Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

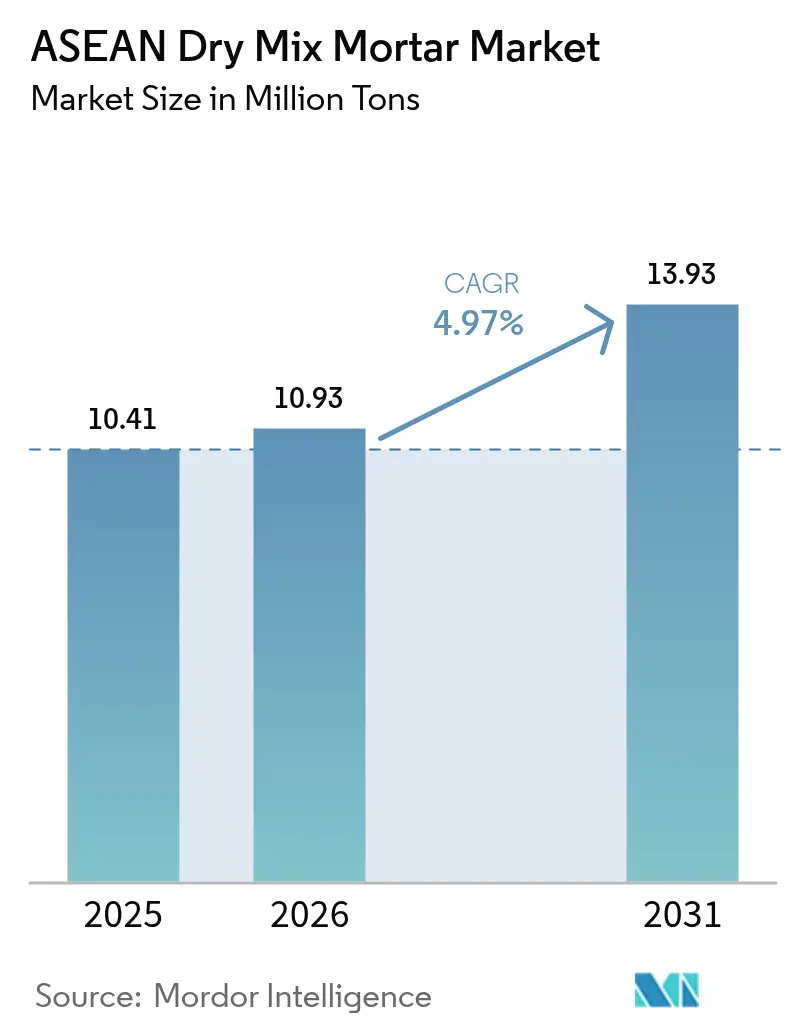

| Base Year Market Size (2025) | 10.41 Million tons |

| Market Volume (2026) | 10.93 Million tons |

| Market Volume (2031) | 13.93 Million tons |

| Growth Rate (2026 - 2031) | 4.97% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

ASEAN Dry Mix Mortar Market Analysis by Mordor Intelligence

The ASEAN Dry Mix Mortar Market size was valued at 10.41 million tons in 2025 and is estimated to grow from 10.93 million tons in 2026 to reach 13.93 million tons by 2031, at a CAGR of 4.97% during the forecast period (2026-2031). Momentum comes from mega-infrastructure programs across Indonesia, Vietnam, Thailand, and the Philippines, a widening skills gap that favors pre-bagged and silo-delivered mixes, and tightening green-building codes that reward low-carbon formulations. Indonesia’s archipelago geography keeps inter-island logistics costs high, steering large contractors toward on-site silos, while Vietnam’s record cement output underpins reliable feedstock for mortar plants. Tile adhesives are the clear outperformer as large-format ceramics proliferate, whereas render and plaster remain volume mainstays for price-sensitive self-builders. Amid rising raw-material and energy costs, producers that secure regional additive supplies and digitalize batch tracking are winning specifications on institutional and infrastructure projects, lifting average selling prices for the ASEAN dry mix mortar market.

Key Report Takeaways

- By application, render products held 40.71% of the ASEAN Dry Mix Mortar market share in 2025; tile adhesives are forecast to advance at a 6.42% CAGR during the forecast period (2026-2031).

- By end-user industry, residential construction captured 64.15% share of the ASEAN Dry Mix Mortar market size in 2025, while industrial and institutional demand is projected to grow at 5.98% CAGR during the forecast period (2026-2031).

- By geography, Indonesia led with 21.34% share in 2025; Vietnam is accelerating at a 6.66% CAGR during the forecast period (2026-2031).

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

ASEAN Dry Mix Mortar Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Mega-infrastructure pipeline accelerates bulk mortar demand | +1.5% | Indonesia, Thailand, Vietnam, Philippines | Medium term (2-4 years) |

| Skilled-labor scarcity drives pre-bagged and silo systems | +1.2% | Singapore, Malaysia, Thailand, with spillover to urban ASEAN | Short term (≤ 2 years) |

| Region-wide green-building codes and cement decarbonization roadmap | +0.8% | Global ASEAN, led by Singapore and Malaysia | Long term (≥ 4 years) |

| ASEAN mutual-recognition arrangement cuts cross-border compliance costs | +0.4% | Cross-border trade corridors (Thailand-Malaysia, Singapore) | Medium term (2-4 years) |

| Growth of 3D-printing and modular builds needing high-performance mixes | +0.9% | Singapore, Thailand, Philippines, Vietnam | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Mega-Infrastructure Pipeline Accelerates Bulk Mortar Demand

New expressways, ports, and rail corridors such as Thailand’s USD 31.5 billion Land Bridge and Vietnam’s Long Thanh International Airport require millions of tons of high-flow render, grout, and waterproofing mortars delivered by automated silos to maintain schedule certainty. Contractors prefer silo systems because pre-bagged formats suffer moisture spoilage during long maritime transits in Indonesia and the Philippines. Localized bulk plants near Sumatra, Kalimantan, and Sulawesi lower delivered costs and ensure batch consistency, making the ASEAN dry mix mortar market increasingly project-channel oriented. Suppliers that invest early in regional silo fleets lock in long-term supply contracts, insulating themselves from commodity-price swings. As more design-build tenders specify batch traceability, bulk mortars are gaining status as a performance, not merely logistical, requirement in the ASEAN dry mix mortar market.

Skilled-Labor Scarcity Drives Pre-Bagged and Silo Systems

ASEAN construction sites confront tightening foreign-worker quotas and an aging domestic workforce, with Singapore projecting a 500,000-worker gap in 2026. Pre-mixed mortars and pneumatic silos slash on-site mixing hours, allowing contractors to redeploy scarce masons to critical path tasks. Regional players report 30-50% time savings on modular-housing sites that shift wet-trades work to factories. Automated conveying equipment from Knauf PFT and m-tec is now standard in bids for metro stations and high-rise façades, further embedding silos in the ASEAN dry mix mortar market. The adoption cycle is self-reinforcing as project specs mandate pre-packaged quality, closing opportunities for traditional sand-cement batching.

Region-Wide Green-Building Codes and Cement Decarbonization Roadmap

The ASEAN Federation of Cement Manufacturers’ 2035 Roadmap targets a 38 million-ton CO₂ cut, prompting mortar formulators to slash clinker factors using fly ash, slag, and calcined clays[1]ASEAN Built, “Cement Decarbonization Roadmap 2035,” aseanbuilt.org. Singapore requires embodied-carbon disclosure on major projects, while Indonesia’s standards body now permits low-carbon binders. Polymer-additive suppliers Wacker and BASF have scaled VAE (Vinyl Acetate-Ethylene) and cellulose-ether capacities in Singapore and Malaysia to optimize low-cement recipes. Early adopters that publish third-party environmental product declarations already command premiums on institutional builds, enhancing margins in the ASEAN dry mix mortar market.

ASEAN Mutual-Recognition Arrangement Cuts Compliance Costs

The 2024 mutual-recognition arrangement lets a tile adhesive tested in Thailand skip retesting in Malaysia, slicing months off launch calendars and saving up to USD 100,000 per product. Multinationals running plants in Vietnam, Indonesia, and Thailand can certify once, then ship region-wide, harvesting scale efficiencies unattainable for single-country players. Vietnam’s 37 million-ton cement export surplus sharpens its appeal as a feedstock hub feeding value-added mortar exports throughout the ASEAN dry mix mortar market. While full operationalization will take time, early movers are already rationalizing regional portfolios around the unified standards.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Price-sensitive informal housing segment | -0.7% | Philippines, Indonesia, Vietnam urban peripheries | Short term (≤ 2 years) |

| High CAPEX for dry-mix plants and inter-island silo logistics | -0.5% | Indonesia, Philippines archipelago regions | Medium term (2-4 years) |

| Petro-polymer additive supply-chain volatility | -0.6% | Global ASEAN, dependent on petrochemical imports | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Price-Sensitive Informal Housing Segment

Self-builders dominating Metro Manila’s 6.57 million-unit backlog still choose generic sand-cement bags over branded products, trimming conversion rates for polymer-modified mortars. Similar dynamics persist in Indonesian kampung upgrades and peripheral Vietnamese settlements, where upfront cost outweighs lifecycle benefits. Large-scale housing programs allocate budgets per unit that barely cover structure and roof, leaving little room for premium tile adhesives. This segment generates volume but a negligible margin, forcing mainstream brands in the ASEAN dry mix mortar market to weigh economy tiers against brand dilution.

High CAPEX for Dry-Mix Plants and Silo Logistics

Automated blending lines cost USD 10-15 million, excluding the USD 5-10 million needed for silo fleets and bulk trucks. Indonesia’s island geography demands multiple plants or long maritime hauls, both eroding returns. Philippine producers face similar challenges across 7,600 islands. Saint-Gobain bypassed greenfield risk by taking 60% in Indocement’s mortar arm, adding three lines to 14 existing ones, illustrating the scale imperative. Smaller firms often resort to toll-manufacturing, surrendering control and margin in the ASEAN dry mix mortar market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Tile Adhesives Outpace Traditional Render

The ASEAN dry mix mortar market size for render stood at 40.71% volume share in 2025, reflecting masonry-heavy residential builds in tropical climates. Tile adhesives, though smaller, are forecast to record the highest 6.42% CAGR during the forecast period (2026-2031) as large-format tiles and porcelain panels demand polymer-rich, sag-resistant formulas[2]Wacker Chemie, “VAE Dispersions for Tile Adhesives,” wacker.com. Grouts and waterproofing slurries ride the same wave, gaining share in commercial kitchens, healthcare, and wet rooms where hygiene and chemical resistance trump cost. Render growth moderates as gypsum boards and Exterior Insulation and Finish Systems (EIFS) gain favor inside high-rise projects. Still, commodity render and plaster will anchor baseline demand in the ASEAN dry mix mortar market, ensuring plant utilization even as margins migrate to specialty products.

Value migration favors suppliers that marry localized bulk capacity with additive know-how. Wacker’s Singapore VAE plant and BASF’s Kuantan cellulose-ether unit shorten lead times for premium adhesives, giving regional players first-mover advantages on green-building projects. Commercial tile contractors increasingly bundle adhesives and grouts from a single brand to ensure warranty coverage, concentrating spend with technical leaders. The divergence between mass-market render and high-performance specialties will widen over the forecast period, reshaping product portfolios in the ASEAN dry mix mortar market.

By End-User Industry: Industrial and Institutional Surge

The residential sector absorbed 64.15% of 2025 tonnage, boosted by PT Semen Indonesia’s 3-million-homes program and fast urbanization in Vietnam and the Philippines. Yet industrial and institutional demand is projected to accelerate at a 5.98% CAGR during the forecast period (2026-2031), powered by data centers, manufacturing upgrades, and hospital modernizations that specify epoxy grouts, self-leveling underlayments, and waterproofing membranes. These mixes carry price premiums of 30-60% over commodity render.

Data-center floors in Singapore require anti-static, high-early-strength mortars cured under tight humidity control, an expertise niche for multinationals like Sika and Mapei. Vietnam’s electronics plants specify chemically resistant toppings to tolerate solvent spills, driving higher value per square meter. Institutional retrofits in Thailand leverage rapid-set repair mortars to minimize service interruptions. Together, these factors lift revenue faster than tonnage for the ASEAN dry mix mortar market.

Supplying the industrial segment necessitates technical support crews and in-house labs, capabilities many regional cement firms lack. Consequently, multinationals are capturing a disproportionate share of wallet despite lower overall volumes. Residential, while still the volume backbone, faces margin compression from informal-housing price caps. Balanced portfolios that target both high-spec institutional projects and mass-market housing are emerging as the most resilient strategy in the ASEAN dry mix mortar market.

Geography Analysis

Indonesia anchored 21.34% of the ASEAN Dry Mix Mortar market volume in 2025 on the back of its vast housing pipeline and 280-million population. Saint-Gobain’s 2026 deal for 60% of Indocement’s mortar arm added three lines to an existing 14-line network, underlining confidence in long-term growth despite low national cement utilization. Inter-island freight costs keep silo systems attractive for large projects, but bagged render remains dominant in the kampung retail trade.

Vietnam is the fastest-growing national segment, with a projected 6.66% CAGR during the forecast period (2026-2031). Cement sales hit 112 million tons in 2025, up 16%, and the 2026 public-investment budget rose 12% to VND 1.08 quadrillion (USD 41.5 billion). Massive expressway and airport completions are filling contractor backlogs and underpinning procurement for high-performance mortars. Local producer Bumatech joined the Southeast Asian Drymix Mortar Association in 2025 and now operates a 5,000-ton-per-month plant, signaling a maturing domestic supply.

Thailand, Malaysia, and the Philippines form a middle cohort. Thailand’s USD 31.5 billion Land Bridge and Eastern Economic Corridor create steady demand for waterproofing and tile adhesives, while Malaysia’s East Coast Rail Link sustains bulk render requirements. The Philippines is pivoting to prefab modules for its six-million-home program, integrating factory-applied mortars that cut build times. Singapore, though small in volume, drives innovation: Sika’s Tuas plant targets metro upgrades, and Münzing’s Singapore hub centralizes additive warehousing for the entire ASEAN dry mix mortar market. Myanmar and the balance of ASEAN remain nascent but hold latent potential once political conditions stabilize.

Competitive Landscape

The ASEAN Dry Mix Mortar market is moderately fragmented. White-space opportunities lie in industrial and data-center builds where performance warranties matter. Suppliers that field project-engineering teams and digital batch-tracking platforms win locked-in contracts and price premiums. Regulatory harmonization under the ASEAN mutual-recognition framework further strengthens regional players with multi-country plants. Single-market firms will find it harder to match the compliance speed and cost base of diversified networks, potentially accelerating consolidation by 2031.

ASEAN Dry Mix Mortar Industry Leaders

Sika AG

Ardex Group

Mapei S.p.A.

Holcim

Siam City Cement Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Saint-Gobain completed the acquisition of Fosroc, Inc. for approximately EUR 960 million (USD 1.03 billion). The deal provided Fosroc, Inc.'s dry mix mortars access to Saint-Gobain's extensive resources and global network, enabling further growth and innovation.

- January 2025: Sika AG inaugurated a new automated and sustainable plant in Singapore, enhancing regional supply capabilities and supporting growth in the ASEAN dry mix mortar market through improved efficiency, reduced waste, and future solar integration.

ASEAN Dry Mix Mortar Market Report Scope

Dry mix mortar is produced by mixing various raw materials, including sand, limestone powder, binders like cement, hydrated lime, white cement, and gypsum, and additives like methylcellulose, synthetic resin, hydrophobic agent, and others.

The ASEAN dry mix mortar market is segmented by application, end-user industry, and geography. By application, the market is segmented into plaster, render, tile adhesive, grout, waterproofing slurry, concrete protection and renovation, insulation and finishing systems, and other applications (bonding mortar, external plaster, etc.). By end-user industry, the market is segmented into residential and non-residential. The report also covers the size and forecasts for the market in seven countries across the region. For each segment, the market sizing and forecasts are based on volume (tons).

By Application

| Plaster |

| Render |

| Tile Adhesive |

| Grout |

| Water Proofing Slurry |

| Concrete Protection and Renovation |

| Insulation and Finishing System |

| Others |

By End-user Industry

| Residential |

| Commercial |

| Infrastructure |

| Industrial and Institutional |

By Geography

| Malaysia |

| Indonesia |

| Thailand |

| Singapore |

| Philippines |

| Vietnam |

| Myanmar |

| Rest of ASEAN |

| By Application | Plaster |

| Render | |

| Tile Adhesive | |

| Grout | |

| Water Proofing Slurry | |

| Concrete Protection and Renovation | |

| Insulation and Finishing System | |

| Others | |

| By End-user Industry | Residential |

| Commercial | |

| Infrastructure | |

| Industrial and Institutional | |

| By Geography | Malaysia |

| Indonesia | |

| Thailand | |

| Singapore | |

| Philippines | |

| Vietnam | |

| Myanmar | |

| Rest of ASEAN |

Key Questions Answered in the Report

What is the projected volume for ASEAN dry mix mortars by 2031?

The ASEAN Dry Mix Mortar market is forecast to reach 13.93 million tons by 2031.

Which application segment is growing fastest?

Tile adhesives are projected to record the highest 6.42% CAGR through 2031.

Which country will post the strongest growth?

Vietnam leads with an expected 6.66% CAGR between 2026-2031

How are green-building codes influencing formulations?

Stricter codes are pushing producers to lower clinker content and adopt supplementary cementitious materials.

Why are silo systems gaining popularity?

They cut labor time, reduce waste, and ensure batch consistency, crucial on mega-infrastructure projects.

Page last updated on: