Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

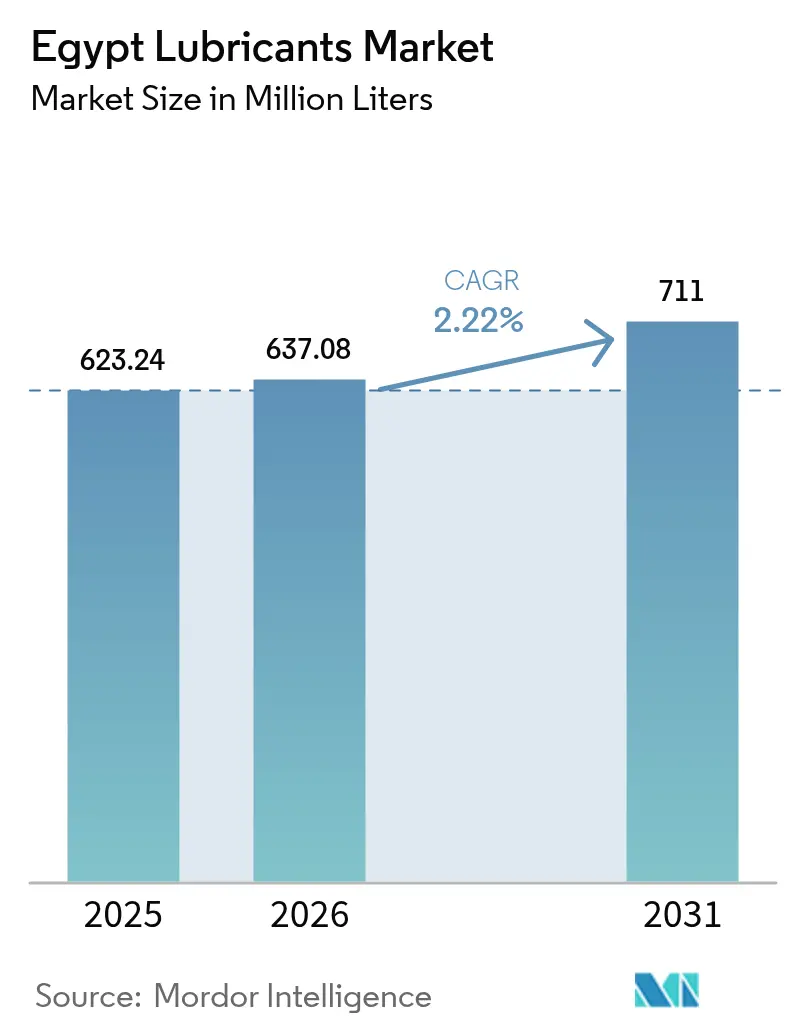

| Base Year Market Size (2025) | 623.24 Million liters |

| Market Volume (2026) | 637.08 Million liters |

| Market Volume (2031) | 711 Million liters |

| Growth Rate (2026 - 2031) | 2.22% CAGR |

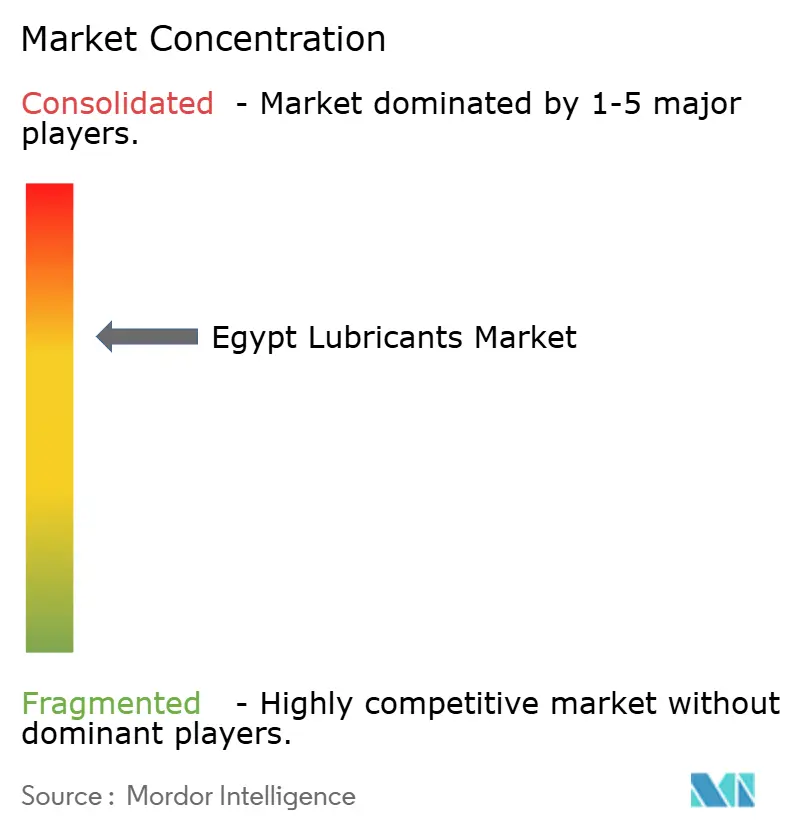

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Egypt Lubricants Market Analysis by Mordor Intelligence

The Egypt Lubricants Market size is expected to increase from 623.24 Million liters in 2025 to 637.08 Million liters in 2026 and reach 711 Million liters by 2031, growing at a CAGR of 2.22% over 2026-2031. Currency depreciation, import-cost inflation, and counterfeit risk keep price sensitivity high, yet investment in local blending, renewable energy, and infrastructure spending is lifting underlying demand. Automotive engine oil dominates volumes, while greases are the fastest-growing product thanks to the USD 169 billion infrastructure pipeline that is expanding heavy-equipment fleets. Foreign direct investment in the Suez Canal Economic Zone and the New Administrative Capital has attracted multinational blenders that view local production as a hedge against tariff and exchange-rate shocks. Parallel moves by electricity utilities toward gas-fired and renewable capacity are raising consumption of turbine, transformer, and hydraulic oils. Although mineral oils still command two-thirds of demand, stricter OEM warranty terms for Euro 6 vehicles and combined-cycle gas turbines are accelerating the adoption of synthetics that promise longer drain intervals and lower lifetime costs.

Key Report Takeaways

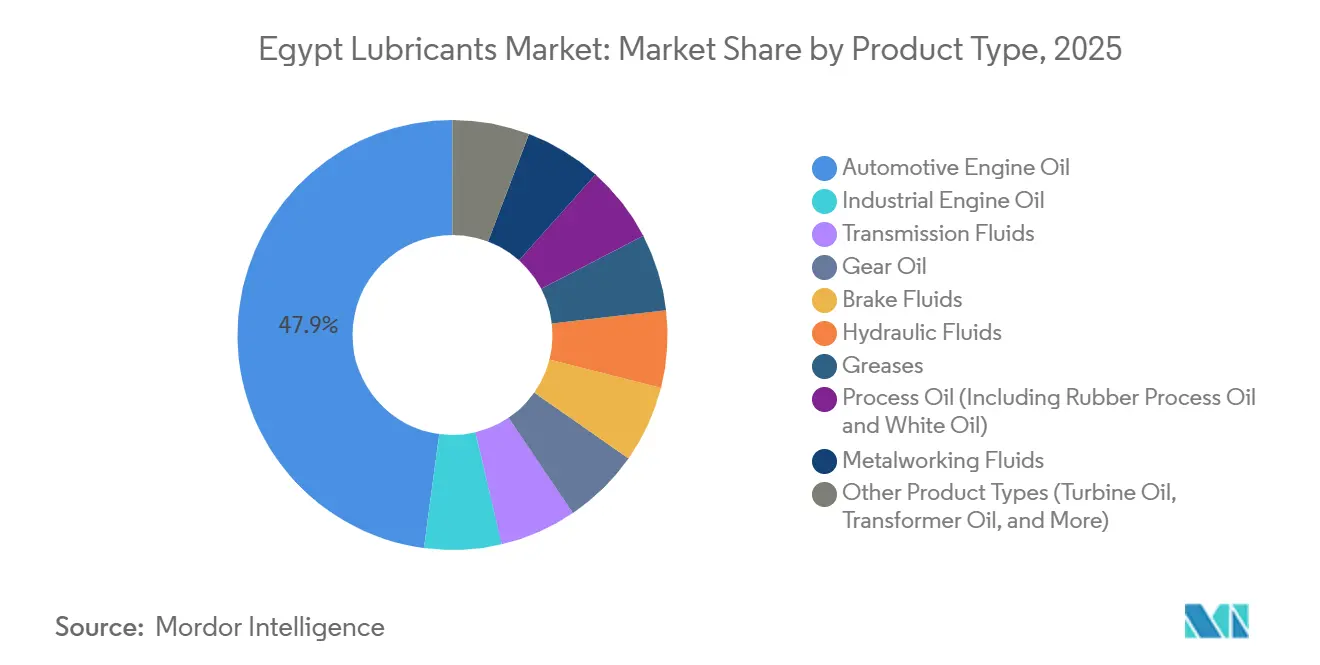

- By product type, automotive engine oil led with 47.89% of the Egypt Lubricants market share in 2025, and greases are forecast to expand at a 4.93% CAGR during the forecast period (2026-2031).

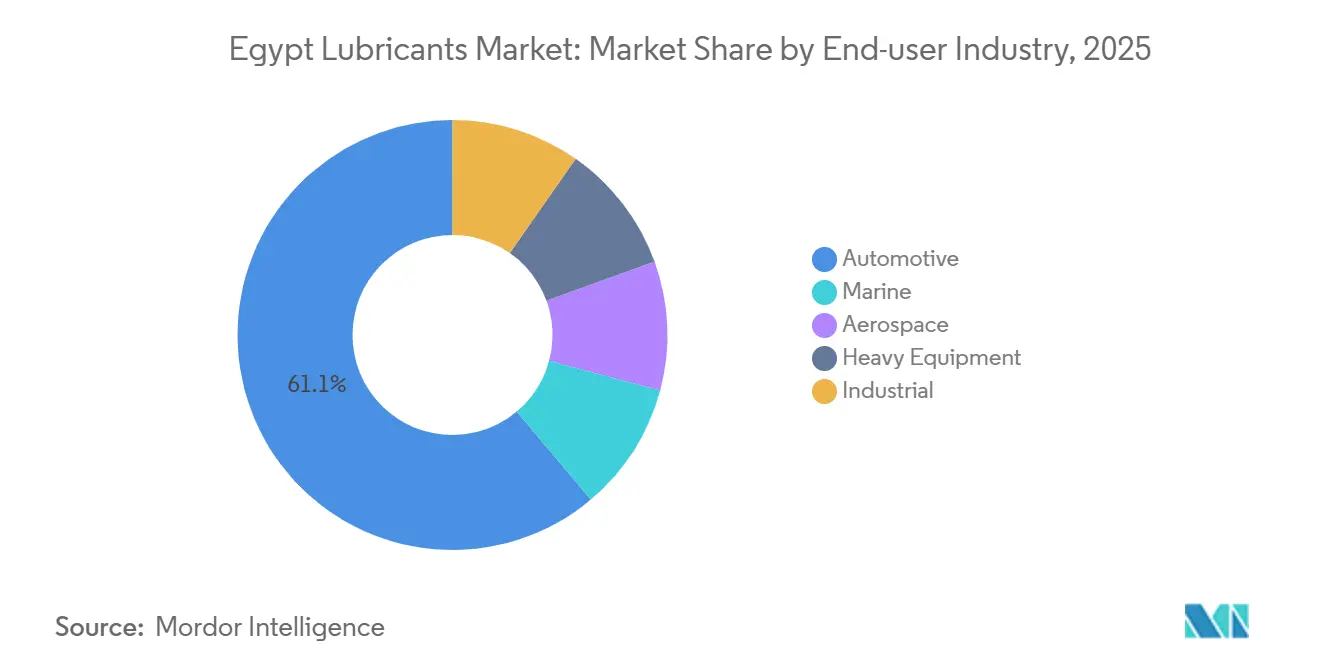

- By end-user industry, automotive accounted for 61.12% of the Egypt Lubricants market size in 2025, while industrial is advancing at a 3.88% CAGR during the forecast period (2026-2031).

- By base stock type, mineral oil-based lubricants accounted for 66.28% of the market share, and during the forecast period (2026-2031), the share of synthetic lubricants is expected to rise with a CAGR of 3.12%.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Egypt Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| FDI-driven manufacturing clusters | +0.6% | Suez Canal Economic Zone, New Administrative Capital | Medium term (2-4 years) |

| Government gas-fired power build-out | +0.5% | National, early gains in Beni Suef, Burullus, New Capital | Long term (≥ 4 years) |

| Local blending hubs hedging FX and tariffs | +0.4% | Alexandria, Borg El Arab, 10th of Ramadan | Short term (≤ 2 years) |

| Fast-growing e-commerce for DIY lubricant sales | +0.2% | Greater Cairo, Alexandria, Nile Delta | Medium term (2-4 years) |

| Green-hydrogen mega-projects | +0.3% | Suez Canal corridor, Gulf of Suez | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

FDI-Driven Manufacturing Clusters in Suez and the New Capital

The influx of multinationals into the Suez Canal Economic Zone and the New Administrative Capital is forming dense supply hubs for automotive assembly, petrochemicals, and logistics. Siemens’ 4.8 GW combined-cycle facility anchors the New Capital power cluster and generates recurring turbine-oil demand over the next two decades[1]Siemens AG, “Egypt Megaproject Fact Sheet,” siemens.com. TVS Motor’s USD 6.5 million motorcycle plant, inaugurated in 2025, boosts two-wheeler engine oil volumes and shortens lead times for local blenders. Egyptian Organization for Standardization and Quality (EOS) Standard 1391/2024 sets uniform metal-working-fluid benchmarks, ensuring locally blended coolants match ISO (International Organization for Standardization) equivalents and reinforcing buyer confidence. FDI (Foreign Direct Investment) concentration also enables just-in-time deliveries that reduce working capital and facilitate rapid formulation upgrades when OEM (Original equipment manufacturer) engine platforms change. Together, these factors underpin stable offtake for premium hydraulic, grease, and gear-oil grades across clustered factories.

Government Gas-Fired Power Build-Out (40 GW+)

Electricity generation grew 6% in fiscal 2023-24 to 229.1 GWh as Egypt shifted toward efficient combined-cycle gas plants that rely on high-performance turbine oils, transformer oils, and insulating fluids. The Egyptian Electricity Transmission Company (EETC) budgeted EGP 44.9 billion (USD 951 million) for grid upgrades in 2025-26, including a 500 kV station financed by the EBRD (European Bank for Reconstruction and Development) that will specify IEC 60296-compliant dielectric oils. GE steam-turbine retrofits at West Damietta and Assiut raise plant efficiency to 61% and lock in long-term demand for synthetic steam-turbine oils. Improved fuel savings, free capex for transformer additions that further widen the lubricant addressable market. As projects move from commissioning to routine service, long drain intervals elevate the role of condition-monitoring additives and premium base stocks.

Local Blending Hubs Hedging FX and Tariff Shocks

Sharp pound depreciation lifted the petroleum trade deficit to USD 7.65 billion in fiscal 2023-24 and made imported finished oils cost-prohibitive. ADNOC Distribution and TotalEnergies reacted by launching ADNOC Voyager in May 2025 at Borg El Arab, targeting 3,000 retail outlets by end-2026 and cutting shipping costs versus Gulf imports. Shell followed with a five-year exclusive production deal at the Egyptian Development Company’s plant in September 2025. Misr Petroleum’s Amriya and Mafroza plants give the state a major 180,000 tons per year of oil capacity, reinforcing its cost edge in public tenders. GOEIC (General Organization for Export and Import Control) Policy 6535/2024 tightened documentation rules, squeezing gray-market importers and channeling volume to compliant domestic blenders.

Fast-Growing E-Commerce for DIY Lubricant Sales

Do-it-yourself consumers in Greater Cairo and Alexandria increasingly order small-pack engine oils through Amazon and Noon, sidestepping congested service stations. ExxonMobil’s Mobilawy loyalty app uses gamified rewards to upsell synthetic grades and won a global program award in 2024. TotalEnergies’ Mobility Business platform, launched in September 2025, integrates telematics, payments, and predictive maintenance that sends timely oil-change prompts to fleet managers. Although online penetration is still below 5%, smartphone adoption and urban time pressure are accelerating digital uptake. Real-time sales data enables blenders to allocate inventory dynamically, shrinking stock-outs during summer peak driving months.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Counterfeit and re-refined products | -0.4% | Cairo, Alexandria, Nile Delta | Short term (≤ 2 years) |

| EGP depreciation affecting additive imports | -0.5% | National | Medium term (2-4 years) |

| ACEA C3 / Euro 6 oil-quality cost pressure | -0.3% | Urban centers with newer fleets | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Counterfeit and Re-Refined Products

Unauthorized dealers in Cairo and Alexandria sell counterfeit engine oils that often lack correct viscosity or additive balance, risking engine seizure and voiding OEM warranties[2]Egyptian Organization for Standardization and Quality, “Counterfeit Lubricant Advisory,” eos.org.eg. Re-refined base stocks, though certified by HiTech Oils & Grease, face image hurdles despite meeting API standards. Weak penalties and limited enforcement staff constrain EOS crackdowns, letting counterfeiters shift operations quickly. Multinationals now invest in hologram seals, tamper-evident caps, and QR tracking, yet fragmented retail channels dilute consumer-education campaigns. Until traceability improves, premium synthetic adoption will lag potential.

EGP Depreciation Constraining Imported Additives

Additives such as Zinc Dialkyl Dithiophosphate (ZDDP) anti-wear agents and viscosity modifiers are imported mainly from Europe, the United States, and Asia, leaving blenders exposed to FX swings. The pound’s decline has lifted landed additive cost by double digits, compressing margins or forcing price hikes that dealers resist. Long-term USD-denominated contracts risk renegotiation if further devaluation occurs, creating supply uncertainty that may trigger production pauses. GOEIC’s stricter import paperwork also extends customs dwell times, compounding inventory-planning challenges. Companies with regional additive storage or multi-currency hedging gain a buffer, but smaller blenders face spot-market volatility.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Engine Oils Anchor Volume, Greases Lead Growth

Automotive engine oil commanded 47.89% of Egypt Lubricants market size in 2025 as vehicle registrations rebounded to 155,950 units after import restrictions eased. Passenger-car owners primarily choose 5W-30 and 10W-40 grades, while light-commercial fleets prefer cost-efficient 15W-40 mineral oils. Greases are forecast to post a 4.93% CAGR during the forecast period (2026-2031), fueled by heavy-equipment deployments on roads, ports, and renewable-energy sites. Centralized lubrication systems on excavators and wheel loaders now specify lithium-complex and calcium-sulfonate greases with higher water-washout resistance, pushing sales of premium thickeners. Metalworking-fluid volumes correlate with textile, appliance, and steel investment in the Suez hub, where local blenders supply semi-synthetic emulsions that meet EOS 1391/2024. Transformer oil demand rises in parallel with EETC substation builds, and turbine oil use climbs as combined-cycle conversions gain momentum. Brake-fluid sales remain steady in older vehicle fleets that predominantly employ DOT 3 specifications, while demand for high-temperature DOT 5.1 silicone fluid stays niche.

A shift toward natural-gas vehicles is spurring adoption of low-ash transmission fluids and factory-fill gear oils approved for spark-ignited engines. GASTEC’s 107% surge in NGV sales during 2024 encouraged blenders to roll out GL-4 and GL-5 products formulated for methane fuel contaminants. Process-oil applications remain limited, yet rising pharmaceutical output in the New Capital industrial parks is opening demand for USP-grade white oils. Together, these trends keep the Egypt lubricants market diversified, though engine oils and greases will continue to dominate volume and value pools.

By End-User Industry: Automotive Dominates, Industrial Accelerates

The automotive sector captured 61.12% of Egypt Lubricants market share in 2025, reflecting the country’s standing as North Africa’s second-largest vehicle market. Passenger cars rely on OEM-approved synthetic blends for warranty retention, yet small independent workshops still favor mineral oils for affordability. Commercial fleets operating Euro 5 trucks are migrating toward extended-drain synthetics like Mobil Delvac 15W-40 to cut downtime, though the pace depends on freight rates and financing costs. Two-wheelers, buoyed by TVS Motor’s 100,000-units-per-year Giza plant, consume 10W-30 motorcycle oils with friction modifiers that protect integrated clutches.

Industrial users are set to grow at a 3.88% CAGR during the forecast period (2026-2031) as the power, metallurgy, and upstream-gas segments scale. EETC’s transmission-upgrade program requires regular transformer oil sampling and top-ups, creating a steady aftermarket. Shell’s 2025 metalworking-fluid trial at a domestic steel mill demonstrated 15% tool-life improvement and has accelerated conversion to chlorine-free neat oils. Offshore gas projects by BP, Chevron, and ExxonMobil rely on high-VI compressors and hydraulic fluids that can withstand high salinity and extreme pressure. Marine lubricants linked to Suez Canal transits dipped after Red Sea security disruptions, yet upside exists once shipping lanes normalize. Construction and mining equipment remain lubricant-intensive, especially as megaprojects push excavator and wheel-loader operating hours higher.

By Base Stock Type: Mineral Oils Prevail, Synthetics Gain Share

Mineral oils represented 66.28% of Egypt Lubricants market size in 2025, driven by price-oriented fleets that still choose conventional 20W-50 grades. Synthetics are forecast to expand at a 3.12% CAGR during the forecast period (2026-2031) as Euro 6 cars, combined-cycle turbines, and hydrogen compressors demand premium thermal stability. Semi-synthetics act as a bridge product, offering moderate oxidative stability at a manageable price point. Bio-based lubricants stay niche, but research from Alexandria University in August 2025 showed palm-oil glycerol greases improved friction by 40% when doped with carbon nanotubes, indicating long-term potential for renewable thickeners.

Misr Petroleum promotes cost-competitive mineral grades through its nationwide filling-station network, while multinationals highlight total-cost-of-ownership savings from synthetics that double service intervals. Regulatory moves such as the EOS viscosity-classification Standard 1418/2020 ensure transparent labelling and encourage gradual upgrading. As per-capita income rises and OEM mandates tighten, mineral-oil dominance will erode, but affordability considerations imply a multi-decade coexistence of base-stock classes within the Egypt Lubricants market.

Geography Analysis

Greater Cairo and the Nile Delta account for the largest share of Egypt Lubricants market size, supported by the densest vehicle parc, most factories, and the country’s busiest logistics arteries. Alexandria hosts the Borg El Arab and Amriya blending hubs that supply Upper Egypt and the Western Desert, while its port handles bulk base-oil imports under long-term supply contracts. Suez Canal corridor demand mirrors maritime traffic, gas-processing hubs, and free-zone manufacturing, though recent Red Sea security issues trimmed bunker oil and marine lubricant volumes.

Upper Egypt, anchored by the Beni Suef and Assiut power complexes, is the fastest-growing regional market as government investment extends transmission lines southward. Combined-cycle plants there consume synthetic turbine oils specified for 12-year service cycles, offering a high-margin aftermarket for global suppliers. The Western Desert’s upstream oil concessions and new onshore gas finds near Matruh create spot opportunities for drilling fluids and high-temperature compressor oils that must endure desert heat.

Sinai and the Red Sea coastal strip remain smaller in volume but strategic in specialty products for petrochemicals, phosphate mining and tourism transport fleets. As green-hydrogen projects cluster around Ain Sokhna, demand for cryogenic, food-grade and perfluoropolyether lubricants is expected to rise sharply after 2028. Taken together, regional diversity cushions the Egypt lubricants market against localized downturns and sustains an aggregate growth trajectory in line with national GDP expansion.

Competitive Landscape

The Egypt Lubricants market is moderately concentrated. Global majors, such as Shell, TotalEnergies, BP, Chevron, and ExxonMobil, compete alongside regional challengers ADNOC Distribution, ENOC, and Gulf Oil, and state-owned Misr Petroleum. Smaller independents carve niches in industrial greases and metal-working fluids, but escalating additive and packaging costs strain balance sheets.

Egypt Lubricants Industry Leaders

Exxon Mobil Corporation

TotalEnergies

Misr Petroleum

Shell plc

BP p.l.c.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Shell Lubricants Egypt unveiled an upgraded lubricants lineup, introducing products tailored to align with the 2025 API SQ standard. Highlighting the new range is Shell Helix Ultra, a product harnessing PurePlus Technology, a process that transforms natural gas into base oil with a purity of 99.5%.

- August 2025: Misr Petroleum reported 8.6 million tons of petroleum products and lubricant sales in FY 2024/25 and upgraded its Alexandria complex to boost exports into Africa and Arab markets.

Egypt Lubricants Market Report Scope

Lubricant products are made from a combination of base oils and additives. The composition of base oil in the formulation of lubricants is primarily between 75-90%. Base oils possess lubricating properties and make up to 90% of the final lubricant product.

The market is segmented by product type and end-user industry. By product type, the market is segmented by automotive engine oil, industrial engine oil, transmission fluids, gear oil, brake fluids, hydraulic fluids, greases, process oil (including rubber process oil and white oil), metalworking fluids, turbine oil, transformer oil, and other product types. By end-user industry, the market is segmented into automotive, marine, aerospace, heavy equipment, and industrial. For each segment, the market sizing and forecasts have been done on the basis of volume (liters).

By Product Type

| Automotive Engine Oil |

| Industrial Engine Oil |

| Transmission Fluids |

| Gear Oil |

| Brake Fluids |

| Hydraulic Fluids |

| Greases |

| Process Oil (Including Rubber Process Oil and White Oil) |

| Metalworking Fluids |

| Turbine Oil |

| Transformer Oil |

| Other Product Types |

By End-user Industry

| Automotive | Passenger Vehicles |

| Commercial Vehicles | |

| Two-Wheelers | |

| Marine | |

| Aerospace | |

| Heavy Equipment | Construction |

| Mining | |

| Agriculture | |

| Industrial | Power Generation |

| Metallurgy and Metalworking | |

| Textiles | |

| Oil and Gas | |

| Other End-Use Industries |

By Base Stock Type

| Mineral Oil-Based Lubricants |

| Synthetic Lubricants |

| Semi-Synthetic Lubricants |

| Bio-Based Lubricants |

| By Product Type | Automotive Engine Oil | |

| Industrial Engine Oil | ||

| Transmission Fluids | ||

| Gear Oil | ||

| Brake Fluids | ||

| Hydraulic Fluids | ||

| Greases | ||

| Process Oil (Including Rubber Process Oil and White Oil) | ||

| Metalworking Fluids | ||

| Turbine Oil | ||

| Transformer Oil | ||

| Other Product Types | ||

| By End-user Industry | Automotive | Passenger Vehicles |

| Commercial Vehicles | ||

| Two-Wheelers | ||

| Marine | ||

| Aerospace | ||

| Heavy Equipment | Construction | |

| Mining | ||

| Agriculture | ||

| Industrial | Power Generation | |

| Metallurgy and Metalworking | ||

| Textiles | ||

| Oil and Gas | ||

| Other End-Use Industries | ||

| By Base Stock Type | Mineral Oil-Based Lubricants | |

| Synthetic Lubricants | ||

| Semi-Synthetic Lubricants | ||

| Bio-Based Lubricants | ||

Key Questions Answered in the Report

What is the Egypt lubricants market size in 2026 and how fast is it growing?

It is expected to reach 637.08 million liters in 2026 and is forecast to expand at a 2.22% CAGR between 2026 and 2031.

Which product category is expanding the quickest?

Greases are projected to grow at a 4.93% CAGR through 2031 on the back of heavy-equipment demand.

Why are local blending plants gaining traction?

They help companies avoid exchange-rate volatility and import tariffs while meeting ISO-quality rules.

How will green-hydrogen projects influence lubricant demand?

Electrolyzers and hydrogen compressors need specialty synthetic lubricants resistant to hydrogen embrittlement, creating a new high-value niche after 2028.

What restrains faster adoption of premium synthetic oils?

Counterfeit products, currency-driven additive cost spikes and higher ACEA C3 formulation prices curb consumer uptake.

Page last updated on: