Mining Dump Truck Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 32.59 Billion |

| Market Size (2031) | USD 42.43 Billion |

| Growth Rate (2026 - 2031) | 5.42% CAGR |

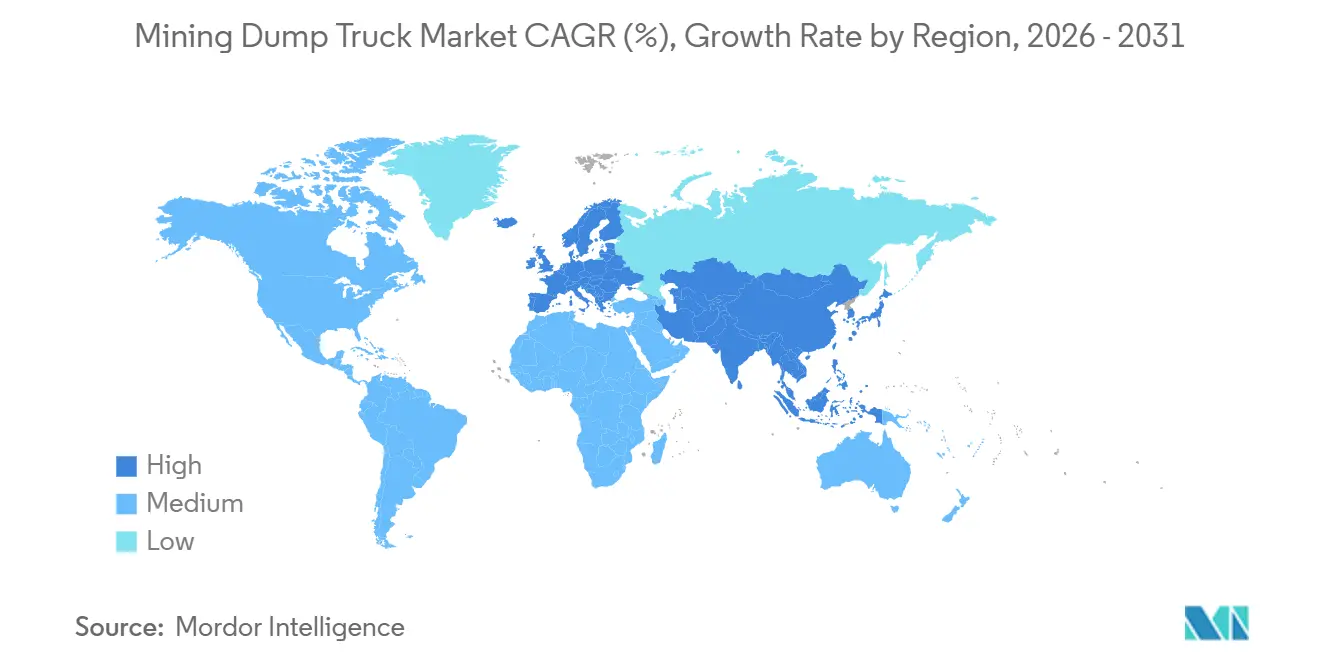

| Fastest Growing Market | Europe |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Mining Dump Truck Market Analysis by Mordor Intelligence

The mining dump truck market size is projected to expand from USD 30.91 billion in 2025 and USD 32.59 billion in 2026 to USD 42.43 billion by 2031, registering a CAGR of 5.42% between 2026 and 2031. Demand momentum reflects operators’ emphasis on cost-per-ton productivity, compliance with tightening emission rules, and the rapid shift toward autonomous haulage ecosystems. Rigid rear-dump platforms dominate long-haul ore movements, yet autonomous configurations are changing fleet economics as mines in Australia, Chile, and Canada move past pilot scale. Electrification remains early-stage but is gaining pace as carbon-credit monetization lowers ownership costs and as pay-per-ton contracts shift residual-value risk to original equipment manufacturers. Competitive dynamics are intensifying because Chinese brands are underwriting 20-30% list-price discounts in Southeast Asian coal and African copper projects, pressuring incumbent original equipment manufacturers to bundle software, financing, and aftermarket services.

Key Report Takeaways

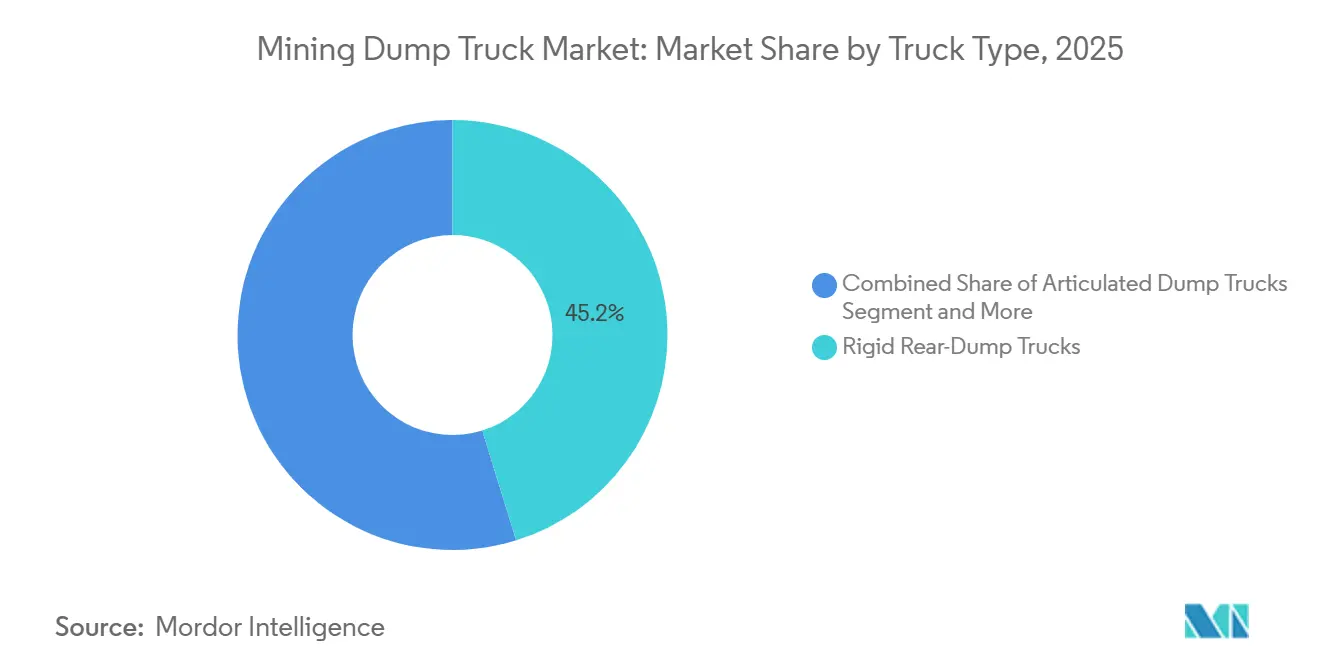

- By truck type, rigid rear-dump trucks accounted for 45.21% of the mining dump truck market share in 2025, while autonomous platforms are projected to advance at a 10.39% CAGR through 2031.

- By fuel/propulsion type, diesel propulsion retained 71.29% of the mining dump truck market share in 2025; battery-electric trucks recorded the fastest growth at a 10.52% CAGR.

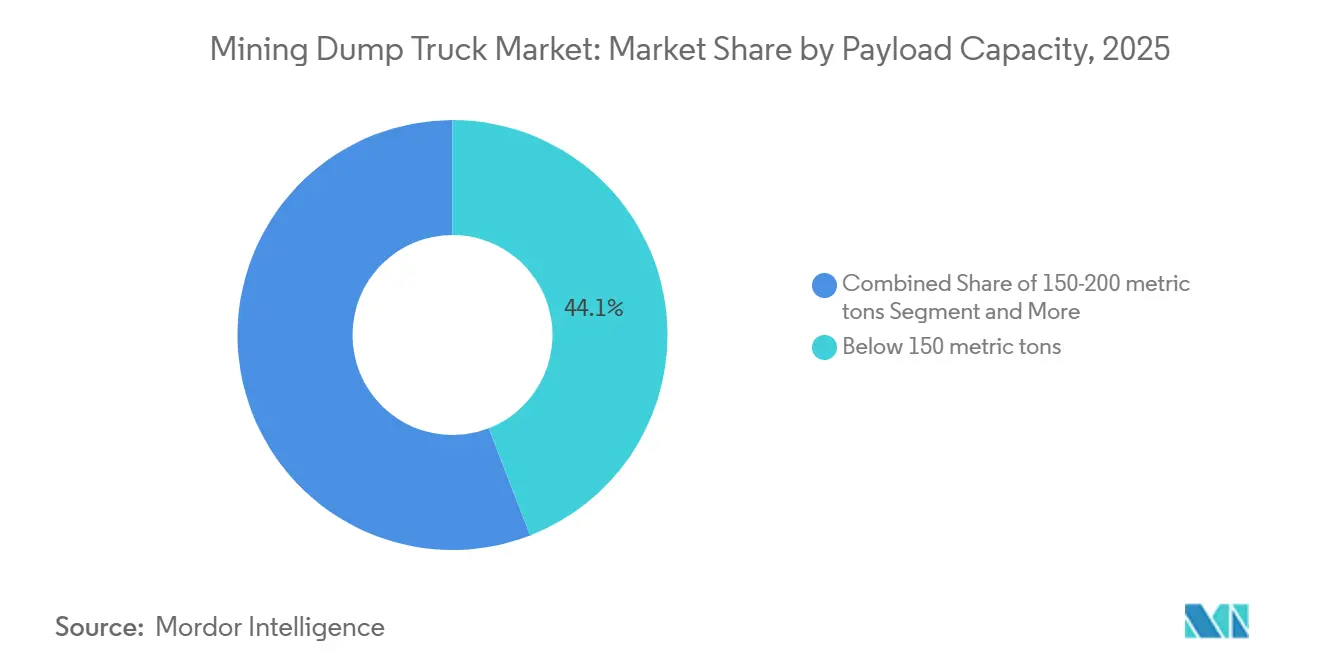

- By payload capacity, trucks below 150 metric tons led the mining dump truck market with 44.11% market share in 2025, whereas ultra-class units above 330 metric tons are forecast to expand at a 7.45% CAGR.

- By application, open-pit metal mining accounted for 56.34% of demand in 2025 and is set to register the highest growth at a 6.04% CAGR to 2031.

- By geography, Asia-Pacific commanded 58.26% of the 2025 volume, yet Europe posts the fastest regional expansion at 6.35% CAGR as Stage-V rules trigger fleet renewal.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Mining Dump Truck Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact On CAGR | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tightening Emission Norms | +1.2% | Global with Europe, North America leading | Short term (≤2 years) |

| Autonomous Haulage Systems | +0.9% | Global; key sites in Australia, Chile | Medium term (2-4 years) |

| Surface Mine Output Expansion | +0.8% | Asia-Pacific Core; spillover to Australia | Medium term (2-4 years) |

| Mine-To-Mill Optimization | +0.7% | Global; early adoption in North America, Australia | Long term (≥4 years) |

| Pay-Per-Ton Leasing Models | +0.6% | Global; focus on emerging regions | Medium term (2-4 years) |

| Carbon Credit Monetization | +0.5% | Europe, North America, Australia | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Tightening Tier-4 and Stage-V Emission Norms Drive Fleet Renewal

The European Union's Stage V regulations mandate a significant reduction in particulate emissions compared to the Tier 4 Final standard [1]“Stage V Non-Road Engine Standards,”, European Commission, europa.eu. This push has hastened the replacement of older diesel trucks, steering preferences towards models equipped with selective catalytic reduction systems. Australian states have tied mine permit renewals to fleet upgrades, contingent on audit verification. This move has spurred orders for compliant units, even with a notable price premium. While larger mining companies easily absorb these added costs, mid-tier operators in Africa and Southeast Asia are extending the lives of their fleets, leading to a noticeable performance disparity. Caterpillar's bookings reveal a significant increase in the adoption of Stage-V engines in European trucks compared to earlier levels.

Autonomous Haulage Proven to Raise Payload-km Productivity

Komatsu's Pilbara FrontRunner fleet has achieved significant milestones, maintaining a record of zero lost-time injuries [2]“Autonomous Haulage System Deployment Statistics 2025,” Komatsu Ltd., komatsu.com. This accomplishment has enhanced its utilization efficiency compared to traditional manual fleets. Meanwhile, Rio Tinto's autonomous fleet has successfully increased throughput without incurring additional haul-road capital expenses. In Chile, Codelco is implementing Caterpillar Command at its Chuquicamata site to reduce labor costs and address challenges such as high-altitude fatigue. Trucks with higher capacities are experiencing the most notable productivity improvements by optimizing engine loads, which also contributes to reduced fuel consumption.

Expansion of Surface-Mine Output in Asia-Pacific

Indonesia has significantly increased its nickel production, driving demand for a substantial number of new heavy trucks. Coal India has outlined plans for incremental capacity expansion, creating a need for additional trucks in key regions such as Jharkhand and Odisha. In the year leading up to March 2025, Western Australia saw iron ore exports reach 889 million tons, marking a 1.6% increase from the previous year[3]"Western Australia Iron Ore Profile", Western Australian Treasury Corporation,watc.wa.gov.au. In Inner Mongolia and Xinjiang, Chinese surface coal production has captured a major share of the country's incremental domestic output, leading to increased orders for rigid truck models from local original equipment manufacturers. These trucks, designed for optimal engine loading, improve fuel efficiency.

Mine-to-Mill Optimization Linking Payload Data to Mill Throughput

Sandvik's OptiMine connects truck load-cells to plant controls across multiple mines, enhancing mill feed consistency and improving throughput without requiring additional crushing capacity. Anglo American leverages Modular Mining's DISPATCH to optimize grade stream prioritization, significantly increasing operational efficiency. Procurement criteria now emphasize sensor fidelity and data latency, favoring original equipment manufacturers with advanced telematics platforms such as Cat MineStar and Komatsu.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Upfront Capex and Long Payback | −0.4% | Global; pronounced in emerging regions | Short term (≤2 years) |

| Commodity Price Volatility and Delays | −0.3% | Global; exploration-stage projects | Medium term (2-4 years) |

| Weak Grid Capacity and Electrification | −0.2% | Remote mining areas worldwide | Medium term (2-4 years) |

| Li-ion Supply Chain Risk | −0.2% | Global; battery-electric adopters | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

High Upfront Capex and Long Payback Cycles

Ultra-class units are high-cost investments that typically require extended recovery periods, creating challenges for mines in regions with higher borrowing costs than in other areas with more favorable rates. Battery-electric models, such as the Komatsu 930E-5SE, are significantly more expensive than their diesel counterparts, further complicating adoption. To manage financial constraints, many operators in regions such as Indonesia and Zambia choose to rebuild their existing fleets, thereby extending their operational lifespan. While this approach compromises fuel efficiency, it helps defer substantial expenditures. Additionally, declining ore grades exacerbate operational challenges, requiring greater material movement to maintain refined copper production levels.

Commodity-Price Volatility Delaying Green-Field Mines

A decline in copper prices led to the postponement of several projects, significantly impacting production capacity. Similarly, a sharp drop in lithium carbonate prices disrupted operations in Argentine brines, leading to the cancellation of truck orders. In Indonesia, falling coal prices led producers to idle a substantial portion of their annual capacity and to delay equipment procurement from local vendors. Additionally, fluctuations in iron ore prices prompted operators in Pilbara to prioritize brownfield debottlenecking over large-scale autonomous technology rollouts.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Truck Type: Autonomous Systems Reshape Traditional Haulage

Autonomous-ready units are the fastest-growing segment of the mining dump truck market, with a 10.39% CAGR over 2026-2031. Rigid rear-dump trucks still capture the lion’s share 45.21% in 2025 because haul distances over three kilometers in copper and iron-ore pits favor payloads of 200-400 t. Retrofit kits enable legacy diesel fleets to transition to autonomous operations, reducing idle time and improving operational efficiency. Rigid side-dump trucks, however, remain a niche segment, primarily serving steep quarries and underground ribbons, where the risk of rollover limits payload scalability.

Caterpillar's Command system has significantly enhanced availability, contributing to increased operational hours. This improvement is crucial for owner-operators when assessing the market size of mining dump trucks. Australia, Chile, and Canada lead in the adoption of Autonomous Haulage Systems (AHS), supported by stable regulatory frameworks and the presence of long-life ore bodies, which justify the integration costs. While Chinese OEMs currently lag in autonomy software, their licensing agreements with Komatsu indicate potential advancements in the future. Globally, as data analytics and autonomy integrate, procurement decisions are increasingly shifting from focusing solely on upfront costs to prioritizing lifetime productivity value.

By Fuel/Propulsion Type: Electrification Accelerates Despite Diesel Dominance

Diesel maintains a 71.29% share of 2025 demand, yet battery-electric platforms post a brisk 10.52% CAGR through 2031, confirming a slow-burn transition in the mining dump truck market. Diesel has a significant advantage due to its high onboard chemical energy, making refueling more convenient than recharging, particularly in remote areas. Hybrid diesel-electric variants, such as Caterpillar’s 798 AC, are emerging as transitional solutions that reduce fuel consumption and align with existing maintenance practices.

Economic shifts often occur first in regions with carbon pricing or strict particulate regulations. For example, specific policies provide a notable operating-cost advantage for electric trucks, validating their use in particular duty cycles within mining operations. Hydrogen-powered vehicles, such as Anglo American’s nuGen, demonstrate technical feasibility but face challenges in achieving commercial viability due to high costs and uncertainties in green-hydrogen supply. Collaborative efforts between manufacturers are expected to lower battery costs, making electric vehicles more cost-effective than diesel counterparts in regulated regions, thereby driving the adoption of zero-emission options in the mining dump truck market.

By Payload Capacity: Ultra-Class Trucks Gain Share in Declining-Grade Pits

Trucks above 330 t register the strongest 7.45% CAGR by 2031, as declining ore grades in Chile, Peru, and Western Australia require more material to be moved per unit of metal. Sub-150 t models still dominate unit sales with 44.11% share in 2025, supported by aggregates, infrastructure, and small-scale metals operations that emphasize agility and lower capex. In the realm of large iron-ore and copper pits, the 201-330 t class stands out as the preferred choice, adeptly balancing shovel compatibility with haul-road standards.

BelAZ’s 75710 boasts an impressive payload-to-weight ratio, significantly reducing truck cycles compared to standard models and enhancing site energy efficiency. Yet, the adoption of these trucks faces hurdles: braking regulations necessitate retarder upgrades for larger trucks. Additionally, haul-road reinforcements pose challenges, particularly outside of new greenfield layouts. Still, metrics from mine-to-mill integrations reveal that ultra-class trucks can substantially lower the cost per ton-kilometer on longer routes, bolstering their foothold in the mining dump truck market.

By Application: Metal Mining Drives Demand Amid Energy Transition

Open-pit metal mining accounted for 56.34% of 2025 demand and is projected to grow at a 6.04% CAGR through 2031, reinforcing its anchor position in the mining dump truck market share hierarchy. Copper expansions at Codelco and Las Bambas require continuous fleet additions, while DRC cobalt projects pivot to 220-300 t trucks with autonomous retrofits as standard specification. Despite coal’s share, energy transition policies signal a gradual contraction, particularly in Indonesia, where annual production declines are forecast through 2031.

Quarrying and aggregates, growing at a notable CAGR, benefit from India’s highway drive and Middle East megaprojects such as NEOM. Articulated platforms with 40-50 t payloads dominate this niche because they navigate soft underfoot conditions without permanent haul-roads. Lithium brine operations on Argentine salt flats prefer smaller 100-150 t units to protect fragile terrain, adding diversity to fleet composition. Ultra-class trucks remain the preserve of copper, iron-ore, and gold mega-pits where economies of scale justify the capital envelope.

Geography Analysis

Asia-Pacific accounted for 58.26% of 2025 shipments, as Indonesia, India, and Australia executed significant surface-mine expansions. Indonesian nickel production has grown significantly, driving the need for additional trucks. Coal India’s mechanization strategy emphasizes the deployment of new units to enhance operational efficiency. Australia has strengthened its iron-ore operations by incorporating autonomous rigs, highlighting its commitment to a technology-driven approach in the mining dump truck market.

South America accounted for a significant share of volume and is expanding at a notable CAGR. Chile leads copper investment cycles, and Peru’s Las Bambas ramp-up underwrites continuous orders for Komatsu 930E units. Brazil's Vale transitioned several trucks at Carajás to autonomous operation, achieving significant utilization gains and substantial annual labor savings. However, volatility in copper prices temporarily stalled multiple greenfield projects, highlighting the region's sensitivity to spot price fluctuations.

Europe, despite holding a modest market share, is expected to have the fastest growth rate, with a 6.35% CAGR by 2031. This growth is driven by stringent compliance requirements, which are accelerating the turnover of quarry and aggregate fleets. Quarries in Germany have been upgrading to advanced models, while the United Kingdom's planned diesel phase-out for non-road machinery is encouraging early adoption of battery-electric trucks. Additionally, off-road hydrogen initiatives in Scandinavia are expected to scale in the near future. North America, with a smaller market share, is leveraging Canadian oil sands and U.S. copper restarts for steady growth, supported by advancements in autonomous regulations.

Competitive Landscape

The market structure exhibits moderate concentration. Caterpillar, utilizing its MineStar platform, integrates haulage, predictive maintenance, and analytics, thereby strengthening customer loyalty to its flagship series. Komatsu's acquisition of GHH broadens its underground reach and positions it as a global leader in installed autonomous equipment. Liebherr is emphasizing modular autonomy kits and collaborating on open protocol interfaces to seamlessly integrate its trucks into diverse OEM fleets.

As competitive dynamics evolve, the focus shifts from unit pricing to lifetime services and software subscriptions. Suppliers are enticing miners with outcome-based contracts that ensure they meet specific cost-per-ton targets. Meanwhile, Chinese companies XCMG and Sany are strategically underbidding on tenders in emerging markets, all while advancing the certification of engines for sales in developed regions.

Innovation is pivoting towards retrofit electrification, lithium-ion recycling, and cloud-driven optimization, transforming truck data into actionable mining strategies. Equipment vendors, in pursuit of comprehensive solutions, are forging alliances with energy giants and grid experts. This shift underscores a broader trend: the mining dump truck market is transitioning its value capture from mere hardware profits to an expansive, integrated ecosystem.

Mining Dump Truck Industry Leaders

-

Caterpillar Inc.

-

Komatsu Ltd.

-

Hitachi Construction Machinery Co., Ltd.

-

BelAZ

-

Volvo Construction Equipment

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: In Beijing, XCMG and Fortescue inked a pivotal agreement, spotlighting their commitment to green mining solutions. XCMG Construction Machinery Co., Ltd. and Fortescue sealed a deal for cutting-edge energy-efficient mining equipment. Between 2028 and 2030, XCMG is set to deliver 150 to 200 units of its 240T battery-electric haul trucks to Fortescue. This deal is China's most significant export order in the field of green mining machinery.

- April 2025: At its Pune facility, SANY India unveiled India's inaugural locally-produced hybrid mining dump truck. The SKT130S, boasting a capacity of 100 tons, marks a pivotal advancement in the nation's mining equipment manufacturing landscape.

Global Mining Dump Truck Market Report Scope

The scope includes segmentation by truck type (rigid rear-dump trucks, rigid side-dump trucks, articulated dump trucks, bottom/belly dump trucks, and autonomous dump trucks (AHS-ready)), fuel/propulsion type (internal-combustion (diesel), hybrid (diesel-electric), battery-electric, and hydrogen fuel-cell), payload capacity (below 150 metric tons, 150-200 metric tons, 201-330 metric tons, and above 330 metric tons), application (open-pit metal mining, coal and lignite mining, quarrying and aggregates, and major infrastructure construction). The analysis also covers regional-level segmentation, including North America, South America, Europe, Asia-Pacific, and the Middle East and Africa. Market size and growth forecasts are presented by value in USD and by volume in units.

| Rigid Rear-Dump Trucks |

| Rigid Side-Dump Trucks |

| Articulated Dump Trucks |

| Bottom/Belly Dump Trucks |

| Autonomous Dump Trucks (AHS-ready) |

| Internal-Combustion (Diesel) |

| Hybrid (Diesel-Electric) |

| Battery-Electric |

| Hydrogen Fuel-Cell |

| Below 150 metric tons |

| 150-200 metric tons |

| 201-330 metric tons |

| Above 330 metric tons |

| Open-pit Metal Mining |

| Coal and Lignite Mining |

| Quarrying and Aggregates |

| Major Infrastructure Construction |

| North America | United States |

| Canada | |

| Rest of North America | |

| South America | Brazil |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Australia | |

| Indonesia | |

| Rest of Asia-Pacific | |

| Middle East and Africa | United Arab Emirates |

| Saudi Arabia | |

| Turkey | |

| Egypt | |

| South Africa | |

| Rest of Middle East and Africa |

| By Truck Type | Rigid Rear-Dump Trucks | |

| Rigid Side-Dump Trucks | ||

| Articulated Dump Trucks | ||

| Bottom/Belly Dump Trucks | ||

| Autonomous Dump Trucks (AHS-ready) | ||

| By Fuel/Propulsion Type | Internal-Combustion (Diesel) | |

| Hybrid (Diesel-Electric) | ||

| Battery-Electric | ||

| Hydrogen Fuel-Cell | ||

| By Payload Capacity | Below 150 metric tons | |

| 150-200 metric tons | ||

| 201-330 metric tons | ||

| Above 330 metric tons | ||

| By Application | Open-pit Metal Mining | |

| Coal and Lignite Mining | ||

| Quarrying and Aggregates | ||

| Major Infrastructure Construction | ||

| By Geography | North America | United States |

| Canada | ||

| Rest of North America | ||

| South America | Brazil | |

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Australia | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | United Arab Emirates | |

| Saudi Arabia | ||

| Turkey | ||

| Egypt | ||

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value of the Mining dump truck market by 2031?

It is forecast to reach USD 42.43 billion, expanding at a 5.42% CAGR from 2026 to 2031.

Which truck type is growing fastest through 2031?

Autonomous-ready dump trucks are advancing at a 10.39% CAGR as mines seek higher payload-kilometer efficiency.

What factors hinder full electrification of mining haulage?

Limited grid capacity at remote sites and high battery-pack costs tie up capital and delay widespread battery-electric adoption.

How do pay-per-ton contracts change fleet economics?

They transfer residual-value risk to OEMs and align costs with production volumes, lowering entry barriers for ultra-class equipment.

How large is Asia-Pacific’s stake in current demand?

The region accounted for 58.26% of 2025 global shipments driven by expansions in Indonesia, India, and Australia.

Page last updated on: