Earphones And Headphones Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

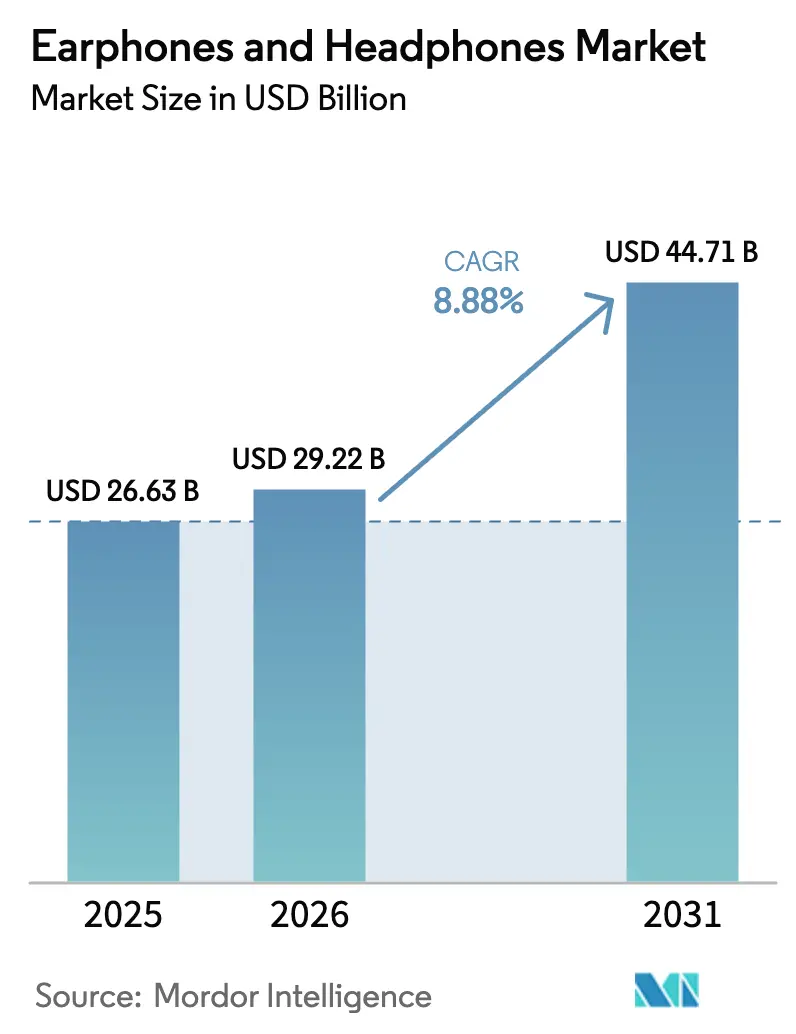

| Market Size (2026) | USD 29.22 Billion |

| Market Size (2031) | USD 44.71 Billion |

| Growth Rate (2026 - 2031) | 8.88% CAGR |

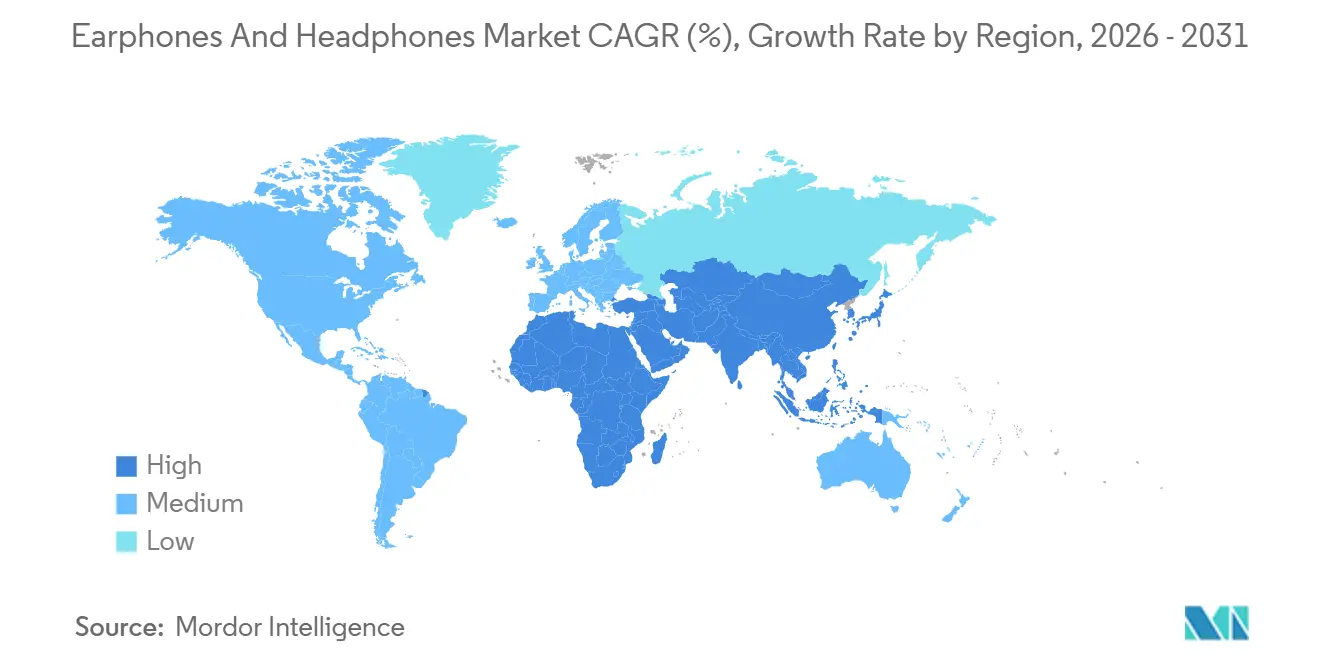

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

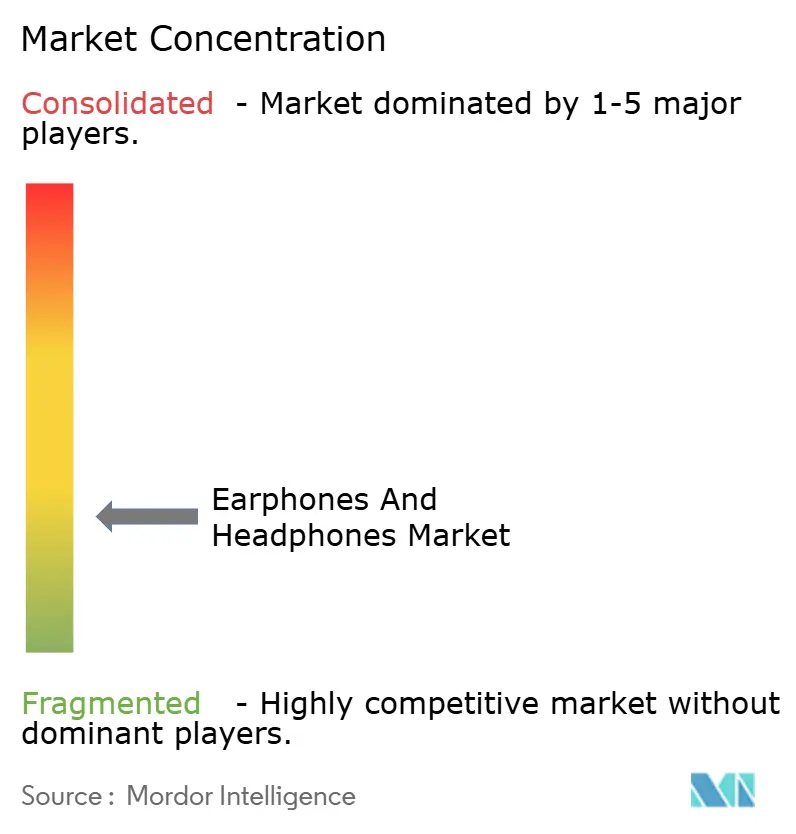

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Earphones And Headphones Market Analysis by Mordor Intelligence

The Earphones And Headphones Market size was valued at USD 26.63 billion in 2025 and is estimated to grow from USD 29.22 billion in 2026 to reach USD 44.71 billion by 2031, at a CAGR of 8.88% during the forecast period (2026-2031).

The market’s current expansion is driven by the rapid migration from wired headsets to wireless designs that integrate adaptive noise cancellation, spatial-audio processing, and biometric sensing. Premium true wireless models now arrive with onboard neural processors that tune sound signatures in real time, while mid-tier products leverage the same codec upgrades within months, shrinking the innovation gap. Subscription-bundled hardware programs are shortening replacement cycles from three years to under two, providing vendors with recurring revenue streams that offset rising compliance costs. Competitive dynamics continue to intensify, as regional challengers use local manufacturing and subsidy-backed supply chains to undercut global brands by as much as 60% without sacrificing headline features.

Key Report Takeaways

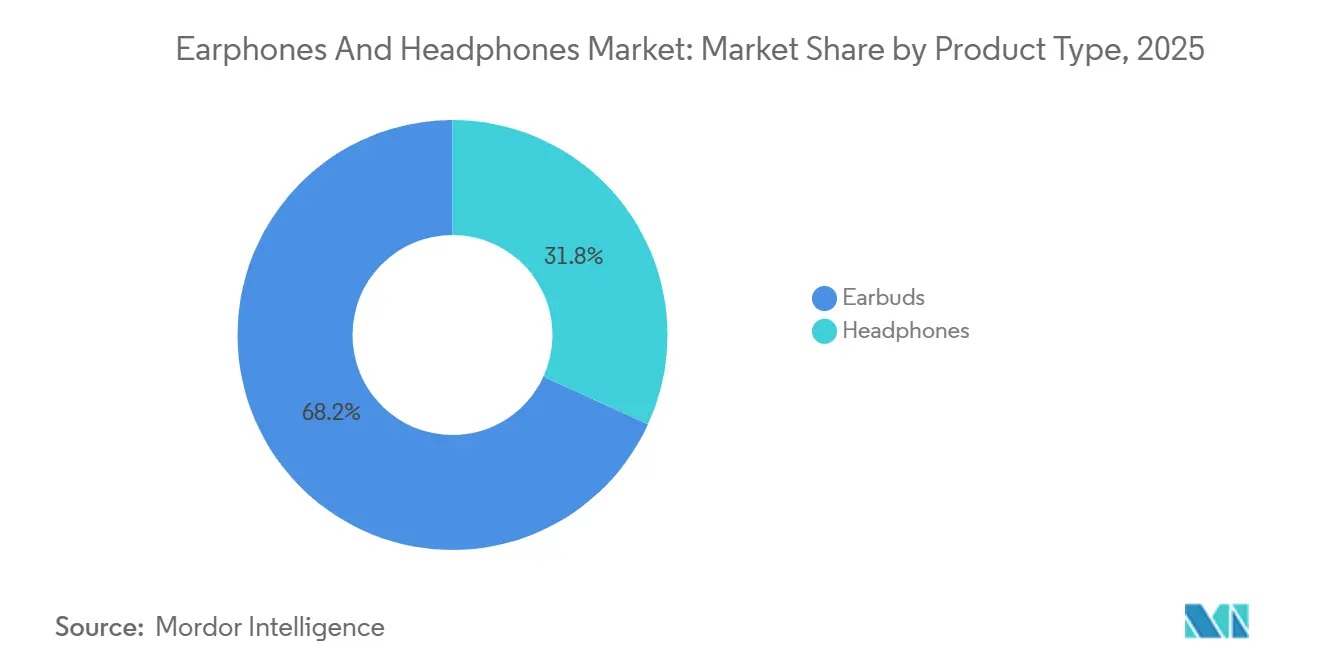

- By product type, true wireless stereo earbuds led with 68.18% revenue share of the earphones and headphones market in 2025, while hybrid ANC headphones are set to record a 10.01% CAGR through 2031.

- By connectivity, wireless designs commanded 72.63% share of the earphones and headphones market in 2025; hybrid ANC earphones are forecast to expand at 10.01% CAGR through 2031.

- By form factor, in-ear models captured 55.29% of the earphones and headphones market share in 2025; open-ear and bone-conduction designs are advancing at a 9.68% CAGR through 2031.

- By price band, the sub-USD 50 tier accounted for 52.57% of the earphones and headphones market in 2025, yet the USD 151–300 segment is projected to grow at a 10.22% CAGR through 2031.

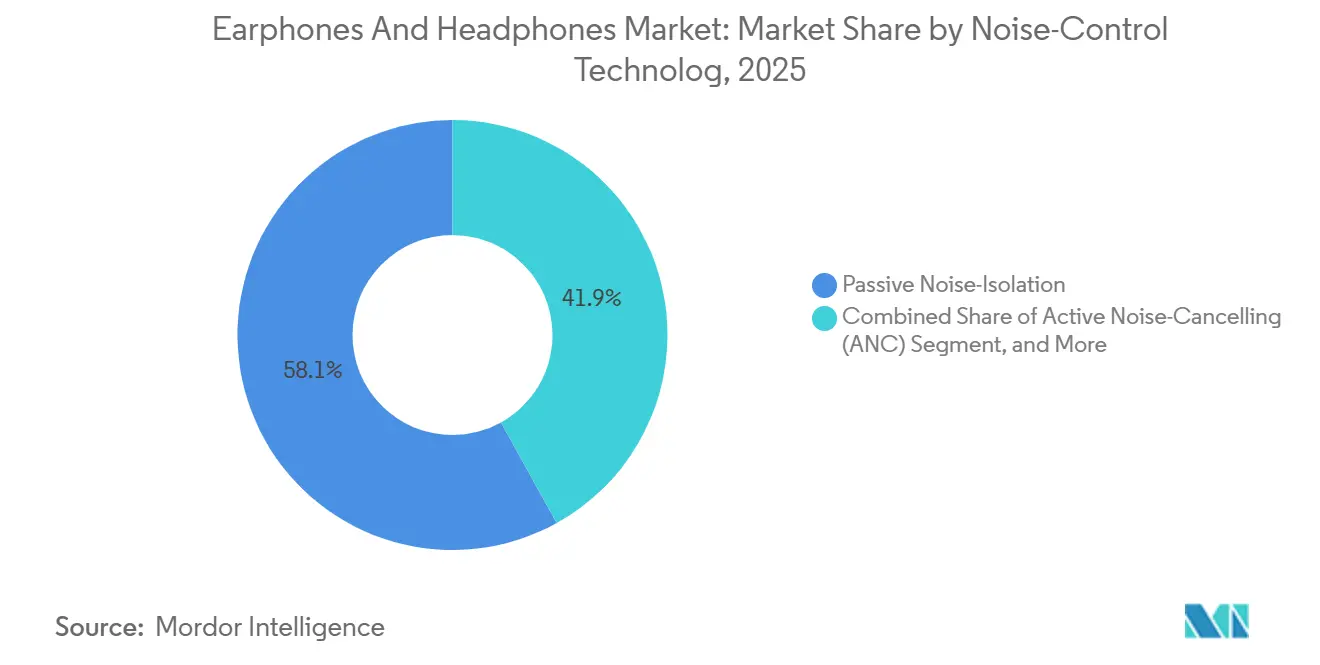

- By noise control technology, passive isolation held 58.06% of the earphones and headphones market in 2025, yet the hybrid ANC segment is projected to grow at a 10.01% CAGR through 2031.

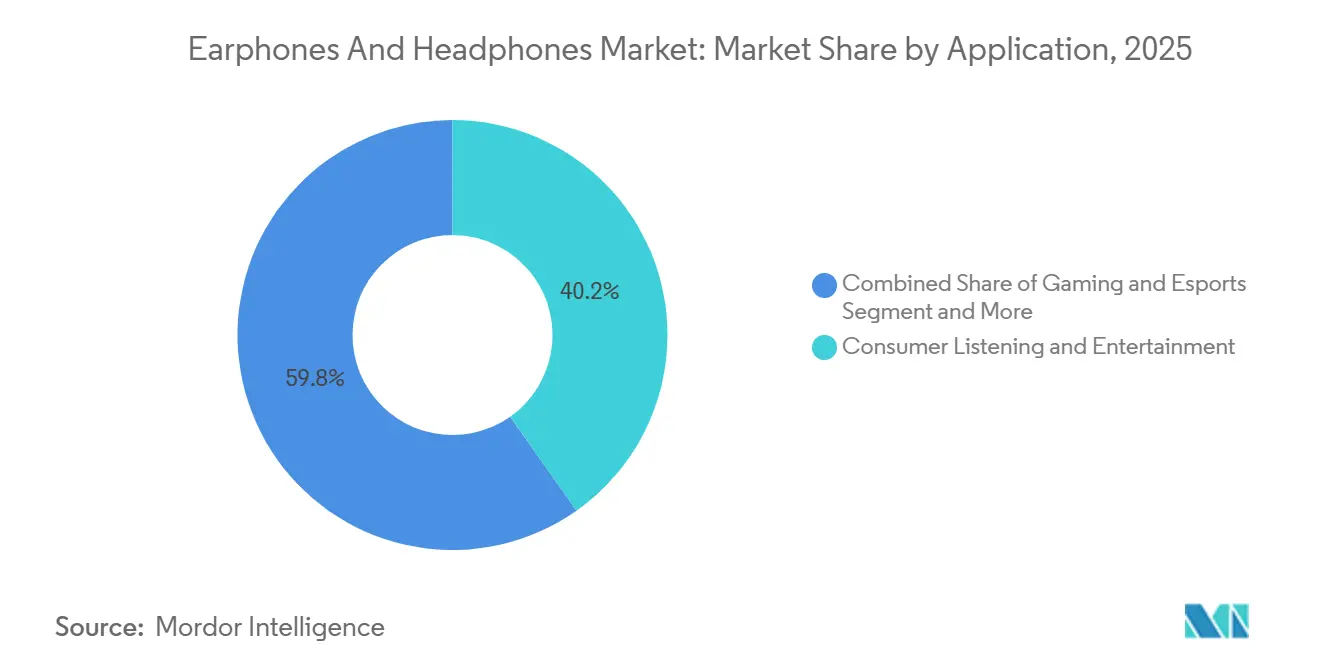

- By application, consumer listening and entertainment held 40.22% of the earphones and headphones market size in 2025, yet the sports and fitness segment is projected to rise at a 9.92% CAGR through 2031.

- By distribution channel, E-commerce and direct-to-consumer sites held 62.06% of the earphones and headphones market size in 2025. The segment is also projected to rise at a 10.15% CAGR through 2031.

- By geography, North America accounted for 35.78% of the earphones and headphones market size in 2025, while Asia Pacific is poised for the fastest regional growth through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Earphones And Headphones Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| In-App Spatial-Audio Ecosystems Accelerating Premium TWS Adoption in Asia | +1.80% | Asia Pacific core, spillover to North America | Medium term (2-4 years) |

| Enterprise Hybrid-Work Policies Fueling Demand for Boom-Mic Headsets in North America | +1.20% | North America and Europe | Short term (≤2 years) |

| Gen-Z Fitness Boom Boosting Open-Ear and Bone-Conduction Sales in Europe | +1.00% | Europe, expanding to North America | Medium term (2-4 years) |

| AI-Enabled Adaptive Noise-Cancellation Differentiating Flagship Models Globally | +1.50% | Global, early adoption in North America and Asia Pacific | Long term (≥4 years) |

| Esports Sponsorships Driving High-Fidelity Gaming Headphones in Middle East | +1.20% | Middle East core (Saudi Arabia, UAE), spillover to North Africa | Medium term (2–4 years) |

| Subscription-Bundled Hardware Models Lifting Upgrade Cycles | +1.50% | North America and Western Europe core, emerging uptake in Asia Pacific | Short to medium term (1–3 years) |

| Source: Mordor Intelligence | |||

In-App Spatial-Audio Ecosystems Accelerating Premium TWS Adoption in Asia

Streaming platforms in China, Japan, and South Korea now treat earbuds as extensions of mobile operating systems rather than commodity accessories. Dolby Atmos and Apple Spatial Audio became default check-box features on Tencent Video and Apple Music catalogs in 2025, encouraging users to upgrade hardware every 18–24 months when older chipsets cannot process head-tracking commands without latency spikes. [1]Apple Inc., “AirPods Pro (3rd Generation) – Technical Specifications,” Apple.com Qualcomm’s Snapdragon Sound S7 Gen 3 platform carried aptX Lossless and spatial-audio rendering to Android devices, allowing Samsung and Xiaomi to match Apple’s experience at a 30–50% price discount. This dual-ecosystem rivalry incentivizes chipset vendors to release annual revisions, embedding headphone upgrades into the same cadence as smartphone refreshes.

Enterprise Hybrid-Work Policies Fueling Demand for Boom-Mic Headsets in North America

Hybrid-work norms have cemented the boom-mic headset as a standard office peripheral. Logitech’s Zone Vibe 125 and Jabra’s Evolve2 75 pair flip-to-mute arms with AI beamforming that masks keyboard clatter, satisfying corporate mandates for intelligible speech during video calls.[2]Logitech International, “Logitech Completes Acquisition of HP’s Poly Business,” Logitech.com Financial services and healthcare firms adopted encrypted USB-C dongles such as Dell’s WL5024 Pro to secure voice traffic under privacy regulations. These enterprise-grade models sustain 40% gross margins despite consumer price compression, primarily because IT departments consolidate purchases under multiyear support contracts.

Gen-Z Fitness Boom Boosting Open-Ear and Bone-Conduction Sales in Europe

Gen-Z runners and cyclists across Germany, the Netherlands, and Scandinavia increasingly favor open-ear designs that preserve ambient awareness. Shokz’s OpenFit Air directs sound toward the ear canal without obstructing it, while its OpenRun Pro 2 uses bone conduction to transmit audio through the cheekbone, mitigating moisture buildup and infection risks. Safety guidelines that encourage audible perception of traffic have provided a regulatory tailwind, and partnerships with Garmin and Strava reinforce the fitness-tracking proposition. European retail chains report double-digit sell-through increases for open-ear SKUs positioned near cycling and running accessories.

AI-Enabled Adaptive Noise-Cancellation Differentiating Flagship Models Globally

Machine-learning-driven ANC now defines premium positioning. Bose’s CustomTune measures ear-canal resonance and optimizes filters within milliseconds, reducing the pressure sensation typical of legacy. Sony’s WH-1000XM6 employs dual neural processors that isolate voice bands while suppressing wind rumble during calls. Apple’s H2 chip samples 48,000 data points per second to cancel noise before it reaches the eardrum, earning a USD 100–150 premium over passive-isolation models. Smaller brands lacking proprietary silicon increasingly license Qualcomm reference platforms, narrowing differentiation and intensifying price competition.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Proliferation of Counterfeit Earbuds Depressing ASPs in South America | -0.8% | South America, spillover to Africa | Short term (≤2 years) |

| Battery-Waste Regulations Increasing Compliance Costs in Europe | -0.6% | Europe, expanding to North America | Medium term (2-4 years) |

| Spectrum-Interference Issues Limiting Ultra-Low-Latency LE Audio in Dense Cities | -0.4% | Global urban centers | Long term (≥4 years) |

| Health-Related Concerns on SPL Exposure Curbing Volume Limits | -0.5% | Global focus in Europe and North America | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Proliferation of Counterfeit Earbuds Depressing ASPs in South America

Customs authorities in Brazil seized more than 1.2 million fake earbuds in 2024, yet replicas that mimic Apple or Samsung designs still enter informal channels at one-third of authentic retail prices.[3]Brazilian Federal Revenue Service, “Customs Seizure Report: Counterfeit Electronics 2024,” Gov.br These products employ uncertified lithium-ion cells that pose fire risks, and when incidents occur, consumers often blame brand owners, eroding goodwill. Multinationals now embed NFC tags and QR-coded serials to enable smartphone verification, but the added USD 1–2 bill-of-materials cost squeezes margins in entry-level tiers. Unless enforcement improves, legitimate vendors will continue facing price erosion and warranty claims they did not cause.

Battery-Waste Regulations Increasing Compliance Costs in EU

The European Union’s revised WEEE and Battery directives obligate manufacturers to finance take-back and recycling programs and to meet a 65% collection rate by 2025 and 70% by 2030.[4]European Commission, “Waste Electrical and Electronic Equipment Directive 2024 Revision,” Eur-lex.europa.eu Compact TWS designs present intricate disassembly challenges: lithium-polymer cells, magnets, and PCBs are glued into housings smaller than 5 cm, forcing producers to invest in robotics such as Apple’s Daisy, which dismantles 200 devices per hour. Smaller brands without capital for automation rely on third-party recyclers, adding EUR 0.50–1.50 per unit and eroding already-thin 25% gross margins. The compliance burden accelerates consolidation as firms lacking scale exit or license designs to white-label assemblers.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: TWS Earbuds Sustain Volume Lead While Over-Ear Designs Retain Audiophile Loyalty

True wireless stereo models accounted for 68.18% of global revenue in 2025 and are projected to expand at a 9.9% CAGR through 2031, keeping the earphones and headphones market on its current innovation treadmill. Flagships combine sub-5 mm system-on-chip packages, six-hour battery endurance per bud, and spatial-audio rendering that once required dedicated digital signal processors. Apple’s H2, Samsung’s proprietary codec, and Qualcomm’s QCC5181 collectively demonstrate how power management and compute convergence enable lighter, more comfortable buds. Over-ear headphones nevertheless maintain carve-outs in studio mixing, professional broadcast, and long-haul travel. Sennheiser’s Momentum 4 integrates 42 mm transducers and adaptive ANC, servicing travelers who prize isolation and extended comfort during 12-hour flights. Audio-Technica’s ATH-M50x still ships more than 1 million units annually to engineers who insist on the reference flatness of wired monitoring rigs. The coexistence of pocketable convenience and circumaural fidelity suggests each form factor will continue addressing discrete use cases rather than converging into a single hybrid design.

Complementary opportunities emerge for brands that cross-pollinate technologies between categories. Sony’s WH-1000XM6 borrows the adaptive ANC cluster from its WF-1000XM earbuds, while Bose’s CustomTune references ear-canal scanning techniques perfected in its in-ear line. Gamers remain a separate cohort: Razer’s BlackShark V2 Pro and Corsair’s HS80 integrate low-latency RF dongles for tournament use, a function less relevant to mainstream listeners. As headset processors become more modular, vendors may introduce modular driver housings that detach for portability, though such innovations risk cannibalizing established segments without clear incremental revenue.

By Form Factor: In-Ear Dominance Confronted by Open-Ear Migration

In-ear and canal-fit models secured 55.29% of 2025 revenue thanks to natural passive isolation, silicone tips that attenuate 15–25 dB of ambient noise, and gym-friendly IP ratings. Yet open-ear and bone-conduction designs are expanding at a 9.7% CAGR through 2031 as fitness-oriented Gen-Z users demand situational awareness on urban streets. Shokz’s OpenFit Air demonstrates how directional speakers angled toward the ear canal can deliver acceptable bass response without blocking environmental cues, addressing regulatory recommendations that cyclists maintain ambient hearing. Over-ear headphones retain prominence in critical listening environments, benefiting from 40–50 mm drivers that reproduce sub-20 Hz frequencies. On-ear sets, once the style icon of commuter chic, chart a shrinking addressable base as consumers either prioritize the immersive seal of over-ears or the feather-weight freedom of TWS buds.

Manufacturers experiment with hybrid shells combining open-ear frames and detachable ANC pods, but user adoption remains speculative. Weight distribution, sweat ingress protection, and battery compartment placement emerge as engineering constraints. Retailers increasingly group open-ear SKUs inside running-accessory aisles rather than audio displays, suggesting cross-category merchandising will determine velocity as much as acoustics.

By Connectivity: Wireless Momentum Outpaces Residual Wired Niche

Wireless designs contributed 72.63% of 2025 revenue and will widen their lead on a 9.3% CAGR, propelled by Bluetooth LE Audio and the LC3 codec that supports near-CD fidelity at sub-300 kbps bitrates. The protocol’s low-latency attribute brings competitive parity with 2.4 GHz gaming dongles, erasing one of the last wired advantages for mainstream users. Neckband-style earbuds retain a following in emerging markets, offering 12–16 hour endurance courtesy of larger battery housings. Wired headphones hang on in studio environments and among audiophiles skeptical of codec claims, with Beyerdynamic’s DT 1990 Pro and Grado’s SR325x exemplifying USD 500-plus investments centered on signal purity. Infrared and legacy RF links fade into aviation and home-theater niches, unlikely to return as consumer standards.

The cost of Bluetooth silicon dropped 35% between 2023 and 2025, opening the door for USD 25 entry-level buds that still advertise LE Audio compatibility. Yet Wi-Fi congestion and urban spectrum interference remain pain points; brands that optimize adaptive frequency hopping enjoy measurably lower call-drop rates in crowded environments, a selling point visible in user-generated benchmarks on e-commerce portals.

By Noise-Control Technology: Hybrid ANC Rises While Passive Isolation Endures

Passive isolation still captured 58.06% of 2025 revenue, thanks to zero power draw and negligible bill-of-materials impact. Nevertheless, hybrid ANC is the fastest mover, expanding 10.01% CAGR through 2031. Bose’s CustomTune and Sony’s dual-sensor designs blend feedforward and feedback microphones with machine-learning filters that adjust to wearer motion and atmospheric pressure within 200 ms. Transparency modes graduated from exotic add-ons to default toggles on every premium TWS model introduced after 2024, reflecting user expectations for seamless transitions between isolation and awareness. Mid-price segments integrate single-channel feedforward ANC that blocks low-frequency drone, but as component costs slide, hybrid arrays will penetrate sub-USD 100 devices, raising the bar for baseline performance. Open-ear headsets incorporate directional ANC to cancel driver leakage rather than external noise, a niche technical twist that further fragments the category.

By Price Band: Value Tier Remains Dominant, Mid-Premium Gains Momentum

The sub-USD 50 bracket retained more than half of 2025 revenue, buoyed by Xiaomi’s Redmi Buds 6 and Anker’s Soundcore Liberty 4, which pair Bluetooth 5.3 radios with six-hour batteries for USD 30–50 price tags. However, the USD 151–300 segment is growing at a 10.22% CAGR as consumers pay premiums for spatial audio, lossless codecs, and IPX7 ratings, without reaching flagship territory. Samsung’s Galaxy Buds 3 Pro, launched at USD 249, underscores the sweet spot: AI-driven ANC, 360-degree head tracking, and USB-C charging below the Apple price umbrella. Above USD 300 lives a connoisseur enclave of Sennheiser, Grado, and Beyerdynamic enthusiasts who invest in external DAC-amps and hi-res libraries. The USD 51–150 middle ground often contains legacy flagships discounted 30–40%, creating value propositions that blur neat price-performance strata.

By Application: Entertainment Dominates, Sports and Fitness Accelerate

Consumer listening and entertainment generated 40.22% of 2025 revenue, supported by Spotify, Apple Music, and Tencent Music vying for subscribers via high-resolution tiers that demand compatible hardware. Sports and fitness usage rises at 9.92% CAGR, riding the wave of heart-rate sensors in Jabra’s Elite 8 Active and IP68 casings in Shokz’s OpenRun Pro 2 that sync with Strava-powered training plans. Gaming headsets enjoy new momentum in the Middle East, where Saudi Arabia’s Vision 2030 earmarked USD 38 billion for esports, securing Razer and Corsair brand visibility in shopping malls once reserved for console kiosks. Professional studio monitoring remains stable but price-resilient, with Audio-Technica and Sennheiser contracting multi-year supply deals with broadcast networks. Enterprise communication, once considered a plateau, now finds fresh impetus as hybrid-work persistence embeds certified headsets in corporate asset lists, raising refresh frequency to match laptop lifecycles.

By Distribution Channel: Online Grows as Offline Reinvents

E-commerce and direct-to-consumer sites captured 62.06% of 2025 sales and are forecast to expand 10.15% CAGR through 2031. Brand webstores bundle music subscriptions or cloud-gaming vouchers, nudging buyers toward premium SKUs and recurring revenue. Marketplaces like Amazon, JD.com, and Flipkart refine recommender algorithms that surface comparisons and user-demo videos, lowering buyer hesitation. Offline stores defend relevance by converting square footage into experiential zones: Apple’s Spatial Audio demo pods and Samsung’s Galaxy Studio provide immersive trials unavailable on a screen. Specialty retailers such as Crutchfield curate amplifier-headphone pairings, leveraging staff expertise as a moat against algorithmic suggestions. Hybrid click-and-collect models offer next-day pickup, bridging instant gratification with showroom advantages.

Geography Analysis

Asia Pacific held a 28% share of global revenue in 2025, driven by burgeoning smartphone penetration in India, Indonesia, and Vietnam, where first-time buyers outnumber replacement customers by 3 to 1. Domestic Chinese brands that combine design agility with local manufacturing captured more than half of the segment below USD 100, pushing multinationals to localize assembly or cede share. Japan and South Korea still record the highest per-capita spend on premium audio, driven by Sony and Samsung ecosystems that integrate wearables into broader device suites. India’s boAt shipped over 15 million units in 2024, using smartwatch bundles to cross-sell earbuds and illustrating how regional specialists can outmaneuver global giants on volume.

North America maintained a 35.78% share in 2025, anchored by an installed base of more than 200 million AirPods that refresh every two to three years and by enterprise headset mandates tied to Microsoft Teams rollouts. Europe followed at 22%, with replacement cycles extending toward 36 months amid macroeconomic caution and regulatory scrutiny on battery sustainability. The Middle East accelerates at 9.5% CAGR through 2031 as Saudi Arabia’s Public Investment Fund bankrolls esports arenas, pulling high-fidelity gaming headsets into mainstream retail assortments. South America struggles with counterfeit dilution and currency volatility but represents latent potential once enforcement stabilizes, especially in Brazil’s 220 million-strong market. Africa remains nascent, yet mobile-money platforms in Kenya and Nigeria shorten the path between brand webstores and underserved consumers, hinting at a leapfrog pattern similar to smartphone adoption.

Regulatory Landscape

Regulation for earphones and headphones is tightening around charging interoperability, radio compliance, and end-of-life obligations, which increases design and documentation requirements for global vendors. In the European Union, the Common Charger Directive (Directive (EU) 2022/2380) made USB-C a legal requirement for most rechargeable earbuds and headphones sold from December 28, 2024, with additional USB Power Delivery requirements when charging exceeds 5V/3A/15W. This accelerated migration away from proprietary connectors and pushed greater SKU harmonization for EU channels.

Product conformity and waste rules add further compliance layers. EU market access depends on CE marking supported by compliance with the Radio Equipment Directive (RED) and Low Voltage Directive (LVD). The revised WEEE and Battery rules strengthen producer take-back obligations and collection-rate targets (65% by 2025 and 70% by 2030), which increases per-unit recycling and reporting overhead for compact TWS designs. Internationally, the Basel Convention e-waste amendments became applicable on January 1, 2025, tightening cross-border movement controls for electrical and electronic waste and increasing the need for auditable reverse-logistics processes across distributors and refurbishers.

Value Chain Analysis

The earphones and headphones value chain begins with component inputs, including Bluetooth and ANC SoCs, microphones, batteries, drivers, and NdFeB magnets, and then moves through industrial design and acoustic tuning, OEM and ODM manufacturing and test, channel packaging, and global distribution across e-commerce, consumer electronics retail, and enterprise procurement. High-end TWS and premium headset assembly remains concentrated among large contract manufacturers such as Luxshare Precision and Goertek, which together capture a dominant share of top-tier orders. Brands differentiate upstream through proprietary silicon, codec stacks, and app ecosystems that bind hardware to platform use.

Pressure points increasingly center on materials and electronics supply. Rare earth elements used in high-performance magnets became a procurement risk after China tightened export licensing requirements in April 2025, prompting audio-electronics makers to diversify sourcing and consider alternative magnet and driver designs where feasible. On the electronics side, wider semiconductor demand cycles have also affected adjacent premium-audio categories, including RAM chip tightness reported in late 2025 for digital audio players. This has reinforced the shift toward buffer inventories for key chips and increased the strategic value of in-house PCB assembly investments by audio specialists seeking tighter control over quality, yields, and lead times.

Competitive Landscape

The top five vendors (Apple, Sony, Samsung, Bose, and Xiaomi) accounted for 45% of revenue in 2025, underscoring a moderately concentrated battlefield that still leaves room for regional disruptors. Apple dominates premium TWS through seamless H2-chip pairing across iPhones, iPads, and Macs, sustaining average selling prices of USD 249 and margins above 35%. Sony and Bose compete on acoustic fidelity and adaptive ANC, while Samsung leverages Galaxy-level bundling to boost attach rates. Xiaomi and boAt scale via cost-efficient local factories, accepting sub-20% gross margins to flood price-sensitive tiers and seed brand awareness for upselling.

Technology leadership centers on chipsets and codec roadmaps. Qualcomm’s Snapdragon Sound brings lossless streaming and sub-20 ms latency to more than 30 Android brands, eroding Apple’s historical latency advantage. Bluetooth SIG’s finalization of the LE Audio catalog enables Auracast broadcasting from a single hub to multiple listener headsets, promising public-venue applications once spectrum coexistence hurdles are resolved. Counterfeit mitigation and battery-recycling mandates pose twin challenges that disproportionately affect mid-tier entrants with thin balance sheets, encouraging licensing partnerships, and potential acquisitions by well-capitalized incumbents eager to fill portfolio gaps.

Earphones And Headphones Industry Leaders

Sony Group Corporation

Skullcandy Inc.

Sennheiser Electronic GmbH & Co. KG (Sennheiser)

Harman International Industries Incorporated

Bose Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Bluetooth LE Audio is creating whitespace beyond personal listening by enabling multi-stream audio and Auracast broadcast use cases in public venues. With compatible earbuds or headsets, a single transmitter can serve multiple listeners. The ecosystem is moving from standards discussion to implementation demonstrations, and at MWC 2026 Fraunhofer IIS and Airoha showcased a high-data-rate, multichannel spatial-audio solution using LC3plus and a Bluetooth SoC reference platform. The demonstration suggests a more practical route for OEMs to commercialize premium spatial-audio experiences using standardized building blocks.

Manufacturing diversification is also creating opportunities for brands and suppliers that can scale outside single-country concentration while meeting tighter sustainability requirements. Capacity expansion activity in Vietnam and India points to where new assembly and subassembly footprints are being placed, including Goertek Vina increasing investment in Bac Ninh in April 2026 to expand electronic equipment manufacturing and add targets including wireless transceivers and headphone charging bases. In October 2025, Foxconn Interconnect Technology outlined plans to upgrade production lines in Hyderabad to raise AirPods capacity. At the product level, EU-driven shifts toward USB-C charging and rising attention to battery longevity support differentiation through repairability and service models, including premium launches that emphasize user-replaceable batteries and longer usable life.

Recent Industry Developments

- May 2026: Sony Electronics unveiled 1000X THE COLLEXION, a premium wireless noise-canceling headphone positioned around the 10th anniversary of the 1000X line, and introduced a Sandstone color option for the WH-1000XM6. The update extends Sony's price ladder above its mainstream flagship to compete more directly for luxury design-led buyers, while keeping the XM-series as the core volume anchor.

- September 2025: HARMAN International completed its acquisition of Sound United, adding brands such as Bowers & Wilkins, Denon, and Marantz under a standalone Strategic Business Unit. The deal strengthens HARMAN's premium-audio portfolio breadth and provides more leverage across shared acoustics R&D, channel relationships, and cross-category bundling that can influence headphone attach opportunities.

- November 2024: Bose finalized the acquisition of McIntosh Group, bringing high-end brands McIntosh and Sonus faber into its portfolio. This expands Bose's reach into luxury audio ecosystems and can create halo effects for premium headphone positioning through shared brand storytelling, retail presence, and high-end customer bases.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the value of earphones and headphones sold as finished audio devices, including in-ear, on-ear, and over-ear formats, across wired and wireless connectivity. The sizing is captured at first commercial sale across consumer and work use cases.

Scope exclusions: We exclude hearing aids, mixed reality headsets, car audio speakers, and standalone smart speakers to avoid counting adjacent audio categories.

Segmentation Overview

- By Product Type

- Headphones

- Earphones/Earbuds

- By Form Factor

- Over-Ear

- On-Ear

- In-Ear/Canal

- Open-Ear/Bone-Conduction

- By Connectivity

- Wired

- Wireless

- True Wireless Stereo (TWS)

- Neckband

- RF/Infra-red

- By Noise-Control Technology

- Active Noise-Cancelling (ANC)

- Passive Noise-Isolation

- Open-Transparency/Ambient Mode

- By Price Band

- Sub-USD 50 (Value)

- USD 51-150

- USD 151-300

- Above USD 300

- By Application

- Consumer Entertainment and Music

- Gaming and Esports

- Sports and Fitness

- Professional Studio and Broadcast

- Enterprise/Call-Center/UC&C

- By Distribution Channel

- Online

- E-commerce Marketplaces

- Brand Webstores

- Offline

- Consumer Electronics Chains

- Specialty Audio Stores

- Hypermarkets/Supermarkets

- Online

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Nordics

- Rest of Europe

- Asia-Pacific

- China

- Japan

- South Korea

- India

- South East Asia

- Australia

- Rest of Asia-Pacific

- South America

- Brazil

- Rest of South America

- Middle East

- United Arab Emirates

- Saudi Arabia

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk work was used to map the basic demand and supply context, then keep the assumptions consistent as the model was assembled. We relied on public trade statistics portals for import and export trends, telecom and digital access indicators from bodies such as ITU and the World Bank, and consumer spending signals from agencies such as the US BEA and Eurostat.

We also reviewed product and standards references, including Bluetooth specifications and battery transport safety rules, since these can explain timing of design shifts and replacement cycles. Company filings, investor presentations, and reputable press were used to understand product mix changes like true wireless adoption and noise canceling penetration. Where needed, a paid subscription focused on company financials and a patent database helped cross-check revenue exposure and innovation intensity. The sources named here are illustrative, and we also used other public references to complete data collection, validation, and targeted clarification.

Primary Interviews and Surveys

Primary work focused on validating what drives units, pricing, and mix, since these shift quickly with promotions and product launches. We spoke with participants across brand owners, contract manufacturers, distributors, and large channel partners, and aligned regional assumptions for APAC, EMEA, and the Americas.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 13% | APAC: 45% |

| Mid tier: 58% | Functional/Unit leaders: 31% | EMEA: 33% |

| Smaller Players: 14% | Managers: 56% | Americas: 22% |

Market-Sizing & Forecasting

The core model starts with a top-down build where consumer electronics demand signals and trade flow direction are used to reconstruct the addressable device pool by region, and then value is derived using a practical price ladder. To keep it grounded, we also corroborated totals using selective bottom-up approximations, such as sampled brand and channel revenue checks, along with unit and ASP sanity tests for a few representative product clusters.

Inputs that mattered most included smartphone installed base and upgrade cycles, true wireless share within total shipments, active noise canceling penetration, average selling price movement by connectivity type, and regional online versus offline mix (which changes promo intensity). For forecasting, scenario analysis was applied because replacement behavior, price compression, and feature adoption do not move in a straight line. When gaps appeared in the bottom-up checks, we handled them through conservative range bounding, then returned to interview contacts to confirm whether the missing value sat in low-cost wired models or premium wireless products.

Data Validation & Update Cycle

Validation is done by comparing outputs with independent signals, like shipment direction, regional trade consistency, and whether implied pricing aligns with observed retail positioning. Outliers are flagged, and the drivers are re-checked before a senior review is completed and the final numbers are signed off.

The study is refreshed annually, and we also run interim checks when material events occur, such as major product refresh cycles, tariff shifts, or large channel inventory corrections. Before delivery, a fresh analyst pass is completed so clients receive the latest updated view based on the newest public data and interview feedback.

Mordor Intelligence's Earphones and Headphones Market Size Versus Other Published Estimates

Published market values for earphones and headphones can vary widely because firms set different product boundaries, pick different base years, and treat pricing and currency timing in their own ways. Differences also show up when some studies lean heavily on shipment narratives, while others anchor on spending or brand revenue, which shifts the total in opposite directions.

By tracking true wireless and wired mix, and refreshing regional ASP ladders with channel and promotion checks, Mordor Intelligence keeps the sizing tied to finished earphones and headphones at first commercial sale, excluding hearing aids and mixed reality headsets that can widen totals.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 29.22 B (2026) | |

| Trade Publisher A | USD 26.00 B (2023) | Uses an earlier base year and a different time window, so later mix shifts like TWS adoption and premium feature uptake are not carried forward in the same way when aligning to 2026. |

| Industry Research Outlet B | USD 34.70 B (2023) | Often applies stronger forward pricing and feature adoption assumptions across regions, and the scope wording can allow adjacent wearable audio products to be counted, which can lift the total. |

Taken together, the spread is mainly explained by year alignment, what gets counted as part of the device market, and how pricing is carried forward as wireless and noise canceling mix expands. Our approach stays repeatable because each step ties back to clear unit, mix, and price inputs that can be re-checked when the market changes.

Key Questions Answered in the Report

What is the current valuation of the earphones and headphones market?

The earphones and headphones market size stands at USD 29.22 billion in 2026 and is projected to reach USD 44.71 billion by 2031.

Which region is expanding the fastest?

Asia Pacific is forecast to grow at a 10.7% CAGR between 2026 and 2031, fueled by middle-class expansion and aggressive pricing from local brands.

What technology trend is most influencing premium models?

AI-enabled adaptive noise-cancellation and spatial-audio integration are the leading differentiators in flagship earphones and headphones.

How are EU regulations affecting product design?

The EU common-charger directive and battery-waste rules compel manufacturers to adopt USB-C ports and design for easier battery removal, increasing compliance costs.

Which price tier shows the highest growth potential?

The above-USD 300 premium segment is expected to advance at a 12% CAGR through 2031 thanks to consumer demand for advanced features and ecosystem connectivity.

Why are open-ear designs gaining traction?

Gen-Z fitness trends emphasize safety and awareness during outdoor activities, driving a 9.7% CAGR for bone-conduction and other open-ear formats.

Page last updated on: