Joint Replacement Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 20.84 Billion |

| Market Size (2031) | USD 25.77 Billion |

| Growth Rate (2026 - 2031) | 4.30% CAGR |

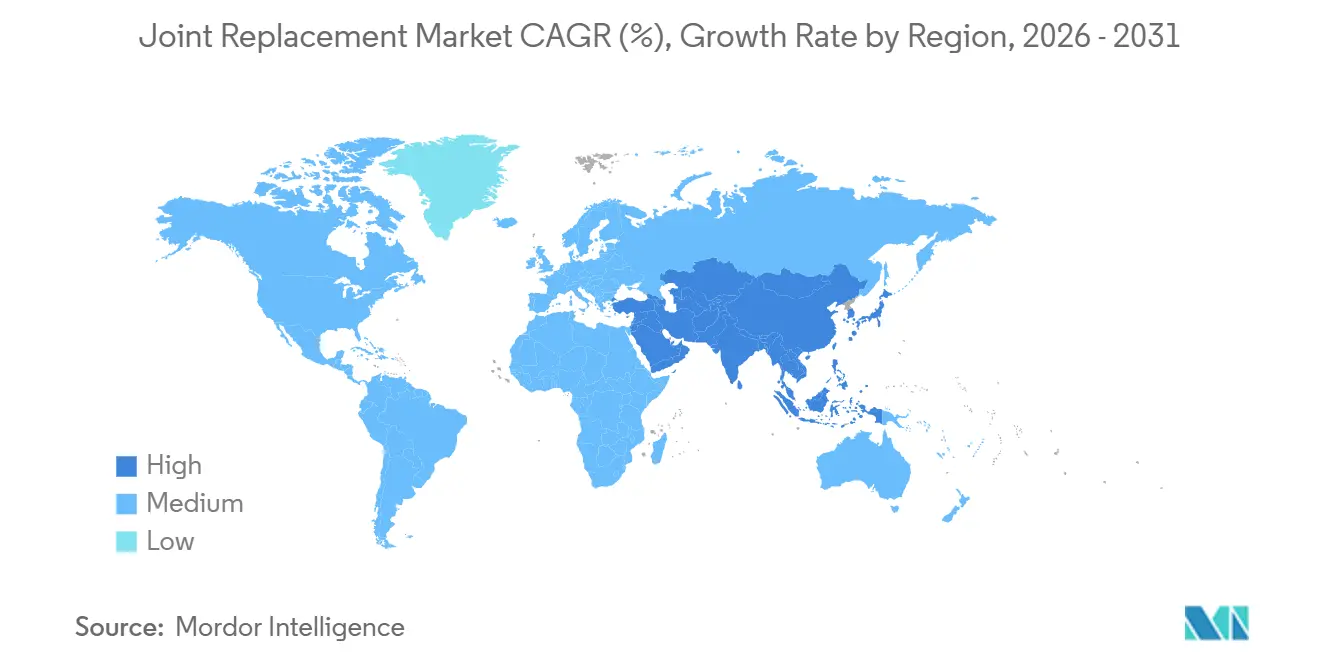

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

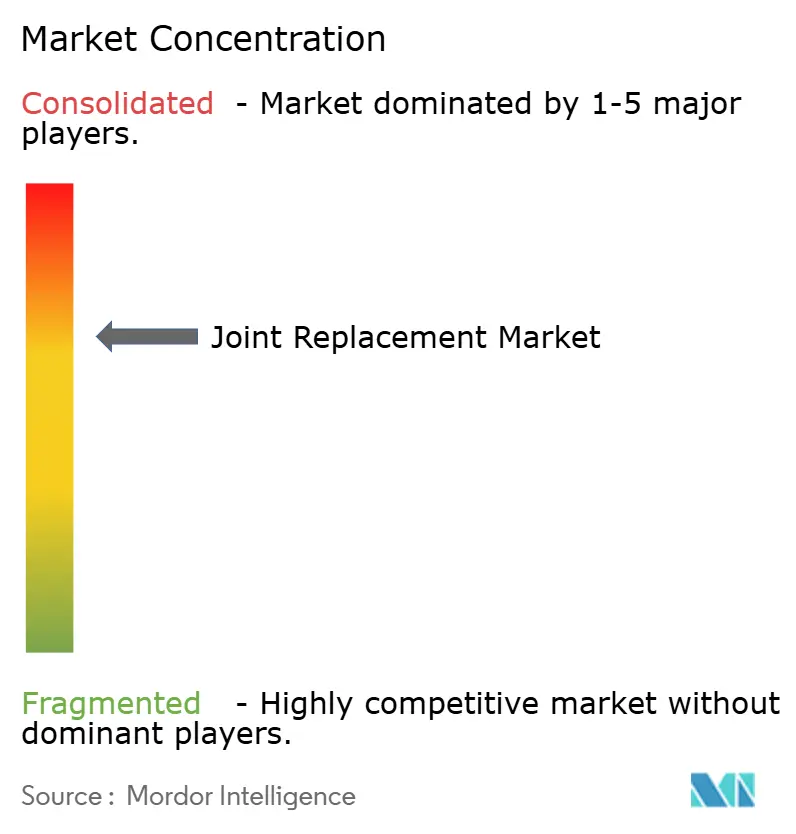

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Joint Replacement Market Analysis by Mordor Intelligence

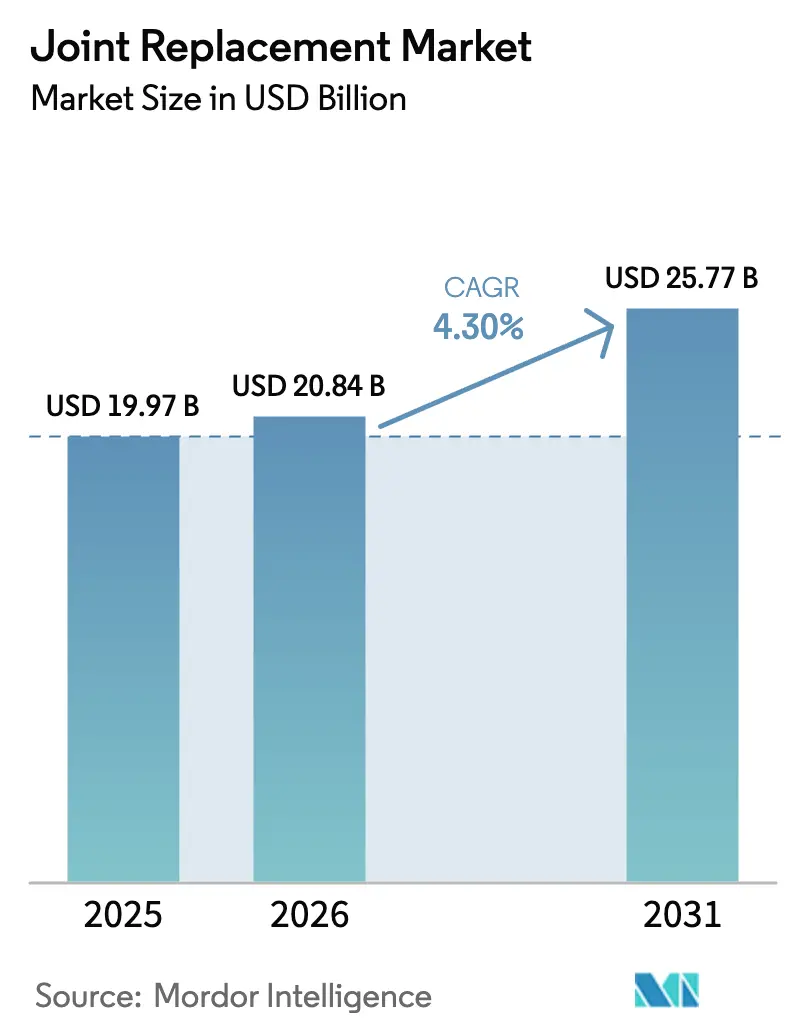

The Joint Replacement Market size is expected to grow from USD 19.97 billion in 2025 to USD 20.84 billion in 2026 and is forecast to reach USD 25.77 billion by 2031 at 4.30% CAGR over 2026-2031.

The joint replacement market is expanding as aging populations, rising obesity, and broadened insurance coverage drive procedure demand. Robotic-assisted platforms, 3D-printed implants, and fast-track rehabilitation protocols are improving operating efficiency and shortening hospital stays, which supports wider payer adoption. Integrated bundled-payment programs in the United States and Europe reward providers that reduce 90-day readmissions, prompting hospitals to invest in precision technologies that cut complications. Meanwhile, supply-chain reshoring to Costa Rica and Eastern Europe reduces tariff exposure and transport delays, ensuring steady implant availability. Competitive dynamics now revolve around ecosystem lock-in, where leading vendors bundle robots, implants, software, and analytics to secure surgeon loyalty, giving the joint replacement market sustained pricing power despite reimbursement pressure.

Key Report Takeaways

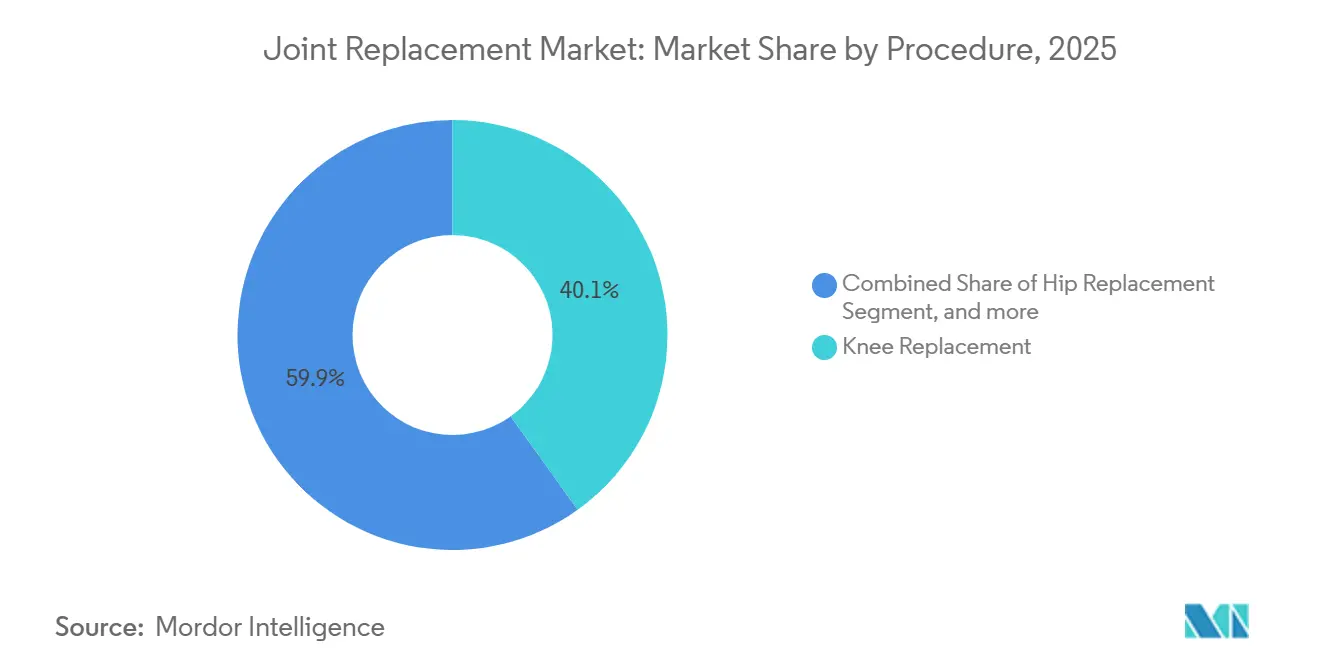

- By procedure, knee replacement captured a 40.1% joint replacement market share in 2025, while shoulder replacement recorded the fastest growth at a 5.1% CAGR through 2031.

- By product, implants accounted for 61% of the joint replacement market size in 2025; bone grafts and substitutes are advancing at a 4.9% CAGR to 2031.

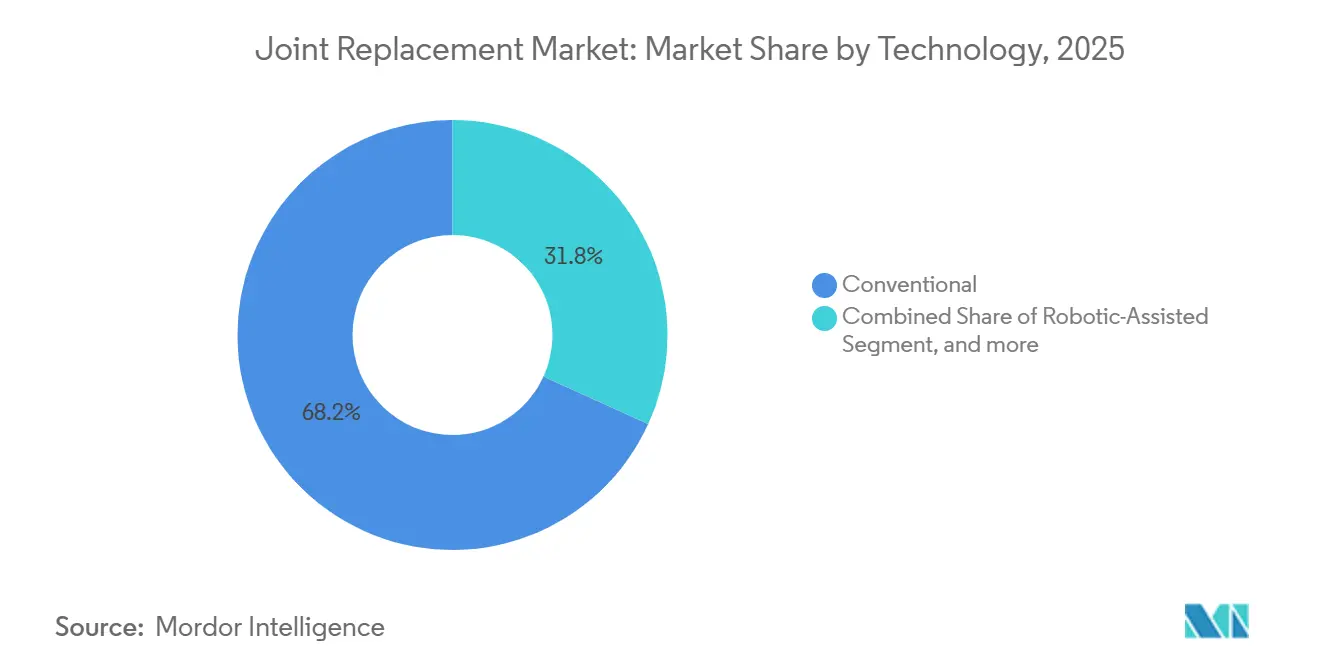

- By technology, conventional techniques held 68.2% of revenue in 2025, whereas robotic-assisted surgery is rising at a 4.7% CAGR to 2031.

- By end user, hospitals commanded 59.8% joint replacement market share in 2025, and ambulatory surgery centers are projected to grow at 5.2% through 2031.

- By geography, North America led with 45.6% of global revenue in 2025; Asia-Pacific is expected to post a 4.5% CAGR to 2031, the highest among all regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Market Trends and Insights

Drivers Impact Analysis of Joint Replacement Market*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Osteoarthritis Prevalence | +0.9% | Global, with acute burden in high-income Asia-Pacific (Japan, South Korea, Singapore) and North America | Long term (≥ 4 years) |

| Rising Geriatric Population | +0.8% | Global, with peak intensity in Japan (29% aged 65+), Europe (21% aged 65+), and China (projected 402 million aged 70+ by 2050) | Long term (≥ 4 years) |

| Growing Preference for Minimally-Invasive and Robotic-Assisted TJA | +0.9% | North America and Europe core, expanding into APAC urban centers (Shanghai, Seoul, Tokyo) | Medium term (2-4 years) |

| Accelerated Post-Op Rehab Protocols Boosting Outpatient TJA Volumes | +0.7% | United States (Medicare ASC expansion), Australia, Germany, and Netherlands | Short term (≤ 2 years) |

| 3D-Printed Patient-Specific Implants Cutting Revision Risk | +0.4% | North America and Europe, with early adoption in Singapore and UAE | Medium term (2-4 years) |

| Strategic Reshoring of Titanium and Cobalt Alloy Supply Chains | +0.3% | North America (Costa Rica nearshoring), Europe (Eastern European hubs), reducing Asia-Pacific dependence | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Osteoarthritis Prevalence

The Global Burden of Disease study counted 607 million osteoarthritis cases in 2021, and forecasts a 75% increase in knee disease by 2050 as people live longer and body-mass-index levels rise. Furthermore, the prevalence of osteoarthritis increases with age. Japan already has 29% of its citizens aged 65 plus, while South Korea will be super-aged in 2025, producing steady joint replacement market demand. Obesity adds complexity and cost, because heavier patients need reinforced implants and face higher revision risk. China’s over-70 cohort is set to reach 402 million by 2050, yet procedure rates remain one-fifth of U.S. levels, creating latent joint replacement market upside once insurance reforms mature. The combined effects of aging, obesity, and broader coverage underpin long-run volume growth, although surgeon shortages and sterile processing capacity could slow uptake in some emerging economies.

Growing Preference for Minimally Invasive and Robotic-Assisted TJA

Robotic total knee arthroplasty reached economic break-even at only 24–50 cases annually in 2024, versus 100-plus in 2020, as platform costs fell and OR times shortened. Community hospitals and ASCs now adopt robots, while vendors bundle implants and software to lock in repeat business. Clinical data show better alignment and lower dislocation rates, pushing payers to reimburse robotic procedures that shorten stays and reduce 90-day readmissions. NICE guidance in 2025 endorsed robotic orthopedics, prompting NHS procurement plans [1]National Institute for Health and Care Excellence, “Robotic-assisted surgery for orthopedic procedures,” nice.org.uk. As evidence accumulates, hospitals without robotic capacity risk losing referrals, keeping the joint replacement market on a technology-upgrade cycle.

Accelerated Post-Op Rehab Protocols Boosting Outpatient TJA Volumes

CMS added total knee procedures to ASC coverage in 2018 and total hip in 2020; same-day discharge now reaches 30–60% at high-volume U.S. centers [2]Centers for Medicare & Medicaid Services, “Ambulatory Surgical Center Payment,” cms.gov. Enhanced recovery bundles have trimmed average stays from three days to under 24 hours and cut per-episode costs by up to 60%, making ASCs attractive for low-risk patients. Bundled payments penalize readmissions, so hospitals steer healthier candidates to outpatient facilities and reserve beds for complex cases. The ASC channel, therefore, expands faster than the overall joint replacement market, pressuring implant vendors to supply streamlined, lower-cost instrument sets.

3D-Printed Patient-Specific Implants Cutting Revision Risk

FDA clearances for restor3d’s total talus and 3D Systems’ ankle guides validated additive manufacturing for anatomically challenging joints. Ten-year survivorship for 3D-printed cementless knees hit 98.1% in 2024, beating conventional designs by three points. Because revisions cost up to USD 80,000, payers accept a 15–20% implant premium to avoid failures. Regulatory pathways still differ across regions, but lattice structures that improve bone ingrowth are moving toward ISO standardization, paving the way for broader uptake and sustaining growth in the joint replacement market.

Restraints Impact Analysis of Joint Replacement Market*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Procedure and Implant Cost | -0.4% | Global, with acute impact in low- and middle-income countries (India, Brazil, South Africa, Indonesia) | Short term (≤ 2 years) |

| Availability of Pharmacological and Arthroscopic Alternatives | -0.3% | North America and Europe (mature markets with conservative treatment protocols), emerging in APAC | Short term (≤ 2 years) |

| Revision-Surgery Burden from Metal Hypersensitivity Claims | -0.3% | North America and Europe (legacy metal-on-metal cohorts), with spillover litigation risks globally | Medium term (2-4 years) |

| Capacity Bottlenecks in Sterilization and Clean-Room Machining | -0.2% | North America (ethylene oxide facility closures), APAC (infrastructure gaps in tier-2 cities) | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Procedure & Implant Cost

U.S. total knee arthroplasty costs USD 30,000–50,000, while implants alone run USD 3,000–7,000, limiting access for under-insured groups. Many patients travel to India or Thailand, where procedures cost 70–90% less, diverting volumes from domestic providers. Spending on viscosupplementation and platelet-rich plasma hit USD 2 billion in 2024, even though evidence is inconsistent, causing patients to delay surgery. Payers promote conservative care to defer expense, tempering near-term joint replacement market growth.

Revision-Surgery Burden from Metal Hypersensitivity Claims

Metal-on-metal hips continue to fail, with hypersensitivity in up to 15% of recipients, forcing costly revisions. The FDA spotlighted a 31.8% ten-year failure rate for the Hintermann H3 ankle, heightening regulatory scrutiny. U.S. ethylene-oxide capacity fell 20% after Sterigenics closures, forcing costly freight to offshore sterilizers and delaying shipments. Cobalt price spikes and tight machining capacity expose supply-chain fragility, adding cost and dampening the joint replacement market outlook until redundancy improves.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Joint Replacement Market Segment Analysis

By Procedure:

Shoulder Replacement Outpaces Mature Knee SegmentShoulder procedures are growing at a 5.1% CAGR to 2031 as reverse designs address fractures and revisions once treated non-operatively. FDA clearance of Stryker’s Aequalis Perform+ and Zimmer’s glenoid reconstruction solutions widened indications. Ten-year survivorship reaches 95%, shifting surgeons from anatomic models for patients over 70. Knee replacement still held 40.1% joint replacement market share in 2025 due to consistent Medicare payment, yet its growth slows as U.S. penetration nears northern European saturation levels. Hip arthroplasty benefits from robotic adoption that cuts dislocations by 40%, while ankle and elbow remain niche but may expand as 3D-printed devices solve complex anatomies.

By Product:

Bone Grafts Gain Share as Revision Volumes ClimbSynthetic and allograft substitutes are advancing at 4.9% CAGR as older implants reach end-of-life. FDA clearances for demineralized matrices and calcium phosphate ceramics bolster surgeon confidence [3]U.S. Food and Drug Administration, “510(k) Clearances – Bone Graft Substitutes,” fda.gov. Improved donor screening lowered infection risk, but tight supply gives tissue banks pricing power. Implants captured 61% of the joint replacement market size in 2025, though share may slip as graft content per case rises. Highly cross-linked polyethylene and ceramic heads halve wear, while single-use instrument kits cut ASC sterilization costs.

By Technology:

Robotic Platforms Erode Conventional ShareRobotic systems grow at 4.7% CAGR as capital hurdles drop and reimbursement recognizes lower readmissions. NICE approval accelerates European uptake, and U.S. ASCs install robots to attract commercially insured patients. Conventional methods still control 68.2% revenue, but their share declines as hospitals look to shorten stays and align with bundled-payment incentives. Augmented-reality navigation offers a lower-cost alternative for mid-volume centers, yet outcome data remain mixed, limiting immediate impact on the joint replacement market.

By End User:

ASCs Capture Share Under Bundled PaymentsAmbulatory centers rise 5.2% annually, supported by protocols that discharge patients in under a day and cut costs by half. Roughly 60% of hip and knee candidates meet current ASC criteria, a ceiling likely to expand with better anesthesia. Hospitals keep complex revisions and high-BMI cases, preserving 59.8% revenue in 2025, but must differentiate with robotics and tertiary care to offset volume shifts. Specialty orthopedic centers offer a hybrid model of efficiency and critical-care backup, reinforcing a multi-channel joint replacement market.

Geography Analysis

North America Joint Replacement Market

North America held 45.6% of global revenue in 2025, supported by the United States’ high procedure rate of 7.2 total knee arthroplasties per 1,000 people and the sale of robotic consoles priced above USD 1 million each. After the Centers for Medicare & Medicaid Services removed total hip arthroplasty from the inpatient-only list in January 2024, more surgeries shifted to outpatient settings, tightening hospital margins and prompting distributor consolidation. Canada’s publicly funded system posted a 12-month median wait for hip replacement in 2024, steering patients to U.S. ambulatory surgery centers near the border. Mexico’s medical-tourism hubs in Tijuana and Monterrey treated 45,000 joint-replacement patients in 2024, offering ISO 13485-certified implants at half of U.S. prices. Regional growth faces a supply pinch because the FDA issued 23 warning letters for excess ethylene oxide residue in 2024, delaying new product launches by up to nine months.

APAC Joint Replacement Market

Asia-Pacific is growing at a 4.5% CAGR, the fastest among all regions. Japan’s super-aged profile, with 29% of residents at least 65 in 2024, helped lift total knee procedures to 180,000 that year, a 12% rise since 2020, after reimbursement changes rewarded cementless porous implants. China expanded insurance to cover 95% of urban residents for joint replacement by 2025, adding further momentum. India drew 120,000 overseas patients to Chennai and Mumbai in 2024, thanks to JCI-accredited hospitals and implant prices 60% below Western levels. South Korea’s insurer began paying for reverse shoulder arthroplasty in 2025, opening access for rotator-cuff cases, while Australia cut approval times for robotic systems to nine months in 2024, letting firms launch locally in the same quarter as U.S. and EU clearances.

EMEA and South America Joint Replacement Market

In Europe, Medical Device Regulation compliance now averages EUR 2 million per product family and extends CE-mark timelines to about two years, slowing growth. Germany and France still perform many hip revisions: the German registry logged 28,000 in 2024, 40% tied to cobalt-chromium debris from older metal-on-metal implants. The United Kingdom’s National Health Service negotiated a 15% price cut on knee implants for 2025, pushing manufacturers to rely on private-pay volumes to protect margins. The Middle East and Africa gain from government spending. Saudi Arabia’s Vision 2030 commits USD 10 billion to build orthopedic centers, aiming for 50,000 annual joint replacements by 2028. South America centers on Brazil, where private insurance covered 27% of citizens in 2024. Public hospitals face wait times longer than 18 months, so private facilities capture demand for premium implants.

Regulatory Landscape

Regulation for joint replacement devices continues to tighten around technical documentation, clinical evidence expectations, and post-market surveillance, with notable region-by-region differences that affect time-to-market and portfolio prioritization. In the European Union, the European Commission adopted delegated regulations in March 2026 amending MDR (EU) 2017/745 to expand the list of implantable and Class III devices treated as well-established technologies, including exemptions tied to clinical investigation and certain notified-body review steps. This shifts the compliance burden for established arthroplasty categories.

In the United States, the FDA published a final rule in April 2026 codifying the classification of a manual surgical instrument used for orthopedic implant patient selection into Class II, anchoring requirements for validated geometry and measurement processes that connect preoperative planning and intraoperative execution. The FDA also signals alignment with evolving standards in December 2025, referencing updated orthopedic consensus standards such as ISO 21536:2023 for knee implants, which shapes how manufacturers prepare submissions. In Australia, market access and pricing for implantables remain closely tied to the Department of Health and Aged Care Prescribed List, with an updated version implemented in July 2026 that informs private health insurer benefits and product listing dynamics.

Value Chain Analysis

The joint replacement value chain spans raw-material inputs (titanium and cobalt-chrome alloys, and polymeric materials such as PEEK), precision manufacturing (machining, additive manufacturing where applicable, finishing), and critical services including coatings, packaging, and sterilization before distribution to hospitals and ambulatory surgery centers (ASCs). Major OEMs such as Stryker, Zimmer Biomet, and DePuy Synthes increasingly complement internal manufacturing with specialized contract manufacturers for components and instruments, while relying on third-party partners for high-compliance steps like coating and sterilization.

Recent supply-chain constraints have focused on imported material exposure, sterilization capacity bottlenecks (notably ethylene oxide), and logistics volatility, which has reinforced strategies such as nearshoring to hubs like Costa Rica and tighter coordination with perioperative capital suppliers. Partnerships that bundle implants with operating room integration and workflow capabilities are also shaping channel economics, as shown by Zimmer Biomet expanding its ASC-facing offering through a July 2025 distribution partnership with Getinge for operating room capital products. OEMs have also used M&A and digital platforms to deepen the procedure ecosystem, including Zimmer Biomet's July 2025 agreement to acquire Monogram Technologies to add autonomous CT-based robotic knee capability and its OneStep collaboration to feed mobility data into the mymobility care platform, affecting downstream utilization, inventory planning, and service attachment.

Competitive Landscape

Zimmer Biomet, Stryker, and DePuy Synthes together control a majority of global revenue, reflecting a moderately concentrated joint replacement market. Their integrated robotic platforms create high switching costs and recurring software fees. Stryker’s Mako achieved 1,400 global installs by mid-2024, and robotic cases now make up 18% of its U.S. knee volumes. Smith & Nephew, Johnson & Johnson, and others are reshoring component machining to Costa Rica and Eastern Europe to cut transit time and tariff risk. Niche players such as Conformis and Medacta pursue patient-specific and augmented-reality niches, while new entrants like Globus aim to leverage existing spine robots for knee modules by 2026. Quality lapses, exemplified by Exactech’s recall of 150,000 polyethylene components, underscore reputational stakes in a safety-critical joint replacement market.

Joint Replacement Industry Leaders

Stryker Corporation

Zimmer Biomet Holdings, Inc.

Depuy Synthes (Johnson & Johnson)

Smith & Nephew

B. Braun SE

- *Disclaimer: Major Players sorted in no particular order

Joint Replacement Market Companies Covered in this Report

- Arthrex

- B. Braun

- Bioimpianti Srl

- Conformis

- Corin Group

- DePuy Synthes

- Enovis

- Exactech

- Globus Medical

- Kyocera Medical

- LimaCorporate

- Medacta Group

- MicroPort

- Smiths Group

- Stryker

- United Orthopedic Corp.

- Uteshiya Medicare

- Waldemar Link

- Zimmer Biomet

Market Opportunities and Future Outlook

A key whitespace in joint replacement is the accelerating shift of eligible procedures into ambulatory and single-specialty settings, pulling demand toward streamlined instrument sets, lower total episode cost, and integrated digital workflow tools that reduce variability. In 2026, multiple facility actions underscore this care-site buildout: Hospital for Special Surgery opened the 94,000-square-foot Kellen Tower in New York (March 2026) to expand specialized capacity for joint replacement and spine, and Boston Bone and Joint Institute opened a 79,500-square-foot orthopedic ASC in Waltham, Massachusetts (June 2026). These expansions strengthen the value proposition for vendor offerings that combine implants with navigation or robotics, analytics, and perioperative services designed for ASC throughput.

Product and enabling-technology opportunities are also concentrating in differentiated materials and AI-assisted intraoperative decision support aimed at reducing complications and standardizing execution across surgeon experience levels. FDA clearances continue to refresh competitive positioning in knees, including DePuy Ireland UC's 510(k) clearance for the ATTUNE Total Knee System (November 2025) and Shalby Advanced Technologies receiving FDA 510(k) clearance for its Tahoe Unicondylar Knee System with a TiNbN overcoat (April 2026). Because bundled-payment programs and 90-day outcomes remain central to provider decision-making, solutions that reduce revisions and infection-related readmissions, while integrating into care-management platforms and outpatient workflows, are seeing clear pull from both health systems and ASCs.

Recent Industry Developments in Joint Replacement Market

- June 2026: DePuy Synthes announced US commercial availability of VELYS Hip Navigation with AI Assistance for total hip arthroplasty. The launch expands J&J MedTechs digital-surgery footprint beyond knee robotics into hip workflows, strengthening its ability to bundle enabling technology with implant portfolios in hospital and ASC accounts.

- April 2026: Stryker launched the Trident II Acetabular System in India, positioning the implant for hip replacement procedures and compatibility with the Mako SmartRobotics ecosystem. The development deepens Strykers emerging-market presence while reinforcing ecosystem lock-in through a connected robot-and-implant pathway.

- October 2025: Zimmer Biomet received FDA Breakthrough Device Designation for an iodine-treated total hip replacement system aimed at addressing infection risk. The designation elevates innovation around infection prevention as a differentiator in arthroplasty, supporting premium positioning where providers and payers focus on reducing costly complications.

Joint Replacement Market Report Scope and Research Methodology

Market Definition and Coverage

For this study, the joint replacement market is defined as the revenue earned from implants, grafts, and dedicated instruments used in procedures that fully or partially replace synovial joints, including primary and revision arthroplasty.

Scope exclusions: Trauma fixation hardware that is not intended for arthroplasty is not counted in this market size.

Segments Covered in This Report

- By Procedure

- Hip Replacement

- Knee Replacement

- Shoulder Replacement

- Ankle Replacement

- Elbow Replacement

- Others

- By Product

- Implants

- Metallic

- Ceramic

- Polymeric & Hybrid Biomaterials

- Bone Grafts & Substitutes

- Autograft

- Allograft

- Synthetic

- Fixation & Instrumentation

- Others

- Implants

- By Technology

- Conventional

- Robotic-Assisted

- Navigation / AR-Guided

- By End User

- Hospitals

- Specialty Orthopaedic Centres

- Ambulatory Surgery Centres

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East & Africa

- GCC

- South Africa

- Rest of Middle East & Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the starting market structure and confirm procedure and patient level signals that drive demand. We relied on public, non-paywalled sources such as the US Centers for Disease Control and Prevention for arthritis burden, the US Food and Drug Administration for device clearances and safety updates, the World Health Organization for aging and musculoskeletal indicators, and OECD health statistics for surgery and hospital activity where available.

To make the inputs workable in a revenue model, we also cross-checked additional references, including orthopedic society publications, peer-reviewed clinical journals on arthroplasty utilization and revision rates, investor presentations, and annual filings. Select paid subscriptions were used for company financials, patent lookups, and shipment level import and export checks to sanity test regional supply signals. The sources listed here are illustrative only, and we reviewed many other references to collect data, validate assumptions, and close gaps.

Primary Interviews and Surveys

Primary discussions were completed with orthopedic device makers, distributors, hospital procurement teams, and clinicians to confirm what is actually used in the operating room and how pricing moves by region. We also tested assumptions on primary versus revision mix, the adoption pace of newer materials and techniques, and where capacity or reimbursement limits can slow procedures across APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 39% | CXOs: 14% | APAC: 48% |

| Mid tier: 42% | Functional/Unit leaders: 28% | EMEA: 34% |

| Smaller Players: 19% | Managers: 58% | Americas: 18% |

Market-Sizing & Forecasting

Sizing starts with a top-down build where population aging and osteoarthritis burden are translated into an addressable procedure pool, then adjusted by treatment rates and healthcare access to arrive at expected arthroplasty volumes. That volume pool is converted into value using average selling price ranges for implants and procedure-related instrument sets, and then aligned to mix shifts across hip, knee, shoulder, ankle, and other joint categories.

A few inputs shape the model most: primary versus revision share, revision rates by joint type, average implant pricing by geography, hospital versus ambulatory procedure share, and the pace of adoption for newer implant materials and surgical approaches that can shift pricing. Where a data series is thin in a country, we use proxy indicators like orthopedic surgeon density, elective surgery capacity, and reimbursement coverage, then correct them using interview feedback.

Forecasts are built using scenario analysis, since procedure volumes and pricing can change with reimbursement updates, waiting list normalization, and capacity constraints in hospitals. We corroborate the totals with selective bottom-up approximations, such as sampled ASP times estimated unit volumes and supplier and channel checks, which keeps the final number practical and repeatable without presenting it as a fully bottom-up model.

Data Validation & Update Cycle

Validation is done through triangulation across demand signals, supply side indicators, and interview feedback, then through step-by-step variance checks at the region level and at global totals. When a country result moves too far from expected procedure trends or trade signals, we reopen assumptions and run follow-up calls to recheck pricing and mix.

Before sign-off, the model and write-up are reviewed by another analyst to ensure definitions, units, and currency handling are consistent. The report is refreshed annually, with interim updates when a material event changes procedure volumes, reimbursement direction, or pricing behavior. Right before delivery, we complete a final pass so the numbers reflect the most recent information available.

Mordor Intelligence's Joint Replacement Market Size Compared With Other Published Estimates

Published market sizes for joint replacement can differ even when they appear to cover the same topic, because the boundary of what is counted is not always identical. Differences commonly come from what is included in the device basket, whether revision procedures are treated distinctly, and how regional pricing is converted into a single USD value.

By tracking procedure volume signals and implant ASP ranges, Mordor Intelligence keeps the estimate tied to synovial joint arthroplasty devices and excludes trauma fixation hardware that does not belong in replacement procedures. This scope line is a common reason totals move between publishers.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 19.97 B (2025) | |

| Trade Journal A | USD 22.60 B (2024) | Uses an editorial estimate for a prior year and does not clearly separate enabling technologies or adjacent orthopedic spend from core joint replacement devices, which can inflate the value when bundled. |

| Global Consultancy B | USD 35.18 B (2031) | Shows a later forecast year and can differ on what is included within joint replacement devices, plus the growth path may reflect a more aggressive assumption on procedure recovery and price uplift across regions. |

The spread in values is mainly explained by year selection and by scope boundaries, especially whether adjacent orthopedic device categories are mixed into the total. Using a clearly stated device definition, procedure-led demand logic, and pricing checks by region helps us keep a balanced number that clients can trace back to simple, repeatable inputs.

Key Questions Answered in the Report

How large is the Joint Replacement market ?

The Joint Replacement market size is expected to reach USD 20.84 billion in 2026 and is projected to grow at a 4.30% CAGR to USD 25.77 billion by 2031.

Which procedure type is expanding fastest in Joint Replacement market?

Shoulder replacement is the fastest-growing segment, advancing at a 5.1% CAGR through 2031 as reverse designs address fractures and revisions.

Why are ambulatory surgery centers gaining share in joint replacement?

Bundled payments and fast-track rehab enable same-day discharge, cutting per-episode costs by up to 60% and driving a 5.2% CAGR for ASCs.

What role do robotic systems play in the Joint Replacement market?

Robots reduce alignment errors, shorten hospital stays, and now reach cost break-even at 24–50 cases annually, fueling a 4.7% CAGR for robotic procedures.

Which region offers the highest growth potential going forward?

Asia-Pacific, led by China and India, is forecast to grow at 4.5% through 2031 as aging populations, rising incomes, and medical tourism boost volumes.

How concentrated is competition among implant makers?

Zimmer Biomet, Stryker, and DePuy Synthes control a majority of revenue, giving the market moderate concentration but still room for niche innovators.

Page last updated on: