Edge Computing In Healthcare Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 9.71 Billion |

| Market Size (2031) | USD 23.22 Billion |

| Growth Rate (2026 - 2031) | 19.05% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

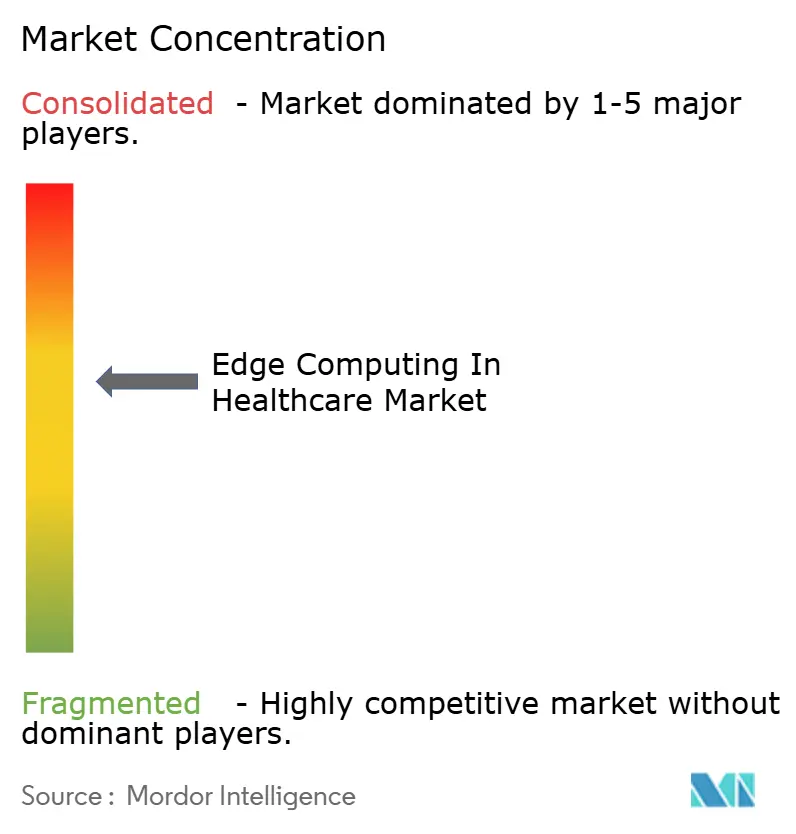

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Edge Computing In Healthcare Market Analysis by Mordor Intelligence

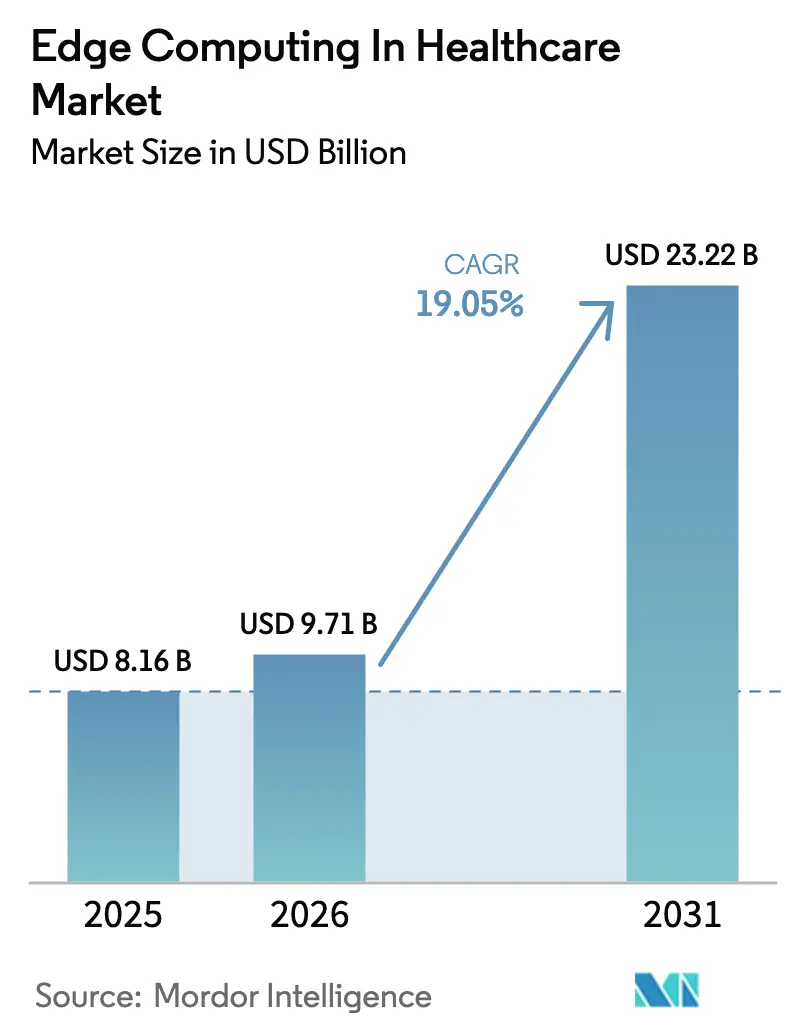

The Edge Computing In Healthcare Market size was valued at USD 8.16 billion in 2025 and estimated to grow from USD 9.71 billion in 2026 to reach USD 23.22 billion by 2031, at a CAGR of 19.05% during the forecast period (2026-2031).

This acceleration reflects hospitals’ urgent need to process life-critical data in sub-millisecond windows, the spread of hospital-at-home reimbursement, and tightening data-residency rules that favor on-premises nodes. Hardware refresh cycles have intensified as clinicians demand deterministic performance for AI-driven image analysis, while managed services gain traction among providers lacking edge-skilled staff. Competitive activity is brisk: hyperscalers extend their clouds to the point of care even as medical-grade specialists introduce purpose-built devices. The convergence of 5G, federated learning and privacy-preserving analytics is creating fresh use cases that anchor the next wave of capital spending across the edge computing in healthcare market.

Key Report Takeaways

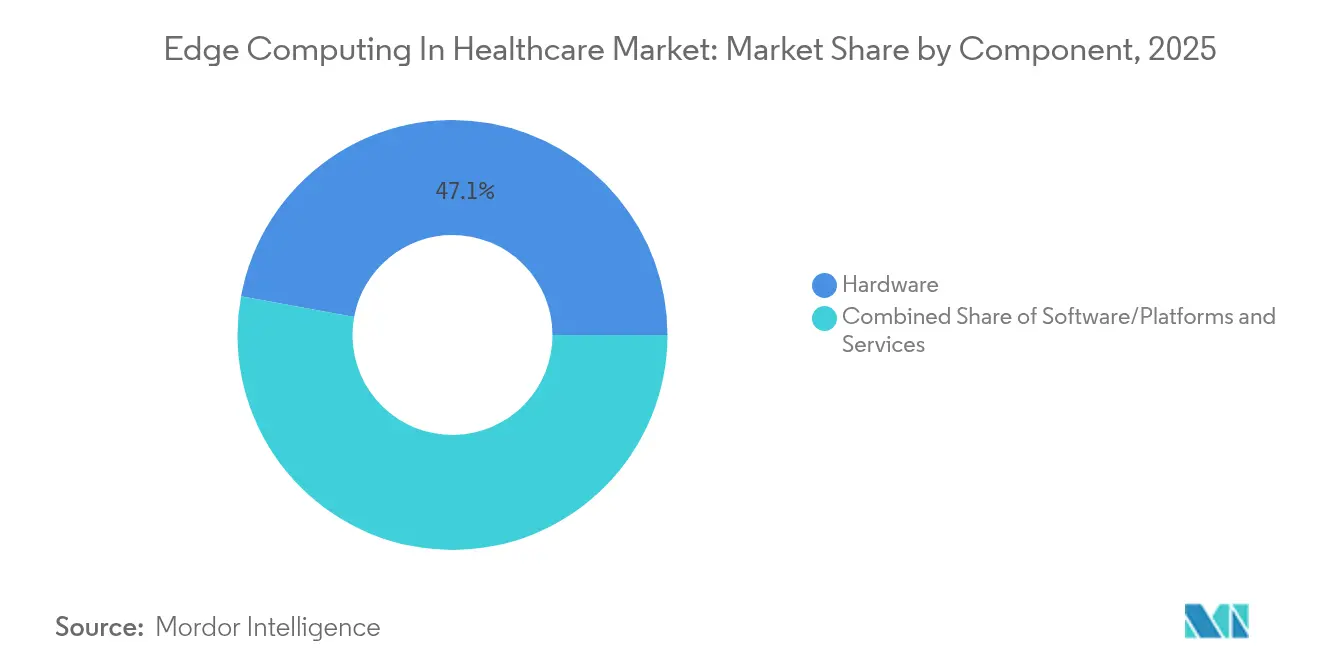

- By component, hardware led with 47.11% of the edge computing in healthcare market share in 2025 and services are projected to expand at a 24.93% CAGR through 2031, the fastest among components.

- By application, diagnostics and monitoring commanded 35.65% of the edge computing in healthcare market size in 2025 and telehealth and remote patient monitoring are slated to grow at a 27.09% CAGR between 2026-2031.

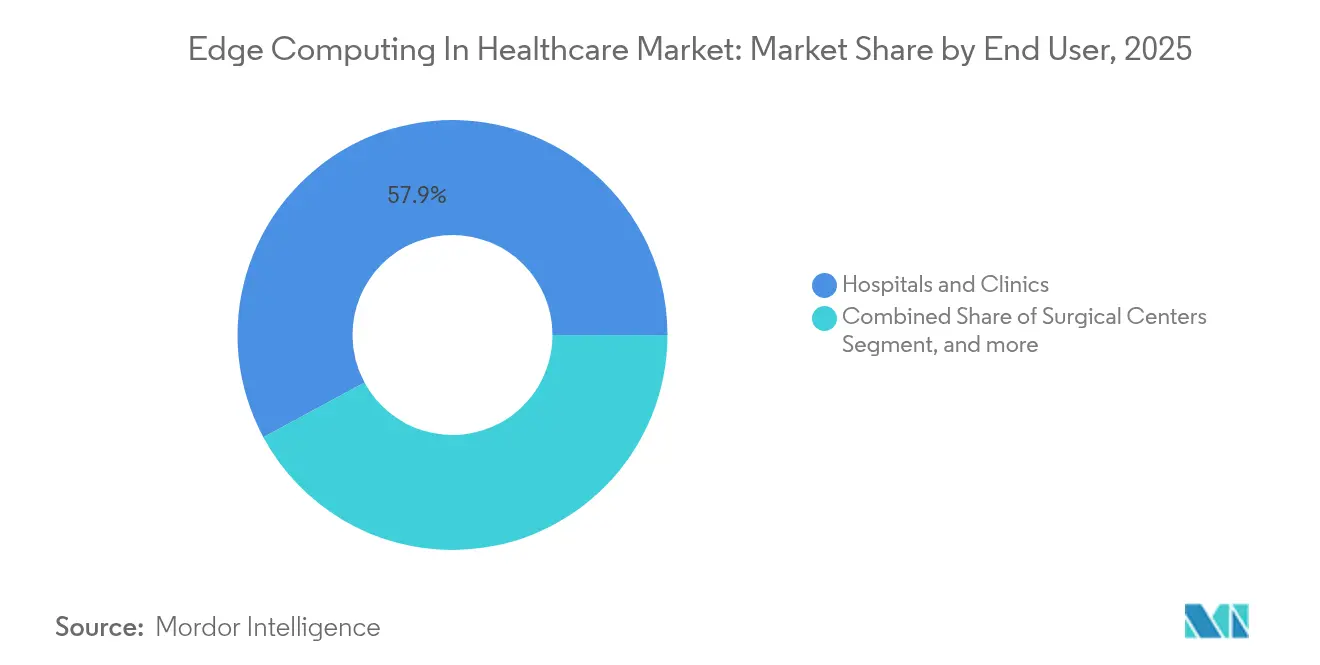

- By end user, hospitals and clinics held a 57.88% share of the edge computing in healthcare market size in 2025 and long-term and home-care providers are forecast to post a 23.45% CAGR to 2031.

- By geography, North America retained a 42.65% edge computing in healthcare market share in 2025, while Asia Pacific is set to register a 28.35% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Edge Computing In Healthcare Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing adoption of IoT-enabled medical devices | +3.2% | Global, with APAC leading adoption | Medium term (2-4 years) |

| Rapid digitalization of healthcare workflows | +2.8% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Demand for ultra-low-latency decision support | +4.1% | Global, concentrated in advanced health-care systems | Medium term (2-4 years) |

| Stricter data-residency regulations | +3.5% | North America, EU, selective APAC markets | Long term (≥ 4 years) |

| Hospital-at-home reimbursement models | +2.9% | North America, selective EU markets | Medium term (2-4 years) |

| Edge-enabled federated learning | +2.7% | Global, led by research-intensive markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Adoption of IoT-Enabled Medical Devices

Healthcare systems are placing compact servers beside beds, ICUs and imaging suites to crunch torrents of sensor data where latency cannot exceed a heartbeat. Continuous glucose monitors, smart infusion pumps and wearable ECG patches now embed edge AI chips that flag anomalies locally, ensuring no packet loss during network outages. Provincial health authorities in Canada use camera-based sleep monitors that generate real-time alerts for long-term-care residents, freeing nurses from manual rounds.[1]Fraser Health, “Digital Sleep Monitoring Pilot,” fraserhealth.ca Vendors respond with ruggedized fan-less servers capable of processing video streams, accelerating the edge computing in healthcare market as procurement teams upgrade device fleets.

Rapid Digitalization of Healthcare Workflows

Voice-driven charting, ambient listening and real-time imaging analysis all depend on deterministic performance that cloud-only architectures cannot guarantee. Bedside gateways equipped with Microsoft’s ambient clinical intelligence tools cut documentation time and raise staff satisfaction, pushing hospitals to budget for more distributed nodes. Surgical OEMs adopt NVIDIA’s Holoscan kits to run inference models inside operating theatres, avoiding WAN jitter that could misalign a robotic arm. As tele-consults become routine, edge orchestration platforms synchronize data across campuses and remote clinics, cementing the case for broader edge computing in healthcare market deployments.

Demand for Ultra-Low-Latency Decision Support in Critical Care

Code blue events leave no margin for cloud round-trips. Emergency departments deploy AI models on-prem to aggregate vitals, labs and images in under 10 ms, raising diagnostic accuracy during the first golden hour. Telesurgery pilots linking Orlando with Dubai relied on 5G-enabled edge nodes to keep end-to-end latency below 50 ms, validating commercial use at scale.[2]Ericsson, “5G-Enabled Tele-Surgery Milestone,” ericsson.com NVIDIA reports that fine-tuning data pathways can shave a further 30% off worst-case latency, adding competitive urgency across the edge computing in healthcare market.

Stricter Data-Residency Regulations Boosting On-Prem Edge Nodes

April 2025 US rules ban outbound transfers of biometric and health data to specified nations, compelling providers to keep processing inside domestic borders.[3]US Department of Justice, “Prohibition of Certain Health Data Transfers,” orrick.com France’s updated certification and new Texas statutes mirror this stance, all but mandating local compute for electronic health records. German guidance tightens cloud conditions for pharma trials, further anchoring demand for compliant edge gear. Vendors that bundle tamper-proof logging and automated location assurance gain an edge as CIOs standardize procurement across jurisdictions.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High deployment & lifecycle costs | -2.1% | Global, impacting smaller providers | Short term (≤ 2 years) |

| Persistent data-security & interoperability concerns | -1.8% | Global, with regional regulatory complexity | Medium term (2-4 years) |

| Scarcity of edge-skilled clinical IT workforce | -1.5% | Global, acute in North America and Europe | Long term (≥ 4 years) |

| Fragmented proprietary hardware ecosystem | -1.2% | Global, vendor hubs in North America & Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Deployment & Lifecycle Costs of Edge Infrastructure

Full-hospital roll-outs can exceed USD 10 million when racks, hardened enclosures, PoE switches and OT protocols are tallied. Integration outlays escalate as legacy PACS, LIS and EMR systems require custom APIs. Yet ROI studies on radiology AI show a 451% five-year return that climbs to 791% once radiologist time savings are monetized. Vendors now offer subscription bundles, shifting cap-ex to op-ex and broadening access across community hospitals eager to enter the edge computing in healthcare market.

Persistent Data-Security & Interoperability Concerns

A record number of healthcare breaches in 2024 exposed the sector’s widening attack surface. Each new IoT skin patch or bedside camera is a potential ingress. Zero-trust micro-segmentation and SBOM inventories mitigate risk, yet add complexity for understaffed IT teams. Interoperability hurdles persist as siloed data formats hinder real-time analytics; semantic AI and FHIR gateways are improving exchange but require rigorous governance. Until confidence rises, some providers will defer large-scale moves, tempering immediate growth within parts of the edge computing in healthcare market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Hardware Remains the Spending Anchor

The hardware segment accounted for 47.11% of the edge computing in healthcare market size in 2025, underlining the capital-intensive nature of distributed computing at the bedside. Rack-mount GPU servers, fan-less DIN-rail units and sterilizable smart displays dominate procurement lists as providers prioritize deterministic processing for AI inferencing. Advantech’s USM-500 with NVIDIA RTX A6000 accelerators is illustrative, delivering PACS-level throughput on a shoebox footprint. Intel’s work with Azure to compress medical-image pipelines shows how silicon-level optimizations cut TCO, nudging price-sensitive buyers toward mid-range SKUs.

Services posted a 24.93% CAGR and are poised to close the gap as hospitals outsource orchestration, SLA monitoring and patch compliance. Managed offerings from Namla deploy Zero-Touch agents to thousands of gateways, reducing manual updates and freeing clinical engineers for patient-facing tasks. Software platforms sit between the two, coordinating workload placement and ensuring that inference models remain within latency budgets, further solidifying the total addressable edge computing in healthcare market.

By Application: Telehealth Surges, Diagnostics Holds the Lead

Diagnostics and monitoring captured 35.65% of the edge computing in healthcare market share in 2025, buoyed by 950 FDA-cleared AI/ML devices; 750 of which support radiology workflows. Siemens Healthineers’ Ciartic Move C-arm leverages embedded edge AI to halve positioning time and cut fluoroscopy dose, illustrating demand for local compute during surgery.

Telehealth and RPM are expanding fastest at 27.09% CAGR as wearables transmit 24/7 vitals into edge gateways that deliver predictive alerts without network round-trips. HealthSnap’s AI-driven RPM platform identifies hypertension exacerbations days earlier than traditional methods, demonstrating clinical pay-off. The edge computing in healthcare industry also sees nascent use cases in connected ambulances, trauma drones and smart ER triage kiosks, widening future demand.

By End User: Acute Care Dominates, Home Care Accelerates

Hospitals and clinics commanded 57.88% of the edge computing in healthcare market size in 2025, reflecting their infrastructure budgets and high-acuity use cases. Microsoft’s collaborations with multi-state systems integrate ambient AI inside exam rooms, driving tangible workflow gains. Teaching hospitals double as living labs, piloting edge-enabled digital twins that optimize patient flow.

Long-term and home-care facilities are tracking a 23.45% CAGR to 2031. Computer-vision boxes such as Kepler Vision’s Night Nurse run on-prem rather than in the cloud, preserving privacy while cutting false alarms by 99%. Nursing-home operators are specifying edge nodes in new-build designs to future-proof against regulatory tightening, ushering in another growth pole for the edge computing in healthcare market.

Geography Analysis

North America retained 42.65% of the 2025 edge computing in healthcare market share thanks to early RPM reimbursement, mature cloud ecosystems and an active MedTech manufacturing base. The United States accounts for the bulk of spending as providers refresh imaging suites and build hybrid clouds that keep PHI inside hospital walls. Canadian provinces pilot province-wide virtual wards, pushing edge nodes into community clinics. Mexico’s public health upgrades, backed by federal digital-transformation funds, are starting to specify local processing to comply with new privacy statutes.

Europe’s growth is steady under the General Data Protection Regulation, which encourages on-prem deployments. France’s tightened Health Data Host rules, Germany’s sector-specific cloud guidance and Italy’s ongoing e-Health Record rollout all incentivize node localization. Vendor competition revolves around turnkey “sovereign edge” bundles that pair hardware with automated residency attestation, a model propelling the broader edge computing in healthcare market forward.

Asia Pacific is projected to clock a 28.35% CAGR through 2031, the fastest globally. Singapore’s AI Verify sandbox gives providers latitude to experiment with diagnostic models, while Japan’s soft-law approach accelerates AI-assisted drug screening. Mainland China, by contrast, enforces strict model registration, propelling demand for in-country inference clusters that conform to its health-data rules. ASEAN ministries invest in disease-surveillance platforms that keep analytics in-region, a policy that dovetails neatly with edge architectures. Together these dynamics anchor rapid regional adoption and position Asia Pacific as a pivotal contributor to future edge computing in healthcare market expansion.

Competitive Landscape

The market sits at a moderate concentration level. Hyperscalers Microsoft, AWS and Google Cloud extend Kubernetes-based stacks to campus closets, bundling observability and AI accelerators. They leverage existing EMR integrations to win enterprise deals yet must adapt to surgical and imaging environments that demand IEC-60601-certified hardware. Intel, NVIDIA and AMD compete on silicon roadmaps, each courting OEMs with reference designs optimized for healthcare inference.

Specialists such as Advantech focus on medical-grade form factors, integrating HBM-equipped GPUs for OR vision pipelines. Their partnership with NVIDIA provides IP protection for clinical models, a differentiator when CIOs fear data spillage. Namla, Edgeworx and ClearBlade vie in orchestration, promising push-button software distribution from cloud to ward. Start-ups targeting federated learning and zero-trust asset management address buyer pain points around privacy and cyber-risk, carving out niches in the expanding edge computing in healthcare market.

Patent filings accelerate: applications cite deterministic scheduling, PACS integration and homomorphic encryption for EHR analytics. M&A activity remains brisk; hardware vendors snap up cybersecurity boutiques while cloud majors acquire compliance specialists. In this climate, vendors able to combine edge appliances, orchestration, and clinical workflow apps under a single support umbrella enjoy a widening competitive moat.

Edge Computing In Healthcare Industry Leaders

Cognizant

IBM

Microsoft

Dell Technologies

Advantech

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Oracle Health, Cleveland Clinic, and UAE's G42 announced a strategic collaboration to develop an AI-based healthcare platform utilizing Oracle's Cloud Infrastructure and AI Data Platform, aimed at enhancing point-of-care clinical data applications and enabling nation-scale data analytics for improved patient outcomes.

- March 2025: Advantech launched comprehensive Edge AI compute solutions powered by Snapdragon X Elite platform, featuring integrated AI acceleration up to 45 TOPS and robust connectivity through 5G and Wi-Fi 7, specifically designed for demanding healthcare applications including computer vision and generative AI.

- July 2024: Cognizant reported the launch of the Cognizant Neuro Edge, a platform designed to empower businesses across industries to leverage artificial intelligence and generative AI at the edge. This solution enables real-time data processing, enhanced data privacy, reduced bandwidth costs, and increased operational resilience so that healthcare organizations can harness the power of edge technology and drive the business forward.

- March 2024: Johnson & Johnson MedTech reported collaborating with NVIDIA to accelerate and scale artificial intelligence (AI) to increase access to real-time analysis and surgical decision-making. The Johnson and Johnson MedTech will utilize the NVIDIA IGX edge computing platform and the NVIDIA Holoscan edge AI platform to create infrastructure to deploy AI-powered software applications in the operation room.

Global Edge Computing In Healthcare Market Report Scope

As per the scope of the report, edge computing in the healthcare market refers to bringing processing capacity and data processing systems closer to medical data sources to analyze medical data more efficiently and enhance patient outcomes.

Edge computing in the healthcare market is segmented into components, applications, end users, and geography. By component, the market is segmented into software, hardware, and services. By application, the market is segmented into diagnostics and monitoring, telehealth and remote patient monitoring, robotic AI-assisted surgery, and ambulances. By end user, the market is segmented into hospitals and clinics, surgical centers, and other end users (diagnostic centers, long-term care centers, and other end users). By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers values (USD) for the above segments.

| Hardware |

| Software/Platforms |

| Services |

| Diagnostics & Monitoring |

| Telehealth & Remote Patient Monitoring |

| Robotic & AI-Assisted Surgery |

| Connected Ambulances & Emergency Services |

| Hospitals & Clinics |

| Surgical Centers |

| Diagnostic & Imaging Centers |

| Long-Term & Home-Care Providers |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Hardware | |

| Software/Platforms | ||

| Services | ||

| By Application | Diagnostics & Monitoring | |

| Telehealth & Remote Patient Monitoring | ||

| Robotic & AI-Assisted Surgery | ||

| Connected Ambulances & Emergency Services | ||

| By End User | Hospitals & Clinics | |

| Surgical Centers | ||

| Diagnostic & Imaging Centers | ||

| Long-Term & Home-Care Providers | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is driving the rapid adoption of edge computing in hospitals and clinics?

Hospitals need sub-millisecond processing for AI imaging, ICU monitoring and telesurgery; on-premise edge nodes eliminate cloud latency while meeting stricter data-residency laws.

How large is the edge computing in healthcare market today?

The edge computing in healthcare market size reached USD 9.71 billion in 2026 and is forecast to hit USD 23.22 billion by 2031.

Which application area is growing fastest?

Telehealth and remote patient monitoring lead growth with a projected 27.09% CAGR as hospital-at-home programs expand reimbursement and wearable sensors proliferate.

Why are services outpacing hardware in future growth?

Managed services ease deployment, cybersecurity and lifecycle upkeep for providers that lack edge-skilled IT staff, pushing the services segment toward a 24.93% CAGR through 2031.

What are the main barriers to wider deployment?

High capital costs, cybersecurity risks, interoperability gaps and a shortage of edge-literate clinical IT personnel slow adoption, especially among smaller providers.

Which region is expected to see the fastest expansion?

Asia Pacific is projected to post a 28.35% CAGR through 2031, propelled by diverse AI regulations, heavy digitization investments and rising demand for connected care solutions.

Page last updated on: