Dodecanedioic Acid (DDDA) Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

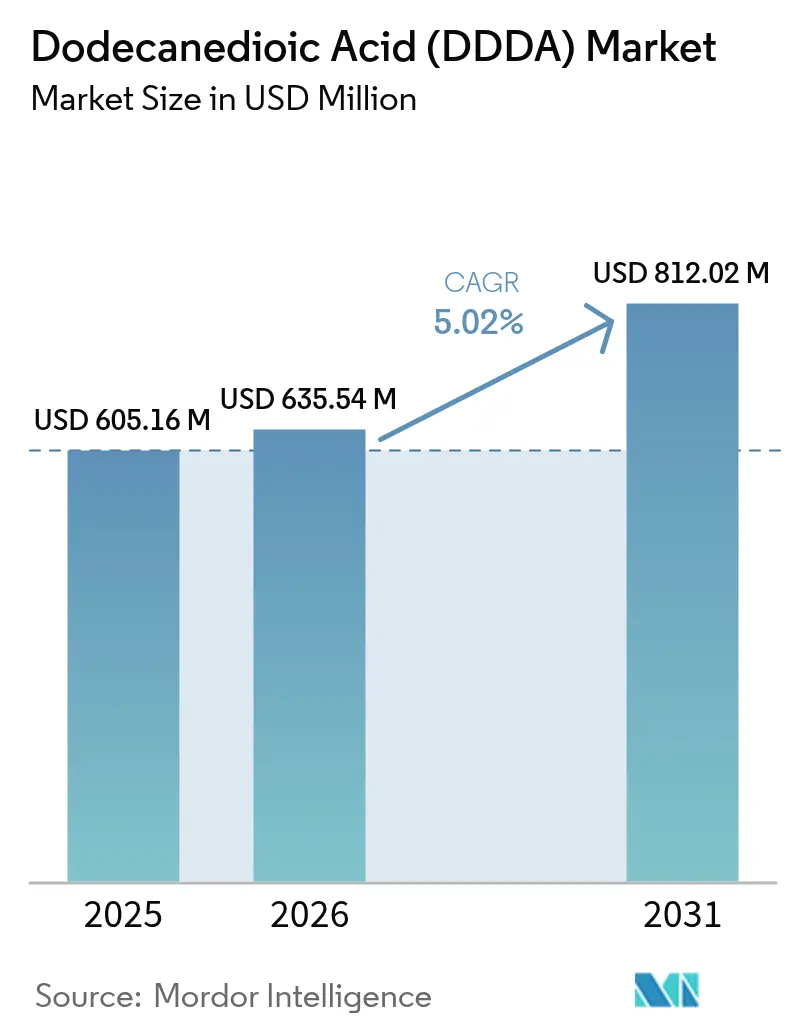

| Market Size (2026) | USD 635.54 Million |

| Market Size (2031) | USD 812.02 Million |

| Growth Rate (2026 - 2031) | 5.02% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dodecanedioic Acid (DDDA) Market Analysis by Mordor Intelligence

Dodecanedioic Acid Market size in 2026 is estimated at USD 635.54 million, growing from 2025 value of USD 605.16 million with 2031 projections showing USD 812.02 million, growing at 5.02% CAGR over 2026-2031. The expansion is underpinned by the compound’s critical role in automotive lightweighting, rising demand for EV-grade thermal-management fluids, and the flexibility producers enjoy in switching between petrochemical and bio-based manufacturing routes. Robust Asia-Pacific consumption, process innovation that lowers bio-route costs, and the segment’s high chemical stability together reinforce the dodecanedioic acid market growth outlook. Competitive advantages accrue to vertically integrated players able to secure feedstock, comply with tightening REACH norms and tailor grades for emerging high-value applications.

Key Report Takeaways

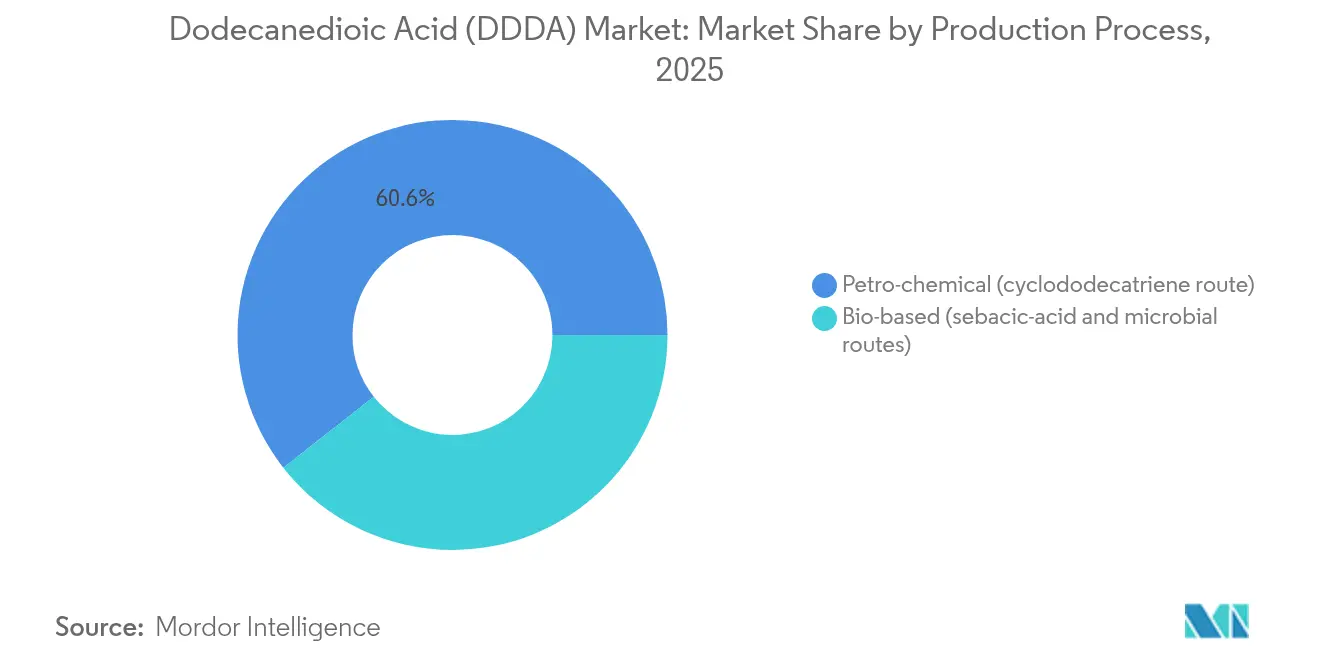

- By production process, the petro-chemical route retained 60.58% of the dodecanedioic acid market share in 2025, while bio-based routes posted the fastest 8.60% CAGR through 2031.

- By application, resins led with a 43.12% revenue share in 2025; powder coatings are projected to expand at a 5.62% CAGR to 2031.

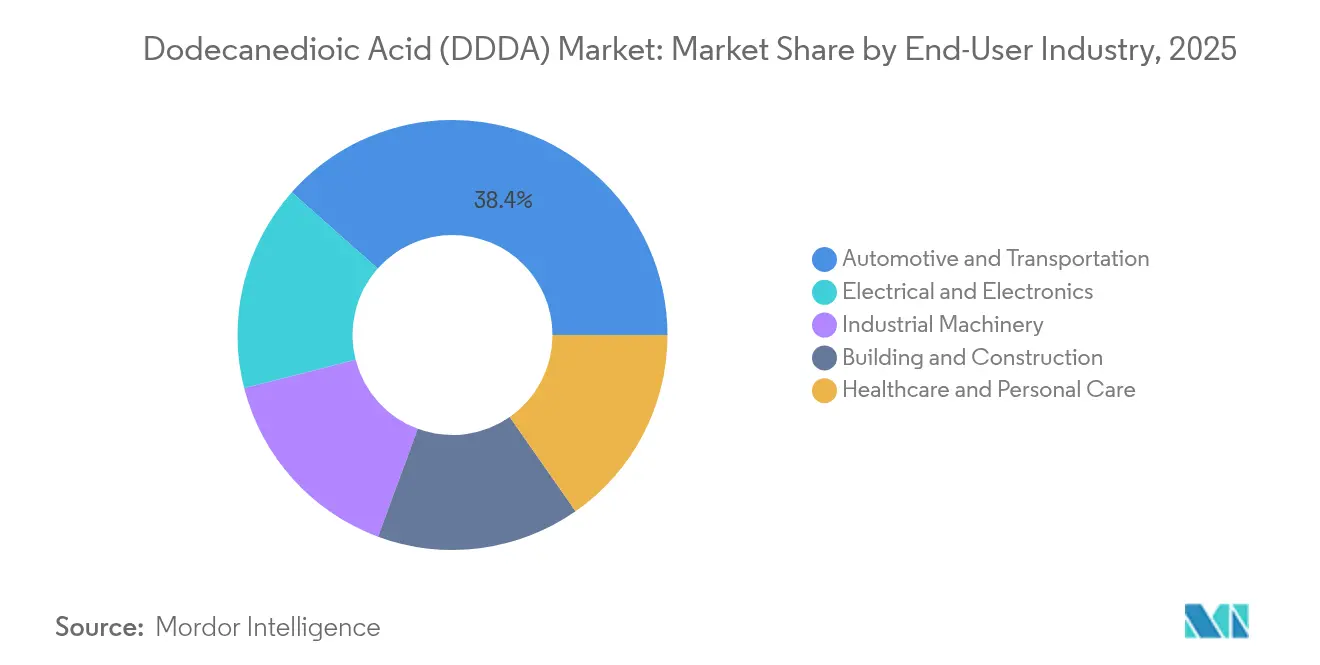

- By end-user industry, automotive and transportation captured 38.44% of the dodecanedioic acid market size in 2025 and is forecast to climb at a 5.49% CAGR through 2031.

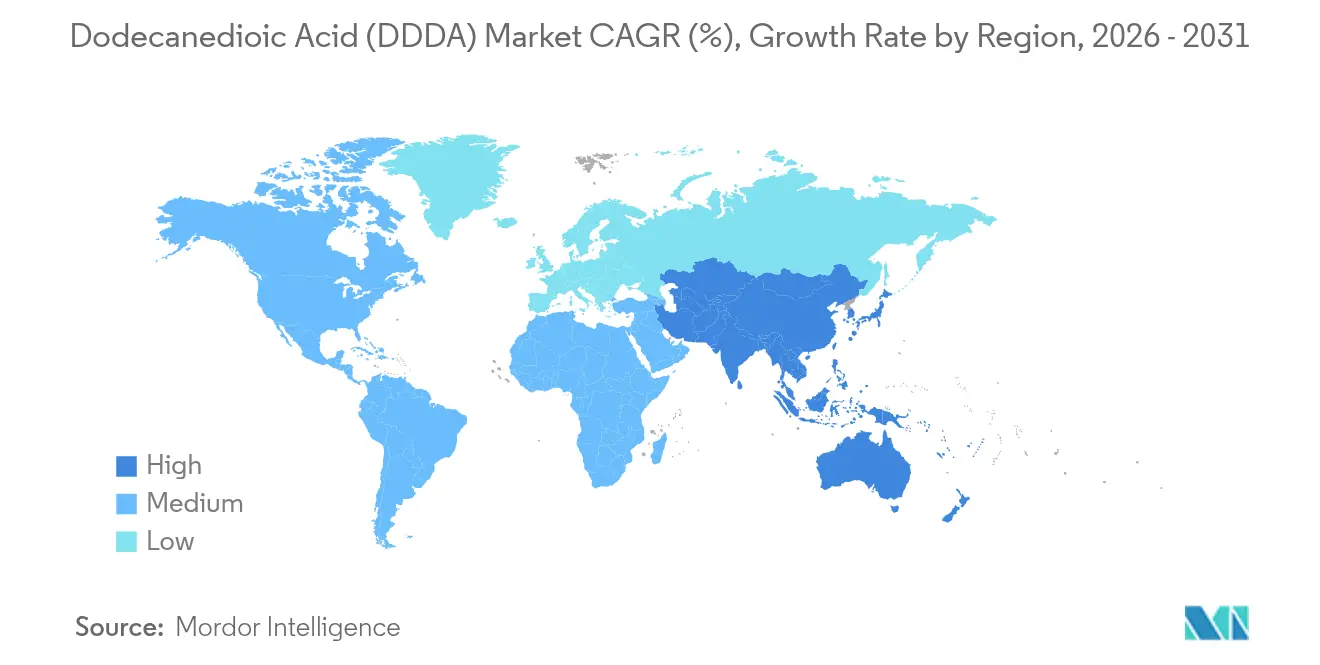

- Asia-Pacific commanded 52.86% of 2025 volume and is set to advance at a 5.28% CAGR, outpacing all other regions.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dodecanedioic Acid (DDDA) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growth in high-performance Nylon-12 & Nylon-6,12 demand from automotive lightweighting | +1.70% | Global, with concentration in North America & Europe | Medium term (2-4 years) |

| Expansion of powder-coated consumer electronics & appliances | +0.80% | APAC core, spill-over to North America | Short term (≤ 2 years) |

| EV-thermal-management lubricants adopting DDDA-based esters | +0.60% | Global, led by China & Europe | Medium term (2-4 years) |

| Bio-route process cost decline via synthetic biology breakthroughs | +0.40% | North America & Europe, emerging in APAC | Long term (≥ 4 years) |

| Adoption in aerospace 3-D printing photopolymers | +0.30% | North America & Europe, with emerging applications in APAC | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growth in High-Performance Nylon-12 & Nylon-6,12 Demand from Automotive Lightweighting

Automakers are setting tighter fleet-weight targets that translate into higher usage of high-performance polyamides, notably nylon-12 and nylon-6,12. BASF’s USD 260 million commitment to new hexamethylenediamine capacity and INVISTA’s recommissioning of HMD assets are emblematic of the supply-chain investments now underway. Vehicle manufacturers aim to trim 7-10% curb weight by 2030 without compromising crashworthiness, and integrated chemical suppliers offering DDDA-based polyamide formulations emerge as preferred partners. The driver adds 1.7 percentage points to forecast CAGR, with tangible demand growth visible in fuel-line, brake-hose, and battery-enclosure applications.

Expansion of Powder-Coated Consumer Electronics & Appliances

Consumer-electronics brands are migrating from solvent-borne to powder coatings to cut VOC emissions and secure thinner, scratch-resistant finishes. DDDA serves as a curing agent that supports ultra-thin acrylic powder layers, helping manufacturers meet miniaturization and sustainability targets. Regulatory pressure in Europe and North America complements the production-scale advantages enjoyed by Asia-Pacific electronics hubs, lifting demand for specialized DDDA grades. Powder-coated appliances and smartphones together propel a 0.8 percentage-point boost to overall CAGR.

EV-Thermal-Management Lubricants Adopting DDDA-Based Esters

Thermal-management fluids for next-generation electric vehicles ask for high dielectric strength, oxidative stability, and low viscosity. DDDA-based esters can perform in integrated battery-and-drivetrain cooling loops that are projected to grow threefold by 2030. ExxonMobil’s R&D around multifunctional PAO blends and TotalEnergies’ water-based fluid highlight an industry pivot toward advanced chemistries[1]“Making Driveline Fluids for Electric Vehicles,” ExxonMobil Chemical, exxonmobilchemical.com . The driver adds 0.6 percentage points to market CAGR.

Bio-Route Process Cost Decline via Synthetic Biology Breakthroughs

Microbial strain engineering now yields 92.5 g/l DDDA, a step-change from earlier titers and a cost reduction of roughly 30% compared with 2024, allowing bio-based producers to match petrochemical economics for select grades. Europe’s Green Deal preference for bio-content and the United States’ synthetic-biology funding sustain R&D momentum. The driver lifts CAGR by 0.4 percentage points and opens premium-pricing windows for green-label products.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Handling & toxicological hazards of DDDA | -0.90% | Global, with stricter enforcement in EU & North America | Short term (≤ 2 years) |

| Feedstock price volatility (sebacic acid / cyclododecane) | -0.30% | Global, with particular impact on APAC producers | Medium term (2-4 years) |

| Supply-chain risk from cyclododecane outage incidents | -0.50% | Global, with critical impact on petro-chemical route producers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Handling & Toxicological Hazards of DDDA

DDDA is classified as a serious eye irritant under REACH, and the 2025 revision tightens documentation and on-site audit requirements. Smaller firms without dedicated EH&S infrastructure face higher compliance costs, potentially lengthening product-approval cycles by up to 18 months. While the substance exhibits low acute toxicity and good biodegradability, mandatory risk management measures—eye-protection programs, automated loading systems, and continuous monitoring—raise operating expenses[2]“Product Safety Summary for Dodecanedioic Acid,” UBE Chemical Europe, jcia-bigdr.jp . The restraint subtracts 0.9 percentage points from projected growth.

Feedstock Price Volatility (Sebacic Acid / Cyclododecane)

Cyclododecane and sebacic acid together account for roughly half of the finished-product cost, and quarterly price swings of 25-40% strain producer margins. The U.S. Department of Defense’s USD 86.2 million reshoring initiative underscores concerns about single-region supply risk. Ocean-freight disruptions and natural-gas price shocks exacerbate lead-time uncertainty, compelling manufacturers to build larger raw-material buffers or invest in backward integration, which lengthens capital-payback cycles. This restraint reduces CAGR by 0.3 percentage points.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Production Process: Bio-Based Routes Gain Competitive Edge

The petro-chemical pathway via cyclododecatriene held 60.58% of the dodecanedioic acid market share in 2025, supported by advantaged natural-gas economics in North America and the Middle East. Bio-based routes, while smaller in absolute tonnage, are forecast to post an 8.60% CAGR, capturing sustainability-driven premiums in automotive and electronics. Bio-producers leveraging engineered Wickerhamiella sorbophila strains have trimmed conversion costs by roughly one-third since 2024, setting the stage for further share accretion.

Competitive positioning now appears bifurcated: high-volume, cost-sensitive resin and adhesive grades continue to be met by petro-chemical output, while low-carbon, high-purity bio-grades win specification in EV lubricants, aerospace photopolymers and premium powder coatings. Capital allocation decisions therefore hinge on regional energy prices, regulatory trajectories and customer sustainability pledges. Firms with dual-route capabilities achieve optionality to swing production toward the more profitable pathway whenever feedstock spreads or carbon-pricing schemes shift materially.

By Application: Powder Coating Disrupts Traditional Resin Dominance

Resins retained the single largest slice of the dodecanedioic acid market size at 43.12% in 2025, supplying polyesters for coil-coating, can-coating, and engineering-plastic compounding. Nonetheless, powder coatings are charting the fastest 5.62% CAGR through 2031, propelled by electronics and appliance brands adopting ultra-thin, VOC-free finishes. Miniaturization puts emphasis on dielectric strength, scratch resistance, and UV durability-all properties enhanced when DDDA acts as a curing co-agent.

Adhesives and lubricants occupy smaller but strategically important niches. EV immersion-cooling fluids depend on DDDA-based esters to withstand high voltages, while aerospace additive-manufacturing powders incorporate DDDA-modified polyamides to improve layer-fusion consistency. Niche pharmaceutical and personal-care uses remain low volume but attract premium pricing due to purity and traceability needs. The application portfolio is therefore evolving toward a dual model: resins offer volume stability, whereas powder coatings and specialty lubricants deliver growth and outsized margins.

By End-User Industry: Automotive Sector Drives Dual Growth Dynamics

Automotive and transportation applications collectively accounted for 38.44% of the dodecanedioic acid market share in 2025 and will expand at a 5.49% CAGR, outpacing the overall average. The sector integrates DDDA into nylon-12 fuel lines, battery-module housings, and EV thermal fluids, reflecting both legacy internal-combustion demand and electrification trajectories. Electrical and electronics follow as the second-largest user, benefiting from powder-coating penetration in smartphones, notebooks, and smart-home appliances.

Industrial machinery consumes DDDA-based resins for abrasion-resistant components, though price-sensitive buyers seek lower-cost diacids when performance tolerances allow. Building and construction demand tracks infrastructure spending and thus grows modestly, while healthcare and personal-care applications remain niche but defend premium price points through value-in-use claims such as pH control and skin-conditioning efficiency. The end-user hierarchy is unlikely to change through 2030, yet margin pools will shift toward electrification-driven and sustainability-oriented segments.

Geography Analysis

Asia-Pacific dominated the dodecanedioic acid market in 2025 with a 52.86% share and is expected to rise at a 5.28% CAGR to 2031. China’s vast chemical-manufacturing base, coupled with Japan’s advanced-materials ecosystem, positions the region for sustained capacity additions. Regional players benefit from integrated petro-chemical complexes, proximity to electronics and automotive export hubs, and skilled labor availability, partly offsetting feedstock-import volatility.

North America secured a smaller but resilient share, anchored by shale-gas cost advantages that favor petrochemical routes. The U.S. Department of Defense’s USD 86.2 million sebacic-acid reshoring grant underscores regional supply-security concerns and may catalyze backward integration in key value chains. Producers are also channeling capex into high-value niche grades rather than bulk tonnage, reflecting a strategic shift toward differentiated products. Market participation is underpinned by comprehensive regulatory and intellectual-property frameworks that safeguard returns on R&D.

Europe represents a mature but innovation-driven landscape. Stringent REACH updates, higher energy costs, and the Green Deal’s bio-content mandates collectively nudge manufacturers toward bio-based pathways and specialty applications. BASF’s French site upgrades demonstrate commitment to local supply resilience despite structural cost pressures. While growth is slower than in Asia-Pacific, the region maintains technological leadership in advanced polyamides, EV fluids and circular-economy initiatives. South America and the Middle East & Africa together account for a modest share yet present pockets of opportunity linked to industrialization and infrastructure builds, tempered by currency volatility and political risk.

Competitive Landscape

The dodecanedioic acid market remains highly consolidated, with the top-tier companies leveraging vertical integration, multiregional production footprints, and R&D depth to defend share. BASF’s upstream investments in HMD and downstream expansions in nylon polymers exemplify lock-in across value steps, while DSM-Firmenich’s focus on bio-route innovation positions it to tap sustainability-linked premiums. Arkema continues to rationalize portfolios and upgrade captive feedstock assets in a bid to cut cost volatility.

Technological differentiation is emerging as the prime competitive lever. Traditional petro-chemical incumbents are optimizing catalysts, debottlenecking existing lines and signing long-term feedstock contracts. In contrast, synthetic-biology specialists work on recombinant strains, modular fermentation skids and in-situ product recovery to achieve cost parity at lower carbon intensity. Patent filings on microbial cannabinoid pathways hint at broader cross-application research that can spill over into dicarboxylic-acid synthesis.

Strategic moves in 2024-25 include selective M&A, such as INVISTA’s exploration of alternatives for its nylon-fibers arm and Evonik’s business-line realignment, both aimed at concentrating on high-margin chemistries. Joint-ventures with electronics OEMs to co-develop powder-coating formulations or with lubricant blenders to qualify immersion-cooling fluids further illustrate customer-proximity tactics. As REACH enforcement tightens and bio-content targets proliferate, the ability to document cradle-to-gate carbon footprints becomes a decisive market-access criterion, reinforcing incumbent advantages.

Dodecanedioic Acid (DDDA) Industry Leaders

BASF

DSM

Evonik Industries AG

INVISTA

UBE Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: BASF announced that it is nearing the completion of its PA 6.6 production expansion in Freiburg, Germany. Dodecanedioic acid, a dicarboxylic acid, plays a pivotal role in producing nylon 6, so this expansion is poised to bolster the market.

- August 2024: INVISTA Nylon Chemicals (China) Co. has announced the successful expansion of its nylon 6,6 polymer facility at the Shanghai Chemical Industry Park (SCIP). The production of Dodecanedioic Acid by the company is anticipated to support nylon 6 production, thereby boosting demand in the market.

Global Dodecanedioic Acid (DDDA) Market Report Scope

Dodecanedioic acid is a dicarboxylic acid having the formula (CH2)10(CO2H)2. It is a white solid used in various products, including materials and polymers. It is used to manufacture nylon 6, 12, adhesives, powder coatings, and paints. DDDA is also employed in manufacturing corrosion inhibitors, pulp, paper, water treatment, chemical facilities, etc. The Dodecanedioic acid market is segmented by application and geography. By application, the market is segmented into resin, powder coating, adhesives, lubricants, and other applications. The report also covers the market size and forecasts for the market in 15 countries across the globe. The market sizing and forecasts are based on each segment's value (USD million).

| Petro-chemical (cyclododecatriene route) |

| Bio-based (sebacic-acid and microbial routes) |

| Resin |

| Powder Coating |

| Adhesives |

| Lubricants |

| Other Applications (Pharmaceutical, Cosmetics, etc.) |

| Automotive and Transportation |

| Electrical and Electronics |

| Industrial Machinery |

| Building and Construction |

| Healthcare and Personal Care |

| Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Rest of Asia-Pacific | |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Russia | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | Saudi Arabia |

| South Africa | |

| Rest of Middle East and Africa |

| By Production Process | Petro-chemical (cyclododecatriene route) | |

| Bio-based (sebacic-acid and microbial routes) | ||

| By Application | Resin | |

| Powder Coating | ||

| Adhesives | ||

| Lubricants | ||

| Other Applications (Pharmaceutical, Cosmetics, etc.) | ||

| By End-User Industry | Automotive and Transportation | |

| Electrical and Electronics | ||

| Industrial Machinery | ||

| Building and Construction | ||

| Healthcare and Personal Care | ||

| By Geography | Asia-Pacific | China |

| Japan | ||

| India | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Russia | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | Saudi Arabia | |

| South Africa | ||

| Rest of Middle East and Africa | ||

Key Questions Answered in the Report

What is the current size of the dodecanedioic acid market in 2026?

The dodecanedioic acid market size stands at USD 635.54 million in 2026.

What CAGR is forecast for the global dodecanedioic acid market between 2026 and 2031?

The market is projected to grow at a 5.02% CAGR during the forecast period.

Which application segment is expanding the fastest?

Powder coatings are set to post the highest 5.62% CAGR through 2031 as electronics and appliances switch to VOC-free finishes.

Which region holds the largest share of dodecanedioic acid demand?

Asia-Pacific leads with 52.86% of global volume, supported by China’s chemical-manufacturing capacity and Japan’s materials innovation.

How are bio-based production routes impacting the market?

Bio-routes, growing at an 8.60% CAGR, benefit from 30% cost reductions since 2024 and capture sustainability-driven premiums in high-value end-uses.

Page last updated on: