Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

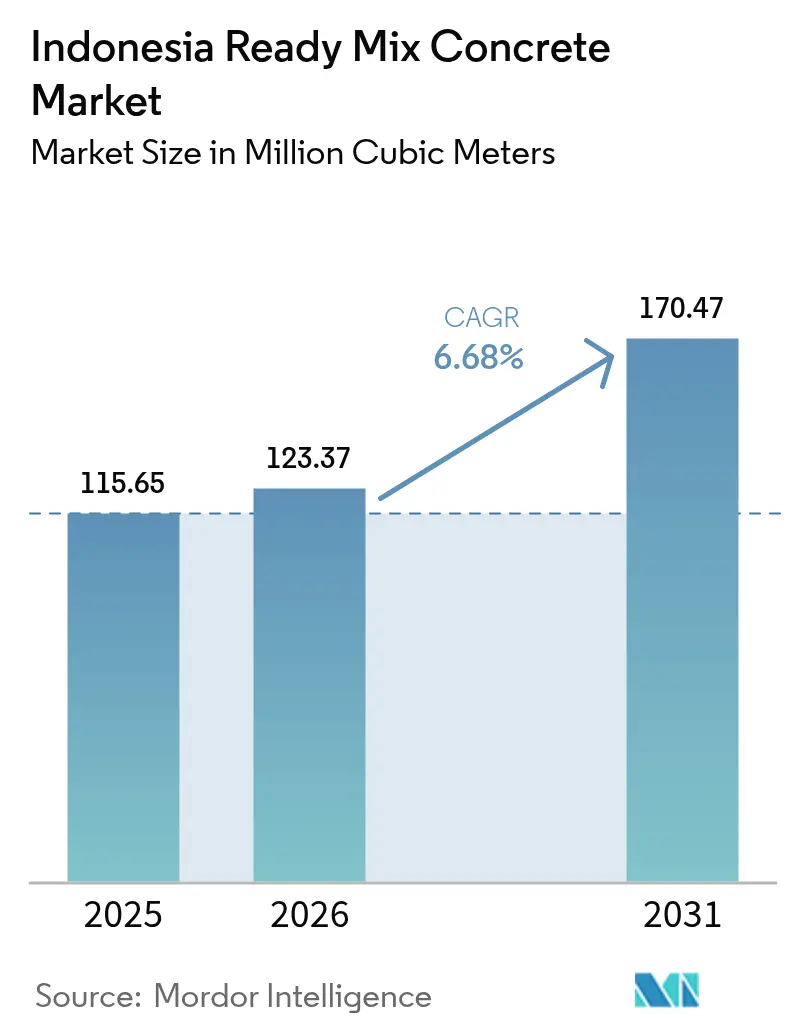

| Base Year Market Size (2025) | 115.65 Million cubic meters |

| Market Volume (2026) | 123.37 Million cubic meters |

| Market Volume (2031) | 170.47 Million cubic meters |

| Growth Rate (2026 - 2031) | 6.68% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Indonesia Ready Mix Concrete Market Analysis by Mordor Intelligence

The Indonesia Ready Mix Concrete Market size was valued at 115.65 Million cubic meters in 2025 and estimated to grow from 123.37 Million cubic meters in 2026 to reach 170.47 Million cubic meters by 2031, at a CAGR of 6.68% during the forecast period (2026-2031). The expansion reflects the country’s sustained infrastructure roll-out, rising vertical housing starts, and a shift toward high-volume commercial builds that favor factory‐controlled batching. Government capital expenditure of USD 25.5 billion earmarked for 2025, alongside 14 additional National Strategic Projects, underpins a predictable demand stream for the Indonesia ready mixed concrete market. Robust bulk-cement logistics networks are lowering delivered costs, a factor that strengthens pricing competitiveness against alternative construction materials. Simultaneously, mandated use of low-carbon blended cements in public works is encouraging producers to pivot toward greener formulations, creating fresh revenue pools for the Indonesia ready mixed concrete market. Structural supply-side constraints, such as persistent cement overcapacity and traffic-induced delivery delays, continue to compress margins. However, these headwinds are being offset by scale plays, logistics innovations, and digital process optimization investments.

Key Report Takeaways

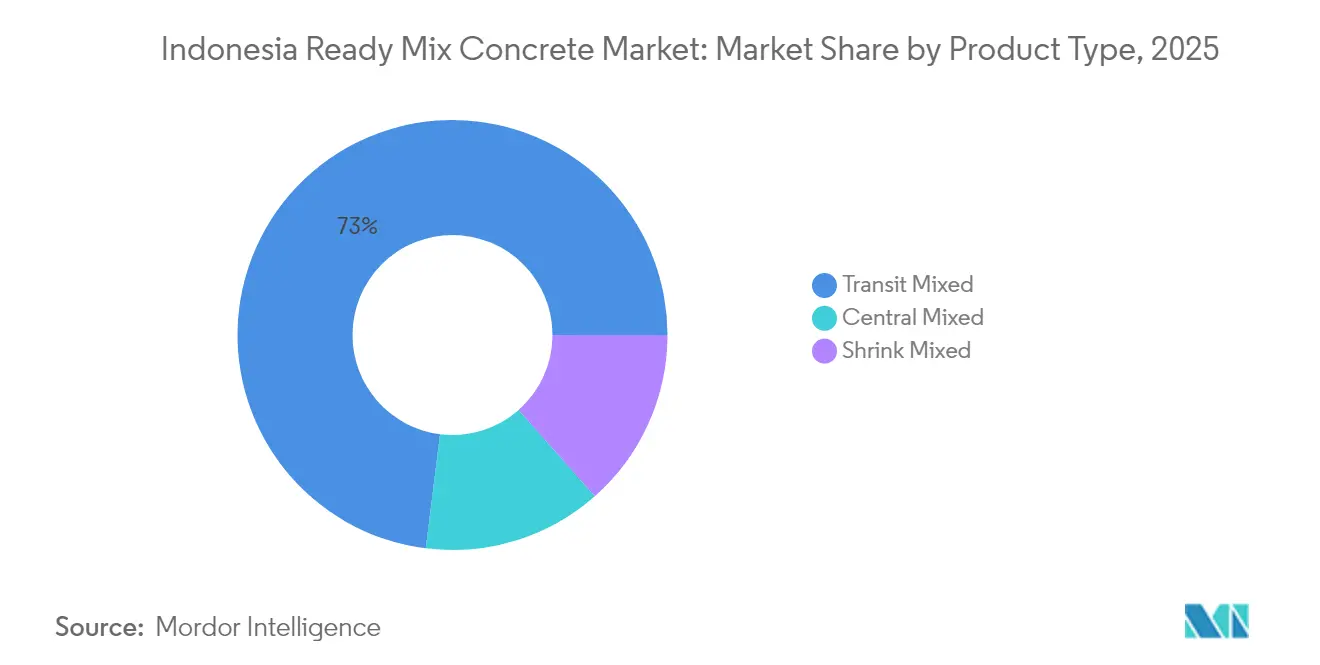

- By product type, Transit Mixed concrete led with 73.02 % of the Indonesia ready mixed concrete market share in 2025. Moreover, it is expected to grow with a CAGR of 6.92% during the forecast period (2026-2031).

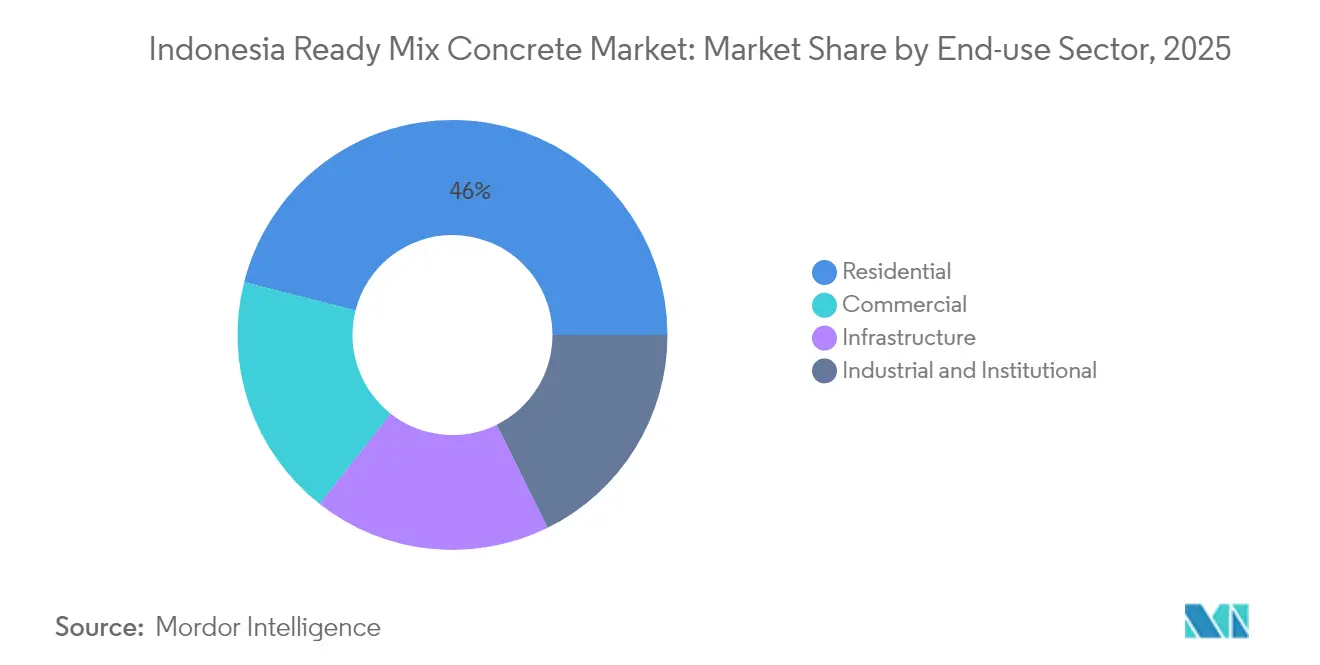

- By end-use sector, the residential sector accounted for 46.05% of the market share in 2025. However, the share of the commercial segment is expected to advance at a CAGR of 7.78 % to 2031, the fastest among all demand categories within the Indonesian ready mixed concrete market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Indonesia Ready Mix Concrete Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Massive public-sector infrastructure pipeline | +2.1% | National, Java & Kalimantan | Medium term (2-4 years) |

| Accelerating urban vertical housing & high-rises | +1.8% | Java, Sumatra, Sulawesi metros | Long term (≥4 years) |

| Growing bulk-cement logistics networks | +1.2% | National | Short term (≤2 years) |

| Mandatory low-carbon blended cements | +0.9% | National | Medium term (2-4 years) |

| Seismic-resilient industrialized systems | +0.7% | Java, Sumatra, Sulawesi | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Massive Public-Sector Infrastructure Pipeline

Sustained state investment keeps the pipeline of roads, rail, ports and social housing filled, providing consistent volume booking for the Indonesia ready mixed concrete market[1]Asian Development Bank, “Indonesia Economic Outlook 2025,” adb.org. The IDR 400.3 trillion infrastructure budget for 2025 represents 1.9% of GDP, ensuring that concrete demand remains insulated from short-term fluctuations in the private sector. Large flagship projects, such as IKN Nusantara and the Trans-Sumatra Toll Road, enable batching-plant operators to negotiate multi-year supply agreements, locking in utilization at profitable levels. The government’s proven ability to disburse funds—capital spending jumped 27.7% in 2023—builds industry confidence in cash-flow visibility. Local producers have responded by adding strategically placed satellite plants to minimize haul distances and preserve the critical 90-minute workability window mandated for on-site placement.

Accelerating Urban Vertical Housing and Commercial High-Rise Builds

Urban land scarcity is driving Indonesia’s municipalities to build upward rather than outward, a structural trend that directly benefits the Indonesian ready-mixed concrete market. The state-backed FLPP scheme targets 165,880 subsidized vertical units in 2025, while private developers tap into steady 5% annual GDP expansion to green-light office, retail, and mixed-use towers. High-rise construction demands high-strength concrete, extended slump retention, and precise admixture dosing, elevating the technical entry bar and allowing premium pricing. Producers able to supply self-compacting and pumpable mixes command higher margins and enjoy repeat contracts from tier-one contractors active in Jakarta, Surabaya, and emerging metros. Equipment investments such as truck-mounted pumps and high-capacity placing booms further fortify competitive differentiation.

Growing Bulk-Cement Logistics Networks Lowering Delivered RMC Costs

The share of bulk deliveries in national cement dispatches increased by 4.4% in H1 2024, signaling a secular shift away from bagged product and toward pneumatic transfer systems that reduce packaging waste and handling losses. Dedicated bulk terminals added in Gresik, Kupang, and Makassar cut sailing times between mills and batching plants, trimming inbound freight bills. A recent IDR 47.15 billion, three-year supply contract between PT MPX Logistic International and PT SCG Ready Mix exemplifies how negotiated volume take-offs can lock in cost advantages for the Indonesia ready mixed concrete market. Lower input costs translate into sharper bids on government tenders without eroding operating margin, a decisive factor in an environment where price competition remains fierce.

Mandatory Use of Low-Carbon Blended Cements in Public Projects

Government circulars now compel state-funded projects to apply blends incorporating pozzolans, slag and industrial by-products, catalyzing demand for specialty binders that reduce CO₂ intensity by up to 50 kg per ton[2]SCG Corporate, “Low-Carbon Cement Portfolio,” scg.com. Leaders such as SCG and Cemindo Gemilang have rolled out second-generation greener lines with 15% lower embodied carbon, extending their first-mover advantage. Project owners, under pressure to meet ESG scorecards, increasingly weigh environmental credentials alongside cost in tender evaluations, effectively making low-carbon capability a qualifying criterion for the Indonesian ready-mixed concrete market. Superior thermal performance and durability also help offset marginal price premiums, thereby enhancing lifecycle value propositions for both public and private developers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Chronic cement over-capacity | -1.5% | National, Java & Sumatra | Short term (≤2 years) |

| High logistics cost & traffic | -1.1% | Java metros | Medium term (2-4 years) |

| La Niña-driven rainfall 2025-27 | -0.8% | Java, Kalimantan, Sulawesi, Sumatra, Papua | Short term (≤2 years) |

| Shift to off-site precast modules | -0.6% | Urban centers with advanced construction | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Chronic Cement Over-Capacity Compressing RMC Margins

The national clinker capacity of 119.9 million t remains drastically above the 64.9 million t domestic demand, limiting kiln runs to a 56.5% utilization rate and eroding pricing power for bulk feedstock. The oversupply environment forces mills to chase dispatch volumes by narrowing ex-works pricing, but trucking, energy, and port tariffs often absorb those concessions before they filter into batching-plant savings. Producers that are backward-integrated into cement thus defend gross margins better than pure-play concrete firms. Although a government moratorium on new permits outside Papua and Maluku aims to arrest capacity creep, the installed base will continue to weigh on sector profitability during the near term.

High Logistics Cost and Traffic Jeopardizing 90-Minute Workability Window

Jakarta’s peak-hour speeds average 18 km/h, which extends transit times for mixer trucks and threatens slump loss before on-site discharge. Route optimization software, RFID tracking, and in-transit cooling jackets have become essential countermeasures, yet smaller fleet operators struggle to fund such upgrades, risking spoilage penalties. Rising fuel costs and toll fees compound the burden, particularly for plants sited on cheaper peripheral land beyond Ring 1 urban zones. Extended-set admixtures offer partial relief but add to variable cost per cubic meter. The result is uneven service reliability across the Indonesian ready-mixed concrete market, with quality-assured suppliers widening share at the expense of under-capitalized rivals.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Transit Mixed Dominates Urban Delivery

Transit Mixed concrete captured 73.02 % of the Indonesia ready mixed concrete market share in 2025 and is projected to register a 6.92 % CAGR through 2031. This dominance is rooted in centralized batching, which ensures uniform quality, a critical attribute for high-specification government and commercial projects. The Indonesia ready mixed concrete market size tied to Transit Mixed solutions is forecast to reach roughly 124.4 million m³ by 2031, reflecting the steady preference for bulk dispatches suitable for dense urban corridors. Central Mixed alternatives carve a smaller but stable niche in segments where laboratory-grade precision takes precedence over haul-time flexibility, such as nuclear power auxiliaries and long-span bridge decks. Shrink Mixed volumes remain limited, reserved for constrained job sites where full-size mixers cannot maneuver. Producers are refurbishing fleet assets with larger drums and telematics to stretch service radii without breaching the 90-minute slump criterion, further reinforcing Transit Mixed dominion within the Indonesia ready mixed concrete market.

Operators have also accelerated plant commissioning near emerging growth zones. SCG Jayamix brought a Bali unit online in February 2025 that features salt-spray-resistant marine concrete, meeting tourism infrastructure needs while validating the geographic agility of the Transit Mixed model. Coupled with falling per-unit cement costs enabled by bulk distribution, Transit Mixed suppliers are now pricing more aggressively against site-mixed alternatives, tightening competitive pressures on artisanal providers in peri-urban districts. These developments collectively sustain Transit Mixed’s central role, ensuring it anchors capacity planning strategies over the full forecast horizon.

By End-use Sector: Commercial Builds Lead Growth

The residential category accounted for 46.05% of 2025 consumption, yet it is pacing behind the commercial sector, which is advancing at an 7.78% CAGR to 2031. Within the Indonesia ready mixed concrete industry, high-rise offices, hotels, and retail complexes are commanding larger pour volumes per footprint, driving the Indonesia ready mixed concrete market size linked to commercial projects to an estimated 58.4 million m³ by 2031. Developers in Jakarta and Surabaya are favoring higher-grade formulations with extended workability for 50-story cores, enabling suppliers to secure price premiums and elevate per-cubic-meter profitability. Infrastructure remains a base-load segment, smoothing demand across election cycles due to multi-year budgets and sovereign guarantees.

Residential demand is underpinned by government programs targeting 3 million units, but subsidies are tilted toward affordable housing, compressing margins. Still, vertical social-housing towers in land-scarce metros require standardized grades, benefiting scaled operators. Industrial builds post robust mid-single-digit growth, driven by resource-processing facilities in Kalimantan and Sulawesi, where high sulfate-resistance mixes are gaining traction. Institutional projects, although smaller in volume, create repeatable business, particularly for specialized grades in hospitals and data centers. Collectively, the diversified end-use mix insulates the Indonesia ready mixed concrete market against cyclical dips in any single sector.

Geography Analysis

Java remains the consumption epicenter, absorbing 52 % of national cement sales and anchoring the Indonesia ready mixed concrete market through robust metropolitan build pipelines. West Java recorded the highest absolute demand as of 2025, while Jakarta had a 2.69 t CO₂e per capita construction footprint, underscoring exceptional vertical density pressures. The tight clustering of integrated cement mills in Gresik, Bogor, and Cilacap shortens lead times and cushions ex-works price volatility, giving Java-based concrete plants a structural cost advantage. High familiarity with pump technology and advanced admixture protocols in the capital region further consolidates value capture for premium grades.

Kalimantan is the fastest-growing region, driven by the new seat of government at IKN Nusantara and the development of resource-corridor infrastructure. Semen Indonesia’s IDR 22.5 billion outlay on dedicated logistics terminals in the province illustrates the scale of supply-chain build-out required to support projected demand. East Kalimantan’s mining complexes also propel specialized sulfate-resistant and fiber-reinforced grades, expanding the technical breadth of the Indonesia ready mixed concrete market. Sumatra, buoyed by 12 % sales growth in 2024, is leveraging connectivity projects such as Trans-Sumatra Toll to lift regional uptake and entice new entrants seeking first-mover advantage. Papua, Sulawesi and the Nusa Tenggara cluster form the frontier markets. Government connectivity programs, including port upgrades and airport extensions, are seeding baseline demand, although logistical frictions and sparse plant networks suppress immediate scalability. Local developers often import standardized mixes from Java, inflating transport costs. Nonetheless, the gradual roll-out of regional cement mills and satellite batching plants is expected to unlock incremental upside, albeit from a small base, during the latter half of the forecast window. These spatial dynamics collectively shape a multi-speed growth contour across the Indonesia ready mixed concrete market.

Competitive Landscape

The Indonesia ready mixed concrete market exhibits moderate concentration. Cost leadership remains paramount, given the chronic oversupply of cement and tight public-tender price ceilings. Lean-manufacturing runs have shaved cycle times by 13.9 %, while pump utilization delivers 5.264× placement efficiency over bucket methods. Smaller regional players survive by focusing on niche grades or proximity contracting, but upgrading to meet mandatory low-carbon specs strains their balance sheets.

Indonesia Ready Mix Concrete Industry Leaders

Heidelberg Materials

PT Cemindo Gemilang Tbk

PT Waskita Beton Precast Tbk

SCG

SIG

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: The Indonesian Readymix Concrete Association (APBRI) inaugurated its new board of directors, who will serve until 2027. They will aim to stimulate increased innovation, efficiency, and sustainability in the ready-mix concrete industry.

- May 2025: PT HSG Material Indonesia, a subsidiary of China-based Fujian Hongsheng Material Technology, broke ground on its concrete plant in Kendal Special Economic Zone near Semarang in Central Java. The plant will have a production capacity of 150,000m²/yr of ready-mix concrete.

Indonesia Ready Mix Concrete Market Report Scope

Commercial, Industrial and Institutional, Infrastructure, Residential are covered as segments by End Use Sector. Central Mixed, Shrink Mixed, Transit Mixed are covered as segments by Product.By End-Use Sector

| Commercial |

| Industrial and Institutional |

| Infrastructure |

| Residential |

By Product Type

| Central Mixed |

| Shrink Mixed |

| Transit Mixed |

| By End-Use Sector | Commercial |

| Industrial and Institutional | |

| Infrastructure | |

| Residential | |

| By Product Type | Central Mixed |

| Shrink Mixed | |

| Transit Mixed |

Market Definition

- END-USE SECTOR - Ready-mix concrete consumed in the construction sectors such as commercial, residential, industrial, institutional, and infrastructure are considered under the scope of the study.

- PRODUCT/APPLICATION - Under the scope of the study, the consumption of transit-mixed, shrink-mixed, and central-mixed ready-mix concrete are considered.

| Keyword | Definition |

|---|---|

| Accelerator | Accelerators are admixtures used to fasten the setting time of concrete by increasing the initial rate and speeding up the chemical reaction between cement and the mixing water. These are used to harden and increase the strength of concrete quickly. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Adhesives | Adhesives are bonding agents used to join materials by gluing. Adhesives can be used in construction for many applications, such as carpet laying, ceramic tiles, countertop lamination, etc. |

| Air Entraining Admixture | Air-entraining admixtures are used to improve the performance and durability of concrete. Once added, they create uniformly distributed small air bubbles to impart enhanced properties to the fresh and hardened concrete. |

| Alkyd | Alkyds are used in solvent-based paints such as construction and automotive paints, traffic paints, flooring resins, protective coatings for concrete, etc. Alkyd resins are formed by the reaction of an oil (fatty acid), a polyunsaturated alcohol (Polyol), and a polyunsaturated acid or anhydride. |

| Anchors and Grouts | Anchors and grouts are construction chemicals that stabilize and improve the strength and durability of foundations and structures like buildings, bridges, dams, etc. |

| Cementitious Fixing | Cementitious fixing is a process in which a cement-based grout is pumped under pressure to fill forms, voids, and cracks. It can be used in several settings, including bridges, marine applications, dams, and rock anchors. |

| Commercial Construction | Commercial construction comprises new construction of warehouses, malls, shops, offices, hotels, restaurants, cinemas, theatres, etc. |

| Concrete Admixtures | Concrete admixtures comprise water reducers, air entrainers, retarders, accelerators, superplasticizers, etc., added to concrete before or during mixing to modify its properties. |

| Concrete Protective Coatings | To provide specific protection, such as anti-carbonation or chemical resistance, a film-forming protective coat can be applied on the surface. Depending on the applications, different resins like epoxy, polyurethane, and acrylic can be used for concrete protective coatings. |

| Curing Compounds | Curing compounds are used to cure the surface of concrete structures, including columns, beams, slabs, and others. These curing compounds keep the moisture inside the concrete to give maximum strength and durability. |

| Epoxy | Epoxy is known for its strong adhesive qualities, making it a versatile product in many industries. It resists heat and chemical applications, making it an ideal product for anyone needing a stronghold under pressure. It is widely used in adhesives, electrical and electronics, paints, etc. |

| Fiber Wrapping Systems | Fiber Wrapping Systems are a part of construction repair and rehabilitation chemicals. It involves the strengthening of existing structures by wrapping structural members like beams and columns with glass or carbon fiber sheets. |

| Flooring Resins | Flooring resins are synthetic materials applied to floors to enhance their appearance, increase their resistance to wear and tear or provide protection from chemicals, moisture, and stains. Depending on the desired properties and the specific application, flooring resins are available in distinct types, such as epoxy, polyurethane, and acrylic. |

| High-Range Water Reducer (Super Plasticizer) | High-range water reducers are a type of concrete admixture that provides enhanced and improved properties when added to concrete. These are also called superplasticizers and are used to decrease the water-to-cement ratio in concrete. |

| Hot Melt Adhesives | Hot-melt adhesives are thermoplastic bonding materials applied as melts that achieve a solid state and resultant strength on cooling. They are commonly used for packaging, coatings, sanitary products, and tapes. |

| Industrial and Institutional Construction | Industrial and institutional construction includes new construction of hospitals, schools, manufacturing units, energy and power plants, etc. |

| Infrastructure Construction | Infrastructure construction includes new construction of railways, roads, seaways, airports, bridges, highways, etc. |

| Injection Grouting | The process of injecting grout into open joints, cracks, voids, or honeycombs in concrete or masonry structural members is known as injection grouting. It offers several benefits, such as strengthening a structure and preventing water infiltration. |

| Liquid-Applied Waterproofing Membranes | Liquid-Applied membrane is a monolithic, fully bonded, liquid-based coating suitable for many waterproofing applications. The coating cures to form a rubber-like elastomeric waterproof membrane and may be applied over many substrates, including asphalt, bitumen, and concrete. |

| Micro-concrete Mortars | Micro-concrete mortar is made up of cement, water-based resin, additives, mineral pigments, and polymers and can be applied on both horizontal and vertical surfaces. It can be used to refurbish residential complexes, commercial spaces, etc. |

| Modified Mortars | Modified Mortars include Portland cement and sand along with latex/polymer additives. The additives increase adhesion, strength, and shock resistance while also reducing water absorption. |

| Mold Release Agents | Mold release agents are sprayed or coated on the surface of molds to prevent a substrate from bonding to a molding surface. Several types of mold release agents, including silicone, lubricant, wax, fluorocarbons, and others, are used based on the type of substrates, including metals, steel, wood, rubber, plastic, and others. |

| Polyaspartic | Polyaspartic is a subset of polyurea. Polyaspartic floor coatings are typically two-part systems that consist of a resin and a catalyst to ease the curing process. It offers high durability and can withstand harsh environments. |

| Polyurethane | Polyurethane is a plastic material that exists in various forms. It can be tailored to be either rigid or flexible and is the material of choice for a broad range of end-user applications, such as adhesives, coatings, building insulation, etc. |

| Reactive Adhesives | A reactive adhesive is made of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Rebar Protectors | In concrete structures, rebar is one of the important components, and its deterioration due to corrosion is a major issue that affects the safety, durability, and life span of buildings and structures. For this reason, rebar protectors are used to protect against degrading effects, especially in infrastructure and industrial construction. |

| Repair and Rehabilitation Chemicals | Repair and Rehabilitation Chemicals include repair mortars, injection grouting materials, fiber wrapping systems, micro-concrete mortars, etc., used to repair and restore existing buildings and structures. |

| Residential Construction | Residential construction involves constructing new houses or spaces like condominiums, villas, and landed homes. |

| Resin Fixing | The process of using resins like epoxy and polyurethane for grouting applications is called resin fixing. Resin fixing offers several advantages, such as high compressive and tensile strength, negligible shrinkage, and greater chemical resistance compared to cementitious fixing. |

| Retarder | Retarders are admixtures used to slow down the setting time of concrete. These are usually added with a dosage rate of around 0.2% -0.6% by weight of cement. These admixtures slow down hydration or lower the rate at which water penetrates the cement particles by making concrete workable for a long time. |

| Sealants | A sealant is a viscous material that has little or no flow qualities, which causes it to remain on surfaces where they are applied. Sealants can also be thinner, enabling penetration to a certain substance through capillary action. |

| Sheet Waterproofing Membranes | Sheet membrane systems are reliable and durable thermoplastic waterproofing solutions that are used for waterproofing applications even in the most demanding below-ground structures, including those exposed to highly aggressive ground conditions and stress. |

| Shrinkage Reducing Admixture | Shrinkage-reducing admixtures are used to reduce concrete shrinkage, whether from drying or self-desiccation. |

| Silicone | Silicone is a polymer that contains silicon combined with carbon, hydrogen, oxygen, and, in some cases, other elements. It is an inert synthetic compound that comes in various forms, such as oil, rubber, and resin. Due to its heat-resistant properties, it finds applications in sealants, adhesives, lubricants, etc. |

| Solvent-borne Adhesives | Solvent-borne adhesives are mixtures of solvents and thermoplastic or slightly cross-linked polymers such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers. |

| Surface Treatment Chemicals | Surface treatment chemicals are chemicals used to treat concrete surfaces, including roofs, vertical surfaces, and others. They act as curing compounds, demolding agents, rust removers, and others. They are cost-effective and can be used on roadways, pavements, parking lots, and others. |

| Viscosity Modifier | Viscosity Modifiers are concrete admixtures used to change various properties of admixtures, including viscosity, workability, cohesiveness, and others. These are usually added with a dosage of around 0.01% to 0.1% by weight of cement. |

| Water Reducer | Water reducers, also called plasticizers, are a type of admixture used to decrease the water-to-cement ratio in the concrete, thereby increasing the durability and strength of concrete. Various water reducers include refined lignosulfonates, gluconates, hydroxycarboxylic acids, sugar acids, and others. |

| Water-borne Adhesives | Water-borne adhesives use water as a carrier or diluting medium to disperse resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a dilutant rather than a volatile organic solvent. |

| Waterproofing Chemicals | Waterproofing chemicals are designed to protect a surface from the perils of leakage. A waterproofing chemical is a protective coating or primer applied to a structure's roof, retaining walls, or basement. |

| Waterproofing Membranes | Waterproofing membranes are liquid-applied or self-adhering layers of water-tight materials that prevent water from penetrating or damaging a structure when applied to roofs, walls, foundations, basements, bathrooms, and other areas exposed to moisture or water. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms