Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 18.37 Billion |

| Market Size (2031) | USD 24.18 Billion |

| Growth Rate (2026 - 2031) | 5.65% CAGR |

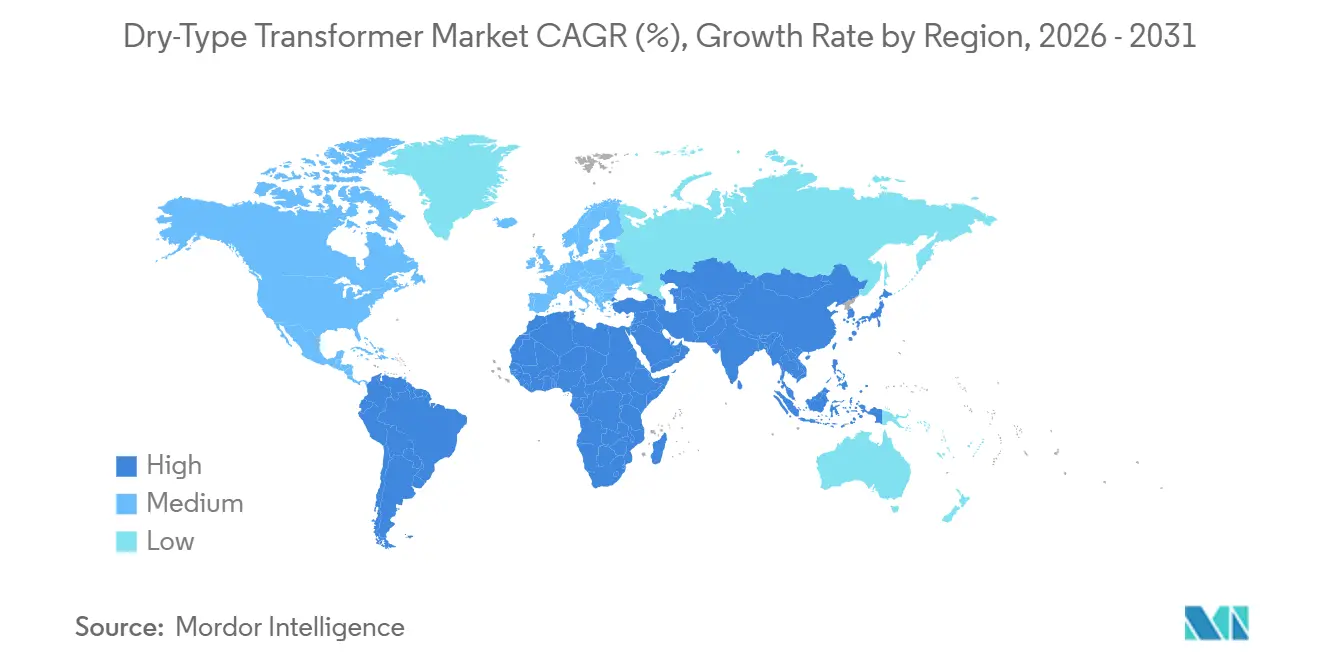

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

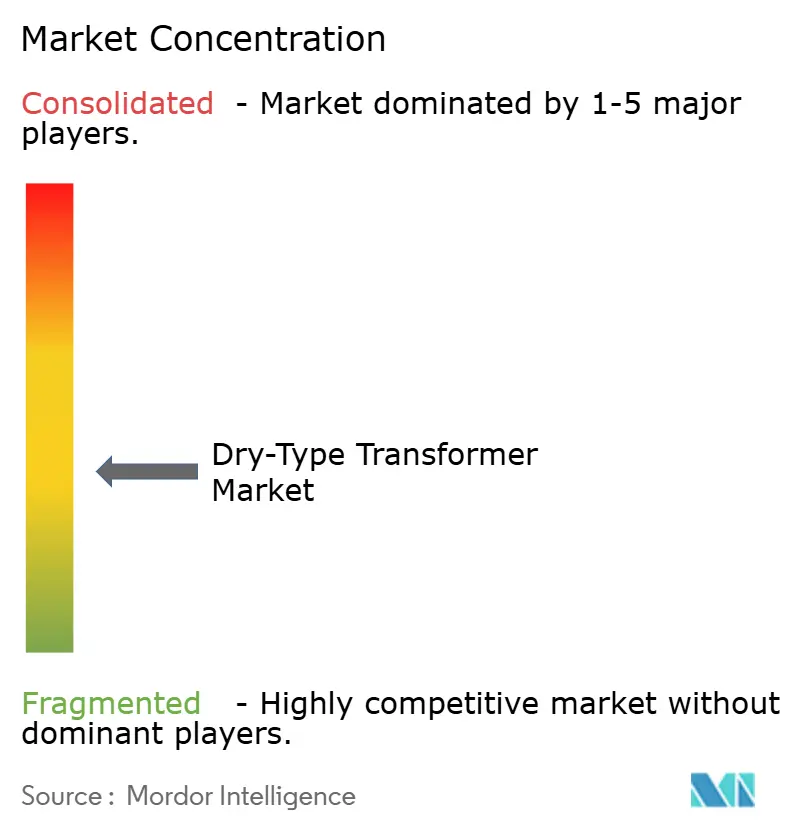

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dry-Type Transformer Market Analysis by Mordor Intelligence

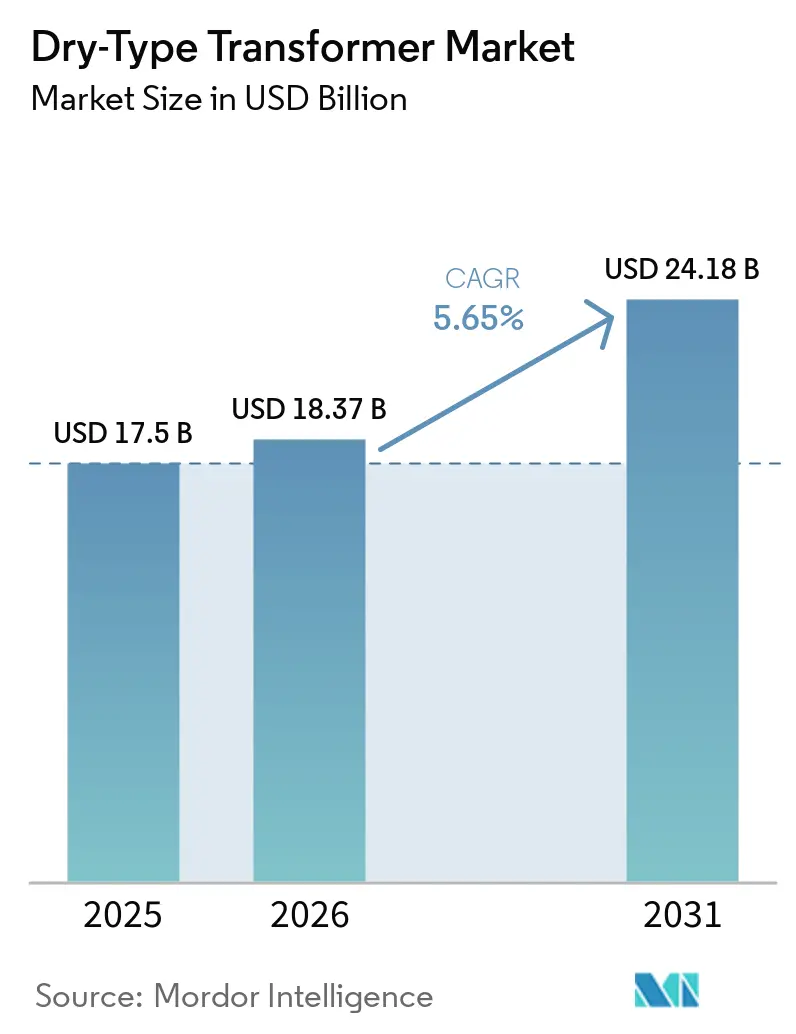

The Dry-Type Transformer Market size is expected to grow from USD 17.5 billion in 2025 to USD 18.37 billion in 2026 and is forecast to reach USD 24.18 billion by 2031 at 5.65% CAGR over 2026-2031.

Demand centers on fire-safe, oil-free installations across data centers, renewable plants, and grid-edge substations, where building codes and environmental rules increasingly prohibit liquid-immersed equipment. Small ratings below 10 MVA dominate today, yet air-forced cooling and AI-enabled monitoring are capturing share as operators seek higher thermal headroom and predictive maintenance. Asia-Pacific retains cost leadership through local incentive schemes, while North America’s Inflation Reduction Act and the European Union’s REPowerEU plan accelerate domestic replacement cycles. Suppliers that pair amorphous-core technology with digital twins are gaining pricing power as total-cost-of-ownership models replace upfront-capex bidding.

Key Report Takeaways

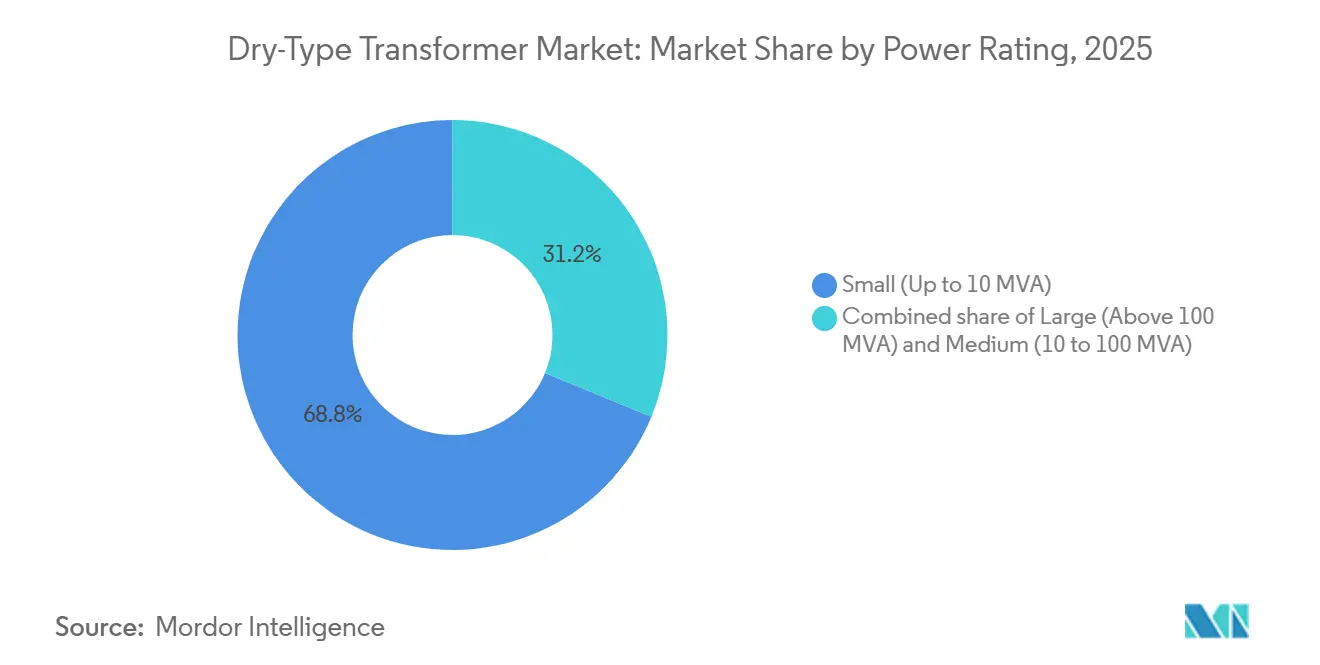

- By power rating, small transformers, up to 10 MVA, held 68.8% of the dry-type transformer market share in 2025 and are projected to expand at an 8.6% CAGR through 2031.

- By cooling method, air-forced units are expected to post the fastest 8.9% CAGR from 2026 to 2031, even as air-natural systems retain a 70.7% revenue share across the dry-type transformers market.

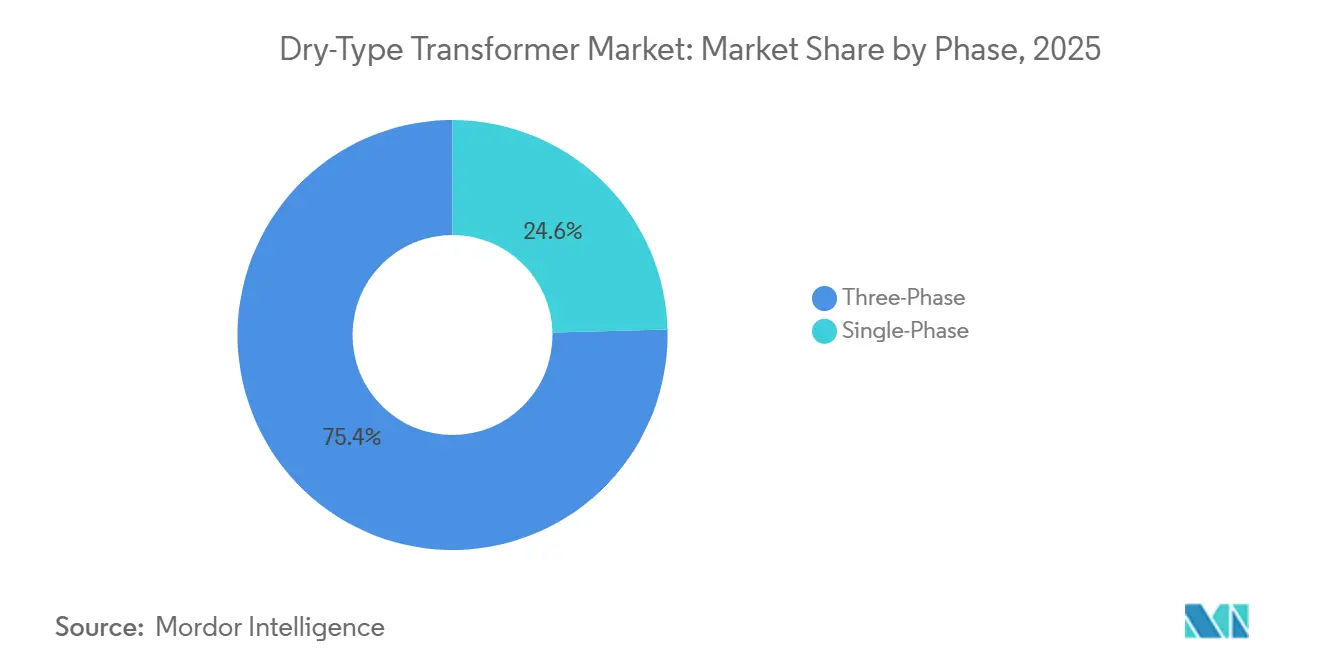

- By phase, three-phase configurations accounted for 75.4% of 2025 shipments, while three-phase demand is projected to grow at a 6.1% CAGR through 2031 within the dry-type transformers market.

- By transformer type, distribution units represented 72.9% of the dry-type transformer market size in 2025 and are expected to grow at a 7.8% CAGR, driven by grid modernization spending.

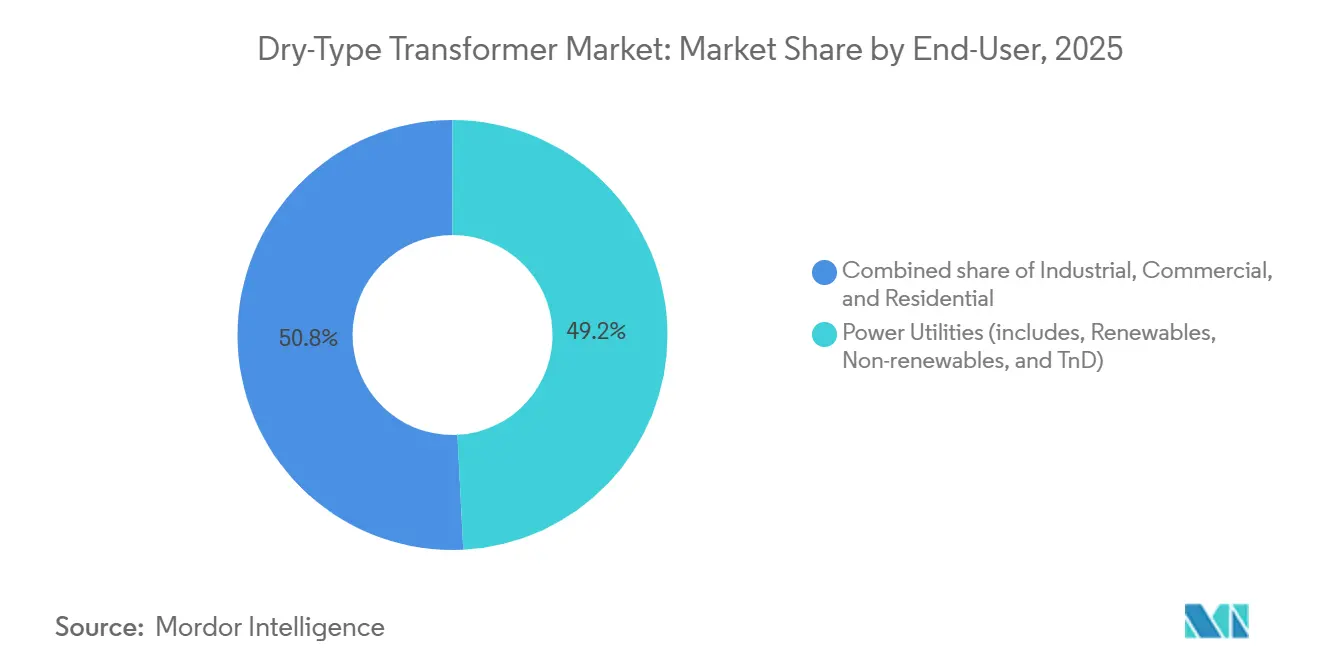

- By end-user, the industrial segment are expected to grow at an 8.2% CAGR, while power utilities held 49.2%.

- By geography, the Asia-Pacific region commanded a 48.1% revenue share in 2025 and is expected to grow at a CAGR of 6.7% from 2026 to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dry-Type Transformer Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Increasing grid-edge medium-voltage replacements | 1.2% | Global, with concentration in North America, Europe, and developed APAC markets | Long term (≥ 4 years) |

| Surge in renewable-tied pad-mounted installations | 1.5% | Global, led by APAC (China, India solar/wind), Europe (offshore wind), and North America (utility-scale solar) | Medium term (2-4 years) |

| Data-center fire-safety mandates favouring oil-free units | 1.3% | North America & Europe (hyperscale hubs), emerging in APAC (Singapore, Tokyo, Mumbai) | Short term (≤ 2 years) |

| Electrification of offshore platforms (EPCI push) | 0.8% | Europe (North Sea), Middle East (Gulf oil & gas), Southeast Asia (Malaysia, Indonesia) | Medium term (2-4 years) |

| AI-enabled remote condition monitoring | 0.6% | Global, with early adoption in North America and Europe utility sectors, expanding to APAC | Medium term (2-4 years) |

| Polymer soft-magnetic composite cores lowering no-load loss | 0.5% | North America and Europe (driven by DOE 2029 efficiency mandates), gradual APAC adoption | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Increasing Grid-Edge Medium-Voltage Replacements

Half of North America’s distribution-transformer fleet now exceeds 33 years in service, driving a replacement wave that favors dry-type units in wildfire-prone regions.[1]National Renewable Energy Laboratory, “Distribution Grid Expansion Needs,” nrel.gov Utilities are pairing transformers with battery storage and solar inverters, demanding K-factor designs above 13 to handle harmonic-rich loads. Pad-mounted configurations cut installation costs by 15-20% because they eliminate oil-containment vaults, and California regulators are accelerating adoption through stringent wildfire-mitigation mandates. Globally, the resulting volume supports economies of scale that lower per-kVA pricing and widen the addressable dry-type transformers market. Suppliers integrating sensors for harmonic distortion and temperature are capturing premium margins as utilities pivot toward condition-based maintenance.

Surge in Renewable-Tied Pad-Mounted Installations

Global renewable capacity additions are forecast to create cumulative step-up demand of 2 TW by 2050. Dry-type pad-mounted units sidestep costly spill-containment berms, shaving up to 12 weeks from construction schedules in environmentally sensitive zones. Offshore wind developers are standardizing IP56-rated cast-coil designs that withstand salt spray, while integrated energy-storage projects require bidirectional transformers capable of cyclical charge-discharge regimes. Product launches such as Eaton’s Envirotran series underscore the shift, and the trend lifts both unit volume and average selling price, reinforcing a robust growth outlook for the dry-type transformers market.

Data-Center Fire-Safety Mandates Favoring Oil-Free Units

NFPA 70 and international building codes restrict flammable liquids inside occupied facilities, leading cloud operators to make dry-type transformers the default at 13.8 kV and 34.5 kV service voltages.[2]National Fire Protection Association, “NFPA 70 National Electrical Code,” nfpa.org Rising AI workloads have doubled rack-level heat, forcing hyperscalers to elevate distribution voltage and specify K-factor 20 transformers that tolerate high harmonic distortion. National Electrical Manufacturers Association guidance now prioritizes surge-withstand capability for 25 kA faults. Coupled with growing insurance incentives, these rules propel steady demand growth within the dry-type transformers market.

Electrification of Offshore Platforms

Projects such as ABB’s Oseberg link have proven that shore-powered platforms cut hundreds of thousands of tonnes of CO₂ annually.[3]ABB Ltd., “Oseberg Offshore Electrification Case Study,” abb.com EPCI contractors choose dry-type units for Zone 1 and Zone 2 hazardous areas to eliminate oil-fire risk and reduce maintenance. Subsea power grids in fields like Johan Sverdrup are rating dry-type designs for 3,000-meter depths. As operators pursue offshore wind-to-hydrogen hybrids, transformers must manage variable inputs and electrolyzer loads, expanding functional requirements and sustaining growth momentum for the dry-type transformers market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile copper & epoxy prices | -0.9% | Global, with acute pressure in APAC manufacturing hubs (China, India, South Korea) | Short term (≤ 2 years) |

| Lengthening LV & MV transformer lead-times | -0.7% | Global, most severe in North America and Europe due to GOES supply constraints | Medium term (2-4 years) |

| Thermal derating above 45°C ambient in MENA | -0.4% | Middle East and North Africa (Saudi Arabia, UAE, Egypt, Kuwait), secondary impact in South Asia and Australia | Long term (≥ 4 years) |

| Certification bottlenecks for >72.5 kV dry units | -0.3% | Global, particularly affecting Europe and North America utility projects requiring high-voltage dry-type transformers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Copper & Epoxy Prices

LME copper peaked at USD 11,104.50 per tonne in 2024, lifting material costs for windings that account for up to 40% of a transformer’s bill of materials.[4]London Metal Exchange, “Historical Copper Prices 2024,” lme.com Epoxy resin tracked oil derivatives higher, squeezing margins on cast-coil designs. Manufacturers reduced price-validity windows to 30-45 days and inserted escalation clauses, pushing commodity risk onto end-users. Aluminum windings gained favor for low-voltage coils, trimming weight by 60% yet demanding larger conductors to match conductivity. Smaller Asian vendors without hedging tools faced order cancellations, a drag on the dry-type transformers market in price-sensitive tenders.

Lengthening LV & MV Transformer Lead-Times

Medium-voltage delivery has stretched to 24 months and up to 48 months for 100 MVA units because only a handful of mills can supply premium grain-oriented steel. OEMs now lock multi-year offtake contracts and build inventory buffers, tying up working capital. Utilities refurbish retired units or lease mobile substations, but those stop-gaps only temper the impact. Capacity expansions, like Hitachi Energy’s USD 4.5 billion program, add slitting lines and amorphous-metal ribbon production. Lead-time uncertainty, therefore, caps near-term growth in the dry-type transformers market until new supply materializes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power Rating: Small Units Anchor Distributed Grid

Small ratings up to 10 MVA accounted for 68.8% of the dry-type transformers market share in 2025. They are projected to grow at 8.6% as rooftop solar, EV-charging hubs, and battery storage expand. The dry-type transformers market size for this class is forecast at USD 16.7 billion by 2031. Medium-power units between 10 MVA and 100 MVA follow with modest uptake in university campuses and industrial complexes, increasingly specified with on-load tap changers for renewable intermittency.

Containerized data-center modules favor 2-5 MVA dry-type blocks, cutting on-site work from 12 weeks to three. Large-MVA step-up requirements remain niche because oil-immersed cooling still delivers better thermal economics at the 400 MVA level. Upcoming U.S. efficiency rules mandate amorphous-core adoption in small distribution units, temporarily inflating capex but improving lifecycle cost, reinforcing momentum in the dry-type transformers market.

By Cooling Method: Air-Forced Systems Gain Thermal Edge

Air-natural designs held 70.7% share in 2025, thanks to simplicity and silent operation. Yet air-forced cooling is advancing at 8.9% CAGR as data-center and industrial retrofits demand higher power density. Variable-speed fans controlled by embedded processors cut auxiliary draw by 50% versus fixed-speed models. Water-forced alternatives surface in Saudi Arabia and Abu Dhabi, where 45 °C ambient temperatures erode air-cooling efficiency; despite niche adoption, their higher price lifts the overall dry-type transformers market size.

Asia-Pacific leads air-forced uptake given land constraints in cities like Singapore and Mumbai. Meanwhile, air-natural retains a foothold in hospitals and schools that require low acoustic profiles.

By Phase: Three-Phase Configurations Dominate Industrial Loads

Three-phase technology captured 75.4% share in 2025 and is growing at 6.1% CAGR through 2031. Material savings, about 15% less core steel and copper than three single-phase units, support preference among utilities to standardize pad-mounted gear for new subdivisions. IEC 61850 compliance further drives three-phase adoption as utilities embed Ethernet switches and sensors for real-time diagnostics.

Single-phase units regain relevance in off-grid solar and remote microgrids, allowing independent phase optimization and simpler inverter design. EV fast-charging corridors that run on 480 V three-phase feeds will continue to reinforce demand for three-phase dry-type installations, sustaining growth in the broader dry-type transformers market.

By Transformer Type: Distribution Leads Volume, Power Units Scale in Renewables

Distribution transformers delivered 72.9% of 2025 revenue and are forecast to expand at 7.8% CAGR, mirroring urbanization and commercial densification. The dry-type transformers market size for distribution equipment is set to top USD 17 billion by 2031. Power transformers from 10 MVA to 100 MVA are growing in solar and wind projects that avoid oil-filled alternatives to simplify permitting.

The U.S. Infrastructure Investment and Jobs Act earmarks USD 65 billion for distribution-grid upgrades, creating a steady replacement funnel. IEC 60076-16 testing costs still slow adoption above 72.5 kV, though modular testing protocols promise to ease the burden and unlock future dry-type transformers market growth.

By End-User: Industrial Segment Outpaces Utilities in Growth

Power utilities held 49.2% of 2025 sales, but industrial facilities are expanding at 8.2% as fabs and battery gigafactories seek harmonic-tolerant, low-inrush transformers. Cloud operators, airports, and hospitals value fire safety and operational continuity, turning to cast-coil units with embedded partial-discharge detectors.

Utilities increasingly procure transformers packaged with cloud analytics that predict failures 6-12 months ahead, extending asset life and optimizing capex. Energy-as-a-service models in commercial real estate further stimulate dry-type transformers market penetration by converting equipment purchase into opex contracts.

Geography Analysis

Asia-Pacific led global revenue with 48.1% share in 2025 and is forecast to grow at 6.7% CAGR. China’s State Grid is adding more than 200 GW of renewable capacity annually, each gigawatt requiring dozens of dry-type step-up units, while India’s Production-Linked Incentive scheme subsidizes local transformer output. Earthquake-resistant versions in Japan and South Korea use flexible bushings to meet seismic codes, underscoring regional customization within the dry-type transformers market.

North America ranks second in size but posts the fastest growth, buoyed by USD 369 billion in Inflation Reduction Act spending and USD 65 billion in infrastructure funding. California utilities specify dry-type units in wildfire corridors, and coastal operators replace oil-filled gear vulnerable to storm-surge contamination. Growing data-center clusters in Virginia and Texas drive further demand for harmonic-rated, fire-safe transformers.

Europe’s REPowerEU initiative accelerates offshore wind deployment. Dry-type transformers step up 66 kV cables to 220 kV shoreside grids, sidestepping oil-spill risks. The Middle East and Africa confront thermal derating penalties above 45 °C; water-forced cooling mitigates the issue, albeit at 30% capital cost premiums. Brazil and Chile anchor Latin American growth through hydro-solar hybrids needing dry-type step-ups. Collectively, these dynamics reinforce a geographically diverse dry-type transformers market.

Competitive Landscape

The top five suppliers, ABB, Siemens Energy, Hitachi Energy, Eaton, and Schneider Electric, control around 40-45% of global revenue, signifying moderate concentration. Vertical integration into amorphous-core ribbon and GOES slitting now separates leaders from regional players such as CG Power, TBEA, LS Electric, and WEG, which leverage cost advantages for local tenders. Hitachi Energy’s USD 4.5 billion capacity build-out adds plants in India, the United States, and Europe to satisfy domestic-content clauses.

Digital twins embedded through ABB Ability and Hitachi Lumada command premium service fees, transforming one-off hardware sales into recurring software revenue. Modular, factory-assembled e-houses from Eaton and Schneider cut installation time by 75%, appealing to data-center and mining projects. Chinese entrants, aided by Belt and Road financing, undercut Western pricing by up to 30%, but concerns over long-term service support limit penetration in Tier-1 utilities.

White-space opportunities abound in sub-10 MVA microgrid transformers, ultra-high-voltage dry-type designs above 72.5 kV, and water-forced cooling for desert climates. Suppliers able to bundle these hardware niches with predictive analytics and maintenance services are poised to capture incremental dry-type transformers market share.

Dry-Type Transformer Industry Leaders

ABB Ltd.

Siemens AG

Schneider Electric SE

Eaton Corporation plc

Hammond Power Solutions Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2026: Fuji Electric Co., Ltd. introduced a compact and lightweight cast resin dry-type transformer designed for Southeast Asia and global markets. The product aims to minimize installation space requirements, catering to data centers, semiconductor facilities, and renewable energy infrastructure.

- September 2025: Hitachi Energy has announced a USD 1 billion investment in U.S. manufacturing to support grid modernization. This investment includes the expansion of transformer production infrastructure, which is expected to indirectly improve the availability of dry-type transformers through increased capacity and technological advancements.

- September 2025: Mehru Electrical & Mechanical Engineers Pvt Ltd entered into an agreement with Hyosung for GIS instrument transformers, highlighting a strategic collaboration in transformer technologies.

- September 2025: Emerald Lake Capital has acquired CORE Transformers, establishing a North American transformer platform. This acquisition enhances capacity and expands the repair and servicing network for transformers, including dry-type units.

Global Dry-Type Transformer Market Report Scope

The dry-type transformer is a type of transformer that uses air as a coolant. A dry-type transformer has no moving parts inside and is a static device that uses environment-friendly temperature insulation systems. It is used in a wide variety of applications and can be installed indoors or outdoors.

The dry-type transformers market is segmented by power rating, cooling method, phase, transformer type, end-user, and geography. By power rating, the market is segmented into large (above 100 MVA), medium (10 to 100 MVA), and small (up to 10 MVA) transformers. By cooling method, the market is segmented into AN (Air Natural), AF (Air Forced), and WF (Water Forced). By phase, the market is segmented into single-phase and three-phase transformers. By transformer type, the market is segmented into power transformers and distribution transformers. By end-user, the market is segmented into power utilities, industrial, commercial, and residential sectors. The report also covers market size and forecasts for the dry-type transformers market across major countries within these regions. For each segment, market sizing and forecasts have been provided in terms of value (USD).

By Power Rating

| Large (Above 100 MVA) |

| Medium (10 to 100 MVA) |

| Small (Up to 10 MVA) |

By Cooling Method

| AN (Air-Natural) |

| AF (Air-Forced) |

| WF (Water-Forced) |

By Phase

| Single Phase |

| Three Phase |

By Transformer Type

| Power |

| Distribution |

By End-User

| Power Utilities |

| Industrial |

| Commercial |

| Residential |

By Geography

| North America | United States |

| Canada | |

| Mexico | |

| Europe | United Kingdom |

| Germany | |

| France | |

| Italy | |

| Spain | |

| Russia | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| ASEAN Countries | |

| Australia and New Zealand | |

| Rest of Asia-Pacific | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| United Arab Emirates | |

| South Africa | |

| Egypt | |

| Rest of Middle East and Africa |

| By Power Rating | Large (Above 100 MVA) | |

| Medium (10 to 100 MVA) | ||

| Small (Up to 10 MVA) | ||

| By Cooling Method | AN (Air-Natural) | |

| AF (Air-Forced) | ||

| WF (Water-Forced) | ||

| By Phase | Single Phase | |

| Three Phase | ||

| By Transformer Type | Power | |

| Distribution | ||

| By End-User | Power Utilities | |

| Industrial | ||

| Commercial | ||

| Residential | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | United Kingdom | |

| Germany | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| ASEAN Countries | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| United Arab Emirates | ||

| South Africa | ||

| Egypt | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the projected value for global dry-type transformers by 2031?

The segment is forecast to reach USD 24.18 billion by 2031.

Which power-rating class shows the fastest growth through 2031?

Units up to 10 MVA are advancing at an 8.6% CAGR, the quickest among all rating brackets.

How does air-forced cooling improve performance over air-natural designs?

Fan-assisted airflow lifts continuous capacity by 25-33% and, with variable-speed controls, cuts auxiliary power use about 50%.

Why are hyperscale data centers adopting dry-type units?

NFPA 70 fire-safety rules restrict flammable liquids indoors, so oil-free cast-coil transformers meet compliance while handling high harmonic loads.

What influence does the Inflation Reduction Act have on North American demand?

It channels USD 369 billion into clean-energy upgrades, accelerating replacement of legacy liquid-filled gear with dry-type alternatives.

Page last updated on: