Edge Computing Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

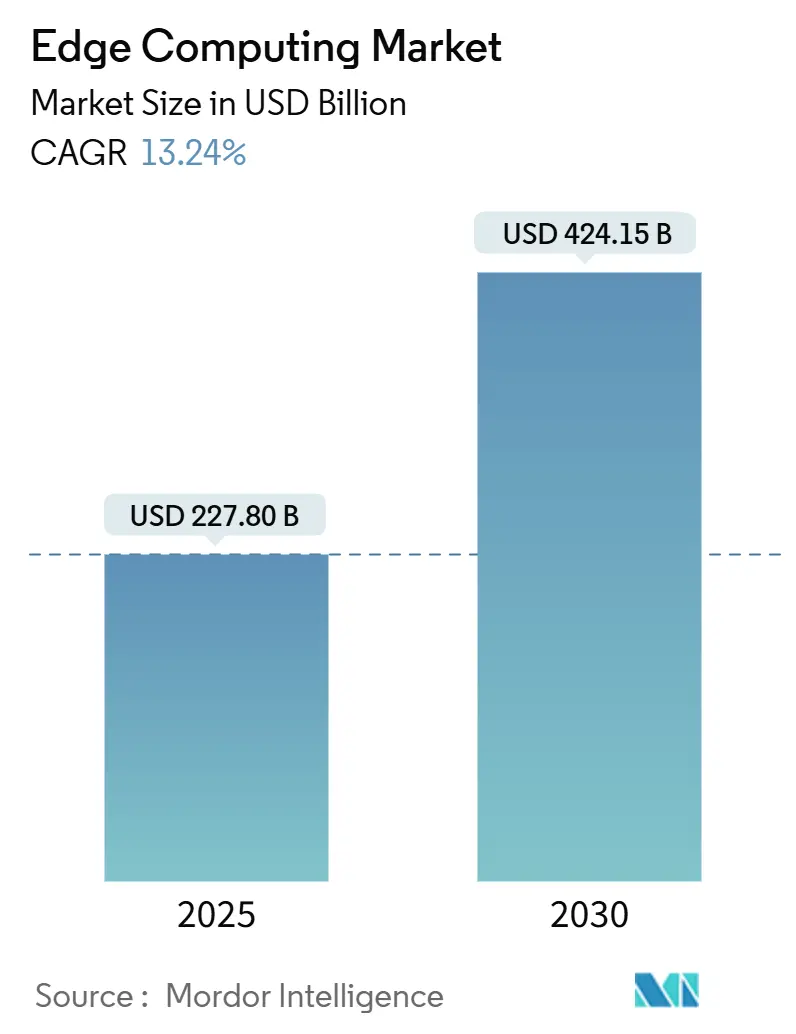

| Market Size (2025) | USD 227.80 Billion |

| Market Size (2030) | USD 424.15 Billion |

| Growth Rate (2025 - 2030) | 13.24% CAGR |

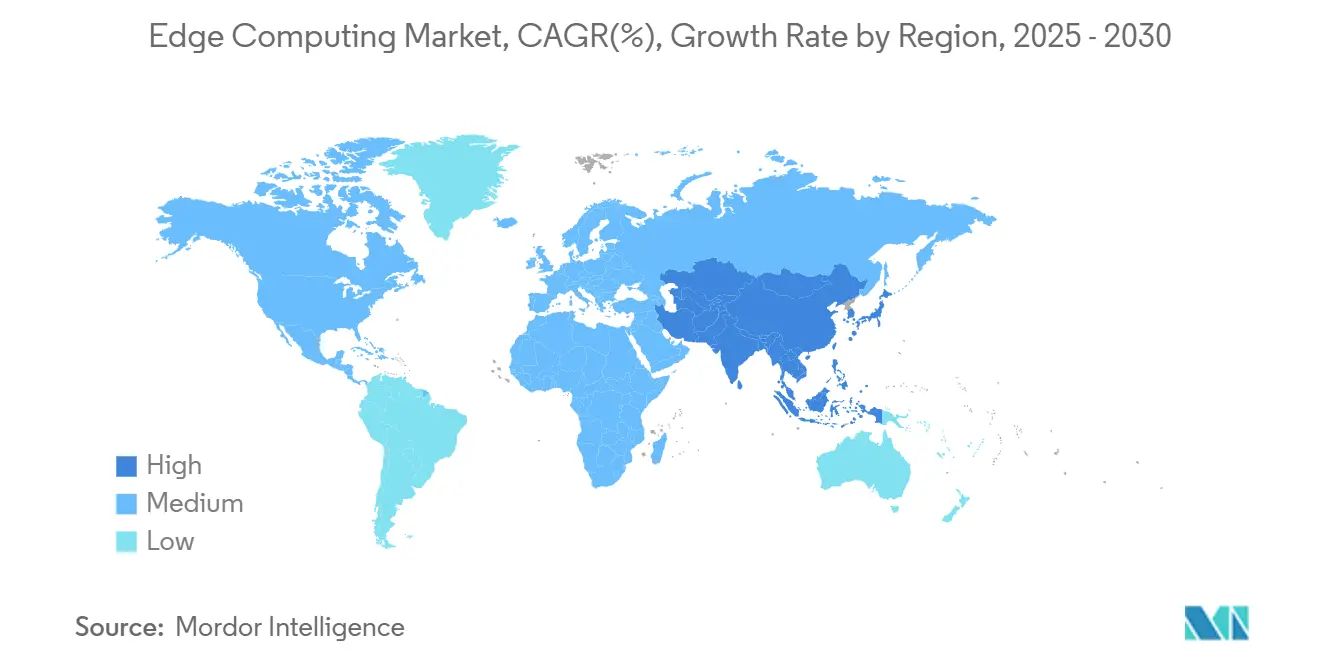

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

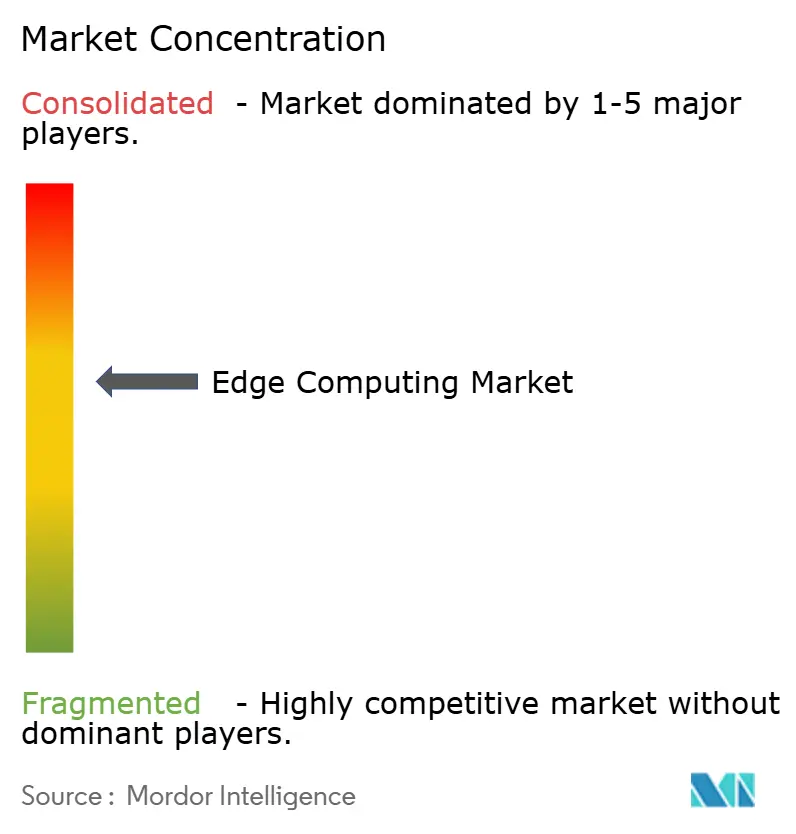

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Edge Computing Market Analysis by Mordor Intelligence

The edge computing market size is estimated at USD 227.80 billion in 2025 and is on track to reach USD 424.15 billion by 2030, advancing at a 13.24% CAGR. Intensifying data-gravity at the network edge, the roll-out of 5G radio access networks, and global data-sovereignty mandates are redefining enterprise architecture by shifting time-sensitive processing away from centralized clouds. Hardware vendors benefit from falling ASIC and SoC prices that lower entry barriers for real-time AI inference, while telecom operators carve new revenue streams through multi-access edge compute (MEC) services aligned with ETSI Phase 4 specifications. Enterprises in manufacturing, energy, and mobility adopt edge nodes to minimize latency, protect sensitive data, and improve operational resilience. At the same time, cloud hyperscalers extend managed services to customer premises, enabling unified observability and lifecycle management of distributed workloads

Key Report Takeaways

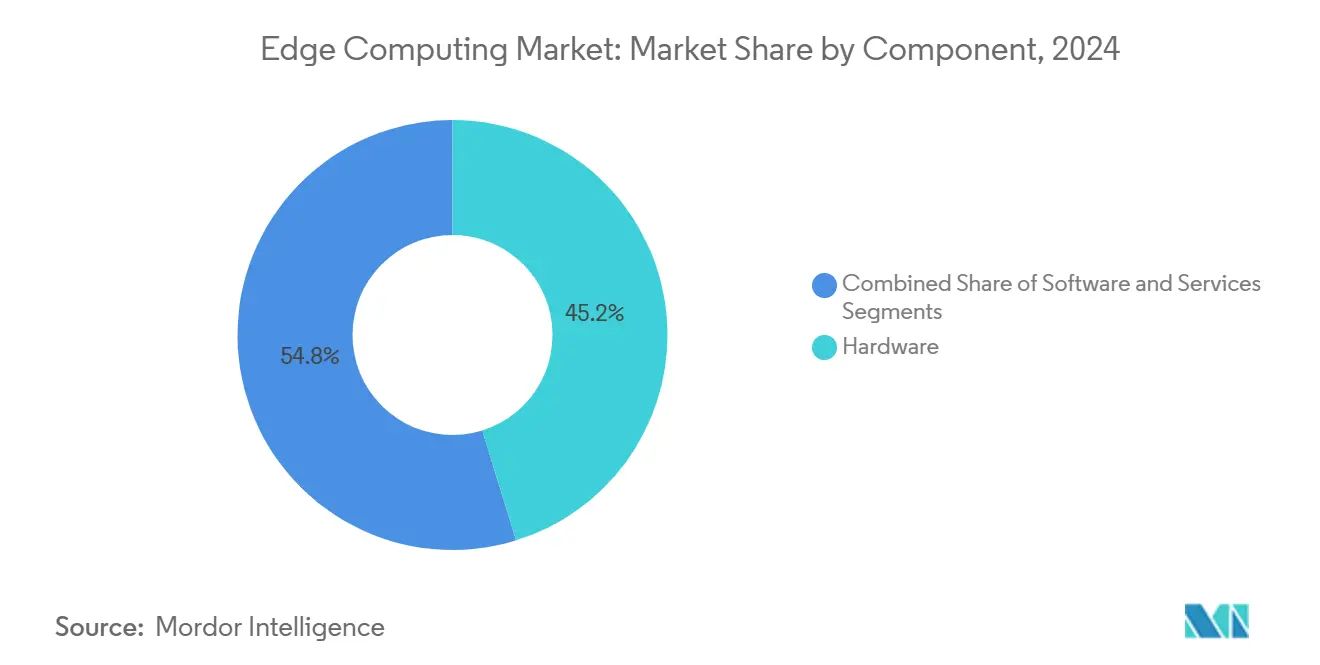

- By component, hardware held 45.2% of the edge computing market share in 2024, whereas software is poised for the fastest 13.7% CAGR through 2030.

- By deployment mode, on-premises solutions commanded 67.2% of the edge computing market in 2024, while cloud-integrated edges are forecast to expand at 14.9% CAGR to 2030.

- By end-user industry, manufacturing led with 18.6% revenue share in 2024; banking and finance are projected to post a 14.3% CAGR through 2030.

- By application, industrial IoT accounted for a 33.3% share of the edge computing market size in 2024, and autonomous systems are advancing at a 15.5% CAGR to 2030.

- By organisation size, large enterprises represented 53.0% of deployments in 2024, whereas SMEs will grow at 14.7% CAGR through 2030.

- By geography, North America led with 24.8% share in 2024; Asia Pacific is projected to accelerate at a 15.1% CAGR to 2030.

Global Edge Computing Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G roll-out catalysing ultra-low-latency use-cases | +2.8% | Global, early gains in North America, Europe, Asia Pacific | Medium term (2-4 years) |

| Proliferation of IoT endpoints and data gravity | +3.1% | Global, concentrated in APAC and North American manufacturing hubs | Long term (≥ 4 years) |

| Regulatory data-sovereignty mandates | +1.9% | Europe, expanding to APAC and selective North American sectors | Short term (≤ 2 years) |

| Declining ASIC/SoC costs for edge inference | +2.2% | Global, with supply-chain concentration in Taiwan and South Korea | Medium term (2-4 years) |

Source: Mordor Intelligence

5G Roll-out Catalyzing Ultra-Low-Latency Use-Cases

Global 5G deployments enable sub-millisecond latency that autonomous vehicles, telesurgery, and immersive maintenance applications require. Verizon and NVIDIA have begun piloting real-time AI services on private 5G networks, anchoring edge nodes at base stations to meet stringent round-trip delay budgets. Hyperscalers now colocate micro-data-centres at telecom exchanges, allowing developers to push containers closer to users. ETSI MEC Phase 4 profiles create common APIs, helping operators monetize differentiated latency tiers while ensuring workload portabilit.[1]European Telecommunications Standards Institute, “ETSI MEC Phase 4 Framework,” etsi.orgThe investment cycle aligns with governments funding rural 5G coverage, extending edge-powered services beyond dense urban corridors.

Proliferation of IoT Endpoints and Data Gravity

Industrial sites deploy thousands of sensors that stream terabytes daily, making centralized analytics both costly and sluggish. Manufacturers report 89% intent to shift AI inference to local gateways for real-time quality control.[2]Intel, “Edge-Ready Platforms and 18A Process Update,” intel.com Edge-native architectures cut bandwidth expenses and avoid cloud egress charges by keeping high-volume data onsite until summarized. Platforms such as TCS Clever Energy use local inference to flag anomalies and trigger immediate corrective action. As IoT devices integrate lightweight GPUs and NPUs, they can execute vision models autonomously, freeing backhaul links for supervisory tasks.

Regulatory Data-Sovereignty Mandates

The EU Data Act, China’s Cybersecurity Law, and India’s emerging data-protection frameworks compel enterprises to process sensitive workloads within national borders. Healthcare providers in Germany route patient telemetry to hospital-campus edge clusters to comply with GDPR while maintaining real-time monitoring.[3]Advantech, “Predictive Maintenance and Vision Inspection Success Stories,” advantech.com Similar sector-specific rules in finance and public safety accelerate adoption of compliant, on-premises micro-data-centres. Vendors that embed audit trails and geo-fencing at the kernel level gain a competitive edge as audit regulators tighten enforcement.

Declining ASIC/SoC Costs for Edge Inference Accelerators

High-volume 4 nm production and chiplet packaging lower per-TOPS cost, allowing mid-market firms to embed dedicated AI processors in kiosks, robots, and traffic cameras. Samsung and Groq target autonomous-vehicle suppliers with power-efficient NPUs, while Huawei’s Ascend 910C shows 60% of H100 performance at materially lower cost. RISC-V designs let OEMs tailor instruction sets, saving 17% power relative to legacy cores, enabling fanless enclosures in harsh field conditions. Cost deflation translates into broader deployment across retail analytics and smart buildings, where margins remain tight.

Restraints Impact Analysis

| Restraint | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cyber-attack surface expansion at distributed nodes | -1.80% | Global, with heightened concerns in critical infrastructure sectors | Short term (≤ 2 years) |

| Skills gap in deploying and managing heterogeneous edge stacks | -2.10% | Global, particularly acute in emerging markets and mid-market enterprises | Medium term (2-4 years) |

| Inter-operability and standards fragmentation (MEC, Open-RAN, LF Edge) | -1.30% | Global, with regional variations in standards adoption | Medium term (2-4 years) |

| Inefficient ROI for brown-field industrial retro-fits | -1.60% | Manufacturing-heavy regions in APAC, Europe, and North America | Long term (≥ 4 years) |

Source: Mordor Intelligence

Cyber-Attack Surface Expansion at Distributed Nodes

Every gateway, sensor, and micro-data-centre becomes a potential ingress point, raising the probability of lateral movement across converged IT/OT networks. Industrial operators deploy zero-trust firmware, hardware root-of-trust, and TPM-backed attestation, yet retrofitted legacy devices often lack secure boot sequences. Physical tampering risk climbs as edge nodes leave protected data-centre premises and reside on factory floors or in roadside cabinets. The scarcity of real-time forensics tools that run locally hampers incident response, extending mean-time-to-contain breaches.

Skills Gap in Deploying and Managing Heterogeneous Edge Stacks

Edge solutions mix routers, gateways, accelerators, and orchestration layers from multiple vendors, each with distinct lifecycle tools. Mid-sized manufacturers struggle to integrate Kubernetes variants, proprietary device OSs, and time-sensitive networking. Training programs lag behind technology cadence, leaving 83% of executives citing security and operations expertise as a deployment bottleneck. As a stop-gap, enterprises rely on managed-service contracts that inflate operating expenditure and can dilute the cost benefits of local processing.

Segment Analysis

By Component: Hardware Dominance Drives Infrastructure Buildout

Hardware accounted for 45.2% of the edge computing market in 2024, reflecting the up-front capital required for ruggedized servers, accelerators, and field-deployable storage. The edge computing market size for hardware reached USD 102.8 billion in 2025 and is expected to grow steadily as ASIC prices fall. Software platforms trail in revenue but lead in innovation, posting the highest 13.7% CAGR as orchestration stacks add AI model lifecycle management and remote observability. Services revenue remains modest yet essential, addressing integration of legacy PLCs and real-time operating systems within brownfield industrial sites.

Intense competition among chipmakers compresses unit costs, enabling high-volume deployment of low-power AI inference cards that withstand industrial temperature ranges. Intel’s 18A roadmap improves transceiver density, boosting deterministic throughput in intelligent gateways. Simultaneously, zero-touch deployment frameworks from Advantech and Namla lower integration costs by automating node provisioning, signalling future growth for managed services that wrap around hardware.

Note: Segment shares of all individual segments available upon report purchase

By Deployment Mode: On-Premises Leads Despite Cloud Integration Momentum

On-premises solutions retained 67.2% of the edge computing market in 2024, driven by data locality and deterministic latency requirements. Hybrid-cloud edges grow rapidly at 14.9% CAGR as enterprises adopt central model training in hyperscale clouds with distributed inference at factory cells. Enterprises pilot workload tiering, where real-time inference runs locally, and non-urgent analytics backhaul to regional availability zones overnight.

Air-gapped cruise-ship payment systems illustrate on-premises resilience, continuing operation when satellite links fail. Conversely, Microsoft’s investment in Armada reflects hyperscaler conviction that unified control planes spanning cloud and edge will win long term. Vendors now ship appliances pre-registered with cloud consoles, enabling frictionless expansion from single-site POCs to multi-country estates

By End-User Industry: Manufacturing Pioneers While Finance Accelerates

Manufacturing captured 18.6% of the edge computing market in 2024, leveraging predictive maintenance to cut downtime and real-time vision inspection to uphold Six Sigma quality. Banking and finance, though smaller today, will expand at 14.3% CAGR as fraud analytics and algorithmic trading migrate to branch-level or colocation edges to shave milliseconds and comply with residency laws. Healthcare, retail, and telecom sectors provide diverse demand, from HIPAA-compliant patient telemetry to in-store personalization.

Edge gateways integrate SCADA, MQTT, and OPC UA, giving plant managers a unified data lake without traversing corporate firewalls. In finance, payment processors deploy trusted execution environments on branch servers to block man-in-the-middle attacks. Healthcare providers use DICOM-enabled edge devices that run inference on CT images, shortening diagnosis cycles from hours to minutes

Note: Segment shares of all individual segments available upon report purchase

By Application: Industrial IoT Dominates While Autonomous Systems Surge

Industrial IoT constituted 33.3% of the edge computing market size in 2024, validating the ROI of condition-based maintenance and throughput optimization. Autonomous vehicles and drones represent the highest 15.5% CAGR, as makers of level-4 roboshuttles push perception and planning models to vehicle-mounted accelerators. Surveillance analytics gain from edge cameras processing feeds locally, avoiding cloud egress costs and reducing privacy exposure.

Factories embed AI in programmable logic controllers to flag vibration anomalies before catastrophic failure, cutting unscheduled downtime by 20% Automotive Edge Computing Consortium pilots show hybrid architectures, with vehicle data pre-filtered at roadside units before off-loading aggregated insights to regional cloudlets. Meanwhile, smart-city authorities deploy micro-data-centres in lampposts that run computer vision to optimize traffic lights in real time

By Organisation Size: Enterprise Leadership With SME Acceleration

Large enterprises owned 53.0% of deployments in 2024, benefiting from scale economies and in-house DevSecOps. The fastest growth, however, comes from SMEs at 14.7% CAGR, enabled by managed edge-as-a-service offers that bundle hardware, connectivity, and lifecycle management into predictable OPEX. Simple, fanless gateways running containerized stacks allow small retailers to deploy inventory analytics without dedicated IT staff.

Enterprises roll out global templates across dozens of factories, enforcing consistent security baselines using GitOps pipelines. SMEs prefer pay-per-use models where orchestration resides in multitenant control planes, and edge devices auto-patch during maintenance windows.

Geography Analysis

North America held 24.8% of the edge computing market in 2024, anchored by robust 5G deployment, a vast hyperscaler footprint, and public funding for semiconductor production. The Biden administration allocated USD 269 million to micro-electronics programs that strengthen domestic edge hardware capacity. Utilities in the United States deploy private LTE coupled with ruggedized MEC nodes to modernize grid operations, and 75% of enterprise-generated data is forecast to remain at or near the source by 2025 Canada follows, targeting autonomous mining and energy workflows that cannot tolerate WAN latency.

Asia Pacific is the fastest-growing region at a 15.1% CAGR through 2030. China’s “new infrastructure” policy incentivizes edge data-centre buildouts close to manufacturing clusters, and Huawei invested 20.8% of its 2024 revenue back into research and development that spans AI, automotive, and cloud services. India’s smart-city programs integrate edge-enabled surveillance and traffic optimization, while Japan’s automation giants embed deterministic Ethernet and TSN in production lines. Regional telcos leverage aggressive fiber roll-outs to backhaul edge aggregates to metro cores, minimizing jitter for immersive gaming and telepresence.

Competitive Landscape

The edge computing market shows moderate fragmentation, with hyperscalers, legacy infrastructure firms, and pure-play startups each owning strategic niches. Amazon Web Services drives managed outbound traffic to customer premises through AWS Outposts, backed by annual revenue surpassing USD 100 billion. Microsoft Azure Arc extends policy enforcement across on-premises clusters, buoyed by a USD 40 million stake in edge orchestration firm Armada Google Cloud emphasizes Anthos-based multi-cloud portability that targets telecom MEC estates.

Traditional vendors leverage hardware provenance and channel depth. Dell booked over USD 12 billion in AI server orders in 2025 and expects edge-ready SKUs to top USD 15 billion per year Cisco ships ruggedized switches with embedded CUDA cores, enabling deterministic routing and local inferencing in a single unit. HPE’s GreenLake platform offers consumption-based pricing that resonates with SME adopters.

Startups innovate on observability, zero-touch deployment, and ultra-low-power silicon. Spectro Cloud attracts funding from Qualcomm Ventures to simplify Kubernetes lifecycle across thousands of heterogeneous nodes. Namla collaborates with Advantech to cut deployment cost by 90% using auto-provisioned edge clusters. In parallel, vertical specialists such as Honeywell integrate 5G modules from Verizon into smart meters, delivering secure, real-time energy analytics to utility back office. Patent filings underscore the race: Intel leads with 522 edge patents, followed by Pure Storage and IBM, illustrating a broad commitment to research and development across compute, storage, and networking.

Edge Computing Industry Leaders

-

Amazon Web Services (AWS)

-

Microsoft Corporation

-

Cisco Systems Inc.

-

Huawei Technologies Co. Ltd.

-

IBM Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: EdgeX Labs secured funding from Ryze Labs to accelerate global edge-node rollout and optimize the EdgeX OS for decentralized AI workloads.

- May 2025: Dell Technologies lifted its profit outlook after confirming USD 14.4 billion in AI system orders and forecasting USD 15 billion in AI server sales for fiscal 2026.

- April 2025: Huawei introduced the Ascend 920 AI accelerator and began shipping the 910C model to domestic customers, bringing high-efficiency inference to factory-floor gateways.

- March 2025: Honeywell and Verizon Business integrated 5G connectivity into smart meters, enabling utilities to manage energy usage through edge-resident analytics.

Global Edge Computing Market Report Scope

Edge computing refers to the distributed computing paradigm, mainly used to bring computing and data storage closer to the location to improve the response time. The analysis tools used across industries are beginning to drive new levels of performance and productivity. Therefore, the distributed computing paradigm called edge computing is gaining traction.

The Edge Computing Market is Segmented by Component (Hardware, Software, and Services), End User (Financial and Banking Industry, Retail, Healthcare and Life Sciences, Industrial, Energy and Utilities, Telecommunications), and Geography (North America, Europe, Asia Pacific, Latin America, Middle East & Africa).

The market sizes and forecasts are provided in terms of value (USD Billion) for all the above segments.

| By Component | Hardware | |||

| Software | ||||

| Services | ||||

| By Deployment Mode | On-Premise | |||

| Cloud | ||||

| By End-user Industry | Manufacturing and Industrial | |||

| Energy and Utilities | ||||

| Healthcare and Life Sciences | ||||

| Retail and E-commerce | ||||

| BFSI | ||||

| Telecommunications and IT | ||||

| Others | ||||

| By Application | Industrial IoT and Predictive Maintenance | |||

| Video Analytics and Surveillance | ||||

| Autonomous Vehicles and Drones | ||||

| Others | ||||

| By Organisation Size | Large Enterprises | |||

| Small and Medium Enterprises | ||||

| By Geography | North America | United States | ||

| Canada | ||||

| Mexico | ||||

| South America | Brazil | |||

| Argentina | ||||

| Rest of South America | ||||

| Europe | Germany | |||

| United Kingdom | ||||

| France | ||||

| Italy | ||||

| Spain | ||||

| Russia | ||||

| Rest of Europe | ||||

| APAC | China | |||

| Japan | ||||

| India | ||||

| South Korea | ||||

| Australia and New Zealand | ||||

| Southeast Asia | ||||

| Rest of APAC | ||||

| Middle East and Africa | Middle East | Saudi Arabia | ||

| United Arab Emirates | ||||

| Turkey | ||||

| Rest of Middle East | ||||

| Africa | South Africa | |||

| Nigeria | ||||

| Egypt | ||||

| Rest of Africa | ||||

| Hardware |

| Software |

| Services |

| On-Premise |

| Cloud |

| Manufacturing and Industrial |

| Energy and Utilities |

| Healthcare and Life Sciences |

| Retail and E-commerce |

| BFSI |

| Telecommunications and IT |

| Others |

| Industrial IoT and Predictive Maintenance |

| Video Analytics and Surveillance |

| Autonomous Vehicles and Drones |

| Others |

| Large Enterprises |

| Small and Medium Enterprises |

| North America | United States | ||

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| APAC | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia and New Zealand | |||

| Southeast Asia | |||

| Rest of APAC | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the edge computing market?

The edge computing market stands at USD 227.80 billion in 2025 and is forecast to hit USD 424.15 billion by 2030.

Which component segment holds the largest edge computing market share?

Hardware leads with 45.2% share in 2024 as enterprises invest in ruggedized servers, accelerators, and networking equipment.

Why is Asia Pacific the fastest-growing region?

Government-backed 5G roll-outs, smart-city programs, and significant R&D spend by vendors like Huawei drive a 15.1% regional CAGR to 2030.

How are data-sovereignty regulations influencing adoption?

Laws such as the EU Data Act require sensitive information to be processed locally, encouraging enterprises to deploy on-premises micro-data-centres that comply with residency rules.