Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

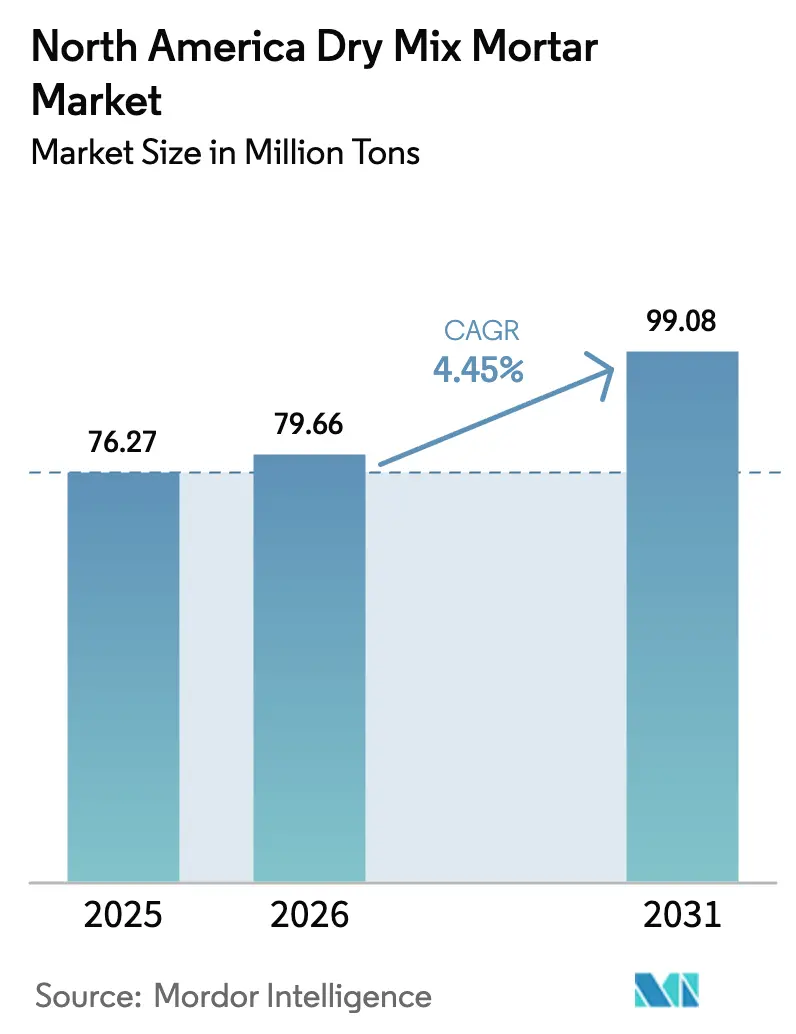

| Base Year Market Size (2025) | 76.27 Million tons |

| Market Volume (2026) | 79.66 Million tons |

| Market Volume (2031) | 99.08 Million tons |

| Growth Rate (2026 - 2031) | 4.45% CAGR |

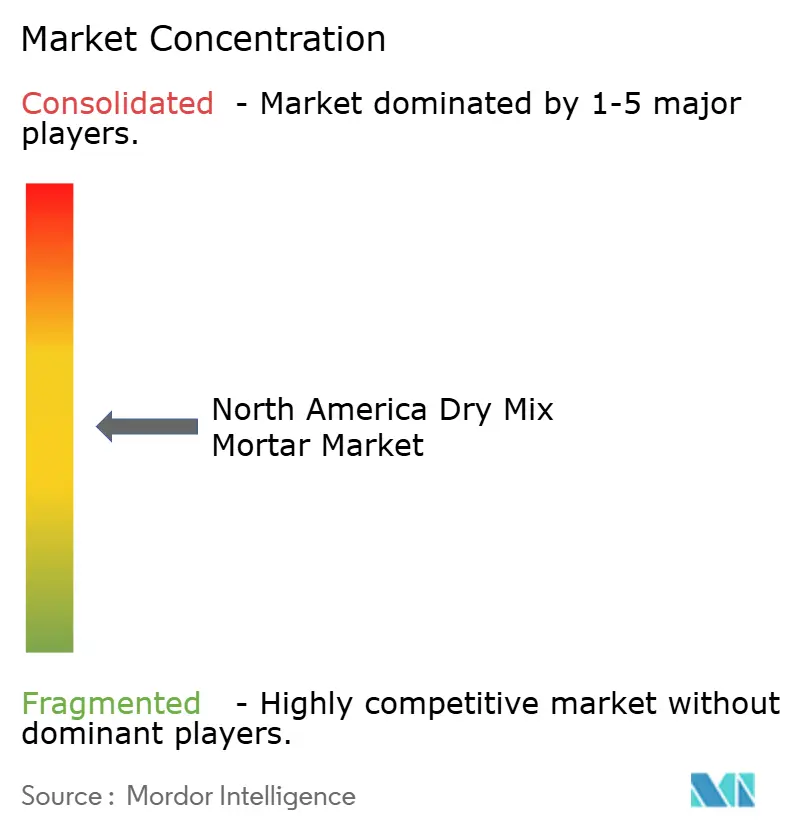

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Dry Mix Mortar Market Analysis by Mordor Intelligence

The North America Dry Mix Mortar Market size is expected to grow from 76.27 million tons in 2025 to 79.66 million tons in 2026 and is forecast to reach 99.08 million tons by 2031 at 4.45% CAGR over 2026-2031. Anchored by resilient construction spending, the region’s builders are pivoting toward factory-produced blends that cut on-site labor, shorten project timelines, and elevate quality consistency. Infrastructure renewal funded by the Infrastructure Investment and Jobs Act (IIJA) continues to pull large volumes of specialty repair and protection mortars into transportation and water projects. Single-family housing starts have staged a measured comeback, and the Southeast–Southwest migration wave is increasing demand for high-performance plasters, tile adhesives, and waterproofing systems. Modular construction, although still a niche market, is growing at double-digit rates; its controlled environments favor premium formulations that meet stringent consistency standards. Supply constraints in skilled labor and the push for lower-carbon materials further propel the shift from job-site mixes to pre-blended alternatives, reinforcing the growth trajectory of the North America dry mix mortar market.

Key Report Takeaways

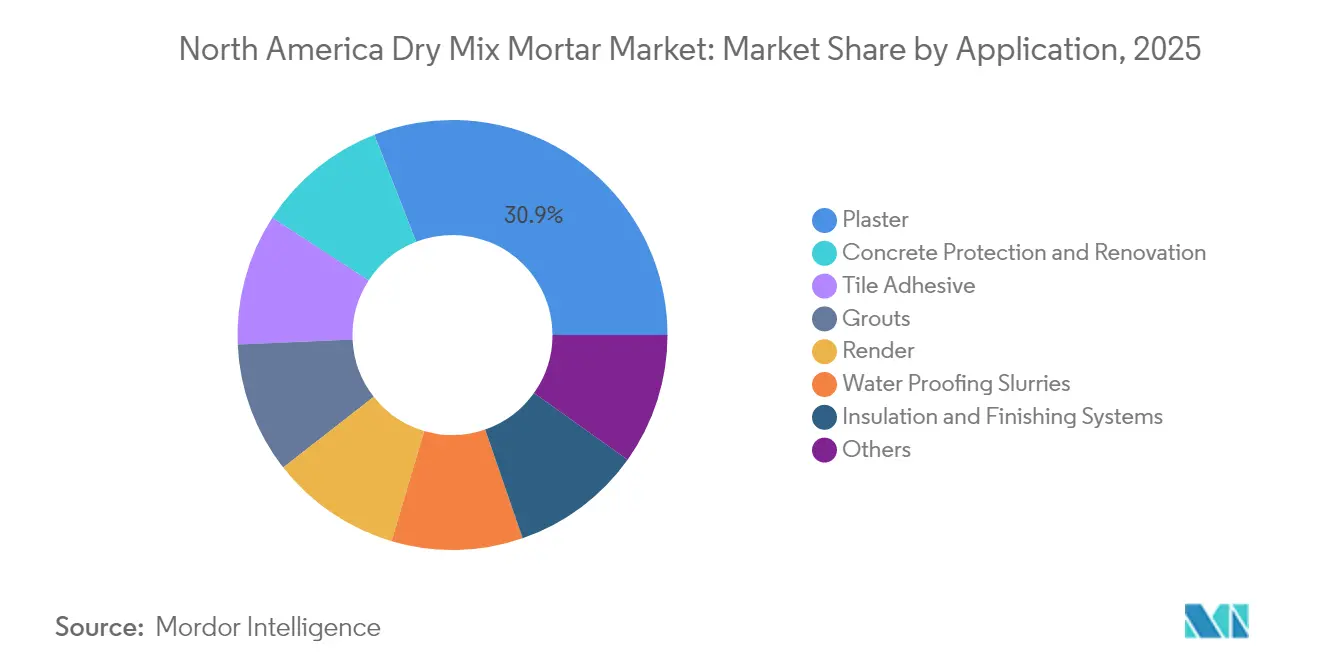

- By application, plaster led with 30.92% of the North America dry mix mortar market share in 2025. Concrete protection and renovation applications are projected to expand at a 6.08% CAGR through 2031, the fastest among all uses.

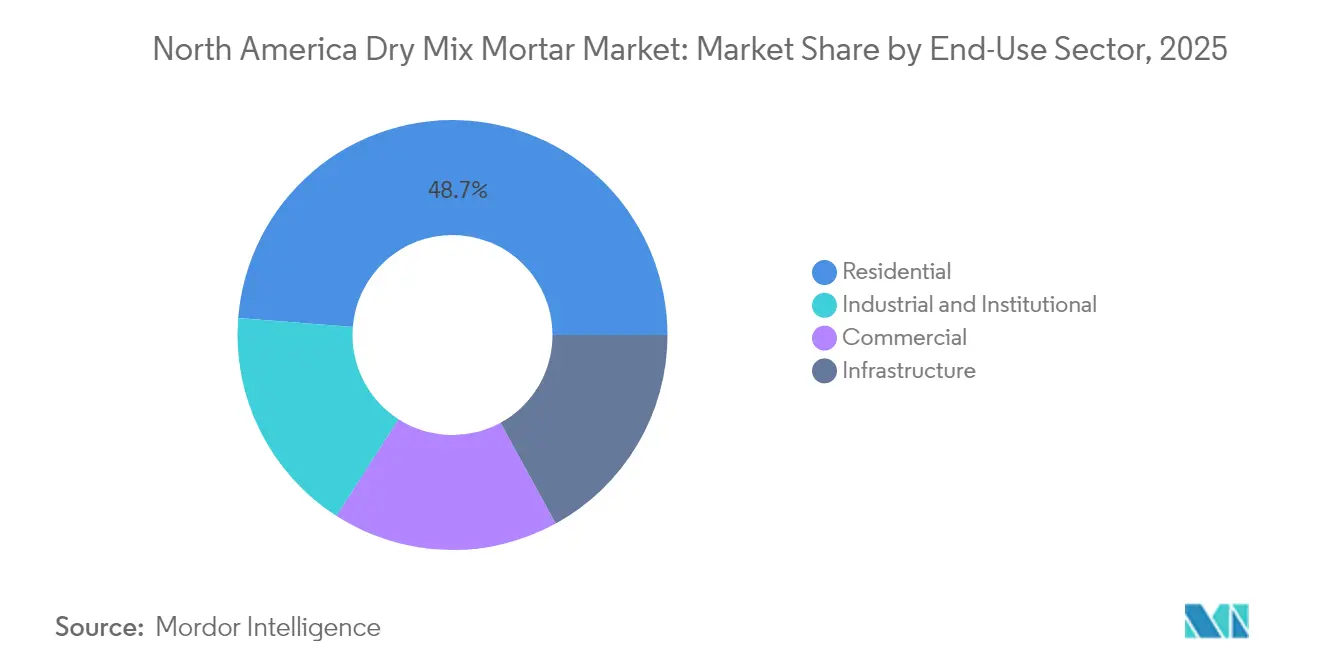

- By end-use sector, residential construction accounted for 48.74% share of the North America dry mix mortar market size in 2025, while industrial and institutional projects are forecast to grow at 5.82% CAGR into 2031.

- By geography, the United States dominated with a 75.12% share in 2025; Mexico is poised to register a 5.19% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Dry Mix Mortar Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in single-family housing starts | +1.2% | United States primarily, spillover to Canada | Medium term (2-4 years) |

| Accelerated rehabilitation of ageing infrastructure | +1.8% | North America-wide, concentrated in US Northeast and Midwest | Long term (≥ 4 years) |

| Shift toward off-site construction | +0.7% | United States and Canada urban centers | Medium term (2-4 years) |

| Rapid adoption of lightweight EIFS systems | +0.9% | North America, strongest in climate-controlled regions | Short term (≤ 2 years) |

| OEM pre-blended formulations for 3-D printing | +0.6% | United States and Canada, concentrated in tech hubs | Long term (≥ 4 years) |

| Carbon-curing incentives in U.S. Inflation Reduction Act | +0.4% | United States primarily, with cross-border supply effects | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in Single-Family Housing Starts

Single-family starts rebounded to 968,000 units in 2024, reversing two years of contraction and signaling stable demand for plasters, tile adhesives, and waterproofing slurries. Tight resale housing inventories have kept builders active despite higher mortgage rates, and demographic momentum from millennials entering peak home-buying years adds further lift. In climate-sensitive Sunbelt markets, builders increasingly favor pre-blended mortars that perform reliably under variable humidity and heat. The National Association of Home Builders anticipates inventory shortfalls persisting through 2027, which sustains premium product demand among contractors seeking schedule certainty[1]National Association of Home Builders, “Housing Forecast,” nahb.org. These trends collectively deepen the adoption of factory-formulated mixes, cementing the North America dry mix mortar market as a core beneficiary of the detached-housing upswing.

Accelerated Rehabilitation of Ageing Infrastructure

The IIJA injects USD 550 billion in new federal outlays, channeling a sizeable share toward bridges, tunnels, and water systems that require high-performance repair mortars. Roughly 45,000 structurally deficient bridges will need concrete protection products able to withstand de-icing salts and freeze-thaw cycles[2]American Road & Transportation Builders Association, “Transportation Investment,” artba.org. State co-funding multiplies federal dollars, as California and Texas together earmark nearly USD 90 billion for complementary works through 2030. Specialized mortars that offer rapid set, low shrinkage, and sulfate resistance now represent mission-critical inputs, positioning concrete protection and renovation as the fastest-growing application within the North America dry mix mortar market.

Shift Toward Off-Site Construction

Factory-built modules captured only 3–6% of regional building activity in 2024, yet volumes are rising 15–20% annually in multifamily and commercial projects. In controlled plants, automated dosage systems ensure every batch meets specification, cutting material waste by up to 40% and reducing remedial work. Leading contractors such as Turner Construction and Skanska have formalized procurement guidelines that prioritize pre-bagged mortars for factory assembly, thereby enlarging premium price corridors. Emerging state regulations, notably California’s streamlined factory-built housing codes, are lowering permitting hurdles and extending modular adoption into affordable housing. These advances underpin a structural rise in off-site demand within the North America dry mix mortar market.

Rapid Adoption of Lightweight EIFS Systems

Energy-code tightening under California’s Title 24 and similar measures in New York, Massachusetts, and Ontario is accelerating uptake of lightweight exterior insulation and finish systems (EIFS). Polymer-modified dry mix mortars enable thinner coats without sacrificing impact resistance, allowing architects to pursue streamlined façades while meeting R-value targets. In seismic and retrofit applications, reduced structural loading is a critical advantage. Early adopters are layering carbon-cured binders—eligible for Inflation Reduction Act tax incentives—into EIFS formulations, creating a pathway to carbon-negative building envelopes. As a result, EIFS-related mortar consumption is gaining share inside the broader North America dry mix mortar market.

Restraints Impact Analysis*

| Restraints | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High price sensitivity in residential retrofit | -0.8% | North America-wide, acute in rural and suburban markets | Short term (≤ 2 years) |

| Volatility in cement and polymer prices | -1.1% | North America, amplified by supply chain dependencies | Medium term (2-4 years) |

| Skilled labour shortage delaying onsite trials | -0.5% | North America-wide, most severe in Canada and US Northeast | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High Price Sensitivity in Residential Retrofit

Renovation spending dipped in 2024 as rising rates eroded home equity and curbed discretionary upgrades. In lower-income Midwest and Appalachian counties, price gaps of 25–40% between basic sand-cement mixes and premium dry mortars remain a deterrent. DIY segments often default to job-site blends, while professional contractors weigh higher material cost against labor savings. Market participants can mitigate sensitivity by offering small-format packaging, training programs that highlight productivity gains, and tiered product lines with value-engineered additives. These tactics ease, but do not fully offset, the near-term drag on portions of the North America dry mix mortar market.

Volatility in Cement and Polymer Prices

Portland cement prices increased in 2024 amid elevated energy costs, while polymer modifiers experienced cost fluctuations tied to petrochemical volatility. Energy accounts for roughly 40% of kiln operating expenses, making cement manufacturers vulnerable to fluctuations in natural-gas prices. Supply diversification strategies—such as additional grinding terminals, broader procurement of waste-derived fuels, and long-term resin contracts—help insulate margins; however, pass-through lags can disrupt bid pricing. For formulators, unpredictable input costs necessitate dynamic pricing models and expanded raw-material storage, prompting some customers to reconsider lower-grade alternatives. Persistent volatility remains the chief economic restraint on the North America dry mix mortar market into the medium term.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By End-Use Sector: Industrial Momentum Outpaces Traditional Segments

Residential construction owned 48.74% of the North America dry mix mortar market size in 2025, lifted by single-family starts and steady multifamily completions. However, industrial and institutional segments are projected to advance at a 5.82% CAGR through 2031, outstripping other sectors. Data-center construction—aimed at meeting the cloud-computing boom—necessitates floor-leveling and thermal-resistant mortars that withstand elevated equipment loads. Healthcare facility upgrades demand anti-microbial, low-VOC tile adhesives, whereas manufacturing reshoring spurs specialty mortars for chemical-resistant floors and heavy-traffic aisles.

Commercial office developments show mixed trajectories as hybrid work persists, yet adaptive-reuse projects often specify high-bond mortars for new partitions. Educational infrastructure gains momentum via federal K-12 modernization grants, adding to institutional demand. Infrastructure projects funnel large tonnage into transportation and public-works upgrades, but the highest unit prices accrue in industrial cleanrooms and high-spec healthcare suites. This diverse yet performance-intensive demand matrix further diversifies the North America dry mix mortar market, insulating it from cyclical swings in any one sector.

By Application: Specialized Formulations Deepen Value Creation

Plaster retained the largest slice of the North America dry mix mortar market share at 30.92% in 2025, buoyed by the housing recovery and architects’ preference for textured wall finishes. Concrete protection and renovation applications, though smaller in tonnage, are slated to grow at a 6.08% CAGR, reflecting bridge rehabs and water-treatment upgrades mandated by IIJA funding. Tile-adhesive demand tracks kitchen and bath remodels that follow demographic shifts to Sunbelt states, while grout consumption rises alongside large-format tile trends that require low-shrinkage mortars. Waterproofing slurries are gaining a foothold as building codes strengthen below-grade moisture protection. Within this landscape, commodity plasters face price pressure, whereas specialized blends achieve premium margins, reinforcing the segmentation of the North America dry mix mortar market.

Although plaster commands volume, render and insulation-finish systems are capturing designers’ attention through energy-efficiency credits and aesthetic versatility, high elasticity renders satisfy seismic compliance in California, and acrylic-enhanced mixes resist ultraviolet degradation in Southwest climates. Other niche applications—decorative overlays, fast-set floor screeds, and self-leveling underlayments—benefit from the labor-saving proposition of factory-blended products. Segment convergence is also visible; EIFS packages integrate base-coat, adhesive, and finishing mortars, anchoring multifunctional demand in a single procurement. Collectively, these shifts drive value over volume, expanding the North America dry mix mortar market size for high-performance applications.

Geography Analysis

The United States contributed 75.12% of North America dry mix mortar market share in 2025, a reflection of its extensive housing stock and unmatched infrastructure backlog. Sunbelt states lead residential momentum, while the Midwest and Northeast channel most rehabilitation spending into highways, bridges, and tunnels. Plant proximity affords major producers logistics efficiencies, but localized shortages in skilled masons push contractors toward easier-to-install factory blends. Federal Buy America clauses add complexity, nudging suppliers toward domestic sourcing of additives and packaging.

Mexico, though smaller in volume, is slated for the swiftest expansion at 5.19% CAGR, driven by near-shored automotive and electronics plants and associated transport corridors. The US-Mexico-Canada Agreement (USMCA) streamlines cross-border supply chains, helping U.S. producers penetrate northern Mexican states with high-value mortars. Industrial facilities in Nuevo León and Chihuahua deploy dust-controlled floor screeds and ultra-flat toppings that satisfy ISO clean-room standards. Canada exhibits steady, climate-conditioned demand; cold-weather admixtures and low-carbon cements dominate specifications in Ontario and British Columbia. Immigration-driven housing formation counters cooling in some urban high-rise markets, keeping the broader geography segment integral to the North America dry mix mortar market.

Competitive Landscape

The competitive landscape of the North America dry mix mortar market is moderately fragmented. Multinational giants leverage vertically integrated cement, aggregate, and admixture networks to secure raw-material cost advantages and nationwide distribution footprints. Regional specialists focus on niche technologies—rapid-set systems, polymer-rich tile adhesives, and consumer-oriented repair mortars. Their agility allows swift product customization and strong contractor loyalty, offsetting the scale advantages of larger rivals. New entrants funnel venture funding into bio-based additives and 3D-printing mortars, though most remain at pilot scale due to regulatory hurdles and performance validation lag. Digital tools—mobile apps that guide batch mixing, QR-coded bags linking to specification sheets—are becoming table stakes for market participants aiming to differentiate on service rather than solely on price. Forward strategy centers on sustainability credentials and supply-chain resilience. Plants equipped with alternative-fuel kilns and automated bagging lines can rapidly dial production mixes to match fluctuating demand profiles. Most majors target 30–40% greenhouse-gas reduction in mortar lines by 2030, aligning with customer ESG goals. Collectively, these efforts intensify rivalry yet lift the innovation baseline, a dynamic that ultimately benefits end users across the North America dry mix mortar market.

North America Dry Mix Mortar Industry Leaders

Sika AG

Saint-Gobain

Ardex Group

HOLCIM

CEMEX S.A.B. de C.V.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: HOLCIM, in collaboration with ELEMENTAL, introduced a novel biochar-based technology that enables mortar to function as a carbon sink. This innovation integrates biochar, significantly reducing CO₂ emissions without compromising performance.

- December 2024: Sika AG broke ground on a new 250,000 sq. ft. mortar production facility in Upper Deerfield Township, New Jersey, with operations expected to commence by late 2025. This strategic investment strengthens Sika’s supply chain in the Northeast United States and enhances proximity to key metropolitan markets.

North America Dry Mix Mortar Market Report Scope

Commercial, Industrial and Institutional, Infrastructure, Residential are covered as segments by End Use Sector. Concrete Protection and Renovation, Grouts, Insulation and Finishing Systems, Plaster, Render, Tile Adhesive, Water Proofing Slurries are covered as segments by Application. Canada, Mexico, United States are covered as segments by Country.By End-Use Sector

| Commercial |

| Industrial and Institutional |

| Infrastructure |

| Residential |

By Application

| Plaster |

| Render |

| Tile Adhesive |

| Grouts |

| Water Proofing Slurries |

| Concrete Protection and Renovation |

| Insulation and Finishing Systems |

| Others |

By Country

| United States |

| Canada |

| Mexico |

| By End-Use Sector | Commercial |

| Industrial and Institutional | |

| Infrastructure | |

| Residential | |

| By Application | Plaster |

| Render | |

| Tile Adhesive | |

| Grouts | |

| Water Proofing Slurries | |

| Concrete Protection and Renovation | |

| Insulation and Finishing Systems | |

| Others | |

| By Country | United States |

| Canada | |

| Mexico |

Market Definition

- END-USE SECTOR - Dry mix mortar consumed in the construction sectors such as commercial, residential, industrial, institutional, and infrastructure are considered under the scope of the study.

- PRODUCT/APPLICATION - Under the scope of the study, consumption of dry mix mortar products for plaster, render, tile adhesive, grouts, waterproofing slurries, concrete protection and renovation, insulated and finishing systems along with other applications are considered.

| Keyword | Definition |

|---|---|

| Accelerator | Accelerators are admixtures used to fasten the setting time of concrete by increasing the initial rate and speeding up the chemical reaction between cement and the mixing water. These are used to harden and increase the strength of concrete quickly. |

| Acrylic | This synthetic resin is a derivative of acrylic acid. It forms a smooth surface and is mainly used for various indoor applications. The material can also be used for outdoor applications with a special formulation. |

| Adhesives | Adhesives are bonding agents used to join materials by gluing. Adhesives can be used in construction for many applications, such as carpet laying, ceramic tiles, countertop lamination, etc. |

| Air Entraining Admixture | Air-entraining admixtures are used to improve the performance and durability of concrete. Once added, they create uniformly distributed small air bubbles to impart enhanced properties to the fresh and hardened concrete. |

| Alkyd | Alkyds are used in solvent-based paints such as construction and automotive paints, traffic paints, flooring resins, protective coatings for concrete, etc. Alkyd resins are formed by the reaction of an oil (fatty acid), a polyunsaturated alcohol (Polyol), and a polyunsaturated acid or anhydride. |

| Anchors and Grouts | Anchors and grouts are construction chemicals that stabilize and improve the strength and durability of foundations and structures like buildings, bridges, dams, etc. |

| Cementitious Fixing | Cementitious fixing is a process in which a cement-based grout is pumped under pressure to fill forms, voids, and cracks. It can be used in several settings, including bridges, marine applications, dams, and rock anchors. |

| Commercial Construction | Commercial construction comprises new construction of warehouses, malls, shops, offices, hotels, restaurants, cinemas, theatres, etc. |

| Concrete Admixtures | Concrete admixtures comprise water reducers, air entrainers, retarders, accelerators, superplasticizers, etc., added to concrete before or during mixing to modify its properties. |

| Concrete Protective Coatings | To provide specific protection, such as anti-carbonation or chemical resistance, a film-forming protective coat can be applied on the surface. Depending on the applications, different resins like epoxy, polyurethane, and acrylic can be used for concrete protective coatings. |

| Curing Compounds | Curing compounds are used to cure the surface of concrete structures, including columns, beams, slabs, and others. These curing compounds keep the moisture inside the concrete to give maximum strength and durability. |

| Epoxy | Epoxy is known for its strong adhesive qualities, making it a versatile product in many industries. It resists heat and chemical applications, making it an ideal product for anyone needing a stronghold under pressure. It is widely used in adhesives, electrical and electronics, paints, etc. |

| Fiber Wrapping Systems | Fiber Wrapping Systems are a part of construction repair and rehabilitation chemicals. It involves the strengthening of existing structures by wrapping structural members like beams and columns with glass or carbon fiber sheets. |

| Flooring Resins | Flooring resins are synthetic materials applied to floors to enhance their appearance, increase their resistance to wear and tear or provide protection from chemicals, moisture, and stains. Depending on the desired properties and the specific application, flooring resins are available in distinct types, such as epoxy, polyurethane, and acrylic. |

| High-Range Water Reducer (Super Plasticizer) | High-range water reducers are a type of concrete admixture that provides enhanced and improved properties when added to concrete. These are also called superplasticizers and are used to decrease the water-to-cement ratio in concrete. |

| Hot Melt Adhesives | Hot-melt adhesives are thermoplastic bonding materials applied as melts that achieve a solid state and resultant strength on cooling. They are commonly used for packaging, coatings, sanitary products, and tapes. |

| Industrial and Institutional Construction | Industrial and institutional construction includes new construction of hospitals, schools, manufacturing units, energy and power plants, etc. |

| Infrastructure Construction | Infrastructure construction includes new construction of railways, roads, seaways, airports, bridges, highways, etc. |

| Injection Grouting | The process of injecting grout into open joints, cracks, voids, or honeycombs in concrete or masonry structural members is known as injection grouting. It offers several benefits, such as strengthening a structure and preventing water infiltration. |

| Liquid-Applied Waterproofing Membranes | Liquid-Applied membrane is a monolithic, fully bonded, liquid-based coating suitable for many waterproofing applications. The coating cures to form a rubber-like elastomeric waterproof membrane and may be applied over many substrates, including asphalt, bitumen, and concrete. |

| Micro-concrete Mortars | Micro-concrete mortar is made up of cement, water-based resin, additives, mineral pigments, and polymers and can be applied on both horizontal and vertical surfaces. It can be used to refurbish residential complexes, commercial spaces, etc. |

| Modified Mortars | Modified Mortars include Portland cement and sand along with latex/polymer additives. The additives increase adhesion, strength, and shock resistance while also reducing water absorption. |

| Mold Release Agents | Mold release agents are sprayed or coated on the surface of molds to prevent a substrate from bonding to a molding surface. Several types of mold release agents, including silicone, lubricant, wax, fluorocarbons, and others, are used based on the type of substrates, including metals, steel, wood, rubber, plastic, and others. |

| Polyaspartic | Polyaspartic is a subset of polyurea. Polyaspartic floor coatings are typically two-part systems that consist of a resin and a catalyst to ease the curing process. It offers high durability and can withstand harsh environments. |

| Polyurethane | Polyurethane is a plastic material that exists in various forms. It can be tailored to be either rigid or flexible and is the material of choice for a broad range of end-user applications, such as adhesives, coatings, building insulation, etc. |

| Reactive Adhesives | A reactive adhesive is made of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Rebar Protectors | In concrete structures, rebar is one of the important components, and its deterioration due to corrosion is a major issue that affects the safety, durability, and life span of buildings and structures. For this reason, rebar protectors are used to protect against degrading effects, especially in infrastructure and industrial construction. |

| Repair and Rehabilitation Chemicals | Repair and Rehabilitation Chemicals include repair mortars, injection grouting materials, fiber wrapping systems, micro-concrete mortars, etc., used to repair and restore existing buildings and structures. |

| Residential Construction | Residential construction involves constructing new houses or spaces like condominiums, villas, and landed homes. |

| Resin Fixing | The process of using resins like epoxy and polyurethane for grouting applications is called resin fixing. Resin fixing offers several advantages, such as high compressive and tensile strength, negligible shrinkage, and greater chemical resistance compared to cementitious fixing. |

| Retarder | Retarders are admixtures used to slow down the setting time of concrete. These are usually added with a dosage rate of around 0.2% -0.6% by weight of cement. These admixtures slow down hydration or lower the rate at which water penetrates the cement particles by making concrete workable for a long time. |

| Sealants | A sealant is a viscous material that has little or no flow qualities, which causes it to remain on surfaces where they are applied. Sealants can also be thinner, enabling penetration to a certain substance through capillary action. |

| Sheet Waterproofing Membranes | Sheet membrane systems are reliable and durable thermoplastic waterproofing solutions that are used for waterproofing applications even in the most demanding below-ground structures, including those exposed to highly aggressive ground conditions and stress. |

| Shrinkage Reducing Admixture | Shrinkage-reducing admixtures are used to reduce concrete shrinkage, whether from drying or self-desiccation. |

| Silicone | Silicone is a polymer that contains silicon combined with carbon, hydrogen, oxygen, and, in some cases, other elements. It is an inert synthetic compound that comes in various forms, such as oil, rubber, and resin. Due to its heat-resistant properties, it finds applications in sealants, adhesives, lubricants, etc. |

| Solvent-borne Adhesives | Solvent-borne adhesives are mixtures of solvents and thermoplastic or slightly cross-linked polymers such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers. |

| Surface Treatment Chemicals | Surface treatment chemicals are chemicals used to treat concrete surfaces, including roofs, vertical surfaces, and others. They act as curing compounds, demolding agents, rust removers, and others. They are cost-effective and can be used on roadways, pavements, parking lots, and others. |

| Viscosity Modifier | Viscosity Modifiers are concrete admixtures used to change various properties of admixtures, including viscosity, workability, cohesiveness, and others. These are usually added with a dosage of around 0.01% to 0.1% by weight of cement. |

| Water Reducer | Water reducers, also called plasticizers, are a type of admixture used to decrease the water-to-cement ratio in the concrete, thereby increasing the durability and strength of concrete. Various water reducers include refined lignosulfonates, gluconates, hydroxycarboxylic acids, sugar acids, and others. |

| Water-borne Adhesives | Water-borne adhesives use water as a carrier or diluting medium to disperse resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a dilutant rather than a volatile organic solvent. |

| Waterproofing Chemicals | Waterproofing chemicals are designed to protect a surface from the perils of leakage. A waterproofing chemical is a protective coating or primer applied to a structure's roof, retaining walls, or basement. |

| Waterproofing Membranes | Waterproofing membranes are liquid-applied or self-adhering layers of water-tight materials that prevent water from penetrating or damaging a structure when applied to roofs, walls, foundations, basements, bathrooms, and other areas exposed to moisture or water. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms