Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

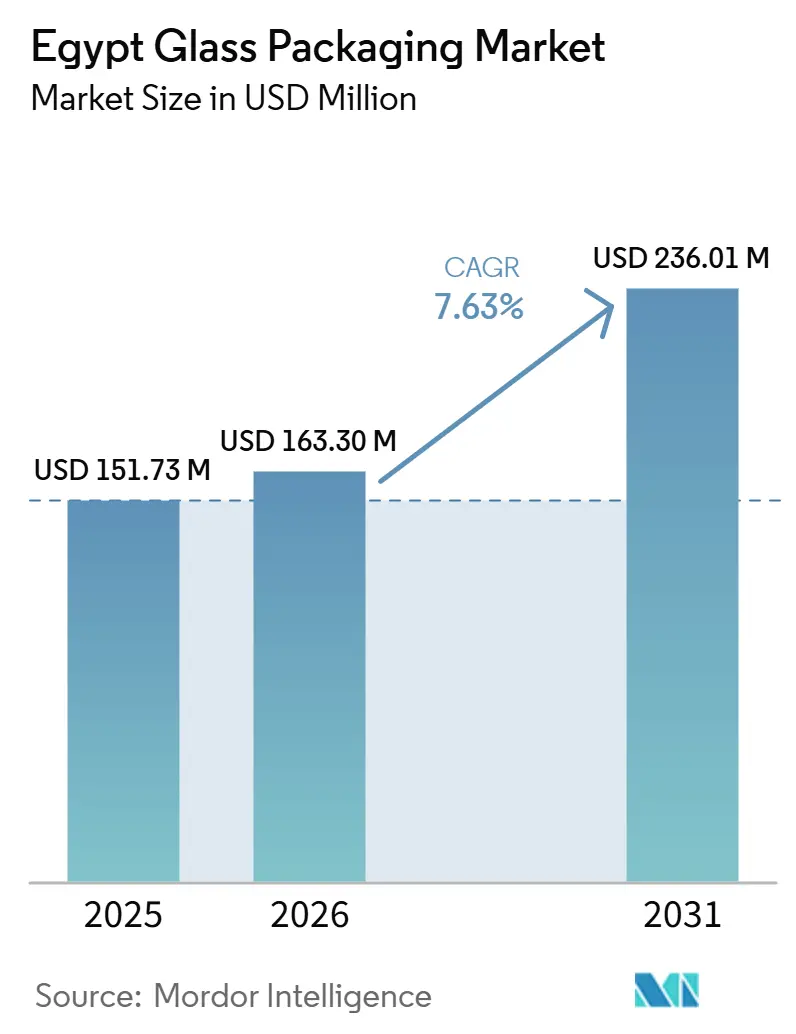

| Base Year Market Size (2025) | USD 151.73 Million |

| Market Size (2026) | USD 163.30 Million |

| Market Size (2031) | USD 236.01 Million |

| Growth Rate (2026 - 2031) | 7.63% CAGR |

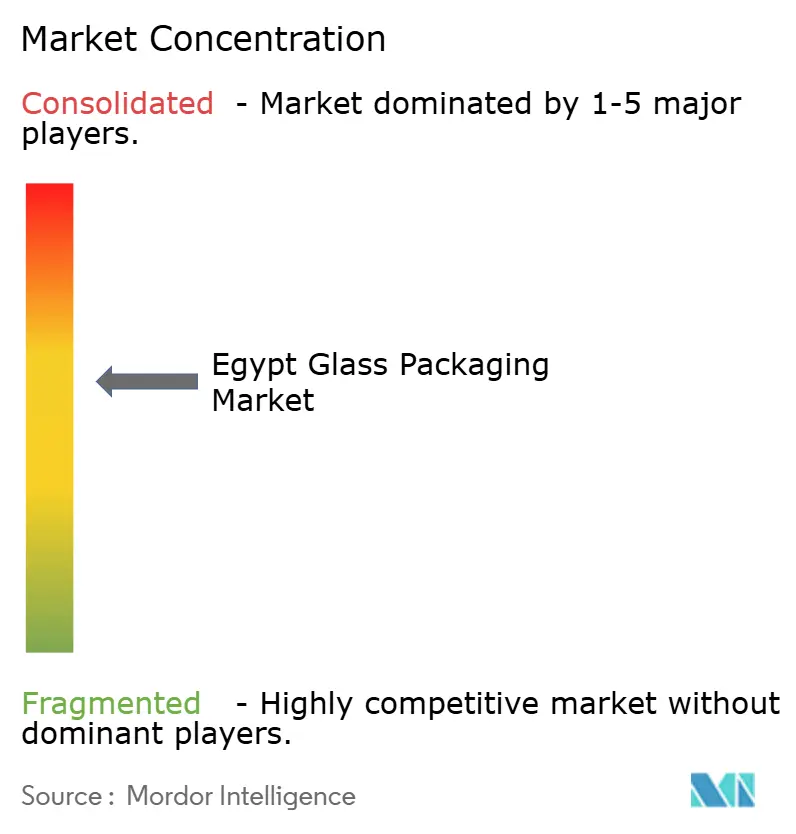

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Egypt Glass Packaging Market Analysis by Mordor Intelligence

The Egypt glass packaging market size is projected to be USD 151.73 million in 2025, USD 163.30 million in 2026, and reach USD 236.01 million by 2031, growing at a CAGR of 7.63% from 2026 to 2031. Continuous investment in new furnaces, cullet treatment, and lightweight-glass technology is raising domestic output and export capacity. Regulatory pressure on single-use plastic, incentives in the Suez Canal Economic Zone, and premiumization in beverages, cosmetics, and pharmaceuticals are widening the demand base. Producers are also insulating margins through in-house energy-efficiency programs and long-term soda-ash contracts, while foreign players exploit free-zone incentives to add incremental capacity. At the same time, the rapid adoption of recycled PET, aluminum, and carton packs forces container-glass makers to compete on design, weight reduction, and full-cycle recyclability to protect the Egyptian glass packaging market against substitution threats.

Key Report Takeaways

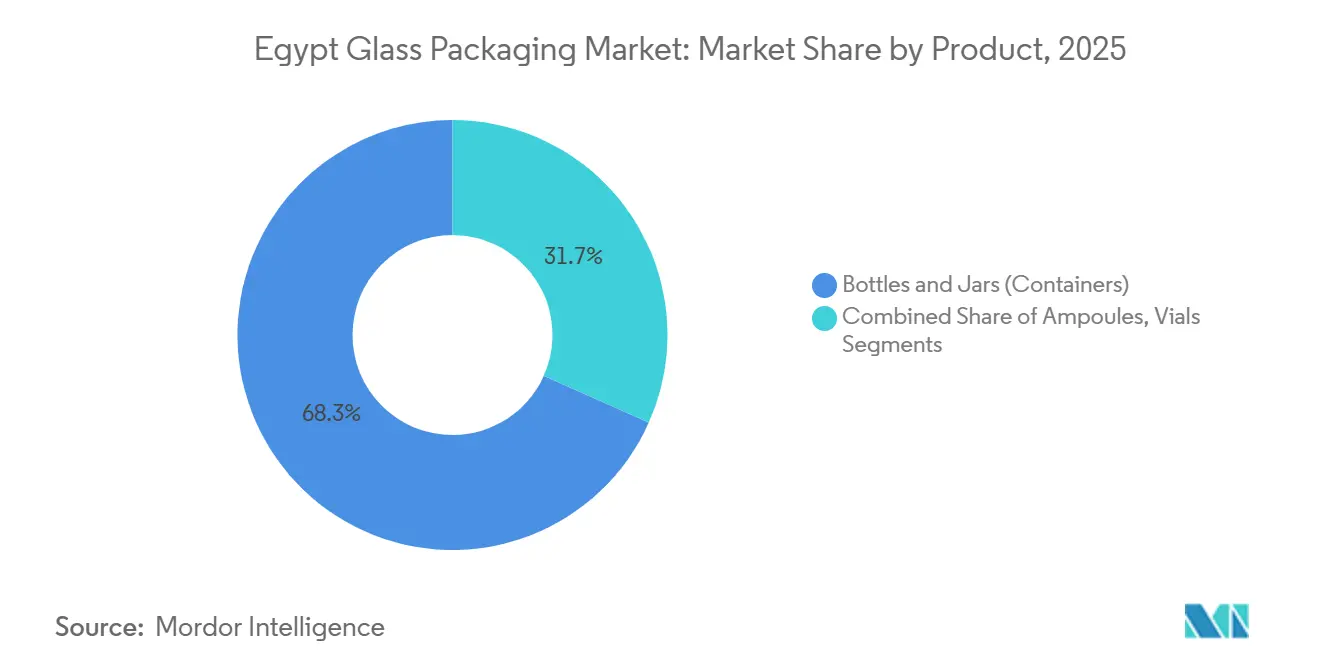

- By product, the bottles and jars segment captured 68.32% of Egypt glass packaging market share in 2025.

- By color, the Egypt glass packaging market size for amber glass is projected to expand at an 8.17% CAGR through 2031.

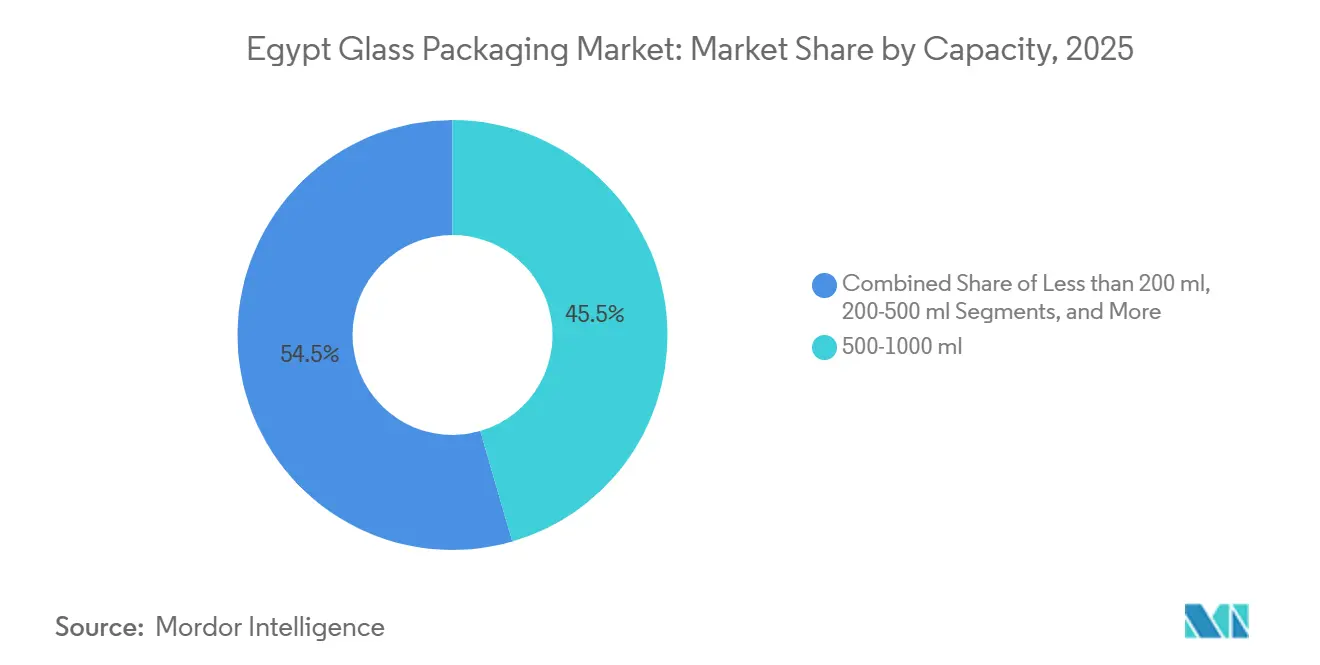

- By capacity, the 500-1,000 ml range captured 45.51% of Egypt glass packaging market share in 2025.

- By end-use industry, the Egypt glass packaging market for pharmaceuticals is poised to register the highest 7.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Egypt Glass Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Eco-Friendly Product Demand | +1.5% | National spillover to export markets in Europe and Gulf | Medium term (2-4 years) |

| Premiumization and Disposable Income Rise | +1.2% | National, concentrated in Greater Cairo and Alexandria | Medium term (2-4 years) |

| Pharmaceutical Manufacturing Boom | +2.0% | National, clusters in SC Zone and 10th of Ramadan City | Short term (≤ 2 years) |

| Suez Canal Economic Zone Export Incentives | +1.3% | Suez, Ain Sokhna, Ataqa Free Zone | Short term (≤ 2 years) |

| Upcoming EPR/DRS Legislation | +0.8% | National | Long term (≥ 4 years) |

| Craft Beverage and Artisanal Foods Surge | +0.6% | National, early adoption in urban centers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Eco-Friendly Product Demand

Egypt’s plan to lift the national recycling rate to 60% by 2027 is steering brands toward infinitely recyclable materials such as glass. The Egyptian Organization for Standardization embedded recyclability disclosure in 2025 packaging rules, tilting specification sheets toward container glass that can be remelted without quality loss. Food and cosmetics exporters gain a premium in European shelves because glass meets EU circular-economy criteria without complex multilayer testing. Middle East Glass, now the only Egyptian producer operating an industrial cullet-treatment line, reports lower batch costs and rising export orders under the new sustainability regime. Although a 2025 life-cycle study highlighted glass’s higher production emissions than Tetra Pak, policy weight is favoring full recyclability over single-trip carbon optimization, sustaining glass demand in the Egypt glass packaging market.

Pharmaceutical Manufacturing Boom

Government self-sufficiency targets have accelerated sterile injectable lines, and with them, demand for vials and ampoules. Ateco Pharma doubled intravenous-solution capacity at Ain Sokhna in Q1 2026 and plans to export 60% of new output, triggering long-term supply contracts for amber and flint vials. Arab Pharmaceutical Glass is adding a third furnace with a 150-tonnes-per-day pull to serve expanding vaccine and ophthalmic pipelines. Foreign capital is also entering: Linuo Glass of China took a 51% stake in European Ampoules Company in 2024, injecting process know-how and quality upgrades.[1]Lina Shen, “Linuo Glass to Acquire Stake in Egyptian Ampoules Firm,” linuo-glass.com The Egyptian glass packaging market, therefore, gains a high-margin niche that is shielded from substitution by PET and aluminum by strict sterility and light-protection rules.

Suez Canal Economic Zone Export Incentives

Custom-duty exemptions on production inputs and near-dock infrastructure make SCZone a springboard for container-glass exports. Middle East Glass already ships more than 50% of its output to 25 countries via Sokhna port, while Kandil Glass secured USD 26.7 million to build a new 100-tonne-per-day furnace in Ataqa Free Zone in February 2026. Chinese newcomers Xinmin Glass and Deli Glass Co have each committed USD 70 million to tableware plants with 80% export allocation, validating Egypt’s position as a regional glass hub.

Premiumization And Disposable Income Rise

Although inflation remains elevated, nominal household spending grew 21.5% in 2025, lifting demand for higher-end beverages, perfumes, and cosmetics that lean on flint and specialty-tinted glass. Disposable income is projected to climb to EGP 255,700 (USD 5,229) by 2028, shrinking the sub-USD 5,000 cohort and nurturing a consumer base willing to pay for premium packaging. Local converters exploit this trend by offering lightweight flint bottles that preserve product integrity and brand cachet without prohibitive logistics costs. Export-oriented cosmetic brands additionally specify frosted and colored flacons to signal luxury, driving value growth in the Egyptian glass packaging market. Producers that master cullet usage and energy efficiency can pass through less of the inflationary cost burden, retaining price-sensitive shoppers while serving premium tiers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Soda-Ash and Energy Prices | -1.8% | National, acute for furnace operations | Short term (≤ 2 years) |

| Plastic and Lightweight Metal Substitution | -1.2% | National, beverages and food segments | Medium term (2-4 years) |

| Energy-Subsidy Reform Inflating Costs | -0.9% | National | Short term (≤ 2 years) |

| Limited Cullet Collection Infrastructure | -0.5% | National, gaps in Upper Egypt and rural areas | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Volatile Soda-Ash and Energy Prices

Natural-gas tariffs for industrial users jumped 21% to USD 5.75 per million British thermal units in September 2025, lifting delivered costs above USD 6.00 when import fees are added. Diesel and fuel hikes followed in April 2025 as subsidies were trimmed under an IMF program. Soda-ash prices softened globally in 2025, yet freight and energy differentials leave Egyptian buyers exposed to 10-20% swings in landed costs. Together, these inputs account for roughly 60% of furnace cost, squeezing margins when export contracts are priced months in advance. Firms hedge by locking two-to-three-month raw-material inventories, retrofitting burners for oxy-fuel melting, and accelerating waste-heat recovery projects to stabilize operating cash flow within the Egypt glass packaging market.

Plastic and Lightweight Metal Substitution

Bariq lifted recycled-PET capacity to 55,000 tonnes per year in late 2024, supplying Coca-Cola, Pepsi, and Nestlé with bottle-grade rPET that carries roughly half the carbon footprint of flint glass and avoids breakage losses.[2]PETplanet Insider, “Bottle-to-Bottle Recycling in Egypt,” petpla.net Aluminum can lines and aseptic carton projects in the SC Zone intensify competition for mass-market juices and dairy drinks, where weight and logistics favor alternatives. For the Egypt glass packaging market to defend its share, container-glass players are adopting narrow-neck press-and-blow and hot-end coating to shave weight without sacrificing line speed or product protection. Brand owners still specify glass for pharmaceuticals, premium spirits, and aromatherapy oils, but retaining beverage contracts will depend on cost-neutral lightweight solutions and robust returnable-bottle cycles.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product: Containers Anchor Volume, Ampoules Drive Momentum

Bottles and jars formed the backbone of the Egyptian glass packaging market, capturing 68.32% share in 2025, driven by carbonated drinks, juices, and culinary oils. Their dominance stems from extensive compatibility with filling lines and consumer preference for refillable formats in horeca channels. Over the forecast horizon, steady growth in domestic beverage spending and seamless rail-port links at Sokhna port keep container-glass shipments expanding in line with overall market volume. Local converters also bundle design services, embossing, and UV coatings to deter imports and lift unit margins.

Ampoules, although representing a smaller absolute tonnage, are forecast to grow at 8.57% annually through 2031, outpacing every other product class. Government import-substitution mandates, combined with Gavi-aligned vaccine programs, are pushing local fill-finish firms to lock in amber ampoule supply. EIACO Factory already runs utilization above 80%, and Linuo’s entry signals further volume acceleration. As a result, the Egyptian glass packaging market share for high-value pharmaceutical products will continue to inch upward, raising the sector’s average price per tonne and strengthening profitability.

By Color: Flint Retains Lead, Amber Accelerates

Flint glass accounted for 58.63% of the Egyptian glass packaging market share in 2025 because beverage, condiment, and cosmetics brands rely on product visibility for shelf appeal. Producers refine sand sourced within 100 kilometers of Cairo and blend high-grade cullet to hit premium clarity, allowing local fills to meet export standards without importing bottles. The segment should maintain a solid but slower trajectory, cushioned by continuous drink consumption and the tourism rebound that lifts premium spirits demand.

Amber glass, protected from ultraviolet degradation, is projected to grow at an 8.17% CAGR driven by injectable drugs, syrups, and vitamin formulations. Arab Pharmaceutical Glass, United Glass Company, and new SC Zone entrants are collectively scaling amber capacity to safeguard supply security. In parallel, craft beer and specialty cold-brew brand owners, though niche, are opting for amber to signal authenticity, broadening the user base.

By Capacity: Mid-Range Dominates, Small Formats Surge

The 500-1,000 ml bracket held 45.51% of the Egyptian glass packaging market share in 2025, anchored by one-liter soft-drink bottles and 750-ml juice packs. Efficient case-per-pallet ratios and returnable-glass programs keep this range central to beverage logistics strategies. Capacity expansions at Middle East Glass and Kandil Glass include multiple IS machines dedicated to mid-range molds, allowing quick color changeovers and line flexibility.

Units below 200 ml are rising at a 8.25% CAGR, propelled by injectable medicine vials, single-serve cold brews, and travel-size perfumes. Export-oriented pharmaceutical fillers impose strict dimensional tolerances, prompting glassmakers to invest in electronic swabbing and in-line inspection for defect detection. As per capita medicine usage rises and e-commerce drives demand for sample-size cosmetics, this small-format niche will represent a growing slice of Egypt's glass packaging market by 2031.

By End-Use Industry: Beverages Rule, Pharma Accelerates

Beverage fillers consumed 58.63% of Egypt glass packaging market size in 2025, with non-alcoholic categories leading domestic volumes. Returnable glass compliance in horeca channels and premium brand positioning in retail sustain steady container turnover. The segment’s growth, however, faces aggressive competition from rPET and carton packs, pushing bottlers toward lightweight flint bottles and creative embossing to justify shelf footprint.

Pharmaceuticals are on track for the highest CAGR of 7.98%, lifted by new vial and ampoule lines aligned with Egypt Vision 2030 healthcare localization goals. Regulatory mandates for inert, light-stable packaging favor amber and Type I borosilicate glass, areas where local producers are scaling capacity. As new vaccine and biologics plants finish commissioning, pharmaceutical conversions will secure a larger share of the Egyptian glass packaging market, cushioning glassmakers against volatility in beverage demand.

Geography Analysis

Most furnaces cluster near Greater Cairo and Alexandria, but export-oriented sites in the Suez Canal Economic Zone (SCZone) are now accounting for a growing share of shipments in Egypt's glass packaging market. Middle East Glass uses the Sokhna gateway to dispatch more than half of its annual output of 385,000 tons to 25 international destinations. Kandil Glass’s planned 100-tonnes-per-day furnace in Ataqa Free Zone will tap an identical rail-port, reinforcing SC Zone’s role as an export corridor.[3]Amwal Al Ghad, “SCZone Breaks Ground on Xinmin Glass Factory,” amwalalghad.com

Domestic demand centers on Cairo’s 20-million-plus metropolitan population, Alexandria’s beverage bottling valley, and delta agro-processing hubs. Yet Upper Egypt is emerging; government-backed honey and jam clusters in Qena specify modern jar designs, seeding incremental orders for flint and frost-clear glass. Simultaneously, pharmaceutical clusters in 10th of Ramadan City and Borg El Arab integrate filling and secondary packaging operations, locking in steady call-offs from nearby vial and ampoule suppliers.

Internationally, Europe remains the prime destination for Egyptian food-jar exports because duty-free entry under the EU–Egypt Association Agreement, combined with strict recyclability mandates that favor glass, makes it the preferred destination. Gulf markets import Egyptian carbonated-soft-drink bottles and fragrance flacons, attracted by competitive freight rates compared with Turkey. Western and Eastern Asian buyers source pharmaceutical vials to diversify supply chains beyond China, adding resilience to the Egypt glass packaging market’s geographic mix.

Competitive Landscape

The competitive structure is moderately concentrated: the five largest producers control roughly 65% of Egypt's glass packaging market share. Middle East Glass tops the league with six furnaces and 17 lines after a capacity-doubling drive that shot 2025 net profit up 550% year on year to USD 22.6 million. Its majority owner, MENA Glass Holdings, now at a 93.7% stake, intends to build a fourth plant within five years, a move that would push annual production toward 500,000 tons.

Kandil Glass, operating two furnaces with a capacity of 420 tons per day, is adding a third furnace in 2026, financed by Banque du Caire.[4]Glass International, “Kandil Secures USD 26.7 Million Financing Agreement,” glass-international.com The new plant will serve both domestic fillers and export customers reachable through SC Zone’s ports, challenging Middle East Glass in color versatility and premium-bottle craftsmanship. Arab Pharmaceutical Glass, United Glass Company, and EIACO Factory specialize in pharmaceutical glass; together, they secure most of the injectable-grade supply through advanced inspection systems and ISO 15378 certification, which serves as a barrier to new entrants.

Xinmin Glass and Deli Glass Co will commission SC Zone tableware lines in 2026, benefiting from tax holidays and lower labor costs to undercut local players on commodity items. Meanwhile, technology differentiation intensifies: Middle East Glass runs the only full-scale cullet treatment plant, Kandil deploys SORG end-fired furnaces with dual regenerative burners, and Dr. Greiche is piloting 2.1-millimeter ultra-thin sheets that might later cascade into lightweight container production. Securing stable soda-ash supply and migrating to oxy-fuel melting will shape cost curves and dictate future Egypt glass packaging market standings.

Egypt Glass Packaging Industry Leaders

Middle East Glass Manufacturing Company S.A.E.

National Company for Glass and Crystal S.A.E.

United Glass Company (UGC)

Arab Pharmaceutical Glass Company

Kandil Glass S.A.E.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2026: Kandil Glass signed a USD 26.7 million financing deal with Banque du Caire to erect a 100-tonnes-per-day furnace in Ataqa Free Zone.

- February 2026: SC Zone inked a USD 175 million pact with Türkiye’s Eroğlu Global Holding for a carton-pack facility, heightening cross-material rivalry.

- December 2025: SCZone laid the foundation stone for Xinmin Glass’s USD 70 million tableware complex, which is set to create 3,000 jobs.

- April 2025: Dr. Greiche Group committed EGP 500 million (USD 10 million) to an automotive-glass campus, introducing 2.1-millimeter ultra-thin technology.

Egypt Glass Packaging Market Report Scope

The Egypt glass packaging market comprises the manufacturing, distribution, and utilization of high-purity glass containers, including bottles, jars, vials, and ampoules designed for the secure storage and transportation of diverse consumer and industrial goods.

The Egypt Glass Packaging Market Report is Segmented by Product (Bottles and Jars, Vials, and Ampoules), Color (Flint, Amber, Green, and Other Colors), Capacity (Less than 200 ml, 200-500 ml, 500-1000 ml, and More than 1000 ml), and End-use Industry (Beverages, Food, Cosmetics and Personal Care, Pharmaceuticals, and Perfumery). The Market Forecasts are Provided in Terms of Value (USD).

By Product

| Bottles and Jars (Containers) |

| Vials |

| Ampoules |

By Color

| Flint |

| Amber |

| Green |

| Other Colors |

By Capacity

| Less than 200 ml |

| 200-500 ml |

| 500-1000 ml |

| More than 1000 ml |

By End-use Industry

| Beverages | Alcoholic | Beer |

| Wine | ||

| Spirits | ||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | ||

| Non-Alcoholic | Juices | |

| Carbonated Drinks (CSDs) | ||

| Dairy Product-Based Drinks | ||

| Other Non-Alcoholic Beverages | ||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | ||

| Cosmetics and Personal Care | ||

| Pharmaceuticals | ||

| Perfumery | ||

| By Product | Bottles and Jars (Containers) | ||

| Vials | |||

| Ampoules | |||

| By Color | Flint | ||

| Amber | |||

| Green | |||

| Other Colors | |||

| By Capacity | Less than 200 ml | ||

| 200-500 ml | |||

| 500-1000 ml | |||

| More than 1000 ml | |||

| By End-use Industry | Beverages | Alcoholic | Beer |

| Wine | |||

| Spirits | |||

| Other Alcoholic Beverages (Cider and Other Fermented Drinks) | |||

| Non-Alcoholic | Juices | ||

| Carbonated Drinks (CSDs) | |||

| Dairy Product-Based Drinks | |||

| Other Non-Alcoholic Beverages | |||

| Food (Jam, Jelly, Marmalades, Honey, Sausages and Condiments, Oil, Pickles) | |||

| Cosmetics and Personal Care | |||

| Pharmaceuticals | |||

| Perfumery | |||

Key Questions Answered in the Report

What is the current value of the Egypt glass packaging market?

The market stood at USD 151.73 million in 2025 and is expected to reach USD 236.01 million by 2031.

Which product category is expanding fastest?

Pharmaceutical ampoules are forecast to grow at an 8.57% CAGR through 2031, outpacing other formats.

Why is amber glass demand rising?

Growth in injectable drugs and light-sensitive formulations is projected to drive a 8.17% CAGR for amber glass.

How do SC Zone incentives benefit glass producers?

Customs-duty exemptions and proximate port access cut logistics costs, enabling firms to export competitively.

What are the key cost headwinds for glassmakers?

Volatile soda-ash prices and higher natural-gas tariffs raise furnace operating expenses in the short term.

How are producers countering plastic substitution?

They are adopting lightweight press-and-blow technology, boosting cullet use, and promoting returnable-glass loops.

Page last updated on: