Integration of CLM with enterprise SaaS suites lowering switching costs in Asia-Pacific | +0.7% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surging Enterprise Demand for Unified Buy-Side and Sell-Side CLM Across Regulated Industries

Unified platforms let organizations monitor obligations and revenue leakages end-to-end, closing the 8.6% average value erosion gap highlighted in Deloitte’s contract excellence survey.[1]Deloitte, “Upping Contract Management Lifecycle ROI,” Deloitte.com Industries with stringent oversight, such as healthcare under the Physician Payments Sunshine Act, prioritize integrated visibility so that procurement, legal, and finance teams detect overlapping clauses before penalties accrue. Financial institutions adopt the same logic to cross-reference trading agreements with onboarding documentation. The trend also shortens audit cycles, as auditors access a single source of truth rather than patchwork repositories

Rapid Shift to AI-Enabled Contract Analytics for Risk and Obligation Management in North America

Generative AI shifts contract repositories from passive storage to decision engines that highlight indemnity gaps, renewal triggers, and force-majeure clauses within seconds. DocuSign’s Intelligent Agreement Management platform illustrates the new baseline; its AI review features contributed to USD 776 million Q4 2025 revenue, beating analyst expectations.[2]CNBC, “Shares of DocuSign Surge 14% on Strong Earnings, AI Boost,” cnbc.com Japanese conglomerates echo this value, with Sojitz Tech Innovation reclaiming 7,000 analyst hours annually via Contract One.[3]PR Times, “Sojitz Tech Innovation Uses Contract One to Cut 7,000 Hours,” prtimes.jp As only 55% of legal departments formally employ CLM today, untapped upside remains substantial.[4]Financial Times, “Generative AI Turns Spotlight on Contract Management,” ft.com

Acceleration of Remote and Hybrid Work Models Driving E-Signature-Native CLM Adoption

Work-from-anywhere policies turned e-signature from convenience into prerequisite. Platforms that embed signing directly into negotiation flows avoid security gaps that arise when legal teams juggle separate best-of-breed tools. DocuSign’s 1.6 million-customer base underscores the secular demand, and SMEs now access comparable rigor without on-premise servers, helping to explain the 13.5% CAGR in smaller-firm uptake.

Vendor Push Toward Verticalised CLM Templates Boosting Uptake in Europe

European providers differentiate by embedding sector-specific clauses for life sciences trials, utility supply contracts, and multilingual GDPR provisions. Conga’s June 2024 launch delivered out-of-the-box templates tied to leading CRM and ERP stacks, accelerating user adoption and creating higher switching costs.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented legacy contract data silos hindering AI model accuracy | -1.4% | Global, particularly affecting large enterprises | Medium term (2-4 years) |

| Low digital maturity of Tier-2 suppliers in South America and Africa limiting addressable market | -0.8% | South America & Africa core, with spillover effects globally | Long term (≥ 4 years) |

| Complex change-management costs within highly regulated government agencies | -0.6% | Global, with concentration in North America & EU | Long term (≥ 4 years) |

| Data-residency restrictions delaying cross-border cloud CLM roll-outs in MEA | -0.4% | Middle East & Africa core, regulatory spillover to APAC | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Fragmented Legacy Contract Data Silos Hindering AI Model Accuracy

Decades of unstructured PDFs and scanned images impede machine learning, forcing costly preprocessing. Conga’s CEO notes that post-merger enterprises often cannot locate evergreen clauses across subsidiaries, risking missed revenue. Japanese firms solve the problem by bulk digitizing archives; Japan Oil Transportation cut 1,000 digitization hours with TOKIUM PR Times. Yet many global companies still face multi-year cleanup projects before AI delivers promised value

Low Digital Maturity of Tier-2 Suppliers in South America and Africa Limiting Addressable Market

Multinationals rolling out advanced CLM platforms cannot reap network effects when subcontractors rely on paper forms. The Asian Development Bank observed that MSME lending averages only 9% of GDP in Central and West Asia, mirroring low tech adoption. Similar pockets in Africa stall e-signature penetration, forcing enterprises to maintain parallel manual workflows and slowing overall platform ROI.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Deployment Mode: Cloud Dominance Accelerates Digital Transformation

Cloud deployments accounted for 76.85% revenue in 2025 as regulators removed lock-in fears through the Data Act, which obliges providers to enable switching within 30 days. The contract management software market size for cloud solutions is projected to reach USD 4.32 billion by 2031 at an 8.32% CAGR. Enterprises prefer elastic capacity to ingest surges of contracts during mergers, while seamless API connectivity accelerates integrated workflows.

On-premise and hybrid models persist in defense and government, where sovereignty and air-gapped infrastructure are mandated. Specialized vendors such as Unison tailor secure enclaves that align with FedRAMP and ITAR directives.

By Component: Services Drive Implementation Success

Software retained 62.75% share in 2025, yet services outpace at 12.02% CAGR because organizations need consulting to harmonize processes, migrate data, and train users. Implementations covering people, process, and technology contain value erosion to near 3%, versus above 8% for tool-only rollouts.

Managed services also include AI model tuning, clause library curation, and ongoing compliance updates. Vendors bundle outcome-based engagements, assuring measurable risk-mitigation metrics that resonate with CFOs seeking post-implementation clarity.

By Contract Type: Non-Commercial Contracts Gain Strategic Importance

Buy-side documents represented 55.12% revenue in 2025 because procurement teams rely on pricing, delivery, and quality clauses to control spend. Internal and policy-driven contracts grow faster at 9.12% as ESG and climate-disclosure rules escalate documentation needs. For example, SEC climate rules from May 2024 require granular reporting on supply chain impact, expanding internal audit workloads.

Sell-side contracts remain critical to recurring revenue, yet firms increasingly feed both commercial and internal documents into unified search so that cross-dependencies surface during renegotiations.

By Business Function: Legal Teams Drive Digital Transformation

Procurement held 33.72% share in 2025, as bulk vendor agreements reside there. Legal teams, however, lead adoption velocity at 9.48% CAGR because AI review tools free attorneys from manual clause redlining. This trend elevates lawyers into strategic advisors who interpret analytics rather than chase signatures.

Sales departments integrate CLM with CPQ to shave weeks off quote-to-cash cycles, while finance plugs in to automate revenue recognition. HR leverages the same engine for employment and confidentiality agreements, bringing every stakeholder onto a single digital track

By Pricing Model: Subscription Model Reinforces SaaS Dominance

Subscription contracts dominated at 92.08% and climb further due to continuous updates and predictable opex budgeting. The contract management software market size under subscription terms is anticipated to capture USD 5.18 billion by 2031, echoing how clients prefer incremental seats over capital budgets.

Per-petual licenses survive in agencies that must freeze features for certification audits but represent a shrinking niche.

By Integration Level: Integrated Solutions Transform Enterprise Workflows

Although standalone tools still command 66.05% revenue in 2025, integrated suites surge at 13.78% CAGR because firms demand data to flow across sourcing, planning, and cash systems. SAP’s Business Network, which processed USD 6.2 trillion in commerce, shows how spend visibility telescopes when contracts feed into procurement analytics.

Integrated offerings reduce swivel-chair work, enforce policy at the point of action, and provide CFOs a consolidated risk dashboard, yielding measurable cycle-time compression and audit readines

By Organization Size: SMEs Embrace Cloud-Native Solutions

Large enterprises owned 64.15% share in 2025, but SMEs grow faster at 13.02% as cloud freemium tiers remove infrastructure hurdles. Japan’s record number of start-ups witnessed a 157% spike in electronic contract inquiries in Q4 FY2025, signaling mainstream penetration.

SMEs appreciate AI features that auto-classify clauses and push renewal alerts without dedicated legal staff. Tiered pricing also aligns spend with contract volume, turning CLM into a variable cost rather than fixed overhead.

By End-User Industry: Healthcare Leads Vertical Specialization

IT and Telecom contributed 18.22% revenue in 2025 because multi-vendor ecosystems need strong governance. Healthcare and life sciences now expand at 10.76% CAGR; templates for clinical-trial agreements and Sunshine Act reporting lower time-to-value.

Utilities, BFSI, and government each demand bespoke compliance matrices, encouraging vendors to build vertical accelerators. Such specialization reinforces stickiness, as migrating to generic tools would require costly re-engineering.

Geography Analysis

North America accounted for 41.05% revenue in 2025 owing to complex litigation exposure, SEC climate-risk filings, and federal acquisition updates that add contract tracking layers. Cloud maturity and procurement digitalization keep the region ahead, while the GSA’s AI Center of Excellence encourages agencies to modernize agreement workflows. Public-sector momentum spills into private verticals, reinforcing a self-sustaining adoption loop.

Asia-Pacific is the fastest climber at 9.18% CAGR through 2031. Japanese conglomerates report AI extraction accuracy hitting 98%, proving local language and format challenges can be solved at scale. South-East Asian SMEs, which represent 97% of enterprises, now gain affordable SaaS access as broadband and e-payment rails mature. China’s manufacturing base and India’s SaaS start-ups inject further velocity, aided by governments prioritizing cross-border trade digitalization.

Europe enjoys steady demand as the Data Act, effective September 2025, enforces portability, boosting confidence in cloud CLM. GDPR continues to drive specialized clauses for personal-data processing, while multilingual contract templates gain traction among pan-EU supply chains. Sub-regions like DACH and Nordics show above-average adoption because of advanced manufacturing and green-transition programs that rely on ESG-ready documentation.

South America and Middle East & Africa remain nascent, hampered by supplier digital gaps and data-residency concerns. Yet signs of momentum emerge as cloud data centers proliferate and governments publish electronic signature statutes. Vendors that offer offline-capable mobile apps position well for these frontier opportunities.

Competitive Landscape

Roughly 150-200 vendors compete, but consolidation is accelerating. DocuSign acquired Lexion for USD 165 million in May 2024 to deepen AI clause-classification competence. Icertis surpassed USD 250 million in annual recurring revenue after launching generative AI copilots that draft contract summaries in seconds. SAP leverages its global ERP footprint to embed CLM inside its Business Network, ensuring direct data flow from sourcing to payment.

Strategic focus centers on:

- AI accuracy: Vendors benchmark clause extraction F-scores and propagate domain-specific LLMs to outperform generic models.

- Vertical depth: Platforms release life-sciences, utilities, and public-sector accelerators to capture niche compliance workflows.

- Ecosystem integration: Open APIs and certified connectors to Salesforce, SAP, and Microsoft Dynamics become table stakes.

Fragmentation persists in local markets where language, compliance, or pricing nuances favor domestic champions. Yet private-equity interest signals a thinning field, evidenced by recurrent rumors of buyouts targeting CLM pure-plays valued between USD 500 million and USD 2 billion. Vendors unable to fund AI roadmaps or vertical modules may become acquisition targets, accelerating market rationalization.

Contract Management Software Industry Leaders

Zycus Inc.

ContractWorks, Inc.

Complinity Technologies Private Limited

Contract Logix, LLC

Concord, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Sansan’s Contract One enabled SmartHR to cut monthly contract tasks by over 100 hours and helped Toho centralize 19,000 media contracts .

- May 2025: Japan Oil Transportation deployed TOKIUM, reducing contract digitization by 1,000 hours and annual management by 100 hours

- April 2025: ConPass achieved 98% AI extraction accuracy, expanding field coverage and security hardening with multiple LLMs

- March 2025: DocuSign posted USD 776 million Q4 FY2025 revenue, guiding full-year revenue to USD 3.13-3.14 billion on AI momentum

- February 2024: Icertis exceeded USD 250 million ARR, crediting generative AI contracting copilots.

Global Contract Management Software Market Report Scope

Contract management software (CMS) streamlines the entire contract lifecycle, automating tasks from creation to renewal. By centralizing and digitizing contract data, it ensures information is both accessible and searchable. This software enhances business collaboration, leading to more efficient contract creation and approval. Beyond just managing contracts, it offers compliance features, aiding businesses in meeting their contractual and regulatory obligations. Automating workflows and minimizing manual errors seamlessly integrates with other systems, enhancing efficiency and data accuracy.

The study tracks the revenue accrued through the sale of contract management software types by various players globally. The study also tracks the key market parameters, underlying growth influencers, and major vendors operating in the industry, which supports the market estimations and growth rates over the forecast period. The study further analyses the overall impact of COVID-19 aftereffects and other macroeconomic factors on the market. The report's scope encompasses market sizing and forecasts for the various market segments.

The contract management software market is segmented by type of deployment (on-premise and cloud), component (software and services), organization size (large enterprises and small and medium enterprises (SMEs)), end-user industry (BFSI, government, healthcare, retail, manufacturing, IT and Telecom, and others), and geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Cloud |

| On-premise |

| Software |

| Services |

| Buy-side |

| Sell-side |

| Non-commercial/Internal |

| Legal |

| Sales and Marketing |

| Procurement and Supply Chain |

| Finance and Accounting |

| HR and Administration |

| Subscription (SaaS) |

| One-time License |

| Standalone CLM |

| Integrated with ERP/CRM/SCM suites |

| Large Enterprises |

| Small and Medium Enterprises (SMEs) |

| BFSI |

| Government and Public Sector |

| Healthcare and Life Sciences |

| Retail and E-commerce |

| Manufacturing and Automotive |

| IT and Telecom |

| Energy and Utilities |

| Others (Media, Education, etc.) |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Nordics | ||

| Rest of Europe | ||

| South America | Brazil | |

| Rest of South America | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South-East Asia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Rest of Africa | ||

| By Deployment Mode | Cloud | ||

| On-premise | |||

| By Component | Software | ||

| Services | |||

| By Contract Type | Buy-side | ||

| Sell-side | |||

| Non-commercial/Internal | |||

| By Business Function | Legal | ||

| Sales and Marketing | |||

| Procurement and Supply Chain | |||

| Finance and Accounting | |||

| HR and Administration | |||

| By Pricing Model | Subscription (SaaS) | ||

| One-time License | |||

| By Integration Level | Standalone CLM | ||

| Integrated with ERP/CRM/SCM suites | |||

| By Organization Size | Large Enterprises | ||

| Small and Medium Enterprises (SMEs) | |||

| By End-user Industry | BFSI | ||

| Government and Public Sector | |||

| Healthcare and Life Sciences | |||

| Retail and E-commerce | |||

| Manufacturing and Automotive | |||

| IT and Telecom | |||

| Energy and Utilities | |||

| Others (Media, Education, etc.) | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Nordics | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Rest of South America | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South-East Asia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Gulf Cooperation Council Countries | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the contract management software market?

The market stands at USD 3.77 billion in 2026 and is projected to reach USD 5.64 billion by 2031 at an 8.39% CAGR

Which deployment model leads the market

Cloud deployment dominates with 76.85% market share in 2025, supported by regulations that simplify provider switching.

Why are services growing faster than software in this space?

Services post a 12.02% CAGR because organizations need consulting, data migration, and training to unlock full platform value.

Which region is growing the fastest?

Asia-Pacific is advancing at a 9.18% CAGR through 2031, driven by digital transformation programs and SME adoption.

How are AI capabilities changing contract management?

Generative AI now extracts clauses, flags risks, and predicts renewals, allowing legal teams to shift from manual review to strategic oversight.

What is driving demand for verticalised CLM solutions?

Industries like healthcare and utilities need sector-specific clauses and workflows to comply with regulations, leading vendors to offer tailored templates

Page last updated on: