India Dry Mix Mortar Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

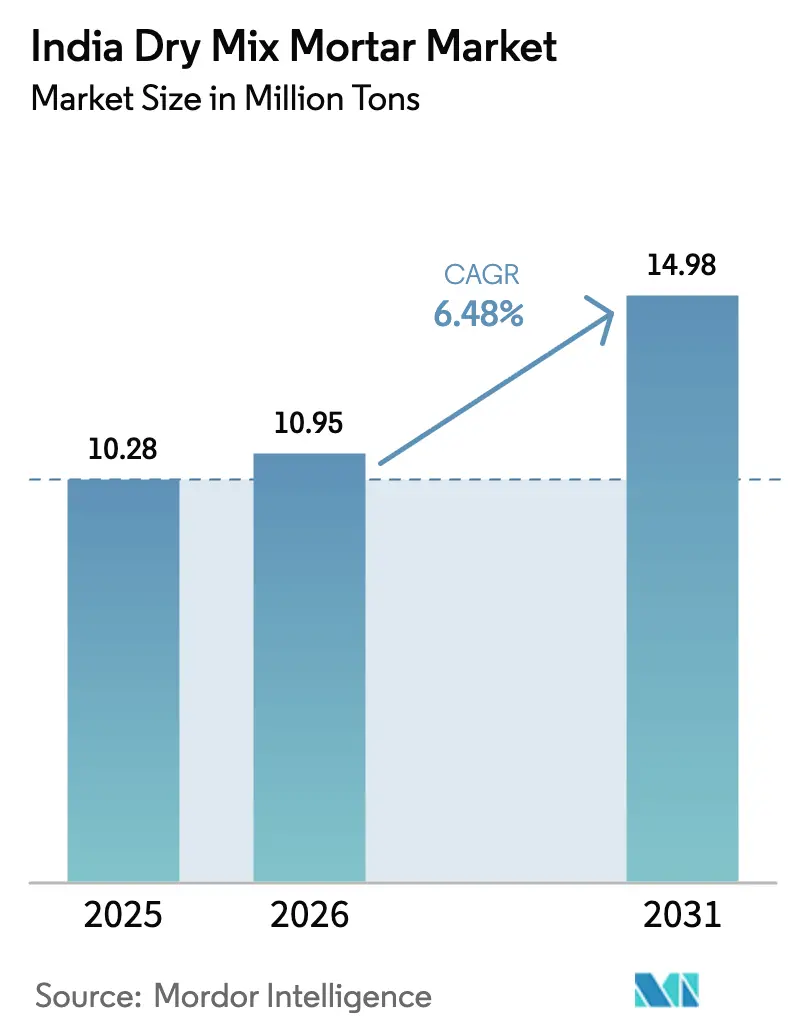

| Base Year Market Size (2025) | 10.28 Million tons |

| Market Volume (2026) | 10.95 Million tons |

| Market Volume (2031) | 14.98 Million tons |

| Growth Rate (2026 - 2031) | 6.48% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

India Dry Mix Mortar Market Analysis by Mordor Intelligence

The India Dry Mix Mortar Market size is expected to grow from 10.28 million tons in 2025 to 10.95 million tons in 2026 and is forecast to reach 14.98 million tons by 2031 at 6.48% CAGR over 2026-2031. Contractors are phasing out on-site sand–cement blending in favor of factory-formulated products that cut labor requirements, improve batch-to-batch consistency, and shorten project schedules. Housing programs under Pradhan Mantri Awas Yojana (PMAY-Urban) and accelerated infrastructure outlays are enlarging the customer base, while tier-2 city commercial work is widening the demand profile. Builders in metro regions increasingly specify ready-to-use mortars to meet tighter quality audits and green-building credits, prompting producers to expand automated capacity near consumption hubs. Still, profit margins are sensitive to cement and polymer-additive swings and to the added costs of complying with Extended Producer Responsibility (EPR) rules for recyclable packaging.

Key Report Takeaways

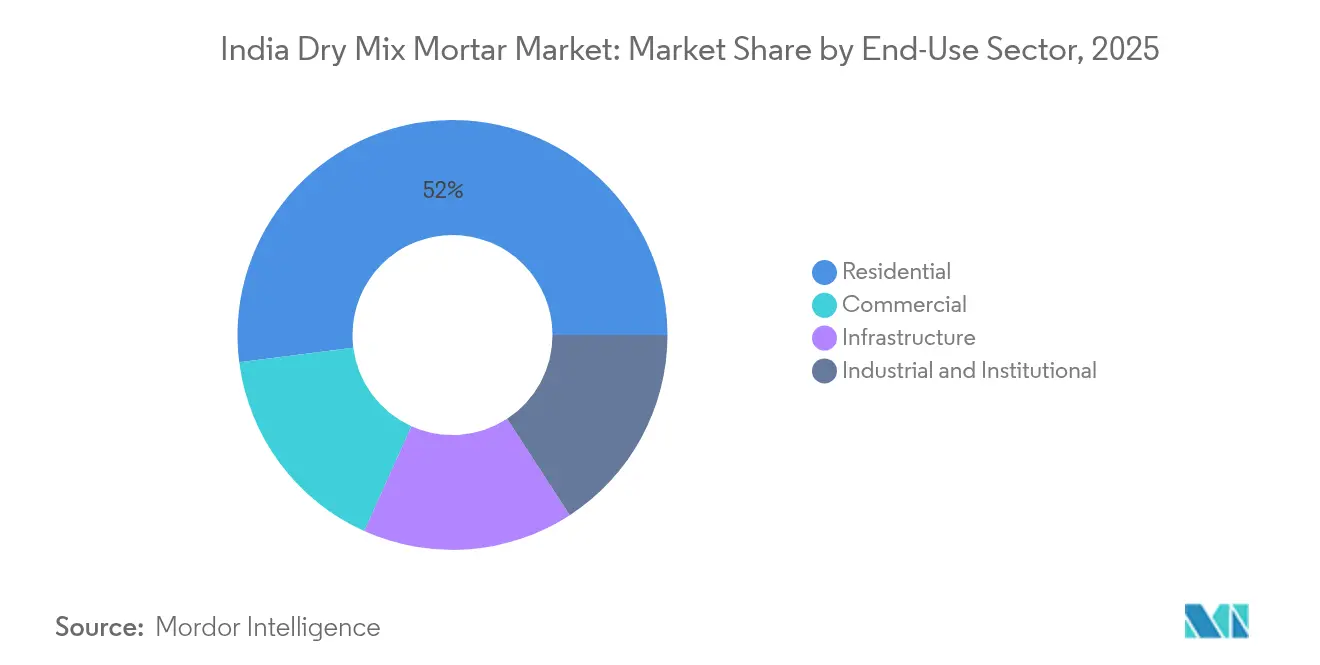

- By end-use sector, residential construction accounted for 52.02% of the India dry mix mortar market share in 2025, whereas commercial projects are projected to post the fastest growth of 7.35% CAGR through 2031.

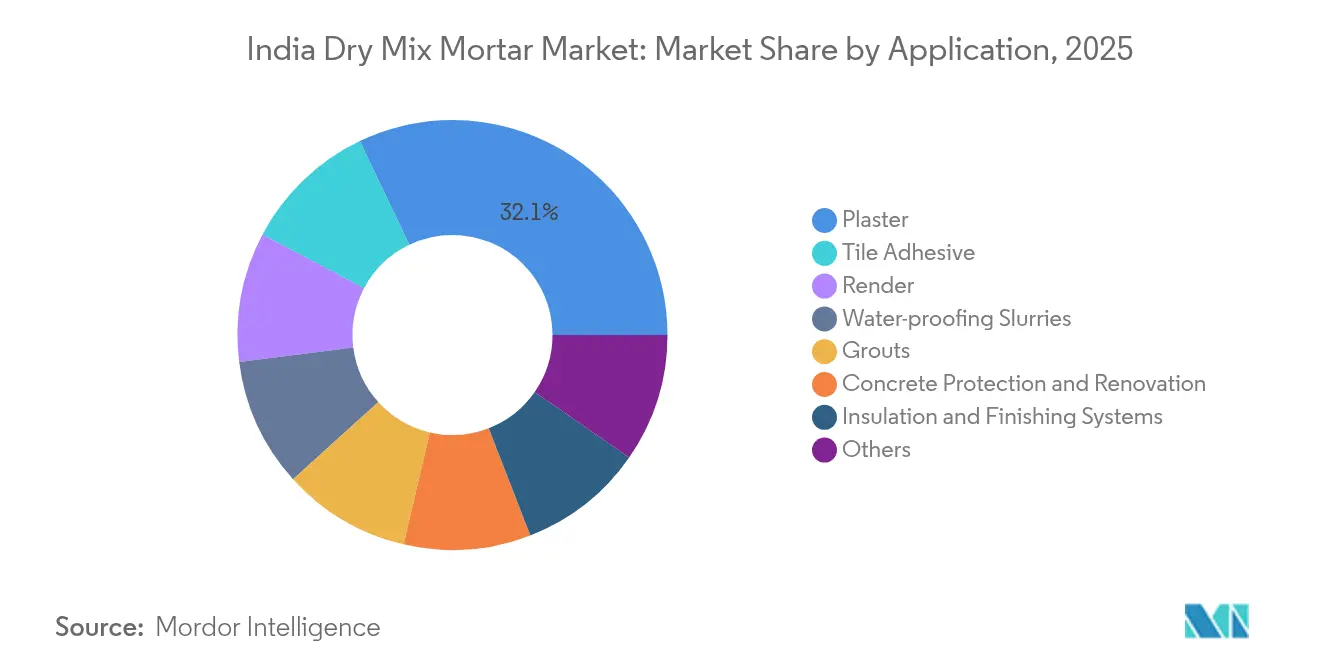

- By application, plaster led with 32.10% volume share in 2025; tile adhesives are forecast to record a 7.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

India Dry Mix Mortar Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid shift from on-site mixing to factory-blended mortars for quality and labour savings | +1.20% | National, with early adoption in metro cities and industrial corridors | Medium term (2-4 years) |

| Affordable-housing and PMAY-Urban project pipeline | +1.10% | National, concentrated in tier-2 and tier-3 cities with PMAY focus | Short term (≤ 2 years) |

| Mandatory EPR and PWM 2024 rules accelerating adoption of moisture-proof, recyclable sacks | +0.50% | National, stricter enforcement in Maharashtra, Gujarat, Tamil Nadu | Short term (≤ 2 years) |

| Growth of modular, prefab, and 3-D printed construction needing thin-bed mortars | +0.90% | Urban centers and industrial zones, early adoption in NCR, Bangalore, Pune | Long term (≥ 4 years) |

| Commercialisation of low-carbon blends (GGBS/bio-char) unlocking green-building credits | +0.80% | Metro cities with green building mandates, IT corridors | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Shift to Factory-Blended Mortars

Construction sites across India face skilled-labor scarcity and tighter completion windows, pushing contractors to adopt bagged mortars that only require water addition. Automated batching plants deliver uniform sand gradation and controlled admixture dosage, reducing rework on large transport corridors and metro-rail packages. Builders’ associations in Mumbai and Bengaluru report productivity gains of 10–15% after switching to silo-fed plaster systems, and warranty issuers now favor projects that document factory testing protocols. The India dry mix mortar market, therefore, absorbs capacity additions by integrated cement majors that retrofit existing grinding units with 20–40 TPH mixers. A concurrent rise in ready-mix concrete penetration to 30% validates broader acceptance of off-site cementitious materials.

Affordable Housing and PMAY-Urban Pipeline

Central-government backing for 20 million urban dwellings through FY 2025 keeps residential tendering buoyant in tier-2 locales such as Indore, Surat, and Lucknow. State housing boards specify pre-approved mortars for bricklaying and thin-joint masonry to accelerate wall raising, which enlarges distributor footprints in semi-urban clusters. Budgetary allocation of INR 80,671 crore in FY 2024-25 created predictable offtake for small-pack plaster lines suited to 300-sq-ft units, and transport subsidies under Gati Shakti ease inter-state shipment of bagged product. Developers also choose dry mixes to meet performance audits tied to interest-subvention subsidies, reinforcing volume visibility for producers through 2027.

Mandatory EPR and PWM 2024 Rules

Revised Plastic Waste Management regulations call for 30% recycled content in laminated sacks and full traceability of packaging material. Large mortar producers have migrated to multi-layer polyethylene bags with solvent-free inks that pass drop-test and moisture-ingress criteria. Investments in in-house recycling plants in Gujarat and Tamil Nadu lower overall compliance costs and allow brand owners to advertise circular-economy credentials. Smaller players lacking scale struggle with third-party collection fees, tilting market share toward integrated firms able to amortize sustainability spending.

Commercialization of Low-Carbon Blends

Public-sector tender documents in Mumbai and Hyderabad now award extra technical credit for mortars incorporating ground-granulated blast-furnace slag (GGBS) or calcined-clay binders. Green Building Council-tracked projects demand environmental product declarations, opening a premium niche for GGBS-bearing tile adhesive that secures IGBC points. Producers marketing 25–30% CO₂-reduced formulas report higher margins, offsetting marginally slower setting times through tailored accelerator dosing.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cement and polymer-additive price volatility | -1.80% | National, with higher impact in regions dependent on long-distance cement transport | Short term (≤ 2 years) |

| High capex for fully-automated dry-mix plants | -0.70% | Manufacturing hubs in Gujarat, Tamil Nadu, Maharashtra, Haryana | Medium term (2-4 years) |

| Compliance cost of India-EPR recycled-content mandates for multilayer sacks | -0.60% | National, stricter enforcement in industrialized states | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Cement and Polymer-Additive Price Volatility

Bagged mortar margins compressed in 2024 when all-India cement quotations slid 7% even as styrene-acrylate and redispersible-powder prices jumped 15% due to shipping bottlenecks. Manufacturers tied to spot-purchase models struggled to honor fixed-price supply contracts for highway packages. Hedging through quarterly price-escalation clauses is gaining favor, though tier-3 city retailers still resist mid-project revisions. The India dry mix mortar market thus sees integrated cement players prioritizing in-house consumption of clinker to buffer price shocks, whereas stand-alone mortar firms add silica-fume substitutes to limit polymer dosage.

High Capex for Fully-Automated Dry-Mix Plants

A 30 TPH twin-shaft mixer line with bulk-bag loading, micro-dosing screws, and inline sampling commands INR 50 million, excluding land cost. While amortization is feasible at 70% utilization, regional demand pockets often cycle below that threshold, extending payback beyond five years. Equipment suppliers now offer lease-finance and modular retrofits, but smaller entrepreneurs still operate semi-manual ribbon blenders. Capacity scale, therefore, concentrates among vertically integrated groups such as ACC and Ambuja, which commission automated plants adjacent to grinding units to capture silo-delivery opportunities[1]ACC, “Integrated Annual Report 2024-25,” acclimited.com .

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-Use Sector: Residential Dominance Meets Commercial Acceleration

The residential segment steered 52.02% of 2025 volumes and accounted for the largest slice of the India dry mix mortar market size because city-periphery housing and PMAY in-situ schemes consume high-tonnage plaster and masonry mortars. The predictable roll-out of 1- and 2-BHK layouts allows suppliers to standardize SKU mixes and cut inventory cycling times. Over the forecast horizon, commercial workspaces in Pune, Hyderabad, and Ahmedabad are forecast to deliver the fastest gains, and will propel the India dry mix mortar market as corporate campus fit-outs employ high-adhesion tile adhesive and self-leveling underlayments.

Traffic-oriented retail extensions, data-center shells, and hospitality refurbishments exhibit higher value-per-ton ratios than mainstream housing, encouraging manufacturers to introduce polymer-rich thin-bed mortars with rapid set times. Infrastructure and institutional sub-segments such as metro-station cladding and university expansions sustain steady baseline consumption, but price sensitivity in public tenders keeps margins tight.

By Application: Plaster Leadership Challenged by Tile Adhesive Innovation

Plaster held 32.10% of 2025 deliveries and remained the anchor application within the India dry mix mortar market size because most wall envelopes still rely on two-coat cement-sand plasters for fire and acoustic ratings. Urban renovation jobs now specify lightweight gypsum-blend plasters to reduce dead load, spurring formulators to incorporate expanded perlite. Tile adhesive represents the quickest-rising stream, and its 7.12% CAGR is raising the profile of polymer-modified blends advertised for 0-void bedding and water-resistance.

Large-format porcelain slabs and natural-stone cladding accelerate this swing away from thick-bed mortar, and training clinics run by Sika and Pidilite equip installers with notched-trowel know-how. Growth in waterproofing slurries accompanies heightened awareness of climate-induced moisture ingress in coastal Maharashtra and Odisha. Concrete protection mortars gain follow-through from bridge-deck overlay contracts sanctioned under the Bharatmala program.

Geography Analysis

Northern India harnesses a robust infrastructure drive, including expressways and dedicated freight corridors, that anchors repeat orders for silo-fed masonry mortars. Ready availability of clinker in Rajasthan and Himachal Pradesh trims inbound freight, letting producers quote sharper ex-plant rates. Delhi-NCR’s township boom further strengthens regional offtake.

Southern states, led by Tamil Nadu and Karnataka, are consolidating cement capacity under large groups, allowing bundled supply contracts that integrate mortar, tile adhesive, and waterproofing kits. Bengaluru’s tech campuses and Chennai’s industrial corridors both specify premium low-shrink grouts. Although laterite block construction in coastal Kerala necessitates customized bonding agents, suppliers opening new plants in Krishnagiri and Hosur cut lead times to these niche markets.

Western India blends petro-chemical infrastructure in Gujarat with high-rise redevelopment in Mumbai, making it an innovation hotspot for GGBS-rich and low-VOC mortars. Proximity to Nhava Sheva Port enables economical import of cellulose ethers, while strong environmental enforcement encourages producers to invest in roofed storage, dust extraction, and VOC abatement.

Competitive Landscape

Industry is moderately fragmented, with vertically integrated cement majors leveraging quarry control and nationwide dealer networks to supply value-added mortars at scale. Integrated cement majors such as UltraTech, ACC, and Ambuja command raw material security and distribution depth, and they collectively own bulk terminals in 15 coastal cities. Their vertically integrated models protect input costs and facilitate high-volume tender participation. Mid-tier chemical specialists—Pidilite, Sika, and MAPEI—compete through proprietary polymers, color-matched premixes, and onsite applicator training programs.

M&A surged in 2024, with ACC purchasing Orient Cement’s 8.5 MTPA capacity for INR 104 billion to gain central India limestone access, and Adani crossing 100 MTPA group capacity, letting it contemplate backward integration into construction chemicals[2]Adani Group, “Adani Acquires Orient Cement at Rs. 8,100 Crore Equity Value,” adani.com . JK Cement’s INR 3,000 crore expansion includes tile adhesive lines targeting aspirational retail chains. Small regional outfits still serve localized plaster markets but face compliance barriers around VOC and recycling declarations.

Product launches emphasize sustainability: Saint-Gobain’s GGBS mortars tout 30% lower embodied carbon, and Asian Paints introduced CoolPlast, merging thermal insulation with crack bridging. Plant automation is climbing; Readymix Construction Machinery logged a 40-unit order book for 20-TPH systems in 2025, showing capex appetite among mid-sized players. Market rivalry remains price-driven outside metro zones yet increasingly shifts toward technical credentials in urban build-outs.

India Dry Mix Mortar Industry Leaders

Adani Group

Asian Paints

Pidilite Industries Ltd.

Sika AG

UltraTech Cement Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Nuvoco Vistas Corp. announced an INR 200 crore investment to expand cement grinding capacity in Eastern India by 4 million Tons per annum by FY2026-27. The expansion includes a new grinding mill at the Arasmeta Cement Plant and debottlenecking initiatives at its Jojobera, Panagarh, and Odisha facilities.

- February 2025: Saint-Gobain, a French multinational corporation specializing in construction materials, acquired Fosroc, Inc. for approximately EUR 960 million (USD 1.03 billion). This acquisition strategically enhances Saint-Gobain's leadership in light and sustainable construction while significantly strengthening Fosroc's position as a key player in the global construction chemicals sector.

India Dry Mix Mortar Market Report Scope

Commercial, Industrial and Institutional, Infrastructure, Residential are covered as segments by End Use Sector. Concrete Protection and Renovation, Grouts, Insulation and Finishing Systems, Plaster, Render, Tile Adhesive, Water Proofing Slurries are covered as segments by Application.| Residential |

| Commercial |

| Infrastructure |

| Industrial and Institutional |

| Plaster |

| Render |

| Tile Adhesive |

| Grouts |

| Concrete Protection and Renovation |

| Water-proofing Slurries |

| Insulation and Finishing Systems |

| Others |

| By End-Use Sector | Residential |

| Commercial | |

| Infrastructure | |

| Industrial and Institutional | |

| By Application | Plaster |

| Render | |

| Tile Adhesive | |

| Grouts | |

| Concrete Protection and Renovation | |

| Water-proofing Slurries | |

| Insulation and Finishing Systems | |

| Others |

Market Definition

- END-USE SECTOR - Dry mix mortar consumed in the construction sectors such as commercial, residential, industrial, institutional, and infrastructure are considered under the scope of the study.

- PRODUCT/APPLICATION - Under the scope of the study, consumption of dry mix mortar products for plaster, render, tile adhesive, grouts, waterproofing slurries, concrete protection and renovation, insulated and finishing systems along with other applications are considered.

| Keyword | Definition |

|---|---|

| Accelerator | Accelerators are admixtures used to fasten the setting time of concrete by increasing the initial rate and speeding up the chemical reaction between cement and the mixing water. These are used to harden and increase the strength of concrete quickly. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Adhesives | Adhesives are bonding agents used to join materials by gluing. Adhesives can be used in construction for many applications, such as carpet laying, ceramic tiles, countertop lamination, etc. |

| Air Entraining Admixture | Air-entraining admixtures are used to improve the performance and durability of concrete. Once added, they create uniformly distributed small air bubbles to impart enhanced properties to the fresh and hardened concrete. |

| Alkyd | Alkyds are used in solvent-based paints such as construction and automotive paints, traffic paints, flooring resins, protective coatings for concrete, etc. Alkyd resins are formed by the reaction of an oil (fatty acid), a polyunsaturated alcohol (Polyol), and a polyunsaturated acid or anhydride. |

| Anchors and Grouts | Anchors and grouts are construction chemicals that stabilize and improve the strength and durability of foundations and structures like buildings, bridges, dams, etc. |

| Cementitious Fixing | Cementitious fixing is a process in which a cement-based grout is pumped under pressure to fill forms, voids, and cracks. It can be used in several settings, including bridges, marine applications, dams, and rock anchors. |

| Commercial Construction | Commercial construction comprises new construction of warehouses, malls, shops, offices, hotels, restaurants, cinemas, theatres, etc. |

| Concrete Admixtures | Concrete admixtures comprise water reducers, air entrainers, retarders, accelerators, superplasticizers, etc., added to concrete before or during mixing to modify its properties. |

| Concrete Protective Coatings | To provide specific protection, such as anti-carbonation or chemical resistance, a film-forming protective coat can be applied on the surface. Depending on the applications, different resins like epoxy, polyurethane, and acrylic can be used for concrete protective coatings. |

| Curing Compounds | Curing compounds are used to cure the surface of concrete structures, including columns, beams, slabs, and others. These curing compounds keep the moisture inside the concrete to give maximum strength and durability. |

| Epoxy | Epoxy is known for its strong adhesive qualities, making it a versatile product in many industries. It resists heat and chemical applications, making it an ideal product for anyone needing a stronghold under pressure. It is widely used in adhesives, electrical and electronics, paints, etc. |

| Fiber Wrapping Systems | Fiber Wrapping Systems are a part of construction repair and rehabilitation chemicals. It involves the strengthening of existing structures by wrapping structural members like beams and columns with glass or carbon fiber sheets. |

| Flooring Resins | Flooring resins are synthetic materials applied to floors to enhance their appearance, increase their resistance to wear and tear or provide protection from chemicals, moisture, and stains. Depending on the desired properties and the specific application, flooring resins are available in distinct types, such as epoxy, polyurethane, and acrylic. |

| High-Range Water Reducer (Super Plasticizer) | High-range water reducers are a type of concrete admixture that provides enhanced and improved properties when added to concrete. These are also called superplasticizers and are used to decrease the water-to-cement ratio in concrete. |

| Hot Melt Adhesives | Hot-melt adhesives are thermoplastic bonding materials applied as melts that achieve a solid state and resultant strength on cooling. They are commonly used for packaging, coatings, sanitary products, and tapes. |

| Industrial and Institutional Construction | Industrial and institutional construction includes new construction of hospitals, schools, manufacturing units, energy and power plants, etc. |

| Infrastructure Construction | Infrastructure construction includes new construction of railways, roads, seaways, airports, bridges, highways, etc. |

| Injection Grouting | The process of injecting grout into open joints, cracks, voids, or honeycombs in concrete or masonry structural members is known as injection grouting. It offers several benefits, such as strengthening a structure and preventing water infiltration. |

| Liquid-Applied Waterproofing Membranes | Liquid-Applied membrane is a monolithic, fully bonded, liquid-based coating suitable for many waterproofing applications. The coating cures to form a rubber-like elastomeric waterproof membrane and may be applied over many substrates, including asphalt, bitumen, and concrete. |

| Micro-concrete Mortars | Micro-concrete mortar is made up of cement, water-based resin, additives, mineral pigments, and polymers and can be applied on both horizontal and vertical surfaces. It can be used to refurbish residential complexes, commercial spaces, etc. |

| Modified Mortars | Modified Mortars include Portland cement and sand along with latex/polymer additives. The additives increase adhesion, strength, and shock resistance while also reducing water absorption. |

| Mold Release Agents | Mold release agents are sprayed or coated on the surface of molds to prevent a substrate from bonding to a molding surface. Several types of mold release agents, including silicone, lubricant, wax, fluorocarbons, and others, are used based on the type of substrates, including metals, steel, wood, rubber, plastic, and others. |

| Polyaspartic | Polyaspartic is a subset of polyurea. Polyaspartic floor coatings are typically two-part systems that consist of a resin and a catalyst to ease the curing process. It offers high durability and can withstand harsh environments. |

| Polyurethane | Polyurethane is a plastic material that exists in various forms. It can be tailored to be either rigid or flexible and is the material of choice for a broad range of end-user applications, such as adhesives, coatings, building insulation, etc. |

| Reactive Adhesives | A reactive adhesive is made of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Rebar Protectors | In concrete structures, rebar is one of the important components, and its deterioration due to corrosion is a major issue that affects the safety, durability, and life span of buildings and structures. For this reason, rebar protectors are used to protect against degrading effects, especially in infrastructure and industrial construction. |

| Repair and Rehabilitation Chemicals | Repair and Rehabilitation Chemicals include repair mortars, injection grouting materials, fiber wrapping systems, micro-concrete mortars, etc., used to repair and restore existing buildings and structures. |

| Residential Construction | Residential construction involves constructing new houses or spaces like condominiums, villas, and landed homes. |

| Resin Fixing | The process of using resins like epoxy and polyurethane for grouting applications is called resin fixing. Resin fixing offers several advantages, such as high compressive and tensile strength, negligible shrinkage, and greater chemical resistance compared to cementitious fixing. |

| Retarder | Retarders are admixtures used to slow down the setting time of concrete. These are usually added with a dosage rate of around 0.2% -0.6% by weight of cement. These admixtures slow down hydration or lower the rate at which water penetrates the cement particles by making concrete workable for a long time. |

| Sealants | A sealant is a viscous material that has little or no flow qualities, which causes it to remain on surfaces where they are applied. Sealants can also be thinner, enabling penetration to a certain substance through capillary action. |

| Sheet Waterproofing Membranes | Sheet membrane systems are reliable and durable thermoplastic waterproofing solutions that are used for waterproofing applications even in the most demanding below-ground structures, including those exposed to highly aggressive ground conditions and stress. |

| Shrinkage Reducing Admixture | Shrinkage-reducing admixtures are used to reduce concrete shrinkage, whether from drying or self-desiccation. |

| Silicone | Silicone is a polymer that contains silicon combined with carbon, hydrogen, oxygen, and, in some cases, other elements. It is an inert synthetic compound that comes in various forms, such as oil, rubber, and resin. Due to its heat-resistant properties, it finds applications in sealants, adhesives, lubricants, etc. |

| Solvent-borne Adhesives | Solvent-borne adhesives are mixtures of solvents and thermoplastic or slightly cross-linked polymers such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers. |

| Surface Treatment Chemicals | Surface treatment chemicals are chemicals used to treat concrete surfaces, including roofs, vertical surfaces, and others. They act as curing compounds, demolding agents, rust removers, and others. They are cost-effective and can be used on roadways, pavements, parking lots, and others. |

| Viscosity Modifier | Viscosity Modifiers are concrete admixtures used to change various properties of admixtures, including viscosity, workability, cohesiveness, and others. These are usually added with a dosage of around 0.01% to 0.1% by weight of cement. |

| Water Reducer | Water reducers, also called plasticizers, are a type of admixture used to decrease the water-to-cement ratio in the concrete, thereby increasing the durability and strength of concrete. Various water reducers include refined lignosulfonates, gluconates, hydroxycarboxylic acids, sugar acids, and others. |

| Water-borne Adhesives | Water-borne adhesives use water as a carrier or diluting medium to disperse resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a dilutant rather than a volatile organic solvent. |

| Waterproofing Chemicals | Waterproofing chemicals are designed to protect a surface from the perils of leakage. A waterproofing chemical is a protective coating or primer applied to a structure's roof, retaining walls, or basement. |

| Waterproofing Membranes | Waterproofing membranes are liquid-applied or self-adhering layers of water-tight materials that prevent water from penetrating or damaging a structure when applied to roofs, walls, foundations, basements, bathrooms, and other areas exposed to moisture or water. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms