Electric Vehicle High-Voltage DC-DC Converter Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Market Size (2025) | USD 1.67 Billion |

| Market Size (2030) | USD 3.21 Billion |

| Growth Rate (2025 - 2030) | 14.05% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Electric Vehicle High-Voltage DC-DC Converter Market Analysis by Mordor Intelligence

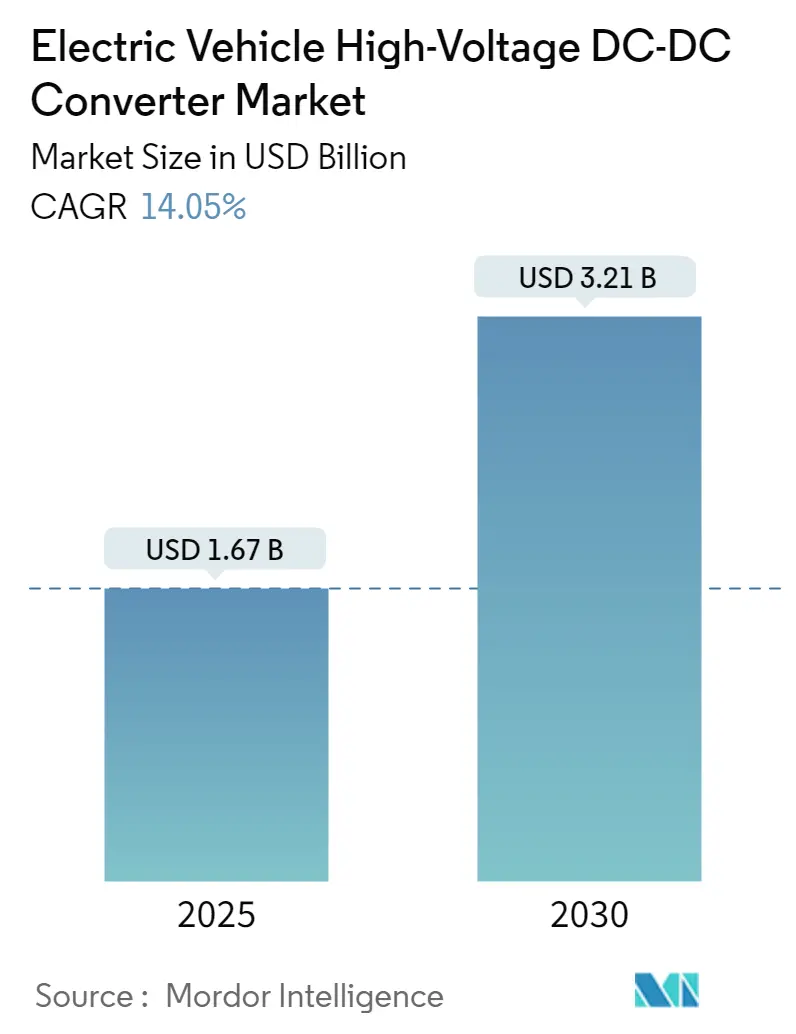

The Electric Vehicle High-Voltage DC-DC Converter Market size is estimated at USD 1.67 billion in 2025, and is expected to reach USD 3.21 billion by 2030, at a CAGR of 14.05% during the forecast period (2025-2030).

The electric vehicle high-voltage DC-DC converter industry is experiencing transformative growth driven by rapid technological advancements and shifting consumer preferences. Recent innovations in semiconductor technology, particularly the development of silicon carbide (SiC) and gallium nitride (GaN) materials, are revolutionizing automotive power converter efficiency and performance capabilities. These advanced materials enable operation at higher frequencies, resulting in significant size reductions of passive components and improved overall system efficiency. The integration of smart technologies, including cloud computing and the Internet of Things (IoT) in battery management systems, has further enhanced the sophistication of DC-DC converter applications in electric vehicles.

The market is witnessing substantial momentum in technological innovation and product development from major industry players. In June 2024, Samsung Electro-Mechanics introduced a groundbreaking high-voltage multi-layer ceramic capacitor specifically designed for EV applications, including high-voltage converters. This development showcases the industry's focus on miniaturization, enhanced stability, and improved capacitance in converter components. The continuous evolution of converter technology is enabling manufacturers to meet the increasing demands for more efficient and compact power management solutions in electric vehicles.

Global electric vehicle adoption continues to show remarkable growth, as evidenced by the International Energy Agency's report showing a 25% increase in electric car sales in Q1 2024 compared to Q1 2023. This surge in EV adoption is driving the demand for more sophisticated power conversion solutions, with manufacturers focusing on developing high-efficiency converters capable of managing the complex power requirements of modern electric vehicles. The industry is seeing increased emphasis on developing converters that can handle higher power densities while maintaining optimal thermal management and reliability. This trend underscores the critical role of EV power electronics in advancing electric vehicle technology.

The market is characterized by a growing emphasis on charging infrastructure development and power management optimization. Industry stakeholders are increasingly focusing on developing converters that can support various charging standards and power levels, ensuring compatibility across different EV platforms. By 2040, industry projections indicate that electric vehicles will represent 54% of new car sales and 33% of global car fleets, highlighting the long-term growth potential for high-voltage DC-DC converter technologies. This transition is spurring investments in research and development of more advanced converter solutions that can meet the evolving requirements of next-generation electric vehicles, emphasizing the importance of automotive power electronics in this evolution.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Electric Vehicle High-Voltage DC-DC Converter Market Trends and Insights

Increased Electric Vehicle Adoption Globally

The automotive industry is witnessing a significant transformation with the rapid adoption of electric vehicles globally, driven by increasing environmental consciousness and supportive government policies. According to the International Energy Agency, new electric car registrations in Europe reached nearly 3.2 million in 2023, marking a substantial 20% increase compared to 2022, with battery electric vehicles accounting for 70% of the electric car stock. This surge in adoption is further supported by various government initiatives worldwide, such as the California Zero Emission Vehicle (ZEV) program, which aims to have 1.5 million electric vehicles on the road by 2025. Countries including India, China, the United Kingdom, South Korea, France, Germany, Norway, and the Netherlands have implemented various incentives to encourage EV adoption, ranging from tax credits to purchase subsidies.

The growing adoption of electric vehicles has catalyzed innovations in power electronics components, particularly automotive DC-DC converters, which are essential for efficient power management in EVs. This trend is evidenced by recent technological developments, such as Eaton's launch of a higher-power version of its low-voltage 48-volt DC-DC converter in May 2024, designed specifically to enhance power conversion efficiency in electric vehicles. The converter's ability to step down power from 48-volt systems to 12 volts for running accessories and other low-power systems demonstrates the industry's response to the increasing sophistication of EV power management systems. Additionally, vehicles registered in Europe until December 31, 2025, are being exempted from ownership tax for 10 years, with this exemption extending until December 31, 2030, further accelerating the transition to electric mobility.

Increasing Investments in Electric Vehicles

The electric vehicle industry is experiencing unprecedented levels of investment from both automotive manufacturers and governments worldwide, creating substantial opportunities for the electric vehicle power converter market. A notable example is India's recent approval of an EV policy in March 2024, which offers import duty concessions to companies establishing manufacturing units with a minimum investment of USD 500 million, attracting major global players like Tesla. This strategic move demonstrates the growing commitment of governments to foster domestic EV manufacturing capabilities and create robust supply chains for critical components, including power electronics.

The investment landscape is further enriched by automotive manufacturers' substantial commitments to research and development in electric vehicle technologies. For instance, major manufacturers are focusing on upgrading their manufacturing sites and investing in new technologies to meet electrification targets. This is exemplified by Hyundai's announcement of a USD 0.12 billion investment in developing new affordable EVs, with plans to manufacture locally and establish strategic partnerships with local vendors for component sourcing. These investments are particularly significant for the high-voltage DC power supply market as manufacturers seek to develop more efficient and cost-effective power management solutions. The trend towards local manufacturing and component sourcing is creating new opportunities for power electronics suppliers and fostering technological innovations in high-voltage DC-DC converters.

Segment Analysis: Vehicle Type

SUV Segment in Electric Vehicle High-Voltage DC-DC Converter Market

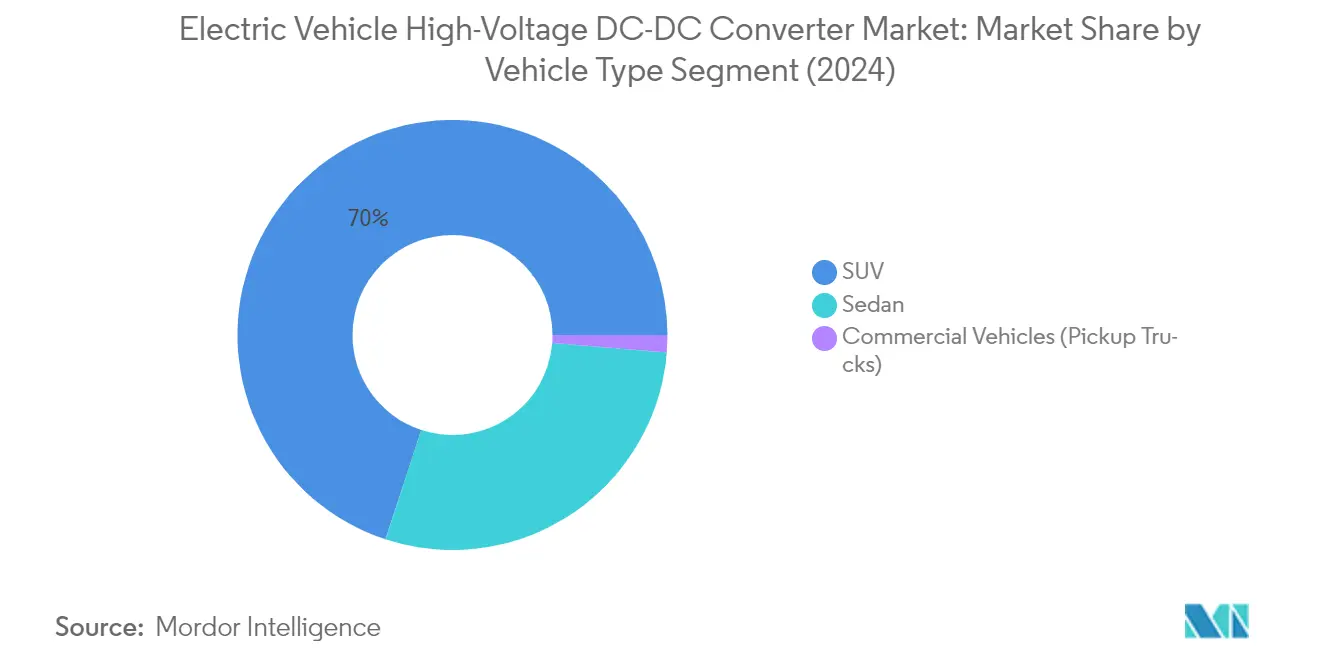

Sport Utility Vehicles (SUVs) continue to dominate the electric vehicle high-voltage DC-DC converter market, commanding approximately 70% of the total market share in 2024. This substantial market leadership is primarily driven by the increasing consumer preference for SUVs in major automotive markets worldwide. The segment's dominance is further strengthened by the extensive lineup of electric SUV models from leading manufacturers and the higher power requirements of these vehicles, necessitating more sophisticated high-voltage converter solutions. Major automotive manufacturers are increasingly focusing on expanding their electric SUV portfolios, with many introducing new models featuring advanced power management systems and high-voltage architecture.

Commercial Vehicle (Pickup Trucks) Segment in Electric Vehicle High-Voltage DC-DC Converter Market

The commercial vehicle segment, particularly pickup trucks, is emerging as the fastest-growing segment in the electric vehicle high-voltage DC-DC converter market, projected to grow at approximately 15% during 2024-2029. This accelerated growth is driven by increasing demand for electric pickup trucks in logistics and municipal sectors, coupled with the entry of several new manufacturers into the electric pickup truck market. The segment's growth is further supported by government initiatives promoting commercial electric vehicle adoption and the increasing focus on reducing emissions in the commercial transportation sector. Major automotive manufacturers are investing heavily in electric pickup truck development, with many introducing new models featuring advanced EV power converter technologies.

Remaining Segments in Vehicle Type

The sedan segment represents a significant portion of the electric vehicle high-voltage DC-DC converter market, offering a balanced combination of performance and efficiency. This segment continues to be an important market driver, particularly in regions with established electric vehicle markets and urban areas where sedans are preferred for their practicality and efficiency. The segment benefits from continuous technological advancements in DC-DC converter designs, focusing on compact solutions that maintain high efficiency while meeting the specific power requirements of electric sedans. Manufacturers are developing specialized converter solutions tailored to sedan platforms, considering their unique power distribution needs and space constraints.

Segment Analysis: Propulsion Type

Battery Electric Vehicle Segment in Electric Vehicle High-Voltage DC-DC Converter Market

The Battery Electric Vehicle (BEV) segment has established itself as both the largest and fastest-growing segment in the electric vehicle high-voltage DC-DC converter market. In 2024, BEVs account for approximately 64% of the total market share, driven by increasing consumer preference for zero-emission vehicles and supportive government policies worldwide. The segment's dominance is further reinforced by major automotive manufacturers expanding their BEV product portfolios and making significant investments in battery technology and charging infrastructure. The growth is particularly notable in key markets like China, Europe, and North America, where consumer adoption of BEVs continues to accelerate. Additionally, technological advancements in DC-DC converter efficiency and power density have made BEVs more attractive to consumers, while decreasing battery costs have improved overall vehicle affordability.

Plug-in Hybrid Vehicle Segment in Electric Vehicle High-Voltage DC-DC Converter Market

The Plug-in Hybrid Vehicle (PHEV) segment represents a significant portion of the electric vehicle high-voltage DC-DC converter market, serving as a bridge between conventional and fully electric vehicles. This segment continues to attract consumers who desire the flexibility of both electric and gasoline powertrains while maintaining concerns about charging infrastructure and range anxiety. Automotive manufacturers are investing in advanced PHEV technologies, focusing on improving electric-only range and overall system efficiency. The segment benefits from ongoing developments in DC-DC converter technology, which enables better integration between the electric and conventional powertrains. Additionally, PHEVs are particularly popular in regions where charging infrastructure is still developing, as they offer a practical transition solution for consumers moving towards electrification.

Remaining Segments in Propulsion Type

The Fuel Cell Electric Vehicle (FCEV) segment, while currently smaller in market share, represents an important emerging technology in the electric vehicle high-voltage DC-DC converter market. FCEVs offer unique advantages such as rapid refueling capabilities and longer range compared to battery-only vehicles, making them particularly attractive for commercial and heavy-duty applications. The segment is seeing increased interest from both automotive manufacturers and government bodies, particularly in regions with established hydrogen infrastructure plans. The development of specialized high-voltage DC-DC converters for fuel cell applications continues to advance, with manufacturers focusing on improving efficiency and power density while reducing costs. This segment's growth is supported by ongoing investments in hydrogen infrastructure and increasing recognition of hydrogen's role in the future of sustainable transportation.

Segment Analysis: Cooling Method

Liquid Cooled Segment in Electric Vehicle High-Voltage DC-DC Converter Market

The liquid-cooled segment continues to dominate the electric vehicle high-voltage DC-DC converter market, commanding approximately 65% of the total market share in 2024. This significant market position is attributed to the superior thermal performance and efficiency advantages offered by liquid cooling systems in electric vehicle applications. The liquid cooling method has become particularly prevalent as it allows DC-DC converters to be easily integrated into existing vehicle cooling loops alongside other critical components like high-voltage batteries and inverters. The direct connection to the vehicle's liquid cooling system enables the generation of very high power density and optimizes thermal management of the modules, which ultimately improves overall EV efficiency. Additionally, manufacturers are increasingly preferring liquid-cooled converters for high-performance electric vehicles due to their ability to maintain consistent performance under varying load conditions and their superior heat dissipation capabilities compared to other cooling methods.

Air Cooled Segment in Electric Vehicle High-Voltage DC-DC Converter Market

The air-cooled segment is emerging as the fastest-growing segment in the market, projected to grow at approximately 14% during the forecast period 2024-2029. This growth is primarily driven by the segment's inherent advantages of simplicity, cost-effectiveness, and easier maintenance requirements. Air cooling systems are particularly gaining traction in applications where power requirements are moderate and where minimizing system complexity is a priority. The segment's growth is further supported by technological advancements in air cooling designs that have improved their efficiency and reliability. Manufacturers are developing innovative air-cooled solutions that offer competitive performance while maintaining lower implementation costs, making them an attractive option for certain electric vehicle applications, especially in regions where cost considerations play a crucial role in technology adoption.

Segment Analysis: Input Voltage

200V-450V Segment in Electric Vehicle High-Voltage DC-DC Converter Market

The 200V-450V segment continues to dominate the electric vehicle high-voltage DC-DC converter market, holding approximately 92% market share in 2024. This segment's prominence is driven by its widespread adoption across various electric vehicle platforms, particularly in mass-market electric vehicles and plug-in hybrids. The segment's dominance is reinforced by the extensive deployment of this voltage range in popular electric vehicle models from major manufacturers, offering an optimal balance between performance and cost-effectiveness. Major automotive manufacturers are actively developing and implementing DC-DC converter solutions within this voltage range, focusing on improving efficiency and reducing overall system complexity. The segment's strong position is further supported by the established infrastructure and standardization around this voltage range, making it a preferred choice for both vehicle manufacturers and component suppliers.

800V-1000V Segment in Electric Vehicle High-Voltage DC-DC Converter Market

The 800V-1000V segment is emerging as the fastest-growing segment in the market, with a projected growth rate of approximately 38% during 2024-2029. This remarkable growth is primarily driven by the increasing adoption of ultra-fast charging capabilities in premium and luxury electric vehicles. The segment is witnessing significant technological advancements, with manufacturers developing more efficient and compact converter solutions capable of handling higher voltage ranges. The transition towards 800V architecture is being spearheaded by luxury automotive brands who are incorporating this technology to achieve superior performance and faster charging capabilities. This voltage range offers significant advantages in terms of reduced charging times, improved power density, and enhanced overall system efficiency, making it increasingly attractive for next-generation electric vehicles.

Remaining Segments in Input Voltage

The 450V-800V segment serves as a crucial intermediate range in the electric vehicle high-voltage DC-DC converter market, bridging the gap between standard and ultra-high voltage systems. This segment caters to a diverse range of vehicle applications, particularly in mid-range electric vehicles and advanced hybrid systems. The segment benefits from its versatility in supporting both existing infrastructure and newer high-voltage architectures. Manufacturers in this segment focus on developing scalable solutions that can accommodate the evolving needs of the electric vehicle market, while maintaining compatibility with current charging infrastructure and power distribution systems. The segment continues to play a vital role in the market's evolution, offering a balanced approach between performance requirements and implementation complexity.

Segment Analysis: Output Voltage

12V-24V Segment in Electric Vehicle High-Voltage DC-DC Converter Market

The 12V-24V segment dominates the electric vehicle high-voltage DC-DC converter market, commanding approximately 93% of the total market share in 2024. This segment's prominence is driven by the increasing adoption of electric vehicles and the growing integration of various electronic components that require a stable low-voltage power supply. The segment's leadership position is further strengthened by the rising demand for safety and comfort features in electric vehicles, including entertainment systems, radio, music systems, and other accessories that typically operate on 12-24V DC power. The growing consumer preference for fuel-efficient electric vehicles, self-driving cars, and vehicle-to-vehicle communication technology has also contributed significantly to this segment's dominance. Additionally, the segment benefits from the increasing integration of electric windows, wipers, and other auxiliary systems in electric vehicles that require nominal output voltage in the 12-24V range. The segment is also experiencing the fastest growth rate in the market, projected to grow at approximately 14% from 2024 to 2029, driven by continuous technological advancements and the expanding electric vehicle market globally.

24V-48V Segment in Electric Vehicle High-Voltage DC-DC Converter Market

The 24V-48V segment represents a smaller but significant portion of the market, catering to specific high-power applications in electric vehicles. This segment serves applications requiring higher voltage outputs, particularly in commercial electric vehicles and advanced powertrain systems. The segment's growth is supported by the increasing adoption of 48V mild hybrid systems and the development of more sophisticated electric vehicle architectures. The demand for 24V-48V converters is particularly strong in premium electric vehicles and commercial vehicle segments where higher power requirements are common. The segment also benefits from ongoing technological advancements in power electronics and the industry's push toward more efficient power conversion solutions. Manufacturers are continuously developing new products in this voltage range to meet the evolving requirements of modern electric vehicles, particularly for applications requiring higher power density and improved efficiency.

Segment Analysis: Output Power

Less than 2kW Segment in Electric Vehicle High-Voltage DC-DC Converter Market

The less than 2kW segment has established itself as the dominant force in the electric vehicle high-voltage DC-DC converter market, commanding approximately 93% market share in 2024. This segment's prominence can be attributed to the increasing adoption of electric vehicles in the passenger car segment, particularly in urban environments where lower power requirements are sufficient for daily commuting needs. The growing integration of safety and comfort features in electric vehicles has further boosted the demand for low-power DC-DC converters, as these components are essential for powering various vehicle electronics and auxiliary systems. The segment is also witnessing strong growth momentum and is projected to grow at around 14% through 2024-2029, driven by the rising consumer preference for fuel-efficient electric vehicles, self-driving cars, and vehicle-to-vehicle communication technology. The increasing focus on developing more efficient and compact converter designs for applications requiring less than 2kW power output continues to strengthen this segment's market position.

2kW and Above Segment in Electric Vehicle High-Voltage DC-DC Converter Market

The 2kW and above segment serves the high-performance and commercial electric vehicle segments, where higher power requirements are essential for optimal vehicle operation. This segment caters to premium electric vehicles, heavy-duty commercial vehicles, and high-performance passenger cars that demand more powerful DC-DC converters to manage their sophisticated electrical systems. The segment has been gaining traction due to the increasing development of luxury electric vehicles and commercial electric vehicles that require higher power handling capabilities. Manufacturers in this segment are focusing on developing advanced cooling technologies and improved efficiency ratings to meet the demanding requirements of high-power applications. The growing trend toward fast-charging capabilities and the integration of more power-hungry features in premium electric vehicles continues to drive innovation in this segment.

Electric Vehicle High-Voltage DC-DC Converter Market Geography Segment Analysis

Electric Vehicle High-Voltage DC-DC Converter Market in North America

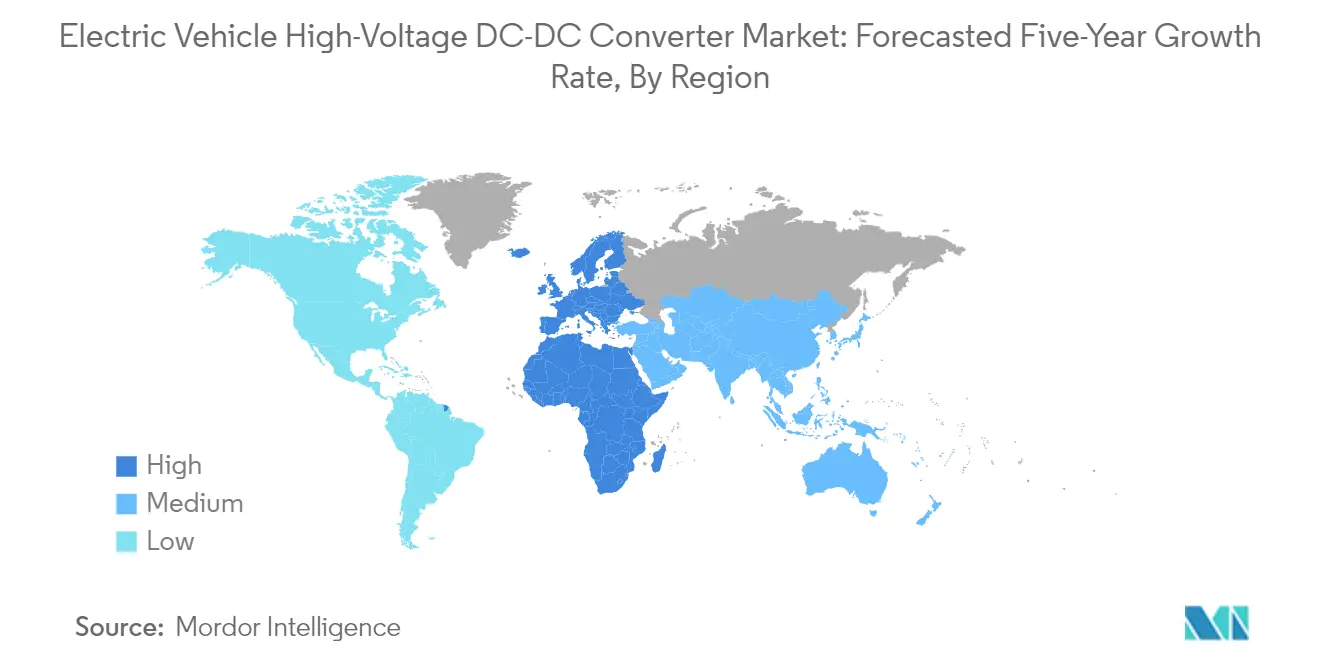

The North American electric vehicle high-voltage DC-DC converter market holds approximately 21% of the global market share in 2024, establishing itself as a significant regional market. The region's market is primarily driven by the strong presence of major electric vehicle manufacturers and extensive charging infrastructure development. The United States leads the regional market, followed by Canada, with both countries demonstrating a strong commitment to electric vehicle adoption through supportive government policies and incentives. The region's technological advancement in power electronics and automotive engineering has attracted substantial investments from both domestic and international players. The presence of key market players like Tesla and established automotive giants transitioning to electric vehicles has created a robust ecosystem for DC-DC converter manufacturing and innovation. The market is further strengthened by the region's advanced research and development capabilities, particularly in high-efficiency power conversion technologies. Consumer awareness about environmental sustainability and the increasing preference for electric vehicles have created a strong demand foundation for high-voltage DC-DC converters in the region. The North American automotive power electronics market is poised for growth, driven by innovations in electric vehicle power electronics.

Electric Vehicle High-Voltage DC-DC Converter Market in Europe

The European market for electric vehicle high-voltage DC-DC converters has demonstrated remarkable growth, with a substantial increase of approximately 39% annually from 2019 to 2024. The region's market is characterized by stringent emission regulations and aggressive electric vehicle adoption targets set by various European nations. Germany, France, and the United Kingdom emerge as the primary markets, supported by their robust automotive manufacturing capabilities and strong focus on electric mobility solutions. The region's market dynamics are shaped by the presence of established automotive manufacturers who are rapidly transitioning their production lines toward electric vehicles. European countries' commitment to phasing out internal combustion engines has created a favorable environment for market growth. The region's strong focus on technological innovation, particularly in power electronics and vehicle electrification, has fostered the development of advanced DC-DC converter solutions. The market benefits from extensive collaboration between automotive manufacturers, technology providers, and research institutions, creating a robust ecosystem for innovation and development. This growth is indicative of the expanding automotive DC-DC converter market in Europe.

Electric Vehicle High-Voltage DC-DC Converter Market in Asia-Pacific

The Asia-Pacific market for electric vehicle high-voltage DC-DC converters is projected to grow at approximately 14% annually from 2024 to 2029, highlighting the region's significant growth potential. The market is predominantly driven by China's massive electric vehicle industry, followed by emerging markets like Japan, South Korea, and India. The region benefits from its established electronics manufacturing infrastructure and growing domestic demand for electric vehicles. Asia-Pacific's market dynamics are characterized by the presence of numerous local manufacturers and increasing investments in electric vehicle technology. The region's competitive advantage in manufacturing costs and strong government support for electric vehicle adoption creates a favorable environment for market expansion. The presence of major automotive manufacturers and their increasing focus on electric vehicle production contributes significantly to market growth. The region's rapid urbanization and increasing environmental awareness among consumers continue to drive the adoption of electric vehicles, consequently boosting the demand for high-voltage DC-DC converters. The automotive power converter industry in Asia-Pacific is set to benefit from these trends.

Electric Vehicle High-Voltage DC-DC Converter Market in South America

The South American electric vehicle high-voltage DC-DC converter market is emerging as a promising growth region, with Brazil leading the regional market development. The region's market is characterized by increasing awareness about electric mobility and growing investments in electric vehicle infrastructure. Government initiatives promoting clean energy transportation and reducing dependency on conventional vehicles are driving market growth. The region's automotive industry is gradually transitioning toward electric vehicle production, creating opportunities for DC-DC converter manufacturers. Local manufacturing capabilities are developing, supported by partnerships with international technology providers. The market is witnessing increasing participation from global players who recognize the region's long-term growth potential. The gradual improvement in charging infrastructure and increasing consumer awareness about environmental sustainability are creating favorable conditions for market expansion. The development of electric vehicle component manufacturing capabilities is crucial for the region's growth.

Electric Vehicle High-Voltage DC-DC Converter Market in Middle East and Africa

The Middle East and African market for electric vehicle high-voltage DC-DC converters is in its nascent stage but shows promising growth potential. The region's market is driven by increasing investments in electric vehicle infrastructure, particularly in countries like the United Arab Emirates and Saudi Arabia. Government initiatives promoting sustainable transportation solutions are creating new opportunities for market growth. The region's focus on diversifying from oil-dependent economies is leading to increased attention toward electric mobility solutions. The market is characterized by growing partnerships between local entities and international technology providers. Rising environmental awareness and the need for sustainable transportation solutions are driving the adoption of electric vehicles in urban areas. The gradual development of charging infrastructure and increasing consumer interest in electric vehicles are creating a foundation for market expansion. The focus on developing electric vehicle component infrastructure is essential for the region's market evolution.

Competitive Landscape

Top Companies in Electric Vehicle High-Voltage DC-DC Converter Market

The electric vehicle high-voltage DC-DC converter market features prominent players like Continental AG, Robert Bosch GmbH, Denso Corporation, Toyota Industries, and Infineon Technologies leading the innovation landscape. These companies are heavily investing in research and development to create advanced automotive power converters with improved efficiency and reduced form factors. The industry witnesses continuous product launches focusing on integrated solutions, such as combo-box architectures that combine multiple powertrain components. Strategic partnerships and collaborations, particularly with automotive OEMs, have become crucial for market expansion. Companies are also emphasizing manufacturing capability enhancement through facility expansions and technological upgrades, while simultaneously working on cost optimization and supply chain resilience to maintain a competitive advantage.

Consolidated Market with Strong Regional Players

The electric vehicle high-voltage DC-DC converter market exhibits a consolidated structure dominated by large automotive technology conglomerates with an established global presence. These major players leverage their extensive R&D capabilities, established distribution networks, and long-term OEM relationships to maintain market leadership. Regional markets show varying competitive dynamics, with European manufacturers like Bosch and Continental holding a significant share in their home market, while Asian players like Denso and Toyota Industries demonstrate a strong presence in the Asia-Pacific region. The market also features specialized power electronics companies that focus exclusively on converter technologies and related components.

The industry has witnessed strategic consolidations through mergers and acquisitions, particularly aimed at technology acquisition and market expansion. Companies are increasingly focusing on vertical integration to strengthen their position in the EV supply chain. The entry barriers remain high due to substantial capital requirements, technical expertise needs, and established customer relationships. Smaller players typically focus on specific geographic regions or niche applications, while larger conglomerates maintain their dominance through comprehensive product portfolios and global reach.

Innovation and Integration Drive Future Success

Success in the EV high-voltage DC-DC converter market increasingly depends on technological innovation and integration capabilities. Companies must focus on developing more efficient, compact, and cost-effective solutions while ensuring compatibility with evolving electric vehicle components architectures. The ability to offer integrated powertrain solutions, rather than standalone components, is becoming a crucial differentiator. Manufacturers need to maintain strong relationships with automotive OEMs while simultaneously investing in next-generation technologies like silicon carbide-based converters and advanced thermal management systems. The growing emphasis on sustainability and energy efficiency creates opportunities for companies that can deliver high-performance, environmentally-friendly solutions.

Market contenders can gain ground by focusing on specialized applications or regional markets where they can build strong customer relationships and technical expertise. Success factors include developing innovative solutions for specific vehicle segments, establishing strategic partnerships with emerging EV manufacturers, and maintaining agility in response to changing market demands. The regulatory landscape, particularly regarding vehicle efficiency and emissions, continues to influence product development strategies. Companies must also address the increasing demand for standardization and interoperability while managing the risk of technological obsolescence through continuous innovation and adaptation.

Electric Vehicle High-Voltage DC-DC Converter Industry Leaders

Tesla Inc

Robert Bosch GmbH

TDK Corporation

Toyota Industries Corporation

HELLA GmbH & Co. KGaA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2023: Infineon Technologies AG and Delta Electronics Inc. expanded their long-term cooperation in EV applications to provide more efficient and higher-density solutions, such as DC-DC converters and on-board chargers. In addition, both parties agreed to set up a joint innovation lab for automotive applications. Both companies will co-manage the Delta-Infineon Automotive Innovation Center.

- October 2023: Bel Power Solutions launched a second-generation DC-DC converter to power auxiliary loads in medium and heavy-duty hybrid and electric vehicles. The 700DNG40-24-8 from Bel Fuse delivers up to 4 kW of power from industrial hybrid (HEV) battery buses and electric vehicles to power low-voltage accessories.

Global Electric Vehicle High-Voltage DC-DC Converter Market Report Scope

A high-voltage DC-DC converter operates at a high input voltage, reducing and increasing voltage upon requirement. A high-voltage DC-DC converter converts the battery's higher voltage to a lower voltage to power infotainment and safety systems.

The electric vehicle high-voltage DC-DC converter market is segmented by vehicle type, propulsion type, cooling method, input voltage, output voltage, power output, and geography. By vehicle type, the market is segmented into passenger cars and commercial vehicles. By propulsion type, the market is segmented into plug-in hybrid vehicles, battery electric vehicles, and fuel cell electric vehicles. By cooling method, the market is segmented into liquid cooled and air cooled. By input voltage, the market is segmented as 200V-450V, 450V-800V, and 800V-1000V. By the output voltage, the market is segmented as 12V-24V and 24V-48V. By power output, the market is segmented as less than 2 kW and 2 kW and above. By geography, the market is segmented into North America, Europe, Asia-Pacific, South America, and Middle East and Africa.

The report offers the market size and forecasts in value (USD) for all the above segments.

| Passenger Cars |

| Commercial Vehicles |

| Plug-in Hybrid Vehicles |

| Battery Electric Vehicles |

| Fuel Cell Electric Vehicles |

| Liquid Cooled |

| Air Cooled |

| 200 V - 450 V |

| 450 V - 800 V |

| 800 V - 1000 V |

| 12 V - 24 V |

| 24 V - 48 V |

| Less Than 2 kW |

| 2 kW and Above |

| North America | United States |

| Canada | |

| Rest of North America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Norway | |

| Poland | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Other Countries |

| Vehicle Type | Passenger Cars | |

| Commercial Vehicles | ||

| Propulsion Type | Plug-in Hybrid Vehicles | |

| Battery Electric Vehicles | ||

| Fuel Cell Electric Vehicles | ||

| Cooling Method | Liquid Cooled | |

| Air Cooled | ||

| Input Voltage | 200 V - 450 V | |

| 450 V - 800 V | ||

| 800 V - 1000 V | ||

| Output Voltage | 12 V - 24 V | |

| 24 V - 48 V | ||

| Output Power | Less Than 2 kW | |

| 2 kW and Above | ||

| Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Norway | ||

| Poland | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Other Countries | ||

Key Questions Answered in the Report

How big is the Electric Vehicle High-Voltage DC-DC Converter Market?

The Electric Vehicle High-Voltage DC-DC Converter Market size is expected to reach USD 1.67 billion in 2025 and grow at a CAGR of 14.05% to reach USD 3.21 billion by 2030.

What is the current Electric Vehicle High-Voltage DC-DC Converter Market size?

In 2025, the Electric Vehicle High-Voltage DC-DC Converter Market size is expected to reach USD 1.67 billion.

Who are the key players in Electric Vehicle High-Voltage DC-DC Converter Market?

Tesla Inc, Robert Bosch GmbH, TDK Corporation, Toyota Industries Corporation and HELLA GmbH & Co. KGaA are the major companies operating in the Electric Vehicle High-Voltage DC-DC Converter Market.

Which is the fastest growing region in Electric Vehicle High-Voltage DC-DC Converter Market?

Asia-Pacific is estimated to grow at the highest CAGR over the forecast period (2025-2030).

Which region has the biggest share in Electric Vehicle High-Voltage DC-DC Converter Market?

In 2025, the Asia-Pacific accounts for the largest market share in Electric Vehicle High-Voltage DC-DC Converter Market.

What years does this Electric Vehicle High-Voltage DC-DC Converter Market cover, and what was the market size in 2024?

In 2024, the Electric Vehicle High-Voltage DC-DC Converter Market size was estimated at USD 1.44 billion. The report covers the Electric Vehicle High-Voltage DC-DC Converter Market historical market size for years: 2019, 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Electric Vehicle High-Voltage DC-DC Converter Market size for years: 2025, 2026, 2027, 2028, 2029 and 2030.

Page last updated on: