Egypt Diabetes Care Drugs And Devices Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

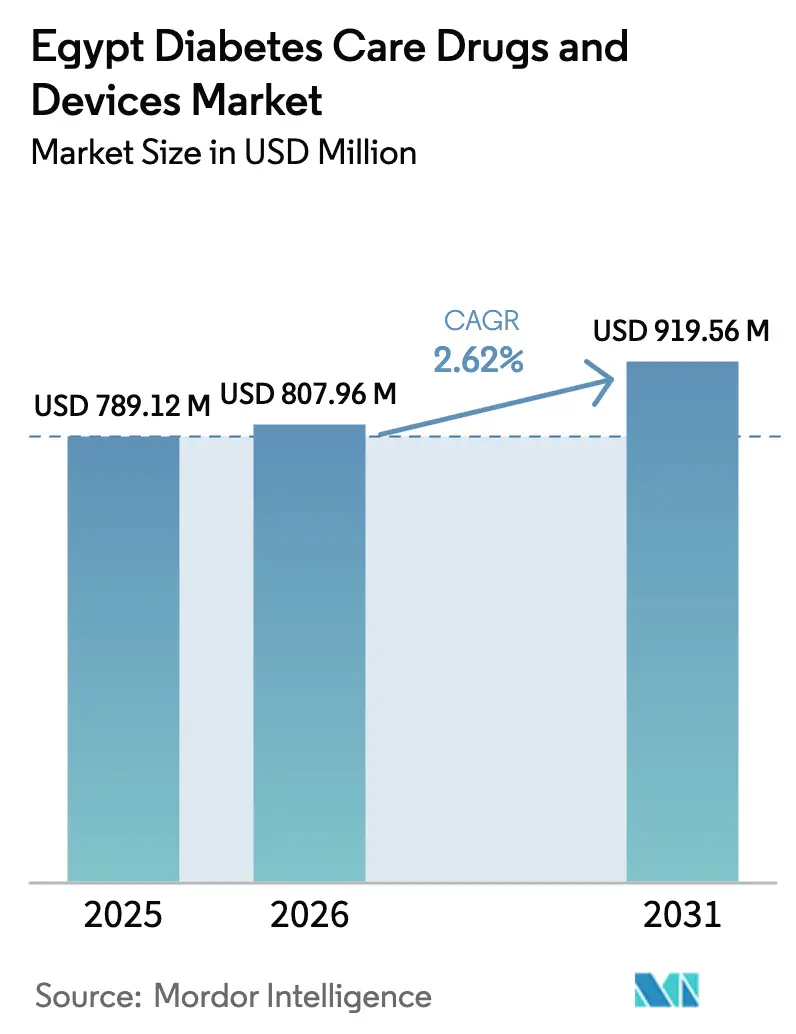

| Base Year Market Size (2025) | USD 789.12 Million |

| Market Size (2026) | USD 807.96 Million |

| Market Size (2031) | USD 919.56 Million |

| Growth Rate (2026 - 2031) | 2.62% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Egypt Diabetes Care Drugs And Devices Market Analysis by Mordor Intelligence

The Egypt Diabetes Care Drugs And Devices Market size is expected to grow from USD 789.12 million in 2025 to USD 807.96 million in 2026 and is forecast to reach USD 919.56 million by 2031 at 2.62% CAGR over 2026-2031.

Tight diagnostic gaps, currency volatility, and local‐manufacturing policies are reshaping supply chains and therapy choices. Sixty-two percent of the country’s 13.2 million adults with diabetes remain undiagnosed, and the national Universal Health Insurance System (UHIS) is turning that latent pool into treated patients through compulsory screening and electronic registries. Government-backed local insulin production, spearheaded by the Eva Pharma–Eli Lilly alliance, already offsets USD 30 million in annual imports and signals a move toward African Continental Free Trade Area (AfCFTA) exports. Continuous glucose monitoring (CGM) and smart insulin-delivery technologies are gaining traction in urban clinics as Abbott’s FreeStyle Libre 2 and Dexcom’s G7 reach price points below USD 50 per sensor. Simultaneously, FX-driven input-cost inflation and high out-of-pocket spending keep affordability at the center of every commercial strategy.

Key Report Takeaways

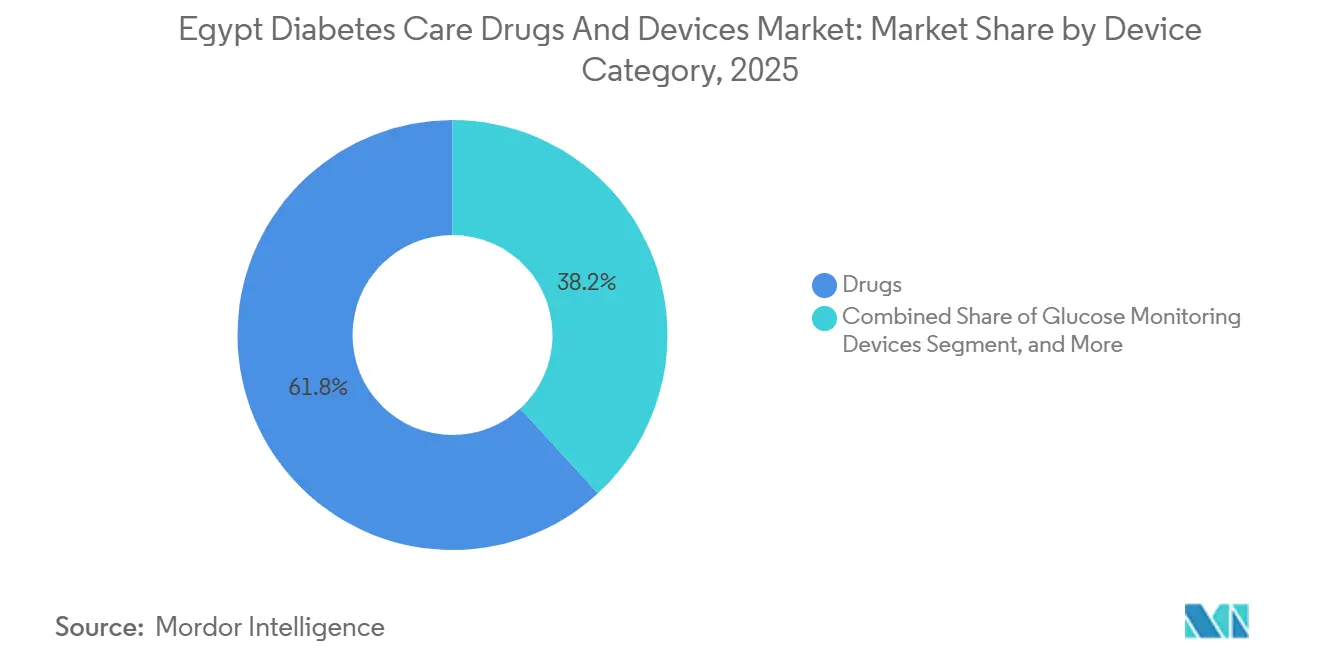

- By device category, drugs led with 61.83% of Egypt diabetes drugs and devices market share in 2025, while insulin-delivery devices are advancing at a 3.79% CAGR to 2031.

- By diabetes type, Type 2 accounted for 87.03% of revenue share in 2025, yet Type 1 is expanding at a 5.17% CAGR through 2031.

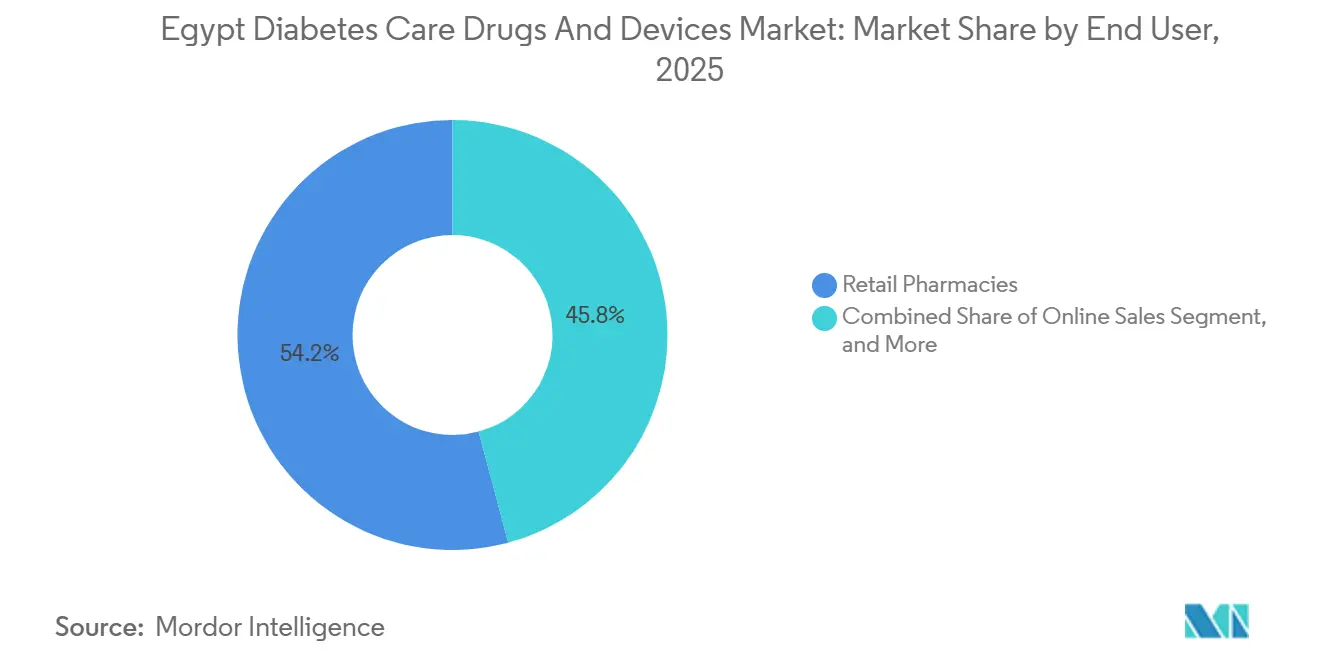

- By end user, retail pharmacies accounted for 54.18% of 2025 sales, whereas online channels are growing fastest, with a 6.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Egypt Diabetes Care Drugs And Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Diabetes Prevalence & Incidence | +0.8% | National, highest in Cairo, Alexandria, Giza | Long term (≥ 4 years) |

| Government UHIS Rollout & National Screening Drives | +0.6% | Nationwide, phased governorates | Medium term (2-4 years) |

| Local Insulin-Manufacturing Push Securing Supply | +0.5% | National, AfCFTA export potential | Medium term (2-4 years) |

| Accelerating Adoption of CGM & Smart Delivery Tech | +0.4% | Urban centers, spreading outward | Short term (≤ 2 years) |

| Expansion of Arabic-Language Telehealth | +0.3% | Urban and peri-urban | Short term (≤ 2 years) |

| Egypt Positioning as AfCFTA Insulin Hub | +0.2% | North and Sub-Saharan Africa | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Diabetes Prevalence & Incidence

Age-standardized prevalence reached 22.4% in 2024, equal to 13.2 million adults, yet 8.2 million remain undiagnosed.[1]International Diabetes Federation, “Egypt – IDF Diabetes Atlas,” idf.org Urban governorates screen more aggressively, leaving rural Upper Egypt lagging by up to 20 percentage points. Each newly diagnosed patient adds approximately USD 235 to annual drug and device spend, so UHIS expansion converts public health need into commercial volume. Diabetes expenditure hit USD 3.1 billion in 2024, underscoring budget pressure but also revealing scope for scale.

Government UHIS Rollout & National Screening Drives

UHIS, backed by EGP 166 billion (USD 5.4 billion), completed Phase 1 by 2024 and is now expanding into Upper Egypt, adding 8 million beneficiaries by 2028.[2]World Bank, “Egypt Health Sector Support,” worldbank.org Protocols require annual screening for adults over 40, creating a sustained funnel of newly diagnosed users for glucose meters, CGM sensors, and generic metformin. A USD 400 million World Bank loan earmarks one-third of the funds for non-communicable disease equipment, accelerating procurement cycles.

Local Insulin-Manufacturing Push Securing Supply

Eva Pharma produced Egypt’s first locally manufactured insulin batch in December 2024 and targets a capacity of 100 million vials by 2027. The factory already saved USD 30 million in import bills during its first year and shielded the supply chain when Denmark-based disruptions hit global insulin output in 2023. A new USD 500 million active pharmaceutical ingredient (API) zone in the Suez Canal Economic Zone aims to reduce import dependence by 70%.

Accelerating Adoption of CGM & Smart Insulin Delivery Tech

CGM penetration climbed to about 35,000 users in 2025, up from 12,000 in 2022.[3]Abbott Diabetes Care, “FreeStyle Libre – Egypt,” freestyle.abbott FreeStyle Libre 2 sensors cost EGP 1,200-1,500 (USD 39-49) and are now covered by limited UHIS and private-insurance plans. A 2025 local study showed that CGM users cut HbA1c by 1.2 percentage points over 6 months. Smart insulin pens that capture dosing data hold under 5% penetration but grow in private clinics that practice data-driven titration.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Out-of-Pocket Costs & Limited Reimbursement | -0.5% | Nationwide, hardest on rural poor | Medium term (2-4 years) |

| FX-Driven Input-Cost Inflation | -0.4% | National importers | Short term (≤ 2 years) |

| Counterfeit / Sub-Standard Medicines | -0.2% | Rural areas at 8% prevalence | Long term (≥ 4 years) |

| Urban-Rural Infrastructure Gap | -0.3% | Upper Egypt, Sinai | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Out-of-Pocket Costs & Limited Device Reimbursement

Out-of-pocket spending reached 60% of total health expenditure in 2024. A FreeStyle Libre sensor costs 3.2 days of wages for the lowest-paid worker, versus 0.5 days for a month of metformin. UHIS covers essential medicines but excludes CGM and GLP-1 drugs, creating a two-tier system in which low-income patients rely on generics and basic meters.

FX-Driven Input-Cost Inflation for Imported Components

The Egyptian pound lost 50% against the USD between 2022 and 2024, raising landed costs for biosensors, LCDs, and API by up to 40% in EGP terms. Central-bank FX rationing slowed device imports by six weeks during 2024, forcing distributors to carry higher inventory and eroding margins. Local API capacity will ease pressure only after 2028.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Device Category: Drug Dominance with Delivery Acceleration

Drugs generated 61.83% of Egypt diabetes drugs and devices market revenue in 2025, and insulin alone contributed nearly half of that value. Within drugs, basal analogs such as glargine and degludec outsell NPH in urban centers, yet low-cost NPH still anchors rural formularies. Oral agents continue to treat the Type 2 majority, though SGLT-2 and GLP-1 uptake stays low because of cost and prescriber habits. Insulin-delivery devices represent the fastest-growing segment, with a 3.79% CAGR, moving users from vial-and-syringe to smart pens that store dose data. CGM shipments grow from a low installed base, while commodity lancets and strips support daily adherence. ISO 15197 compliance keeps no-name meters out, consolidating share with Roche, Abbott, and Sinocare.

Drugs will keep the lion’s share in the Egypt diabetes drugs and devices market through 2031 because every Type 1 and one-third of Type 2 patients depend on insulin. Yet value migrates toward delivery hardware as local pen fills drive down prices and as hospital tenders start to bundle drug+device. Meanwhile, insulin biosimilars push average insulin price per vial down, but higher treated volumes offset margin contraction.

By Diabetes Type: Type 2 Scale, Type 1 Velocity

Type 2 accounted for 87.03% of 2025 sales and will stay above 85% through 2031, reflecting demographic weight and lifestyle risk factors. However, Type 1 shows a 5.17% CAGR, driven by pediatric screening and improved survival. The Egypt diabetes drugs and devices market share for Type 1 is small yet revenue-rich because CGM, smart pens, and pump candidates cluster here. Novo Nordisk’s Changing Diabetes in Children will extend free insulin and meters to help establish adherence habits early.

Clinicians are moving eligible Type 2 patients toward SGLT-2 inhibitors and GLP-1 drugs that reduce cardiovascular-renal events, but uptake of 20% and 3%, respectively, reveals room for growth. As affordability barriers ease, guideline-driven polytherapy will lift per-capita spend. The Egyptian diabetes drugs and devices industry also sees growing gestational diabetes screening; each identified case draws short-term insulin therapy and postpartum meters.

By End User: Retail Strength, Online Momentum

Retail pharmacies held 54.18% of the Egypt diabetes drugs and devices market in 2025, driven by a dense 60,000-store network and the cultural habit of pharmacist counseling. Chains like Seif and Ezaby use loyalty apps and same-day delivery to retain urban shoppers. Online channels grew at a 6.05% CAGR and already account for one-quarter of urban sales. Chefaa’s subscription model offers 15% medication discounts, while Yodawy integrates e-prescriptions from Vezeeta’s telehealth visits.

Hospital pharmacies accounted for roughly one-third of spending, relying on bulk tenders that emphasize generic insulin and basic glucose meters. UHIS's capitation rules push hospitals to biosimilars and cost-controlled devices. Other end users, such as workplace clinics and NGO centers, fill rural gaps but carry small volumes. The Egypt diabetes drugs and devices market size flowing through online channels is slated to nearly double between 2026 and 2031 as smartphone penetration climbs above 80% and last-mile courier costs fall.

Geography Analysis

Cairo alone accounts for 40% of drug and device sales because it hosts most endocrinologists, private hospitals, and chain pharmacies. UHIS Phase 1 already covered Port Said, Luxor, and other governorates, setting the stage for growth in secondary cities. Moving into Aswan, Qena, and Sohag will unlock large pools of undiagnosed patients whose treatment begins with low-cost metformin and progresses to insulin and CGM as infrastructure matures.

Cold-chain gaps, summer heat above 40 °C, and long travel distances restrain device penetration in the near term, yet government grants for solar-powered refrigerators promise gradual improvement.

The Sinai Peninsula and Red Sea governorates contribute less than 5% of revenue due to sparse populations, but they host medical tourism pockets where expatriates demand premium CGM and pumps. International corridors matter too. With AfCFTA, Egypt positions itself as an export hub: Eva Pharma’s planned 100 million-vial insulin capacity can satisfy part of Nigeria, Kenya, and South Africa demand by shipping through Suez ports with favorable tariffs.

Competitive Landscape

Multinationals Novo Nordisk, Sanofi, and Eli Lilly jointly account for significant sales of insulin and branded oral drugs, while regional and local producers split the rest. Novo Nordisk’s USD 3-per-vial Access to Insulin Commitment sets price ceilings and forces local firms to match or beat that level. Sanofi defends its basal insulin share with Lantus and Toujeo, but now faces three biosimilar glargines priced up to 40% lower. Eli Lilly gains leverage through its production pact with Eva Pharma, securing local supply and export optionality.

Eva Pharma exemplifies the rise of local champions. It already reduced the national insulin import bill by USD 30 million in 2025 and is preparing for sub-Saharan expansion. Sinocare supplies low-cost meters that meet ISO accuracy, capturing rural and price-sensitive niches. Digital-health players Vezeeta, Cura, and Altibbi create service ecosystems linking teleconsults, e-prescriptions, and pharmacy fulfillment, making them potential acquisition targets for device makers.

Technology is the clearest differentiator. Abbott’s FreeStyle Libre 2 and Dexcom’s G7 deliver real-time data that reduces hypoglycemia events by up to 50%. Medtronic’s next-generation closed-loop system is still absent in Egypt but could enter via private clinics once reimbursement is introduced. Local manufacturers watch margin pressure but gain resilience by sourcing APIs domestically once the Suez Canal Economic Zone hub goes live.

Egypt Diabetes Care Drugs And Devices Industry Leaders

Roche

Omnipod

Medtronic

Sanofi S.A.

Novo Nordisk A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2024: Eli Lilly, in partnership with Eva Pharma, received approval from the Egyptian Drug Authority for locally manufactured insulin glargine. The collaboration, launched in 2022, aims to provide affordable insulin to at least 1 million people annually in low- to middle-income countries, with a strong focus on Africa.

- September 2024: Biocon partnered with Tabuk to launch GLP-1 products in the Middle East, targeting diabetes management and weight control across select nations in the region.

Egypt Diabetes Care Drugs And Devices Market Report Scope

Patients with type 1 diabetes must be given insulin because their pancreas cannot produce it. To control blood sugar levels, insulin must be given several times daily, such as before meals or with meals. Many people with type 2 diabetes also need to take antidiabetic drugs. These drugs include diabetes medications and insulin injections.

The Egypt Diabetes Drugs and Devices Market Report is Segmented by Device Category (Drugs [Insulin, Oral Anti-Diabetic Drugs, Adjunctive Therapies], Glucose Monitoring Devices [SMBG, CGM], Insulin Delivery Devices, Other Devices), Diabetes Type (Type 1, Type 2, Gestational & Others), End User (Hospital Pharmacies, Retail Pharmacies, Online Sales, Other End Users), and Geography (Egypt). Market Forecasts are Provided in Value (USD) and Volume (Units).

| Drugs | Insulin |

| Oral Anti-Diabetic Drugs | |

| Adjunctive Therapies | |

| Glucose Monitoring Devices | Self-Monitoring Blood Glucose (SMBG) Devices |

| Continuous Glucose Monitoring (CGM) Devices | |

| Insulin Delivery Devices | |

| Other Diabetes-Care Devices |

| Type 1 Diabetes |

| Type 2 Diabetes |

| Gestational & Others |

| Hospital Pharmacies |

| Retail Pharmacies |

| Online Sales |

| Other End Users |

| By Device Category | Drugs | Insulin |

| Oral Anti-Diabetic Drugs | ||

| Adjunctive Therapies | ||

| Glucose Monitoring Devices | Self-Monitoring Blood Glucose (SMBG) Devices | |

| Continuous Glucose Monitoring (CGM) Devices | ||

| Insulin Delivery Devices | ||

| Other Diabetes-Care Devices | ||

| By Diabetes Type | Type 1 Diabetes | |

| Type 2 Diabetes | ||

| Gestational & Others | ||

| By End User | Hospital Pharmacies | |

| Retail Pharmacies | ||

| Online Sales | ||

| Other End Users | ||

Key Questions Answered in the Report

What is the forecast value of Egypt’s diabetes drugs and devices market by 2031?

The market is expected to reach USD 0.92 billion by 2031.

How fast is the insulin-delivery device segment growing?

Insulin-delivery devices are advancing at a 3.79% CAGR between 2026 and 2031.

Which channel grows quickest for diabetes products?

Online pharmacies such as Chefaa and Yodawy are expanding at a 6.05% CAGR.

Why is local insulin production important?

It offsets import costs, secures supply during FX swings, and positions Egypt as an AfCFTA export hub.

Page last updated on: